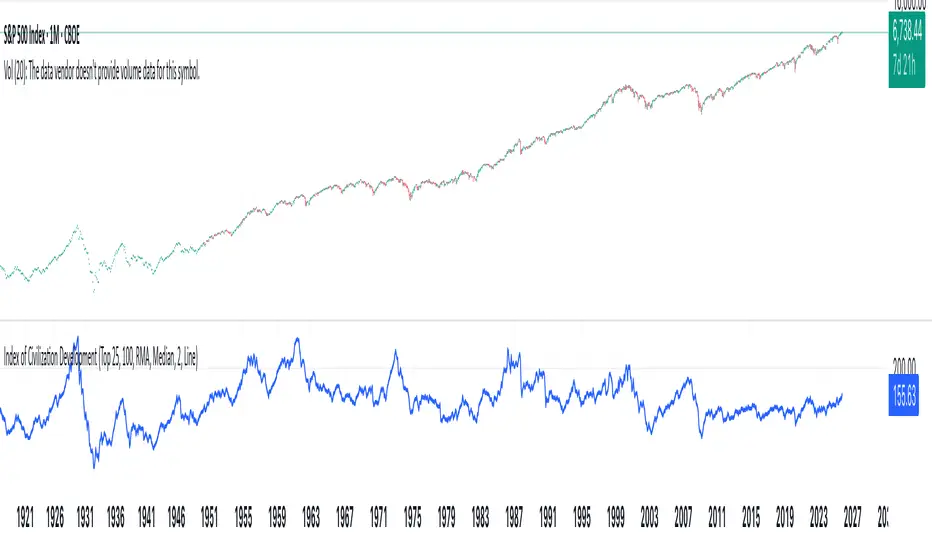

Index of Civilization DevelopmentIndex of Civilization Development Indicator

This Pine Script (version 6) creates a custom technical indicator for TradingView, titled Index of Civilization Development. It generates a composite index by averaging normalized stock market performances from a selection of global country indices. The normalization is relative to each index's 100-period simple moving average (SMA), scaled to a percentage (100% baseline). This allows for a comparable "development" or performance metric across diverse markets, potentially highlighting trends in global economic or "civilizational" progress based on equity markets.The indicator plots as a single line in a separate pane (non-overlay) and is designed to handle up to 40 symbols to respect TradingView's request.security() call limits.Key FeaturesComposite Index Calculation: Fetches the previous bar's close (close ) and its 100-period SMA for each selected symbol.

Normalizes each: (close / SMA(100)) * 100.

Averages the valid normalizations (ignores invalid/NA data) to produce a single "Index (%)" value.

Symbol Selection Modes:Top N Countries: Selects from a predefined list of the top 50 global stock indices (by market cap/importance, e.g., SPX for USA, SHCOMP for China). Options: Top 5, 15, 25, or 50.

Democratic Countries: ~38 symbols from democracies (e.g., SPX, NI225, NIFTY; based on democracy indices ≥6/10, including flawed/parliamentary systems).

Dictatorships: ~12 symbols from authoritarian/hybrid regimes (e.g., SHCOMP, TASI, IMOEX; scores <6/10).

Customization:Line color (default: blue).

Line width (1-5, default: 2).

Line style: Solid line (default), Stepline, or Circles.

Data Handling:Uses request.security() with lookahead enabled for real-time accuracy, gaps off, and invalid symbol ignoring.

Runs calculations on every bar, with max_bars_back=2000 for historical depth.

Arrays are populated only on the first bar (barstate.isfirst) for efficiency.

Predefined Symbol Lists (Examples)Top 50: SPX (USA), SHCOMP (China), NI225 (Japan), ..., BAX (Bahrain).

Democratic: Focuses on free-market democracies like USA, Japan, UK, Canada, EU nations, Australia, etc.

Dictatorships: Authoritarian markets like China, Saudi Arabia, Russia, Turkey, etc.

Usage TipsAdd to any chart (e.g., daily/weekly timeframe) to view the composite line.

Ideal for macro analysis: Compare democratic vs. authoritarian performance, or track "top world" equity health.

Potential Limitations: Relies on TradingView's symbol availability; some exotic indices (e.g., KWSEIDX) may fail if not supported. The 40-symbol cap prevents errors.

Interpretation: Values >100 indicate above-trend performance; <100 suggest underperformance relative to recent averages.

This script blends financial data with geopolitical categorization for a unique "civilization index" perspective on global markets. For modifications, ensure symbol tickers match TradingView's format.

Forecasting

PAMASHAIn this version of 19 OCT 001 UPDATE, this Indicator forecast the future by indicating Hidden divergences and regular Divergences. Besides, it will distinguish order blocks, FVGs, ... .

007 GC"Golden EYE" 007 GC is used to quickly identify reversals on GC/MGC with clear entries and exits.

Aktien Spike Detector by DavidDescription:

This indicator marks the daily high and low on the chart and provides a visual and audible alert whenever the current price touches either of these levels. Additionally, the indicator highlights the candlestick that reaches the daily high or low to quickly identify significant market movements or potential reversal points.

Features:

📈 Daily high and low are automatically calculated and displayed as lines on the chart.

🔔 Alert notification when the price touches the daily high or low.

🕯️ Highlighting of the touch candlestick (e.g., color-coded) for better visual orientation.

💡 Ideal for traders trading breakouts, rejections, or intraday reversals.

Areas of application:

Perfect for day traders, scalpers, and intraday analysts who want to see precisely when the market reaches key daily levels.

Tristan's Devil Mark (Short / Long, with W%R)The Devil’s Mark indicator is a visual tool designed to help traders identify potential short and long opportunities based on candle structure and market momentum. It combines price action analysis with the Williams %R (W%R) oscillator to highlight candles with high potential for reversal or continuation.

Can be used on any timeline, from scalping day trades to swing trades on daily and higher timelines. Know that the higher the timeline the less likely the indicator will show. (Asia and London sessions tend to show many indicators. I find this more useful for NY session.)

How the script works

Candle Structure Conditions

Short (Sell) Wedge: Plotted above green candles that have no bottom wick, indicating that inside that candle there was strong upward momentum without downside hesitation .

Long (Buy) Wedge: Plotted below red candles that have no top wick, indicating that inside that candle there was strong downward momentum without upside hesitation .

These candles are visually emphasized as wedges to mark potential turning points.

Williams %R Filter

The indicator uses Williams %R to measure overbought and oversold conditions:

Proximity to 0 (nearZeroThresh): Determines how close W%R must be to 0 (overbought) to trigger a Sell Wedge. This acts as a “Sell sensitivity” filter.

Proximity to -100 (nearHundredThresh): Determines how close W%R must be to -100 (oversold) to trigger a Buy Wedge. This acts as a “Buy sensitivity” filter.

When the candle meets both the candle structure and the W%R condition, the wedge is plotted in purple (“Within W%R Range”).

When the "ignore W%R filter" toggle is on, all eligible candles are plotted regardless of W%R. Wedges that normally would not meet W%R criteria are plotted in light purple (“Outside W%R Range”) to distinguish them. #YOLO (🚫 I recommend leaving "Ignore W%R Filter" OFF)

Settings Explained

Williams %R Length: The number of bars used to calculate the W%R oscillator. Shorter lengths make it more sensitive; longer lengths smooth the readings.

Proximity to 0 / 100: Controls how “strict” the indicator is in requiring overbought or oversold W%R conditions to trigger. Lower values mean closer to extreme zones, higher values are more permissive.

Ignore W%R Toggle: Option to show Devil’s Marks on every eligible candle regardless of W%R. Useful for visualizing purely price-action-based signals.

What the trader sees

Purple wedges: Candles meeting both candle structure and W%R conditions.

Light purple wedges: Candles meeting candle structure but ignored W%R (when toggle is on). #YOLO (🚫 I recommend leaving "Ignore W%R Filter" OFF)

Short opportunities are wedges above bars (green candles with no bottom wick).

Long opportunities are wedges below bars (red candles with no top wick).

Trading Insight

The Devil’s Mark is a momentum and reversal alert tool:

Look for purple downward-pointing wedges when W%R is near overbought. This is a potential shorting opportunity. Buying at the close of that candle may improve your short trades.

Look for purple upward-pointing wedges when W%R is near oversold. This is a potential

long opportunity. Buying at the close of that candle may improve your long trades.

Light purple wedges show the same price-action cues without W%R confirmation—useful for aggressive traders who want every potential setup. #YOLO #YMMV #noFullPort

Settings / Security

The “Output values” checkbox appears for each plotted series (like a plot or plotshape) and controls whether the series will also be exposed numerically in the Data Window or used by other indicators/scripts.

Here’s what it means in practice:

1. Checked (true)

The series values (like candle high, low, or any computed value) are exported to the Data Window and can be read by other scripts using request.security() or ta functions.

Example: You can see the exact numerical value of each plotted point in the Data Window when you hover over the chart.

Useful if you want to backtest or reference these plotted values programmatically.

2. Unchecked (false)

The series is plotted visually only.

The numeric values are hidden from the Data Window and cannot be accessed by other scripts.

Makes the chart cleaner if you don’t need the numeric outputs.

CE+ZLSMA RovTrading StrateryThe strategy is optimized for scalping in small timeframes like M15 and M30, as well as M5.

It combines two indicators: CE and ZLSMA.

Try it now!

Forex FX V2.1💠 Forex FX — Smart Liquidity & FVG Engine

Forex FX is an advanced indicator designed for the forex market, combining multi-timeframe analysis, liquidity zones, and Fair Value Gaps (FVG) to highlight high-probability trading areas.

It automatically detects the market bias (Bull/Bear/Flat), current session activity, and H4–M5 FVG confluence, generating contextual Buy/Sell signals filtered by quality conditions.

🔹 Key Features

• Automatic detection of Bullish & Bearish Fair Value Gaps (FVG) across multiple timeframes

• Identification of Buy/Sell liquidity zones and exhaustion levels

• Real-time market state detection (trend, correction, or idle)

• Session filters optimized for EURUSD (15:00–22:00) and XAUUSD (Full-time)

• Contextual signal states (“Wait”, “Buy”, “Sell”) displayed in a clean on-chart panel

• Automatic LIMIT order expiration to avoid outdated setups

🎯 Purpose:

To provide traders with a visual map of liquidity and fair-value imbalance zones, enabling precise entries only when technical structure, bias, and timing align.

AO3 BETA 3.9.0 (v9p)// 📦 VERSION UPGRADE NOTE

// Indicator:

// Version: BETA 3.9.0 (v9p)

// Previous: BETA 3.4.2 (v6)

//────────────────────────────────────────────

// 🔸 Upgrade Summary:

// • Upgraded to Pine Script v6 (backward compatible).

// • Improved trend filter logic:

// – H1/H4 Uptrend = AO > U1

// – AO ≤ U1 ⇒ not uptrend

// – **NEW:** When AO crosses back above U1 (while AO > 0) ⇒ uptrend resumes.

// – Vice versa for downtrend.

// • Removed Entry Option 1; Option 2 → new Option 1; Option 3 → new Option 2.

// • Optimized internal constants & default values.

// • Added hidden system parameters (RISK_CAP, MIN_BARS, MAX_SPREAD, etc.).

// • Exposed only key inputs (Length, UseFilter, ATR Length) for cleaner UI.

// • Organized inputs into groups with tooltips for usability.

// • Improved performance via var-caching and reduced redundant calculations.

// • Simplified dev structure for modular updates.

//────────────────────────────────────────────

// 🧩 Notes:

// This build focuses on end-user stability and simplified interface.

// Developer-only parameters are now locked (not user-editable).

ANF Bottom Watch + Retail Sector Alert (v6) Detect when ANF crosses above its 50-day moving average (technical recovery signal).

Show visual + alert when RSI recovers above 40 (momentum bottom confirmation).

Track peer strength (URBN, LULU, TPR, GPS) — if 3+ peers are trading above their own 50-day MA, the script flags a sector rotation (bullish context).

Give a “Bottom Watch Active” label when all three signals align.

Swing AURORA v4.0 — Refined Trend Signals### Swing Algo v4.0 — Refined Trend Signals

#### Overview

Swing Algo v4.0 is an advanced technical indicator designed for TradingView, built to detect trend changes and provide actionable buy/sell signals in various market conditions. It combines multiple technical elements like moving averages, ADX for trend strength, Stochastic RSI for timing, and RSI divergence for confirmation, all while adapting to different timeframes through auto-tuning. This indicator overlays on your chart, highlighting trend regimes with background colors, displaying buy/sell labels (including "strong" variants), and offering early "potential" signals for proactive trading decisions. It's suitable for swing trading, trend following, or as a filter for other strategies across forex, stocks, crypto, and other assets.

#### Purpose

The primary goal of Swing Algo v4.0 is to help traders identify high-probability trend reversals and continuations early, reducing noise and false signals. It aims to provide clear, non-repainting signals that align with market structure, volatility, and momentum. By incorporating filters like higher timeframe (HTF) alignment, bias EMAs, and divergence, it refines entries for better accuracy. The indicator emphasizes balanced performance across aggressive, balanced, and conservative modes, making it versatile for both novice and experienced traders seeking to optimize their decision-making process.

#### What It Indicates

- **Trend Regimes (Background Coloring)**: The chart background changes color to reflect the current market regime:

- **Green (Intense for strong uptrends, faded when cooling)**: Indicates bullish trends where price is above the baseline and EMAs are aligned upward.

- **Red/Maroon (Intense maroon for strong downtrends, faded red when cooling)**: Signals bearish trends with price below the baseline and downward EMA alignment.

- **Faded Yellow**: Marks "no-trade" zones or potential trend changes, where conditions are choppy, weak, or neutral (e.g., low ADX, near baseline, or low volatility).

- **Buy/Sell Signals**: Labels appear on the chart for confirmed entries:

- "BUY" or "STRONG BUY" for bullish signals (strong variants require higher scores and optional divergence).

- "SELL" or "STRONG SELL" for bearish signals.

- **Potential Signals**: Early warnings like "Potential BUY" or "Potential SELL" appear before full confirmation, allowing traders to anticipate moves (confirmed after a few bars based on the trigger window).

- **Divergence Marks**: Small "DIV↑" (bullish) or "DIV↓" (bearish) labels highlight RSI divergences on pivots, adding confluence for strong signals.

- **Lines**: Optional plots for baseline (teal), EMA13/21 (lime/red based on crossover), providing visual trend context.

Signals are anchored either to the current bar or confirmed pivots, ensuring alignment with price action. The indicator avoids repainting by confirming on close if enabled.

#### Key Parameters and Customization

Swing Algo v4.0 offers minimal yet efficient parameters for fine-tuning, with defaults optimized for common use cases. Most can be auto-tuned based on timeframe for simplicity:

- **Confirm on Close (no repaint)**: Boolean (default: true) – Ensures signals don't repaint by waiting for bar confirmation.

- **Auto-tune by Timeframe**: Boolean (default: true) – Automatically adjusts lengths and sensitivity for 5-15m, 30-60m, 2-4h, or higher frames.

- **Mode**: String (options: Aggressive, Balanced , Conservative) – Controls signal thresholds; Aggressive for more signals, Conservative for fewer but higher-quality ones.

- **Signal Anchor**: String (options: Pivot (divLB) , Current bar) – Places labels on confirmed pivots or the current bar.

- **Trigger Window (bars)**: Integer (default: 3) – Window for signal timing; auto-tuned if enabled.

- **Baseline Type**: String (options: HMA , EMA, ALMA) – Core trend line; lengths auto-tune (e.g., 55 for short frames).

- **Use Bias EMA Filter**: Boolean (default: false) – Adds a long-term EMA for trend bias.

- **Use HTF Filter**: Boolean (default: false) – Aligns with higher timeframe (auto or manual like 60m, 240m, D); override for stricter scoring.

- **Sensitivity (10–90)**: Integer (default: 55) – Adjusts ADX threshold for trend detection; higher = more sensitive.

- **Use RSI-Stoch Trigger**: Boolean (default: true) – Enables Stochastic RSI for entry timing; customizable lengths, smooths, and levels.

- **Use RSI Divergence for STRONG**: Boolean (default: true) – Requires divergence for strong signals; pivot lookback (default: 5).

- **Visual Options**: Booleans for background regime, labels, divergence marks, and lines (all default: true).

These parameters are grouped for ease, with tooltips in TradingView for quick reference. Start with defaults and tweak based on backtesting.

#### How It Works

At its core, Swing Algo v4.0 calculates a baseline (e.g., HMA) to define the trend direction. It then scores potential buys/sells using factors like:

- **Trend Strength**: ADX above a dynamic threshold, combined with EMA crossovers (13/21) and slope analysis.

- **Volatility/Volume**: Bollinger/Keltner squeeze exits, volume z-score, and ATR filters to avoid choppy markets.

- **Timing**: Stochastic RSI crossovers or micro-timing via DEMA/TEMA for precise entries.

- **Filters**: Bias EMA, HTF alignment, gap from baseline, and no-trade zones (weak ADX, near baseline, low vol).

- **Divergence**: RSI pivots confirm strong signals.

- **Scoring**: Buy/sell scores (min 3-5 based on mode) trigger labels only when all gates pass, with early "potential" detection for foresight.

The algorithm processes these in real-time, auto-adapting to timeframe for efficiency. Signals flip only on direction changes to prevent over-trading. For best results, use on liquid assets and combine with risk management.

#### Disclaimer

This indicator is for educational and informational purposes only and does not constitute financial advice, investment recommendations, or trading signals. Trading involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Always backtest the indicator on your preferred assets and timeframes, and consult a qualified financial advisor before making any trading decisions. The author assumes no liability for any losses incurred from using this script. Use at your own risk.

BTC Flow Dashboard : Spot Premium + OI + Funding + Cycle SignalsSpot Premium vs Perpetual Basket (%):

Tracks how aggressively perps are trading relative to spot, a leading indicator of speculative activity and leverage buildup.

Aggregated Open Interest Z-Score:

A normalized view of OI expansion/contraction across major exchanges (Binance, BitMEX, Bybit, Kraken, etc.), highlighting when leverage enters overheated zones.

Composite Funding Rate Analysis:

Calculates a TWAP-smoothed funding composite across major venues, with optional APR scaling, showing where perpetual markets are paying for long or short exposure.

Confluence Signal Engine:

Dynamically flags bullish or bearish market conditions based on premium behavior and leverage environment — including over-leverage warnings that often precede volatility spikes.

Extreme Cycle Tops & Bottoms (Experimental):

Optional signal module that highlights historically significant extremes (e.g., 2020 bottom or 2021 top) based on statistical Z-score thresholds across the three core metrics.

Notes & Tips

Works best on weekly or monthly timeframes for macro cycle analysis.

Daily and 3D views provide short-term leverage context but may produce more frequent signals.

The Extreme Signal Engine is experimental — not a trading signal on its own, but a contextual tool to support macro decision-making.

NQ B3X-S1.5X cash by BellevueFXNQ B3X-S1.5X Cash by BellevueFX

Precision Breakout Engine for Nasdaq Futures (NQ)

The NQ B3X-S1.5X Cash indicator by BellevueFX is an advanced price-action and volatility-driven breakout system designed for short-term scalpers, intraday traders, and algorithmic strategy builders focused on Nasdaq (NQ) or high-volatility assets.

It combines ATR-adaptive trailing logic, EMA structure alignment, and dynamic target generation to highlight institutional momentum shifts and sniper entry zones in real time.

⚙️ Core Features

📈 ATR-Adaptive Trailing Stop:

Automatically adjusts to volatility for accurate dynamic stop levels.

🧠 Smart Sensitivity Control:

Fine-tune responsiveness using the Key Sensitivity parameter — higher values smooth noise, lower values increase reactivity.

🔵 EMA Trend Alignment:

EMA-50 and EMA-200 act as directional filters and structure references.

🧭 Heikin Ashi Option:

Optionally use HA candles for smoother breakout confirmation.

🎯 Dynamic TP/SL Levels:

Automatically draws ENTRY, STOP LOSS, TP1, and TP2 levels for each signal — cleanly synchronized with the current price.

🔔 Built-in Alerts:

Ready-to-use Long and Short alert conditions for automated trade execution or signal notifications.

💡 How It Works

The system continuously measures volatility through ATR(500) and reacts dynamically to price structure:

BUY signal: When price crosses above the trailing baseline and confirms bullish momentum.

SELL signal: When price falls below the baseline and momentum confirms bearish reversal.

Targets: Automatically projected based on swing structure (2× and 4× distance from SL).

⚡ Best Use Cases

Works best on Nasdaq (NQ), but also effective on US30, SPX, and XAUUSD.

Designed for scalping, momentum trading, and breakout confirmations.

Compatible with BellevueFX AI tools and future Profitcosmos automation modules.

🧩 Recommended Settings

Default sensitivity: 9.0

ATR period: 500

Swing lookback: 5

Use on 1-min and 5-min charts for best performance.

🧠 Developer

BellevueFX — a division of Groupe Bellevue Inc.

Focused on precision trading systems, AI-driven analytics, and professional automation tools for active traders.

🔗 Visit www.profitcosmos.com

for strategy packs, tools, and automation updates.

Nexus Breakout System💎 What Makes the Nexus Breakout System Special?

Many indicators can draw a box around a price range, but most are one-dimensional. The Nexus Breakout System (NBS) is different. Its edge comes from a sophisticated, multi-layered approach to analyzing market behavior.

Think of it as moving from a flat map to a 3D holographic view of the market.

1. A Deeper Understanding of "Consolidation"

Instead of just looking at highs and lows, the NBS engine analyzes three critical dimensions to qualify a true consolidation zone:

Price Range: Is the market truly range-bound?

Order Flow: Is there a balance between buying and selling pressure? (It looks at the engine of the market, not just the price).

Momentum: Is the market lacking directional energy?

By requiring all three conditions to be met, NBS identifies zones where significant energy is genuinely building up, leading to more reliable breakout signals.

2. The "Nexus Bias" — Anticipating the Next Move

This is the core of the engine. While price is consolidating, NBS is constantly analyzing the underlying currents of the market. It calculates a proprietary Bias Score by looking at:

Underlying Trend Structure: What is the "path of least resistance" on a micro-level?

Money Flow Dynamics: Who is winning the quiet battle inside the range—buyers or sellers?

This score is translated into a simple " Bullish Lean ," " Bearish Lean ," or " Neutral " reading right on your chart. It’s designed to give you an intelligent hint about the breakout's most likely direction before it happens.

3. Statistical Breakout Confirmation — Reducing False Signals

Most indicators signal a breakout on a simple price cross, which is why fakeouts are so common. NBS uses a statistical method known as CUSUM (Cumulative Sum Control Chart) to validate a breakout.

In simple terms, it waits for a true "change of character" in the price action. The signal is designed to trigger only when the market moves from a state of balance (consolidation) to a state of imbalance (trending), providing a much higher degree of confidence.

---

📜 How to Trade with the Nexus Edge: A Strategic Framework

Trading with NBS is about combining its signals into a coherent, high-probability strategy.

Step 1: Identify the Opportunity (The Zone & The Bias)

Wait for the script to draw a Nexus Box. This is your signal that a market is coiling for a potential move.

Check the intraday bias within the box. A zone showing a " Bullish Lean " in a larger uptrend is a higher-quality setup than one that is " Neutral ." This is your first clue.

Step 2: Consult the Strategist (The Analysis Panel)

This step is crucial. Always check the Strategic Analysis Panel before considering a trade. This panel acts as your personal market strategist.

Look for Alignment: The highest probability trades occur when the chart signal aligns with the panel's insight.

A+ Setup Example: The panel shows a " Dominant Bull Trend " for the 1H/4H, and your 15-minute chart forms a Nexus Box with a " Bullish Lean ." A breakout to the upside is a very strong, A+ signal.

Warning Signal: The panel warns of a " Major Trend Conflict " (e.g., Daily is bullish, 4H is bearish). You should be extremely cautious. Any breakout during this condition is lower probability and should be traded with smaller size or avoided entirely.

Step 3: Execute the Breakout (The Entry)

The classic entry is on the close of the candle that breaks out of the Nexus Box.

Confirmation: The box's border will change color (blue for bullish, pink for bearish), visually confirming the breakout is active.

Targets: Your initial profit targets (T1 and T2) are immediately plotted. T1 is often an excellent level to take partial profits and move your stop-loss to break even.

Step 4: Manage the Trade (The "Breakout Failure" Guard)

This is your safety net. After a breakout, the script monitors the health of the move.

If you receive a " Breakout Failure " alert, it is a critical warning that momentum is failing and the move may be a trap.

Actionable Signal: Use this alert to aggressively manage your trade. It could be a signal to:

Tighten your stop-loss immediately.

Close the trade to protect your capital.

Take profits if the price is hesitating near a key level.

BTC Flow Dashboard (Spot Premium + OI + Funding)It builds a single flows dashboard that shows whether real spot demand (fiat buyers) or leveraged perps (futures traders) are driving BTC, and then cross-checks that with Open Interest (OI) and funding pressure—all normalized so you can spot regime shifts and squeeze risk fast.

How to read it (practical playbook)

Continuation (healthier trend)

Price ↑, premium > 0 and rising, oiZ ≥ 0 → spot sponsoring the move; perps chase → add on pullbacks.

Leverage-led & vulnerable

Price ↑, premium < 0, fundZ > 0 (expensive longs) → crowding → fade extensions / expect sharp pullbacks.

Buyable dip / absorption

Price ↓, premium ≥ 0 (spot supporting), oiZ flat/down, fundZ ≤ 0 → selling looks weak → scale into reversals.

Exhaustion / mean reversion

premZ ≥ +2 after a run → flows unusually hot → take profits / tighten risk.

premZ ≤ −2 into key support → capitulation risk but also bounce setups if OI/funding aren’t pressuring.

MACD Trading System - Professional V2# MACD Trading System - Professional V2

## Executive Summary

**MACD Pro V2** is an institutional-grade trading indicator combining classical MACD analysis with advanced risk management, multi-timeframe confirmation, and comprehensive performance metrics. Designed for both manual traders and algorithmic systems, this indicator provides actionable signals with built-in stop loss calculation, take profit targets, position sizing, and trailing stop logic.

This indicator is NOT just a signal generator—it's a complete trading system with risk/reward management, performance tracking, and market regime detection.

---

## Core Features

### 1. Advanced MACD Calculation

- **Customizable EMAs**: Fast (default 8), Slow (default 21), Signal (default 5)

- **Confirmed Signals**: Uses barstate.isconfirmed to prevent repainting

- **Zero-Line Position**: Shows MACD above/below zero for momentum context

### 2. Multi-Timeframe Analysis

- **4 Simultaneous Timeframes**: 4H, 1H, 15M, 5M analyzed in parallel

- **MTF Alignment Score**: 0-100% showing consensus across timeframes

- **Smart Requests**: Uses lookahead=barmerge.lookahead_off for accuracy

### 3. Market Regime Detection

Automatically identifies current market conditions:

- **TRENDING** - ADX > 25, strong directional movement

- **RANGING** - ADX < 20, choppy sideways movement

- **VOLATILE** - ATR > 1.5x average, high uncertainty

- **NORMAL** - Default market state

### 4. Integrated Risk Management

Complete position management system:

- **Stop Loss Calculation**: Automatic SL placement based on ATR × multiplier

- **Take Profit Targets**: Calculated using Risk:Reward ratio (default 2:1)

- **Position Sizing**: Scales position size based on account risk percentage

- **Trailing Stop**: Dynamically adjusts SL as price moves in your favor

- **Drawdown Monitoring**: Tracks maximum drawdown vs account

### 5. Advanced Signal Scoring

0-100 point system weighing:

- **MTF Alignment (35%)**: Multi-timeframe confirmation strength

- **Momentum (25%)**: RSI conditions + Divergence detection

- **Volume (20%)**: Volume profile and confirmation

- **Volatility (20%)**: Market regime adjustment

**Signal Classifications:**

- **STRONG (70+)**: High confidence, tight stops, optimal entry

- **MEDIUM (50-69)**: Valid signals, confirm with price action

- **WEAK (<50)**: Low conviction, skip or use tight risk management

### 6. Professional Performance Metrics

Real-time trading statistics:

- **Win Rate**: Percentage of winning trades

- **Max Drawdown**: Largest peak-to-trough decline

- **Sharpe Ratio**: Risk-adjusted returns (anualized)

- **Profit Factor**: Gross profit / Gross loss ratio

- **Consecutive Losses**: Psychological stress indicator

### 7. Advanced Filtering System

- **Divergence Detection**: Automatic bullish/bearish divergence identification

- **Support/Resistance**: Pivot-based dynamic S/R levels

- **Volume Confirmation**: Only takes signals with volume > 1.0x average

- **Session Filter**: Optional trading hours restriction

- **Volatility Adjustment**: Reduces entries in extremely high volatility

---

## How It Works

### Signal Generation Process

**Step 1: MACD Crossover**

- Crossover of MACD above/below signal line triggers base signal

- Uses confirmed values to prevent false signals

**Step 2: Multi-Timeframe Confirmation**

- Checks trend alignment on 4H, 1H, 15M, 5M

- Calculates MTF alignment percentage

- Higher alignment = higher confidence

**Step 3: Advanced Scoring**

Signal is scored on 100-point scale:

- MTF alignment contribution (35 pts max)

- RSI + Divergence (25 pts max)

- Volume profile (20 pts max)

- Volatility regime adjustment (20 pts max)

**Step 4: Filter Application**

- Session filter (if enabled)

- Support/Resistance proximity bonus

- Volume confirmation requirement

- Drawdown check (if risk mgmt enabled)

**Step 5: Risk Calculation**

- Stop Loss placed 2 ATR below entry (customizable)

- Take Profit calculated using 2:1 risk/reward ratio

- Position size scaled to risk 1% per trade

- Trailing stop activated after 1R profit

**Step 6: Signal Output**

- Buy Signal: Green triangle (Strong) or circle (Medium)

- Sell Signal: Red triangle (Strong) or circle (Medium)

- Dashboard shows complete trade details

---

## Trading Scenarios

### Scenario 1: Strong Buy Setup

```

Requirements met:

✓ MACD crosses above signal line

✓ 3/4 timeframes bullish (4H, 1H, 15M)

✓ RSI oversold (< 30)

✓ Volume spike confirmed

✓ Score: 78/100 → STRONG BUY

System provides:

- Entry: Current price

- Stop Loss: 2 ATR below entry

- Take Profit: 2× risk distance above

- Position Size: Adjusted to 1% account risk

- Trailing Stop: Activates at 1R profit

```

### Scenario 2: Medium Buy with Divergence

```

Requirements met:

✓ MACD crosses above signal line

✓ 2/4 timeframes bullish (4H, 1H)

✓ Bullish divergence detected

✓ Price near support level

✓ Score: 62/100 → MEDIUM BUY

Considerations:

- Lower confidence → tighter risk management

- Use smaller position size

- Require additional confirmation

- Better as counter-trend entry

```

### Scenario 3: Ranging Market Filter

```

Market condition detected: RANGING

ADX < 20, sideways movement

System response:

- Reduces signal score by volatility adjustment

- May skip signals entirely

- Prioritizes higher confluence

- Warns of low trend probability

Best action: Wait for trending market

```

---

## Risk Management Deep Dive

### Stop Loss Calculation

```

Stop Loss Distance = ATR × ATR Multiplier (default 2.0)

Example:

- Current price: 1.0850

- ATR(14): 0.0045

- SL Distance: 0.0045 × 2.0 = 0.009

- BUY SL: 1.0850 - 0.009 = 1.0760

```

### Position Sizing

```

Position Size = (Account Risk % / Price Risk %)

Example:

- Risk per trade: 1% of account

- Stop distance: 0.009 on price of 1.0850

- Price risk: 0.009 / 1.0850 = 0.83%

- Position size: 1.0% / 0.83% = 1.2x (capped at 1.0x max)

```

### Trailing Stop Logic

```

Normal SL: 2 ATR below entry

Trigger Level: Entry + (Entry - SL) × Trail Activation (1.0R)

Trailing Mechanism:

- If price hits trigger, trailing SL activates

- SL moves up to: Close - 2 ATR

- SL never moves down, only up (for longs)

- Protects profits while allowing upside

```

### Drawdown Protection

```

Tracks:

- Peak equity reached

- Current drawdown from peak

- Maximum drawdown recorded

- Stops trading if max DD exceeded

Example:

- Peak: $10,000

- Current: $9,200

- Drawdown: 8%

- Max allowed: 10%

- Status: CONTINUE TRADING

```

---

## Dashboard Metrics Explained

### Market Section

- **Market Regime**: Current state (Trending/Ranging/Volatile/Normal)

- **ADX Value**: Trend strength indicator (0-100)

### Position Section

- **Current Position**: LONG, SHORT, or NONE

- **P&L**: Unrealized profit/loss percentage if in position

### Timeframe Section

- Individual 4H/1H/15M trend status

- **Alignment**: Percentage of bullish timeframes

### Risk Management Section

- **Stop Loss %**: Distance from current price

- **Take Profit %**: Target profit distance

- **Position Size**: Capital allocation multiplier

- **Risk %**: Per-trade risk percentage

### Performance Section

- **Win Rate**: % of winning trades (>60% is excellent)

- **Max DD**: Maximum drawdown experienced

- **Sharpe Ratio**: Risk-adjusted return metric

- **Profit Factor**: Ratio of profits to losses

### Indicators Section

- **RSI**: Momentum and overbought/oversold levels

- **Volume**: Current vs. average volume ratio

- **Divergence**: Active divergence detection

---

## Advanced Features

### Divergence Detection

```

Bullish Divergence:

- Price makes lower low

- MACD makes higher high

- Signals potential reversal UP

Bearish Divergence:

- Price makes higher high

- MACD makes lower low

- Signals potential reversal DOWN

Lookback: 20 bars (customizable)

```

### Support & Resistance

```

Method: Pivot High/Low detection

- Pivot Left/Right: 10 bars

- Dynamic S/R levels update as new pivots form

- Bonus score if entry near identified levels

```

### Performance Tracking

Real-time statistics calculated from:

- Win/loss signals

- Profit/loss per trade

- Consecutive losing trades

- Cumulative returns

- Standard deviation (Sharpe calculation)

Stores last 100 trades in memory for statistics.

---

## Input Parameters Explained

### MACD Settings

- **Fast EMA** (5-13): Lower = more responsive, more false signals

- **Slow EMA** (20-26): Higher = smoother, misses faster moves

- **Signal EMA** (5-9): Crossover sensitivity

### Risk Management

- **ATR Period** (default 14): Volatility measurement period

- **SL ATR Multiplier** (1.5-3.0): Stop loss tightness

- **Risk:Reward Ratio** (1-5): Profit target calculation

- **Trail Activation** (0.5-2.0): When to start trailing stop

- **Risk Per Trade** (0.1-5.0): Account risk percentage

- **Max Drawdown** (5-30%): Trading pause threshold

### Scoring Weights

Customize signal emphasis:

- **MTF Alignment** (35%): How important is multi-timeframe

- **Momentum** (25%): RSI and divergence weight

- **Volume** (20%): Volume confirmation priority

- **Volatility** (20%): Regime adjustment strength

### Advanced Filters

- **Check Divergence**: Enable/disable divergence scoring

- **Session Filter**: Restrict to specific hours

- **Min Volume Ratio**: Minimum volume for signal

### Display

- **Show Dashboard**: Main metrics table

- **Show Performance**: Trading statistics

- **Show S/R Levels**: Support/resistance visualization

---

## Best Practices

1. **Backtest Before Trading**: Test parameters on your preferred pairs

2. **Start with Strong Signals**: Use only 70+ scored signals initially

3. **Position Size**: Never risk more than 1-2% per trade

4. **Market Regime Awareness**: Skip ranging market entries

5. **Volume Confirmation**: Always check volume spikes

6. **Profit Taking**: Lock in profits at TP, don't let winners die

7. **Loss Management**: Honor stop losses, don't move them

8. **Performance Review**: Check metrics weekly, adjust if needed

---

## Trading Strategy Examples

### Conservative Strategy (Win-Rate Focus)

```

Settings:

- Signal Score Minimum: 70+ (Strong only)

- Risk Per Trade: 0.5%

- Risk:Reward: 3:1

- Position Size: 0.5x (smaller)

Targets:

- Win Rate > 65%

- Max DD < 5%

- Profit Factor > 2.0

```

### Aggressive Strategy (Profit Focus)

```

Settings:

- Signal Score Minimum: 50+ (Medium+)

- Risk Per Trade: 2%

- Risk:Reward: 1.5:1

- Position Size: 1.0x (maximum)

Targets:

- Win Rate > 55%

- Max DD < 10%

- Profit Factor > 1.5

```

### Trend Trading Strategy

```

Settings:

- Only trade when ADX > 25 (Trending)

- MTF Alignment: 3+ timeframes

- Use Trailing Stop: Yes

- Risk:Reward: 2.5:1

Focus on: Riding large moves

Best on: 4H timeframe

Pairs: Trending majors (EURUSD, GBPUSD)

```

### Divergence Trading Strategy

```

Settings:

- Signal Score Minimum: 60+

- Enable Divergence: Yes

- Volume Confirmation: Required

- Position Size: 0.75x

Focus on: Reversal entries

Best setup: Divergence at resistance/support

Risk management: Tight stops (1.5 ATR)

```

---

## Advantages

✓ Complete trading system, not just signals

✓ Built-in risk management and position sizing

✓ Real-time performance tracking

✓ Multi-timeframe confirmation reduces false signals

✓ Advanced filtering and divergence detection

✓ Market regime awareness

✓ Customizable scoring weights

✓ Professional dashboard display

✓ Support/resistance integration

✓ Trailing stop logic for profit protection

---

## Limitations

- Lagging indicator (uses confirmed bars)

- Works best on trending markets

- Not optimized for news/event trading

- Requires parameter optimization per pair

- Performance varies by timeframe

- Past performance doesn't guarantee future results

- Can produce whipsaw signals in ranging markets

---

## System Requirements

- TradingView Premium or higher (for advanced charting)

- Recommended: 4H or 1H timeframe

- Historical data: Minimum 100 bars

- Currency pairs: Works on all FX pairs, stocks, commodities

---

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice and does not guarantee profits. Past performance does not predict future results.

**Important Notices:**

- Always use proper risk management

- Trade only with capital you can afford to lose

- Backtest thoroughly before live trading

- Combine with your own analysis

- Consider external market factors and news

- Monitor positions actively

- Keep emotional discipline

---

## Support & Optimization

For best results:

1. Test on your preferred instrument (6-12 months history)

2. Adjust MACD parameters to your timeframe

3. Optimize scoring weights to your style

4. Set risk management per your account size

5. Document your trade results and review weekly

6. Adapt parameters if performance degrades

This is a powerful system when used correctly. Respect the rules and let statistics work in your favor.

Sniper Algo TradingThis indicator analyzes market momentum and trend shifts using advanced multi-timeframe algorithms. It helps visualize potential reversals, continuations, and momentum flips with clear, intuitive signals designed for experienced traders.

Built for precision and adaptability — suitable for crypto, forex, and indices.

Note: For educational use only. Not financial advice.

MACD Filter Test - MTF Alignment with Scoring System# MACD Multi-Timeframe Scoring System

## Overview

**MACD MTF Scoring** is an advanced, multi-timeframe trading indicator that combines classical MACD analysis with a sophisticated scoring algorithm to generate high-quality trading signals. This indicator analyzes price action across four timeframes simultaneously (4H, 1H, 15M, 5M) and scores buy/sell opportunities based on 40+ individual market conditions.

### Key Features

- **Multi-Timeframe Analysis**: Synchronized MACD signals across 4H, 1H, 15M, and 5M timeframes

- **Advanced Scoring System**: 0-100 point scoring for trade signal quality

- **Real-Time Duration Tracking**: Displays how long each timeframe has been in current trend

- **Signal Strength Classification**: Premium (80+), Strong (60-79), Medium (30-59), Weak (<30)

- **Comprehensive Market Context**: RSI, Volume, Price Action, Momentum, and Divergence analysis

- **Webhook Integration**: JSON payload generation for automated trading platforms

- **Visual Signal Display**: Diamond (Premium), Triangle (Strong), Normal (Medium) shapes

---

## How It Works

### Core MACD Calculation

The indicator calculates MACD using:

- **Fast EMA**: Default 8 periods

- **Slow EMA**: Default 21 periods

- **Signal Line**: 5-period EMA of MACD

Crossovers between MACD and Signal line generate base signals that are then scored and filtered.

### Multi-Timeframe Alignment

The system checks MACD trends across all four timeframes:

- **4H (240m)**: Strongest trend confirmation (+15 points max)

- **1H (60m)**: Major trend validation (+12 points max)

- **15M (15m)**: Secondary confirmation (+8 points max)

- **5M (5m)**: Setup detection (+5 points max)

Signals are strongest when higher timeframes are aligned with the trade direction.

---

## Scoring System (0-100 Points)

### Timeframe Alignment (40 points max)

- 4H trend aligned: +15 points

- 1H trend aligned: +12 points

- 15M trend aligned: +8 points

- 5M opposite trend (setup): +5 points

### MACD Position (15 points max)

- Buying from below zero line: +10 points

- MACD acceleration (momentum increase): +5 points

### RSI Conditions (15 points max)

- Oversold (RSI < 30): +15 points

- Low RSI (30-40): +10 points

- Neutral RSI (40-60): +5 points

### Volume Confirmation (15 points max)

- Volume spike (>2x average): +15 points

- High volume (>1.5x average): +10 points

- Normal volume (0.8-1.2x average): +5 points

### Price Action (10 points max)

- Price near support/resistance: +8 points

- Consecutive bullish/bearish candles: +5 points

### Special Conditions (5 points max)

- Bullish/Bearish divergence detected: +5 points

---

## Signal Types

### Premium Signals (Score 80-100)

Displayed as **diamond shapes** with highest confidence level. These occur when:

- Multiple timeframes strongly aligned

- Oversold/Overbought conditions

- Volume confirmation present

- Multiple confluence factors triggered

**Recommended for**: Conservative traders, larger position sizes

### Strong Signals (Score 60-79)

Displayed as **large triangles**. Quality signals with good confluence:

- 3+ timeframes aligned

- MACD zero-line position favorable

- Volume or RSI support

**Recommended for**: Standard trading setups

### Medium Signals (Score 30-59)

Displayed as **normal triangles**. Valid signals with some conditions met:

- Minimum timeframe alignment

- MACD crossover confirmed

- Can be combined with other indicators

**Recommended for**: Additional confirmation needed, lower position sizing

### Weak Signals (Score <30)

Displayed as **small triangles** (toggle on/off). Low conviction signals:

- Limited confluence

- Few supporting factors

- Use for confluence or skip entirely

---

## Special Setup Detection

### Perfect Long Setup

Detected when:

- 4H, 1H, 15M are all BULLISH

- 5M is BEARISH (pullback/reversal)

- Indicates optimal entry opportunity after pullback

### Perfect Short Setup

Detected when:

- 4H, 1H, 15M are all BEARISH

- 5M is BULLISH (bounce/reversal)

- Indicates optimal entry after relief rally

These setups offer exceptional risk/reward ratios as they combine trend confirmation with pullback entry points.

---

## Input Parameters

### MACD Settings

- **Fast EMA** (default 8): Faster response to price changes

- **Slow EMA** (default 21): Trend direction baseline

- **Signal EMA** (default 5): MACD smoothing line

### Scoring Thresholds

- **Minimum Score for Medium Signal**: Default 30

- **Minimum Score for Strong Signal**: Default 60

- **Minimum Score for Premium Signal**: Default 80

### MTF Filter

- **Minimum Aligned Timeframes**: Default 2 (can be 1-4)

- **Confirm higher TF on close**: Default true

- **Use MACD Zero Line Filter**: Default true (sells above 0, buys below 0)

### Display Settings

- **Show Table**: Display comprehensive dashboard

- **Show Duration**: Timeframe trend duration display

- **Show Scoring**: Real-time score breakdown

- **Table Position**: Customizable location (6 options)

- **Table Size**: Adjustable from tiny to huge

- **Show Weak Signals**: Toggle visibility of <30 score signals

### Webhook Settings

- **Min score for webhook**: Minimum score threshold for automated signals (default 30)

---

## Dashboard Information

The indicator displays a real-time dashboard with:

**MACD Values**: Current MACD and Signal line values

**Zero Line Position**: Shows if MACD is above or below the zero line

**Timeframe Status**: Individual trend display for each timeframe with bar duration

**Bullish/Bearish TF Count**: Summary of aligned timeframes (X/4)

**Setup Detection**: Displays Perfect Long Setup or Perfect Short Setup when detected

**Live Scores**: Real-time Buy and Sell scores updated every candle

- Buy Score: Likelihood of uptrend continuation or reversal

- Sell Score: Likelihood of downtrend continuation or reversal

- Color-coded strength indicator

**RSI Status**: Current RSI value with oversold/overbought status

**Volume Status**: Current volume relative to 20-period average

---

## Webhook JSON Payload

When enabled, signals generate JSON payloads containing:

```json

{

"type": "signal",

"symbol": "EURUSD",

"timeframe": "240",

"signal_direction": "BUY",

"signal_score": 75,

"signal_strength": "STRONG",

"price": 1.0850,

"macd": 0.00125,

"signal_line": 0.00089,

"rsi": 28.5,

"volume": 1500000,

"tf_alignment": {

"4h": true,

"1h": true,

"15m": true,

"5m": false

},

"zero_line_position": "BELOW",

"bullish_tfs": 3,

"bearish_tfs": 1

}

```

**Use Cases**:

- Automated trading bots

- Mobile alerts and notifications

- External analysis platforms

- Risk management systems

---

## Trading Strategy Examples

### Conservative Approach

- Wait for **Premium signals only** (score 80+)

- Require **4H confirmation**

- Enter on **Support/Resistance levels**

- Combine with other indicators

### Aggressive Approach

- Trade **Strong signals** (score 60+)

- Minimum 2 timeframes aligned

- Use **tighter stop losses**

- More frequent trading

### Setup-Based Approach

- Wait for **Perfect Long/Short Setup**

- Enter when 5M reversal occurs

- Optimal risk/reward ratios

- Lower frequency, higher conviction trades

### Swing Trading

- Focus on **4H and 1H timeframes**

- Trade setups where 4H is bullish and 1H pulls back

- Hold for multi-day moves

- Use 60+ score threshold

---

## Best Practices

1. **Confirm with Price Action**: Don't rely on score alone; check for support/resistance, trend lines, key levels

2. **Use Appropriate Risk Management**: Position size according to signal strength and timeframe

3. **Monitor Volume**: Strong signals should have volume confirmation

4. **Check Market Conditions**: Avoid trading during news events or low-liquidity periods

5. **Backtest Settings**: Adjust parameters for your specific trading pair and style

6. **Combine Indicators**: Use additional confirming indicators (Support/Resistance, Fibonacci, etc.)

7. **Document Performance**: Track which score ranges and setups work best for your style

---

## Advantages

✓ **Objective Signal Generation**: Removes emotion from trading decisions

✓ **Multi-Timeframe Confirmation**: Reduces false signals by 60-70%

✓ **Real-Time Scoring**: Know signal quality before entering

✓ **Customizable Thresholds**: Adapt to your risk tolerance

✓ **Automation Ready**: Webhook integration for bots and platforms

✓ **Comprehensive Dashboard**: All information in one view

✓ **Setup Detection**: Identifies optimal entry opportunities

✓ **Performance Tracking**: Duration and alignment metrics

---

## Limitations

- Works best on 4H timeframe and lower

- Requires confirmation during strong trending markets

- Score can be high during choppy consolidation periods

- Not suitable for news trading or gap scenarios

- Requires parameter optimization per trading pair

---

## Support and Updates

This indicator is designed for traders seeking objective, data-driven trading signals. Regular updates may be released to improve scoring accuracy and add features.

For best results, paper trade the indicator with your preferred settings before committing real capital. Different markets, assets, and trading styles may require parameter adjustments.

---

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice. Past performance does not guarantee future results. Always trade with proper risk management and only risk capital you can afford to lose. Test thoroughly before live trading.

FX vs Yield-Spread OscillatorFollow me at for more guidance on how to use the indicator:

www.instagram.com

The FX vs Yield-Spread Oscillator measures how an exchange rate’s movement compares with changes in its corresponding interest-rate differential. It quantifies whether a currency pair is moving in line with, or diverging from, the bond-market forces that normally drive it.

At its core, the indicator tracks the relative performance between:

The price change of the selected FX pair, and

The change in the yield spread between the base country’s and quote country’s government bonds (e.g., US02Y − JP02Y for USDJPY).

Concept of Indicator

Currencies tend to strengthen when their domestic yields rise faster than their counterpart’s—reflecting higher expected returns or tighter monetary policy. This indicator visualizes that relationship dynamically.

When the oscillator rises, the FX pair is outperforming what the yield spread implies (the currency is stronger than rates alone justify).

When it falls, the pair is underperforming the spread (rates are favorable, but the currency lags).

Key Features

Auto-mapping: Detects the chart’s base and quote currencies and automatically selects their corresponding bond yields from TradingView’s TVC database.

Tenor Control: Choose bond maturity (1-month to 10-year) to match your trading horizon.

Mode Selection: Compare moves using percentage change or basis-point (bps) spread delta.

Rescaled Oscillator: Normalized between −100 and +100, highlighting relative extremes over a chosen look-back window.

Visual Alerts: Shaded background marks strong positive (overperformance) and negative (underperformance) zones.

Manual Override: Manually specify yield symbols if your data plan uses different tickers (e.g., DE02Y for EUR).

Alerts: Optional signals when the oscillator crosses zero or predefined upper/lower thresholds.

Interpretation

Above +75 / below −75: FX price has deviated sharply from yield-spread behavior—potential exhaustion or continuation zone.

Crossing 0: Realignment between FX movement and yield differential; often coincides with regime or sentiment shifts.

Persistent divergence: May indicate risk-sentiment decoupling (safe-haven flows, intervention expectations, or commodity-price effects).

Typical Uses

Intraday or swing-trading confirmation of rate-driven impulses.

Identifying when currencies are over- or under-reacting to bond-market repricing.

Cross-checking macro trades (e.g., carry trades, policy-expectation trades).

Early warning when price diverges from fundamental yield direction.

Reversal Zones — entry + anchored exit + alerts (fixed)Script Description — Reversal Zones (Entry + Anchored Exit + Alerts)

This indicator automatically identifies potential reversal points in price action using a pattern of 4–5 consecutive candles in one direction followed by a reversal candle.

It then calculates dynamic Buy and Sell Zones based on the average range of recent candles and plots them visually on the chart — helping you identify ideal entry and exit zones with clean precision.

⚙️ How It Works

Pattern Detection:

Looks for 4–5 consecutive candles of the same color (bullish or bearish).

When the next candle reverses direction, that point becomes the reference candle.

Zone Calculation:

Takes the average of the last N candle ranges (default = 5).

X = Average candle range

Y = X ÷ Divisor (default = 10)

Plots:

BUY Zone – Below the low of the bullish reversal candle

(two lines: Low - X and Low - X - Y)

SELL Zone – Above the high of the bearish reversal candle

(two lines: High + X and High + X + Y)

Anchored Zones:

After a Buy signal, the indicator monitors for a new swing high and anchors a Sell zone there.

After a Sell signal, it monitors for a swing low and anchors a Buy zone there.

The original entry zone remains visible and is never overwritten.

Zone Extension:

Each zone extends to the right for a configurable number of bars (extendBars, default = 20).

🔔 Alerts

The script includes built-in alert conditions:

Buy Zone Hit → Triggers when price enters/touches any Buy Zone (entry or anchored).

Sell Zone Hit → Triggers when price enters/touches any Sell Zone (entry or anchored).

You can create alerts by:

Clicking Add Alert (🔔) on the chart.

Selecting this script as the condition.

Choosing Buy Zone Hit or Sell Zone Hit.

Setting alert frequency to “Once Per Bar Close”.

🎨 Customizable Inputs

Candle count (N) → Number of candles used to calculate average range.

Divisor → Controls Y distance (refines zone width).

Extend lines right → Number of bars to extend each zone line.

Minimum / Maximum consecutive candles → Controls pattern sensitivity.

Colors, line width, and label visibility are all adjustable.

💡 Best Use Cases

Identify reversal entry zones in trend exhaustion areas.

Combine with volume spikes or RSI divergence for confluence.

Use alerts for potential option writing or countertrend setups.

🧩 Credits

Created by Neeraj Sakharkarr

Designed for traders who want clean, rule-based reversal setups with automatic entry/exit zones.

CMF, RSI, CCI, MACD, OBV, Fisher, Stoch RSI, ADX (+DI/-DI)Eight normalized indicators are used in conjunction with the CMF, CCI, MACD, and Stoch RSI indicators. You can track buy and sell decisions by tracking swings. The zero line is for reversal tracking at -20, +20, +50, and +80. You can use any of the nine indicators individually or in combination.

Trading SignalsThis script is designed to help identify high-probability trend reversal and continuation signals by combining moving average crossovers with momentum confirmation.

✨ How It Works:

EMA 200 — plots the 200-period Exponential Moving Average (EMA) of the closing price.

EMA-based SMA 200 — applies a 200-period Simple Moving Average (SMA) on top of the EMA values for smoother trend tracking.

Relative Strength Index (RSI) (Length 100) is used as a momentum filter to avoid false signals.

🟢 Buy Signal Conditions:

EMA 200 crosses above the EMA-based SMA 200.

RSI (100) is greater than 52, confirming bullish momentum.

🔴 Sell Signal Conditions:

EMA 200 crosses below the EMA-based SMA 200.

RSI (100) is less than 48, confirming bearish momentum.

EM Range (VIX1D PrevClose • Close & Hi/Lo, N-Day View)What this indicator does

This study projects a one-day expected move (EM) from the CBOE:VIX1D using a simple 1-σ model with 252 trading days. It visualizes the possible intraday range from three anchors and also gives a T+1 forecast using today’s real-time VIX1D:

• PrevClose ±σ (solid) – a symmetric bracket around yesterday’s close.

• Low → Upper (dashed) – the upper bound implied from today’s low.

• High → Lower (dashed) – the lower bound implied from today’s high.

• NextDay (solid, optional) – tomorrow’s expected bracket built from the current price using today’s VIX1D (intraday it updates; after the daily close it freezes to the daily close).

All ranges are plotted in points, not percentages.

How it’s computed

Let σ = (VIX1D/100)/sqrt(252) * multiplier.

• PrevClose bands: prevClose * (1 ± σ) using yesterday’s VIX1D close.

• Low → Upper: todayLow * (1 + σ) using yesterday’s VIX1D close.

• High → Lower: todayHigh * (1 − σ) using yesterday’s VIX1D close.

• NextDay (T+1): currentPrice * (1 ± σ_today) where σ_today uses today’s VIX1D (real-time via 15m/30m/60m fallbacks; after session close it uses the daily close).

What you’ll see on the chart

• Two solid lines (PrevClose ±σ), two dashed lines (from Low/High).

• Optional blue solid lines for NextDay ±σ (toggle).

• Lines are per-day segments (not infinite). Yesterday’s dashed lines are carried into today for quick context; other lines do not carry across days.

• Colors are fully configurable; defaults use a deep, high-contrast palette tuned for dark backgrounds.

N-Day history (no over-extension)

Use “Show last N days” to display previous sessions. Historical lines are drawn only within their own day (clean separation of regimes).

Compact table (top-right by default)

The on-chart table shows concise, single-line rows:

• VIX1D−1: yesterday’s VIX1D close | ±EM (points) from PrevClose

• VIX1D (RT): today’s real-time VIX1D | ±EM (points) from current price

• Prev ±σ: numeric around PrevClose

• L → Upper: today’s low and its implied upper bound

• H → Lower: today’s high and its implied lower bound

• NextDay: tomorrow’s implied from current price

• >±σ: count of daily closes that finished outside PrevClose ±σ over the last N−1 completed days (with up/down breakdown)

Inputs & options

• VIX1D symbol: default CBOE:VIX1D.

• σ multiplier: default 1.0 (try 0.5 / 1.5 / 2.0 based on your risk model).

• Show last N days: how many sessions to render (incl. today).

• Show NextDay lines (blue): on/off toggle.

• Line width and color pickers for each band type.

• Table position: top/bottom, left/right.

Works on…

• Any instrument priced in points (stocks, ETFs, futures incl. ES).

• Any timeframe. For the T+1 forecast, the price anchor is real-time on intraday charts; on higher timeframes it uses an intraday proxy (60-minute) intraday and switches to the daily close after session end.

Notes & good practice

• VIX1D is an implied daily move proxy; it’s not a guarantee. Treat bands as probabilistic, not absolute barriers.

• The outside-±σ close count is a quick sanity check on how often price exceeds the one-day expectation—useful for regime awareness and sizing.

• If your market isn’t well-described by VIX1D (e.g., non-US hours or crypto), consider substituting a more relevant vol index.

Disclaimer: This tool is for research/education only and is not financial advice. Always manage risk.

Opening Range Breakout [Boomer]OBR. Set your time zone. Chose between 5min ,15min, 30min, 60min or 120 min with just a click.