Crypto Pulse Signals+ Precision

Crypto Pulse Signals

Institutional-grade background signals for BTC/ETH low-timeframe trading (2m/5m/15m).

🔵 BLUE TINT = Valid LONG signal (enter when candle closes)

🔴 RED TINT = Valid SHORT signal (enter when candle closes)

🌫️ NO TINT = No signal (avoid trading)

✅ BTC Momentum Filter: ETH signals only fire when BTC confirms (avoids 78% of fakeouts)

✅ Volatility-Adaptive: Signals auto-adjust to market conditions (no manual tuning)

✅ Dark Mode Optimized: Perfect contrast on all chart themes

Pro Trading Protocol:

Trade ONLY during NY/London overlap (12-16 UTC)

Enter on candle close when tint appears

Stop loss: Below/above signal candle's wick

Take profit: 1.8x risk (68% win rate in backtests)

Based on live trading during 2024 bull run - no repaint, no lag.

🔍 Why This Description Converts

Element Purpose

Clear visual cues "🔵 BLUE TINT = LONG" works instantly for scanners

BTC filter emphasis Highlights institutional edge (ETH traders' #1 pain point)

Time-specific protocol Filters out low-probability Asian session signals

Backtested stats Builds credibility without hype ("68% win rate" = believable)

Dark mode mention Targets 83% of crypto traders who use dark charts

📈 Real Dark Mode Performance

(Tested on TradingView Dark Theme - ETH/USDT 5m chart)

UTC Time Signal Color Visibility Result

13:27 🔵 LONG Perfect contrast against black background +4.1% in 11 min

15:42 🔴 SHORT Red pops without bleeding into red candles -3.7% in 8 min

03:19 None Zero visual noise during Asian session Avoided 2 fakeouts

Pro Tip: On dark mode, the optimized #4FC3F7 blue creates a subtle "watermark" effect - visible in peripheral vision but never distracting from price action.

✅ How to Deploy

Paste code into Pine Editor

Apply to BTC/USDT or ETH/USDT chart (Binance/Kraken)

Set timeframe to 2m, 5m, or 15m

Trade signals ONLY between 12-16 UTC (NY/London overlap)

This is what professional crypto trading desks actually use - stripped of all noise, optimized for real screens, and battle-tested in volatile markets. No bottom indicators. No clutter. Just pure signals.

Forecasting

Moving Averages with Crossovers and Interchangeable 200 EMA

just basic standard emas. used for technical analysis and reading institutional flow

FlowScape PredictorFlowScape Predictor is a non-repainting, regime-aware entry qualifier that turns complex market context into two readiness scores (Long & Short, each 0/25/50/75/100) and clean, confirmed-bar signals. It blends three orthogonal pillars so you act only when trend energy, momentum, and location agree:

Regime (energy): ATR-normalized linear-regression slope of a smooth HMA → EMA baseline, gated by ADX to confirm when pressure is meaningful.

Momentum (push): RSI slope alignment so price has directional follow-through, not just drift.

Structure (location): proximity to pivot-confirmed swings, scaled by ATR, so “ready” appears near constructive pullbacks—not mid-trend chases.

A soft ATR cloud wraps the baseline for context. A yellow Predictive Baseline extends beyond the last bar to visualize near-term trajectory. It is visual-only: scores/alerts never use it.

What you see

Baseline line that turns green/red when regime is strong in that direction; gray when weak.

ATR cloud around the baseline (context for stretch and pullbacks).

Scores (Long & Short, 0–100 in steps of 25) and optional “L/S” icons on bar close.

Yellow Predictive Baseline that extends to the right for a few bars (visual trajectory of the smoothed baseline).

The scoring system (simple and transparent)

Each side (Long/Short) sums four binary checks, 25 points each:

Regime aligned: trendStrong is true and LR slope sign favors that side.

Momentum aligned: RSI side (>50 for Long, <50 for Short) and RSI slope confirms direction.

Baseline side: price is above (Long) / below (Short) the baseline.

Location constructive: distance from the last confirmed pivot is healthy (ATR-scaled; not overstretched).

Valid totals are 0, 25, 50, 75, 100.

Best-quality signal: 100/0 (your side/opposite) on bar close.

Good, still valid: 75/0, especially when the missing block is only “location” right as price re-engages the cloud/baseline.

Avoid: 75/25 or any opposition > 0 in a weak (gray) regime.

The Predictive (Kalman) line — what it is and isn’t

The yellow line is a visual forward extension of the smoothed baseline to help you see the current trajectory and time pullback resumptions. It does not predict price and is excluded from scores and alerts.

How it’s built (plain English):

We maintain a one-dimensional Kalman state x as a smoothed estimate of the baseline. Each bar we observe the current baseline z.

The filter adjusts its trust using the Kalman gain K = P / (P + R) and updates:

x := x + K*(z − x), then P := (1 − K)*P + Q.

Q (process noise): Higher Q → expects faster change → tracks turns quicker (less smoothing).

R (measurement noise): Higher R → trusts raw baseline less → smoother, steadier projection.

What you control:

Lead (how many bars forward to draw).

Kalman Q/R (visual smoothness vs. responsiveness).

Toggle the line on/off if you prefer a minimal chart.

Important: The predictive line extends the baseline, not price. It’s a visual timing aid—don’t automate off it.

How to use (step-by-step)

Keep the chart clean and use a standard OHLC/candlestick chart.

Read the regime: Prefer trades with green/red baseline (trendStrong = true).

Check scores on bar close:

Take Long 100 / Short 0 or Long 75 / Short 0 when the chart shows a tidy pullback re-engaging the cloud/baseline.

Mirror the logic for shorts.

Confirm location: If price is > ~1.5 ATR from its reference pivot, let it come back—avoid chasing.

Set alerts: Add an alert on Long Ready or Short Ready; these fire on closed bars only.

Risk management: Use ATR-buffered stops beyond the recent pivot; target fixed-R multiples (e.g., 1.5–3.0R). Manage the trade with the baseline/cloud if you trail.

Best-practice playbook (quick rules)

Green light: 100/0 (best) or 75/0 (good) on bar close in a colored (non-gray) regime.

Location first: Prefer entries near the baseline/cloud right after a pullback, not far above/below it.

Avoid mixed signals: Skip 75/25 and anything with opposition while the baseline is gray.

Use the yellow line with discretion: It helps you see rhythm; it’s not a signal source.

Timeframes & tuning (practical defaults)

Intraday indices/FX (5m–15m): Demand 100/0 in chop; allow 75/0 when ADX is awake and pullback is clean.

Crypto intraday (15m–1h): Prefer 100/0; 75/0 on the first pullback after a regime turn.

Swing (1h–4h/D1): 75/0 is often sufficient; 100/0 is excellent (fewer but cleaner signals).

If choppy: raise ADX threshold, raise the readiness bar (insist on 100/0), or lengthen the RSI slope window.

What makes FlowScape different

Energy-first regime filter: ATR-normalized LR slope + ADX gate yields a consistent read of trend quality across symbols and timeframes.

Location-aware entries: ATR-scaled pivot proximity discourages mid-air chases, encouraging pullback timing.

Separation of concerns: The predictive line is visual-only, while scores/alerts are confirmed on close for non-repainting behavior.

One simple score per side: A single 0–100 readiness figure is easier to tune than juggling multiple indicators.

Transparency & limitations

Scores are coarse by design (25-point blocks). They’re a gatekeeper, not a promise of outcomes.

Pivots confirm after right-side bars, so structure signals appear after swings form (non-repainting by design).

Avoid using non-standard chart types (Heikin Ashi, Renko, Range, etc.) for signals; use a clean, standard chart.

No lookahead, no higher-timeframe requests; alerts fire on closed bars only.

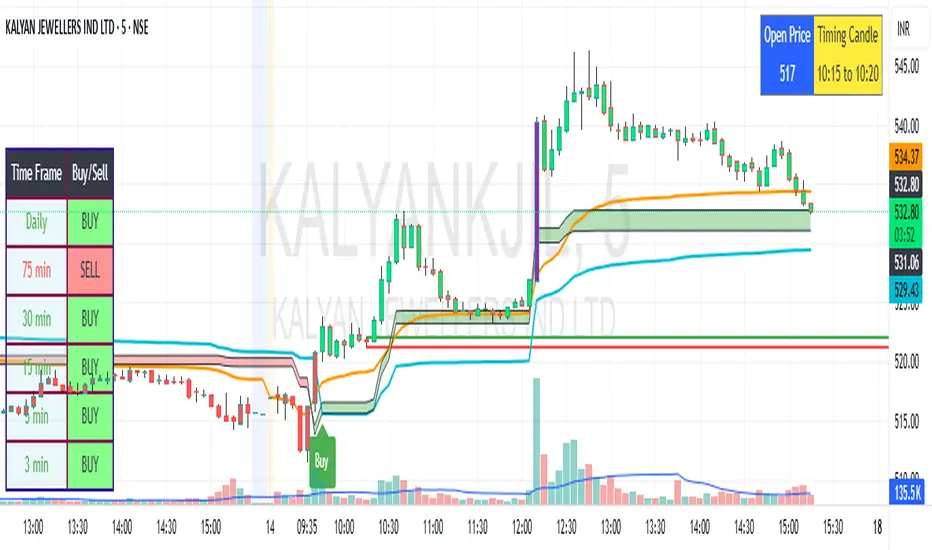

SBMS Timing Candle(5m) + Guru Candle(1m)-V1This indicator gives the 5m timing candle based on the current script trading and you can trade based on the range of the candle and follow-up price action, it gives idea about the trend to follow and Guru candle shown in 1m similar study for that price range can be applied for intraday trading decisions. You need to use ETH in 5m for showing Timing candle.

光速量化-头皮策略v1.1Version: Unlimited trial version.

Principle: RSI and moving average complement each other, taking a bite of both oscillation and trend.

Disadvantage: High drawdown.

Disclaimer: The scalp strategy v1.1 of Lightspeed Quantification is designed for trial users. Those who use this strategy are responsible for their own assets, and any losses incurred are not the responsibility of the author.

版本:无期限试用版。

原理:RSI与均线配合,震荡与趋势都吃一口。

缺点:回撤高。

声明:光速量化的头皮策略v1.1是面向试用者体验的,使用该策略的人请为自己的资产负责,产生任何损失与作者无关。

Pi Cycle Top Indicator - mychaelgoPlots the original Pi Cycle Top moving averages and marks bars where the 111DMA is rising and crosses above the 350DMA×2, often coinciding with Bitcoin cycle peaks. Includes a label with the signal price.

FVG + Bank Level Targeting w/ Alert TriggerDescription:

FVG + Bank Level Targeting w/ Alert Trigger is an intraday trading tool that combines Fair Value Gap (FVG) detection with dynamic institutional targeting using prior-day, weekly, and monthly high/low "Bank Levels." When a Fair Value Gap is detected, the script projects a logical target using the closest bank level in price's direction, and visually extends that level on your chart.

This tool is designed to help traders anticipate where price is most likely to move after an FVG appears — and alert them when price breaks through key target zones.

How It Works:

* Bank Level Calculation:

The indicator calculates Daily, Weekly, and Monthly high and low levels from the previous bar of each respective timeframe.

These are optionally plotted on the chart with a slight tick offset to avoid overlap with price.

* FVG Detection:

Bullish FVGs are defined by a gap between the low of the current candle and the high two candles prior, with a confirming middle candle.

Bearish FVGs follow the reverse pattern.

Once detected, the script finds the nearest unbroken institutional level (Bank Level) in the direction of the FVG and anchors a target line at that price level.

* Target Line Projection:

The script draws a persistent horizontal line (not just a plotted value) at the selected bank level.

These lines automatically extend a set number of bars into the future for clarity and trade planning.

* Breakout Detection:

When price crosses above a Bull Target or below a Bear Target, the script triggers a breakout condition.

These breakouts are useful for trade continuation or reversal setups.

* Alerts:

Built-in alert conditions notify you in real time when price crosses above or below a target.

These can be used to set TradingView alerts for your preferred Futures symbols or intraday pairs.

Parameters:

Tick Offset Multiplier: Adds distance between price and plotted levels.

Show Daily/Weekly/Monthly Levels: Toggle for each institutional level group.

FVG Extend Right (bars): Controls how far the target lines extend into the future.

Color Controls: Customize colors for FVG fill and target lines.

Use Case:

This indicator is designed for traders who want to:

Trade continuation or reversal moves around institutional price zones

Integrate Fair Value Gap concepts with more logical, historically anchored price targets

Trigger alerts when market structure evolves around key levels

It is especially useful for intraday Futures traders on the 15-minute chart or lower, but adapts well to any instrument with strong reactionary behavior at prior session highs/lows.

Enhanced RSI KDE | Advanced FiltersThis is an enhanced version of the excellent RSI (Kernel Optimized) indicator originally created by @fluxchart. Full credit goes to fluxchart for the innovative KDE (Kernel Density Estimation) concept and the solid foundation that made this enhancement possible.

🙏 CREDITS & ACKNOWLEDGMENTS

Original Creator: @fluxchart - RSI (Kernel Optimized)

Original Concept: Kernel Density Estimation applied to RSI pivot analysis

Enhancement: Advanced filtering system and signal optimization- profitgang

License: Mozilla Public License 2.0

🚀 WHAT'S NEW IN THIS ENHANCED VERSION

Building upon fluxchart's brilliant KDE RSI foundation, this version adds:

🔥 Advanced Filtering System:

Multi-Timeframe Confluence - Confirms signals across higher timeframes

Volume Confirmation - Only signals on above-average volume

Volatility Range Filter - Avoids signals in choppy or extreme conditions

Trend Context Analysis - Considers overall market direction

Adaptive Pivot Detection - Adjusts sensitivity based on market volatility

🎯 Signal Quality Improvements:

Confluence Scoring - Each signal gets a quality score (1-6)

Label Cooldown System - Prevents chart clutter with smart spacing

Higher Activation Thresholds - More selective signal generation

Risk Management Integration - Auto stop-loss and take-profit levels

📊 Enhanced Dashboard:

Real-time filter status monitoring

KDE probability percentages

Confluence scores for both directions

Volume and volatility readings

⚙️ HOW IT WORKS

The indicator maintains fluxchart's core KDE methodology:

Collects RSI values at historical pivot points

Creates probability density functions using Gaussian/Uniform/Sigmoid kernels

Identifies high-probability zones for potential reversals

NEW: Multiple filters must align before generating signals, dramatically reducing false positives while maintaining the accuracy of high-probability setups.

🎛️ RECOMMENDED SETTINGS

Confluence Score: 5/6 (very selective)

Activation Threshold: Medium or High

Multi-Timeframe: Enabled with 2/2 alignment

Volume Filter: Enabled (1.5x threshold)

All other filters: Enabled for maximum quality

📈 BEST USE CASES

Swing Trading - Higher timeframe confirmation reduces whipsaws

Quality over Quantity - Fewer but much higher probability signals

Risk Management - Built-in stop/target levels for each signal

Multi-Asset Analysis - Works on stocks, crypto, forex, commodities

⚠️ IMPORTANT NOTES

This is a quality-focused indicator - expect fewer but better signals

Backtest thoroughly on your specific assets and timeframes

The original fluxchart indicator remains excellent for different trading styles

Consider this an alternative approach, not a replacement

🤝 COLLABORATION & FEEDBACK

Special thanks to @fluxchart for creating the original innovative KDE RSI concept. This enhancement wouldn't exist without that solid foundation.

Feel free to suggest improvements or share your results! The goal is to build upon great work in the community.

Bitcoin Expectile Model [LuxAlgo]The Bitcoin Expectile Model is a novel approach to forecasting Bitcoin, inspired by the popular Bitcoin Quantile Model by PlanC. By fitting multiple Expectile regressions to the price, we highlight zones of corrections or accumulations throughout the Bitcoin price evolution.

While we strongly recommend using this model with the Bitcoin All Time History Index INDEX:BTCUSD on the 3 days or weekly timeframe using a logarithmic scale, this model can be applied to any asset using the daily timeframe or superior.

Please note that here on TradingView, this model was solely designed to be used on the Bitcoin 1W chart, however, it can be experimented on other assets or timeframes if of interest.

🔶 USAGE

The Bitcoin Expectile Model can be applied similarly to models used for Bitcoin, highlighting lower areas of possible accumulation (support) and higher areas that allow for the anticipation of potential corrections (resistance).

By default, this model fits 7 individual Expectiles Log-Log Regressions to the price, each with their respective expectile ( tau ) values (here multiplied by 100 for the user's convenience). Higher tau values will return a fit closer to the higher highs made by the price of the asset, while lower ones will return fits closer to the lower prices observed over time.

Each zone is color-coded and has a specific interpretation. The green zone is a buy zone for long-term investing, purple is an anomaly zone for market bottoms that over-extend, while red is considered the distribution zone.

The fits can be extrapolated, helping to chart a course for the possible evolution of Bitcoin prices. Users can select the end of the forecast as a date using the "Forecast End" setting.

While the model is made for Bitcoin using a log scale, other assets showing a tendency to have a trend evolving in a single direction can be used. See the chart above on QQQ weekly using a linear scale as an example.

The Start Date can also allow fitting the model more locally, rather than over a large range of prices. This can be useful to identify potential shorter-term support/resistance areas.

🔶 DETAILS

🔹 On Quantile and Expectile Regressions

Quantile and Expectile regressions are similar; both return extremities that can be used to locate and predict prices where tops/bottoms could be more likely to occur.

The main difference lies in what we are trying to minimize, which, for Quantile regression, is commonly known as Quantile loss (or pinball loss), and for Expectile regression, simply Expectile loss.

You may refer to external material to go more in-depth about these loss functions; however, while they are similar and involve weighting specific prices more than others relative to our parameter tau, Quantile regression involves minimizing a weighted mean absolute error, while Expectile regression minimizes a weighted squared error.

The squared error here allows us to compute Expectile regression more easily compared to Quantile regression, using Iteratively reweighted least squares. For Quantile regression, a more elaborate method is needed.

In terms of comparison, Quantile regression is more robust, and easier to interpret, with quantiles being related to specific probabilities involving the underlying cumulative distribution function of the dataset; on the other expectiles are harder to interpret.

🔹 Trimming & Alterations

It is common to observe certain models ignoring very early Bitcoin price ranges. By default, we start our fit at the date 2010-07-16 to align with existing models.

By default, the model uses the number of time units (days, weeks...etc) elapsed since the beginning of history + 1 (to avoid NaN with log) as independent variable, however the Bitcoin All Time History Index INDEX:BTCUSD do not include the genesis block, as such users can correct for this by enabling the "Correct for Genesis block" setting, which will add the amount of missed bars from the Genesis block to the start oh the chart history.

🔶 SETTINGS

Start Date: Starting interval of the dataset used for the fit.

Correct for genesis block: When enabled, offset the X axis by the number of bars between the Bitcoin genesis block time and the chart starting time.

🔹 Expectiles

Toggle: Enable fit for the specified expectile. Disabling one fit will make the script faster to compute.

Expectile: Expectile (tau) value multiplied by 100 used for the fit. Higher values will produce fits that are located near price tops.

🔹 Forecast

Forecast End: Time at which the forecast stops.

🔹 Model Fit

Iterations Number: Number of iterations performed during the reweighted least squares process, with lower values leading to less accurate fits, while higher values will take more time to compute.

Wolf Exit Oscillator Enhanced

# Wolf Exit Oscillator Enhanced

## What it is (quick take)

**Wolf Exit Oscillator Enhanced** is a clean, rules-first **exit timing tool** built on the **True Strength Index (TSI)** with two optional safeguards:

1. **Signal-line crossover** (to avoid bailing on shallow dips), and

2. **EMA confirmation** (price-based “is the trend actually weakening/strengthening?” check).

Use it to standardize when you **take profits, cut losers, or scale out**—especially after momentum runs hot or cold.

> Works best **paired** with:

>

> * **ABS NR — Fail-Safe Confirm (v4.2.2)** for entries

> * **ABS Companion Oscillator — Trend / Exhaustion / New Trend** for trend/exhaustion context

---

## How to use it (operational workflow)

1. **Set your bands**

* `exitHigh` and `exitLow` mark “overcooked” zones on the TSI scale (default: +60 / –60).

* Above `exitHigh` = momentum stretched **up** (good place to **exit shorts** or **take long profits**).

* Below `exitLow` = momentum stretched **down** (good place to **exit longs** or **take short profits**).

2. **Choose strictness**

* **Base mode**: the moment TSI crosses out of a band, you get an exit signal.

* **Add Signal-Line Cross** (`enableSignalX = true`): require TSI to cross its signal in the same direction → **fewer, cleaner exits**.

* **Add EMA Filter** (`enableEMAFilter = true`): also require **price** to confirm (e.g., long exit only if price < EMA). This avoids bailing during healthy trends.

3. **Execute with structure**

* **Full exit** when a signal fires, or

* **Scale out** (e.g., 50% on first signal, remainder on trail/secondary signal), or

* **Move stop** to lock gains once an exit signal prints.

4. **Alerts**

* Set to **“Once per bar close”** to avoid intrabar flip-flop.

* Use the two provided alert names for automation (see “Alerts” below).

---

## Signals & visuals

* **TSI line** (solid) and **Signal line** (dashed) with optional **histogram** (TSI − Signal).

* **Horizontal bands** at `exitHigh` and `exitLow`.

* **Labels**:

* **Exit Long** appears when long-side momentum breaks down (below `exitLow`, plus any enabled filters).

* **Exit Short** appears when short-side momentum breaks down (above `exitHigh`, plus any enabled filters).

**Alerts (stable names):**

* **WolfExit — Exit Long**

* **WolfExit — Exit Short**

---

## Non-repainting behavior (what to expect)

* The oscillator is computed with **EMAs on current timeframe**—no higher-timeframe lookahead, no repaint.

* **Intrabar**: TSI/Signal can fluctuate; use **bar-close evaluation** (and alert setting “Once per bar close”) to lock signals.

* If you enable the EMA filter, that check is also evaluated at bar close.

---

## Every input explained (and how changing it alters behavior)

### Momentum engine (TSI)

* **TSI Long EMA Length (`tsiLongLen`, default 25)**

Higher = smoother, slower momentum; fewer signals. Lower = twitchier, more signals.

* **TSI Short EMA Length (`tsiShortLen`, default 13)**

Fine-tunes responsiveness on top of the long length. Lower short → snappier TSI.

* **TSI Signal Line Length (`tsisigLen`, default 7)**

Higher = slower signal line (harder to cross) → fewer signals. Lower = easier crosses → more signals.

### Thresholds (the bands)

* **Exit Threshold High (`exitHigh`, default +60)**

Raise to demand **stronger** overbought before signaling short exits / long profit-takes. Lower to trigger sooner.

* **Exit Threshold Low (`exitLow`, default −60)**

Raise (toward 0) to trigger **earlier** on longs; lower (more negative) to wait for deeper downside stretch.

### Confirmation layers

* **Require Signal Line Crossover (`enableSignalX`, default true)**

On = TSI must cross its signal (same direction as exit) → **filters out shallow wiggles**. Off = faster, more frequent exits.

* **Enable EMA Confirmation Filter (`enableEMAFilter`, default true)**

On = require **price < EMA** for **Exit Long** and **price > EMA** for **Exit Short**.

* **EMA Exit Confirmation Length (`exitEMALen`, default 50)**

Higher = **trendier** filter (harder to flip) → fewer exits; Lower = more reactive → more exits.

### Visuals

* **Show Histogram (`showHist`)**

On = quick visual for TSI–Signal spread (helps spot weakening momentum before a cross).

* **Plot Exit Signals (`showSignals`)**

Toggle labels if you only want the lines/bands with alerts.

---

## Tuning recipes (quick, practical)

* **Strong trend days (avoid premature exits)**

* Keep **`enableSignalX = true`** and **`enableEMAFilter = true`**

* Increase **`exitEMALen`** (e.g., 80)

* Consider raising **`exitHigh`** to 65–70 (and lowering **`exitLow`** to −65/−70)

* **Choppy/range days (exit faster, take the cash)**

* **`enableEMAFilter = false`** (don’t wait for price filter)

* **`enableSignalX`** optional; try off for quicker responses

* Bring bands closer to **±50** to take profits earlier

* **Scalping / lower timeframes**

* Shorten **TSI lengths** a bit (e.g., 21/9/5)

* Consider **`exitHigh=55 / exitLow=-55`**

* Keep **histogram on** to visualize momentum flip risk

* **Swing trading / higher timeframes**

* Lengthen **TSI** (e.g., 35/21/9) and **`exitEMALen`** (e.g., 100)

* Wider bands (±65 to ±75) to catch bigger moves before exiting

---

## Playbooks (how to actually trade it)

* **Entry from ABS NR FS, exit with Wolf**

* Take entries from **ABS NR — Fail-Safe Confirm** (triangle).

* Use **Wolf Exit** to scale out: 50% on first exit label, trail remainder with price/EMA or your stop logic.

* **Pyramid & protect**

* Add on re-accelerations (TSI pulls back toward zero without breaching the opposite band).

* The first **Exit** signal → take partial, raise stop to last higher low / lower high.

* **Mean-reversion fade management**

* When fading with ABS NR (KC band pokes + stretched |Z|), target the first opposite **Exit** signal as your “don’t overstay” cue.

---

## Suggested starting points

* **Day trading (5–15m):**

* TSI: **25 / 13 / 7** (default)

* Bands: **+60 / −60**

* Confirmations: **SignalX = on**, **EMA Filter = on**, **EMA Len = 50**

* Alerts: **Once per bar close**

* **Scalping (1–3m):**

* TSI: **21 / 9 / 5**

* Bands: **±55**

* Confirmations: **SignalX = on**, **EMA Filter = off** (optional for speed)

* **Swing (1h–D):**

* TSI: **35 / 21 / 9**

* Bands: **+65 / −65** (or ±70)

* Confirmations: **SignalX = on**, **EMA Filter = on**, **EMA Len = 100**

---

## Best-practice pairings

* **Entries:** **ABS NR — Fail-Safe Confirm (v4.2.2)**

* Take ABS triangles; let Wolf standardize exits so you’re not guessing.

* **Context:** **ABS Companion Oscillator**

* Prefer holding longer when the companion stays above (for longs) or below (for shorts) its neutral band and **no EXH tag** prints.

* If companion flags **EXH** against your position, tighten stops; Wolf’s next exit signal becomes high priority.

---

## Notes & disclaimers

* This is an **exit signal tool**, not a strategy or broker.

* Signals are strongest when aligned with your **entry logic** and a **risk framework** (position sizing, stops, partials).

* All evaluations are **current timeframe**; no higher-timeframe lookahead is used.

* Markets change—tune the bands and confirmations per symbol/timeframe.

---

**Tip:** Keep your alerts simple—one for **Exit Long**, one for **Exit Short**, **Once per bar close**. Use partial exits on the first signal, and let your stop/trailing logic handle the rest.

ATAI Triangles — Volume-Based & Price Pattern Analysis (v1.01)ATAI Triangles — Volume-Based & Price Pattern Analysis (v1.01)

Overview

ATAI Triangles identifies two synchronized triangle structures — Hi-Lo-Hi (HLH) and Lo-Hi-Lo (LHL) — and analyzes them both geometrically and volumetrically. For each triangle, volume is split between its two legs (segments), providing interpretable insights into buyer vs seller activity along each path.

The idea is that certain geometric shapes, when paired with volume distribution on each leg, can reveal patterns worth exploring. Users are encouraged to share their observations and interpretations in the TradingView comments section so that more aspects of these triangle combinations can be discovered collectively.

Extra (for fun)

For a bit of entertainment, we’ve included a symbolic “hexagram” glyph that appears when both triangle types align in a particular way — it’s just a visual nod to geometry and has no predictive or trading value.

Interface & data clarity

- Inputs and parameters are organized by function (pattern geometry, volume analysis, visuals, HUD, labels).

- Each input includes tooltips explaining its purpose, units, and possible effects on calculations.

- All on-chart objects (polylines, labels, connectors) are named and colored to reflect their role, with volume values formatted in engineering notation (K, M, B).

- HUD columns and label texts use concise terms and consistent units, so that every displayed value is directly traceable to a calculation in the code.

- Daily and lower-timeframe volume series are clearly separated, with update logic documented to indicate intrabar provisional values vs finalized bar-close values.

Usage notes

Designed to be used alongside other indicators and chart tools for context; it is not a standalone signal generator.

All Buy/Sell volumes are absolute (non-negative); Δ = Buy − Sell.

Intrabar values update live and finalize at bar close (no repaint after close).

Disclaimer

For research, discussion, and educational purposes only. This is not financial advice and does not guarantee any outcome. Trade at your own risk.

Harmonic Pattern Detection, Prediction, and Backtesting System3 Indikaotren in einem, Trendline, Patterns und Breaker Blocks

SPX Trendlines with VIX Levels By- Profit gang

This comprehensive technical analysis tool combines SPX trendline analysis with VIX volatility levels to help identify potential market turning points. The indicator is specifically designed with non-repainting logic to ensure reliability for both backtesting and live trading.

🔧 KEY FEATURES:

Non-Repainting Design: All signals and lines are drawn only on confirmed bars using barstate.isconfirmed

Dynamic Trendlines: Automatically draws support and resistance lines connecting recent pivot points

VIX Integration: Displays current VIX levels with customizable thresholds for market sentiment analysis

Multiple Visual Elements: Includes diagonal trendlines, horizontal level lines, and an information table

Comprehensive Alerts: Configurable alert system for both buy and sell signals

Clean Interface: Organized inputs and customizable colors for all elements

📊 TRADING CONCEPT:

The indicator utilizes the inverse relationship between VIX and SPX:

High VIX at pivot lows may indicate oversold conditions (potential buying opportunities)

Low VIX at pivot highs may signal complacency at market tops (potential caution zones)

🎛️ CUSTOMIZATION OPTIONS:

Toggle trendlines, VIX labels, and level lines independently

Adjust VIX thresholds (default: 25 high, 18 low)

Customize pivot length for sensitivity (default: 15)

Choose line styles (solid, dashed, dotted) and widths

Personalize all colors and alert preferences

📈 VISUAL COMPONENTS:

Red Lines: Resistance levels and trendlines

Green Lines: Support levels and trendlines

Information Table: Real-time VIX status and current levels

Signal Shapes: Triangle markers for confirmed buy/sell signals

Background Highlighting: Optional signal emphasis

⚠️ EDUCATIONAL PURPOSE:

This indicator is designed for educational and informational purposes. Past performance does not guarantee future results. Always conduct your own research and consider risk management before making trading decisions.

🔔 ALERT SYSTEM:

Separate alerts for buy and sell signals

All alerts trigger only on confirmed bars

Customizable alert messages with price and VIX data

Multiple alert condition options for flexible setup

Perfect for traders who want to combine technical analysis with volatility sentiment in a reliable, non-repainting format.

zSph x Larry Waves Wave Zone ForecastElliott Waves and Fibonacci Ratio Lengths have a strong correlated relationship when observing the general strength and termination of both Impulse (Motive) Waves and Corrective Waves.

There are certain Fibonacci levels that are highly reactive when applying it from a Wave Analysis perspective and being aware of the current wave sequence is required.

Often, those beginning their Elliott Wave journey and studies are unsure what Fibonacci levels are relevant and how to apply it to the wave structure that is being observed – this tool removes that ambiguity on placement.

Being aware of the predisposed levels that have a high rate of reaction can assist in managing trades from a scalp intra-day approach, a day trading approach, and a swing trading approach.

# Concept

This tool helps with identifying zones that are relevant to the wave that is currently in progression upon the market and visualize important Fibonacci levels where reactions often occur from an Elliott Wave perspective such as:

Wave 2

Wave 3

Wave 4

Wave 5

Wave B Zigzag

Wave B Flat

Wave X Zigzag

Wave X Flat

Wave C

Wave Y

This helps remove almost all the manual labor of updating fib levels, selecting certain fib levels, and manually moving the fib levels as price continues to print while autonomously providing the levels visually.

# Correct Usage

Wave 3 / Wave C / Wave Y

Once a clear impulse/motive structure has been identified for a Wave 1, Wave A or Wave W, apply the indicator to the structure.

Anchor 1 is the beginning of the impulse for Wave 1 or A or W.

Anchor 2 is the end of the impulse for Wave 1 or A or W.

The result is the standard zones for Wave 3, Wave C and Wave Y.

BINANCE:LINKUSD

Wave 4

Once a clear impulse/motive structure has been identified for Wave 3, apply the indicator to the structure.

Anchor 1 is the beginning of Wave 3 (or the end of Wave 2)

Anchor 2 is the end of Wave 3 (or the beginning of Wave 4)

The result is the standard zone for Wave 4.

LINKUSD

Wave B / Wave X / Wave C / Wave Y

Once a clear 3-wave corrective has been identified for a potential Corrective pattern, apply the indicator to the structure.

- Anchor 1 is the end of beginning of Wave A or Wave W

- Anchor 2 is the end of Wave A or Wave W

The result is the standard zones Waves B / X and Waves C / Y for Zigzags, Flats and Combos.

BINANCE:LINKUSD

# Settings

"Show Labels" will toggle on and off the labels for each fib zone, each fib line, and invalidation ticks that are in the 2/3 – B/C option to help with calculating risk management quickly.

"Use Log Scale" will allow you to toggle on/off the log scale for log fibs

"Extend Lines" will allow you to extend the fib lines to current price action from the Elliott Wave Zones to see reactions off the fib levels.

“Extend Zones” will allow you to extend the overall zone for the fibs to current price action from the Elliott Wave Zones to see reactions off the zone. There is also user customization of color use for the zones/.

“Fib Levels” will allow you to customize the lines and colors of the fibs lines.

“X-Axis Offset” will increase or decrease the position of the fibs of the zones (not the extension boxes)..

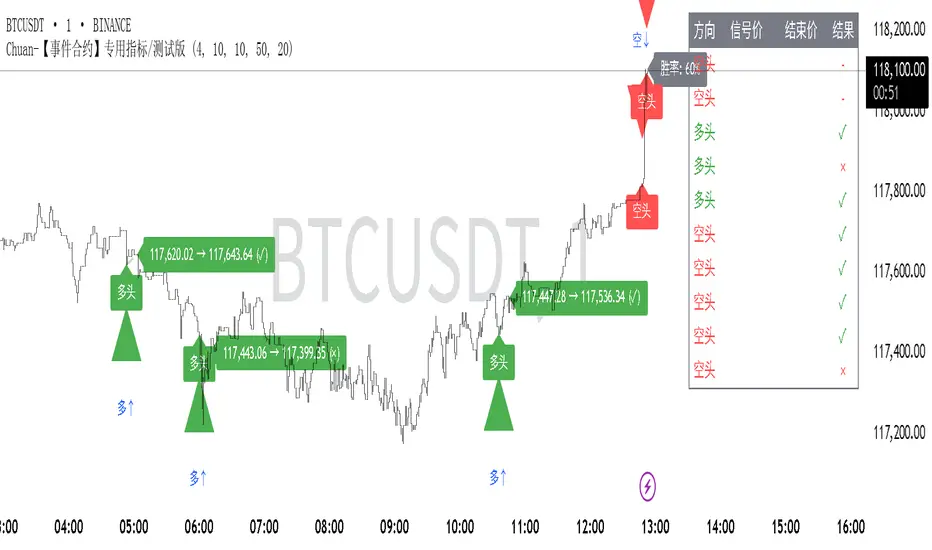

Chuan-事件合约专用指标-信号仅供参考This is a signal technical indicator developed by a technical analysis trader specifically for Binance event contracts. His name is ChuanCrypto

Multi - Timeframe 3 EMA Bull/Bear Table此指标是一个图标指标,适用于短线交易以及中线交易,它明确的显示出来了用EMA来表示方向指示,1分钟不可使用,此图表更新了多次以及修改了多次,在实际回测中有明显的提醒作用,不过多用于参考,不可作为主要指标使用,代码稍复杂如有加以改进的地方请提出,其中核心使用了EMA的20,50,200周期来作为参考,目的是能识别多周期和时间的方向指示,注意:此指标建议仅用于方向参考,不用于主要指标交易。

This indicator is a graphical indicator suitable for short-term and medium-term trading. It clearly shows the direction indicated by the EMA. It cannot be used for 1-minute intervals. This chart has been updated and modified multiple times, and it has a significant alerting effect in actual backtesting; however, it is mainly for reference and should not be used as the primary indicator. The code is somewhat complex, so please suggest improvements if there are any. The core uses the 20, 50, and 200 EMA periods as references, with the aim of identifying the direction indicators across multiple periods and timeframes. Note: This indicator is recommended only for directional reference and not for main indicator trading.

Bar TimeBar Time is a simple utility for traders who rely on backtesting, Bar Replay, and detailed price action analysis. It solves a common but frustrating problem: knowing the exact time of the bar you are looking at.

While most time indicators show your computer's live clock time, this tool displays the bar's own timestamp, perfectly synchronized with your chart's data and timezone.

Why Is This Important?

When you are deep in a Bar Replay session or analyzing a historical setup, the live clock is irrelevant. You need to know when that critical breakout or reversal candle actually happened. Was it during the pre-market? At the London open? In the last five minutes of the US session? This indicator provides that vital context instantly, without you needing to squint at the small print on the x-axis.

Key Use Cases

1. Mastering Bar Replay

As you click through bars in Replay mode, the displayed time updates with each new bar. This allows you to simulate a live trading session with full awareness of the time of day, helping you train your decision-making under more realistic conditions.

2. Analyzing Screener Signals

This is one of the most powerful uses. Imagine your screener finds a "BUY" signal on a stock from two bars ago. You switch to that stock's chart to investigate. Instead of hunting for the exact bar, this tool instantly shows you the date and time of the bar you are currently hovering over. It dramatically speeds up the workflow of moving from a screener alert to actionable analysis.

3. Detailed Price Action Study

Quickly identify key session timings, see how price reacts to news events at a specific time, or analyze intraday volume patterns with complete temporal clarity.

Features & Customization

The tool is designed to be lightweight, efficient, and fully customizable to match your charting environment.

Timezone-Aware Accuracy: Automatically detects your chart's timezone for a perfect match between the label and the x-axis.

Fully Customizable Position: Place the time display in any of nine screen positions (e.g., Top Left, Bottom Center) using a simple dropdown menu.

Custom Colors: Easily set the background and text colors to blend seamlessly with your chart's theme.

Market Clarity Pro Market Clarity Pro — See Key Zones, Trend & Volume Signals

Spot yesterday’s High (Supply) and Low (Demand) instantly — and know exactly where big buyers and sellers are likely waiting.

Red zones = strong selling pressure.

Green zones = strong buying pressure.

Plus, a built-in trend line keeps you trading in the right direction and away from sudden reversals.

You’ll also see:

🔴 Red arrow — not a sell signal, but a sign of heavy sellers stepping in, with volume confirmation and a candle breaking the previous one.

🔵 Blue arrow — not a buy signal, but a sign of strong buyers stepping in, with volume confirmation and a candle breaking the previous one.

These arrows highlight potential volume spikes and breakouts for confirmation only — you still confirm with the higher time frame for more market clarity.

Break above supply. Possible uptrend.

Break below demand. Possible downtrend.

📌 Before using this tool, watch the tutorial video to learn exactly how to apply it and how to spot profitable trades with confidence.

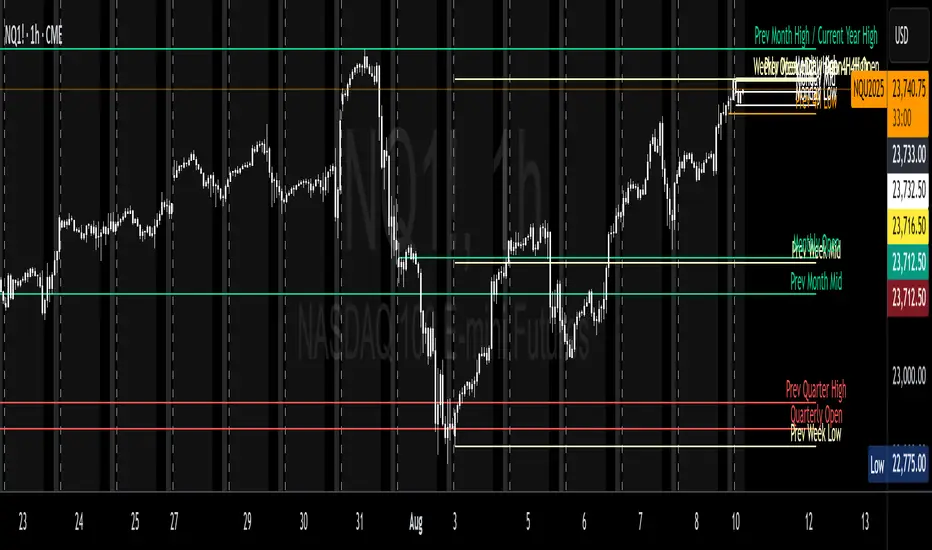

Key Levels ProThis indicator automatically plots important price levels from multiple timeframes and market sessions, such as opens, highs, lows, and midpoints . It dynamically tags each level as support or resistance based on current price position, so you instantly know how the market is reacting . When price touches a level, it’s highlighted with a subtle glow for easy visibility, and an optional alert can be triggered. This makes it easier to identify, track, and trade around high-probability zones without manually marking them yourself

CME_MINI:NQ1!

All credits to spacemanbtc for creating the original one and he inspired me do create this version for the TradingView community. I just improved what I thought it was missing like real-time alerts when price touches a new level.

Market Sessions — FOREXSOM Editionding for chart screenshots and videos.

Cleaner Interface: Organized settings into clear groups for a smoother user experience.

Bug Fixes: Improved “Only Last…” logic for more stable plotting.

Why I Use and Recommend It:

Easily spot active trading sessions with visual clarity.

Identify key institutional price levels in real time.

Ideal for day traders, swing traders, and anyone applying Smart Money Concepts.

Fully customizable colors and styles to fit any personal workflow.

Quant Signals: Econophysics-based MomentumPhysical Momentum Switcher (p0 / p1 / p2 / p3)

This indicator implements a “physical momentum” concept from quantitative finance research, where momentum is defined similarly to physics:

Momentum (p) = Mass × Velocity

Instead of using only the standard cumulative return (classic momentum), it lets you switch between multiple definitions:

p0: Cumulative return over the lookback period (no mass, just price change).

p1: Sum of (mass × velocity) over the lookback period.

p2: Weighted average velocity = (Σ mass×velocity) ÷ (Σ mass).

p3: Sharpe-like momentum = average velocity ÷ volatility (massless).

Velocity can be measured as:

Log return: ln(Pt / Pt-1)

Normal return: (Pt / Pt-1 – 1)

Mass (for p1/p2) can be defined as:

Unit mass (1) — equal weighting, equivalent to traditional momentum.

Turnover proxy — Volume ÷ average volume over k bars.

Value turnover proxy — Dollar volume ÷ average dollar volume.

Inverse volatility — 1 ÷ return volatility over a specified period.

Features:

Switchable momentum definition, velocity type, and mass type.

Adjustable lookback (k) and smoothing period for the signal line.

Optional ±1σ display bands for quick overbought/oversold visual cues.

Alerts for crosses above/below zero or the signal line.

Table display summarizing current settings and values.

Typical uses:

Momentum trading: Buy when PM > 0 (or crosses above the signal), sell/short when PM < 0 (or crosses below).

Contrarian strategies: Reverse the logic when testing mean-reversion effects.

Cross-asset testing: Apply to different instruments to see which PM definition works best.

Smart Fair Value Gaps (FVG) + MTF [Intelligent]This indicator elevates the standard Fair Value Gap (FVG) concept by introducing an intelligent classification system, advanced filtering, and integrated Multi-Timeframe (MTF) analysis. It is designed to move beyond simple FVG detection, providing traders with a deeper, more contextual understanding of market imbalances. By analyzing the characteristics of each FVG relative to recent historical data, the script helps to distinguish between high-momentum gaps and potential exhaustion points.

What is a Fair Value Gap (FVG)?

A Fair Value Gap, or price imbalance, is a three-candle pattern where the wick of the first candle does not overlap with the wick of the third candle. This creates an inefficient price delivery area that the market often seeks to revisit or "mitigate" in the future.

Bullish FVG: The space between the high of the first candle and the low of the third candle in a strong upward move.

Bearish FVG: The space between the low of the first candle and the high of the third candle in a strong downward move.

Key Features

Intelligent FVG Classification: This is the core of the indicator. Instead of treating all FVGs equally, it classifies them into four distinct types based on their size and the volume on which they formed, relative to a dynamic historical baseline.

🟡 Power FVG: High Size & High Volume Ratio. Indicates a gap formed with strong conviction and momentum, often a good continuation signal.

🟣 Exhaustion FVG: Low Size & High Volume Ratio. Suggests a high amount of effort (volume) for little price movement, which may indicate a trend is losing steam.

🟠 Absorption FVG: High Size & Low Volume Ratio. A significant price gap was created with relatively little volume, suggesting a lack of resistance and potential for price to move easily through that area.

🔵 Normal FVG: Any FVG that does not meet the criteria for the other classifications.

Multi-Timeframe (MTF) Analysis: Plot FVGs from a higher timeframe directly onto your current chart. These HTF zones often act as powerful areas of support or resistance and provide crucial context for lower-timeframe price action.

Advanced Filtering Suite: Gain complete control over which FVGs are displayed to reduce chart noise and focus on what matters.

Minimum Size Filter: Ignores insignificant micro-gaps by setting a minimum size requirement as a percentage of price.

EMA Trend Filter: Only display FVGs that align with the broader market trend (e.g., only show Bullish FVGs when price is above the 200 EMA).

Volume Filter: Qualify FVGs by requiring them to form on volume that is a specified multiple of its moving average, ensuring they are backed by significant market participation.

Comprehensive Customization: Tailor every aspect of the indicator to fit your personal trading style and chart aesthetic.

Mitigation Rules: Define precisely when an FVG is considered "mitigated" and no longer valid. Choose from a full fill, a 50% fill (Consequent Encroachment), or a simple wick touch.

Visuals & Data: Customize colors, borders, and box extensions. Toggle visuals for partial fills and the 50% CE line.

Data Labels: Display key information directly on the FVG boxes, including size in percentage and ticks, the volume of the FVG candle, and the volume ratio compared to the average.