RSI Div at Daily VWAP StDevMean Reversion indicator based on RSI Divergences at Overbought/Oversold conditions with Price above/below a Standard Deviation from Daily VWAP. Useful for intra-day trading.

Signal criteria:

1. RSI is at Overbought/Oversold

2. RSI Divergence present (not hidden)

3. RSI has not reached Neutral level (i.e. 50)

4. Price has crossed above/below a Standard Deviation from Daily VWAP

Config Options:

- RSI length (default:14)

- Divergence Lookback Period (default:14)

- RSI Oversold/Overbought tresholds (default: 70/30)

- RSI Reset Level (default: 55/45)

- Use VWAP Std Dev (default: yes)

- Standard Deviation from Daily VWAP (default: 1.51)

Use with discretion.

Volume Weighted Average Price (VWAP)

EmperorBTC's VWAP IndicatorThis indicator was created after EmperorBTC's conditions. Conditions displayed below:

Good timeframes for it: 30', 15', 5'

To convert from strategy to study switch the commented lines in the beginning and at the end of the script

What this indicator does is:

1) Check if Pivot Point was crossed

2) Stoch-RSI and VWAP were crossed up in current or previous candle

3) Candle (or previous candle) is green

Then, it will plot a Long opportunity.

FUTURE IDEAS:

- Volume Expansion

- Candle Stick patterns

(JS) Interchanging ATR & VWAP BandsOkay so this is pretty simple, but I think it's a great tool for day trading especially. I just took the default VWAP and Keltner channel scripts and combined them together.

The top option allows you to choose which one you'd prefer to use, "Use ATR instead of VWAP" .

The next options, "ATR Source", "KC Length", and "ATR Length" are the parameters for the ATR Bands.

"Number of Bands" allows you to choose how many bands you'd like to be on display (you can choose 1-8).

"Use Expoential MA" and "Band Style" are more default parameters from Keltner Channels used to set up the ATR Bands.

The "ATR Bands" are just stacked Keltner Channels separated by 1 ATR each, whereas the "VWAP Bands" are separated by standard deviation just like the default script from Trading View.

In these example chart, you can see the weekly VWAP with 8 deviation bands and 5 ATR bands with Keltner Channels.

USDT Average VolumeThis is showing the Volume multiplied by the VWAP to give a better visual of how much USD (or whatever currency you use) is traded per candle.

I use this on a 5min chart to see if trading on that coin could be useful with higher amounts.

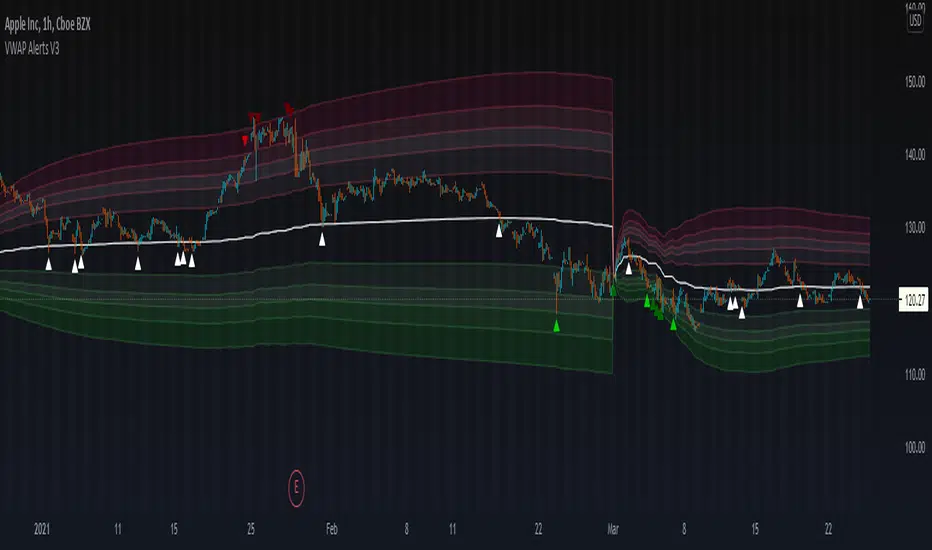

VWAP Alerts V3VWAP Alerts signal over bought/over sold conditions, relative to volume weighted average price, while deviation bands plot an extremely accurate point of mean reversion.

VWAP Alerts V3 includes multiple timeframe selection, along with multiplier input for deviation band setting

Alerts can be set for each individual band, for extreme oversold/overbought conditions, use "Vwap Low Deviation 4" and "Vwap High Deviation 4".

Alerts can also be set for VWAP bounces, by simply setting "VWAP Alert"

Chart Champions - Part 1 - nPOC - Levels - VWAPsThank you for sparing you time to read my indicator.

This indicator has been created as a suite of 3. This was to ensure that those with only the Free Trading View account could benefit (with their restriction to 3 indicators). Please ensure you install each indicator and read each indicator write up to fully understand what has tried to achieved.

Chart Champions – Part 1 –Lvls nPOC VWAPS

This indicator is broken down into:

• Levels

• VWAPS

• Naked Point of Control

Levels

It displays the levels to the right of the price Axis to enable the user to have a cleaner chart.

The below levels will automatically appear:

dOpen – pdHigh – pdLow – pdEQ – pwEQ

Optional Levels include:

mOpen – pmOpen – pdOpen – dbyOpen – wOpen – pwOpen

VWAPs

Optional VWAPs

Daily (including pdVWAP close) – Weekly – Monthly

Naked Points of Control (nPOC)

To view the nPOC move the chart back in time to pick up the nPOCs.

Chart Champions – Part 2 – CCV IBs POC

This indicator is broken down into:

• Chart Champions Value

• Initial Balance

• Points of Control

Chart Champions Value (CCV)

CCV is based on the 80% rule of the dOpen opening outside of the pdVAH/pdVAL. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Initial Balance (IB)

IB is based on the first 60 minutes of the market opening. It captures the highest and lowest points within that 60 minutes. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Points of Control (POCs)

POC are the price levels where the most volume was traded.

Developing POC (dPOC) will constantly move with volume/price action through out the day.

Optional POCs

Previous Day POC (pdPOC) – Day Before Yesterday POC (dbyPOC)

Chart Champions – Part 3 – Sessions - Manual Input

This indicator is broken down into:

• Manual Inputs (daily, weekly, monthly)

• IGOR SessionsTtimes

• Pre + Market Openings

Manual Input

Daily x3

Weekly x 3

Monthly x 3

This allows the trader to put in specific levels.

IGOR Session Times

This is a user specific requirement to highlight cetain times during the day, displayed at the bottom of the chart in the colour strip.

Pre + Market Openings

This allows the user to see when pre market trading has started and with the live maket has started, displayed at the top of the chart in colours.

A huge thank you goes out to:

Stackoverflow users AnyDozer and Bjorn.

TV user ahancock for allow me use of this code.

Disclaimer the lower the timeframe the more information it processes.

Gunzo Market SRGunzo Market SR is a set of 3 tools combined for trend analysis on day trading strategy.

VWAP (Volume Weighted Average Price) :

The VWAP indicator is generally used for trend analysis. For example if the VWAP line is under the closing price for a long period of time, the trend is strong. In this script, the VWAP has been optimized for day trading as the indicator is calculated inside the daily range, and resets when a new day starts. This way the indicator reflects the daily trend and not the overall trend. You can also use the position of closing price according to the VWAP to find optimal entry points according to the indicator.

Highs / Lows :

The Highs / Lows are generally used for trend analysis too. The High / Lows are mainly used to identify prices that have been key during the past and that we can use as an indication for the following candles. In this script, the Highs / Lows are computed on the daily period and then displayed on the current period (recommended to use on a daily period or lower). This way the indicator reflects the highest point and the lowest point of the day (can be modified to have a longer range of pivot days even if I recommend to stay on 1 day for day trading).

Support / Resistance :

The Support / Resistance is generally used for trend analysis too. The Support / Resistance are found by searching local high and lows. The longer the supports and resistance are, the strongest it can be considered. In this script, the Highs / Lows are computed by default on a lower time frame (usually 3-4 times lower). For example on a 15 minute graph, the Highs / Lows will be computed on the 5 minute graph (can be modified if the displayed result is not optimized for your asset).

How to use this set of tools :

I personally recommend to use this tool at the start of your day of trading. This way you will get a clear vision of the daily situation and try to identify key prices and the trend for the current day. I then suggest to set up an alert on the key price to be notified when you're getting close to it.

Strongholds - Objective & Accurate Reference Points / StructuresVery early in my trading career, I came across Pivot Points only to find out that there are as many calculations as one pleases. It was hard to find out which ones work. Most of them probably did only out of randomness, so I ditched the strategy and looked for something else.

I previously used my Oracle Eye and Reference Points scripts but it is time for an upgrade.

Stronghold is a script I have used for quite some time now. I ditched daily and weekly closing prices as not that important. Instead, Strongholds are equipped with:

►Daily High & Low • Azure color

►Weekly High & Low • Dark blue

►Weekly old High & Low • Semi-transparent dark circles

►Monthly High & Low • Wizardly purple

There is an option to print:

►4h High & Low • Semi-transparent red

►VWAP • Lovely purple

►Weekly VWAP • Black

All of the levels and lines are set for 1m, 5m, 10m, 15m, 30m, 1h, 4h, 1D timeframes. If you use any alien timeframe, you may need to enter the code.

You can opt-in and out for certain timeframes. For example, daily levels are visible from 15m or 30, so the indicator won't draw them unless you want to. However, they will not be seen on higher timeframes as there is no reason to show them and oversaturate the chart with lines.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

Remember that if you use this script with auto-scale, you need to tick Scale Price Chart Only . Otherwise, your chart will fly to the moon!

Good luck & have fun!

Cvwap-Pvwap 2.0A simple vwap based Intraday trend indicator.

Volume-Weighted Average Price (VWAP) - the average price weighted by volume, starts when trading opens and ends when it closes. This can help institutions buy or sell in large orders, without disturbing the market.

After buying or selling, institutions compare instrument price to closing VWAP values at end of the day.

For big financial institutions;

A buy order executed below the VWAP value, considered a good fill because the security was bought at a below average price.

A sell order executed above the VWAP would be deemed a good fill because it was sold at an above average price.

Simple price based moving average is not helpful for them; = as it doesn't incorporates volume traded. Hence - VWAP :)

So how it helps us in decoding the IntraDay-trend? - Through a 2 day vwap co-relation.

So, Closing value of previous day vwap = Pvwap

Today's running vwap = Cvwap

Defining the IntraDay Trend:

Moderately Bullish = candle closing price above Pvwap but below Cvwap

Super Bullish = Closing price is above both (Cvwap and Pvwap)

Moderately Bearish = Closing price is above Cvwap but below Pvwap

Super Bearish = Closing Price is below both (Cvwap and Pvwap)

A big gap between the Cvwap and the candle closing price defines the strong participation from institutions in that direction. (Strong Trend)

Moving with the smart money, in the overall trend is a wise decision for any intraday trader and this helps at its best.

Origin VWAP: OVWAPDraw a VWAP support/resistance line anchored to the origin of the data series (like a daily VWAP, but from the beginning of time, never resetting).

Ideally the origin would be the first bar after the IPO. Tradingview (or your connected broker) doesn't always have a complete dataset, and in that case the OVWAP will be 'wrong', but converging to the correct value over time.

You can try to simulate this with the built-in VWAP indicator but it has several bugs and limitations. Firstly, the longest time period is century, but it is not 100 years, ie. a rolling century but the beginning of the century: 21 years ago. Secondly, even if your dataset is less than 21 years, if you use a lower time frame then the built-in VWAP's origin becomes the left-most loaded bar (about 5,000 bars ago) - it will draw the wrong value. The new Anchored VWAP drawing tool can't be used on lower time frames as it won't draw the line at all unless it sees the point where you anchored it.

You may want to cut 'n paste this code to use in some larger strategy. Unfortunately that's probably not possible. This script uses the 'resolution=' option of 'study()' set to '1W', so the whole script runs at the 1 week resolution. You would think it would be possible to instead use the 'security()' function to request data at the '1W' resolution, but it just resamples the current data set and so is limited to the rightmost 5,000 bars.

Look in the options to enable standard deviation lines.

Flunki VWAP minus MA OscillatorHerewith a simple oscillator that show the difference in price between a Moving Average of the price, and the current VWAP

This show as a histogram

On top of that is a Moving Average of the histogram value, shown as a blue / red line with an option to hight these crossing and also crossing zero

Simple idea ; code open.

VWAP with Standard Deviation BandsVolume Weighted Average Price (VWAP), with Standard Deviation Bands

VWAP is a moving average with weighting for traded volume, so heavier trading activity has a greater impact on its direction. Low volume periods will move the VWAP less than high volume periods.

The VWAP is important because institutional investors often use it to determine what is ‘fair value’. You can often see the market reacting when it gets close to the VWAP.

This version is time segmented VWAP. It reset ma values when selected time period expires.

Time periods are able to be selected in the settings: "1D", "2D", "W", "14D", "M", "60D", "12M", "24M", "Custom".

Additionally script determines VWAP standard deviations.

Multipliers for VWAP Standard Deviation Bands can be changed in the settings.

There is also option to show previous VWAP and its Standard Deviation Bands before timeframe reset.

|AG| VWAP ANALYSIS|AG| VWAP ANALYSIS

The volume-weighted average price (VWAP) is a trading benchmark used by traders that gives the average price security has traded throughout the day, based on both volume and price.

It is important because it provides traders with insight into both the trend and value of the security.

VWAP is calculated by adding up the $ traded for every transaction (price multiplied by the number of shares traded) and then dividing by the total shares traded.

A detailed formula and calculations could be found here:

-> fanf2.user.srcf.net

Actually, TradingView has an option for Anchored Vwap is a really good implementation for specific analysis.

The following script takes into account the #Time_Period_Change and plots the VWAP calculation.

The #Time_Period Available for this script are:

-> Day

-> Week

-> Monthly

-> Quarter

-> Year

1. The option that we have is the SOURCE:

-> HLC3 (High, Low, Close)/3 is the right way to calculate VWAP.

-> But I included other traditional options:

-> open, high, low, close, hl2, hlc3, ohlc4

2. The option of Turn ON/OFF VWAP

-> Timeframe selection:

-> All, 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year, 6. >=Weekly, 7. >=Montlhy

-> With this, we could select the time for plotting the VWAP. And some cool features such as >= that we are going to plot different Timeframes VWAP calculations.

-> Vwap Label:

-> We could select if show labels or not

3. The option of Turn ON/OFF Previous VWAP Level

-> VWAP of one selected Time Period is going to end with a final price this level most of the time is retested and gives us a good opportunity for entry into one trade.

Or could be used as Stop Loss.

-> Timeframe selection:

-> 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year, 6. >=Weekly, 7. >=Montlhy, 8. >=Daily

-> Factor

-> The factor options lead as increment the extension of the previous time period.

-> Example: D is the normal time period and with factor, we change from 1D to 2D in order to extend previous levels of VWAP.

->The Factor option is only available in 1. Day and 2. Week. With a Min Value of 1 and a Maximum Value of 50.

-> Labels:

-> We could select if show labels or not

4. The option of Turn ON/OFF Standard Deviation Bands

-> Label:

-> We could select if show labels or not

-> Timeframe selection:

-> 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year

5. The option of Turn ON/OFF Previous Standard Deviation

-> Timeframe selection:

-> None, 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year, 6. >=Weekly, 7. >=Montlhy, 8. Quarter & Year

-> STDEV LEVEL

-> Since there are different options for Standard Deviation I included 4 options

-> 1

-> 2

-> 3

-> User Selection

-> In this option we could select any NUMBER for STVDEV 0.25 of step.

-> Label:

-> We could select if show labels or not

6. The Lockback Setting

-> This Script also includes an option to only plot a certain amount of days back.

The main reason in order to have a more clear chart.

-> We could select between:

-> PLOT ALL

-> CUSTOM

-> If we select Custom Then we could select the Number of Days Back that is going to be plotted.

7. Color Theme

Here we select the color (Visual Desing)

-> Color Theme

-> Text Color

-> Here I use the recent input.color option added for TradingView making the color selection really simple

8. Time Period Highlighter

-> In this option, we could select one time period in order to plot one tiny background and identify the change in the time period.

-> Timeframe selection:

-> 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year

9. Label Offset

-> Finally, this option leads us to change the position of the labels into the X-axis by default 20.

This script has many options the combinations and the possibilities of making different analyses are bast.

Here some examples of what we could make:

DEFAULT SETTING:

PREVIOUS VWAP FOR TIME PERIOD >= WEEK

(work good as S&D levels)

PREVIOUS VWAP Week WITH A FACTOR OF 4

STANDARD DEVIATION BANDS - DAY

STANDARD DEVIATION BANDS - WEEK

STANDARD DEVIATION BANDS - MONTH

STANDARD DEVIATION BANDS - QUARTER

STANDARD DEVIATION BANDS - YEAR

PREVIOUS STANDARD DEVIATION - DAY SDTV 3

PREVIOUS STANDARD DEVIATION - WEEK SDTV 3

USING STANDARD DEVIATION BANDS - WEEK

WITH LOCKBACK -> PLOT ALL

WITH CUSTOM 30 DAYS

I think the options possibilities of analysis using #VWAP are truly awesome.

I like the relationship that one previous VWAP has with Standard Pivot Points.

Good Luck,

Anderson,

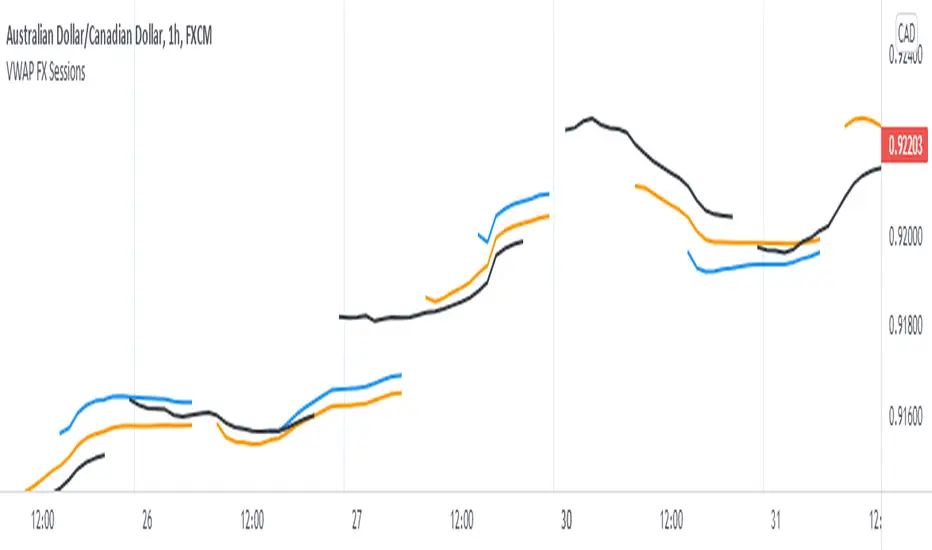

Triple VWAP for FOREX SessionsThis script runs on my previous script Masterwork VWAP .

►It uses regular built-in VWAP improved to avoid weird connecting of the line with its yesterday's value.

►It starts a new VWAP when London session opens . You can select to end it next morning or when the session is about to close.

►It starts a new VWAP when New York session opens . You can select to end it next morning or when the session is about to close.

►You can select intelligent_enabler function to plot the VWAPs on your chart when viewing low timeframe charts (1m, 5m, 15m, 30m)

VWAPmP (ATR as % Version)This indicator displays a histogram for the distance of closing price from a VWAP value. The VWAP length is rolling and its value is user defined. Additionally, there are 3 bands which are based on the %-value of the underlying ATR. The ATR's length can be chosen by the user, and the distance multipliers may also be chosen. Lastly, there are two simple moving averages which have user-defined lengths and are based on the histograms value.

Divergence RSI-VWAPCombination of the script from XaviZ of RSI-VWAP and divergence detector from Libertus.

MTF VWAP + Fibo Incremental deviationsI made a Fibo variant of my first script "VWAPs + devs" :

This new indicator give you the possibility to plot multi timeframes VWAP (D, W, M, 3M and 12M ) and Fibo deviations for each one.

VWAP is a powerfull indicator which is used by big players to get informations if the price is "overbought" or "oversold". Deviations give the opportunity to have supports and resistances in those "over"-zones.

I searched for better results and found those defaults values :

Fib 1 level : 0.618

Fib 2 level : 0.786

Fib 3 level : 1.000

Fib 4 level : 1.618

Fib 5 level : 2.618

In the thumbnail, we can see that the 1.618 deviation level made a great support on the last uptrend for BTCUSDT .

You can change each values but low ones as 0.382 and 0.5 don't give really interesting supports/resistances.

I made this script as clear and simple as possible with only one menu in the parameters.

Some examples of what you can do :

BTCUSDT (Binance) H4 / D, W, M, 3M ,12M VWAP without devs

BTCUSDT (Binance) M5 / Daily VWAP + Fibo devs

Hope this will be useful for you !

Ultimate VWAP Bands- Ultimate VWAP Bands is a script that helps to decide and further clarify areas of oversold and overbought conditions.

- For example, when the price is in the lowest band it is extremely oversold relative to the VWAP . Hence it should be considered a good place to buy with a high risk to reward payoff.

- Each band is set at a fixed offset away from the VWAP . The "VWAP Band Multiplier" adjusts this and is a key part of the script. This allows the indicator to be adjusted based on the assets volatility . For example, with Crypto. A multiplier of 1 would be strongly advised. Whilst a multiplier of 0.1-0.25 would be useful for currency pairs.

- This indicator can be used for all manners of trading. However, it is most effective when used for scalping and swing trading.

Nic's Anchored VWAP 4Poor mans anchored vwap. Allows you to identified the volume weighted average price from 4 specific points in time.

Best used on key pivot point high's and lows'

CC - Array-meta Consolidated Interval Display (ACID)This script extends my other two Array examples (which I've also provided to you open source):

The Ticker-centric 5m,15m,45m,1h,4h,1d resolution labels using arrays:

And the more Macro VIX,GLD,TLT,QQQ,SPY,IWM 1d resolution labels using arrays:

This script aims to show how to use min/max/avg with Arrays easily. My next example after this will be exploring the usage of variance versus covariance ratios over different periodic interval resolutions. Currently, this is using the following intervals: 5m,15m,45m,1h,4h,1d. It takes these intervals, calculates the values at those resolutions and puts the absolute min and max from the 5 minute to the 1 day resolutions.

It's more of an example of the power that arrays can hold, as all this truly is right now is a min/max bound calculator. The real gem lies in the avg calculators for multiple resoltuions tied into a single label with readable data. Check out the code and let me know what you think. If you need more examples, the other two scripts I mentioned before are also open source.

Using this on intervals of less than 1D sometimes times out, the way I wrote it is memory intensive, may not work for non-pro users.

Thanks!

NONE OF THIS IS FOREWARD LOOKING STATEMENTS, THIS IS NOT A PREDECTIVE ANALYSIS TOOL. THIS IS A RESEARCH ATTEMPT AT A NOVEL INDICATOR. I am not responsible for outcomes using it.

Please use and give criticisms freely. I am experimenting with combining resolutions and comparing covariance values at different levels right now, so let me know your thoughts! The last indicator will likely not be open source, but may be depending on how complex I get.