PubLibSwingLibrary "PubLibSwing"

swing high and swing low conditions, prices, bar indices and range ratios for indicator and strategy development

sh()

swing high condition

Returns: bool

sl()

swing low condition

Returns: bool

shbi(occ)

swing high bar index, condition occurrence n

Parameters:

occ (simple int)

Returns: int

slbi(occ)

swing low bar index, condition occurrence n

Parameters:

occ (simple int)

Returns: int

shcp(occ)

swing high close price, condition occurrence n

Parameters:

occ (simple int)

Returns: float

slcp(occ)

swing low close price, condition occurrence n

Parameters:

occ (simple int)

Returns: float

shp(occ)

swing high price, condition occurrence n

Parameters:

occ (simple int)

Returns: float

slp(occ)

swing low price, condition occurrence n

Parameters:

occ (simple int)

Returns: float

shpbi(occ)

swing high price bar index, condition occurrence n

Parameters:

occ (simple int)

Returns: int

slpbi(occ)

swing low price bar index, condition occurrence n

Parameters:

occ (simple int)

Returns: int

shrr(occ)

swing high range ratio, condition occurrence n

Parameters:

occ (simple int)

Returns: float

slrr(occ)

swing low range ratio, condition occurrence n

Parameters:

occ (simple int)

Returns: float

Techindicator

PubLibCandleTrendLibrary "PubLibCandleTrend"

candle trend, multi-part candle trend, multi-part green/red candle trend, double candle trend and multi-part double candle trend conditions for indicator and strategy development

chh()

candle higher high condition

Returns: bool

chl()

candle higher low condition

Returns: bool

clh()

candle lower high condition

Returns: bool

cll()

candle lower low condition

Returns: bool

cdt()

candle double top condition

Returns: bool

cdb()

candle double bottom condition

Returns: bool

gc()

green candle condition

Returns: bool

gchh()

green candle higher high condition

Returns: bool

gchl()

green candle higher low condition

Returns: bool

gclh()

green candle lower high condition

Returns: bool

gcll()

green candle lower low condition

Returns: bool

gcdt()

green candle double top condition

Returns: bool

gcdb()

green candle double bottom condition

Returns: bool

rc()

red candle condition

Returns: bool

rchh()

red candle higher high condition

Returns: bool

rchl()

red candle higher low condition

Returns: bool

rclh()

red candle lower high condition

Returns: bool

rcll()

red candle lower low condition

Returns: bool

rcdt()

red candle double top condition

Returns: bool

rcdb()

red candle double bottom condition

Returns: bool

chh_1p()

1-part candle higher high condition

Returns: bool

chh_2p()

2-part candle higher high condition

Returns: bool

chh_3p()

3-part candle higher high condition

Returns: bool

chh_4p()

4-part candle higher high condition

Returns: bool

chh_5p()

5-part candle higher high condition

Returns: bool

chh_6p()

6-part candle higher high condition

Returns: bool

chh_7p()

7-part candle higher high condition

Returns: bool

chh_8p()

8-part candle higher high condition

Returns: bool

chh_9p()

9-part candle higher high condition

Returns: bool

chh_10p()

10-part candle higher high condition

Returns: bool

chh_11p()

11-part candle higher high condition

Returns: bool

chh_12p()

12-part candle higher high condition

Returns: bool

chh_13p()

13-part candle higher high condition

Returns: bool

chh_14p()

14-part candle higher high condition

Returns: bool

chh_15p()

15-part candle higher high condition

Returns: bool

chh_16p()

16-part candle higher high condition

Returns: bool

chh_17p()

17-part candle higher high condition

Returns: bool

chh_18p()

18-part candle higher high condition

Returns: bool

chh_19p()

19-part candle higher high condition

Returns: bool

chh_20p()

20-part candle higher high condition

Returns: bool

chh_21p()

21-part candle higher high condition

Returns: bool

chh_22p()

22-part candle higher high condition

Returns: bool

chh_23p()

23-part candle higher high condition

Returns: bool

chh_24p()

24-part candle higher high condition

Returns: bool

chh_25p()

25-part candle higher high condition

Returns: bool

chh_26p()

26-part candle higher high condition

Returns: bool

chh_27p()

27-part candle higher high condition

Returns: bool

chh_28p()

28-part candle higher high condition

Returns: bool

chh_29p()

29-part candle higher high condition

Returns: bool

chh_30p()

30-part candle higher high condition

Returns: bool

chl_1p()

1-part candle higher low condition

Returns: bool

chl_2p()

2-part candle higher low condition

Returns: bool

chl_3p()

3-part candle higher low condition

Returns: bool

chl_4p()

4-part candle higher low condition

Returns: bool

chl_5p()

5-part candle higher low condition

Returns: bool

chl_6p()

6-part candle higher low condition

Returns: bool

chl_7p()

7-part candle higher low condition

Returns: bool

chl_8p()

8-part candle higher low condition

Returns: bool

chl_9p()

9-part candle higher low condition

Returns: bool

chl_10p()

10-part candle higher low condition

Returns: bool

chl_11p()

11-part candle higher low condition

Returns: bool

chl_12p()

12-part candle higher low condition

Returns: bool

chl_13p()

13-part candle higher low condition

Returns: bool

chl_14p()

14-part candle higher low condition

Returns: bool

chl_15p()

15-part candle higher low condition

Returns: bool

chl_16p()

16-part candle higher low condition

Returns: bool

chl_17p()

17-part candle higher low condition

Returns: bool

chl_18p()

18-part candle higher low condition

Returns: bool

chl_19p()

19-part candle higher low condition

Returns: bool

chl_20p()

20-part candle higher low condition

Returns: bool

chl_21p()

21-part candle higher low condition

Returns: bool

chl_22p()

22-part candle higher low condition

Returns: bool

chl_23p()

23-part candle higher low condition

Returns: bool

chl_24p()

24-part candle higher low condition

Returns: bool

chl_25p()

25-part candle higher low condition

Returns: bool

chl_26p()

26-part candle higher low condition

Returns: bool

chl_27p()

27-part candle higher low condition

Returns: bool

chl_28p()

28-part candle higher low condition

Returns: bool

chl_29p()

29-part candle higher low condition

Returns: bool

chl_30p()

30-part candle higher low condition

Returns: bool

clh_1p()

1-part candle lower high condition

Returns: bool

clh_2p()

2-part candle lower high condition

Returns: bool

clh_3p()

3-part candle lower high condition

Returns: bool

clh_4p()

4-part candle lower high condition

Returns: bool

clh_5p()

5-part candle lower high condition

Returns: bool

clh_6p()

6-part candle lower high condition

Returns: bool

clh_7p()

7-part candle lower high condition

Returns: bool

clh_8p()

8-part candle lower high condition

Returns: bool

clh_9p()

9-part candle lower high condition

Returns: bool

clh_10p()

10-part candle lower high condition

Returns: bool

clh_11p()

11-part candle lower high condition

Returns: bool

clh_12p()

12-part candle lower high condition

Returns: bool

clh_13p()

13-part candle lower high condition

Returns: bool

clh_14p()

14-part candle lower high condition

Returns: bool

clh_15p()

15-part candle lower high condition

Returns: bool

clh_16p()

16-part candle lower high condition

Returns: bool

clh_17p()

17-part candle lower high condition

Returns: bool

clh_18p()

18-part candle lower high condition

Returns: bool

clh_19p()

19-part candle lower high condition

Returns: bool

clh_20p()

20-part candle lower high condition

Returns: bool

clh_21p()

21-part candle lower high condition

Returns: bool

clh_22p()

22-part candle lower high condition

Returns: bool

clh_23p()

23-part candle lower high condition

Returns: bool

clh_24p()

24-part candle lower high condition

Returns: bool

clh_25p()

25-part candle lower high condition

Returns: bool

clh_26p()

26-part candle lower high condition

Returns: bool

clh_27p()

27-part candle lower high condition

Returns: bool

clh_28p()

28-part candle lower high condition

Returns: bool

clh_29p()

29-part candle lower high condition

Returns: bool

clh_30p()

30-part candle lower high condition

Returns: bool

cll_1p()

1-part candle lower low condition

Returns: bool

cll_2p()

2-part candle lower low condition

Returns: bool

cll_3p()

3-part candle lower low condition

Returns: bool

cll_4p()

4-part candle lower low condition

Returns: bool

cll_5p()

5-part candle lower low condition

Returns: bool

cll_6p()

6-part candle lower low condition

Returns: bool

cll_7p()

7-part candle lower low condition

Returns: bool

cll_8p()

8-part candle lower low condition

Returns: bool

cll_9p()

9-part candle lower low condition

Returns: bool

cll_10p()

10-part candle lower low condition

Returns: bool

cll_11p()

11-part candle lower low condition

Returns: bool

cll_12p()

12-part candle lower low condition

Returns: bool

cll_13p()

13-part candle lower low condition

Returns: bool

cll_14p()

14-part candle lower low condition

Returns: bool

cll_15p()

15-part candle lower low condition

Returns: bool

cll_16p()

16-part candle lower low condition

Returns: bool

cll_17p()

17-part candle lower low condition

Returns: bool

cll_18p()

18-part candle lower low condition

Returns: bool

cll_19p()

19-part candle lower low condition

Returns: bool

cll_20p()

20-part candle lower low condition

Returns: bool

cll_21p()

21-part candle lower low condition

Returns: bool

cll_22p()

22-part candle lower low condition

Returns: bool

cll_23p()

23-part candle lower low condition

Returns: bool

cll_24p()

24-part candle lower low condition

Returns: bool

cll_25p()

25-part candle lower low condition

Returns: bool

cll_26p()

26-part candle lower low condition

Returns: bool

cll_27p()

27-part candle lower low condition

Returns: bool

cll_28p()

28-part candle lower low condition

Returns: bool

cll_29p()

29-part candle lower low condition

Returns: bool

cll_30p()

30-part candle lower low condition

Returns: bool

gc_1p()

1-part green candle condition

Returns: bool

gc_2p()

2-part green candle condition

Returns: bool

gc_3p()

3-part green candle condition

Returns: bool

gc_4p()

4-part green candle condition

Returns: bool

gc_5p()

5-part green candle condition

Returns: bool

gc_6p()

6-part green candle condition

Returns: bool

gc_7p()

7-part green candle condition

Returns: bool

gc_8p()

8-part green candle condition

Returns: bool

gc_9p()

9-part green candle condition

Returns: bool

gc_10p()

10-part green candle condition

Returns: bool

gc_11p()

11-part green candle condition

Returns: bool

gc_12p()

12-part green candle condition

Returns: bool

gc_13p()

13-part green candle condition

Returns: bool

gc_14p()

14-part green candle condition

Returns: bool

gc_15p()

15-part green candle condition

Returns: bool

gc_16p()

16-part green candle condition

Returns: bool

gc_17p()

17-part green candle condition

Returns: bool

gc_18p()

18-part green candle condition

Returns: bool

gc_19p()

19-part green candle condition

Returns: bool

gc_20p()

20-part green candle condition

Returns: bool

gc_21p()

21-part green candle condition

Returns: bool

gc_22p()

22-part green candle condition

Returns: bool

gc_23p()

23-part green candle condition

Returns: bool

gc_24p()

24-part green candle condition

Returns: bool

gc_25p()

25-part green candle condition

Returns: bool

gc_26p()

26-part green candle condition

Returns: bool

gc_27p()

27-part green candle condition

Returns: bool

gc_28p()

28-part green candle condition

Returns: bool

gc_29p()

29-part green candle condition

Returns: bool

gc_30p()

30-part green candle condition

Returns: bool

rc_1p()

1-part red candle condition

Returns: bool

rc_2p()

2-part red candle condition

Returns: bool

rc_3p()

3-part red candle condition

Returns: bool

rc_4p()

4-part red candle condition

Returns: bool

rc_5p()

5-part red candle condition

Returns: bool

rc_6p()

6-part red candle condition

Returns: bool

rc_7p()

7-part red candle condition

Returns: bool

rc_8p()

8-part red candle condition

Returns: bool

rc_9p()

9-part red candle condition

Returns: bool

rc_10p()

10-part red candle condition

Returns: bool

rc_11p()

11-part red candle condition

Returns: bool

rc_12p()

12-part red candle condition

Returns: bool

rc_13p()

13-part red candle condition

Returns: bool

rc_14p()

14-part red candle condition

Returns: bool

rc_15p()

15-part red candle condition

Returns: bool

rc_16p()

16-part red candle condition

Returns: bool

rc_17p()

17-part red candle condition

Returns: bool

rc_18p()

18-part red candle condition

Returns: bool

rc_19p()

19-part red candle condition

Returns: bool

rc_20p()

20-part red candle condition

Returns: bool

rc_21p()

21-part red candle condition

Returns: bool

rc_22p()

22-part red candle condition

Returns: bool

rc_23p()

23-part red candle condition

Returns: bool

rc_24p()

24-part red candle condition

Returns: bool

rc_25p()

25-part red candle condition

Returns: bool

rc_26p()

26-part red candle condition

Returns: bool

rc_27p()

27-part red candle condition

Returns: bool

rc_28p()

28-part red candle condition

Returns: bool

rc_29p()

29-part red candle condition

Returns: bool

rc_30p()

30-part red candle condition

Returns: bool

cdut()

candle double uptrend condition

Returns: bool

cddt()

candle double downtrend condition

Returns: bool

cdut_1p()

1-part candle double uptrend condition

Returns: bool

cdut_2p()

2-part candle double uptrend condition

Returns: bool

cdut_3p()

3-part candle double uptrend condition

Returns: bool

cdut_4p()

4-part candle double uptrend condition

Returns: bool

cdut_5p()

5-part candle double uptrend condition

Returns: bool

cdut_6p()

6-part candle double uptrend condition

Returns: bool

cdut_7p()

7-part candle double uptrend condition

Returns: bool

cdut_8p()

8-part candle double uptrend condition

Returns: bool

cdut_9p()

9-part candle double uptrend condition

Returns: bool

cdut_10p()

10-part candle double uptrend condition

Returns: bool

cdut_11p()

11-part candle double uptrend condition

Returns: bool

cdut_12p()

12-part candle double uptrend condition

Returns: bool

cdut_13p()

13-part candle double uptrend condition

Returns: bool

cdut_14p()

14-part candle double uptrend condition

Returns: bool

cdut_15p()

15-part candle double uptrend condition

Returns: bool

cdut_16p()

16-part candle double uptrend condition

Returns: bool

cdut_17p()

17-part candle double uptrend condition

Returns: bool

cdut_18p()

18-part candle double uptrend condition

Returns: bool

cdut_19p()

19-part candle double uptrend condition

Returns: bool

cdut_20p()

20-part candle double uptrend condition

Returns: bool

cdut_21p()

21-part candle double uptrend condition

Returns: bool

cdut_22p()

22-part candle double uptrend condition

Returns: bool

cdut_23p()

23-part candle double uptrend condition

Returns: bool

cdut_24p()

24-part candle double uptrend condition

Returns: bool

cdut_25p()

25-part candle double uptrend condition

Returns: bool

cdut_26p()

26-part candle double uptrend condition

Returns: bool

cdut_27p()

27-part candle double uptrend condition

Returns: bool

cdut_28p()

28-part candle double uptrend condition

Returns: bool

cdut_29p()

29-part candle double uptrend condition

Returns: bool

cdut_30p()

30-part candle double uptrend condition

Returns: bool

cddt_1p()

1-part candle double downtrend condition

Returns: bool

cddt_2p()

2-part candle double downtrend condition

Returns: bool

cddt_3p()

3-part candle double downtrend condition

Returns: bool

cddt_4p()

4-part candle double downtrend condition

Returns: bool

cddt_5p()

5-part candle double downtrend condition

Returns: bool

cddt_6p()

6-part candle double downtrend condition

Returns: bool

cddt_7p()

7-part candle double downtrend condition

Returns: bool

cddt_8p()

8-part candle double downtrend condition

Returns: bool

cddt_9p()

9-part candle double downtrend condition

Returns: bool

cddt_10p()

10-part candle double downtrend condition

Returns: bool

cddt_11p()

11-part candle double downtrend condition

Returns: bool

cddt_12p()

12-part candle double downtrend condition

Returns: bool

cddt_13p()

13-part candle double downtrend condition

Returns: bool

cddt_14p()

14-part candle double downtrend condition

Returns: bool

cddt_15p()

15-part candle double downtrend condition

Returns: bool

cddt_16p()

16-part candle double downtrend condition

Returns: bool

cddt_17p()

17-part candle double downtrend condition

Returns: bool

cddt_18p()

18-part candle double downtrend condition

Returns: bool

cddt_19p()

19-part candle double downtrend condition

Returns: bool

cddt_20p()

20-part candle double downtrend condition

Returns: bool

cddt_21p()

21-part candle double downtrend condition

Returns: bool

cddt_22p()

22-part candle double downtrend condition

Returns: bool

cddt_23p()

23-part candle double downtrend condition

Returns: bool

cddt_24p()

24-part candle double downtrend condition

Returns: bool

cddt_25p()

25-part candle double downtrend condition

Returns: bool

cddt_26p()

26-part candle double downtrend condition

Returns: bool

cddt_27p()

27-part candle double downtrend condition

Returns: bool

cddt_28p()

28-part candle double downtrend condition

Returns: bool

cddt_29p()

29-part candle double downtrend condition

Returns: bool

cddt_30p()

30-part candle double downtrend condition

Returns: bool

CandleAnalysisLibrary "CandleAnalysis"

A collection of frequently used candle analysis functions in my scripts.

isBullish(barsBack)

Checks if a specific bar is bullish.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar is bullish, otherwise returns false.

isBearish(barsBack)

Checks if a specific bar is bearish.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar is bearish, otherwise returns false.

isBE(barsBack)

Checks if a specific bar is break even.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar is break even, otherwise returns false.

getBodySize(barsBack, inPriceChg)

Calculates a specific candle's body size.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

inPriceChg (bool) : (bool) True to return the body size as a price change value. The default is false (in points).

Returns: The candle's body size in points.

getTopWickSize(barsBack, inPriceChg)

Calculates a specific candle's top wick size.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

inPriceChg (bool) : (bool) True to return the wick size as a price change value. The default is false (in points).

Returns: The candle's top wick size in points.

getBottomWickSize(barsBack, inPriceChg)

Calculates a specific candle's bottom wick size.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

inPriceChg (bool) : (bool) True to return the wick size as a price change value. The default is false (in points).

Returns: The candle's bottom wick size in points.

getBodyPercent(barsBack)

Calculates a specific candle's body size as a percentage of its entire size including its wicks.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: The candle's body size percentage.

isHammer(fib, bullish, barsBack)

Checks if a specific bar is a hammer candle based on a given fibonacci level.

Parameters:

fib (float) : (float) The fibonacci level to base candle's body on. The default is 0.382.

bullish (bool) : (bool) True if the candle must to be green. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a hammer candle, otherwise returns false.

isShootingStar(fib, bearish, barsBack)

Checks if a specific bar is a shooting star candle based on a given fibonacci level.

Parameters:

fib (float) : (float) The fibonacci level to base candle's body on. The default is 0.382.

bearish (bool) : (bool) True if the candle must to be red. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a shooting star candle, otherwise returns false.

isDoji(wickSize, bodySize, barsBack)

Checks if a specific bar is a doji candle based on a given wick and body size.

Parameters:

wickSize (float) : (float) The maximum top wick size compared to the bottom and vice versa. The default is 1.5.

bodySize (float) : (bool) The maximum body size as a percentage compared to the entire candle size. The default is 5.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a doji candle.

isBullishEC(gapTolerance, rejectionWickSize, engulfWick, barsBack)

Checks if a specific bar is a bullish engulfing candle.

Parameters:

gapTolerance (int)

rejectionWickSize (int) : (int) The maximum top wick size compared to the body as a percentage. The default is 10.

engulfWick (bool) : (bool) True if the engulfed candle's wick requires to be engulfed as well. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a bullish engulfing candle.

isBearishEC(gapTolerance, rejectionWickSize, engulfWick, barsBack)

Checks if a specific bar is a bearish engulfing candle.

Parameters:

gapTolerance (int)

rejectionWickSize (int) : (int) The maximum bottom wick size compared to the body as a percentage. The default is 10.

engulfWick (bool) : (bool) True if the engulfed candle's wick requires to be engulfed as well. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a bearish engulfing candle.

MarcosLibraryLibrary "MarcosLibrary"

A colection of frequently used functions in my scripts.

bullFibRet(priceLow, priceHigh, fibLevel)

Calculates a bullish fibonacci retracement value.

Parameters:

priceLow (float) : (float) The lowest price point.

priceHigh (float) : (float) The highest price point.

fibLevel (float) : (float) The fibonacci level to calculate.

Returns: The fibonacci value of the given retracement level.

bearFibRet(priceLow, priceHigh, fibLevel)

Calculates a bearish fibonacci retracement value.

Parameters:

priceLow (float) : (float) The lowest price point.

priceHigh (float) : (float) The highest price point.

fibLevel (float) : (float) The fibonacci level to calculate.

Returns: The fibonacci value of the given retracement level.

bullFibExt(priceLow, priceHigh, thirdPivot, fibLevel)

Calculates a bullish fibonacci extension value.

Parameters:

priceLow (float) : (float) The lowest price point.

priceHigh (float) : (float) The highest price point.

thirdPivot (float) : (float) The third price point.

fibLevel (float) : (float) The fibonacci level to calculate.

Returns: The fibonacci value of the given extension level.

bearFibExt(priceLow, priceHigh, thirdPivot, fibLevel)

Calculates a bearish fibonacci extension value.

Parameters:

priceLow (float) : (float) The lowest price point.

priceHigh (float) : (float) The highest price point.

thirdPivot (float) : (float) The third price point.

fibLevel (float) : (float) The fibonacci level to calculate.

Returns: The fibonacci value of the given extension level.

isBullish(barsBack)

Checks if a specific bar is bullish.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar is bullish, otherwise returns false.

isBearish(barsBack)

Checks if a specific bar is bearish.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar is bearish, otherwise returns false.

isBE(barsBack)

Checks if a specific bar is break even.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar is break even, otherwise returns false.

getBodySize(barsBack, inPriceChg)

Calculates a specific candle's body size.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

inPriceChg (bool) : (bool) True to return the body size as a price change value. The default is false (in points).

Returns: The candle's body size in points.

getTopWickSize(barsBack, inPriceChg)

Calculates a specific candle's top wick size.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

inPriceChg (bool) : (bool) True to return the wick size as a price change value. The default is false (in points).

Returns: The candle's top wick size in points.

getBottomWickSize(barsBack, inPriceChg)

Calculates a specific candle's bottom wick size.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

inPriceChg (bool) : (bool) True to return the wick size as a price change value. The default is false (in points).

Returns: The candle's bottom wick size in points.

getBodyPercent(barsBack)

Calculates a specific candle's body size as a percentage of its entire size including its wicks.

Parameters:

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: The candle's body size percentage.

isHammer(fib, bullish, barsBack)

Checks if a specific bar is a hammer candle based on a given fibonacci level.

Parameters:

fib (float) : (float) The fibonacci level to base candle's body on. The default is 0.382.

bullish (bool) : (bool) True if the candle must to be green. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a hammer candle, otherwise returns false.

isShootingStar(fib, bearish, barsBack)

Checks if a specific bar is a shooting star candle based on a given fibonacci level.

Parameters:

fib (float) : (float) The fibonacci level to base candle's body on. The default is 0.382.

bearish (bool) : (bool) True if the candle must to be red. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a shooting star candle, otherwise returns false.

isDoji(wickSize, bodySize, barsBack)

Checks if a specific bar is a doji candle based on a given wick and body size.

Parameters:

wickSize (float) : (float) The maximum top wick size compared to the bottom and vice versa. The default is 1.5.

bodySize (float) : (bool) The maximum body size as a percentage compared to the entire candle size. The default is 5.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a doji candle.

isBullishEC(gapTolerance, rejectionWickSize, engulfWick, barsBack)

Checks if a specific bar is a bullish engulfing candle.

Parameters:

gapTolerance (int)

rejectionWickSize (int) : (int) The maximum top wick size compared to the body as a percentage. The default is 10.

engulfWick (bool) : (bool) True if the engulfed candle's wick requires to be engulfed as well. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a bullish engulfing candle.

isBearishEC(gapTolerance, rejectionWickSize, engulfWick, barsBack)

Checks if a specific bar is a bearish engulfing candle.

Parameters:

gapTolerance (int)

rejectionWickSize (int) : (int) The maximum bottom wick size compared to the body as a percentage. The default is 10.

engulfWick (bool) : (bool) True if the engulfed candle's wick requires to be engulfed as well. The default is false.

barsBack (int) : (int) The number of bars to look back. The default is 0 (current bar).

Returns: True if the bar matches the requirements of a bearish engulfing candle.

VandelayIndicatorLibLibrary "VandelayIndicatorLib"

Art Vandelay's Indicator library

STC_VIL(EEEEEE, BBBB, BBBBB)

Schaff Trend Cycle Calculations

Parameters:

EEEEEE (int) : = Slengt, BBBB = FALenght, BBBBB = SLOLenght

BBBB (simple int)

BBBBB (simple int)

Returns: Long : mAAAAA > mAAAAA - Short : mAAAAA < mAAAAA

stc(source, fast, slow, cycle, d1, d2)

Calculates the value of the Schaff Trend Cycle indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

fast (simple int) : (simple int) Length for the MACD fast smoothing parameter calculation.

slow (simple int) : (simple int) Length for the MACD slow smoothing parameter calculation.

cycle (simple int) : (simple int) Number of bars for the Stochastic values (length).

d1 (simple int) : (simple int) Length for the initial %D smoothing parameter calculation.

d2 (simple int) : (simple int) Length for the final %D smoothing parameter calculation.

Returns: (float) The oscillator value.

Cinnamon_Bear Indicators MA LibraryLibrary "Cinnamon_BearIndicatorsMALibrary"

This is a personal Library of the NON built-in PineScript Moving Average function used to code indicators

ma_dema(source, length)

Double Exponential Moving Average (DEMA)

Parameters:

source (simple float)

length (simple int)

Returns: A double level of smoothing helps to follow price movements more closely while still reducing noise compared to a single EMA.

ma_dsma(source, length)

Double Smoothed Moving Average (DSMA)

Parameters:

source (simple float)

length (simple int)

Returns: A double level of smoothing helps to follow price movements more closely while still reducing noise compared to a single SMA.

ma_tema(source, length)

Triple Exponential Moving Average (TEMA)

Parameters:

source (simple float)

length (simple int)

Returns: A Triple level of smoothing helps to follow price movements even more closely compared to a DEMA.

ma_vwema(source, length)

Volume-Weighted Exponential Moving Average (VWEMA)

Parameters:

source (simple float)

length (simple int)

Returns: The VWEMA weights based on volume and recent price, giving more weight to periods with higher trading volumes.

ma_hma(source, length)

Hull Moving Average (HMA)

Parameters:

source (simple float)

length (simple int)

Returns: The HMA formula combines the properties of the weighted moving average (WMA) and the exponential moving average (EMA) to achieve a smoother and more responsive curve.

ma_ehma(source, length)

Enhanced Moving Average (EHMA)

Parameters:

source (simple float)

length (simple int)

Returns: The EHMA is calculated similarly to the Hull Moving Average (HMA) but uses a different weighting factor to further improve responsiveness.

ma_trix(source, length)

Triple Exponential Moving Average (TRIX)

Parameters:

source (simple float)

length (simple int)

Returns: The TRIX is an oscillator that shows the percentage change of a triple EMA. It is designed to filter out minor price movements and display only the most significant trends. The TRIX is a momentum indicator that can help identify trends and buy or sell signals.

ma_lsma(source, length)

Linear Weighted Moving Average (LSMA)

Parameters:

source (simple float)

length (simple int)

Returns: A moving average that gives more weight to recent prices. It is calculated using a formula that assigns linear weights to prices, with the highest weight given to the most recent price and the lowest weight given to the furthest price in the series.

ma_wcma(source, length)

Weighted Cumulative Moving Average (WCMA)

Parameters:

source (simple float)

length (simple int)

Returns: A moving average that gives more weight to recent prices. Compared to a LSMA, the WCMA the weights of data increase linearly with time, so the most recent data has a greater weight compared to older data. This means that the contribution of the most recent data to the moving average is more significant.

ma_vidya(source, length)

Variable Index Dynamic Average (VIDYA)

Parameters:

source (simple float)

length (simple int)

Returns: It is an adaptive moving average that adjusts its momentum based on market volatility using the formula of Chande Momentum Oscillator (CMO) .

ma_zlma(source, length)

Zero-Lag Moving Average (ZLMA)

Parameters:

source (simple float)

length (simple int)

Returns: Its aims to minimize the lag typically associated with MA, designed to react more quickly to price changes.

ma_gma(source, length, power)

Generalized Moving Average (GMA)

Parameters:

source (simple float)

length (simple int)

power (simple int)

Returns: It is a moving average that uses a power parameter to adjust the weight of historical data. This allows the GMA to adapt to various styles of MA.

ma_tma(source, length)

Triangular Moving Average (TMA)

Parameters:

source (simple float)

length (simple int)

Returns: MA more sensitive to changes in recent data compared to the SMA, providing a moving average that better adapts to short-term price changes.

[ALGOA+] AutofiboLibrary "Autofibo"

fibonacci(up, down, calculate, log, color1, color2, plot)

Creates an array with fibbonaci levels and plots lines.

Parameters:

up (float)

down (float)

calculate (bool)

log (bool)

color1 (color)

color2 (color)

plot (bool)

Returns: --> var float tupple.

fibonacciExtension(up, down, direction, log, calculate, color1, plot)

Fibonacci extension.

@description up (float) Up level.

@description down (float) Down level.

@description direction (string) Options "up" or "down".

Parameters:

up (float)

down (float)

direction (string)

log (bool)

calculate (bool)

color1 (color)

plot (bool)

Returns: -> var float, var float

trendFibo(uptrend, downtrend, log_option, color1, color2, plot)

Calculates automatic fibo values based on trends, returning a tupple with most important values.

Parameters:

uptrend (bool)

downtrend (bool)

log_option (bool)

color1 (color)

color2 (color)

plot (bool)

Returns:

VolumeSpreadAnalysisLibrary "VolumeSpreadAnalysis"

A library for Volume Spread Analysis (VSA).

spread(_barIndex)

Calculates the spread of a bar.

Parameters:

_barIndex (int) : (int) The index of the bar.

Returns: (float) The spread of the bar.

volume(_barIndex)

Retrieves the volume of a bar.

Parameters:

_barIndex (int) : (int) The index of the bar.

Returns: (float) The volume of the bar.

body(_barIndex)

Calculates the body of a bar.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The body size of the bar.

wickUpper(_barIndex)

Calculates the upper wick of a bar (upper shadow).

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The upper wick size of the bar.

wickLower(_barIndex)

Calculates the lower wick of a bar (lower shadow).

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The lower wick size of the bar.

calcForecastedSMA(_source, _length, _forecastedLevel)

Calculates the forecasted Simple Moving Average (SMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the SMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted SMA value.

calcForecastedEMA(_source, _length, _forecastedLevel)

Calculates the forecasted Exponential Moving Average (EMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the EMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted EMA value.

calcForecastedRMA(_source, _length, _forecastedLevel)

Calculates the forecasted Relative Moving Average (RMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the RMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted RMA value.

calcForecastedWMA(_source, _length, _forecastedLevel)

Calculates the forecasted Weighted Moving Average (WMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the WMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted WMA value.

calcElapsedTimePercent()

Calculates the elapsed time percent of the current bar.

Returns: (float) The elapsed time percent.

calcForecastedSpread(multiplierAtMidpoints, multiplierAtPeaks)

Calculates the forecasted spread using elapsed time and dynamic multipliers, handling spread's non-linear nature.

Parameters:

multiplierAtMidpoints (float) : (float) The multiplier value at midpoints.

multiplierAtPeaks (float) : (float) The multiplier value at peaks.

Returns: (float) The forecasted spread value.

calcForecastedVolume()

Calculates the forecasted volume using elapsed time, satisfying volume's linear nature.

Returns: (float) The forecasted volume value.

calcForecastedMA(_source, _length, _forecastedSource, _type)

Calculates the forecasted Moving Average (MA) based on the specified type.

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the MA.

_forecastedSource (float) : (float) The forecasted level to include in the calculation.

_type (simple string) : (string) The type of the MA ("SMA", "EMA", "SMMA (RMA)", "WMA").

Returns: (float) The forecasted MA value.

calcMA(_source, _length, _type)

Calculates the Moving Average (MA) based on the specified type.

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the MA.

_type (simple string) : (string) The type of the MA ("SMA", "EMA", "SMMA (RMA)", "WMA").

Returns: (float) The MA value.

bullBar(_barIndex)

Determines if the bar is bullish.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if the bar is bullish, otherwise false.

bearBar(_barIndex)

Determines if the bar is bearish.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if the bar is bearish, otherwise false.

breakout(_barIndex)

Determines if there is a breakout above the previous bar.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if there is a breakout, otherwise false.

breakdown(_barIndex)

Determines if there is a breakdown below the previous bar.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if there is a breakdown, otherwise false.

rejectionWickUpper(_rejectionWick)

Determines if the upper wick is a rejection wick.

Parameters:

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if the upper wick is a rejection wick, otherwise false.

rejectionWickLower(_rejectionWick)

Determines if the lower wick is a rejection wick.

Parameters:

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if the lower wick is a rejection wick, otherwise false.

setupDataVolume(_data, _mult_Low, _mult_High, _mult_Ultra, _maLengthVolume, _maTypeVolume)

Sets up data for volume levels.

Parameters:

_data (map) : (map) The map to store the levels.

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthVolume (simple int) : (int) The length for MA.

_maTypeVolume (simple string) : (string) The type for MA.

Returns: (void) Nothing.

setupDataSpread(_data, _mult_Low, _mult_High, _mult_Ultra, _maLengthSpread, _maTypeSpread)

Sets up data for spread levels.

Parameters:

_data (map) : (map) The map to store the levels.

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthSpread (simple int) : (int) The length for MA.

_maTypeSpread (simple string) : (string) The type for MA.

Returns: (void) Nothing.

setupDataForecastVolume(_dataForecast, _mult_Low, _mult_High, _mult_Ultra, _maLengthVolume, _predictedLevelVolume, _maTypeVolume)

Sets up data for volume and spread levels for forecast.

Parameters:

_dataForecast (map)

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthVolume (simple int) : (int) The length for MA.

_predictedLevelVolume (float) : (float) The predicted level for MA.

_maTypeVolume (simple string) : (string) The type for MA.

Returns: (void) Nothing.

setupDataForecastSpread(_dataForecast, _mult_Low, _mult_High, _mult_Ultra, _maLengthSpread, _predictedLevelSpread, _maTypeSpread)

Sets up data for spread levels for forecast.

Parameters:

_dataForecast (map)

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthSpread (simple int) : (int) The length for MA.

_predictedLevelSpread (float) : (float) The predicted level for MA.

_maTypeSpread (simple string) : (string) The type for MA.

Returns: (void) Nothing.

isVolumeLow(_data, _barIndex)

Determines if the volume is low.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is low, otherwise false.

isVolumeNormal(_data, _barIndex)

Determines if the volume is normal.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is normal, otherwise false.

isVolumeHigh(_data, _barIndex)

Determines if the volume is high.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is high, otherwise false.

isVolumeUltra(_data, _barIndex)

Determines if the volume is ultra.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is ultra, otherwise false.

isSpreadLow(_data, _barIndex)

Determines if the spread is low.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is low, otherwise false.

isSpreadNormal(_data, _barIndex)

Determines if the spread is normal.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is normal, otherwise false.

isSpreadHigh(_data, _barIndex)

Determines if the spread is high.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is high, otherwise false.

isSpreadUltra(_data, _barIndex)

Determines if the spread is ultra.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is ultra, otherwise false.

isVolumeText(_data)

Determines text string representing the volume area level.

Parameters:

_data (map) : (map) The data map with volume levels.

Returns: (string) Text string of Low, Normal, High, or Ultra.

isSpreadText(_data)

Determines text string representing the spread area level.

Parameters:

_data (map) : (map) The data map with spread levels.

Returns: (string) Text string of Low, Normal, High, or Ultra.

calcBarColor(_value, _level)

Calculates the color based level.

Parameters:

_value (float) : (float) The value to check.

_level (float) : (float) The value level for comparison.

Returns: (color) The color for the bar.

bullPinBar(_maxBodyPercent, _minWickPercent)

Determines if the bar is a bull pin bar.

Parameters:

_maxBodyPercent (simple float) : (float) The maximum body percentage.

_minWickPercent (simple float) : (float) The minimum wick percentage.

Returns: (bool) True if the bar is a bull pin bar, otherwise false.

bearPinBar(_maxBodyPercent, _minWickPercent)

Determines if the bar is a bear pin bar.

Parameters:

_maxBodyPercent (simple float) : (float) The maximum body percentage.

_minWickPercent (simple float) : (float) The minimum wick percentage.

Returns: (bool) True if the bar is a bear pin bar, otherwise false.

dojiBar(_maxBodyPercent)

Determines if the bar is a doji.

Parameters:

_maxBodyPercent (simple float) : (float) The maximum body percentage.

Returns: (bool) True if the bar is a doji, otherwise false.

spinningTopBar(_minWicksPercent, _emaLength)

Determines if the bar is a spinning top.

Parameters:

_minWicksPercent (simple float) : (float) The minimum wicks percentage.

_emaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if the bar is a spinning top, otherwise false.

highWaveBar(_minBodyPercent, _minWickPercent, _bars)

Determines if the bar is a high wave bar.

Parameters:

_minBodyPercent (simple float) : (float) The minimum body percentage.

_minWickPercent (simple float) : (float) The minimum wick percentage.

_bars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if the bar is a high wave bar, otherwise false.

consolidationBar(_data, _spread, _bars)

Determines if the bars are in consolidation.

Parameters:

_data (map) : (map) The data map with spread levels.

_spread (simple float) : (float) The spread percentage for comparison.

_bars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if the bars are in consolidation, otherwise false.

S_DownThrust(_data, _bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of strength (DownThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of strength (DownThrust), otherwise false.

S_SellingClimax(_data, _rejectionWick)

Determines if there is a sign of strength (Selling Climax).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if there is a sign of strength (Selling Climax), otherwise false.

S_NoEffortBearishResult()

Determines if there is a sign of strength (No Effort Bearish Result).

Returns: (bool) True if there is a sign of strength (No Effort Bearish Result), otherwise false.

S_BearishEffortNoResult()

Determines if there is a sign of strength (Bearish Effort No Result).

Returns: (bool) True if there is a sign of strength (Bearish Effort No Result), otherwise false.

S_InverseDownThrust(_data, _bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of strength (Inverse DownThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of strength (Inverse DownThrust), otherwise false.

S_FailedSellingClimax()

Determines if there is a sign of strength (Failed Selling Climax).

Returns: (bool) True if there is a sign of strength (Failed Selling Climax), otherwise false.

S_BullOutsideReversal(_data)

Determines if there is a sign of strength (Bull Outside Reversal).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of strength (Bull Outside Reversal), otherwise false.

S_EndOfFallingMarket(_data)

Determines if there is a sign of strength (End of Falling Market).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of strength (End of Falling Market), otherwise false.

S_PseudoDownThrust(_bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of strength (Pseudo DownThrust).

Parameters:

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of strength (Pseudo DownThrust), otherwise false.

S_NoSupply(_bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of strength (No Supply).

Parameters:

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of strength (No Supply), otherwise false.

W_UpThrust(_data, _bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of weakness (UpThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of weakness (UpThrust), otherwise false.

W_BuyingClimax(_data, _rejectionWick)

Determines if there is a sign of weakness (Buying Climax).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if there is a sign of weakness (Buying Climax), otherwise false.

W_NoEffortBullishResult()

Determines if there is a sign of weakness (No Effort Bullish Result).

Returns: (bool) True if there is a sign of weakness (No Effort Bullish Result), otherwise false.

W_BullishEffortNoResult()

Determines if there is a sign of weakness (Bullish Effort No Result).

Returns: (bool) True if there is a sign of weakness (Bullish Effort No Result), otherwise false.

W_InverseUpThrust(_data, _bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of weakness (Inverse UpThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of weakness (Inverse UpThrust), otherwise false.

W_FailedBuyingClimax()

Determines if there is a sign of weakness (Failed Buying Climax).

Returns: (bool) True if there is a sign of weakness (Failed Buying Climax), otherwise false.

W_BearOutsideReversal(_data)

Determines if there is a sign of weakness (Bear Outside Reversal).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of weakness (Bear Outside Reversal), otherwise false.

W_EndOfRisingMarket(_data)

Determines if there is a sign of weakness (End of Rising Market).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of weakness (End of Rising Market), otherwise false.

W_PseudoUpThrust(_bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of weakness (Pseudo UpThrust).

Parameters:

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of weakness (Pseudo UpThrust), otherwise false.

W_NoDemand(_bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of weakness (No Demand).

Parameters:

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of weakness (No Demand), otherwise false.

N_QuietDoji(_dojiBarMaxBody)

Determines if there is a neutral signal (Quiet Doji).

Parameters:

_dojiBarMaxBody (simple float) : (float) The maximum body percentage for doji bar.

Returns: (bool) True if there is a neutral signal (Quiet Doji), otherwise false.

N_BalancedDoji(_data, _dojiBarMaxBody)

Determines if there is a neutral signal (Balanced Doji).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_dojiBarMaxBody (simple float) : (float) The maximum body percentage for doji bar.

Returns: (bool) True if there is a neutral signal (Balanced Doji), otherwise false.

N_StrongDoji(_dojiBarMaxBody)

Determines if there is a neutral signal (Strong Doji).

Parameters:

_dojiBarMaxBody (simple float) : (float) The maximum body percentage for doji bar.

Returns: (bool) True if there is a neutral signal (Strong Doji), otherwise false.

N_QuietSpinningTop(_spinningTopBarMinWicks, _spinningTopBarEmaLength)

Determines if there is a neutral signal (Quiet Spinning Top).

Parameters:

_spinningTopBarMinWicks (simple float) : (float) The minimum wicks percentage for spinning top bar.

_spinningTopBarEmaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if there is a neutral signal (Quiet Spinning Top), otherwise false.

N_BalancedSpinningTop(_data, _spinningTopBarMinWicks, _spinningTopBarEmaLength)

Determines if there is a neutral signal (Balanced Spinning Top).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_spinningTopBarMinWicks (simple float) : (float) The minimum wicks percentage for spinning top bar.

_spinningTopBarEmaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if there is a neutral signal (Balanced Spinning Top), otherwise false.

N_StrongSpinningTop(_spinningTopBarMinWicks, _spinningTopBarEmaLength)

Determines if there is a neutral signal (Strong Spinning Top).

Parameters:

_spinningTopBarMinWicks (simple float) : (float) The minimum wicks percentage for spinning top bar.

_spinningTopBarEmaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if there is a neutral signal (Strong Spinning Top), otherwise false.

N_QuietHighWave(_highWaveBarMinBody, _highWaveBarMinWick, _highWaveBarBars)

Determines if there is a neutral signal (Quiet High Wave).

Parameters:

_highWaveBarMinBody (simple float) : (float) The minimum body percentage for high wave bar.

_highWaveBarMinWick (simple float) : (float) The minimum wick percentage for high wave bar.

_highWaveBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Quiet High Wave), otherwise false.

N_BalancedHighWave(_data, _highWaveBarMinBody, _highWaveBarMinWick, _highWaveBarBars)

Determines if there is a neutral signal (Balanced High Wave).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_highWaveBarMinBody (simple float) : (float) The minimum body percentage for high wave bar.

_highWaveBarMinWick (simple float) : (float) The minimum wick percentage for high wave bar.

_highWaveBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Balanced High Wave), otherwise false.

N_StrongHighWave(_highWaveBarMinBody, _highWaveBarMinWick, _highWaveBarBars)

Determines if there is a neutral signal (Strong High Wave).

Parameters:

_highWaveBarMinBody (simple float) : (float) The minimum body percentage for high wave bar.

_highWaveBarMinWick (simple float) : (float) The minimum wick percentage for high wave bar.

_highWaveBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Strong High Wave), otherwise false.

N_Consolidation(_data, _consolidationBarSpread, _consolidationBarBars)

Determines if there is a neutral signal (Consolidation).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_consolidationBarSpread (simple float) : (float) The spread percentage for consolidation bar.

_consolidationBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Consolidation), otherwise false.

ImrLibraryLibrary "ImrLibrary"

TODO: add library description here

STG(Length)

TODO: add function description here

Parameters:

Length (int)

Returns: TODO: add what function returns

ISI(Length)

Parameters:

Length (simple int)

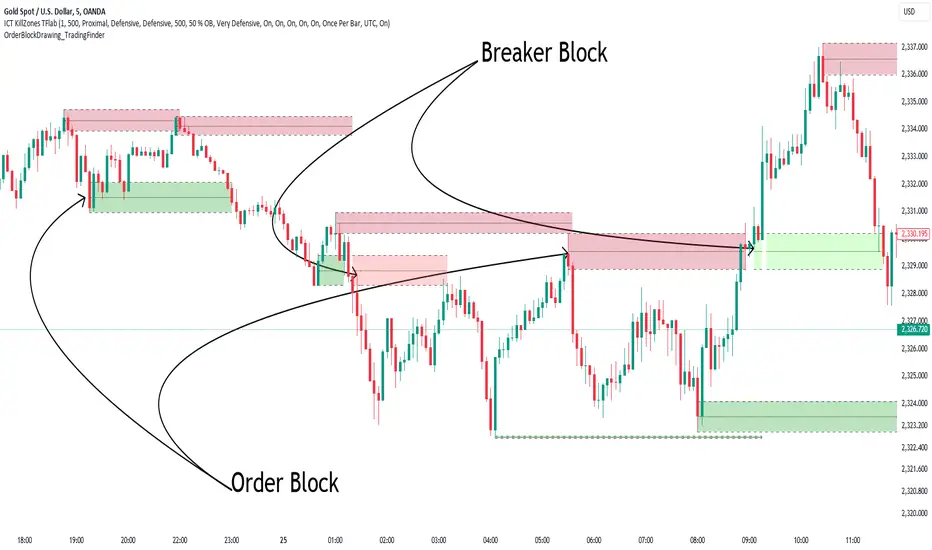

Order Block Drawing [TradingFinder]🔵 Introduction

Perhaps one of the most challenging tasks for Pine script developers (especially beginners) is properly drawing order blocks. While utilizing the latest technical analysis methods for "Price Action," beginners heavily rely on accurately plotting "Supply" and "Demand" zones, following concepts like "Smart Money Concept" and "ICT".

However, drawing "Order Blocks" may pose a challenge for developers. Therefore, to minimize bugs, increase accuracy, and speed up the process of coding order blocks, we have released the "Order Block Drawing" library.

Below, you can read more details about how to use this library.

Important :

This library has direct and indirect outputs. The indirect output includes the ranges of order blocks plotted on the chart. However, the direct output is a "Boolean" value that becomes "true" only when the price touches an order block, colloquially termed as "Mitigate." You can use this output for setting up alerts.

🔵 How to Use

First, you can add the library to your code as shown in the example below.

import TFlab/OrderBlockDrawing_TradingFinder/1

🟣Parameters

OBDrawing(OBType, TriggerCondition, DistalPrice, ProximalPrice, Index, OBValidDis, Show, ColorZone) =>

Parameters:

• OBType (string)

• TriggerCondition (bool)

• DistalPrice (float)

• ProximalPrice (float)

• Index (int)

• OBValidDis (int)

• Show (bool)

• ColorZone (color)

OBType : All order blocks are summarized into two types: "Supply" and "Demand." You should input your order block type in this parameter. Enter "Demand" for drawing demand zones and "Supply" for drawing supply zones.

TriggerCondition : Input the condition under which you want the order block to be drawn in this parameter.

DistalPrice : Generally, if each zone is formed by two lines, the farthest line from the price is termed "Distal." This input receives the price of the "Distal" line.

ProximalPrice : Generally, if each zone is formed by two lines, the nearest line to the price is termed "Proximal" line.

Index : This input receives the value of the "bar_index" at the beginning of the order block. You should store the "bar_index" value at the occurrence of the condition for the order block to be drawn and input it here.

OBValidDis : Order blocks continue to be drawn until a new order block is drawn or the order block is "Mitigate." You can specify how many candles after their initiation order blocks should continue. If you want no limitation, enter the number 4998.

Show : You may need to manage whether to display or hide order blocks. When this input is "On", order blocks are displayed, and when it's "Off", order blocks are not displayed.

ColorZone : You can input your preferred color for drawing order blocks.

🔵 Function Outputs

This function has only one output. This output is of type "Boolean" and becomes "true" only when the price touches an order block. Each order block can be touched only once and then loses its validity. You can use this output for alerts.

= Drawing.OBDrawing('Demand', Condition, Distal, Proximal, Index, 4998, true, Color)

AminioLibraryLibrary "AminioLibrary"

: this is my personal library that is being used in different indicators and strategies

calculateMA(source, len, maType)

This fuction returns a moving average value based on the type

Parameters:

source (float) : Is the time series source to calculate average from

len (simple int) : The length of the moving average, this should be integer

maType (string) : The type of moving average, acceptable types are : SMA, HMA, EMA, RMA, WMA, VWMA

Returns: value of moving average

atr(source, len)

This fuction returns atr value for a given source

Parameters:

source (float) : Is the time series source to calculate atr from

len (simple int) : The length of the atr, this should be integer

Returns: value of atr from source

superTrend(source, factor, len)

This fuction returns value of super trend indicator and the trend direction as a tupple

Parameters:

source (float) : Is the time series source to calculate super trend from

factor (simple float) : The multiplication factor for upper and lower band calcualtion, this can be a float

len (simple int) : The length of the super trend, this should be integer

Returns: value of atr from source

halfTrend(am, chdev)

This fuction returns a hTrend type carrying different values for half trend indicator

Parameters:

am (int) : This is the amplitude used for calcucating the half trend, use integers

chdev (float) : This is the Channel Deviation value used for calculating upper and lower atr channel boundaries, you can use floats

Returns: hTrend data type

hTrend

Fields:

halfTrend (series__float)

trend (series__integer)

atrHigh (series__float)

atrLow (series__float)

arrowUp (series__float)

arrowDown (series__float)

Order Block Refiner [TradingFinder]🔵 Introduction

The "Refinement" feature allows you to adjust the width of the order block according to your strategy. There are two modes, "Aggressive" and "Defensive," in the "Order Block Refine". The difference between "Aggressive" and "Defensive" lies in the width of the order block.

For risk-averse traders, the "Defensive" mode is suitable as it provides a lower loss limit and a greater reward-to-risk ratio. For risk-taking traders, the "Aggressive" mode is more appropriate. These traders prefer to enter trades at higher prices, and this mode, which has a wider order block width, is more suitable for this group of individuals.

Important :

One of the advantages of using this library is increased code accuracy. Not only does it have the capability to create order blocks, but you can also simply define the condition for order block creation (true/false) and "bar_index," and you'll find the primary range without applying any filters.

🟣 Order Block Refinement Algorithm

The order block ranges are filtered in two stages. In the first stage, the "Open," "High," "Low," and "Close" of the current order block candle, its two or three previous candles, and one subsequent candle (if available) are examined. In this stage, minimum and maximum distances are calculated, and logical range filters are applied.

In the second stage, two modes, "Aggressive" and "Defensive," are calculated.

For the "Defensive" mode, the width of these ranges is compared with the "ATR" (Average True Range) of period 55, and if they are smaller than "ATR" or 1 to more than 4 times "ATR," the width of the range is reduced from 0 to 80 percent.

For the "Aggressive" mode, you get the same output as the first filter, which usually has a wider width than the "Defensive" mode.

• Order Block Refiner : Off

• Order Block Refiner : On / "Aggressive Mode"

• Order Block Refiner : On / "Defensive Mode"

🔵 How to Use

OBRefiner(string OBType, string OBRefine, string RefineMethod, bool TriggerCondition, int Index) =>

Parameters:

• OBType (string)

• OBRefine (string)

• RefineMethod (string)

• TriggerCondition (bool)

• Index (int)

To add "Order Block Refiner Library", you must first add the following code to your script.

import TFlab/OrderBlockRefiner_TradingFinder/1

OBType : This parameter receives 2 inputs. If the order block you want to "Refine" is of type demand, you should enter "Demand," and if it's of type supply, you should enter "Supply."

OBRefine : Set to "On" if you want the "Refine" operation to be performed. Otherwise, set to "Off."

RefineMethod : This input receives 2 modes, "Aggressive" and "Defensive." You can switch between these modes according to your needs.

TriggerCondition : Enter the condition with which the order block is formed in this parameter.

Index : Enter the "bar_index" of the candle where the order block is formed in this parameter.

🟣 Function Outputs

This function has 6 outputs: "bar_index" at the beginning of the "Distal" line, "bar_index+1" at the end of the "Distal" line, "Price" at the "Distal" line, "bar_index" at the beginning of the "Proximal" line, "bar_index+1" at the end of the "Proximal" line, and "Price" at the "Proximal" line, which can be used to draw order blocks.

Sample :

= Refiner.OBRefiner('Demand', 'Off', 'Aggressive',BuMChMain_Trigger, BuMChMain_Index)

if BuMChMain_Trigger

BuMChHlineMain := line.new(BuMChMain_Xp1 , BuMChMain_Yp12 , bar_index , BuMChMain_Yp12, color = color.black , style = line.style_dotted)

BuMChLlineMain := line.new(BuMChMain_Xd1 , BuMChMain_Yd12 , bar_index , BuMChMain_Yd12, color = color.black , style = line.style_dotted)

BuMChFilineMain := linefill.new(BuMChHlineMain ,BuMChLlineMain , color = color.rgb(76, 175, 80 , 75 ) )

divergingchartpatternLibrary "divergingchartpattern"

Library having implementation of converging chart patterns

getPatternNameByType(patternType)

Returns pattern name based on type

Parameters:

patternType (int) : integer value representing pattern type

Returns: string name of the pattern

method find(this, sProperties, dProperties, patterns, ohlcArray)

find converging patterns for given zigzag

Namespace types: zg.Zigzag

Parameters:

this (Zigzag type from Trendoscope/ZigzagLite/2) : Current zigzag Object

sProperties (ScanProperties) : ScanProperties Object

dProperties (DrawingProperties type from Trendoscope/abstractchartpatterns/5) : DrawingProperties Object

patterns (array type from Trendoscope/abstractchartpatterns/5) : array of existing patterns to check for duplicates

ohlcArray (array type from Trendoscope/ohlc/1) : array of OHLC values for historical reference

Returns: string name of the pattern

ScanProperties

Object containing properties for pattern scanning

Fields:

baseProperties (ScanProperties type from Trendoscope/abstractchartpatterns/5) : Object of Base Scan Properties

convergingDistanceMultiplier (series float)

swinglibraryLibrary "swinglibrary"

This library is for calculating non-repainting swings for further calculation on them.

These swings can later be drawn, but drawing is not part of this library, only the calculation.

What do I need to use the library?

You better include the following constants into your script using this library:

int SWING_NO_ACTION = 0

int SWING_FLIP = 1

int SWING_FLIP_NEW_SWING = 2

int SWING_FLIP_UPDATED = 3

int RELATION_HIGHER = 1

int RELATION_EQUAL = 0

int RELATION_LOWER = -1

Choosing the function, that fits your needs

This library contains 4 functions for calculating swings, the difference between them are the data you get for every swing point and additional average values for length and duration:

swings()

swingsR()

swingsL()

swingsLDR()

The naming scheme of these functions is the following:

The base version swings() is only for the swings containing the following swingPoint type:

swingPoint

Fields:

x (integer) : bar index

y (float) : price

hilo (integer) 1 -> high, -1 -> low

and the return type:

swingReturn

Fields:

swings (array) : array of the last x swing points

newSwingHigh (integer) : flag to detect changes for swing highs see constants (SWING_NO_ACTION, SWING_FLIP_NEW_SWING, SWING_FLIP_UPDATED)

newSwingLow (integer) : flag to detect changes for swing lows see constants (SWING_NO_ACTION, SWING_FLIP_NEW_SWING, SWING_FLIP_UPDATED)

The R in swingsR() stands for relation where the previously shown types do also contain the relation between the swings of the same swing type (highs and lows respectively).

The same goes for L in swingsL() for length containing the price difference between the current and previous swing point in ticks.

And in the following version swingsLDR() there is also the duration between the current and previous point included.

The parameters for the other functions and type definitions include only the ones, that are needed, the "full" version of the function is described here:

swingsLDR(swingSize, dtbStrength, init, SWING_HISTORY_NUM)

Parameters:

swingSize (int) This parameter defines the size of the swings to look after, meaning higher values will lead to bigger swings

dtbStrength (int) Value between 0 and 100 is a factor (%) to the ATR that is used to calculate equal highs/lows (double tops / bottoms).

Higher values will result in a higher tolerance of price difference between the swings.

init (bool) This value is usually set to false on default.

It has a special use case, where we need to reduce memory usage and calculation time on the script using this library by start calculating at x bars back instead of the beginning of the chart.

In this case, we set init = true on the first bar we start calculating the swings on to perform the correct initialization.

SWING_HISTORY_NUM (int) This is the max number of swings that are stored in the array, so only the last SWING_HISTORY_NUM swings are stored in the array to reduce the memory usage.

New ones remove the oldest ones like in a ring buffer.

This is also influencing the average duration and average swing length.

swingPointLDR

Fields:

x (integer) : bar index

y (float) : price

hilo (integer) : 1 -> high, -1 -> low

length (float) : price difference to the previous swing point in ticks

duration (integer) : duration difference to the previous swing point in number of bars