Strong Potential Asset Strategy (EMA + EMA)During experiments with the market, I found out that simple strategy is the best solution. However, I decided to bring some of my ideas on the 2 MA strategy.

- Instead of SMA - there will be 2 EMA, so the strategy will be more sensitive to the latest data;

- There is an option, which regulates the difference between those 2 EMAs, this should protect us from false trend enter;

- There is an option "Exit tolerance", which regulates how much could be the difference between 2 EMAs after crossover. This supposed to protect us from the false trend exit.

Hope this will be helpful :)

Strategy

Ehlers Fisher Stochastic Relative Vigor Index StrategyBy John Ehlers from his book "Cybernetic Analysis for Stocks and Futures".

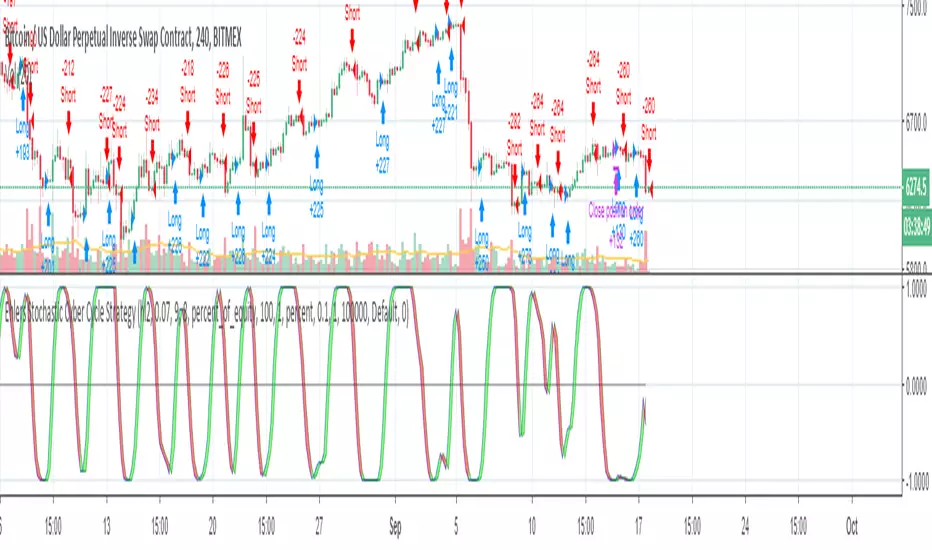

Ehlers Stochastic Cyber Cycle StrategyBy John Ehlers from his book "Cybernetic Analysis for Stocks and Futures".

Momentum Strategy, rev.2This is a revised version of the Momentum strategy listed in the built-ins.

For more information check out this resource:

www.forexstrategiesresources.com

Ehlers Cyber Cycle StrategyEhlers Cyber Cycle Strategy by John Ehlers from his book "Cybernetic Analysis for Stocks and Futures".

Ehlers Instantaneous Trendline StrategyInstantaneous Trendline Strategy by John Ehlers from his book "Cybernetic Analysis for Stocks and Futures".

You can choose implementation of stop-loss. Don't forget to define correct spread for your instrument.

dP magnet//Strategy based on the idea that stop loss and take profit are often placed at full price levels or round numbers, whcih acts as resistance and supports levels

//Buy Rules:

//Actual price (close) is above round number.

//Round number level was not touched in previous ten bars (arbitrary value).

//Place a buy and follow the order with a trail step because price can bounce at round number (support) or can go through it.

//Sell Rules are the same of buy rules but inverted.

//

//Need improvement on conditions' logic and round numbers definitions

Strategy Backtester TemplateA template for building a strategy tester:

- date range selector

- stop loss

- take profit

- long and short strategy type selector

MTF stochastic strategyThis strategy is based on MTF strategy found on Forex Factory forum and published by bobby2 (credits to him).

This is quite simple but need improvement to work properly:

1- it is made for 5 min chart

2- when 15min stochastic cross above 50 and 5min stochastic is rising, buy

3- when 15min stochastic cross below 50 and 5min stochastic is falling, sell

Gidra's RSI or MFI Strategy v 0.1Strategy based on Gregg_s indicator RSI or MFI (ru.tradingview.com)

When crossing above 0 - close short, open long

When crossing below 1 - close long, open short

For crypto/fiat and any timeframe

Gidra's Vchain Strategy v0.1Tested on "BTC/USD", this is a reversible strategy

If the RSI is lower than "RSI Limit" (for last "RSI Signals" candles) and there were "Open Color, Bars" green Heiken Ashi candles - close short, open long

If the RSI is higher than 100-"RSI Limit" (for last "RSI Signals" candles) and there were "Open Color, Bars" red Heiken Ashi candles - close long, open short

- timeframe: 5m (the best)

RSI Period = 14

RSI Limit = 30

RSI Signals = 3

Open Color = 2

Piramiding = 100

Lot = 100 %

- timeframe: 1h

RSI Period = 2

RSI Limit = 30

RSI Signals = 3

Open Color = 2

Piramiding = 100

Lot = 100 %

Ehlers-Smoothed Stochastic RSI StrategyI have been asked by several people for a Strategy based on the ES Stoch RSI Alert so here it is. The strategy has an adjustable backtest date range so that you can adjust the test time period to whatever you like. This strategy is based on a script by fskrypt.

BB limitMarket maker strategy using Bollinger bands as entry, moving average as close and simple stop-loss with percentage of entry position. It was extremely profitable in june on xbtusd.

Script functionality test - work in progress (2RS + BB + MA)This is the first script I've written. Its sole purpose is to make me learn a bit of pine script. Its not intended to trade live.

Feel free to modify it if you wish and let me know if you do it. Also any comments are welcome!

Also i need help in two things:

1. Im unable to print the "in-strategy" rsi on chart

2. I want to ignore the first buy signal after each sell. I was looking to ad a counter to the signals but im unable to do it.

Any help will be greatly appreciated!

Dynamic Momentum Index (DMI) Backtest This indicator plots Dynamic Momentum Index indicator. The Dynamic Momentum

Index (DMI) was developed by Tushar Chande and Stanley Kroll. The indicator

is covered in detail in their book The New Technical Trader.

The DMI is identical to Welles Wilder`s Relative Strength Index except the

number of periods is variable rather than fixed. The variability of the time

periods used in the DMI is controlled by the recent volatility of prices.

The more volatile the prices, the more sensitive the DMI is to price changes.

In other words, the DMI will use more time periods during quiet markets, and

less during active markets. The maximum time periods the DMI can reach is 30

and the minimum is 3. This calculation method is similar to the Variable

Moving Average, also developed by Tushar Chande.

The advantage of using a variable length time period when calculating the RSI

is that it overcomes the negative effects of smoothing, which often obscure short-term moves.

The volatility index used in controlling the time periods in the DMI is based

on a calculation using a five period standard deviation and a ten period average

of the standard deviation.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Linda Raschke's Holy GrailAnother script based on Linda Raschke's strategy with the same name from her book about swing trading.

Stupid strategyStrategy with simple stop-loss and take-profit in percentage. If last trade was a successful one then repeat it. If not successful - do a reversal trade.

MACD+EMA crossovers Strategy customIt is a Strategy to use EMA crossover and MACD to decide when "buy" and when "sell", the key is spend some time "tuning" the parameters and using the simulation tool to find the best parameters for EMA and MACD there are 6 parameters, but with Excel and patience you could find the best configuration for the past and apply it to the future and see.

Simple profitable trading strategyThis strategy has three components.

Philakones EMAs are a sequence of five fibonacci EMAs. They range from 55 candles (green) to 8 candles (red) in length. A strong trend or breakout is marked by the emas appearing in sequence of their length from 8 to 55 or vice versa. These EMAs are also used to signal an exit. Only two EMAs are used for exit signals - when the 13 EMA crosses over/under the 55 EMA.

RSI gives a bullish signal when 40 > rsi > 70. Exit signals are oversold (30) or overbought (70)

Stochastics give a bullish signal when stoch < 80 and an exit signal when > 95.

Results include 3 ticks of slippage and taker fees of .002. Provides a pretty smooth equity curve with a 73% win rate and beats buy and hold by than 10x (returns about 60x overall) since start of 2017.

MACD Strategy custom for cryptosIt is a MACD with strategy simulation implemented to "tune" the MACD parameters for cryptos, it only use long and close strategy, not short

Try to go long at a moving averageA simple experimental strategy that tries to go long at a moving average bounce / support level, and looks for upside.

Average Directional Movement Index Rating Backtest The Average Directional Movement Index Rating (ADXR) measures the strength

of the Average Directional Movement Index (ADX). It's calculated by taking

the average of the current ADX and the ADX from one time period before

(time periods can vary, but the most typical period used is 14 days).

Like the ADX, the ADXR ranges from values of 0 to 100 and reflects strengthening

and weakening trends. However, because it represents an average of ADX, values

don't fluctuate as dramatically and some analysts believe the indicator helps

better display trends in volatile markets.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.