Hilega Milega v6 - Pure EMA/SMA (Nitesh Kumar) + Full BacktestHilega to milega

he Hilega Milega Strategy, inspired by the technique of Nitesh Kumar, is designed for intraday and swing traders who want structured entries and exits with clear demand–supply logic.

🔑 Core Features

Demand & Supply Zones – Automatically plots potential strong buying and selling zones for high-probability trades.

Trend Identification – Uses a blend of EMAs/SMA crossovers to identify bullish and bearish market bias.

Buy & Sell Signals – Generates real-time visual signals based on “Hilega Milega” rules for quick decision-making.

Risk Management – Suggested stop-loss levels are derived from recent demand–supply areas to minimize drawdowns.

Backtesting Enabled – Traders can test the performance across multiple assets (stocks, forex, crypto, commodities).

📊 How It Works

Buy Signal → When price action confirms a bullish zone with supporting trend filters.

Sell Signal → When price action confirms a bearish zone or reversal pattern.

Flat/Exit → Position closed when opposite signal triggers or demand–supply imbalance fades.

⚡ Best Use Cases

Intraday trading (5m, 15m, 1H charts).

Swing trading (4H, Daily charts).

Works across stocks, crypto, commodities, and forex.

⚠️ Disclaimer: This strategy is for educational purposes. Backtest thoroughly and apply proper risk management before live trading.

Oscillators

Hazel nut BB Strategy, volume base- lite versionHazel nut BB Strategy, volume base — lite version

Having knowledge and information in financial markets is only useful when a trader operates with a well-defined trading strategy. Trading strategies assist in capital management, profit-taking, and reducing potential losses.

This strategy is built upon the core principle of supply and demand dynamics. Alongside this foundation, one of the widely used technical tools — the Bollinger Bands — is employed to structure a framework for profit management and risk control.

In this strategy, the interaction of these tools is explained in detail. A key point to note is that for calculating buy and sell volumes, a lower timeframe function is used. When applied with a tick-level resolution, this provides the most precise measurement of buyer/seller flows. However, this comes with a limitation of reduced historical depth. Users should be aware of this trade-off: if precise tick-level data is required, shorter timeframes should be considered to extend historical coverage .

The strategy offers multiple configuration options. Nevertheless, it should be treated strictly as a supportive tool rather than a standalone trading system. Decisions must integrate personal analysis and other instruments. For example, in highly volatile assets with narrow ranges, it is recommended to adjust profit-taking and stop-loss percentages to smaller values.

◉ Volume Settings

• Buyer and seller volume (up/down volume) are requested from a lower timeframe, with an option to override the automatic resolution.

• A global lookback period is applied to calculate moving averages and cumulative sums of buy/sell/delta volumes.

• Ratios of buyers/sellers to total volume are derived both on the current bar and across the lookback window.

◉ Bollinger Band

• Bands are computed using configurable moving averages (SMA, EMA, RMA, WMA, VWMA).

• Inputs allow control of length, standard deviation multiplier, and offset.

• The basis, upper, and lower bands are plotted, with a shaded background between them.

◉ Progress & Proximity

• Relative position of the price to the Bollinger basis is expressed as percentages (qPlus/qMinus).

• “Near band” conditions are triggered when price progress toward the upper or lower band exceeds a user-defined threshold (%).

• A signed score (sScore) represents how far the close has moved above or below the basis relative to band width.

◉ Info Table

• Optional compact table summarizing:

• - Upper/lower band margins

• - Buyer/seller volumes with moving averages

• - Delta and cumulative delta

• - Buyer/seller ratios per bar and across the window

• - Money flow values (buy/sell/delta × price) for bar-level and summed periods

• The table is neutral-colored and resizable for different chart layouts.

◉ Zone Event Gate

• Tracks entry into and exit from “near band” zones.

• Arming logic: a side is armed when price enters a band proximity zone.

• Trigger logic: on exit, a trade event is generated if cumulative buyer or seller volume dominates over a configurable window.

◉ Trading Logic

• Orders are placed only on zone-exit events, conditional on volume dominance.

• Position sizing is defined as a fixed percentage of strategy equity.

• Long entries occur when leaving the lower zone with buyer dominance; short entries occur when leaving the upper zone with seller dominance.

◉ Exit Rules

• Open positions are managed by a strict priority sequence:

• 1. Stop-loss (% of entry price)

• 2. Take-profit (% of entry price)

• 3. Opposite-side event (zone exit with dominance in the other direction)

• Stop-loss and take-profit levels are configurable

◉ Notes

• This lite version is intended to demonstrate the interaction of Bollinger Bands and volume-based dominance logic.

• It provides a framework to observe how price reacts at band boundaries under varying buy/sell pressure, and how zone exits can be systematically converted into entry/exit signals.

When configuring this strategy, it is essential to carefully review the settings within the Strategy Tester. Ensure that the chosen parameters and historical data options are correctly aligned with the intended use. Accurate back testing depends on applying proper configurations for historical reference. The figure below illustrates sample result and configuration type.

Liquidation Strategy📈 It enters a long trade when long liquidation spikes above a set threshold.

📉 It enters a short trade when short liquidation drops below the negative threshold.

🧮 It optionally filters entries using an EMA multiplier.

🔁 It exits long when RSI crosses below its smoothed version.

🔄 It exits short when RSI crosses above its smoothed version.

🔗 It requires linking to the Liquidations indicator on Bybit or OKX charts.

DNSE VN301!, ADX Momentum StrategyDiscover the tailored Pine Script for trading VN30F1M Futures Contracts intraday.

This strategy applies the Statistical Method (IQR) to break down the components of the ADX, calculating the threshold of "normal" momentum fluctuations in price to identify potential breakouts for entry and exit signals. The script automatically closes all positions by 14:30 to avoid overnight holdings.

www.tradingview.com

Settings & Backtest Results:

- Chart: 30-minute timeframe

- Initial capital: VND 100 million

- Position size: 4 contracts per trade (includes trading fees, excludes tax)

- Backtest period: Sep-2021 to Sep-2025

- Return: over 270% (with 5 ticks slippage)

- Trades executed: 1,000+

- Win rate: ~40%

- Profit factor: 1.2

Default Script Settings:

Calculates the acceleration of changes in the +DI and -DI components of the ADX, using IQR to define "normal" momentum fluctuations (adjustable via Lookback period).

Calculates the difference between each bar’s Open and Close prices, using IQR to define "normal" gaps (adjustable via Lookback period).

Entry & Exit Conditions:

Entry Long: Change in +DI or -DI > Avg IQR Value AND Close Price > Previous Close

Exit Long: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI < Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price < Previous Close

Entry Short: Change in +DI or -DI > Avg IQR Value AND Close Price < Previous Close

Exit Short: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI > Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price > Previous Close

Disclaimers:

Trading futures contracts carries a high degree of risk, and price movements can be highly volatile. This script is intended as a reference tool only. It should be used by individuals who fully understand futures trading, have assessed their own risk tolerance, and are knowledgeable about the strategy’s logic.

All investment decisions are the sole responsibility of the user. DNSE bears no liability for any potential losses incurred from applying this strategy in real trading. Past performance does not guarantee future results. Please contact us directly if you have specific questions about this script.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

Daily CMO + Volume Intraday Strategy v6 by Subirrmomentum strategy. buy on next hourly candle after signal. target 5%, sl 1%

Supertrend [TradingConToto]Supertrend — ADX/DI + EMA Gap + Breakout (with Mobile UI)

What makes it original

Supertrend combines trend strength (ADX/DI), multi-timeframe bias (EMA63 and EMA 200D equivalent), a structural filter based on the distance between EMA2400 and EMA4800 expressed in ATR units, and a momentum confirmation through a previous high breakout.

This is not a random mashup — it’s a sequence of filters designed to reduce trades in ranging markets and prioritize mature trends:

Direction: +DI > -DI (trend led by buyers).

Strength: ADX > mean(ADX) (avoids weak, choppy phases).

Short-term bias: Close > EMA63.

Long-term bias: Close > EMA4800 ≈ EMA200 daily on H1.

Momentum: Close > High (immediate breakout).

Structure: (EMA2400 − EMA4800) > k·ATR (ensures separation in ATR units, filters out flat phases).

Entries & exits

Entry: when all six conditions are met and no open position exists.

Exit: if +DI < -DI or Close < EMA63.

Visuals: EMA63 is painted green while in position and red otherwise, with a supertrend-style band; “BUY” labels appear below the green band and “SELL” labels above the red band.

UI: includes a compact table (mobile-friendly) showing the state of each condition.

Default parameters used in this publication

Initial capital: 10,000

Position size: 10% of equity (≤10% per trade is considered sustainable).

Commission: 0.01% per side (adjust to your broker/market).

Slippage: 1 tick

Pyramiding: 0 (only one position at a time)

Adjust commission/slippage to match your market. For US equities, commissions are often per share; for spot crypto, 0.10–0.20% total is common. I publish with 0.01% per side as a conservative example to avoid overestimating results.

Recommended backtest dataset

Timeframe: H1

Multi-cycle window (e.g. 2015–today)

Symbols with high liquidity (e.g. NASDAQ-100 large caps, or BTC/ETH spot) to generate 100+ trades. Avoid cherry-picked short windows.

Why each filter matters

+DI > -DI + ADX > mean: reduce counter-trend trades and weak signals.

Close > EMA63 + Close > EMA4800: enforce trend alignment in short and long horizons.

Breakout High : requires immediate momentum, avoids early entries.

EMA gap in ATR units: blocks flat or compressed structures where EMA200D aligns with price.

Limitations

The breakout filter may skip healthy pullbacks; the design prioritizes continuation over perfect entry price.

No fixed trailing stop/TP; exits depend on trend degradation via DI/EMA63.

Results vary with real costs (commissions, slippage, funding). Adjust defaults to your broker.

How to use

Apply it on a clean chart (no other indicators when publishing).

Keep in mind the default parameters above; if you change them, mention it in your notes and use the same values in the Strategy Tester.

Ensure your dataset produces 100+ trades for statistical validity.

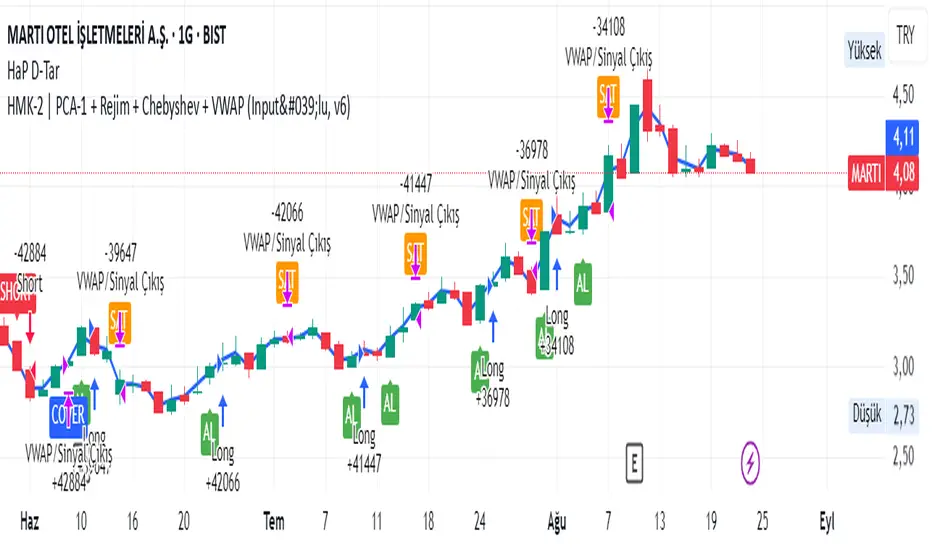

HMK-2 | PCA-1 + Rejim + Chebyshev + VWAP (Input'lu, v6)📌 HMK-2 | PCA-1 + Regime + Chebyshev + VWAP Strategy

1️⃣ Core Structure

Instead of relying on a single indicator, this system uses the Z-Score normalized average of three oscillators (RSI, MFI, ROC).

Signal (PCA-1):

RSI(14), MFI(14), ROC(5) → each is converted into a z-score.

Their average becomes the “composite signal,” our PCA-1 value.

Trend direction: If the Z-score EMA is rising → trend UP. If falling → trend DOWN.

2️⃣ Side Filters

Regime Filter (ADX + EMA)

ADX is calculated manually.

If ADX > 20 → trend exists → a 50-period EMA of this value smooths it.

This turns “trend regime” into a probability between 0–1.

Chebyshev Filter

A return series is checked against mean ± k*sigma bands.

If the return is within this band → valid signal. Extreme moves are filtered out.

VWAP Filter

Long trades: price must be above VWAP.

Short trades: price must be below VWAP.

Trades are only taken on the correct side of institutional cost averages.

3️⃣ Entry Conditions

Long:

PCA-1 signal crosses above threshold.

Trend Up + Regime OK + Chebyshev OK + Above VWAP.

Short:

PCA-1 signal crosses below threshold.

Trend Down + Regime OK + Chebyshev OK + Below VWAP.

4️⃣ Exit Mechanism

Main Exit: ATR-based stop/target.

Stop = entry price – ATR × (SL factor).

Take profit = entry price + ATR × (TP factor).

Additional Exit:

If price crosses to the opposite side of VWAP.

If PCA-1 signal crosses zero.

👉 Prevents trades from being locked, makes exits adaptive.

5️⃣ Labels / Visualization

AL / SHORT → entry points.

SAT / COVER → exit points.

VWAP line plotted in blue.

🧩 Strategy Features

Optimizable parameters:

Z-window (zWin)

Threshold

Chebyshev factor

ATR stop/target multipliers

This system works with:

Disciplined core (PCA-1 signal)

Triple protection (Regime + Chebyshev + VWAP)

Adaptive exits (ATR + VWAP/signal cross)

👉 Not a “single-indicator robot,” but a multi-filtered trade direction engine.

💡 Final Note

This is a base model of the system — open for further development.

I’ve shared the logic to give you a roadmap.

If you spot errors, fix them → that’s how you’ll improve it.

Don’t waste time asking me questions — refine and build it better yourselves.

Wishing you profitable trades. Stay well 🙏

PowerTrend Pro Strategy – Gold OptimizedTired of false signals on Gold?

PowerTrend Pro combines VWAP, Supertrend, RSI, and smart MA filters with trailing stops & break-even logic to deliver high-probability trades on XAUUSD.

PowerTrend Pro Strategy is a professional-grade trading system designed to capture high-probability swing and intraday opportunities on XAUUSD (Gold) and other volatile markets.

🔑 Core Features

VWAP Anchoring – institutional fair value reference to filter trades.

Supertrend (ATR-based) – adaptive trend filter tuned for Gold’s volatility.

Multi-Timeframe RSI – confirms momentum alignment across intraday and higher timeframe.

EMA + SMA Combo – ensures trades follow strong directional bias, reducing false signals.

Dynamic Risk Management

Adjustable Take Profit / Stop Loss (%)

Trailing Stop that locks in profits on extended moves

Break-Even Logic (stop loss moves to entry once price is in profit)

⚡ Gold-Tuned Presets

XAUUSD 1H → tighter TP/SL & faster entries for active intraday trading.

XAUUSD 4H → wider ATR filter & trailing stops to capture bigger swings.

Generic Mode → works on Forex, Indices, and Crypto (fully customizable).

🎯 Why It Works

Gold is notoriously volatile — quick spikes wipe out weak strategies. PowerTrend Pro solves this by combining:

✅ Institutional bias (VWAP)

✅ Adaptive trend filter (Supertrend)

✅ Momentum confirmation (RSI MTF)

✅ Robust trend structure (EMA + SMA)

✅ Smart exits (TP, SL, trailing & breakeven)

This multi-layer confirmation makes entries stronger and keeps risk under control.

🛠️ Usage

Add the strategy to your chart.

Choose a preset (XAUUSD 1H, 4H, or Generic).

Run Strategy Tester for performance metrics.

Optimize TP/SL and ATR values for your broker & market conditions.

🔥 Pro Tip: Combine this strategy with a session filter (London/NY overlap) or volume confirmation to boost accuracy in Gold.

Adaptive MVRV & RSI Strategy V6 (Dynamic Thresholds)Strategy Explanation

This is an advanced Dollar-Cost Averaging (DCA) strategy for Bitcoin that aims to adapt to long-term market cycles and changing volatility. Instead of relying on fixed buy/sell signals, it uses a dynamic, weighted approach based on a combination of on-chain data and classic momentum.

Core Components:

Dual-Indicator Signal: The strategy combines two powerful indicators for a more robust signal:

MVRV Ratio: An on-chain metric to identify when Bitcoin is fundamentally over or undervalued relative to its historical cost basis.

Weekly RSI: A classic momentum indicator to gauge long-term market strength and identify overbought/oversold conditions.

Dynamic, Self-Adjusting Thresholds: The core innovation of this strategy is that it avoids fixed thresholds (e.g., "sell when RSI is 70"). Instead, the buy and sell zones are dynamically calculated based on a long-term (2-year) moving average and standard deviation of each indicator. This allows the strategy to automatically adapt to Bitcoin's decreasing volatility and changing market structure over time.

Weighted DCA (Scaling In & Out): The strategy doesn't just buy or sell a fixed amount. The size of its trades is scaled based on conviction:

Buying: As the MVRV and RSI fall deeper into their "undervalued" zones, the percentage of available cash used for each purchase increases.

Selling: As the indicators rise further into "overvalued" territory, the percentage of the current position sold also increases.

This creates an adaptive system that systematically accumulates during periods of fear and distributes during periods of euphoria, with the intensity of its actions directly tied to the extremity of market conditions.

Institution Accumulation/DistributionLeveraging the Williams%R oscillator, the script has been optimized to pick out key turning point in the market specifically at Resistance (Overbought) or Support (Oversold)

The algo has been programmed to print both buy and sell alerts at extremes/when conditions flip eg a long position will be closed simultaneously opening a short position above resistance.

Best used as a scalping tool targeting 30m and below works well with currency pairs

Nifty Power -> Nifty 50 chart + EMA of RSI + avg volume strategyThis strategy works in 1 hour candle in Nifty 50 chart. In this strategy, upward trade takes place when there is a crossover of RSI 15 on EMA50 of RSI 15 and volume is greater than volume based EMA21. On the other hand, lower trade takes place when RSI 15 is less than EMA50 of RSI 15. Please note that there is no stop loss given and also that the trade will reverse as per the trend. Sometimes on somedays, there will be no trades. Also please note that this is an Intraday strategy. The trade if taken closes on 15:15 in Nifty 50. This strategy can be used for swing trading. Some pine script code such as supertrend and ema21 of close is redundant. Try not to get confused as only EMA50 of RSI 15 is used and EMA21 of volume is used. I am using built-in pinescript indicators and there is no special calculation done in the pine script code. I have taken numbars variable to count number of candles. For example, if you have 30 minuite chart then numbars variable will count the intraday candles accordingly and the same for 1 hour candles.

RSI + MACD Long-Only StrategyRSI + MACD Long-Only Strategy

Overview: Momentum-based, long-only strategy combining RSI and MACD. Entries favor upside momentum; exits trigger on momentum fades or risk targets. Signals are state-gated so you get one exit per entry (no multiple exits without a prior entry).

Entry conditions:

RSI crosses above the midline (default 50) while MACD is bullish (MACD > Signal, optionally MACD > 0), OR

MACD crosses above its Signal while RSI is at/above the midline.

Optional filters:

EMA trend filter: only enter if price > EMA(n).

Oversold context: only enter within N bars after RSI dipped below the oversold threshold.

Exit conditions:

RSI crosses below the midline, OR

MACD crosses below its Signal with MACD histogram ≤ 0.

Optional risk exit: Take Profit / Stop Loss based on percentage from average entry price.

Risk management:

Inputs: Use TP/SL (on/off), TP% (default 3.0), SL% (default 1.5).

Implements protective strategy.exit (limit/stop) while in position.

Signal-based exit uses strategy.close to flatten.

Position management:

Long-only, no pyramiding (single position at a time).

Internal state ensures entries occur only when flat and exits only when in a position.

Inputs you can tune:

RSI: length, overbought, oversold, midline.

MACD: fast length, slow length, signal length; toggle “Require MACD > 0”.

Signals: oversold lookback window; EMA trend on/off and EMA length.

Risk: TP% and SL%.

Visuals: show entry/exit markers, bar coloring; optional debug background on raw triggers.

Visuals and alerts:

Plots EMA (optional), draws entry/exit markers, optional bar coloring, and a faint background on raw long triggers to aid tuning.

Alert conditions provided for entries and exits.

Notes:

Designed for bar-close evaluation; performance varies by symbol/timeframe—tune inputs accordingly.

Long-only; intended for trend-following momentum with basic risk control.

Not financial advice.

Mutanabby_AI | Algo Pro Strategy# Mutanabby_AI | Algo Pro Strategy: Advanced Candlestick Pattern Trading System

## Strategy Overview

The Mutanabby_AI Algo Pro Strategy represents a systematic approach to automated trading based on advanced candlestick pattern recognition and multi-layered technical filtering. This strategy transforms traditional engulfing pattern analysis into a comprehensive trading system with sophisticated risk management and flexible position sizing capabilities.

The strategy operates on a long-only basis, entering positions when bullish engulfing patterns meet specific technical criteria and exiting when bearish engulfing patterns indicate potential trend reversals. The system incorporates multiple confirmation layers to enhance signal reliability while providing comprehensive customization options for different trading approaches and risk management preferences.

## Core Algorithm Architecture

The strategy foundation relies on bullish and bearish engulfing candlestick pattern recognition enhanced through technical analysis filtering mechanisms. Entry signals require simultaneous satisfaction of four distinct criteria: confirmed bullish engulfing pattern formation, candle stability analysis indicating decisive price action, RSI momentum confirmation below specified thresholds, and price decline verification over adjustable lookback periods.

The candle stability index measures the ratio between candlestick body size and total range including wicks, ensuring only well-formed patterns with clear directional conviction generate trading signals. This filtering mechanism eliminates indecisive market conditions where pattern reliability diminishes significantly.

RSI integration provides momentum confirmation by requiring oversold conditions before entry signal generation, ensuring alignment between pattern formation and underlying momentum characteristics. The RSI threshold remains fully adjustable to accommodate different market conditions and volatility environments.

Price decline verification examines whether current prices have decreased over a specified period, confirming that bullish engulfing patterns occur after meaningful downward movement rather than during sideways consolidation phases. This requirement enhances the probability of successful reversal pattern completion.

## Advanced Position Management System

The strategy incorporates dual position sizing methodologies to accommodate different account sizes and risk management approaches. Percentage-based position sizing calculates trade quantities as equity percentages, enabling consistent risk exposure across varying account balances and market conditions. This approach proves particularly valuable for systematic trading approaches and portfolio management applications.

Fixed quantity sizing provides precise control over trade sizes independent of account equity fluctuations, offering predictable position management for specific trading strategies or when implementing precise risk allocation models. The system enables seamless switching between sizing methods through simple configuration adjustments.

Position quantity calculations integrate seamlessly with TradingView's strategy testing framework, ensuring accurate backtesting results and realistic performance evaluation across different market conditions and time periods. The implementation maintains consistency between historical testing and live trading applications.

## Comprehensive Risk Management Framework

The strategy features dual stop loss methodologies addressing different risk management philosophies and market analysis approaches. Entry price-based stop losses calculate stop levels as fixed percentages below entry prices, providing predictable risk exposure and consistent risk-reward ratio maintenance across all trades.

The percentage-based stop loss system enables precise risk control by limiting maximum loss per trade to predetermined levels regardless of market volatility or entry timing. This approach proves essential for systematic trading strategies requiring consistent risk parameters and capital preservation during adverse market conditions.

Lowest low-based stop losses identify recent price support levels by analyzing minimum prices over adjustable lookback periods, placing stops below these technical levels with additional buffer percentages. This methodology aligns stop placement with market structure rather than arbitrary percentage calculations, potentially improving stop loss effectiveness during normal market fluctuations.

The lookback period adjustment enables optimization for different timeframes and market characteristics, with shorter periods providing tighter stops for active trading and longer periods offering broader stops suitable for position trading approaches. Buffer percentage additions ensure stops remain below obvious support levels where other market participants might place similar orders.

## Visual Customization and Interface Design

The strategy provides comprehensive visual customization through eight predefined color schemes designed for different chart backgrounds and personal preferences. Color scheme options include Classic bright green and red combinations, Ocean themes featuring blue and orange contrasts, Sunset combinations using gold and crimson, and Neon schemes providing high visibility through bright color selections.

Professional color schemes such as Forest, Royal, and Fire themes offer sophisticated alternatives suitable for business presentations and professional trading environments. The Custom color scheme enables precise color selection through individual color picker controls, maintaining maximum flexibility for specific visual requirements.

Label styling options accommodate different chart analysis preferences through text bubble, triangle, and arrow display formats. Size adjustments range from tiny through huge settings, ensuring appropriate visual scaling across different screen resolutions and chart configurations. Text color customization maintains readability across various chart themes and background selections.

## Signal Quality Enhancement Features

The strategy incorporates signal filtering mechanisms designed to eliminate repetitive signal generation during choppy market conditions. The disable repeating signals option prevents consecutive identical signals until opposing conditions occur, reducing overtrading during consolidation phases and improving overall signal quality.

Signal confirmation requirements ensure all technical criteria align before trade execution, reducing false signal occurrence while maintaining reasonable trading frequency for active strategies. The multi-layered approach balances signal quality against opportunity frequency through adjustable parameter optimization.

Entry and exit visualization provides clear trade identification through customizable labels positioned at relevant price levels. Stop loss visualization displays active risk levels through colored line plots, ensuring complete transparency regarding current risk management parameters during live trading operations.

## Implementation Guidelines and Optimization

The strategy performs effectively across multiple timeframes with optimal results typically occurring on intermediate timeframes ranging from fifteen minutes through four hours. Higher timeframes provide more reliable pattern formation and reduced false signal occurrence, while lower timeframes increase trading frequency at the expense of some signal reliability.

Parameter optimization should focus on RSI threshold adjustments based on market volatility characteristics and candlestick pattern timeframe analysis. Higher RSI thresholds generate fewer but potentially higher quality signals, while lower thresholds increase signal frequency with corresponding reliability considerations.

Stop loss method selection depends on trading style preferences and market analysis philosophy. Entry price-based stops suit systematic approaches requiring consistent risk parameters, while lowest low-based stops align with technical analysis methodologies emphasizing market structure recognition.

## Performance Considerations and Risk Disclosure

The strategy operates exclusively on long positions, making it unsuitable for bear market conditions or extended downtrend periods. Users should consider market environment analysis and broader trend assessment before implementing the strategy during adverse market conditions.

Candlestick pattern reliability varies significantly across different market conditions, with higher reliability typically occurring during trending markets compared to ranging or volatile conditions. Strategy performance may deteriorate during periods of reduced pattern effectiveness or increased market noise.

Risk management through stop loss implementation remains essential for capital preservation during adverse market movements. The strategy does not guarantee profitable outcomes and requires proper position sizing and risk management to prevent significant capital loss during unfavorable trading periods.

## Technical Specifications

The strategy utilizes standard TradingView Pine Script functions ensuring compatibility across all supported instruments and timeframes. Default configuration employs 14-period RSI calculations, adjustable candle stability thresholds, and customizable price decline verification periods optimized for general market conditions.

Initial capital settings default to $10,000 with percentage-based equity allocation, though users can adjust these parameters based on account size and risk tolerance requirements. The strategy maintains detailed trade logs and performance metrics through TradingView's integrated backtesting framework.

Alert integration enables real-time notification of entry and exit signals, stop loss executions, and other significant trading events. The comprehensive alert system supports automated trading applications and manual trade management approaches through detailed signal information provision.

## Conclusion

The Mutanabby_AI Algo Pro Strategy provides a systematic framework for candlestick pattern trading with comprehensive risk management and position sizing flexibility. The strategy's strength lies in its multi-layered confirmation approach and sophisticated customization options, enabling adaptation to various trading styles and market conditions.

Successful implementation requires understanding of candlestick pattern analysis principles and appropriate parameter optimization for specific market characteristics. The strategy serves traders seeking automated execution of proven technical analysis techniques while maintaining comprehensive control over risk management and position sizing methodologies.

Energy Advanced Policy StrategyThis trading strategy emphasizes both technical trading as well as sentiment trading. Using news and government policy decisions, it can determine either positive or negative sentiment in the energy sector.

How the Strategy Works

This strategy has two main parts that work together to find good trades:

1. The "Policy & Sentiment Engine "

Policy Event Detection : The script spots potential big news or policy changes by looking for big, sudden price moves and huge trading volume. You can play with the Policy Event Volume Threshold and Policy Event Price Threshold (%) settings to make it more or less sensitive.

Sentiment Score : When the script finds a positive or negative event, it adds to a sentiment score. This score isn't forever, though; it fades over time, so the newest events matter the most.

Manual Override : The Manual News Sentiment setting lets you tell the script exactly what the market's mood is for a set time, which is perfect for when you already know about a big upcoming announcement.

The strategy only looks for a trade if the overall feeling is bullish enough. This makes sure you're trading with the big, fundamental forces of the market, not against them.

2. Technical Confirmation & Precision

After the policy and sentiment part gives a green light, the strategy uses a variety of technical indicators to confirm the trend and ideal entry positions.

Long-Term Trend : The script makes sure the market is in a strong uptrend by checking if the fast and medium-speed moving averages are going up, and if the price is above a long-term moving average.

Momentum : The MACD is used to make sure the price's upward momentum is getting stronger, not weaker.

Oscillator : It also uses the RSI to check if the market has gone up too much, too fast, which could mean it's about to turn around.

How to Use the Script

You can customize this strategy to fit your trading style and how much risk you're comfortable with. The inputs are grouped into logical sections for easy adjustment.

News & Policy Analysis : You can play with the Policy Event thresholds to make the script more or less sensitive to market shocks. And you can always use the Manual News Sentiment to take over when you're watching a specific news event.

Technical Analysis : Feel free to change the settings for things like the moving averages, RSI, and MACD to match what you like to trade and on what timeframe.

[Stratégia] VWAP Mean Magnet v9 (Simple Alert)This strategy is specifically designed for a ranging (sideways-moving) Bitcoin market.

A trade is only opened and signaled on the chart if all three of the following conditions are met simultaneously at the close of a candle:

Zone Entry

The price must cross into the signal zone: the red band for a Short (sell) position, or the green band for a Long (buy) position.

RSI Confirmation

The RSI indicator must also confirm the signal. For a Short, it must go above 65 (overbought condition). For a Long, it must fall below 25 (oversold condition).

Volume Filter

The volume on the entry candle cannot be excessively high. This safety filter is designed to prevent trades during risky, high-momentum breakouts.

Medico Action Zone self adjust TF version 2to create buy sell signal with adjusted EMA and timeframe

Fisher Crossover StrategyThe Fisher Crossover Strategy is a popular technical trading method that uses the Fisher Transform indicator developed by John Ehlers. This indicator mathematically converts price data into a normal Gaussian distribution, making market turning points sharper and easier to identify. The strategy is based on two lines: the Fisher line, which is the main transformed price value, and the Trigger line, which is a one-period lag of the Fisher line. Traders use the crossover of these lines to determine buy and sell opportunities.

A buy signal is generated when the Fisher line crosses above the Trigger line, indicating that bullish momentum may be starting, while a sell signal occurs when the Fisher line crosses below the Trigger line, suggesting a possible bearish reversal. Signals that occur relative to the zero line are often considered stronger; for example, a buy signal below the zero line may indicate a deeper market reversal. The strategy is simple to follow and can be applied to various markets including stocks, forex, commodities, and cryptocurrencies.

However, like all crossover strategies, it can produce false signals during sideways or ranging markets. To reduce whipsaws, traders often combine the Fisher Crossover Strategy with other tools such as support and resistance levels, volume analysis, or moving averages. Proper risk management with stop-loss and take-profit levels is also essential. Overall, the Fisher Crossover Strategy is valued for its clear entry and exit rules and its ability to highlight potential market reversals earlier than many other indicators.

Advanced Supertrend StrategyA comprehensive Pine Script v5 strategy featuring an enhanced Supertrend indicator with multiple technical filters, risk management, and advanced signal confirmation for automated trading on TradingView.

## Features

- **Enhanced Supertrend**: Configurable ATR-based trend following with improved accuracy

- **RSI Filter**: Optional RSI-based signal filtering to avoid overbought/oversold conditions

- **Moving Average Filter**: Trend confirmation using SMA/EMA/WMA with customizable periods

- **Risk Management**: Built-in stop-loss and take-profit based on ATR multiples

- **Trend Strength Analysis**: Filters weak signals by requiring minimum trend duration

- **Breakout Confirmation**: Optional price breakout validation for stronger signals

- **Visual Interface**: Comprehensive chart plotting with multiple indicator overlays

- **Advanced Alerts**: Multiple alert conditions with detailed signal information

- **Backtesting**: Full strategy backtesting with commission and realistic execution

Modular Range-Trading Strategy (V9.2)# 模块化震荡行情策略 (V9.2)

# Modular Range-Trading Strategy (V9.2)

## 策略简介 | Strategy Overview

该策略基于布林带 (Bollinger Bands)、RSI、MACD、ADX 等经典指标的组合,通过多逻辑模块化结构识别震荡区间的价格反转机会,支持多空双向操作,并在相同逻辑下允许智能加仓,适用于震荡市场的回测和研究。

This strategy combines classic indicators such as Bollinger Bands, RSI, MACD, and ADX to identify price reversal opportunities within ranging markets. It features a modular multi-logic structure, allowing both long and short trades with intelligent pyramiding under the same logic. It is designed for backtesting and research in range-bound conditions.

---

## 功能特点 | Key Features

- **多逻辑结构**:支持多套震荡逻辑(动能确认均值回归、布林带极限反转等)。

- **加仓与仓位互斥**:同逻辑下可智能加仓,不同逻辑间自动互斥,避免冲突。

- **回测可调时间范围**:可自定义回测起止时间,精准评估策略表现。

- **指标可视化**:布林带、RSI、MACD 及动态 ATR 止损线实时绘图。

- **K线收盘确认信号**:通过 `barstate.isconfirmed` 控制信号,避免未收盘的虚假信号。

- **Multi-logic structure**: Supports multiple range-trading logics (e.g., momentum-based mean reversion, Bollinger Band reversals).

- **Pyramiding with mutual exclusion**: Allows intelligent pyramiding within the same logic while preventing conflicts between different logics.

- **Adjustable backtesting range**: Customizable start and end dates for accurate performance evaluation.

- **Visual indicators**: Real-time plotting of Bollinger Bands, RSI, MACD, and dynamic ATR stop lines.

- **Close-bar confirmation**: Uses `barstate.isconfirmed` to avoid false signals before bar close.

---

## 使用说明 | Usage

1. 将该脚本添加到 TradingView 图表。

2. 在参数中设置回测时间段和指标参数。

3. 仅用于学习与策略研究,请勿直接用于实盘交易。

1. Add this script to your TradingView chart.

2. Configure backtesting dates and indicator parameters as needed.

3. For educational and research purposes only. **Not for live trading.**

---

## ⚠️ 免责声明 | Disclaimer

本策略仅供学习和研究使用,不构成任何形式的投资建议。

作者不参与任何实盘交易、资金管理或收益分成,也不保证策略盈利能力。

严禁将本脚本用于任何非法集资、私募募资或与虚拟货币相关的金融违法活动。

使用本策略即表示您自行承担所有风险与法律责任。

This strategy is for educational and research purposes only and does not constitute investment advice.

The author does not participate in live trading, asset management, or profit sharing, nor guarantee profitability.

The use of this script in illegal fundraising, private placements, or cryptocurrency-related financial activities is strictly prohibited.

By using this strategy, you accept all risks and legal responsibilities.

---

[Stratégia] VWAP Mean Magnet v2 (VolSzűrő)Ez a stratégia BTC- oldalazó időszakára van kifejlestve 1 perces chartra.

SwingTrade ADX Strategy v6This is a swing trading strategy that combines VWAP (Volume Weighted Average Price), ADX (Average Directional Index) for trend strength, and volume ratios to generate long/short entry and exit signals. It's designed for daily charts but can be adapted.

#### Key Features:

- **Entries**: Based on VWAP crossovers, rising/falling delta (price deviation from VWAP), ADX trend confirmation, and volume ratios.

- **Exits**: Dynamic exits when VWAP delta reverses after a peak.

- **Filters**: Optional toggles for VWAP signals, ADX, and volume. Backtest date range for custom periods.

- **Visuals**: VWAP line, signal shapes/labels, and an info panel showing key metrics (VWAP Delta %, ADX, Volume Ratio).

- **Alerts**: Built-in alerts for buy/sell entries and exits.

#### How to Use:

1. Apply to your chart (e.g., stocks, forex, crypto).

2. Adjust parameters in the settings (e.g., ADX threshold, volume period).

3. Enable/disable indicators as needed.

4. Backtest using the date filters and review equity curve.

**Disclaimer**: This is for educational purposes only. Past performance is not indicative of future results. Not financial advice—trade at your own risk. Backtest thoroughly and use with proper risk management.

Feedback welcome! If you find it useful, give it a like.