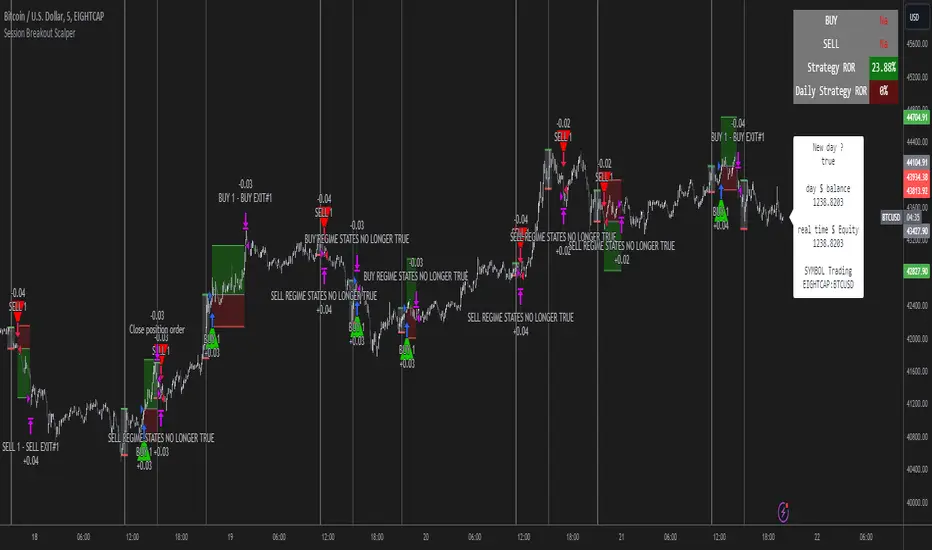

Session Breakout Scalper Trading BotHi Traders !

Introduction:

I have recently been exploring the world of automated algorithmic trading (as I prefer more objective trading strategies over subjective technical analysis (TA)) and would like to share one of my automation compatible (PineConnecter compatible) scripts “Session Breakout Scalper”.

The strategy is really simple and is based on time conditional breakouts although has more ”relatively” advanced optional features such as the regime indicators (Regime Filters) that attempt to filter out noise by adding more confluence states and the ATR multiple SL that takes into account volatility to mitigate the down side risk of the trade.

What is Algorthmic Trading:

Firstly what is algorithmic trading? Algorithmic trading also known as algo-trading, is a method of using computer programs (in this case pine script) to execute trades based on predetermined rules and instructions (this trading strategy). It's like having a robot trader who follows a strict set of commands to buy and sell assets automatically, without any human intervention.

Important Note:

For Algorithmic trading the strategy will require you having an essential TV subscription at the minimum (so that you can set alerts) plus a PineConnecter subscription (scroll down to the .”How does the strategy send signals” headings to read more)

The Strategy Explained:

Is the Time input true ? (this can be changed by toggling times under the “TRADE MEDIAN TIMES” group for user inputs).

Given the above is true the strategy waits x bars after the session and then calculates the highest high (HH) to lowest low (LL) range. For this box to form, the user defined amount of bars must print after the session. The box is symmetrical meaning the HH and LL are calculated over a lookback that is equal to the sum of user defined bars before and after the session (+ 1).

The Strategy then simultaneously defines the HH as the buy level (green line) and the LL as the sell level (red line). note the strategy will set stop orders at these levels respectively.

Enter a buy if price action crosses above the HH, and then cancel the sell order type (The opposite is true for a stop order).

If the momentum based regime filters are true the strategy will check for the regime / regimes to be true, if the regime if false the strategy will exit the current trade, as the regime filter has predicted a slowing / reversal of momentum.

The image below shows the strategy executing these trading rules ( Regime filters, "Trades on chart", "Signal & Label" and "Quantity" have been omitted. "Strategy label plots" has been switched to true)

Other Strategy Rules:

If a new session (time session which is user defined) is true (blue vertical line) and the strategy is currently still in a trade it will exit that trade immediately.

It is possible to also set a range of percentage gain per day that the strategy will try to acquire, if at any point the strategy’s profit is within the percentage range then the position / trade will be exited immediately (This can be changed in the “PERCENT DAY GAIN” group for user inputs)

Stops and Targets:

The strategy has either static (fixed) or variable SL options. TP however is only static. The “STRAT TP & TP” group of user inputs is responsible for the SL and TP values (quoted in pips). Note once the ATR stop is set to true the SL values in the above group no longer have any affect on the SL as expected.

What are the Regime Filters:

The Larry Williams Large Trade Index (LWLTI): The Larry Williams Large Trade Index (LWTI) is a momentum-based technical indicator developed by iconic trader Larry Williams. It identifies potential entries and exits for trades by gauging market sentiment, particularly the buying and selling pressure from large market players. Here's a breakdown of the LWTI:

LWLTI components and their interpretation:

Oscillator: It oscillates between 0 and 100, with 50 acting as the neutral line.

Sentiment Meter: Values above 75 suggest a bearish market dominated by large selling, while readings below 25 indicate a bullish market with strong buying from large players.

Trend Confirmation: Crossing above 75 during an uptrend and below 25 during a downtrend confirms the trend's continuation.

The Andean Oscillator (AO) : The Andean Oscillator is a trend and momentum based indicator designed to measure the degree of variations within individual uptrends and downtrends in the prices.

Regime Filter States:

In trading, a regime filter is a tool used to identify the current state or "regime" of the market.

These Regime filters are integrated within the trading strategy to attempt to lower risk (equity volatility and/or draw down). The regime filters have different states for each market order type (buy and sell). When the regime filters are set to true, if these regime states fail to be true the trade is exited immediately.

For Buy Trades:

LWLTI positive momentum state: Quotient of the lagged trailing difference and the ATR > 50

AO positive momentum state: Bull line > Bear line (signal line is omitted)

For Sell Trades:

LWLTI negative momentum stat: Quotient of the lagged trailing difference and the ATR < 50

AO negative momentum state: Bull line < Bear line (signal line is omitted)

How does the Strategy Send Signals:

The strategy triggers a TV alert (you will neet to set a alert first), TV then sends a HTTP request to the automation software (PineConnecter) which receives the request and then communicates to an MT4/5 EA to automate the trading strategy.

For the strategy to send signals you must have the following

At least a TV essential subscription

This Script added to your chart

A PineConnecter account, which is paid and not free. This will provide you with the expert advisor that executes trades based on these strategies signals.

For more detailed information on the automation process I would recommend you read the PineConnecter documentation and FAQ page.

Dashboard:

This Dashboard (top right by defualt) lists some simple trading statistics and also shows when a trade is live.

Important Notice:

- USE THIS STRATEGY AT YOUR OWN RISK AND ALWAYS DO YOUR OWN RESEARCH & MANUAL BACKTESTING !

- THE STRATEGY WILL NOT EXHIBIT THE BACKTEST PERFORMANCE SEEN BELOW IN ALL MARKETS !

Average True Range (ATR)

ATR StopThe "ATR Stop" indicator is designed to provide traders with insights into potential stop levels based on Average True Range (ATR) calculations specifically tailored for profitable (green candles) and unprofitable (red candles) price movements. This tool aims to assist traders in identifying potential stop levels that adjust dynamically based on the volatility of distinct market conditions.

The indicator functions by calculating two types of ATR: one for profitable movements and the other for unprofitable movements. The Average True Range is calculated separately for green and red candles, allowing users to assess potential stop levels more accurately based on the nature of price movements.

Key features of the "ATR Stop" indicator include:

Custom ATR Calculation: It calculates the ATR for profitable (green) and unprofitable (red) movements separately, considering only specific candle types based on their closing price relative to their opening price.

Dynamic Multiplier: Users can adjust the multiplier to fine-tune the sensitivity of the ATR-based stop levels, accommodating different risk preferences and market conditions.

Clear Visualization: The indicator plots the ATR levels for profitable (green) and unprofitable (red) movements one candle ahead on the chart, providing a visual representation of potential stop levels.

To use the indicator effectively, traders can adjust the ATR length and multiplier parameters based on their trading strategies and risk management preferences. By considering distinct price movements, this tool can assist in setting more informed stop levels in varying market conditions.

Please note that while the "ATR Stop" indicator can be a valuable addition to a trader's toolbox, it should be used in conjunction with other technical analysis tools and risk management strategies to make well-informed trading decisions.

Nasan Rate of Change (ROC)**NOTE: FOR COMPARISON TRADITIONAL ROC IS PLOTTED WITH THE SAME ROC LENGTH OF 9. IT IS NOT PART OF THE INDICATOR"

The Nasan ROC indicator is smoothed version of the of the traditional ROC indicator. The Nasna ROC uses a triple pass moving average differencing strategy. A cumulative sum of the deviations obtained from the moving average differencing provides a smooth "noise free" trend and this cumulative sum of deviations is used for calculating ROC.

Let's break down the components and understand the indicator we discussed earlier:

Sequential Triple Pass Filter:

Three filters with lengths specified by length1, length2, and length3 are applied to the closing prices (close).

The filters involve calculating the cumulative sum of the differences between the closing prices and their respective moving averages.

The idea is to detrend the data and accumulate the deviations from the average over time, emphasizing longer-term trends.

Calculation of Rate of Change (ROC) of Cumulative Sum:

The Rate of Change (ROC) of the cumulative sum (rocCumulativeSum) is calculated using the ta.roc function with a specified length (rocLength).

ROC measures the percentage change in the cumulative sum over a specified period.

The ROC histogram provides insights into the momentum of the detrended series. Positive values suggest increasing momentum, while negative values suggest decreasing momentum.

Pay attention to the color of the histogram bars.

The histogram bars are colored green if the current ROC value is greater than or equal to the previous ROC value, and red otherwise.

This coloring is based on the concept that a positive ROC suggests upward momentum, while a negative ROC suggests downward momentum.

Volatility - Volume Impact:

The Average True Range (ATR) is calculated with a period of 14.

Volume strength is calculated as a factor (VCF) that considers the ratio of the simple moving average (SMA) of the current volume to the SMA of the volume over a longer period (144).

This volume factor (VCF) is then multiplied by ATR, creating a synergy with volatility and volume.

Visualization with Background Color Gradient:

A background color gradient is applied to the chart based on the calculated volume strength (f1).

The gradient color ranges from black (indicating low ATR and volume strength) to purple (indicating high ATR and volume strength). A low value indicates a ranging market with no significant price movements and it is safter to avoid signals generated from ROC histogram in these region.

Synergy of ROC and Volume Strength:

Observe how the ROC signals align with the background color gradient. For example, confirm whether positive ROC aligns with periods of high ATR and volume strength.

This synergy can provide confirmation or divergence signals, adding another layer of analysis.

Average True Range Level█ Overview

The indicator uses color-coded columns to represent different levels of normalized ATR, helping traders identify periods of high or low volatility.

█ Calculations

The normalization process involves dividing the current True Range by the Average True Range. The formula for normalized ATR in the code is:

nAtr = nz(barRange/atr)

█ How To Use

Level < 1

During periods when the normalized ATR is less than 1, suggesting a lower level of volatility, traders may explore inside bar strategies. These strategies focus on trading within the range of the previous bar, aiming to capitalize on potential breakout opportunities.

Level between 1 and 3

In instances where the normalized ATR falls between 1 and 3, indicating moderate volatility, a pullback strategy may be considered. Traders look for temporary corrections against the prevailing trend, entering positions in anticipation of the trend's resumption

Level between 2 and 3

Within the range of normalized ATR between 2 and 3, signifying a balanced level of volatility, traders might explore breakout strategies. These strategies involve identifying potential breakout levels using support and resistance or other indicators and entering trades in the direction of the breakout.

Level > 3

When the normalized ATR exceeds 3, signaling high volatility, traders should approach with caution. While not ideal for typical mean reversion strategies, this condition may indicate that the price has become overextended. Traders might wait for subsequent candles, observing a normalized ATR between 2 and 3, to consider mean reversion opportunities after potential overpricing during the high volatility period.

* Note: These strategies are suggestions and may not be suitable for all trading scenarios. Traders should exercise discretion, conduct their own analysis, and adapt strategies based on individual preferences and risk tolerance.

Red Candle ATRThis ATR - Average True Range - Measures only red candles, giving the average true range of market declines.

RMI Trend Sync - Strategy [presentTrading]█ Introduction and How It Is Different

The "RMI Trend Sync - Strategy " combines the strength of the Relative Momentum Index (RMI) with the dynamic nature of the Supertrend indicator. This strategy diverges from traditional methodologies by incorporating a dual analytical framework, leveraging both momentum and trend indicators to offer a more holistic market perspective. The integration of the RMI provides an enhanced understanding of market momentum, while the Super Trend indicator offers clear insights into the end of market trends, making this strategy particularly effective in diverse market conditions.

BTC 4h long/short performance

█ Strategy: How It Works - Detailed Explanation

- Understanding the Relative Momentum Index (RMI)

The Relative Momentum Index (RMI) is an adaptation of the traditional Relative Strength Index (RSI), designed to measure the momentum of price movements over a specified period. While RSI focuses on the speed and change of price movements, RMI incorporates the direction and magnitude of those movements, offering a more nuanced view of market momentum.

- Principle of RMI

Calculation Method: RMI is calculated by first determining the average gain and average loss over a given period (Length). It differs from RSI in that it uses the price change (close-to-close) rather than absolute gains or losses. The average gain is divided by the average loss, and this ratio is then normalized to fit within a 0-100 scale.

- Momentum Analysis in the Strategy

Thresholds for Decision Making: The strategy uses predetermined thresholds (pmom for positive momentum and nmom for negative momentum) to trigger trading decisions. When RMI crosses above the positive threshold and other conditions align (e.g., a bullish trend), it signals a potential long entry. Similarly, crossing below the negative threshold in a bearish trend may trigger a short entry.

- Super Trend and Trend Analysis

The Super Trend indicator is calculated based on a higher time frame, providing a broader view of the market trend. This indicator uses the Average True Range (ATR) to adapt to market volatility, making it an effective tool for identifying trend reversals.

The strategy employs a Volume Weighted Moving Average (VWMA) alongside the Super Trend, enhancing its capability to identify significant trend shifts.

ETH 4hr long/short performance

█ Trade Direction

The strategy offers flexibility in selecting the trading direction: long, short, or both. This versatility allows traders to adapt to their market outlook and risk tolerance, whether looking to capitalize on bullish trends, bearish trends, or a combination of both.

█ Usage

To effectively use the "RMI Trend Sync" strategy, traders should first set their preferred trading direction and adjust the RMI and Super Trend parameters according to their risk appetite and trading goals.

The strategy is designed to adapt to various market conditions, making it suitable for different asset classes and time frames.

█ Default Settings

RMI Settings: Length: 21, Positive Momentum Threshold: 70, Negative Momentum Threshold: 30

Super Trend Settings: Length: 10, Higher Time Frame: 480 minutes, Super Trend Factor: 3.5, MA Source: WMA

Visual Settings: Display Range MA: True, Bullish Color: #00bcd4, Bearish Color: #ff5252

Additional Settings: Band Length: 30, RWMA Length: 20

RSI & Backed-Weighted MA StrategyRSI & MA Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators that work best together: the Relative Strength Index (RSI) and the Moving Average (MA). We're going to use the RSI as a trend-follower indicator, rather than a reversal indicator as most are used to. To the signals sent by the RSI, we'll add a condition on the chart's MA, filtering out irrelevant signals and considerably increasing our winning rate. This is a medium/long-term strategy. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RSI :

The RSI is one of the best-known and most widely used indicators in trading. Its purpose is to warn traders when an asset is overbought or oversold. It was designed to send reversal signals, but we're going to use it as a trend indicator by increasing its length to 20. The RSI formula is as follows :

RSI (n) = 100 - (100 / (1 + (H (n)/L (n))))

With n the length of the RSI, H(n) the average of days closing above the open and L(n) the average of days closing below the open.

MA :

The Moving Average is also widely used in technical analysis, to smooth out variations in an asset. The SMA formula is as follows :

SMA (n) = (P1 + P2 + ... + Pn) / n

where n is the length of the MA.

However, an SMA does not weight any of its terms, which means that the price 10 days ago has the same importance as the price 2 days ago or today's price... That's why in this strategy we use a RWMA, i.e. a back-weighted moving average. It weights old prices more heavily than new ones. This will enable us to limit the impact of short-term variations and focus on the trend that was dominating. The RWMA used weights :

The 4 most recent terms by : 100 / (4+(n-4)*1.30)

The other oldest terms by : weight_4_first_term*1.30

So the older terms are weighted 1.30 more than the more recent ones. The moving average thus traces a trend that accentuates past values and limits the noise of short-term variations.

PARAMETERS :

RSI Length : Lenght of RSI. Default is 20.

MA Type : Choice between a SMA or a RWMA which permits to minimize the impact of short term reversal. Default is RWMA.

MA Length : Length of the selected MA. Default is 19.

RSI Long Signal : Minimum value of RSI to send a LONG signal. Default is 60.

RSI Short signal : Maximum value of RSI to send a SHORT signal. Default is 40.

ROC MA Long Signal : Maximum value of Rate of Change MA to send a LONG signal. Default is 0.

ROC MA Short signal : Minimum value of Rate of Change MA to send a SHORT signal. Default is 0.

TP activation in multiple of ATR : Threshold value to trigger trailing stop Take Profit. This threshold is calculated as multiple of the ATR (Average True Range). Default value is 5 meaning that to trigger the trailing TP the price need to move 5*ATR in the right direction.

Trailing TP in percentage : Percentage value of trailing Take Profit. This Trailing TP follows the profit if it increases, remaining selected percentage below it, but stops if the profit decreases. Default is 3%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD with a timeframe set to 6h. Parameters are set as follows :

MA type: RWMA

MA Length: 19

RSI Long Signal: >60

RSI Short Signal : <40

ROC MA Long Signal : <0

ROC MA Short Signal : >0

TP Activation in multiple ATR : 5

Trailing TP in percentage : 3

ENTER RULES :

The principle is very simple:

If the asset is overbought after a bear market, we are LONG.

If the asset is oversold after a bull market, we are SHORT.

We have defined a bear market as follows : Rate of Change (20) RWMA < 0

We have defined a bull market as follows : Rate of Change (20) RWMA > 0

The Rate of Change is calculated using this formula : (RWMA/RWMA(20) - 1)*100

Overbought is defined as follows : RSI > 60

Oversold is defined as follows : RSI < 40

LONG CONDITION :

RSI > 60 and (RWMA/RWMA(20) - 1)*100 < -1

SHORT CONDITION :

RSI < 40 and (RWMA/RWMA(20) - 1)*100 > 1

EXIT RULES FOR WINNING TRADE :

We have a trailing TP allowing us to exit once the price has reached the "TP Activation in multiple ATR" parameter, i.e. 5*ATR by default in the profit direction. TP trailing is triggered at this point, not limiting our gains, and securing our profits at 3% below this trigger threshold.

Remember that the True Range is : maximum(H-L, H-C(1), C-L(1))

with C : Close, H : High, L : Low

The Average True Range is therefore the average of these TRs over a length defined by default in the strategy, i.e. 20.

RISK MANAGEMENT :

This strategy may incur losses. The method for limiting losses is to set a Stop Loss equal to 3*ATR. This means that if the price moves against our position and reaches three times the ATR, we exit with a loss.

Sometimes the ATR can result in a SL set below 10% of the trade value, which is not acceptable. In this case, we set the SL at 10%, limiting losses to a maximum of 10%.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

Ranges With Targets [ChartPrime]The Ranges With Targets indicator is a tool designed to assist traders in identifying potential trading opportunities on a chart derived from breakout trading. It dynamically outlines ranges with boxes in real-time, providing a visual representation of price movements. When a breakout occurs from a range, the indicator will begin coloring the candles. A green candle signals a long breakout, suggesting a potential upward movement, while a red candle indicates a short breakout, suggesting a potential downward movement. Grey candles indicate periods with no active trade. Ranges are derived from daily changes in price action.

This indicator builds upon the common breakout theory in trading whereby when price breaks out of a range; it may indicate continuation in a trend.

Additionally, users have the ability to customize their risk-reward settings through a multiplier referred to as the Target input. This allows traders to set their Take Profit (TP) and Stop Loss (SL) levels according to their specific risk tolerance and trading strategy.

Furthermore, the indicator offers an optional stop loss setting that can automatically exit losing trades, providing an additional layer of risk management for users who choose to utilize this feature.

A dashboard is provided in the top right showing the statistics and performance of the indicator; winning trades; losing trades, gross profit and loss and PNL. This can be useful when analyzing the success of breakout trading on a particular asset or timeframe.

Anticipated Profit Targets (APT)Anticipated Profit Targets (APT)

Purpose:

The Anticipated Profit Targets script is a specialized tool designed to assist traders in visualizing potential exit points for their trades. This is achieved by leveraging the Average True Range (ATR), a renowned measure of market volatility.

How It Works:

ATR Computations: At its core, the script calculates the ATR based on a user-defined number of periods. The ATR captures the range between the high and low prices of an asset over a specific duration, providing a snapshot of its volatility.

Multiplier Application: To fine-tune the profit targets, the ATR is multiplied by a user-defined multiplier. This step adjusts the ATR value, setting the profit targets at a distance from the current price, thus accounting for potential price movements.

Adaptable Timeframes: One of the standout features of this script is its adaptability. Users can select their desired timeframe for the profit target calculations. This flexibility means that a trader can be on a 15-minute chart but visualize profit targets based on the volatility of a 1-hour chart.

Visual Representation: The calculated profit targets are then overlaid onto the current chart. This visual aid provides traders with a clear perspective of potential exit points in relation to ongoing price movements.

Originality and Usefulness:

While the concept of using ATR for setting profit targets isn't new, this script's adaptability across timeframes and its user-centric customization options make it a unique offering. The combination of ATR with dynamic multipliers and timeframe adaptability ensures that traders get a tool tailored to their specific needs, rather than a one-size-fits-all solution.

Usage Guidelines:

After adding the script to the chart, traders can adjust the input parameters to their preferences. The anticipated profit targets will then be displayed, offering potential exit points. It's recommended to use these targets in conjunction with other technical indicators and chart patterns for a holistic trading strategy.

Features:

ATR Periods: The ATR is calculated using a user-defined number of periods. By default, it's set to 14 periods, a standard setting. The ATR gauges the asset's volatility, and adjusting the periods can increase or decrease its sensitivity to recent price fluctuations.

ATR Multiplier: The ATR is multiplied by a user-defined factor to determine the profit targets. With a default multiplier of 1.5, the profit target will be positioned 1.5 times the ATR above (for bullish trades) or below (for bearish trades) the current price.

Target Timeframe: Traders can choose the timeframe for which the profit targets are calculated. This feature enables viewing of profit targets from higher timeframes on the current chart. For instance, while observing a 15-minute chart, one can see the 1-hour profit targets.

Visual Indicators:

1. Two lines are plotted: the bullish target (in green) and the bearish target (in red).

2. At the onset of each new candle in the selected higher timeframe, labels indicating the precise profit target values are displayed.

3. Price scale labels also showcase the profit targets, offering a quick reference for potential exit points.

Customization:

Traders can modify the following parameters:

1. ATR Periods: Adjusting the number of periods can refine the ATR's sensitivity to price changes.

2. Multiplier for ATR: Tweaking this value alters the distance between the profit targets and the current price.

3. Timeframe for Profit Targets: A variety of timeframes are available, granting flexibility in viewing profit targets.

How to Use:

After integrating the script into their chart, traders can modify the input parameters as desired. The anticipated profit targets will then be overlaid on the chart, offering potential exit points. When used alongside other technical indicators and chart patterns, this tool can enhance trading decision-making.

Note: This script is designed for educational purposes and should not be considered as financial advice. Always conduct your own research and consult with a financial advisor before making any trading decisions.

ATR SpikeALWAYS TRADE THE DIRECTION OF THE TREND

This indicator is useful for 5-minute Bank Nifty intraday trading.

It compares the Open-Close value for a 5-minute bar with the current ATR value.

When a bar has higher than the ATR value then it means that the current bar has a higher Open-Close than the ATR.

This means that after a period of dull action, some action has taken place.

And more action will follow in the direction of the immediate trend.

It signals the start of momentum which I look for as a intraday trader.

Feel free to experiment and change values as it suits you.

I use it on Bank Nifty only on 5 minute timeframe with 14 period ATR.

MA Slope [EMA Magic]█ Overview:

The MA Slope calculates the slope based on a given moving average.

The Moving Average Slope indicator allows you to identify the direction and the strength of a trend.

It calculates the rate of change in percentage based on the user-defined moving average.

█ Calculation: This indicator calculates the slope based on the changes of moving average and normalizes it with Average True Range(ATR).

The default value of ATR is 7.I recommend not changing it unless you know exactly what are you doing.

█ Input Settings:

The settings are divided into three sections:

The first section is for time frame adjustments. Modify it separately from the chart, Allows you to use moving averages from different time frames.

In the second section, you can configure the base calculation,including Moving Average and Average True Range(ATR) settings.

In the third section, you can detect breakout and sudden change signals, which are highlighted in the background of the indicator.

Note that When you change the breakout limit value, it also affects the band limit indicator on your chart.

To avoid signal confusion, use only one at a time.

Here is the example the breakout signals:

█ Usage:

When the slope is increasing, it indicates an uptrend.

When the slope is decreasing, it indicates a downtrend.

When the slope is moving around zero and choppy, it indicates no specific trend or price is in a range zone.

Uptrend and Range Zone example:

Downtrend example:

Slope peaks on extreme levels can signal a potential trend reversal point.

Breakout of the upper or lower bands can be translated into a trading signal.Indicating that price will probably continue to move in the direction of the breakout.

Favor long setups when the slope is increasing or it is positive and favor short setups when the slope is decreasing or it is negative.

Fits with any moving average you use, e.g., EMA, WMA, MA Ribbon, and more.

█ Alert

Alerts are available for both signal conditions.

█ Recap

Take the time to study price movements alongside this indicator for a deeper understanding.Whether you're a novice or experienced trader, this indicator can come helpful

Open, Open +/- EMA ATR Lines with LabelsThis indicator provides traders with a clear visualization of the opening price and its potential movement range for a specific timeframe, based on the Exponential Moving Average (EMA) of the Average True Range (ATR).

Features:

Opening Price Line: A green line representing the opening price for the chosen timeframe.

EMA ATR Lines:

An upper blue line, calculated as the opening price plus the EMA of the ATR.

A lower blue line, calculated as the opening price minus the EMA of the ATR.

Labels: Each line comes with a label on its right side, displaying the price level and, for the EMA ATR lines, the distance in pips from the opening price.

Custom Timeframes: Users can select their desired timeframe for calculations, making this tool versatile for different trading strategies.

Usage:

The EMA-smoothed ATR provides a measure of volatility. By plotting this value above and below the opening price, traders get a sense of potential price movement for the selected timeframe. This can be particularly useful for setting stop losses, take profit levels, or identifying breakout points.

For instance, if the price breaks above the upper EMA ATR line, it might indicate a potential upward move, especially if other market conditions align.

Customization:

Timeframe: Choose from various timeframes like 1-minute, 5-minutes, daily, weekly, and more.

ATR Length: Adjust the length of the ATR for more or less sensitivity.

This indicator is designed to offer traders a quick way to gauge potential price movement for their chosen timeframe. By combining the principles of the opening price and volatility measured by the EMA-smoothed ATR, it provides a straightforward yet powerful tool for various trading scenarios.

[Spinn] Average True RangeThe "Average True Range" indicator is a popular tool that measures price volatility. In this modified indicator, I present two methods of calculating ATR: the outdated classical one based on RMA (EMA, SMA, WMA), and the modernized one using the Super Smoother filter.

Why has exponential smoothing become outdated?

Exponential smoothing (EMA) has drawbacks, especially when it comes to identifying cyclical components in the data (and RMA is a variant of EMA). EMA creates phase shifts and distortions, making it less predictable and accurate in tracking real price movements. Modern filters, such as Super Smoother, offer a higher degree of adaptability and precision while ensuring significantly less lag, better smoothness, and superior cycle detection.

Why use more contemporary filters like Super Smoother?

The Super Smoother filter combines exponential smoothing and trigonometric functions for more accurate and smooth tracking of price movements. This filter enhances cycle tracking and reduces the lag often found when using EMA. As a result, signals based on Super Smoother are often more precise and representative of real price movements.

Drawbacks of other smoothing filters commonly used with ATR:

SMA. The lag is (N-1)/2, where N = period. This is terrible.

WMA. According to John F. Ehlers, "It appears that the WMA was invented by a trader who did not have a firm grasp of filter theory in hopes of reducing lag". It has been proven that WMA has worse suppression than the equivalent SMA, and WMA has more delay in the passband than the equivalent EMA. In short, WMA has drawbacks but no advantages compared to other popular moving averages.

It is also a good idea to use the median to average the results.

Test, experiment, use!

Consolidation indicator█ Overview

The "Consolidation Indicator" is a custom indicator for TradingView designed to identify consolidation periods in the price chart. Consolidation typically occurs when the price of an asset moves within a narrow range, and this indicator helps traders recognize such conditions. It can be a useful tool for traders looking to identify potential breakouts or periods of reduced volatility.

█ Indicator Settings

1 — Timeframe: This setting allows you to select the timeframe for which you want to analyze consolidation. You can choose from various timeframes available in TradingView.

2 — Price Smoothing Length: This parameter controls the smoothing of price data. You can adjust the value, with a minimum of 1, to control the level of smoothing applied to the price data.

3 — Average Range Length (range_len): This setting defines the length of the average range used in the calculation of the indicator. By default, it is set to 14.

4 — Threshold for Narrow Range (NR_threshold): The indicator will consider a price range as narrow if it falls below this threshold as a percentage of the average range. It is set to 80% by default.

5 — Consecutive Narrow Ranges for Consolidation: This parameter allows you to specify how many consecutive narrow price ranges are required to confirm a consolidation period. The default value is 3.

6 — Candle Color: You can choose the color for the consolidation candles. The default is a bright green color.

█ Indicator Output

The indicator visually displays consolidation and breakout periods on the price chart using colored candles and breakout icons.

• Candles: During a consolidation period, the indicator colorizes the candles in a specified color (default is green) with a transparency that decreases as the number of consecutive narrow ranges increases. This allows you to easily spot consolidation periods on the chart.

• Breakout Icons: The indicator also places a breakout icon (💥) below the price chart to indicate potential breakout opportunities. When a breakout condition is met, the icon appears with an orange color.

█ Alerts

The indicator provides two alert conditions:

1 — Consolidation Begins: This alert triggers when a consolidation period starts. It indicates that the price is moving within a narrow range compared to the average range.

2 — Breakout: This alert triggers when a potential breakout from the consolidation is detected.

█ How to Use

1 — Apply the "Consolidation Indicator" to your TradingView chart by adding it as a custom indicator.

2 — Customize the indicator settings based on your trading preferences, such as timeframe, smoothing length, and threshold for a narrow range.

3 — Monitor the chart for colored candles. The indicator will color candles to highlight consolidation periods.

4 — Look for the breakout icon (💥) below the chart, which indicates potential breakout opportunities.

5 — Set up alerts to be notified when a consolidation begins or a breakout is detected, helping you stay on top of potential trading opportunities.

Keep in mind that this indicator is a tool to assist in identifying consolidation periods, and it should be used in conjunction with other analysis methods for comprehensive trading decisions.

ATR Multiples PlottedInspired by @jeffsuntrading and @Fred6724 's ATR% multiple from 50-MA .

There are no catch-all values, however a high of 6 and a low of -4 generally has been valuable to me. I tend to look at the historical highs and lows of the indicator, and adjust the Value High and Value Low accordingly to get an idea when profit-taking may be sensible.

The essence is the difference between price and the selected moving average, measured in ATRs.

Average True Range (ATR) % KTSLSome traders calculate using percentages when trading. The original ATR indicator calculates using price movements, so it differs for each stock. To avoid this, I changed the ATR indicator to show price movement as a percentage. The red line is the percentage value of the volatility of the original ATR indicator. The white line is 1.6 times the original indicator. The green line is 2.5 times the white line. These values can be adjusted. I wish you good luck.

True Range Moving Average Deviation🔶 Overview

The True Range Moving Average Deviation Indicator (TRMAD) is a technical analysis tool that combines elements of price deviation, volatility, and overbought/oversold conditions.

🔶 Key Components

Current price (Close) : most recent closing price of the asset.

Moving Average (MA) : represents a smoothed trendline of the asset's closing prices over a specified period. By default, TRMAD uses the Simple Moving Average (SMA) with a 20-period setting.

Average True Range (ATR) : reflects the average price range between the high and low over a given time frame. By default, TRMAD uses a 14-period ATR setting with a Simple Moving Average (SMA) calculation. ATR quantifies the historical price volatility of the asset, which is crucial for normalizing the price deviation.

🔶 Calculation

(Close - MA) / ATR

🔶 Interpretation

When TRMAD is above +3 ATR , it is often considered an indication that the asset may be overbought, suggesting a potential reversal or correction to the downside.

When TRMAD is below -3 ATR , it is often considered an indication that the asset may be oversold, suggesting a potential reversal or bounce to the upside.

TRMAD values around 0 ATR may indicate a balanced market condition.

🔶 Usage

🔹 Overbought and Oversold Conditions:

TRMAD can help identify overbought and oversold conditions. When TRMAD reaches or exceeds certain user-defined thresholds (e.g., +3 ATR or -3 ATR), it can signal that the asset is in an extreme condition.

Traders can use these extreme conditions to adjust their positions or look for potential reversal opportunities.

🔹 Divergence Analysis:

Traders often analyze divergences between the TRMAD indicator and price movements. For example, if the price is making higher highs while TRMAD is making lower highs (bearish divergence), it could indicate a potential trend reversal.

🔹 Trend Confirmation:

TRMAD can be used in conjunction with other technical indicators to confirm trends. For example, if TRMAD is consistently positive during an uptrend, it can provide confirmation of the trend's strength.

Positive TRMAD : When TRMAD is positive but hasn't reached the overbought threshold (e.g., +3 ATR), it suggests that there is some bullish momentum, but traders may exercise caution and look for other confirming signals before considering a long position.

Negative TRMAD : When TRMAD is negative but hasn't reached the oversold threshold (e.g., -3 ATR), it suggests some bearish sentiment, but traders may want to seek additional confirmation before considering a short position.

🔹 Risk Management:

Traders can use TRMAD as part of their risk management strategy. For instance, if TRMAD suggests that an asset is overbought, a trader might consider tightening their stop-loss orders to manage potential downside risk.

🔶 Credits

The idea about this indicator came from Fabio Figueiredo (Vlad)

VWAP Divergence | Flux ChartsThe VWAP Divergence indicator aims to find divergences between price action and the VWAP indicator. It uses filters to filter out many of the false divergences and alert high quality, accurate signals.

Red dots above the candle represent bearish divergences, while green dots below the candle represent bullish divergences.

The main filter for divergences focuses on ATR and the price movement in the past candles up to the lookback period. Divergences are determined when a price movement over the lookback period is sharp enough to be greater/less than the ATR multiplier multiplied by the ATR.

Settings

Under "Divergence Settings", both the lookback period and ATR multiplier can be adjusted.

Due to the nature of the calculations, the ATR multiplier and the lookback period should be set lower on higher time frames. As price movements become more averaged, for example on the 15 minute chart, sharp price movements happen less frequently and are often contained in fewer candles as they happen on lower time frames. Less volatile stocks such as KO, CL, or BAC should also use lower ATR multipliers and lower lookback periods.

Under "Visual Settings", you can change the color of the VWAP line, show alternating VWAP colors, adjust divergence signal size, and show the VWAP line.

3kilos BTC 15mThe "3kilos BTC 15m" is a comprehensive trading strategy designed to work on a 15-minute timeframe for Bitcoin (BTC) or other cryptocurrencies. This strategy combines multiple indicators, including Triple Exponential Moving Averages (TEMA), Average True Range (ATR), and Heikin-Ashi candlesticks, to generate buy and sell signals. It also incorporates risk management features like take profit and stop loss.

Indicators

Triple Exponential Moving Averages (TEMA): Three TEMA lines are used with different lengths and sources:

Short TEMA (Red) based on highs

Long TEMA 1 (Blue) based on lows

Long TEMA 2 (Green) based on closing prices

Average True Range (ATR): Custom ATR calculation with EMA smoothing is used for volatility measurement.

Supertrend: Calculated using ATR and a multiplier to determine the trend direction.

Simple Moving Average (SMA): Applied to the short TEMA to smooth out its values.

Heikin-Ashi Close: Used for additional trend confirmation.

Entry & Exit Conditions

Long Entry: Triggered when the short TEMA is above both long TEMA lines, the Supertrend is bullish, the short TEMA is above its SMA, and the Heikin-Ashi close is higher than the previous close.

Short Entry: Triggered when the short TEMA is below both long TEMA lines, the Supertrend is bearish, the short TEMA is below its SMA, and the Heikin-Ashi close is lower than the previous close.

Take Profit and Stop Loss: Both are calculated as a percentage of the entry price, and they are set for both long and short positions.

Risk Management

Take Profit: Set at 1% above the entry price for long positions and 1% below for short positions.

Stop Loss: Set at 3% below the entry price for long positions and 3% above for short positions.

Commission and Pyramiding

Commission: A 0.07% commission is accounted for in the strategy.

Pyramiding: The strategy does not allow pyramiding.

Note

This strategy is designed for educational purposes and should not be considered as financial advice. Always do your own research and consider consulting a financial advisor before engaging in trading.

ATR Adaptive RSI OscillatorThe " ATR Adaptive RSI Oscillator " is a versatile technical analysis tool designed to help traders make informed decisions in dynamic market conditions. It combines the Relative Strength Index (RSI) with the Average True Range (ATR) to provide adaptive and responsive insights into price trends.

Key Features :

Adaptive RSI Periods : The indicator introduces the concept of adaptive RSI periods based on the ATR (Average True Range) of the market. When enabled, it dynamically adjusts the RSI calculation period, offering longer periods during high volatility and shorter periods during low volatility. This adaptability enhances the accuracy of RSI signals across varying market conditions.

Volume-Based Smoothing : The indicator includes a smoothing feature that computes a time-decayed weighted moving average of RSI values over the last two bars, using volume-based weights. This approach offers a time-sensitive smoothing effect, reducing noise for a clearer view of trend strength compared to the standard RSI.

Divergence Detection : Traders can enable divergence detection to identify potential reversal points in the market. The indicator highlights regular bullish and bearish divergences, providing valuable insights into market sentiment shifts.

Customizable Parameters : Traders have the flexibility to customize various parameters, including RSI length, adaptive mode, ATR length, and divergence settings, to tailor the indicator to their trading strategy.

Overbought and Oversold Levels : The indicator includes overbought (OB) and oversold (OS) boundary lines that can be adjusted to suit individual preferences. These levels help traders identify potential reversal zones.

The "ATR Adaptive RSI Oscillator" is a powerful tool for traders seeking to adapt their trading strategies to changing market dynamics. Whether you're a trend follower or a contrarian trader, this indicator provides valuable insights to support your decision-making process.

ATR Trend Reversal Zone indicatorThis indicator helps avoid taking reversal trades too close to the 21 EMA, which may fail since the market often continues its trend after retracing from the 21 EMA level. It does not generate a direct signal for reversal trades but rather indicates points where you can consider potential reversal trades based on your trading methodology

This script defines an indicator that calculates the 21 Exponential Moving Average (EMA) and the Average True Range (ATR) for a given period. It then computes the distance between the most recent closing price and the 21 EMA in terms of ATR units. If this distance is equal to or greater than 3 ATRs, a small green circle is plotted below the corresponding bar on the chart, indicating a potential reversal condition.

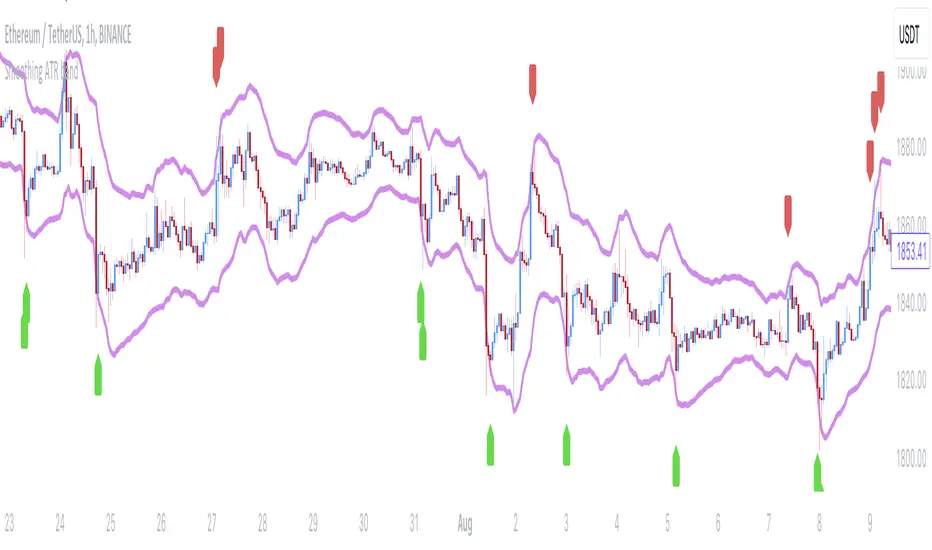

Smoothing ATR bandThere are two bands calculated with the ATR and I added "Smoothing" into the script.

Smoothing ATR with multiplier can display two bands above and below the price.

We can ONLY find some ATR bands in Community Scripts with "Basic" setting which is used to set Stop Loss.

And yet , Smoothing ATR with multiplier is capable of making traders manifestly recognize OverBought & OverSold.

FurtherMore, I added a condition with "plotshape", which is "Stop Hunt"

Stop Hunt is an absolutely usual strategy to clean the leverage and it always makes high volatility moves.

When high> above band and close< above band , long signal, it means it had been abundantly bought but the larger traders weren't satisfied; therefore, they quickly sold out to lower the price. The sell condition is on the contrary.

The signals mainly make traders manifestly recognize OverBought & OverSold.

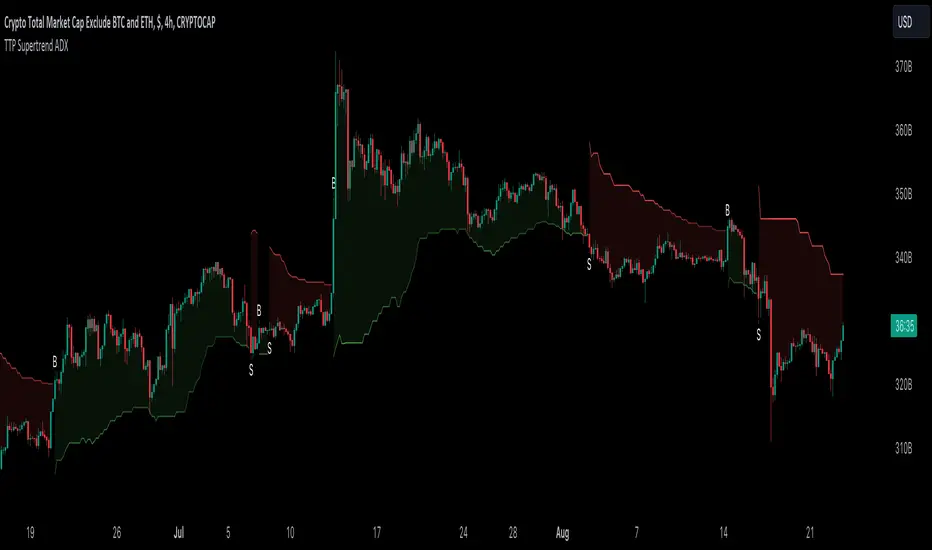

TTP SuperTrend ADXThis indicator uses the strength of the trend from ADX to decide how the SuperTrend (ST) should behave.

Motivation

ST is a great trend following indicator but it's not capable of adapting to the trend strength.

The ADX, Average Directional Index measures the strength of the trend and can be use to dynamically tweak the ST factor so that it's sensitivity can adapt to the trend strength.

Implementation

The indicator calculates a normalised value of the ADX based on the data available in the chart.

Based on these values ST will use different factors to increase or reduce the factor use by ST: expansion or compression.

ST expansion vs compression

Expanding the ST would mean that the stronger a trends get the ST factor will grow causing it to distance further from the price delaying the next ST trend flip.

Compressing the ST would mean that the stronger a trends get the ST factor will shrink causing it to get closer to the price speeding up the next ST trend flip.

Features

- Alerts for trend flip

- Alerts for trend status

- Backtestable stream

- SuperTrend color gets more intense with the strength of the trend