[CT] Donchian Histogram w/Candle ColorsDonchian Histogram, originally created by RafaelZioni and enhanced with optional price bar coloring, is a momentum-style oscillator that shows where the current close sits inside a dynamic Donchian channel and how that position is evolving over time. The script calculates a rolling high and low over a multi-session lookback period based on your chosen Donchian timeframe, then normalizes the close within that range to create a percentage position between the recent high and low. This normalized value is smoothed with a signal length and plotted as a histogram around a zero line, making it easy to see whether price is pressing toward the upper side of its recent range, the lower side, or oscillating near the middle. Positive values indicate that price is trading closer to the Donchian high, negative values indicate price is closer to the Donchian low, and the magnitude of the histogram reflects how strongly price is favoring one side of the range. The color logic highlights this state visually: stronger positive conditions can be shown in teal, moderate positive conditions in lime, stronger negative conditions in red, and neutral or transitional states in orange. The script also includes an option to color the actual chart candles with the same colors as the histogram, so traders can see Donchian-based pressure directly on the main price chart without constantly looking down at the lower pane. The indicator works on completed bars using standard highest/lowest and moving average functions, so it behaves like a normal oscillator and does not use any lookahead tricks. It is best used as a contextual tool to gauge whether price is pushing to the edges of its recent range or reverting toward balance, and to visually synchronize that information with candle colors when desired.

ความผันผวน

Regime MapRegime Map — Volatility State Detector

This indicator is a PineScript friendly approximation of a more advanced Python regime-analysis engine.

The original backed identifies market regimes using structural break detection, Hidden-Markov Models, wavelet decomposition, and long-horizon volatility clustering. Since Pine Script cannot execute these statistical models directly, this version implements a lightweight, real-time proxy using realised volatility and statistical thresholds.

The purpose is to provide a clear visual map of evolving volatility conditions without requiring any heavy offline computation.

________________________________________

Mathematical Basis: Python vs Pine

1. Volatility Estimation

Python (Realised Volatility):

RVₜ = √N × stdev( log(Pₜ) − log(Pₜ₋₁) )

Pine Approximation:

RVₜ = stdev( log(Pₜ) − log(Pₜ₋₁), lookback )

Rationale:

Realised volatility captures volatility clustering — a key characteristic of regime transitions.

________________________________________

2. Regime Classification

Python (HMM Volatility States):

Volatility is modelled as belonging to hidden states with different means and variances:

State μ₁, σ₁

State μ₂, σ₂

State μ₃, σ₃

with state transitions determined by a probability matrix.

Pine Approximation (Z-Score Regimes):

Zₜ = ( RVₜ − mean(RV) ) / stdev(RV)

Regime assignment:

• Regime 0 (Low Vol): Zₜ < Zₗₒw

• Regime 1 (Normal): Zₗₒw ≤ Zₜ ≤ Zₕᵢgh

• Regime 2 (High Vol): Zₜ > Zₕᵢgh

Rationale:

Z-scores provide clean statistical boundaries that behave similarly to HMM state separation but are computable in real time.

________________________________________

3. Structural Break Detection vs Rolling Windows

Python (Bai–Perron Structural Breaks):

Segments the volatility series into periods with distinct statistical properties by minimising squared error over multiple regimes.

Pine Approximation:

Rolling mean and rolling standard deviation of volatility over a long window.

Rationale:

When structural breaks are not available, long-window smoothing approximates slow regime changes effectively.

________________________________________

4. Multi-Scale Cycles

Python (Wavelet Decomposition):

Volatility decomposed into long-cycle (A₄) and short-cycle components (D bands).

Pine Approximation:

Single-scale smoothing using long-horizon averages of RV.

Rationale:

Wavelets reveal multi-frequency behaviour; Pine captures the dominant low-frequency component.

________________________________________

Indicator Output

The background colour reflects the active volatility regime:

• Low Volatility (Green): trending behaviour, cleaner directional movement

• Normal Volatility (Yellow): balanced environment

• High Volatility (Red): sharp swings, traps, mean-reversion phases

Regime labels appear on the chart, with a status panel displaying the current regime.

________________________________________

Operational Logic

1. Compute log returns

2. Calculate short-horizon realised volatility

3. Compute long-horizon mean and standard deviation

4. Derive volatility Z-score

5. Assign regime classification

6. Update background colour and labels

This provides a stable, real-time map of market state transitions.

________________________________________

Practical Applications

Intraday Trading

• Low-volatility regimes favour trend and breakout continuation

• High-volatility regimes favour mean reversion and wide stop placement

Swing Trading

• Compression phases often precede multi-day trending moves

• Volatility expansions accompany distribution or panic events

Risk Management

• Enables volatility-adjusted position sizing

• Helps avoid leverage during expansion regimes

________________________________________

Notes

• Does not repaint

• Fully configurable thresholds and lookbacks

• Works across indices, stocks, FX, crypto

• Designed for real-time volatility regime identification

________________________________________

Disclaimer

This script is intended solely for educational and research purposes.

It does not constitute financial advice or a recommendation to buy or sell any instrument.

Trading involves risk, and past volatility patterns do not guarantee future outcomes.

Users are responsible for their own trading decisions, and the author assumes no liability for financial loss.

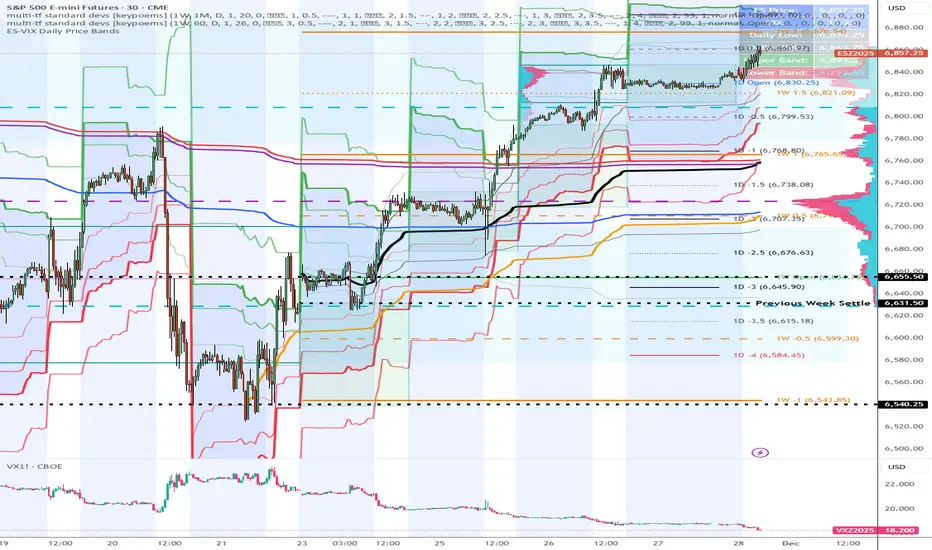

ES-VIX Daily Price Bands - Inner and OuterES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Outer upper band (green) at 150% of expected move

Outer lower band (red) at 150% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

MFM - Light Context HUD (Free)Overview

MFM Light Context HUD is the free version of the Market Framework Model. It gives you a fast and clean view of the current market regime and phase without signals or chart noise. The HUD shows whether the asset is in a bullish or bearish environment and whether it is in a volatile, compression, drift, or neutral phase. This helps you read structure at a glance.

Asset availability

The free version works only on a selected list of five assets.

Supported symbols are

SP:SPX

TVC:GOLD

BINANCE:BTCUSD

BINANCE:ETHUSDT

OANDA:EURUSD

All other assets show a context banner only.

How it works

The free version uses fixed settings based on the original MFM model. It calculates the regime using a higher timeframe RSI ratio and identifies the current phase using simplified momentum conditions. The chart stays clean. Only a small HUD appears in the top corner. Full visual phases, ratio logic, signals, and auto tune are part of the paid version.

The free version shows the phase name only. It does not display colored phase zones on the chart.

Phase meaning

The Market Framework Model uses four structural phases to describe how the market behaves. These are not signals but context layers that show the underlying environment.

Volatile (Phase 1)

The market is in a fast, unstable or directional environment. Price can move aggressively with stronger momentum swings.

Compression (Phase 2)

The market is in a contracting state. Momentum slows and volatility decreases. This phase often appears before expansion, but it does not predict direction.

Drift (Phase 3)

The market moves in a more controlled, persistent manner. Trends are cleaner and volatility is lower compared to volatile phases.

No phase

No clear structural condition is active.

These phases describe market structure, not trade entries. They help you understand the conditions you are trading in.

Cross asset context

The Market Framework Model reads markets as a multi layer system. The full version includes cross asset analysis to show whether the asset is acting as a leader or lagger relative to its benchmark. The free version uses the same internal benchmark logic for regime detection but does not display the cross asset layer on the chart.

Cross asset structure is a core part of the MFM model and is fully available in the paid version.

Included in this free version

Higher timeframe regime

Current phase name

Clean chart output

Context only

Works on a selected set of assets

Not included

No forecast signals

No ratio leader or lagger logic

No MRM zones

No MPF timing

No auto tune

The full version contains all features of the complete MFM model.

Full version

You can find the full indicator here:

payhip.com

More information

Model details and documentation:

mfm.inratios.com

Disclaimer

The Market Framework Model (MFM) and all related materials are provided for educational and informational purposes only. Nothing in this publication, the indicator, or any associated charts should be interpreted as financial advice, investment recommendations, or trading signals. All examples, visualizations, and backtests are illustrative and based on historical data. They do not guarantee or imply any future performance. Financial markets involve risk, including the potential loss of capital, and users remain fully responsible for their own decisions. The author and Inratios© make no representations or warranties regarding the accuracy, completeness, or reliability of the information provided. MFM describes structural market context only and should not be used as the sole basis for trading or investment actions.

By using the MFM indicator or any related insights, you agree to these terms.

© 2025 Inratios. Market Framework Model (MFM) is protected via i-Depot (BOIP) – Ref. 155670. No financial advice.

2t's MA 50, MA 150, ATRThis indicator displays three key technical signals on the chart:

SMA 50 – Short-term trend direction

SMA 150 – Medium-term trend direction

ATR – Market volatility (Average True Range)

Line colors and lengths can be customized in the settings.

The ATR is plotted on the same chart for quick volatility reference without needing a separate panel.

This tool is designed for traders who want a clean, lightweight view of trend strength and volatility in a single indicator.

@Unwind Pressure Detector - AUDITED v3.0SQUEEZE → UNWIND PRESSURE DETECTOR v3.0

The first indicator that not only finds oversold squeezes… but tells you exactly when the move is exhausting and it’s time to take profits.

Fully audited, clean Pine Script v6, zero repainting, zero lag tricks.

WHAT IT DOES

• Detects high-probability squeeze setups (RSI + Volume + VIX + Trend confluence)

• Scores pressure from 0–115 with dynamic sensitivity (Low to Extreme)

• Identifies CRITICAL zones where explosive moves are most likely

• Most importantly → flags the UNWIND when trapped shorts are finally covering and the rally is running out of fuel (perfect profit-taking signal)

FEATURES

• Real-time pressure dashboard (top-right)

• Color-coded background zones (Critical = red, High = orange)

• Smart anti-spam labels with ATR offset

• Three alert conditions:

→ Squeeze Setup

→ Critical Squeeze

→ Unwind / Take Profit

• Works on all markets & timeframes (stocks, forex, crypto, futures)

WHY THIS VERSION IS DIFFERENT

- v3.0 completely rewrote the unwind logic (now requires rally + sharp pressure drop)

- No false unwinds during strong trends

- Built for real trading, not just pretty screenshots

100% Open Source • Fully commented • Free to modify & rep, I want this in the public library forever.

Created with love for the TradingView community

Drop a ♥ and follow if you find it useful!

#squeeze #ttmsqueeze #unwind #volatility #vix #takeprofits #smartmoney

ES-VIX Daily Price Bands - Inner bands (80% and 50%)ES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price Bands - Inner bandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price BandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

@Complete Squeeze Cycle Detector v2.0 FINALDescription:

The Complete Squeeze Cycle Detector identifies and tracks the full lifecycle of squeeze formations, from pre-squeeze consolidation through active squeeze periods to squeeze completion. The indicator systematically detects the characteristic conditions that precede and accompany squeeze events.

The indicator monitors multiple factors associated with squeeze development including:

• Volatility compression relative to recent volume activity

• Elevated market stress conditions as measured by VIX levels

• Momentum compression through rate of change measurements across multiple time periods

• Alignment of multiple exponential moving averages indicating consolidation

The squeeze cycle is classified into three distinct phases: Pre-Squeeze Setup, Active Squeeze, and Squeeze Complete. Each phase is identified based on threshold levels of multiple compression metrics, with adjustable sensitivity settings to control the strictness of detection.

The indicator provides visual identification of each phase through labels, background coloring, and an optional dashboard, allowing users to distinguish between the preparation phase where volatility contracts, the active squeeze phase where compression reaches critical levels, and the completion phase where the squeeze releases and directional movement resumes.

This systematic approach enables users to identify squeeze formations throughout their complete development cycle rather than focusing only on the breakout phase.

Santhosh Zero lag Trend change AlertThis indicator alert whenever these is a change in trend direction. Change input to match with your Asset/Index. This works well in all time frame, I recommend this for Scalping and Position trading

ES-VIX Expected Daily MoveThis indicator calculates the expected daily price movement for ES futures based on current volatility levels as measured by the VIX (CBOE Volatility Index).

Formula:

Expected Daily Move = (ES Price × VIX Price) / √252 / 100

The calculation converts the annualized VIX volatility into an expected daily move by dividing by the square root of 252 (the approximate number of trading days per year).

Features:

Real-time calculation using current ES futures price and VIX level

Histogram visualization in a separate pane for easy trend analysis

Information table displaying:

Current ES futures price

Current VIX level

Expected daily move in points

Expected daily move as a percentage

Elite Energy Alpha MatrixThe Elite Energy Alpha Matrix indicator provides comprehensive analysis of the energy sector, focusing on the complex relationships between crude oil benchmarks, natural gas, energy-related ETFs, and the performance dynamics across various energy sub-sectors.

The indicator tracks multiple energy price data sources including WTI crude oil, Brent crude, natural gas, and oil ETFs, enabling detailed monitoring of price relationships and divergences within the energy complex.

Key analytical components include:

• Correlation analysis between major energy benchmarks

• Multi-timeframe examination of energy price relationships

• Sector rotation detection within energy sub-sectors including integrated oil majors, exploration and production companies, oilfield services, refiners, pipelines, and renewable energy

• Performance monitoring across different energy market segments

The indicator provides a structured framework for analyzing the internal dynamics of the energy sector, identifying periods of alignment or divergence between different energy price instruments, and monitoring relative performance across energy sub-sectors.

This approach enables users to assess the consistency of price movements across the energy complex and identify situations where different components of the energy market are exhibiting divergent behavior, which can provide insight into the underlying drivers affecting the sector.2.6s

Dynamic Ratchet Trend Strategy [VIX Filter]Overview This strategy is a long-only trend-following system designed to capture major market moves while strictly managing downside risk through a state-machine based "Ratchet" exit logic. It incorporates a volatility filter using the CBOE VIX index to stay out of (or exit) the market during high-stress environments.

Key Features

1. Multi-Condition Entries The strategy looks for momentum shifts and trend breakouts using four Simple Moving Averages (25, 50, 100, 200).

Momentum Cross: SMA 25 crossover above SMA 50.

Trend Breakouts: A specific "3-Bar Breakout" logic above the SMA 50, 100, or 200. This requires the price to hold above the SMA for 3 consecutive bars after being below it, reducing false signals compared to simple closes.

2. VIX Volatility Filter Before entering any trade, the script checks the CBOE:VIX.

Filter: If VIX is above the threshold (default 32), new entries are blocked.

Panic Exit: If you are in a position and the VIX spikes above the threshold, the strategy executes an immediate "Panic Exit" to preserve capital during market crashes.

3. The "Ratchet" Exit System (3 Stages) Unlike a standard trailing stop, this strategy uses a 3-stage dynamic exit mechanism that tightens as profits grow:

Stage 0 (Initial Risk): Standard percentage-based Stop Loss from the entry price.

Stage 1 (The Lock-In): Triggered when profit hits 10% (configurable).

Unique Logic: Instead of trailing from the highest high, the stop is calculated based on the price at the exact moment this stage was triggered. It "steps up" once and holds, securing the initial move without being prematurely stopped out by normal volatility.

Stage 2 (Trailing Mode): Triggered when profit hits 15% (configurable).

The strategy switches to a classic Trailing Stop, following the percentage distance from the Highest High.

4. Emergency Backup A "Dead Cross" (SMA 25 crossing under SMA 50) acts as a final fail-safe to close positions if the trend reverses completely before hitting a stop.

Settings & Inputs

SMAs: Customize the lengths for all four moving averages.

VIX Filter: Toggle the filter on/off and set the panic threshold.

Exit Logic: Fully customizable percentages for Initial SL, Stage 1 Trigger/Distance, and Stage 2 Trigger/Trailing Distance.

Disclaimer This script is for educational purposes only. Past performance is not indicative of future results. Always manage your risk appropriately.

Ratchet Exit Trend Strategy with VIX FilterThis strategy is a trend-following system designed specifically for volatile markets. Instead of focusing solely on the "perfect entry," this script emphasizes intelligent trade management using a custom **"Ratchet Exit System."**

Additionally, it integrates a volatility filter based on the CBOE Volatility Index (VIX) to minimize risk during extreme market phases.

### 🎯 The Concept: Ratchet Exit

The "Ratchet" system operates like a mechanical ratchet tool: the Stop Loss can only move in one direction (up, for long trades) and "locks" into specific stages. The goal is to give the trade "room to breathe" initially to avoid being stopped out by noise, then aggressively reduce risk as the trade moves into profit.

The exit logic moves through 3 distinct phases:

1. **Phase 0 (Initial Risk):** At the start of the trade, a wide Stop Loss is set (Default: 10%) to tolerate normal market volatility.

2. **Phase 1 (Risk Reduction):** Once the trade reaches a specific floating profit (Default: +10%), the Stop Loss is raised and "pinned" to a fixed value (Default: -8% from entry). This drastically reduces risk while keeping the trade alive.

3. **Phase 2 (Trailing Mode):** If the trend extends to a higher profit zone (Default: +15%), the Stop switches to a dynamic Trailing Mode. It follows the **Highest High** at a fixed percentage distance (Default: 8%).

### 🛡️ VIX Filter & Panic Exit

High volatility is often the enemy of trend-following strategies.

* **Entry Filter:** The system will not enter new positions if the VIX is above a user-defined threshold (Default: 32). This helps avoid entering "falling knife" markets.

* **Panic Exit:** If the VIX spikes above the threshold (32) while a trade is open, the position is closed immediately to protect capital (Emergency Exit).

### 📈 Entry Signals

The strategy trades **LONG only** and uses Simple Moving Averages (SMAs) to identify trends:

* **Golden Cross:** SMA 25 crosses over SMA 50.

* **3-Bar Breakouts:** A confirmation logic where the price must close above the SMA 50, 100, or 200 for 3 consecutive bars.

### ⚙️ Settings (Inputs)

All parameters are fully customizable via the settings menu:

* **SMAs:** Lengths for the trend indicators (Default: 25, 50, 100, 200).

* **VIX Filter:** Toggle the filter on/off and adjust the panic threshold.

* **Ratchet Settings:** Percentages for Initial Stop, Trigger Levels for Stages 1 & 2, and the Trailing Distance.

### ⚠️ Technical Note & Risk Warning

This script uses `request.security` to fetch VIX data. Please ensure you understand the risks associated with trading leveraged or volatile assets. Past performance is not indicative of future results.

Z-EMA Fusion BandsDesigned with crypto markets in mind, particularly Bitcoin , it builds on the concept that the 1-Week 50 EMA often serves as a long-term bull/bear market threshold — an area where institutional bias, momentum shifts, and cyclical rotations tend to occur.

🔹 Core Components & Synergies:

1. 1W 50 EMA (Higher Timeframe)

- This EMA is calculated on a weekly timeframe, regardless of your current chart.

- In crypto, price above the 1W 50 EMA typically aligns with long-term bull market phases, while extended periods below can signify bearish macro structure.

- The slope of the EMA is also analyzed to add directional confidence to trend strength.

2. ±1 Standard Deviation Bands

- Surrounding the 50 EMA, these bands visualize normal price dispersion relative to trend.

- When price consistently hugs or breaks outside these bands, it often reflects market expansion, volatility events, or mean-reversion opportunity.

3. Z-Score Gradient Fill

- The area between the bands is filled using a Z-score-based gradient, which dynamically adjusts color based on how far price is from the EMA (in terms of standard deviations).

- Color shifts from aqua (near EMA) to fuchsia (far from EMA) help you spot price compression, equilibrium, or overextension at a glance.

- The fill also uses transparency scaling, making it fade as price stretches further, emphasizing the core structure.

4. Directional EMA Coloring

- The EMA line itself is colored based on:

- The slope of the EMA (rising/falling)

- Whether the HTF candle is bullish or bearish

- This provides intuitive color-coded confirmation of momentum alignment or potential exhaustion.

5. Price/EMA Divergence Detection

- The script detects bullish and bearish divergence between price and the EMA (rather than using a traditional oscillator).

- Bullish Divergence: Price makes a lower low, EMA makes a higher low.

- Bearish Divergence: Price makes a higher high, EMA makes a lower high.

- These signals often mark transitional zones where momentum fades before a trend reversal or correction.

📊 Suggested Uses:

🔸 Swing and Position Trading:

- Use the 1W 50 EMA as a macro-trend anchor.

- Stay long-biased when price is above with positive slope, and short-biased when below.

- Consider entries near band edges for mean-reversion plays, especially if confluence forms with divergence signals.

🔸 Volatility-Based Filtering:

- Use the Z-score fill to identify volatility compression (near EMA) or expansion (edge of bands).

- Combine this with breakout strategies or dynamic position sizing.

🔸 Divergence Confirmation:

- Combine divergence markers with HTF EMA slope for high-probability setups.

- Bullish div + EMA flattening/rising can signal the start of accumulation after a macro dip.

🔸 Multi-Timeframe Analysis:

- Works well as a structural overlay on intraday charts (1H, 4H, 1D).

- Use this indicator to track long-term bias while executing lower timeframe trades.

⚠️ Disclaimer:

This indicator is designed for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset.

Always use proper risk management, and combine with your own analysis, tools, and strategy. Performance in past market conditions does not guarantee future results.

Simple Price ChannelSimple Price Channel

This indicator plots a basic volatility-based channel around a moving average.

Features:

Midline using Simple Moving Average (SMA)

Upper & lower bands using ATR or true range

Channel fill for easy trend visualisation

This script is designed for educational and analytical purposes only.

It does not provide signals, alerts, or financial advice.

Bollinger Bands with ATR SL Hariss 369Bollinger Bands are a popular technical analysis tool developed by John Bollinger. They consist of three lines plotted on a price chart:

Middle Band – a simple moving average (usually 20 periods).

Upper Band – the middle band plus two standard deviations.

Lower Band – the middle band minus two standard deviations.

Key Features:

Volatility Indicator: The bands expand when volatility increases and contract when volatility decreases.

Trend Analysis: Prices near the upper band indicate overbought conditions, while prices near the lower band indicate oversold conditions.

Trading Signals: Traders often look for price touches, breaks, or rebounds from the bands to identify potential entries or exits.

To strengthen the trend quality RVOL has been considered. The ideal value of RVOL is 1.5

Higher Time Frame Trend filter gives trend clarity in higher time frame. One can select RVOL and HTF (Higher Time Frame) filter.

Bollinger bands indicator is basically a trend following indicator. We should go with the trend rather book profit @1:1 or 1:2 basis. In that case we might miss the long trend. The middle band is generally considered as stop loss. However, ATR based stop loss has been designed in the script in order to capture the volatility in decent way.

Break out signal is initiated on break out with volume taking higher time frame into consideration.

One can use this indicator in any time frame and any class of asset. To filter higher time frame eg. entry / exit 5 min chart, 15m/1h can be taken as higher time frame, for 1h entry/ exit, 4h can be taken as higher time frame trend filter.

APEX TREND: Macro & Hard Stop SystemAPEX TREND: Macro & Hard Stop System

The APEX TREND System is a composite trend-following strategy engineered to solve the "Whipsaw" problem inherent in standard breakout systems. It orchestrates four distinct technical theories—Macro Trend Filtering, Volatility Squeeze, Momentum, and Volatility Stop-Loss—into a single, hierarchical decision-making engine.

This script is not merely a collection of indicators; it is a rules-based trading system designed for Swing Traders (Day/Week timeframes) who aim to capture major trend extensions while strictly managing downside risk through a "Hard Stop" mechanism.

🧠 Underlying Concepts & Originality

Many trend indicators fail because they treat all price movements equally. The APEX TREND differentiates itself by applying an "Institutional Filter" logic derived from classic Dow Theory and Modern Volatility Analysis.

1. The Macro Hard Stop (The 200 EMA Logic)

Origin: Based on the institutional mandate that “Nothing good happens below the 200-day moving average.”

Function: Unlike standard super trends that flip constantly in sideways markets, this system integrates a 200-period Exponential Moving Average (EMA) as a non-negotiable "Hard Stop."

Synergy: This acts as the primary gatekeeper. Even if the volatility engine signals a "Buy," the system suppresses the signal if the price is below the Macro Baseline, effectively filtering out counter-trend traps.

2. The Volatility Engine (Squeeze Theory)

Origin: Derived from John Carter’s TTM Squeeze concept.

Function: The script identifies periods where Bollinger Bands (Standard Deviation) contract inside Keltner Channels (ATR). This indicates a period of potential energy build-up.

Synergy: The system only triggers an entry when this energy is released (Breakout) AND coincides with Linear Regression Momentum, ensuring the breakout is genuine.

3. Anti-Chop Filter (ADX Integration)

Origin: J. Welles Wilder’s Directional Movement Theory.

Function: A common failure point for trend systems is low-volatility chop. This script utilizes the Average Directional Index (ADX).

Synergy: If the ADX is below the threshold (Default: 20), the market is deemed "Choppy." The script visually represents this by painting candles GRAY, signaling a "No-Trade Zone" regardless of price action.

4. The "Run Trend" Stop Loss (Factor 4.0 ATR)

Origin: Adapted from the Turtle Trading rules regarding volatility-based stops.

Function: Standard Trailing Stops (usually Factor 3.0) are too tight for crypto or volatile equities on daily timeframes.

Optimization: This system employs a wider ATR Multiplier of 4.0. This allows the asset to fluctuate naturally within a trend without triggering a premature exit, maximizing the "Run Trend" potential.

🛠 How It Works (The Algorithm)

The script processes data in a specific order to generate a signal:

Check Macro Trend: Is Price > EMA 200? (If No, Longs are disabled).

Check Volatility: Is ADX > 20? (If No, all signals are disabled).

Check Volume: Is Current Volume > 1.2x Average Volume? (Confirmation of institutional participation).

Trigger: Has a Volatility Breakout occurred in the direction of the Macro Trend?

Execution: If ALL above are true -> Generate Signal.

🎯 Strategy Guide

1. Long Setup (Bullish)

Signal: Look for the Green "APEX LONG" Label.

Condition: The price must be ABOVE the White Line (EMA 200).

Execution: Enter at the close of the signal candle.

Stop Loss: Initial stop at the Green Trailing Line.

2. Short Setup (Bearish)

Signal: Look for the Red "APEX SHORT" Label.

Condition: The price must be BELOW the White Line (EMA 200).

Execution: Enter at the close of the signal candle.

Stop Loss: Initial stop at the Red Trailing Line.

3. Exit Rules (Crucial)

This system employs a Dual-Exit Mechanism:

Soft Exit (Profit Taking): Close the position if the price crosses the Trailing Stop Line (Green/Red line). This locks in profits during a trend reversal.

Hard Exit (Emergency): Close the position IMMEDIATELY if the price crosses the White EMA 200 Line against your trade. This prevents holding a position during a major market regime change.

⚙️ Settings

Momentum Engine: Adjust Bollinger Band/Keltner Channel lengths to tune breakout sensitivity.

Apex Filters: Toggle the EMA 200 or ADX filters on/off to adapt to different asset classes.

Risk Management: The ATR Multiplier (Default 4.0) controls the width of the trailing stop. Lower values = Tighter stops (Scalping); Higher values = Looser stops (Swing).

Disclaimer: This script is designed for trend-following on higher timeframes (4H, 1D, 1W). Please backtest on your specific asset before live trading.

ADR / $Volume DashboardSee 5 / 20 days ADR / Volume and price %age from low of day on top of the chart

LazyTradeLazyTrade is a clean, high-confidence trend-following indicator built on TradingView’s non-repainting SuperTrend V6 engine. It adds intelligent RSI confirmation, profit-tracking labels, trend-flip markers, and optional background shading to highlight momentum shifts. Designed for intraday and swing traders who want fast, reliable signals without chart clutter.

Features:

• Non-repainting Buy/Sell signals

• Smart RSI confirmation (Aggressive / Standard / Conservative)

• Auto P&L between opposite signals

• Trend-flip circles and transparent background zones

• Clean visual structure optimized for daily and leveraged ETF trading

A simple, intuitive tool that keeps you aligned with the dominant trend—no noise, no over-complication.

Beast Mode Adaptive Oscillator V6⭐ Beast Mode Adaptive Oscillator V6

Description (Copy/Paste for Publishing)

Beast Mode Adaptive Oscillator V6 is a high-precision, regime-aware momentum engine that adapts dynamically to market conditions.

It blends ADX-based market regime filtering, StochRSI adaptive oscillation, and ATR-driven signal validation to deliver a powerful, low-noise, context-smart oscillator.

Instead of giving the same overbought/oversold signals in every environment, this oscillator changes its behavior depending on market regime:

Market Regime Filter (MRF)

Automatically detects:

✔ Strong Bull Trend

✔ Strong Bear Trend

✔ Ranging Bull

✔ Ranging Bear

✔ Noise / Low-Volatility Environment

ADX + DI structure determines how aggressive or conservative the oscillator becomes.

Adaptive Regime Oscillator (ARO)

A smart StochRSI core whose OB/OS levels shift depending on trend regime:

• In strong trends → wider OB/OS bands (10–90)

• In ranges → tighter, mean-reverting bands (20–80)

• Higher accuracy and fewer false reversals

Price/Volatility Control (PVC)

Built-in ATR risk modules:

• ATR-based stop zones

• ATR-based target zones

• Internal validation to confirm signal strength

Optional Visual Aids

• Entry signal markers

• Regime bar at the bottom of the chart

• ADX line display

• Custom colors for trend strength

What This Indicator Is Best At

• Avoiding bad signals during chop

• Catching trend continuation entries

• Identifying exhaustion points in strong moves

• Adapting OB/OS logic to match volatility

• Confirming strength with ADX + DI structure

Perfect For

• Intraday traders

• Swing traders

• Trend traders

• Mean-reversion setups

• Volatility-based strategies

This is a complete adaptive oscillator system designed to stay accurate across every market condition.

Tesla 3-6-9 Vortex OscillatorTesla 3-6-9 Vortex Oscillator — Description

The Tesla 3-6-9 Vortex Oscillator is a unique market-structure indicator inspired by Nikola Tesla’s 3-6-9 theory, vortex mathematics, and digital-root numerical cycles.

This tool analyzes price and volume through digit-reduction patterns to track the frequency of “sacred” 3-6-9 values versus traditional 1-2-4-5-7-8 “material world” values.

Core Concept

In vortex math, all numbers reduce to a single digit (1–9).

However, 3, 6, and 9 form a special control triad, representing cyclical creation, harmony, and completion.

This indicator measures how often market data resolves into these higher-cycle digits — creating a real-time “vortex energy ratio” for trend bias and momentum shifts.

What the Indicator Measures

✔ Digital Root of Price / Volume / Range

✔ 3-6-9 Frequency vs. Counter Digit Frequency

✔ Vortex Ratio (%) – percentage dominance of 3/6/9 activity

✔ Smoothed Vortex Oscillator – trend-ready version

✔ Tesla Wave – a cyclical sine-wave based on vortex length & chosen (3, 6, or 9) multiplier

✔ Optional Visual Layers:

• Digital-root analysis

• Vortex spiral visualization

• Harmonic 3-6-9 levels

How to Use It

High Vortex Values (above 60%)

→ Market dominated by 3-6-9 cycles

→ Often aligns with expansion, breakouts, or trend strengthening

Low Vortex Values (below 40%)

→ Counter-digit dominance

→ Consolidation, weakening trend, or potential mean-reversion

Tesla Wave Crosses

→ Can signal timing windows and rhythm shifts within the cycle.

Who This Indicator Is For

• Traders who like numerical cycle analysis

• Users of vortex math, digital-root, or harmonic structures

• People who want a non-lagging sentiment oscillator

• Anyone blending TA + number theory for timing large moves