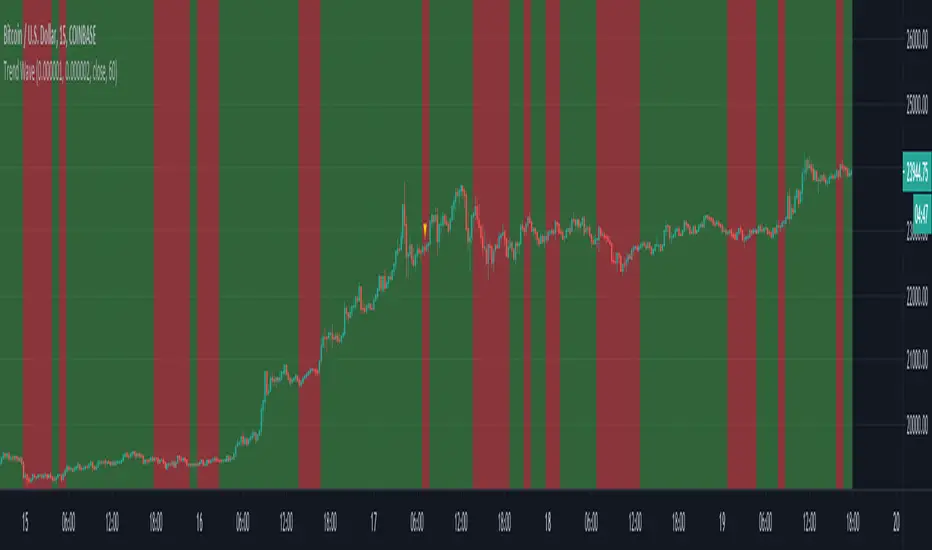

Trend WaveHello Traders!

You know, I can sill remember the first time I started tinkering with Pinescript. As I had no prior programming experience, I learned by experimenting with other open-source scripts on TradingViews Marketplace. Tearing apart and combining interesting scripts to see what the output would be. @ChrisMoody was a huge source of inspiration for learning, and I wanted to thank him, as well as @TheLark for the concept behind this script.

The Trend Wave is based on @ChrisMoody's PPO-PercentileRank-Mkt-Tops-Bottoms , which also happens to be based on @TheLark's TheLark-Laguerre-PPO/ .

Within my experimentation, I found that if I isolate the ppoT & ppoB variables and plot them calculated from extremely small decimals, you can get an extremely fast reacting, mirroring trend detector.

Within the script, you have the ability to plot the background colors based on trend to make it easier to see where crossovers occured, as well as a Mirror Input to view the mirrored version of the script.

-@DayTradingOil

ค้นหาในสคริปต์สำหรับ "tradingview+金龙指数"

Krown Cryptos 6 Moving AveragesCouldnt find Krown's moving average indicator so I took the time to make my own use and to aid those who follow his channel.

The moving averages are a mixed batch with mostly EMAS with the 10SMA and 200SMA included. The MAs are labelled so if you question which one is which

10SMA

21EMA

50EMA

89EMA

200SMA

200EMA

377EMA

If anyone has experience with tradingviews pineeditor and knows how to change the title of each MA so I can remove the "6 moving averages" part that would be a great help so please feel free to inbox me.

Moving Averages Cross - MTF - StrategyBacktesting Script for the following strategy

Strategy Injector Source: github.com

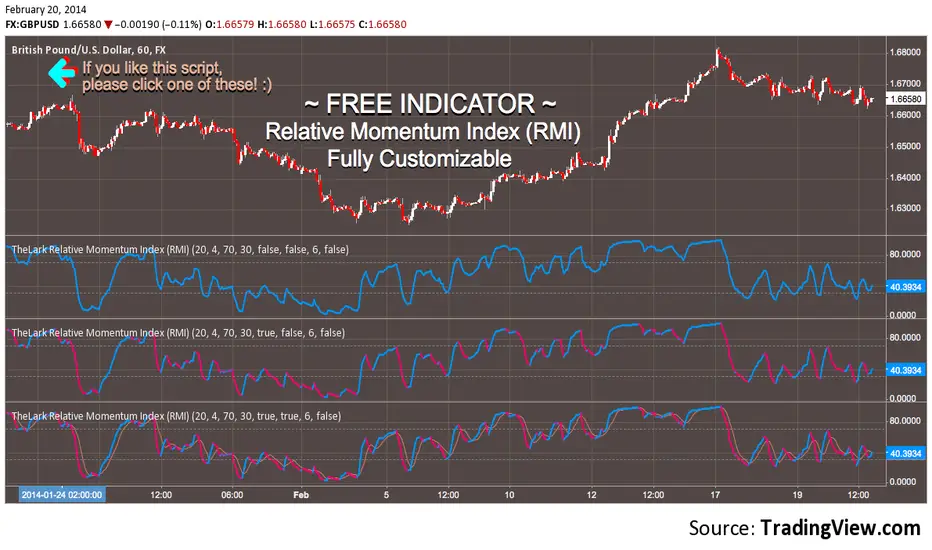

FREE INDICATOR: Relative Momentum Index (RMI)RMI, as requested by glaz

Description:

The Relative Momentum Index was developed by Roger Altman and was introduced in his article in the February, 1993 issue of Technical Analysis of Stocks & Commodities magazine.

While your typical RSI counts up and down days from close to close, the Relative Momentum Index counts up and down days from the close relative to a close x number of days ago. The result is an RSI that is a bit smoother.

Usage:

Use in the same way you would any other RSI. There are overbought and oversold zones, and can also be used for divergence and trend analysis .

Grab the source code here: pastebin.com

Installation video by @ChrisMoody here : vimeopro.com

░░░░░░░░░░░░░░░ Feel free to follow me to keep up with my latest scripts! ░░░░░░░░░░░░░░░

░░░░░░░░░░░░ PLEASE THUMB UP OR STAR IF YOU LIKE THIS INDICATOR! ░░░░░░░░░░░░

I'd like as many people as possible to get it :)

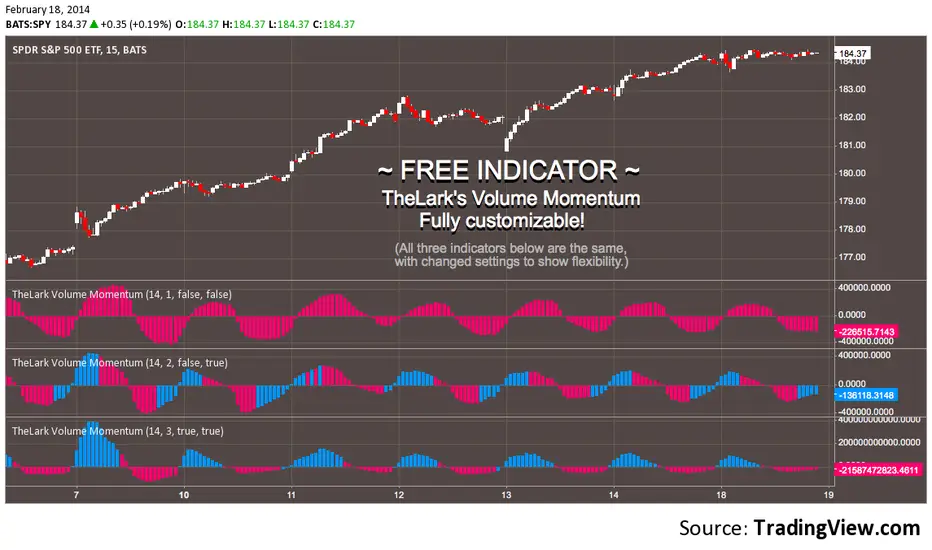

FREE INDICATOR: VOLUME MOMENTUMFor the momentum trader there are plenty of price momentum indicators, here's one that tracks the volume's momentum. Rising momentum in both price and volume is great for any momentum trader.

Add this to your chart, play with the settings, and maybe you'll notice something new!

Grab the source code here: pastebin.com

Installation video by @ChrisMoody here : vimeopro.com

·´¯`·.¸¸.·´¯`· Feel free to follow me to keep up with my latest scripts! ·´¯`·.¸¸.·´¯`·

·´¯`·.¸¸.·´¯`· PLEASE THUMB UP OR STAR IF YOU LIKE THIS INDICATOR! ·´¯`·.¸¸.·´¯`·

I'd like as many people as possible to get it :)

Quantum Market Analyzer X7Quantum Market Analyzer X7 - Complete Study Guide

Table of Contents

1. Overview

2. Indicator Components

3. Signal Interpretation

4. Live Market Analysis Guide

5. Best Practices

6. Limitations and Considerations

7. Risk Disclaimer

________________________________________

Overview

The Quantum Market Analyzer X7 is a comprehensive multi-timeframe technical analysis indicator that combines traditional and modern analytical methods. It aggregates signals from multiple technical indicators across seven key analysis categories to provide traders with a consolidated view of market sentiment and potential trading opportunities.

Key Features:

• Multi-Indicator Analysis: Combines 20+ technical indicators

• Real-Time Dashboard: Professional interface with customizable display

• Signal Aggregation: Weighted scoring system for overall market sentiment

• Advanced Analytics: Includes Order Block detection, Supertrend, and Volume analysis

• Visual Progress Indicators: Easy-to-read progress bars for signal strength

________________________________________

Indicator Components

1. Oscillators Section

Purpose: Identifies overbought/oversold conditions and momentum changes

Included Indicators:

• RSI (14): Relative Strength Index - momentum oscillator

• Stochastic (14): Compares closing price to price range

• CCI (20): Commodity Channel Index - cycle identification

• Williams %R (14): Momentum indicator similar to Stochastic

• MACD (12,26,9): Moving Average Convergence Divergence

• Momentum (10): Rate of price change

• ROC (9): Rate of Change

• Bollinger Bands (20,2): Volatility-based indicator

Signal Interpretation:

• Strong Buy (6+ points): Multiple oscillators indicate oversold conditions

• Buy (2-5 points): Moderate bullish momentum

• Neutral (-1 to 1 points): Balanced conditions

• Sell (-2 to -5 points): Moderate bearish momentum

• Strong Sell (-6+ points): Multiple oscillators indicate overbought conditions

2. Moving Averages Section

Purpose: Determines trend direction and strength

Included Indicators:

• SMA: 10, 20, 50, 100, 200 periods

• EMA: 10, 20, 50 periods

Signal Logic:

• Price >2% above MA = Strong Buy (+2)

• Price above MA = Buy (+1)

• Price below MA = Sell (-1)

• Price >2% below MA = Strong Sell (-2)

Signal Interpretation:

• Strong Buy (6+ points): Price well above multiple MAs, strong uptrend

• Buy (2-5 points): Price above most MAs, bullish trend

• Neutral (-1 to 1 points): Mixed MA signals, consolidation

• Sell (-2 to -5 points): Price below most MAs, bearish trend

• Strong Sell (-6+ points): Price well below multiple MAs, strong downtrend

3. Order Block Analysis

Purpose: Identifies institutional support/resistance levels and breakouts

How It Works:

• Detects historical levels where large orders were placed

• Monitors price behavior around these levels

• Identifies breakouts from established order blocks

Signal Types:

• BULLISH BRK (+2): Breakout above resistance order block

• BEARISH BRK (-2): Breakdown below support order block

• ABOVE SUP (+1): Price holding above support

• BELOW RES (-1): Price rejected at resistance

• NEUTRAL (0): No significant order block interaction

4. Supertrend Analysis

Purpose: Trend following indicator based on Average True Range

Parameters:

• ATR Period: 10 (default)

• ATR Multiplier: 6.0 (default)

Signal Types:

• BULLISH (+2): Price above Supertrend line

• BEARISH (-2): Price below Supertrend line

• NEUTRAL (0): Transition period

5. Trendline/Channel Analysis

Purpose: Identifies trend channels and breakout patterns

Components:

• Dynamic trendline calculation using pivot points

• Channel width based on historical volatility

• Breakout detection algorithm

Signal Types:

• UPPER BRK (+2): Breakout above upper channel

• LOWER BRK (-2): Breakdown below lower channel

• ABOVE MID (+1): Price above channel midline

• BELOW MID (-1): Price below channel midline

6. Volume Analysis

Purpose: Confirms price movements with volume data

Components:

• Volume spikes detection

• On Balance Volume (OBV)

• Volume Price Trend (VPT)

• Money Flow Index (MFI)

• Accumulation/Distribution Line

Signal Calculation: Multiple volume indicators are combined to determine institutional activity and confirm price movements.

________________________________________

Signal Interpretation

Overall Summary Signals

The indicator aggregates all component signals into an overall market sentiment:

Signal Score Range Interpretation Action

STRONG BUY 10+ Overwhelming bullish consensus Consider long positions

BUY 4-9 Moderate to strong bullish bias Look for long opportunities

NEUTRAL -3 to 3 Mixed signals, consolidation Wait for clearer direction

SELL -4 to -9 Moderate to strong bearish bias Look for short opportunities

STRONG SELL -10+ Overwhelming bearish consensus Consider short positions

Progress Bar Interpretation

• Filled bars indicate signal strength

• Green bars: Bullish signals

• Red bars: Bearish signals

• More filled bars = stronger conviction

________________________________________

Live Market Analysis Guide

Step 1: Initial Assessment

1. Check Overall Summary: Start with the main signal

2. Verify with Component Analysis: Ensure signals align

3. Look for Divergences: Identify conflicting signals

Step 2: Timeframe Analysis

1. Set Appropriate Timeframe: Use 1H for intraday, 4H/1D for swing trading

2. Multi-Timeframe Confirmation: Check higher timeframes for trend context

3. Entry Timing: Use lower timeframes for precise entry points

Step 3: Signal Confirmation Process.

For Buy Signals:

1. Oscillators: Look for oversold conditions (RSI <30, Stoch <20)

2. Moving Averages: Price should be above key MAs

3. Order Blocks: Confirm bounce from support levels

4. Volume: Check for accumulation patterns

5. Supertrend: Ensure bullish trend alignment.

For Sell Signals:

1. Oscillators: Look for overbought conditions (RSI >70, Stoch >80)

2. Moving Averages: Price should be below key MAs

3. Order Blocks: Confirm rejection at resistance levels

4. Volume: Check for distribution patterns

5. Supertrend: Ensure bearish trend alignment.

Step 4: Risk Management Integration

1. Signal Strength Assessment: Stronger signals = larger position size

2. Stop Loss Placement: Use Order Block levels for stops

3. Take Profit Targets: Based on channel analysis and resistance levels

4. Position Sizing: Adjust based on signal confidence

________________________________________

Best Practices

Entry Strategies

1. High Conviction Entries: Wait for STRONG BUY/SELL signals

2. Confluence Trading: Look for multiple components aligning

3. Breakout Trading: Use Order Block and Trendline breakouts

4. Trend Following: Align with Supertrend direction.

Risk Management

1. Never Risk More Than 2% Per Trade: Regardless of signal strength

2. Use Stop Losses: Place at invalidation levels

3. Scale Positions: Stronger signals warrant larger (but still controlled) positions

4. Diversification: Don't rely solely on one indicator.

Market Conditions

1. Trending Markets: Focus on Supertrend and MA signals

2. Range-Bound Markets: Emphasize Oscillator and Order Block signals

3. High Volatility: Reduce position sizes, widen stops

4. Low Volume: Be cautious of breakout signals.

Common Mistakes to Avoid

1. Signal Chasing: Don't enter after signals have already moved significantly

2. Ignoring Context: Consider overall market conditions

3. Overtrading: Wait for high-quality setups

4. Poor Risk Management: Always use appropriate position sizing

________________________________________

Limitations and Considerations

Technical Limitations

1. Lagging Nature: All technical indicators are based on historical data

2. False Signals: No indicator is 100% accurate

3. Market Regime Changes: Indicators may perform differently in various market conditions

4. Whipsaws: Possible in choppy, sideways markets.

Optimal Use Cases

1. Trending Markets: Performs best in clear trending environments

2. Medium to High Volatility: Requires sufficient price movement for signals

3. Liquid Markets: Works best with adequate volume and tight spreads

4. Multiple Timeframe Analysis: Most effective when used across different timeframes.

When to Use Caution

1. Major News Events: Fundamental analysis may override technical signals

2. Market Opens/Closes: Higher volatility can create false signals

3. Low Volume Periods: Signals may be less reliable

4. Holiday Trading: Reduced participation affects signal quality

________________________________________

Risk Disclaimer

IMPORTANT LEGAL DISCLAIMER FROM aiTrendview

WARNING: TRADING INVOLVES SUBSTANTIAL RISK OF LOSS

This Quantum Market Analyzer X7 indicator ("the Indicator") is provided for educational and informational purposes only. By using this indicator, you acknowledge and agree to the following terms:

No Investment Advice

• The Indicator does NOT constitute investment advice, financial advice, or trading recommendations

• All signals generated are based on historical price data and mathematical calculations

• Past performance does not guarantee future results

• No representation is made that any account will achieve profits or losses similar to those shown.

Risk Acknowledgment

• TRADING CARRIES SUBSTANTIAL RISK: You may lose some or all of your invested capital

• LEVERAGE AMPLIFIES RISK: Margin trading can result in losses exceeding your initial investment

• MARKET VOLATILITY: Financial markets are inherently unpredictable and volatile

• TECHNICAL ANALYSIS LIMITATIONS: No technical indicator is infallible or guarantees profitable trades.

User Responsibility

• YOU ARE SOLELY RESPONSIBLE for all trading decisions and their consequences

• CONDUCT YOUR OWN RESEARCH: Always perform independent analysis before making trading decisions

• CONSULT PROFESSIONALS: Seek advice from qualified financial advisors

• RISK MANAGEMENT: Implement appropriate risk management strategies

No Warranties

• The Indicator is provided "AS IS" without warranties of any kind

• aiTrendview makes no representations about the accuracy, reliability, or suitability of the Indicator

• Technical glitches, data feed issues, or calculation errors may occur

• The Indicator may not work as expected in all market conditions.

Limitation of Liability

• aiTrendview SHALL NOT BE LIABLE for any direct, indirect, incidental, or consequential damages

• This includes but is not limited to: trading losses, missed opportunities, data inaccuracies, or system failures

• MAXIMUM LIABILITY is limited to the amount paid for the indicator (if any)

Code Usage and Distribution

• This indicator is published on TradingView in accordance with TradingView's house rules

• UNAUTHORIZED MODIFICATION or redistribution of this code is prohibited

• Users may not claim ownership of this intellectual property

• Commercial use requires explicit written permission from aiTrendview.

Compliance and Regulations

• VERIFY LOCAL REGULATIONS: Ensure compliance with your jurisdiction's trading laws

• Some trading strategies may not be suitable for all investors

• Tax implications of trading are your responsibility

• Report trading activities as required by law

Specific Risk Factors

1. False Signals: The Indicator may generate incorrect buy/sell signals

2. Market Gaps: Overnight gaps can invalidate technical analysis

3. Fundamental Events: News and economic data can override technical signals

4. Liquidity Risk: Some markets may have insufficient liquidity

5. Technology Risk: Platform failures or connectivity issues may prevent order execution.

Professional Trading Warning

• THIS IS NOT PROFESSIONAL TRADING SOFTWARE: Not intended for institutional or professional trading

• NO REGULATORY APPROVAL: This indicator has not been approved by any financial regulatory authority

• EDUCATIONAL PURPOSE: Designed primarily for learning technical analysis concepts

FINAL WARNING

NEVER INVEST MONEY YOU CANNOT AFFORD TO LOSE

Trading financial instruments involves significant risk. The majority of retail traders lose money. Before using this indicator in live trading:

1. Practice on paper/demo accounts extensively

2. Start with small position sizes

3. Develop a comprehensive trading plan

4. Implement strict risk management rules

5. Continuously educate yourself about market dynamics

By using the Quantum Market Analyzer X7, you acknowledge that you have read, understood, and agree to this disclaimer. You assume full responsibility for all trading decisions and their outcomes.

Contact: For questions about this disclaimer or the indicator, contact aiTrendview through official TradingView channels only.

________________________________________

This study guide and indicator are published on TradingView in compliance with TradingView's community guidelines and house rules. All users must adhere to TradingView's terms of service when using this indicator.

Document Version: 1.0

Publisher: aiTrendview

________________________________________

Disclaimer

The content provided in this blog post is for educational and training purposes only. It is not intended to be, and should not be construed as, financial, investment, or trading advice. All charting and technical analysis examples are for illustrative purposes. Trading and investing in financial markets involve substantial risk of loss and are not suitable for every individual. Before making any financial decisions, you should consult with a qualified financial professional to assess your personal financial situation.

XAutoTrade Alert Builder v1.1Automate Your NinjaTrader Trading with TradingView Alerts

The XAutoTrade Alert Builder is a flexible Pine Script strategy that bridges TradingView alerts with

NinjaTrader automated trading. Design custom entry signals, configure exit strategies, and execute trades

automatically on your NinjaTrader account - all from TradingView charts.

Key Features

📊 Flexible Signal Logic

- Configure buy/sell signals independently

- Compare any two indicators or price sources using crossover, crossunder, greater than, or less than

logic

- Visual buy/sell markers on chart for easy signal verification

🎯 Multiple Exit Methods

1. ATM Strategy - Leverage your existing NinjaTrader ATM templates for advanced order management

2. Source Signals - Exit positions based on opposite entry signals

3. Fixed Levels - Set stop loss and profit targets using ticks or percentage

⚙️ NinjaTrader Integration

- Direct webhook integration with XAutoTrade backend service

- Multi-account support (trade multiple accounts simultaneously)

- Position sizing and max position limits

- Market or limit order types with configurable offset

- Time-in-force options (DAY/GTC)

- Active hours filter (US ET timezone) to control when alerts execute

🔐 Secure & Reliable

- Webhook secret authentication

- Symbol override capability

- Real-time status indicator showing configuration readiness

How It Works

1. Configure Entry Signals - Choose your buy/sell logic by comparing any two data sources (price,

indicators, etc.)

2. Set Exit Strategy - Select ATM templates, signal-based exits, or fixed stop/profit levels

3. Connect to NinjaTrader - Enter your XAutoTrade webhook secret and account details

4. Create Alert - Use the strategy's alert system to send formatted JSON payloads to your XAutoTrade

webhook

5. Trade Futures & Stocks Automatically - TradingView alerts trigger real trades in your NinjaTrader account

Perfect For

- Traders wanting to automate TradingView strategies in NinjaTrader

- Users with existing ATM templates who want TradingView signal automation

- Multi-account traders managing several NinjaTrader accounts

- Anyone seeking a no-code bridge between TradingView and NinjaTrader

Requirements

- Active XAutoTrade account and subscription

- NinjaTrader 8 with XAutoTrade AddOn installed

- TradingView Premium/Pro account (for webhook alerts)

Koosha Dab's True Momentum OscillatorTrue Momentum Oscillator based on code written by SparkyFlary:

tradingview.com/u/SparkyFlary/

Different timeframe calculations added to the code.

pine script tradingbot - many ema oscillator## 🧭 **Many EMA Oscillator (TradingView Pine Script Indicator)**

*A multi-layer EMA differential oscillator for trend strength and momentum analysis*

---

### 🧩 **Overview**

The **Many EMA Oscillator** is a **TradingView Pine Script indicator** designed to help traders visualize **trend direction**, **momentum strength**, and **multi-timeframe EMA alignment** in one clean oscillator panel.

It’s a **custom EMA-based trend indicator** that shows how fast or slow different **Exponential Moving Averages (EMAs)** are expanding or contracting — helping you identify **bullish and bearish momentum shifts** early.

This **Pine Script EMA indicator** is especially useful for traders looking to combine multiple **EMA signals** into one **momentum oscillator** for better clarity and precision.

---

### ⚙️ **How It Works**

1. **Multiple EMA Layers:**

The indicator calculates seven **EMAs** (default: 20, 50, 100, 150, 200, 300) and applies a **smoothing filter** using another EMA (default smoothing = 20).

This removes short-term noise and gives a smoother, professional-grade momentum reading.

2. **EMA Gap Analysis:**

The oscillator measures the **difference between consecutive EMAs**, revealing how trend layers are separating or converging.

```

diff1 = EMA(20) - EMA(50)

diff2 = EMA(50) - EMA(100)

diff3 = EMA(100) - EMA(150)

diff4 = EMA(150) - EMA(200)

diff5 = EMA(200) - EMA(300)

```

These gaps (or “differentials”) show **trend acceleration or compression**, acting like a **multi-EMA MACD system**.

3. **Color-Coded Visualization:**

Each differential (`diff1`–`diff5`) is plotted as a **histogram**:

- 🟢 **Green bars** → EMAs expanding → bullish momentum growing

- 🔴 **Red bars** → EMAs contracting → bearish momentum or correction

This gives a clean, compact view of **trend strength** without cluttering your chart.

4. **Automatic Momentum Signals:**

- **🟡 Up Triangle** → All EMA gaps increasing → strong bullish trend alignment

- **⚪ Down Triangle** → All EMA gaps decreasing → trend weakening or bearish transition

---

### 📊 **Inputs**

| Input | Default | Description |

|-------|----------|-------------|

| `smmoth_emas` | 20 | Smoothing factor for all EMAs |

| `Length2`–`Length7` | 20–300 | Adjustable EMA periods |

| `Length21`, `Length31`, `Length41`, `Length51` | Optional | For secondary EMA analysis |

---

### 🧠 **Interpretation Guide**

| Observation | Meaning |

|--------------|----------|

| Increasing green bars | Trend acceleration and bullish continuation |

| Decreasing red bars | Trend exhaustion or sideways consolidation |

| Yellow triangles | All EMA layers aligned bullishly |

| White triangles | All EMA layers aligned bearishly |

This **EMA oscillator for TradingView** simplifies **multi-EMA trading strategies** by showing alignment strength in one place.

It works great for **swing traders**, **scalpers**, and **trend-following systems**.

---

### 🧪 **Best Practices for Use**

- Works on **all TradingView timeframes** (1m, 5m, 1h, 1D, etc.)

- Suitable for **stocks, forex, crypto, and indices**

- Combine with **RSI**, **MACD**, or **price action** confirmation

- Excellent for detecting **EMA compression zones**, **trend continuation**, or **momentum shifts**

- Can be used as part of a **multi-EMA trading strategy** or **trend strength indicator setup**

---

### 💡 **Why It Stands Out**

- 100% built in **Pine Script v6**

- Optimized for **smooth EMA transitions**

- Simple color-coded momentum visualization

- Professional-grade **multi-timeframe trend oscillator**

This is one of the most **lightweight and powerful EMA oscillators** available for TradingView users who prefer clarity over clutter.

---

### ⚠️ **Disclaimer**

This indicator is published for **educational and analytical purposes only**.

It does **not provide financial advice**, buy/sell signals, or investment recommendations.

Always backtest before live use and trade responsibly.

---

### 👨💻 **Author**

Developed by **@algo_coders**

Built in **Pine Script v6** on **TradingView**

Licensed under the (mozilla.org)

ahr999 Index BITSTAMP

Credits to discountry for making the original script.

reference:

Updates:

- Updated the historical data to use BITSTAMP:BTCUSD since BLX:BNC api is not working anymore

- Implemented a tooltip label displaying the latest AHR index value.

CM_Donchian Channels V5NOTE: this indicator was created by @ChrisMoody. I found it really useful, so I upgraded it from v3 to v5

This Indicator replicates the Donchian Channels, but with Alerts Capability

You can set up an alert for when the price breaks above the upper band or when the price breaks below the lower band

It will display respectively a green upward arrow or a red downward arrow

It is possible to change the length of the Indicator

Original Post:

Micro SuiteWhat it is: One Pine v5 indicator that stacks several tools: EMA ribbon + a color-flipping 11/34 EMA trend line, multi-timeframe RSI pressure arrows, and a Bollinger Band re-entry system that marks Top/Bottom triggers (T/B) and later “r” confirmations. It also sprinkles in 3-Line Strike, Leledc exhaustion dots, and a small “Micro Dots” engine (ATR regime + VMA filter). Alerts for all of it.

TradingView

The core signals you’ll actually use:

RSI arrows: Up arrow when current RSI(6) < 30 and selected higher-TF RSIs are also < 30; down arrow when > 70 cluster cools. Idea = stacked OB/OS “pressure.”

TradingView

Bollinger re-entry (T/B + r):

T = first close back inside upper band; B = first close back inside lower band.

r = confirmation within N bars (price takes out the trigger bar’s high/low). These bars tint so they’re easy to see.

TradingView

Trend filter: EMA-11 vs EMA-34 color flip + optional VMA trend line; helps you ignore counter-trend stabs.

TradingView

Quick playbook (how to read it):

Reversal short: See a T near the top band → get the r within your window → bonus if a down RSI arrow or a Leledc high dot shows up.

Reversal long: Mirror that with B → r, plus an up RSI arrow/Leledc low dot.

Continuation: If Micro Dot stays green (or red) and 11>34 EMA holds, ignore isolated T/B traps.

TradingView

Inputs that matter:

confirmBars for the T/B “r” window.

Which higher-TF RSIs must agree for arrows.

Show/hide and lengths for EMAs and BB.

Micro block: show dots, VMA line, and speed (Fast/Med/Slow).

TradingView

Why people like it: You get trend, momentum, and mean-revert cues on one pane with ready-made alerts, so it’s easier to build a ruleset (e.g., “only take B→r longs when 11>34 and there’s an RSI up arrow”).

TradingView

Caveats: It’s still just TA—OB/OS clusters can persist in trends; confirmations can miss V-shaped turns; and stacking signals can be late in fast markets. Pair it with risk rules (fixed R, ATR stops) and a higher-TF bias.

One-liner cheat sheet:

Longs: B → r + RSI up arrow + 11>34 (optional Micro Dot green).

Shorts: T → r + RSI down arrow + 11<34 (optional Micro Dot red).

TradingView

MA Dist% Screener [Pineify]MA Distance Screener: Multi-Asset Market Scanner for TradingView

Screen multiple symbols and multiple timeframes on TradingView with the MA Distance Screener. Compare asset prices to flexible moving average types. Visual table view, custom assets, timeframes, and MA types. Supercharge your TradingView screener, optimize your workflow, and catch opportunities across assets in real time.

Key Features

Screen up to 10 custom symbols simultaneously across four configurable timeframes.

Choose from multiple Moving Average types: EMA, SMA, WMA, HMA, RMA, VWMA for flexible market context.

Visualize real-time % distance between price and moving average per asset/timeframe in a clean, color-coded table.

Highly customizable: Set your own symbol list, timeframes, MA length and type.

Alerts for symbol/MA deviations—instantly see overbought/oversold status with intuitive background coloring.

Optimized for crypto, FX, and traditional assets – all asset types supported.

How It Works

The MA Distance Screener acts as a dynamic multi-symbol, multi-timeframe scanner. For each selected symbol and timeframe, it calculates the percentage distance between the latest close price and the selected type of moving average (EMA/SMA/etc.). This is achieved by making secure `request.security` calls per asset/timeframe combination, retrieving updated values for each matrix cell. The computed distance (%) is displayed in a color-coded table: a positive value signals price above the MA (potential trend strength), while negatives indicate price below the MA (potential weakness or retracement). Custom colors highlight extreme overbought/oversold readings for quick visual cues.

Trading Ideas and Insights

Quickly spot assets showing the largest deviation from their moving averages – ideal for mean reversion or trend-following entries.

Identify clusters of assets and timeframes lining up in overbought or oversold states; optimize entries with multi-timeframe confirmation.

Scan the market in one glance—reduce chart-hopping and never miss an opportunity when multiple assets align for signals.

The ability to scan distance-to-MA across assets and periods gives traders a statistical edge, surfacing hidden pivots, breakouts, and mean-reversion trades that single-chart analysis may miss.

How Multiple Indicators Work Together

At its core, this screener allows the trader to configure what gets scanned—pick your top 10 assets and favorite 4 timeframes. With each matrix cell, the selected MA (e.g., 14-period EMA) is recalculated, and the current price's distance (%) from that value is computed. By offering six distinct moving average algorithms (EMA, SMA, RMA, HMA, WMA, VWMA), traders can choose their preferred method, adapting the screener for trend, swing, or mean-reversion style. All values are visualized in a single table, creating a true "market dashboard" effect for real-time cross-asset assessment.

Unique Aspects

True cross-asset, cross-timeframe screening in a unified table—rare for Pine Script indicators.

Full flexibility—customizable list of assets, timeframes, and MA parameters to suit any market/trading plan.

Intuitive color-coding and table display eliminates guesswork, enabling “at-a-glance” screening and rapid decision-making.

Efficient, optimized Pine v6 codebase—minimal lag even with 40+ concurrent streams.

How to Use

Add the indicator to your TradingView chart (overlay: off, use a clean chart).

In the settings panel, enter up to 10 symbols (tickers) you want to screen—crypto, stocks, FX, or indices.

Set the 4 timeframes to scan (e.g., 1m, 5m, 15m, 1h), plus your preferred moving average length and type.

Review the results in the pop-up table, where each cell shows "% Distance" from MA for each symbol/timeframe.

Monitor table background/text color for overbought vs. oversold cues.

Customization

Symbol List: Track any asset by typing its TradingView ticker.

Timeframes: Full freedom to select 4 timeframes per scan, from 1min to monthly.

MA Config: Choose period length and MA algorithm (classic or exotic types).

Color Themes: Easily spot signals with dynamic color backgrounds and customizable thresholds.

Conclusion

The MA Distance Screener is a must-have tool for systematic traders, portfolio managers, and retail chartists seeking a true multi-asset edge. With real-time cross-checking against multiple moving averages and timeframes, it empowers faster, more confident decision-making, while reducing chart fatigue and missed setups.

Unlock new insights, catch broad and hidden opportunities, and optimize your market workflow—all in a single TradingView panel.

BOCS Channel Scalper Indicator - Mean Reversion Alert System# BOCS Channel Scalper Indicator - Mean Reversion Alert System

## WHAT THIS INDICATOR DOES:

This is a mean reversion trading indicator that identifies consolidation channels through volatility analysis and generates alert signals when price enters entry zones near channel boundaries. **This indicator version is designed for manual trading with comprehensive alert functionality.** Unlike automated strategies, this tool sends notifications (via popup, email, SMS, or webhook) when trading opportunities occur, allowing you to manually review and execute trades. The system assumes price will revert to the channel mean, identifying scalp opportunities as price reaches extremes and preparing to bounce back toward center.

## INDICATOR VS STRATEGY - KEY DISTINCTION:

**This is an INDICATOR with alerts, not an automated strategy.** It does not execute trades automatically. Instead, it:

- Displays visual signals on your chart when entry conditions are met

- Sends customizable alerts to your device/email when opportunities arise

- Shows TP/SL levels for reference but does not place orders

- Requires you to manually enter and exit positions based on signals

- Works with all TradingView subscription levels (alerts included on all plans)

**For automated trading with backtesting**, use the strategy version. For manual control with notifications, use this indicator version.

## ALERT CAPABILITIES:

This indicator includes four distinct alert conditions that can be configured independently:

**1. New Channel Formation Alert**

- Triggers when a fresh BOCS channel is identified

- Message: "New BOCS channel formed - potential scalp setup ready"

- Use this to prepare for upcoming trading opportunities

**2. Long Scalp Entry Alert**

- Fires when price touches the long entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "LONG scalp signal at 24731.75 | TP: 24743.2 | SL: 24716.5"

**3. Short Scalp Entry Alert**

- Fires when price touches the short entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "SHORT scalp signal at 24747.50 | TP: 24735.0 | SL: 24762.75"

**4. Any Entry Signal Alert**

- Combined alert for both long and short entries

- Use this if you want a single alert stream for all opportunities

- Message: "BOCS Scalp Entry: at "

**Setting Up Alerts:**

1. Add indicator to chart and configure settings

2. Click the Alert (⏰) button in TradingView toolbar

3. Select "BOCS Channel Scalper" from condition dropdown

4. Choose desired alert type (Long, Short, Any, or Channel Formation)

5. Set "Once Per Bar Close" to avoid false signals during bar formation

6. Configure delivery method (popup, email, webhook for automation platforms)

7. Save alert - it will fire automatically when conditions are met

**Alert Message Placeholders:**

Alerts use TradingView's dynamic placeholder system:

- {{ticker}} = Symbol name (e.g., NQ1!)

- {{close}} = Current price at signal

- {{plot_1}} = Calculated take profit level

- {{plot_2}} = Calculated stop loss level

These placeholders populate automatically, creating detailed notification messages without manual configuration.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This indicator is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Indicator**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the indicator ideal for active day traders who want continuous alert opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased signal frequency also means higher potential commission costs and requires disciplined trade selection when acting on alerts.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The indicator normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The indicator uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The indicator tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The indicator uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. Visual markers (arrows and labels) appear on chart, and configured alerts fire immediately.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents alert spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long alert will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The indicator includes a multi-timeframe ATR filter to avoid alerts during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while viewing 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Alerts enabled

- If ATR < threshold: No alerts fire

This prevents notifications during dead zones where mean reversion is unreliable due to insufficient price movement. The ATR status is displayed in the info table with visual confirmation (✓ or ✗).

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. These levels are displayed as visual lines with labels and included in alert messages for reference when manually placing orders.

### Stop Loss Placement:

Stop losses are calculated just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. SL levels are displayed on chart and included in alert notifications as suggested stop placement.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

## INPUT PARAMETERS:

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long alert generation on/off

- **Enable Short Scalps**: Toggle short alert generation on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between alerts (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for alert enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time indicator status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Long Color**: Customize long signal color (default: darker green for readability)

- **Short Color**: Customize short signal color (default: red)

- **TP/SL Colors**: Customize take profit and stop loss line colors

- **Line Length**: Visual length of TP/SL reference lines (5-200 bars)

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short alerts

- **TP/SL reference lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing channel status, last signal, entry/TP/SL prices, risk/reward ratio, and ATR filter status

- **Visual confirmation** when alerts fire via on-chart markers synchronized with notifications

## HOW TO USE:

### For 1-3 Minute Scalping with Alerts (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars to reduce alert spam

- **Alert Setup**: Configure "Any Entry Signal" for combined long/short notifications

- **Execution**: When alert fires, verify chart visuals, then manually place limit order at entry zone with provided TP/SL levels

### For 5-15 Minute Day Trading with Alerts:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- **Alert Setup**: Configure separate "Long Scalp Entry" and "Short Scalp Entry" alerts if you trade directionally based on bias

- **Execution**: Review channel structure on alert, confirm ATR filter shows ✓, then enter manually

### For 30-60 Minute Swing Scalping with Alerts:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- **Alert Setup**: Use "New Channel Formation" to prepare for setups, then "Any Entry Signal" for execution alerts

- **Execution**: Larger timeframes allow more analysis time between alert and entry

### Webhook Integration for Semi-Automation:

- Configure alert webhook URL to connect with platforms like TradersPost, TradingView Paper Trading, or custom automation

- Alert message includes all necessary order parameters (direction, entry, TP, SL)

- Webhook receives structured data when signal fires

- External platform can auto-execute based on alert payload

- Still maintains manual oversight vs full strategy automation

## USAGE CONSIDERATIONS:

- **Manual Discipline Required**: Alerts provide opportunities but execution requires judgment. Not all alerts should be taken - consider market context, trend, and channel quality

- **Alert Timing**: Alerts fire on bar close by default. Ensure "Once Per Bar Close" is selected to avoid false signals during bar formation

- **Notification Delivery**: Mobile/email alerts may have 1-3 second delay. For immediate execution, use desktop popups or webhook automation

- **Cooldown Necessity**: Without cooldown, rapidly touching price action can generate excessive alerts. Start with 3-bar cooldown and adjust based on alert volume

- **ATR Filter Impact**: Enabling ATR filter dramatically reduces alert count but improves quality. Track filter status in info table to understand when you're receiving fewer alerts

- **Commission Awareness**: High alert frequency means high potential trade count. Calculate if your commission structure supports frequent scalping before acting on all alerts

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features are not included in this indicator version. Multi-timeframe ATR requires higher-tier TradingView subscription for request.security() functionality on timeframes below chart timeframe.

## KNOWN LIMITATIONS:

- **Indicator does not execute trades** - alerts are informational only; you must manually place all orders

- **Alert delivery depends on TradingView infrastructure** - delays or failures possible during platform issues

- **No position tracking** - indicator doesn't know if you're in a trade; you must manage open positions independently

- **TP/SL levels are reference only** - you must manually set these on your broker platform; they are not live orders

- **Immediate touch entry can generate many alerts** in choppy zones without adequate cooldown

- **Channel deletion at 10-tick breaks** may be too aggressive or lenient depending on instrument tick size

- **ATR filter from lower timeframes** requires TradingView Premium/Pro+ for request.security()

- **Mean reversion logic fails** in strong breakout scenarios - alerts will fire but trades may hit stops

- **No partial closing capability** - full position management is manual; you determine scaling out

- **Alerts do not account for gaps** or overnight price changes; morning alerts may be stale

## RISK DISCLOSURE:

Trading involves substantial risk of loss. This indicator provides signals for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Mean reversion strategies can experience extended drawdowns during trending markets. Alerts are not guaranteed to be profitable and should be combined with your own analysis. Stop losses may not fill at intended levels during extreme volatility or gaps. Never trade with capital you cannot afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Always verify alerts against current market conditions before executing trades manually.

## ACKNOWLEDGMENT & CREDITS:

This indicator is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based alert generation, comprehensive alert condition system with customizable notifications, multi-timeframe ATR volatility filtering, cooldown period for alert management, dual TP methods (fixed points vs channel percentage), visual TP/SL reference lines, and real-time status monitoring table. This indicator version is specifically designed for manual traders who prefer alert-based decision making over automated execution.

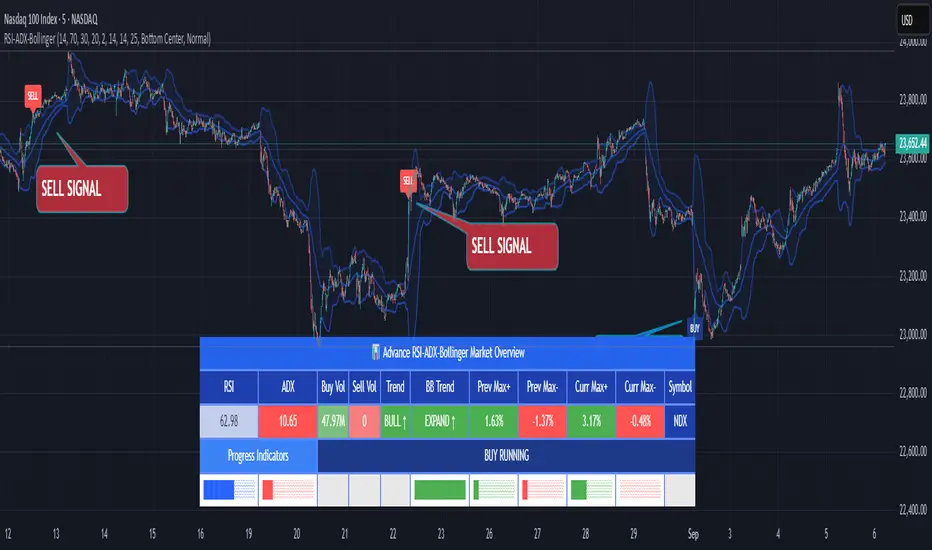

RSI ADX Bollinger Analysis High-level purpose and design philosophy

This indicator — RSI-ADX-Bollinger Analysis — is a compact, educational market-analysis toolkit that blends momentum (RSI), trend strength (ADX), volatility structure (Bollinger Bands) and simple volumetrics to provide traders a snapshot of market condition and trade idea quality. The design philosophy is explicit and layered: use each component to answer a different question about price action (momentum, conviction, volatility, participation), then combine answers to form a more robust, explainable signal. The mashup is intended for analysis and learning, not automatic execution: it surfaces the why behind signals so traders can test, learn and apply rules with risk management.

________________________________________

What each indicator contributes (component-by-component)

RSI (Relative Strength Index) — role and behavior: RSI measures short-term momentum by comparing recent gains to recent losses. A high RSI (near or above the overbought threshold) indicates strong recent buying pressure and potential exhaustion if price is extended. A low RSI (near or below the oversold threshold) indicates strong recent selling pressure and potential exhaustion or a value area for mean-reversion. In this dashboard RSI is used as the primary momentum trigger: it helps identify whether price is locally over-extended on the buy or sell side.

ADX (Average Directional Index) — role and behavior: ADX measures trend strength independently of direction. When ADX rises above a chosen threshold (e.g., 25), it signals that the market is trending with conviction; ADX below the threshold suggests range or weak trend. Because patterns and momentum signals perform differently in trending vs. ranging markets, ADX is used here as a filter: only when ADX indicates sufficient directional strength does the system treat RSI+BB breakouts as meaningful trade candidates.

Bollinger Bands — role and behavior: Bollinger Bands (20-period basis ± N standard deviations) show volatility envelope and relative price position vs. a volatility-adjusted mean. Price outside the upper band suggests pronounced extension relative to recent volatility; price outside the lower band suggests extended weakness. A band expansion (increasing width) signals volatility breakout potential; contraction signals range-bound conditions and potential squeeze. In this dashboard, Bollinger Bands provide the volatility/structural context: RSI extremes plus price beyond the band imply a stronger, volatility-backed move.

Volume split & basic MA trend — role and behavior: Buy-like and sell-like volume (simple heuristic using close>open or closeopen) or sell-like (close1.2 for validation and compare win rate and expectancy.

4. TF alignment: Accept signals only when higher timeframe (e.g., 4h) trend agrees — compare results.

5. Parameter sensitivity: Vary RSI threshold (70/30 vs 80/20), Bollinger stddev (2 vs 2.5), and ADX threshold (25 vs 30) and measure stability of results.

These exercises teach both statistical thinking and the specific failure modes of the mashup.

________________________________________

Limitations, failure modes and caveats (explicit & teachable)

• ADX and Bollinger measures lag during fast-moving news events — signals can be late or wrong during earnings, macro shocks, or illiquid sessions.

• Volume classification by open/close is a heuristic; it does not equal TAPEDATA, footprint or signed volume. Use it as supportive evidence, not definitive proof.

• RSI can remain overbought or oversold for extended stretches in persistent trends — relying solely on RSI extremes without ADX or BB context invites large drawdowns.

• Small-cap or low-liquidity instruments yield noisy band behavior and unreliable volume ratios.

Being explicit about these limitations is a strong point in a TradingView description — it demonstrates transparency and educational intent.

________________________________________

Originality & mashup justification (text you can paste)

This script intentionally combines classical momentum (RSI), volatility envelope (Bollinger Bands) and trend-strength (ADX) because each indicator answers a different and complementary question: RSI answers is price locally extreme?, Bollinger answers is price outside normal volatility?, and ADX answers is the market moving with conviction?. Volume participation then acts as a practical check for real market involvement. This combination is not a simple “indicator mashup”; it is a designed ensemble where each element reduces the others’ failure modes and together produce a teachable, testable signal framework. The script’s purpose is educational and analytical — to show traders how to interpret the interplay of momentum, volatility, and trend strength.

________________________________________

TradingView publication guidance & compliance checklist

To satisfy TradingView rules about mashups and descriptions, include the following items in your script description (without exposing source code):

1. Purpose statement: One or two lines describing the script’s objective (educational multi-indicator market overview and idea filter).

2. Component list: Name the major modules (RSI, Bollinger Bands, ADX, volume heuristic, SMA trend checks, signal tracking) and one-sentence reason for each.

3. How they interact: A succinct non-code explanation: “RSI finds momentum extremes; Bollinger confirms volatility expansion; ADX confirms trend strength; all three must align for a BUY/SELL.”

4. Inputs: List adjustable inputs (RSI length and thresholds, BB length & stddev, ADX threshold & smoothing, volume MA, table position/size).

5. Usage instructions: Short workflow (check TF alignment → confirm participation → define stop & R:R → backtest).

6. Limitations & assumptions: Explicitly state volume is approximated, ADX has lag, and avoid promising guaranteed profits.

7. Non-promotional language: No external contact info, ads, claims of exclusivity or guaranteed outcomes.

8. Trademark clause: If you used trademark symbols, remove or provide registration proof.

9. Risk disclaimer: Add the copy-ready disclaimer below.

This matches TradingView’s request for meaningful descriptions that explain originality and inter-component reasoning.

________________________________________

Copy-ready short publication description (paste into TradingView)

Advanced RSI-ADX-Bollinger Market Overview — educational multi-indicator dashboard. This script combines RSI (momentum extremes), Bollinger Bands (volatility envelope and band expansion), ADX (trend strength), simple SMA trend bias and a basic buy/sell volume heuristic to surface high-quality idea candidates. Signals require alignment of momentum, volatility expansion and rising ADX; volume participation is displayed to support signal confidence. Inputs are configurable (RSI length/levels, BB length/stddev, ADX length/threshold, volume MA, display options). This tool is intended for analysis and learning — not for automated execution. Users should back test and apply robust risk management. Limitations: volume classification here is a heuristic (close>open), ADX and BB measures lag in fast news events, and results vary by instrument liquidity.

________________________________________

Copy-ready risk & misuse disclaimer (paste into description or help file)

This script is provided for educational and analytical purposes only and does not constitute financial or investment advice. It does not guarantee profits. Indicators are heuristics and may give false or late signals; always back test and paper-trade before using real capital. The author is not responsible for trading losses resulting from the use or misuse of this indicator. Use proper position sizing and risk controls.

________________________________________

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Back test thoroughly and use proper risk management.

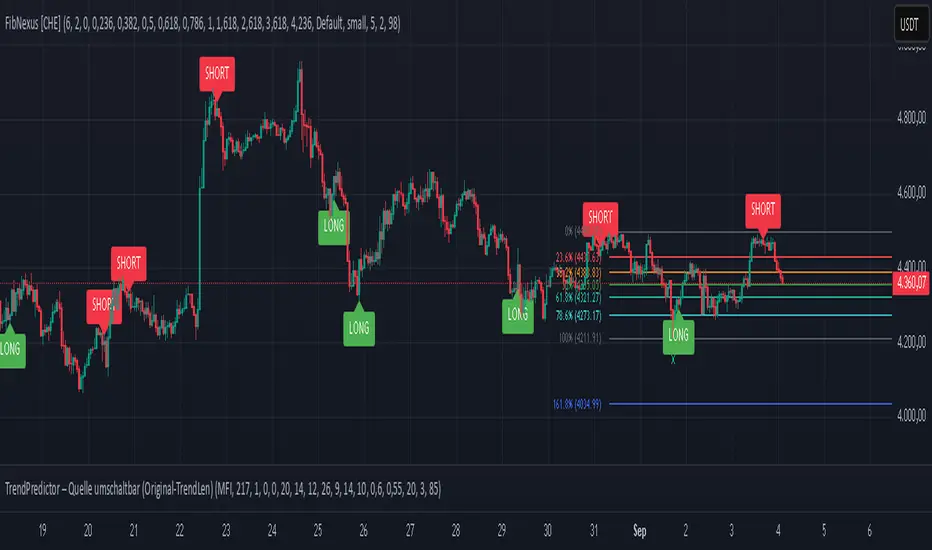

FibNexus [CHE]FibNexus — Auto-Fibonacci with Adaptive TrendLen + TFRSI Triggers

What it is.

FibNexus is a chart overlay that auto-anchors Fibonacci levels to the most relevant swing range without any manual timeframe picking. It does this by computing an adaptive trend length (“TrendLen”) from recent price behavior, then drawing retracements/extensions from the detected swing High/Low. A built-in TFRSI module adds LONG/SHORT triggers and ready-made alerts.

What makes FibNexus different (the TrendLen edge)

Most Fibonacci tools either (a) use fixed lookbacks or (b) force you to choose a higher reference timeframe (or a multiplier of it) and then place Fibs on those higher-TF swings. Your earlier Ultimate Fibonacci Trading Tool \ follows that higher-reference approach (auto TF, multiplier, or manual) and emphasizes custom level/label options. ( )

FibNexus flips that workflow:

* It doesn’t rely on a higher timeframe or a static lookback.

* Instead, it measures multiple window lengths inside the current chart timeframe and selects the one that best fits the data right now.

* From that data-driven window, it automatically finds the most recent swing high & low and draws the entire Fib stack from there.

* When the statistically “best” window changes, anchors update once, labels refresh cleanly, and then lines just extend to the right on each new bar.

Result: No more guesswork about “which timeframe or lookback should I use?”—FibNexus adapts the anchors to market conditions and keeps the drawing noise low.

How TrendLen works (transparent, deterministic)

1. Scan windows: The script evaluates a series of lookbacks (10, 20, …, 500 bars).

2. Score by correlation: For each window, it computes the correlation between price and its lagged version and picks the window with the highest correlation (the strongest, most self-consistent trend segment).

3. Anchor the swing: On a confirmed bar and only when TrendLen changes, it scans the last `TrendLen` bars to capture the highest high and lowest low and marks them with “X”.

4. Draw once, extend later: It deletes the old Fib objects, redraws the active levels from those anchors, and from then on extends the lines to the right as new bars print (no redraw spam).

This makes FibNexus responsive (it adapts when the structure shifts) and quiet (it doesn’t constantly repaint Fibs).

Fibonacci engine (levels, labels, direction)

* Retracements: 0.000 · 0.236 · 0.382 · 0.500 · 0.618 · 0.786 · 1.000

* Extensions: 1.618 · 2.618 · 3.618 · 4.236

* Label styles: *Default* (percent + price), *None*, *Percentage*, *Price*

* Label sizing: *tiny → huge*

* Bull/Bear context: Direction is inferred from mid-range positioning; prices are projected accordingly (retracement vs. extension math is handled for both cases).

* Selective toggles: You can show/hide any level and color it independently.

Momentum & signals (TFRSI module)

FibNexus embeds your TFRSI (“The Forbidden RSI \ ”) as the momentum/trigger layer. TFRSI is your open-source oscillator published on TradingView and designed for fast, normalized momentum readouts with customizable length/smoothing. ( )

* Defaults: `TFRSI length = 6`, `signal smoothing = 2`

* Triggers:

* LONG when TFRSI crosses up through the Long level (default 2.0)

* SHORT when TFRSI crosses down through the Short level (default 98.0)

* On-chart labels: Green LONG under the bar, red SHORT above the bar.

* Spam control: Keep only the N most recent labels to avoid clutter.

* Confirmed bars only: Signals/labels finalize at bar close to reduce flicker.

Alerts (ready for TradingView)

* LONG signal (TFRSI crossover)

* SHORT signal (TFRSI crossunder)

* TrendLen changed (anchors/Fibs recalculated)

* Price crossed a Fib level (any active level)

Use the provided `alertcondition(...)` entries in the TV dialog. Optionally enable instant `alert()` calls with verbose text (avoid duplicates if you also add alertconditions).

Typical use-cases & playbook

* Level reaction trading: In trends, watch 0.382 / 0.5 / 0.618 for reaction. A TFRSI up-cross near a retracement in an uptrend is a straightforward continuation setup; the opposite applies in downtrends.

* Breakout objectives: After clearing the 1.000 line (old swing), 1.618 is a common first extension target; beyond that, 2.618/3.618/4.236 map stretch objectives.

* Chop control: In range conditions, keep signals conservative (e.g., stick with the tight defaults 2.0/98.0 or raise thresholds). Always seek confluence (candlesticks, volume, HTF bias).

* Less micromanagement: You don’t need to babysit timeframe selection or anchors—TrendLen recomputes only when the data say so.

Inputs (by group)

* Core: TFRSI length & smoothing.

* Fibonacci Levels: Per-level toggles, numeric values, colors.

* Fibonacci Labels: Style (percentage/price/both/none) and size.

* Signals: Max number of visible LONG/SHORT labels (or 0 = off).

* TFRSI Trigger: Long/Short thresholds (defaults 2.0 / 98.0).

* Alerts: Master enable, per-event toggles, optional instant `alert()`.

Performance & UX

* Overlay indicator; efficient object handling.

* Clean redraw policy: Full re-draw only when TrendLen changes; otherwise Fibs extend horizontally.

* Clarity: Auto-marked swing anchors (“X”), configurable labels/colors.

Credits & references

* TFRSI – “The Forbidden RSI \ ” (open-source publication and description on TradingView). Used here as the momentum basis.

* “Ultimate Fibonacci Trading Tool \ ” (your earlier open-source tool on TradingView). Focuses on higher-reference timeframe selection (auto/multiplier/manual) and rich labeling controls; FibNexus replaces the fixed/higher-TF anchor logic with adaptive TrendLen in the current timeframe.

Risk disclaimer

This indicator is for educational/information purposes only and is not financial advice. No performance guarantees; past behavior does not predict future results. Trading involves substantial risk (including total loss). Always do your own research, test on demo, use risk management, and consult a licensed advisor where appropriate. Use at your own risk.

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence with FibNexus ! 🚀

Happy trading

Chervolino

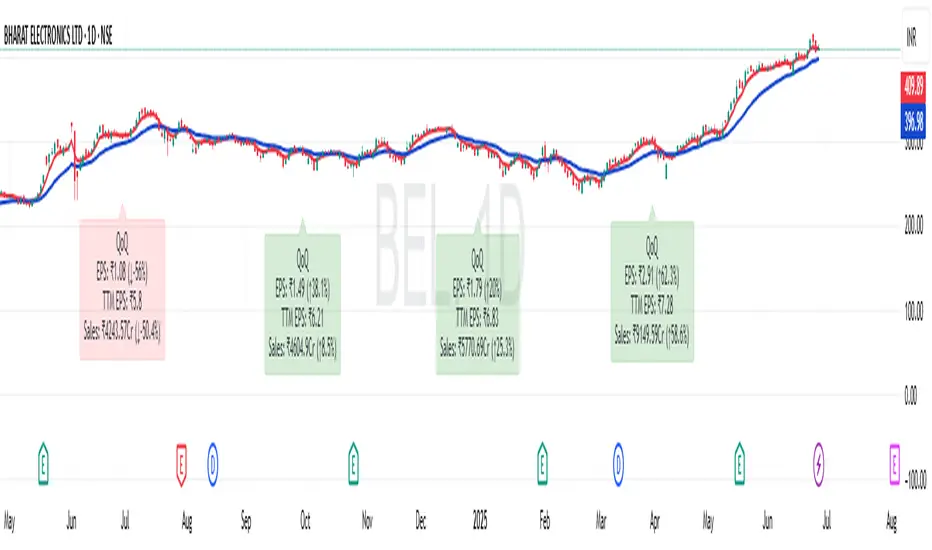

EPS and Sales Magic Indicator V2EPS and Sales Magic Indicator V2

EPS and Sales Magic Indicator V2

Short Title: EPS V2

Author: Trading_Tomm

Platform: TradingView (Pine Script v6)

License: Free for public use under fair usage guidelines

Overview

The EPS and Sales Magic Indicator V2 is a powerful stock fundamental visualization tool built specifically for TradingView users who wish to incorporate earnings intelligence directly onto their price chart. Designed and developed by Trading_Tomm, this upgraded version of the original 'EPS and Sales Magic Indicator' includes an enriched and more insightful presentation of company performance metrics — now with TTM EPS support, advanced color-coding, label sizing, and refined control options.

This indicator is tailored for retail traders, swing investors, and long-term fundamental analysts who need to view Quarter-over-Quarter (QoQ) earnings and revenue changes directly on the price chart without switching tabs or breaking focus.

What Does It Display?

The EPS and Sales Magic Indicator V2 intelligently detects quarterly financial updates and displays the following data points via labels:

1. EPS (Earnings Per Share) – Current Quarterly Value

This is the most recent Diluted EPS published by the company, fetched using TradingView’s request.financial() function.

Displayed in the format: EPS: ₹20.45

2. EPS QoQ Percentage Change

Shows the percentage change in EPS compared to the previous quarter.

Highlights improvement or decline using arrows (up for improvement, down for decline).

Displayed in the format: EPS: ₹20.45 (up 15.3 percent)

3. Sales (Revenue) – Current Quarterly Value

Fetches and displays Total Revenue of the company in ₹Crores for easier Indian-market readability.

Displayed in the format: Sales: ₹460Cr

4. Sales QoQ Percentage Change

Measures and presents the quarter-over-quarter percentage change in total revenue.

Uses arrows to indicate growth or contraction.

Displayed in the format: Sales: ₹460Cr (down 3.8 percent)

5. EPS TTM (Trailing Twelve Months)

You now get the TTM EPS — the sum of the last four quarterly EPS values.

This value provides a better long-term earnings snapshot compared to a single quarter.

Displayed in the format: TTM EPS: ₹78.12

All of these values are automatically calculated and displayed only on the bars where a new financial report is detected, keeping your chart clean and insightful.

Customization Features

This indicator is built with user control in mind, allowing you to personalize how and what you want to see:

Show EPS in Label: Enable or disable the display of EPS and EPS QoQ values.

Show Sales in Label: Toggle the visibility of revenue and sales change percentage.

Color Options for Label Themes: The label background color is automatically determined based on performance.

Green: Both EPS and Sales increased QoQ.

Red: Both decreased.

Orange: One increased and the other decreased.

Gray: Default color (if values are unavailable or mixed).

Label Text Size: Choose from Tiny, Small (default), or Normal.

Visual Design

Placement: The labels are positioned just below the candlesticks using yloc.belowbar, so they do not obstruct price action or interfere with technical indicators.

Anchor: Aligned precisely with the financial reporting bars to maintain clarity in historical comparisons.

Background Style: Clean, semi-transparent styling with soft text colors for comfortable viewing.

How It Works

The indicator relies on TradingView’s powerful request.financial() function to extract fiscal quarterly financials (FQ). Internally, it uses detection logic to identify fresh data updates by comparing current vs. previous values, arithmetic to compute QoQ percentage changes in EPS and Sales, logic to build formatted labels dynamically based on user selections, and conditional color and sizing logic to enhance interpretability.

Use Cases

For Long-Term Investors: Quickly identify if a company’s profitability and revenue are improving over time.

For Swing Traders: Combine recent earnings trends with price action to evaluate if post-result momentum has real backing.

For Technical and Fundamental Traders: Layer it with moving averages, RSI, or volume to create a hybrid analysis environment.

Limitations and Notes

Financial data is provided by TradingView’s financial API, and occasional missing values may occur for less-covered stocks.

This tool does not repaint but depends on the timing of the official financial updates.

All values are rounded and formatted to prioritize readability.

Works best on Daily or higher timeframes (weekly or monthly also supported).

License and Fair Use

This script is free to use and share under TradingView’s open-use guidelines. You may copy, fork, and build upon this indicator for personal or educational purposes, but commercial usage requires attribution to the author: Trading_Tomm.

Future Enhancements (Planned)

Addition of Net Profit (QoQ and TTM)

Inclusion of Operating Margin, Profit Margin, and Book Value

Option to switch between numeric and graphical display (table mode)

Alerts on extreme earnings deviation or sales slumps

Final Thoughts

The EPS and Sales Magic Indicator V2 represents a clean, visual, and smart way to monitor a company’s core performance from your chart screen. It helps you align fundamental strength with technical strategies and provides instant financial clarity, which is especially vital in today’s fast-moving markets.

Whether you’re preparing for an earnings season or scanning past performance to pick your next investment, this indicator saves time, enhances insights, and sharpens decisions.

SIP Evaluator and Screener [Trendoscope®]The SIP Evaluator and Screener is a Pine Script indicator designed for TradingView to calculate and visualize Systematic Investment Plan (SIP) returns across multiple investment instruments. It is tailored for use in TradingView's screener, enabling users to evaluate SIP performance for various assets efficiently.

🎲 How SIP Works

A Systematic Investment Plan (SIP) is an investment strategy where a fixed amount is invested at regular intervals (e.g., monthly or weekly) into a financial instrument, such as stocks, mutual funds, or ETFs. The goal is to build wealth over time by leveraging the power of compounding and mitigating the impact of market volatility through disciplined, consistent investing. Here’s a breakdown of how SIPs function:

Regular Investments : In an SIP, an investor commits to investing a fixed sum at predefined intervals, regardless of market conditions. This consistency helps inculcate a habit of saving and investing.

Cost Averaging : By investing a fixed amount regularly, investors purchase more units when prices are low and fewer units when prices are high. This approach, known as dollar-cost averaging, reduces the average cost per unit over time and mitigates the risk of investing a large amount at a peak price.

Compounding Benefits : Returns generated from the invested amount (e.g., capital gains or dividends) are reinvested, leading to exponential growth over the long term. The longer the investment horizon, the greater the potential for compounding to amplify returns.

Dividend Reinvestment : In some SIPs, dividends received from the underlying asset can be reinvested to purchase additional units, further enhancing returns. Taxes on dividends, if applicable, may reduce the reinvested amount.

Flexibility and Accessibility : SIPs allow investors to start with small amounts, making them accessible to a wide range of individuals. They also offer flexibility in terms of investment frequency and the ability to adjust or pause contributions.

In the context of the SIP Evaluator and Screener , the script simulates an SIP by calculating the number of units purchased with each fixed investment, factoring in commissions, dividends, taxes and the chosen price reference (e.g., open, close, or average prices). It tracks the cumulative investment, equity value, and dividends over time, providing a clear picture of how an SIP would perform for a given instrument. This helps users understand the impact of regular investing and make informed decisions when comparing different assets in TradingView’s screener. It offers insights into key metrics such as total invested amount, dividends received, equity value, and the number of installments, making it a valuable resource for investors and traders interested in understanding long-term investment outcomes.

🎲 Key Features

Customizable Investment Parameters: Users can define the recurring investment amount, price reference (e.g., open, close, HL2, HLC3, OHLC4), and whether fractional quantities are allowed.

Commission Handling: Supports both fixed and percentage-based commission types, adjusting calculations accordingly.

Dividend Reinvestment: Optionally reinvests dividends after a user-specified period, with the ability to apply tax on dividends.

Time-Bound Analysis: Allows users to set a start year for the analysis, enabling historical performance evaluation.

Flexible Dividend Periods: Dividends can be evaluated based on bars, days, weeks, or months.

Visual Outputs: Plots key metrics like total invested amount, dividends, equity value, and remainder, with customizable display options for clarity in the data window and chart.

🎲 Using the script as an indicator on Tradingview Supercharts

In order to use the indicator on charts, do the following.

Load the instrument of your choice - Preferably a stable stocks, ETFs.

Chose monthly timeframe as lower timeframes are insignificant in this type of investment strategy

Load the indicator SIP Evaluator and Screener and set the input parameters as per your preference.

Indicator plots, investment value, dividends and equity on the chart.

🎲 Visualizations

Installments : Displays the number of SIP installments (gray line, visible in the data window).

Invested Amount : Shows the cumulative amount invested, excluding reinvested dividends (blue area plot).

Dividends : Tracks total dividends received (green area plot).

Equity : Represents the current market value of the investment based on the closing price (purple area plot).

Remainder : Indicates any uninvested cash after each installment (gray line, visible in the data window).

🎲 Deep dive into the settings

The SIP Evaluator and Screener offers a range of customizable settings to tailor the Systematic Investment Plan (SIP) simulation to your preferences. Below is an explanation of each setting, its purpose, and how it impacts the analysis:

🎯 Duration

Start Year (Default: 2020) : Specifies the year from which the SIP calculations begin. When Start Year is enabled via the timebound option, the script only considers data from the specified year onward. This is useful for analyzing historical SIP performance over a defined period. If disabled, the script uses all available data.

Timebound (Default: False) : A toggle to enable or disable the Start Year restriction. When set to False, the SIP calculation starts from the earliest available data for the instrument.

🎯 Investment

Recurring Investment (Default: 1000.0) : The fixed amount invested in each SIP installment (e.g., $1000 per period). This represents the regular contribution to the SIP and directly influences the total invested amount and quantity purchased.

Allow Fractional Qty (Default: True) : When enabled, the script allows the purchase of fractional units (e.g., 2.35 shares). If disabled, only whole units are purchased (e.g., 2 shares), with any remaining funds carried forward as Remainder. This setting impacts the precision of investment allocation.

Price Reference (Default: OPEN): Determines the price used for purchasing units in each SIP installment. Options include:

OPEN : Uses the opening price of the bar.

CLOSE : Uses the closing price of the bar.

HL2 : Uses the average of the high and low prices.

HLC3 : Uses the average of the high, low, and close prices.

OHLC4 : Uses the average of the open, high, low, and close prices. This setting affects the cost basis of each purchase and, consequently, the total quantity and equity value.

🎯 Commission

Commission (Default: 3) : The commission charged per SIP installment, expressed as either a fixed amount (e.g., $3) or a percentage (e.g., 3% of the investment). This reduces the amount available for purchasing units.

Commission Type (Default: Fixed) : Specifies how the commission is calculated: