Pi Cycle Top Indicator for BTCUSDThis indicator adds the Pi Cycle Top Indicator for BTCUSD to your chart.

Indicator Overview

The Pi Cycle Top Indicator has historically been effective in picking out the timing of market cycle highs to within 3 days. It uses the 111 day moving average (111DMA) and a newly created multiple of the 350 day moving average, the 350DMA x 2.

For the past three market cycles, when the 111DMA moves up and crosses the 350DMA x 2 we see that it coincides with the price of Bitcoin peaking. It is also interesting to note that 350 / 111 is 3.153, which is very close to Pi = 3.142. In fact, it is the closest we can get to Pi when dividing 350 by another whole number.

It once again demonstrates the cyclical nature of Bitcoin price action over long time frames. Though in this instance it does so with a high degree of accuracy over the past 7 years.

How It Can Be Used

Pi Cycle Top is useful to indicate when the market is very overheated. So overheated that the shorter term moving average, which is the 111 day moving average, has reached a x2 multiple of the 350 day moving average. Historically it has proved advantageous to sell Bitcoin at this time in Bitcoin's price cycles.

ค้นหาในสคริปต์สำหรับ "bitcoin"

Pi Cycle Top IndicatorIndicator Overview

The Pi Cycle Top Indicator has historically been effective in picking out the timing of market cycle highs to within 3 days.

It uses the 111 day moving average (111DMA) and a newly created multiple of the 350 day moving average, the 350DMA x 2.

Note: The multiple is of the price values of the 350DMA not the number of days.

For the past three market cycles, when the 111DMA moves up and crosses the 350DMA x 2 we see that it coincides with the price of Bitcoin peaking.

It is also interesting to note that 350 / 111 is 3.153, which is very close to Pi = 3.142. In fact, it is the closest we can get to Pi when dividing 350 by another whole number.

It once again demonstrates the cyclical nature of Bitcoin price action over long time frames. Though in this instance it does so with a high degree of accuracy over the past 7 years.

How It Can Be Used

Pi Cycle Top is useful to indicate when the market is very overheated. So overheated that the shorter term moving average, which is the 111 day moving average, has reached a x2 multiple of the 350 day moving average. Historically it has proved advantageous to sell Bitcoin at this time in Bitcoin's price cycles.

Created By

Philip Swift

Combo VIX and DXYHello traders

It's been a while :)

I wanted to share a cool script that you can use for any asset class.

The script isn't really special - though what it displays is super helpful

Volatility Index $VIX

(Source: Wikipedia)

VIX is the ticker symbol and the popular name for the Chicago Board Options Exchange's CBOE Volatility Index, a popular measure of the stock market's expectation of volatility based on S&P 500 index options.

It is calculated and disseminated on a real-time basis by the CBOE, and is often referred to as the fear index or fear gauge.

I consider that a $VIX above 30% is a very bearish signal.

Above 30% translating investors selling in masse their assets. #blood #on #the #street

Dollar Index $DXY

(Source: Wikipedia)

The U.S. Dollar Index (USDX, DXY, DX, or, informally, the "Dixie") is an index (or measure) of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies.

The Index goes up when the U.S. dollar gains "strength" (value) when compared to other currencies.

The index is designed, maintained, and published by ICE (Intercontinental Exchange, Inc.), with the name "U.S. Dollar Index" a registered trademark.

It is a weighted geometric mean of the dollar's value relative to following select currencies:

Euro (EUR), 57.6% weight

Japanese yen (JPY) 13.6% weight

Pound sterling (GBP), 11.9% weight

Canadian dollar (CAD), 9.1% weight

Swedish krona (SEK), 4.2% weight

Swiss franc (CHF) 3.6% weight

In "bear markets", the $DXY usually goes up.

People are selling their hard assets to get some $USD in return - pumping the $DXY higher

Corollary

I'm not sure which one happens first between a bearish $DXY or bearish $DXY... though both are usually correlated

If:

- $VIX goes above 30%, usually $DXY increases and assets versus the good old' $USD drop

- $VIX goes below 30%, usually $DXY decreases and assets versus the good old' $USD increases

This is a nice lever effect between both the $VIX, $DXY and the assets versus the $USD

That's being said, I don't only use those 2 information to enter in a trade.

It gives me though a strong confirmation whenever I'm long or short

Imagine I get a LONG signal but the combo $VIX + $DXY is bearish... this tells me to be cautious and to:

- enter at a pullback

- protect my position quickly at breakeven

- take my profit quick

For a mega bull market (some called it hyperinflation), you want your fiat to drop in value for the counter-asset to increase in value.

And before you ask.... yes I look at what $DXY is doing before taking a trade on $BTCUSD :)

In other words, $DXY going down is quite bullish for Bitcoin.

Settings and Alerts

The settings by default are the ones I use for my trading.

The background colors will be colored whenever the COMBO is bullish (green) or bearish (red)

Alerts are enabled using the brand new alert function published last week by @TradingView

That's it for today, I hope you'll like it :)

PS: In this chart above, I'm using the Supertrend indicator from @KivancOzbilgic

Dave

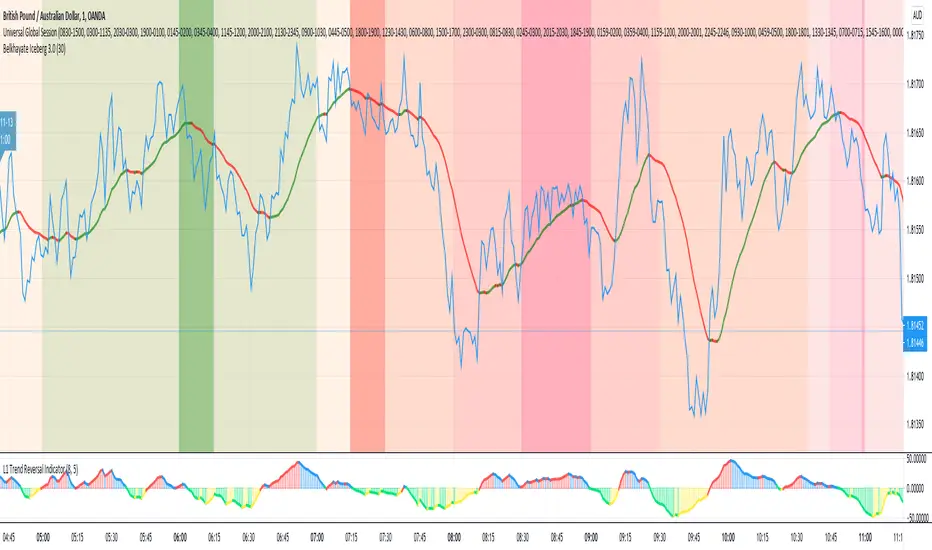

Universal Global SessionUniversal Global Session

This Script combines the world sessions of: Stocks, Forex, Bitcoin Kill Zones, strategic points, all configurable, in a single Script, to capitalize the opening and closing times of global exchanges as investment assets, becoming an Universal Global Session .

It is based on the great work of @oscarvs ( BITCOIN KILL ZONES v2 ) and the scripts of @ChrisMoody. Thank you Oscar and Chris for your excellent judgment and great work.

At the end of this writing you can find all the internet references of the extensive documentation that I present here. To maximize your benefits in the use of this Script, I recommend that you read the entire document to create an objective and practical criterion.

All the hours of the different exchanges are presented at GMT -6. In Market24hClock you can adjust it to your preferences.

After a deep investigation I have been able to show that the different world sessions reveal underlying investment cycles, where it is possible to find sustained changes in the nominal behavior of the trend before the passage from one session to another and in the natural overlaps between the sessions. These underlying movements generally occur 15 minutes before the start, close or overlap of the session, when the session properly starts and also 15 minutes after respectively. Therefore, this script is designed to highlight these particular trending behaviors. Try it, discover your own conclusions and let me know in the notes, thank you.

Foreign Exchange Market Hours

It is the schedule by which currency market participants can buy, sell, trade and speculate on currencies all over the world. It is open 24 hours a day during working days and closes on weekends, thanks to the fact that operations are carried out through a network of information systems, instead of physical exchanges that close at a certain time. It opens Monday morning at 8 am local time in Sydney —Australia— (which is equivalent to Sunday night at 7 pm, in New York City —United States—, according to Eastern Standard Time), and It closes at 5pm local time in New York City (which is equivalent to 6am Saturday morning in Sydney).

The Forex market is decentralized and driven by local sessions, where the hours of Forex trading are based on the opening range of each active country, becoming an efficient transfer mechanism for all participants. Four territories in particular stand out: Sydney, Tokyo, London and New York, where the highest volume of operations occurs when the sessions in London and New York overlap. Furthermore, Europe is complemented by major financial centers such as Paris, Frankfurt and Zurich. Each day of forex trading begins with the opening of Australia, then Asia, followed by Europe, and finally North America. As markets in one region close, another opens - or has already opened - and continues to trade in the currency market. The seven most traded currencies in the world are: the US dollar, the euro, the Japanese yen, the British pound, the Australian dollar, the Canadian dollar, and the New Zealand dollar.

Currencies are needed around the world for international trade, this means that operations are not dominated by a single exchange market, but rather involve a global network of brokers from around the world, such as banks, commercial companies, central banks, companies investment management, hedge funds, as well as retail forex brokers and global investors. Because this market operates in multiple time zones, it can be accessed at any time except during the weekend, therefore, there is continuously at least one open market and there are some hours of overlap between the closing of the market of one region and the opening of another. The international scope of currency trading means that there are always traders around the world making and satisfying demands for a particular currency.

The market involves a global network of exchanges and brokers from around the world, although time zones overlap, the generally accepted time zone for each region is as follows:

Sydney 5pm to 2am EST (10pm to 7am UTC)

London 3am to 12 noon EST (8pm to 5pm UTC)

New York 8am to 5pm EST (1pm to 10pm UTC)

Tokyo 7pm to 4am EST (12am to 9am UTC)

Trading Session

A financial asset trading session refers to a period of time that coincides with the daytime trading hours for a given location, it is a business day in the local financial market. This may vary according to the asset class and the country, therefore operators must know the hours of trading sessions for the securities and derivatives in which they are interested in trading. If investors can understand market hours and set proper targets, they will have a much greater chance of making a profit within a workable schedule.

Kill Zones

Kill zones are highly liquid events. Many different market participants often come together and perform around these events. The activity itself can be event-driven (margin calls or option exercise-related activity), portfolio management-driven (asset allocation rebalancing orders and closing buy-in), or institutionally driven (larger players needing liquidity to complete the size) or a combination of any of the three. This intense cross-current of activity at a very specific point in time often occurs near significant technical levels and the established trends emerging from these events often persist until the next Death Zone approaches or enters.

Kill Zones are evolving with time and the course of world history. Since the end of World War II, New York has slowly invaded London's place as the world center for commercial banking. So much so that during the latter part of the 20th century, New York was considered the new center of the financial universe. With the end of the cold war, that leadership appears to have shifted towards Europe and away from the United States. Furthermore, Japan has slowly lost its former dominance in the global economic landscape, while Beijing's has increased dramatically. Only time will tell how these death zones will evolve given the ever-changing political, economic, and socioeconomic influences of each region.

Financial Markets

New York

New York (NYSE Chicago, NASDAQ)

7:30 am - 2:00 pm

It is the second largest currency platform in the world, followed largely by foreign investors as it participates in 90% of all operations, where movements on the New York Stock Exchange (NYSE) can have an immediate effect (powerful) on the dollar, for example, when companies merge and acquisitions are finalized, the dollar can instantly gain or lose value.

A. Complementary Stock Exchanges

Brazil (BOVESPA - Brazilian Stock Exchange)

07:00 am - 02:55 pm

Canada (TSX - Toronto Stock Exchange)

07:30 am - 02:00 pm

New York (NYSE - New York Stock Exchange)

08:30 am - 03:00 pm

B. North American Trading Session

07:00 am - 03:00 pm

(from the beginning of the business day on NYSE and NASDAQ, until the end of the New York session)

New York, Chicago and Toronto (Canada) open the North American session. Characterized by the most aggressive trading within the markets, currency pairs show high volatility. As the US markets open, trading is still active in Europe, however trading volume generally decreases with the end of the European session and the overlap between the US and Europe.

C. Strategic Points

US main session starts in 1 hour

07:30 am

The euro tends to drop before the US session. The NYSE, CHX and TSX (Canada) trading sessions begin 1 hour after this strategic point. The North American session begins trading Forex at 07:00 am.

This constitutes the beginning of the overlap of the United States and the European market that spans from 07:00 am to 10:35 am, often called the best time to trade EUR / USD, it is the period of greatest liquidity for the main European currencies since it is where they have their widest daily ranges.

When New York opens at 07:00 am the most intense trading begins in both the US and European markets. The overlap of European and American trading sessions has 80% of the total average trading range for all currency pairs during US business hours and 70% of the total average trading range for all currency pairs during European business hours. The intersection of the US and European sessions are the most volatile overlapping hours of all.

Influential news and data for the USD are released between 07:30 am and 09:00 am and play the biggest role in the North American Session. These are the strategically most important moments of this activity period: 07:00 am, 08:00 am and 08:30 am.

The main session of operations in the United States and Canada begins

08:30 am

Start of main trading sessions in New York, Chicago and Toronto. The European session still overlaps the North American session and this is the time for large-scale unpredictable trading. The United States leads the market. It is difficult to interpret the news due to speculation. Trends develop very quickly and it is difficult to identify them, however trends (especially for the euro), which have developed during the overlap, often turn the other way when Europe exits the market.

Second hour of the US session and last hour of the European session

09:30 am

End of the European session

10:35 am

The trend of the euro will change rapidly after the end of the European session.

Last hour of the United States session

02:00 pm

Institutional clients and very large funds are very active during the first and last working hours of almost all stock exchanges, knowing this allows to better predict price movements in the opening and closing of large markets. Within the last trading hours of the secondary market session, a pullback can often be seen in the EUR / USD that continues until the opening of the Tokyo session. Generally it happens if there was an upward price movement before 04:00 pm - 05:00 pm.

End of the trade session in the United States

03:00 pm

D. Kill Zones

11:30 am - 1:30 pm

New York Kill Zone. The United States is still the world's largest economy, so by default, the New York opening carries a lot of weight and often comes with a huge injection of liquidity. In fact, most of the world's marketable assets are priced in US dollars, making political and economic activity within this region even more important. Because it is relatively late in the world's trading day, this Death Zone often sees violent price swings within its first hour, leading to the proven adage "never trust the first hour of trading in America. North.

---------------

London

London (LSE - London Stock Exchange)

02:00 am - 10:35 am

Britain dominates the currency markets around the world, and London is its main component. London, a central trading capital of the world, accounts for about 43% of world trade, many Forex trends often originate from London.

A. Complementary Stock Exchange

Dubai (DFM - Dubai Financial Market)

12:00 am - 03:50 am

Moscow (MOEX - Moscow Exchange)

12:30 am - 10:00 am

Germany (FWB - Frankfurt Stock Exchange)

01:00 am - 10:30 am

Afríca (JSE - Johannesburg Stock Exchange)

01:00 am - 09:00 am

Saudi Arabia (TADAWUL - Saudi Stock Exchange)

01:00 am - 06:00 am

Switzerland (SIX - Swiss Stock Exchange)

02:00 am - 10:30 am

B. European Trading Session

02:00 am - 11:00 am

(from the opening of the Frankfurt session to the close of the Order Book on the London Stock Exchange / Euronext)

It is a very liquid trading session, where trends are set that start during the first trading hours in Europe and generally continue until the beginning of the US session.

C. Middle East Trading Session

12:00 am - 06:00 am

(from the opening of the Dubai session to the end of the Riyadh session)

D. Strategic Points

European session begins

02:00 am

London, Frankfurt and Zurich Stock Exchange enter the market, overlap between Europe and Asia begins.

End of the Singapore and Asia sessions

03:00 am

The euro rises almost immediately or an hour after Singapore exits the market.

Middle East Oil Markets Completion Process

05:00 am

Operations are ending in the European-Asian market, at which time Dubai, Qatar and in another hour in Riyadh, which constitute the Middle East oil markets, are closing. Because oil trading is done in US dollars, and the region with the trading day coming to an end no longer needs the dollar, consequently, the euro tends to grow more frequently.

End of the Middle East trading session

06:00 am

E. Kill Zones

5:00 am - 7:00 am

London Kill Zone. Considered the center of the financial universe for more than 500 years, Europe still has a lot of influence in the banking world. Many older players use the European session to establish their positions. As such, the London Open often sees the most significant trend-setting activity on any trading day. In fact, it has been suggested that 80% of all weekly trends are set through the London Kill Zone on Tuesday.

F. Kill Zones (close)

2:00 pm - 4:00 pm

London Kill Zone (close).

---------------

Tokyo

Tokyo (JPX - Tokyo Stock Exchange)

06:00 pm - 12:00 am

It is the first Asian market to open, receiving most of the Asian trade, just ahead of Hong Kong and Singapore.

A. Complementary Stock Exchange

Singapore (SGX - Singapore Exchange)

07:00 pm - 03:00 am

Hong Kong (HKEx - Hong Kong Stock Exchange)

07:30 pm - 02:00 am

Shanghai (SSE - Shanghai Stock Exchange)

07:30 pm - 01:00 am

India (NSE - India National Stock Exchange)

09:45 pm - 04:00 am

B. Asian Trading Session

06:00 pm - 03:00 am

From the opening of the Tokyo session to the end of the Singapore session

The first major Asian market to open is Tokyo which has the largest market share and is the third largest Forex trading center in the world. Singapore opens in an hour, and then the Chinese markets: Shanghai and Hong Kong open 30 minutes later. With them, the trading volume increases and begins a large-scale operation in the Asia-Pacific region, offering more liquidity for the Asian-Pacific currencies and their crosses. When European countries open their doors, more liquidity will be offered to Asian and European crossings.

C. Strategic Points

Second hour of the Tokyo session

07:00 pm

This session also opens the Singapore market. The commercial dynamics grows in anticipation of the opening of the two largest Chinese markets in 30 minutes: Shanghai and Hong Kong, within these 30 minutes or just before the China session begins, the euro usually falls until the same moment of the opening of Shanghai and Hong Kong.

Second hour of the China session

08:30 pm

Hong Kong and Shanghai start trading and the euro usually grows for more than an hour. The EUR / USD pair mixes up as Asian exporters convert part of their earnings into both US dollars and euros.

Last hour of the Tokyo session

11:00 pm

End of the Tokyo session

12:00 am

If the euro has been actively declining up to this time, China will raise the euro after the Tokyo shutdown. Hong Kong, Shanghai and Singapore remain open and take matters into their own hands causing the growth of the euro. Asia is a huge commercial and industrial region with a large number of high-quality economic products and gigantic financial turnover, making the number of transactions on the stock exchanges huge during the Asian session. That is why traders, who entered the trade at the opening of the London session, should pay attention to their terminals when Asia exits the market.

End of the Shanghai session

01:00 am

The trade ends in Shanghai. This is the last trading hour of the Hong Kong session, during which market activity peaks.

D. Kill Zones

10:00 pm - 2:00 am

Asian Kill Zone. Considered the "Institutional" Zone, this zone represents both the launch pad for new trends as well as a recharge area for the post-American session. It is the beginning of a new day (or week) for the world and as such it makes sense that this zone often sets the tone for the remainder of the global business day. It is ideal to pay attention to the opening of Tokyo, Beijing and Sydney.

--------------

Sidney

Sydney (ASX - Australia Stock Exchange)

06:00 pm - 12:00 am

A. Complementary Stock Exchange

New Zealand (NZX - New Zealand Stock Exchange)

04:00 pm - 10:45 pm

It's where the global trading day officially begins. While it is the smallest of the megamarkets, it sees a lot of initial action when markets reopen Sunday afternoon as individual traders and financial institutions are trying to regroup after the long hiatus since Friday afternoon. On weekdays it constitutes the end of the current trading day where the change in the settlement date occurs.

B. Pacific Trading Session

04:00 pm - 12:00 am

(from the opening of the Wellington session to the end of the Sydney session)

Forex begins its business hours when Wellington (New Zealand Exchange) opens local time on Monday. Sydney (Australian Stock Exchange) opens in 2 hours. It is a session with a fairly low volatility, configuring itself as the calmest session of all. Strong movements appear when influential news is published and when the Pacific session overlaps the Asian Session.

C. Strategic Points

End of the Sydney session

12:00 am

---------------

Conclusions

The best time to trade is during overlaps in trading times between open markets. Overlaps equate to higher price ranges, creating greater opportunities.

Regarding press releases (news), it should be noted that these in the currency markets have the power to improve a normally slow trading period. When a major announcement is made regarding economic data, especially when it goes against the predicted forecast, the coin can lose or gain value in a matter of seconds. In general, the more economic growth a country produces, the more positive the economy is for international investors. Investment capital tends to flow to countries that are believed to have good growth prospects and subsequently good investment opportunities, leading to the strengthening of the country's exchange rate. Also, a country that has higher interest rates through its government bonds tends to attract investment capital as foreign investors seek high-yield opportunities. However, stable economic growth and attractive yields or interest rates are inextricably intertwined. It's important to take advantage of market overlaps and keep an eye out for press releases when setting up a trading schedule.

References:

www.investopedia.com

www.investopedia.com

www.investopedia.com

www.investopedia.com

market24hclock.com

market24hclock.com

Buy the Dips (by Coinrule)Taking your first steps into automated trading may be challenging. Coinrule's mission is to make it as easy as possible, also for beginners.

Here follows the best trading strategy to get started with Coinrule. This strategy doesn't involve complex indicators, yet was proved to be effective in the long term for many coins. Results seem to be improved when trading a coin vs Bitcoin.

The strategy buys the dips of a coin to sell with a profit. A stop-loss protects every trade.

Crypto markets offer high volatility and, thus, excellent opportunities for trading. Excluding times of severe downtrend, buying the dip is a simple and effective long-term trading strategy. The buy-signal is set to a 2% drop in a 30-minutes time frame.

Each trade comes with a take profit and a stop loss. Both set at 2%.

You can adjust these percentages to the market volatility as an advanced setup. You can backtest the outcomes using the backtesting tool from Tradingview

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

True Inflation Compensator (USD)This script will draw your underlying ticker compensating for a truer USD inflation rate based on an average between the M2 money supply increase and the government's reported CPI. It only considers the last year of inflation by default, but you can set any amount of years in the options.

This is especially relevant given the current massive printing that is going on within the US economic system. If you look at the S&P500 the market has by no means completely recovered, but due to massive printing most do not realize this by just looking at the base chart. A similar concept applies to Bitcoin. Unfortunately due to today's economic climate one must compensate for printing to get a true analysis of how investments are doing.

STOCH_HVP(picte)This indicator is made up of a stochastic oscillator and of historical volatility percentile. Historical volatility percentile basically tells you how volatile the market is based on how volatile it has been in the history.

Historical volatility is great for trading options but i have also found it to be great at finding trades with good risk/reward ratio. When market has extremely low volatility we can expect a bigger move to emerge along with expansion of volatility. But since historical volatility does not imply the direction of the market i added a stochastic oscillator with some horizontal levels i have found to serve as good support/resistance levels.

I found it useful for trading Forex pairs but it is especially powerful with bitcoin.

Ranged Volume Strategy - evoThis is the strategy version for the ranged volume indicator I published a few days ago.

Long : First yellow break-out after red

Short : First red break-out after yellow

Because this is volume, you want to be using this on an exchange with high volume for the best results. Default settings are not optimized but work great on bitcoins daily chart.

A short explanation of the indicator below:

OneGeenCandle - Tether-Printer**************** OnegreenCandle - Tether Printer ************************

Shows the total market cap of USDT (US Dollar Tether) currency. Helpful for swing trading longer timeframes and indentifying new supply in the crypto market.

FTX Index Advance Decline LineAs of publishing, all the tickers from FTX with the word "index" in it, plus bitcoin.

This is your regular ADL except instead of hundreds in the basket you've got them condensed into 7 (for now) and in open/close candle form instead of a line.

I'm a bit disappointed because I thought I'd lever more utility from indexes. It may just need some tweaking.

Doesn't it look like Renko?

Some notes:

Reason why it expands:

Total number of constituents is a static 7, to fix that use time to change the total variable based on dates of introduction.

Reallly looks like Renko:

Renko with ATR, length 14, hourly chart.

Voss Strategy (Filter + Trend Indicator) [Bitduke]Created strategy based on Voss Predictive Filter, implemented by TradingView user e2e4mfck.

Voss Predictive Filter

This is a relatively new filter from John F. Ehlers’ article, “A Peek Into The Future .” Ehlers describes the calculation of a new filter that could help signal cyclical turning points in markets.

But filter has a negative group delay and while an indicator based on it cannot actually see into the future, it may provide the trader with signals in advance of other indicators.

In mentioned article he tested filter on SPY and at one point in time "it went into a trend mode in January 2019, and the cycle signal failed miserably, signaling a short position during the runup. <...> The only way to minimize the impact of this condition is to employ an additional trend detector."

Thus I've added another Ehlers' based trend based indicator Instantaneous Trendline (thanks to LazyBear for implementation) to minimize the impact of the trend mode and got a good results on XBTUSD pair 4h.

Backtest :

> Range: 2016 - 2020

> XBTUSD

> 4h

> ~20% drawdown

> Sharpe (0.361, not too impressive)

I think it can be improved with Risk Management system and experimenting with various trend following indicators.

BTC Transaction/On-Chain Volume (Basic)Description:

Whale: Whale utilizing discounted prices (increasing on-chain volume & decreasing price)

Recovering: Positive momentum in price after potential whale activity

Cycle Volume Support: The transaction volume support during a cycle

What’s the best time to invest?

After institutions make up their mind at low price levels.

How’s on-chain volume related to whales or institutional money?

On-chain volume is contributed not only by using BTC as payment methods, but more importantly by large custodians using the BTC chain to settle internal whale trades. When OTC volume is estimated 2-3 times of exchange volume, and when total on-chain volume is only a small fraction of the exchange volume, the OTC settlement plays a big factor in moving the on-chain volume around.

Why does the price drop further after spotting whale money?

Does new money equal higher true value? Yes.

Does new money equal higher price? No.

Whales could not only ladder in when they see the price on discount, but also push the price further down to accumulate at better price levels. However, either route chosen, it’s most likely for the price to rise to a higher level compared to the level when the whales enter. Whales are here to make money after all.

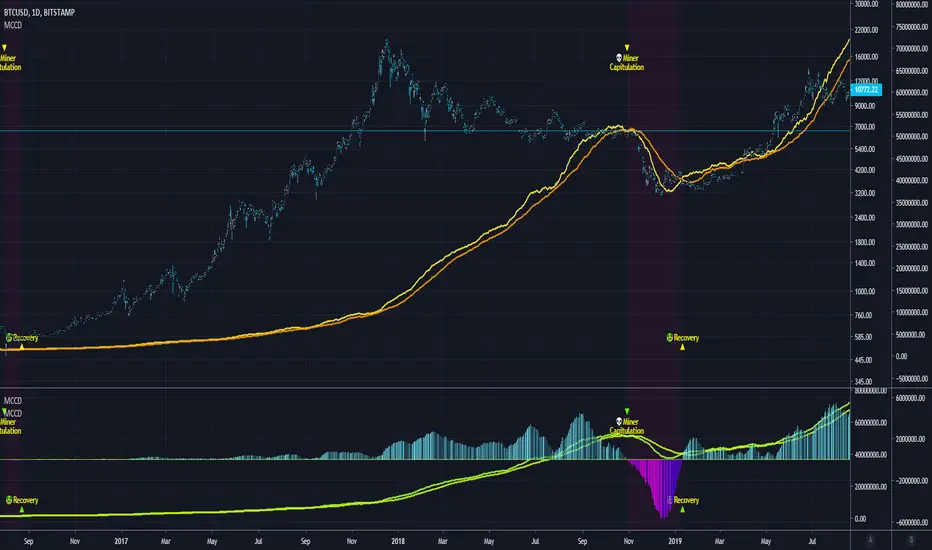

Blockchain Fundamentals - MCCD - Miner Capitulation Conv/Div🔗Blockchain Fundamentals - MCCD - Miner Capitulation & Convergence Divergence

(a.k.a. Hash Ribbons)

Intro

Miner Capitulation has been talked about alot recently in the news and on twitter. I wanted to join the in fun and add my own spin on things.

Description

This shows the 30 (yellow) and 60 (orange) day moving average of the hash rate of bitcoin. I added an option to show the convergence/divergence of the two moving averages in a visual manner similar to the MACD.

I also added the ability to select both the length and type of MA used in the calculation of the capitulation so you can experiment.

Other additions include bar coloration by trade state, and background highlighting of capitulation periods.

Editable Capitulation/Recovery plots will show clearly when the crosses happen.

The way to replicate my display is to add the indicator twice below the chart and combine in the same pane. First indicator displays the averages by default. The second one you enable convergence/divergence display option and uncheck the rest.

Last I add the indicator one more time and dragged it on chart. Do not combine the scales into one, of else it will ruin the scale (you want them separate scales). Its just showing you possibilities, use whatever works for you!

👍 We hope you enjoyed this indicator and find it useful! We post free crypto analysis, strategies and indicators regularly. This is our 73rd script on Tradingview!

💬Check my Signature for other information

Mayer Multiple [ChuckBanger]The Mayer Multiple is calculated by dividing the current price by 200-day moving average so you have to use daily charts fort it to work properly. This script is design to be a help for deciding when to buy Bitcoin and when it is time to sell your HODL position. This script uses moving average for optimal sell and buy points. In time of writing the average Mayer Multiple is 1.47 for the history of Bitcoin.

ANN MACD (BTC)

Logic is correct.

But I prefer to say experimental because the sample set is narrow. (300 columns)

Let's start:

6 inputs : Volume Change , Bollinger Low Band chg. , Bollinger Mid Band chg., Bollinger Up Band chg. , RSI change , MACD histogram change.

1 output : Future bar change (Historical)

Training timeframe : 15 mins (Analysis TF > 4 hours (My opinion))

Learning cycles : 337

Training error: 0.009999

Input columns: 6

Output columns: 1

Excluded columns: 0

Grid

Training example rows: 301

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Network

Input nodes connected: 6

Hidden layer 1 nodes: 8

Hidden layer 2 nodes: 0

Hidden layer 3 nodes: 0

Output nodes: 1

Learning rate : 0.6 Momentum : 0.8

More info :

EDIT : This code is open source under the MIT License. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com

Power Law S/RBerger's article on the Power Law Model for Bitcoin is a compelling read and gives the best evidence so far of the diminishing case for retracing below $3000, of a slowing market on a log-log plot, and reducing but continued volatility.

After seeing it acts as support routinely in the last 10 years, I put together a quick little script that plots his midline curve for Bitcoin. You can change the intercept and slope but will need to do your own calculations for other curves.

I hope you all like it.

Crypto Prices InfoPanel V2Hello traders

Following the introduction of ByBit to TradingView ByBit on TradingView

I decided to upgrade my previous Bitcoin InfoPanel Bitcoin-Prices-InfoPanel/

Now it's more dynamic (thumbs up) but only work with Bitcoin, Ethereum and Litecoin . If you select any other asset than those 3, the script won't work

This is due to a technical limitation on TradingView because I can't do more than 40 security calls per script

If you don't know what the security function is, here's a reminder : Security documentation . If you don't know what is TradingView... I cannot do anything for you...

Now you can use this panel to have a very cool arbitrage view directly from TradingView and use the info to gamble between brokers (not financial advice)

See you all tomorrow for a huge update regarding the Strategy Builder. I'll show you how to connect it to a Backtest system

____________________________________________________________

Feel free to hit the thumbs up as it shows me that I'm not doing this for nothing and will motivate to deliver more quality content in the future.

- I'm an officially approved PineEditor/LUA/MT4 approved mentor on codementor. You can request a coaching with me if you want and I'll teach you how to build kick-ass indicators and strategies

Jump on a 1 to 1 coaching with me

- You can also hire for a custom dev of your indicator/strategy/bot/chrome extension/python

Moving Average Strategy of BiznesFilosofWhat is brilliant is simple! Therefore, this strategy works very well. It is configured on bitcoin. But you can use it for other tools. Only need to change the settings.

Remember that this is not a panacea, but only an assistant! You yourself have to choose which entry and exit points to choose.

In more detail about strategy on my channel in YouTube.

===

Что гениально, то просто! Потому, эта стратегия очень хорошо работает. Настроена она на биткоин. Но можно использовать и для других инструментов. Только нужно поменять настройки.

Помните, что это не панацея, а только помощник! Вы сами должны панимать, какие выбирать точки входа и выхода.

Более подробно про стратегию на моём канале в Ютуб.

Crypto Indicators #u9tusA set of low timeframe (LTF), medium timeframe (MTF), and high timeframe (HTF) indicators for use in crypto currencies / bitcoin.

Traditionally the 10, 20, 50, 100, and 200 SMAs are used in TA. With cryptos, I've found that the 8 EMA, 21, 55, and 128 SMAs backtest better, while no change in length was necessary for the 200. I wanted to combine all these into one indicator to easily add them to a chart layout, hence this script.

You can customize the length of each MA to your liking in the settings, or accept the defaults.

LTF Indicators:

8 EMA in blue hues, medium line stroke.

MTF Indicators:

21, 55 SMA in purple hues, medium line stroke.

HTF Indicators:

128, 200 SMA in yellow hues, thick line stroke.

Defaults are for daily timeframes and lower; suggest changing up the intervals for weekly and monthly to:

21 -> 30

55 -> 50

128 -> 100

$BTC, $ETH, #ALTS

twitter.com

(c) @jhaurawachsman 20190515

Stock to Flowthis study gives the option to plot the stock to flow

OR the number of blocks per month. (you must edit the code by deleting the //)

it should be used only on the monthly timeframe

idea credited to:

medium.com

200/150

This a variation to my 120/60 Trend Model for the daily chart on Bitcoin, which has quite reliably been determining the over all trend as well as low risk entries within a longer term trend. It's a combination of 150 & 220 SMA, used on the 1D chart. Once price closes below both SMAs trend is an early bearish signal, while the SMAs flipping to red is later but more reliable bearish signal. For bullish trend it is the same thing just the opposite. Once the "cloud" switches red trend is bearish while once it switches green it's bullish.

Bitcoin tends to get rejected by the cloud during bullish and bearish trends. Once Bitcoin pushes through the cloud the trend will typically reverse.

Bitcoin trading within or close to the cloud is generally a good long or short entries, depending on the color of the cloud (red: short & green: long).

GBTC/BTC(average) premium percentageI updated the GBTC premium percentage indicator to the average bitcoin price (average between bitfinex, coinbase, bitstamp, bittrex, and gemini). I also left this new script open so you can update the amount of bitcoin per share because it is always changing. you can find the amount of bitcoin per share at grayscale.co half way down on the left.

Mayer MultipleThis indicator was created by Trace Mayer as a way to analyze the price of Bitcoin in a historical context. Consider it as a kind of Volatility Ratio that was created by Jack Schwager for the securities.

To learn more about Mayer Multiple see:

charts.woobull.com

mayermultiple.info

www.theinvestorspodcast.com

Good luck!