IU Range Trading StrategyIU Range Trading Strategy

The IU Range Trading Strategy is designed to identify range-bound markets and take trades based on defined price ranges. This strategy uses a combination of price ranges and ATR (Average True Range) to filter entry conditions and incorporates a trailing stop-loss mechanism for better trade management.

User Inputs:

- Range Length: Defines the number of bars to calculate the highest and lowest price range (default: 10).

- ATR Length: Sets the length of the ATR calculation (default: 14).

- ATR Stop-Loss Factor: Determines the multiplier for the ATR-based stop-loss (default: 2.00).

Entry Conditions:

1. A range is identified when the difference between the highest and lowest prices over the selected range is less than or equal to 1.75 times the ATR.

2. Once a valid range is formed:

- A long trade is triggered at the range high.

- A short trade is triggered at the range low.

Exit Conditions:

1. Trailing Stop-Loss:

- The stop-loss adjusts dynamically using ATR targets.

- The strategy locks in profits as the trade moves in your favor.

2. The stop-loss and take-profit levels are visually plotted for transparency and easier decision-making.

Features:

- Automated box creation to visualize the trading range.

- Supports one position at a time, canceling opposite-side entries.

- ATR-based trailing stop-loss for effective risk management.

- Clear visual representation of stop-loss and take-profit levels with colored bands.

This strategy works best in markets with defined ranges and can help traders identify breakout opportunities when the price exits the range.

ค้นหาในสคริปต์สำหรับ "bands"

CCI Threshold StrategyThe CCI Threshold Strategy is a trading approach that utilizes the Commodity Channel Index (CCI) as a momentum indicator to identify potential buy and sell signals in financial markets. The CCI is particularly effective in detecting overbought and oversold conditions, providing traders with insights into possible price reversals. This strategy is designed for use in various financial instruments, including stocks, commodities, and forex, and aims to capitalize on price movements driven by market sentiment.

Commodity Channel Index (CCI)

The CCI was developed by Donald Lambert in the 1980s and is primarily used to measure the deviation of a security's price from its average price over a specified period.

The formula for CCI is as follows:

CCI=(TypicalPrice−SMA)×0.015MeanDeviation

CCI=MeanDeviation(TypicalPrice−SMA)×0.015

where:

Typical Price = (High + Low + Close) / 3

SMA = Simple Moving Average of the Typical Price

Mean Deviation = Average of the absolute deviations from the SMA

The CCI oscillates around a zero line, with values above +100 indicating overbought conditions and values below -100 indicating oversold conditions (Lambert, 1980).

Strategy Logic

The CCI Threshold Strategy operates on the following principles:

Input Parameters:

Lookback Period: The number of periods used to calculate the CCI. A common choice is 9, as it balances responsiveness and noise.

Buy Threshold: Typically set at -90, indicating a potential oversold condition where a price reversal is likely.

Stop Loss and Take Profit: The strategy allows for risk management through customizable stop loss and take profit points.

Entry Conditions:

A long position is initiated when the CCI falls below the buy threshold of -90, indicating potential oversold levels. This condition suggests that the asset may be undervalued and due for a price increase.

Exit Conditions:

The long position is closed when the closing price exceeds the highest price of the previous day, indicating a bullish reversal. Additionally, if the stop loss or take profit thresholds are hit, the position will be exited accordingly.

Risk Management:

The strategy incorporates optional stop loss and take profit mechanisms, which can be toggled on or off based on trader preference. This allows for flexibility in risk management, aligning with individual risk tolerances and trading styles.

Benefits of the CCI Threshold Strategy

Flexibility: The CCI Threshold Strategy can be applied across different asset classes, making it versatile for various market conditions.

Objective Signals: The use of quantitative thresholds for entry and exit reduces emotional bias in trading decisions (Tversky & Kahneman, 1974).

Enhanced Risk Management: By allowing traders to set stop loss and take profit levels, the strategy aids in preserving capital and managing risk effectively.

Limitations

Market Noise: The CCI can produce false signals, especially in highly volatile markets, leading to potential losses (Bollinger, 2001).

Lagging Indicator: As a lagging indicator, the CCI may not always capture rapid market movements, resulting in missed opportunities (Pring, 2002).

Conclusion

The CCI Threshold Strategy offers a systematic approach to trading based on well-established momentum principles. By focusing on overbought and oversold conditions, traders can make informed decisions while managing risk effectively. As with any trading strategy, it is crucial to backtest the approach and adapt it to individual trading styles and market conditions.

References

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Lambert, D. (1980). Commodity Channel Index. Technical Analysis of Stocks & Commodities, 2, 3-5.

Pring, M. J. (2002). Technical Analysis Explained. New York: McGraw-Hill.

Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124-1131.

Strategic Multi-Step Supertrend - Strategy [presentTrading]The code is mainly developed for me to stimulate the multi-step taking profit function for strategies. The result shows the drawdown can be reduced but at the same time reduced the profit as well. It can be a heuristic for futures leverage traders.

█ Introduction and How it is Different

The "Strategic Multi-Step Supertrend" is a trading strategy designed to leverage the power of multiple steps to optimize trade entries and exits across the Supertrend indicator. Unlike traditional strategies that rely on single entry and exit points, this strategy employs a multi-step approach to take profit, allowing traders to lock in gains incrementally. Additionally, the strategy is adaptable to both long and short trades, providing a comprehensive solution for dynamic market conditions.

This template strategy lies in its dual Supertrend calculation, which enhances the accuracy of trend detection and provides more reliable signals for trade entries and exits. This approach minimizes false signals and increases the overall profitability of trades by ensuring that positions are entered and exited at optimal points.

BTC 6h L/S Performance

█ Strategy, How It Works: Detailed Explanation

The "Strategic Multi-Step Supertrend Trader" strategy utilizes two Supertrend indicators calculated with different parameters to determine the direction and strength of the market trend. This dual approach increases the robustness of the signals, reducing the likelihood of entering trades based on false signals. Here is a detailed breakdown of how the strategy operates:

🔶 Supertrend Indicator Calculation

The Supertrend indicator is a trend-following overlay on the price chart, typically used to identify the direction of the trend. It is calculated using the Average True Range (ATR) to ensure that the indicator adapts to market volatility. The formula for the Supertrend indicator is:

Upper Band = (High + Low) / 2 + (Factor * ATR)

Lower Band = (High + Low) / 2 - (Factor * ATR)

Where:

- High and Low are the highest and lowest prices of the period.

- Factor is a user-defined multiplier.

- ATR is the Average True Range over a specified period.

The Supertrend changes its direction based on the closing price in relation to these bands.

🔶 Entry-Exit Conditions

The strategy enters long positions when both Supertrend indicators signal an uptrend, and short positions when both indicate a downtrend. Specifically:

- Long Condition: Supertrend1 < 0 and Supertrend2 < 0

- Short Condition: Supertrend1 > 0 and Supertrend2 > 0

- Long Exit Condition: Supertrend1 > 0 and Supertrend2 > 0

- Short Exit Condition: Supertrend1 < 0 and Supertrend2 < 0

🔶 Multi-Step Take Profit Mechanism

The strategy features a multi-step take profit mechanism, which allows traders to lock in profits incrementally. This is achieved through four user-configurable take profit levels. For each level, the strategy specifies a percentage increase (for long trades) or decrease (for short trades) in the entry price at which a portion of the position is exited:

- Step 1: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent1 / 100)

- Step 2: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent2 / 100)

- Step 3: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent3 / 100)

- Step 4: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent4 / 100)

This staggered exit strategy helps in locking profits at multiple levels, thereby reducing risk and increasing the likelihood of capturing the maximum possible profit from a trend.

BTC Local

█ Trade Direction

The strategy is highly flexible, allowing users to specify the trade direction. There are three options available:

- Long Only: The strategy will only enter long trades.

- Short Only: The strategy will only enter short trades.

- Both: The strategy will enter both long and short trades based on the Supertrend signals.

This flexibility allows traders to adapt the strategy to various market conditions and their own trading preferences.

█ Usage

1. Add the strategy to your trading platform and apply it to the desired chart.

2. Configure the take profit settings under the "Take Profit Settings" group.

3. Set the trade direction under the "Trade Direction" group.

4. Adjust the Supertrend settings in the "Supertrend Settings" group to fine-tune the indicator calculations.

5. Monitor the chart for entry and exit signals as indicated by the strategy.

█ Default Settings

- Use Take Profit: True

- Take Profit Percentages: Step 1 - 6%, Step 2 - 12%, Step 3 - 18%, Step 4 - 50%

- Take Profit Amounts: Step 1 - 12%, Step 2 - 8%, Step 3 - 4%, Step 4 - 0%

- Number of Take Profit Steps: 3

- Trade Direction: Both

- Supertrend Settings: ATR Length 1 - 10, Factor 1 - 3.0, ATR Length 2 - 11, Factor 2 - 4.0

These settings provide a balanced starting point, which can be customized further based on individual trading preferences and market conditions.

FlexiMA x FlexiST - Strategy [presentTrading]█ Introduction and How it is Different

The FlexiMA x FlexiST Strategy blends two analytical methods - FlexiMA and FlexiST, which are opened in my early post.

- FlexiMA calculates deviations between an indicator source and a dynamic moving average, controlled by a starting factor and increment factor.

- FlexiST, on the other hand, leverages the SuperTrend model, adjusting the Average True Range (ATR) length for a comprehensive trend-following oscillator.

This synergy offers traders a more nuanced and multifaceted tool for market analysis.

BTC 6H L/S Performance

Local

█ Strategy, How It Works: Detailed Explanation

The strategy combines two components: FlexiMA and FlexiST, each utilizing unique methodologies to analyze market trends.

🔶FlexiMA Component:

- Calculates deviations between an indicator source and moving averages of variable lengths.

- Moving average lengths are dynamically adjusted using a starting factor and increment factor.

- Deviations are normalized and analyzed to produce median and standard deviation values, forming the FlexiMA oscillator.

Length indicator (50)

🔶FlexiST Component:

- Uses SuperTrend indicators with varying ATR (Average True Range) lengths.

- Trends are identified based on the position of the indicator source relative to the SuperTrend bands.

- Deviations between the indicator source and SuperTrend values are calculated and normalized.

Starting Factor (5)

🔶Combined Strategy Logic:

- Entry Signals:

- Long Entry: Triggered when median values of both FlexiMA and FlexiST are positive.

- Short Entry: Triggered when median values of both FlexiMA and FlexiST are negative.

- Exit Signals:

- Long Exit: Triggered when median values of FlexiMA or FlexiST turn negative.

- Short Exit: Triggered when median values of FlexiMA or FlexiST turn positive.

This strategic blend of FlexiMA and FlexiST allows for a nuanced analysis of market trends, providing traders with signals based on a comprehensive view of market momentum and trend strength.

█ Trade Direction

The strategy is designed to cater to various trading preferences, offering "Long", "Short", and "Both" options. This flexibility allows traders to align the strategy with their specific market outlook, be it bullish, bearish, or a combination of both.

█ Usage

Traders can effectively utilize the FlexiMA x FlexiST Strategy by first selecting their desired trade direction. The strategy then generates entry signals when the conditions for either the FlexiMA or FlexiST are met, indicating potential entry points in the market. Conversely, exit signals are generated when the conditions for these indicators diverge, thus signaling a potential shift in market trends and suggesting a strategic exit point.

█ Default Settings

1. Indicator Source (HLC3): Provides a balanced and stable price source, reducing the impact of extreme market fluctuations.

2. Indicator Lengths (20 for FlexiMA, 10 for FlexiST): Longer FlexiMA length smooths out short-term fluctuations, while shorter FlexiST length allows for quicker response to market changes.

3. Starting Factors (1.0 for FlexiMA, 0.618 for FlexiST): Balanced start for FlexiMA and a harmonized approach for FlexiST, resonating with natural market cycles.

4. Increment Factors (1.0 for FlexiMA, 0.382 for FlexiST): FlexiMA captures a wide range of market behaviors, while FlexiST provides a gradual transition to capture finer trend shifts.

5. Normalization Methods ('None'): Uses raw deviations, suitable for markets where absolute price movements are more significant.

6. Trade Direction ('Both'): Allows strategy to consider both long and short opportunities, ideal for versatile market engagement.

*More details:

1. FlexiMA

2. FlexiST

Donchian Channel Strategy IdeaThis strategy idea is a variation of the "Donchian Channel" trading strategy. It is built with a highest-high band, a lowest-low band, and a baseline which is average the highest-high and the lowest-low bands. This strategy is very useful in trending instruments on 1W and 1D timeframes. This is the implementation used in the QuantCT app.

You can set the operation mode to be Long/Short or long-only.

You also can set a fixed stop-loss or ignore it so that the strategy acts solely based on entry and exit signals.

Trade Idea

When the close price breaks up the previous highest-high, it is a long signal, the market is considered rising (bullish), and the plotted indicator becomes green. Long positions are held until the close price crosses under the baseline.

When the close price breaks down the previous lowest-low, it is a short signal, the market is considered falling (bearish), and the plotted indicator becomes red. Short positions are held until the close price crosses above the baseline.

Otherwise, if we have no position in the market, the market is considered ranging, and the plotted indicator becomes orange.

Entry/Exit rules

Enter LONG if the close price breaks up the previous highest-high (i.e. when the plotted indicator becomes green).

Exit LONG if the close price crosses under the baseline (i.e. when the plotted indicator becomes orange).

Enter SHORT if the close price breaks down the previous lowest-low (i.e. when the plotted indicator becomes red).

Exit SHORT if the close price crosses above the baseline (i.e. when the plotted indicator becomes orange).

CAUTION

It's just a bare trading idea - a profitable one. However, you can enhance this idea and turn it into a full trading strategy with enhanced risk/money management and optimizing it, and you ABSOLUTELY should do this!

DON'T insist on using Long/Short mode on all instruments! This strategy performs much better in Long-Only mode on many (NOT All) trending instruments (Like BTC, ETH, etc.).

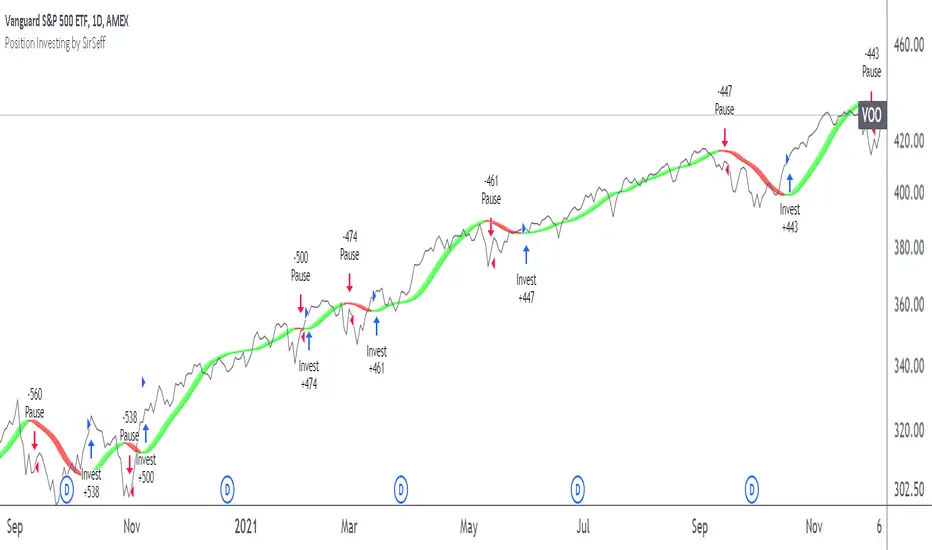

Position Investing by SirSeffThis is for my group.

The ideas is to dollar cost average whenever the band is green and pause investing when the band is red.

This gives you two things:

1. You'll minimize averaging down. Ibig sabihin maiiwasan mo bumili tapos kinabukasan down agad.

2. you'll maximize averaging up or scaling up. Ibig sabihin, most likely nakaka bili ka na green days and green kinabukasan.

Join the FB group fb.com/groups/usstocksforfilipinos

With Net profit of 87.72 % at hindi pa kasama compounding effect niyan whenever you top up on green bands.

Percent Profitable is 2.07 ibig sabihin ma dodoble mo ang account mo when you religiously follow this.

Max Loss Drawdown is 7.43 %, ibig sabihin maminimize mo ang losses down to 7.43%

Long only strategy VWAP with BB and Golden Cross EMA50/200

This is strategy, mainly designed for stock markets

It makes uses of the EMA 50/ 200 ( Golden cross) and VWAP and Bollinger bands.

It only takes long positions. It can be adapted to all time frames, but preferably to be used with longer timeframes 1h +

The rules for entry are the next ones :

1. EMA50 > EMA 200

2. if current close > vwap session value

3. check if price dipped BB lower band for any of last 10 candles

EXIT RULE

1. price closes above BB upper

STOP LOSS EXIT

1. As configured --- default is set to 1%

Combo Backtest 123 Reversal & Donchian Channel Width This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Donchian Channel was developed by Richard Donchian and it could be compared

to the Bollinger Bands. When it comes to volatility analysis, the Donchian Channel

Width was created in the same way as the Bollinger Bandwidth technical indicator was.

As was mentioned above the Donchian Channel Width is used in technical analysis to measure

volatility. Volatility is one of the most important parameters in technical analysis.

A price trend is not just about a price change. It is also about volume traded during this

price change and volatility of a this price change. When a technical analyst focuses his/her

attention solely on price analysis by ignoring volume and volatility, he/she only sees a part

of a complete picture only. This could lead to a situation when a trader may miss something and

lose money. Lets take a look at a simple example how volatility may help a trader:

Most of the price based technical indicators are lagging indicators.

When price moves on low volatility, it takes time for a price trend to change its direction and

it could be ok to have some lag in an indicator.

When price moves on high volatility, a price trend changes its direction faster and stronger.

An indicator's lag acceptable under low volatility could be financially suicidal now - Buy/Sell signals could be generated when it is already too late.

Another use of volatility - very popular one - it is to adapt a stop loss strategy to it:

Smaller stop-loss recommended in low volatility periods. If it is not done, a stop-loss could

be generated when it is too late.

Bigger stop-loss recommended in high volatility periods. If it is not done, a stop-loss could

be triggered too often and you may miss good trades.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & DAPD This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator is similar to Bollinger Bands. It based on DAPD - Daily

Average Price Delta. DAPD is based upon a summation for each of the

highs (hod) for the 21 days prior to today minus the summation for

each of the lows (lod) for the last 21 days prior to today. The result

of this calculation would then be divided by 21.

It will be buy when high above previos DAPD high and sell if low below previos DAPD low

WARNING:

- For purpose educate only

- This script to change bars colors.

ATR Long Only Strategy lower band buyATR with ATR bands. Buy low band sell high band. Tested on weekly charts.

Donchian Channel Width Strategy The Donchian Channel was developed by Richard Donchian and it could be compared

to the Bollinger Bands. When it comes to volatility analysis, the Donchian Channel

Width was created in the same way as the Bollinger Bandwidth technical indicator was.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

DAPD - Strategy Backtest This indicator is similar to Bollinger Bands. It based on DAPD - Daily

Average Price Delta. DAPD is based upon a summation for each of the

highs (hod) for the 21 days prior to today minus the summation for

each of the lows (lod) for the last 21 days prior to today. The result

of this calculation would then be divided by 21.

It will be buy when high above previos DAPD high and sell if low below previos DAPD low

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

News Volatility Bracketing StrategyThis is a news-volatility bracketing strategy. Five seconds before a scheduled release, the strategy brackets price with a buy-stop above and a sell-stop below (OCO), then converts the untouched side into nothing while the filled side runs with a 1:1 TP/SL set the same distance from entry. Distances are configurable in USD or %, so it scales to the instrument and can run on 1-second data (or higher TF with bar-magnifier). The edge it’s trying to capture is the immediate, one-directional burst and liquidity vacuum that often follows market-moving news—entering on momentum rather than predicting direction. Primary risks are slippage/spread widening and whipsaws right after the print, which can trigger an entry then snap back to the stop.

OPTIMAL super trend tripple confirm for leverage. Ai implemented for higher r:r still a work in progresss

Twin Range Filter StrategyClarity Over Confusion: See price action through a全新的 lens. Watch as erratic, choppy movements are smoothed into a clear, actionable trajectory. The path of least resistance becomes obvious.

Confidence Over Hesitation: Receive high-probability entry and exit signals with a proven logic that waits for the market to commit before you do. No more second-guessing.

Discipline Over Emotion: Our algorithm enforces a systematic approach, helping you avoid emotional FOMO chasing and panic selling. Stick to the plan and execute with precision.

What Can You Expect?

Dynamic Adaptability: Unlike static indicators, continuously adapts to volatility. It widens its filter in turbulent markets to avoid whipsaws and tightens it in trending markets to capture more of the move.

The Power of Two: By synthesizing data from two distinct market perspectives, it confirms strength and filters out weakness, providing a confluence that standalone indicators simply cannot match.

Clean, Unambiguous Signals: We’ve eliminated the clutter. The software provides clear visual alerts (Green Arrows for Long, Red Arrows for Short) right on your chart, telling you exactly when the equilibrium has shifted.

Who is this for?

Swing Traders looking to capture the heart of a trend and avoid false breakouts.

Day Traders needing a reliable filter to navigate volatile intraday action.

Systematic Traders seeking a robust logic layer to add to their automated strategy.

Anyone overwhelmed by indicator overload and craving a single, trusted source of truth on their chart

VWAP Executor — v6 (VWAP fix)tarek helishPractical scalping plan with high-rate (sometimes reaching 70–85% in a quiet market)

Concept: “VWAP bounce with a clear trend.”

Tools: 1–3-minute chart for entry, 5-minute trend filter, VWAP, EMA(50) on 5M, ATR(14) on 1M, volume.

When to trade: London session or early New York session; avoid 10–15 minutes before/after high-impact news.

Entry rules (buy for example):

Trend: Price is above the EMA(50) on 5M and has an upward trend.

Entry zone: First bounce to VWAP (or a ±1 standard deviation channel around it).

Signal: Bullish rejection/engulfing candle on 1M with increasing volume, and RSI(2) has exited oversold territory (optional).

Order: Entry after the confirmation candle closes or a limit close to VWAP.

Trade Management:

Stop: Below the bounce low or 0.6xATR(1M) (strongest).

Target: 0.4–0.7xATR(1M) or the previous micro-high (small return to increase success rate).

Trigger: Move the stop to breakeven after +0.25R; close manually if the 1M candle closes strongly against you.

Filter: Do not trade if the spread widens, or the price "saws" around VWAP without a trend.

Sell against the rules in a downtrend.

Why this plan raises the heat-rate? You buy a "small discount" within an existing trend and near the institutional average price (VWAP), with a small target price.

مواقعي شركة الماسة للخدمات المنزلية

شركة تنظيف بالرياض

نقل عفش بالرياض

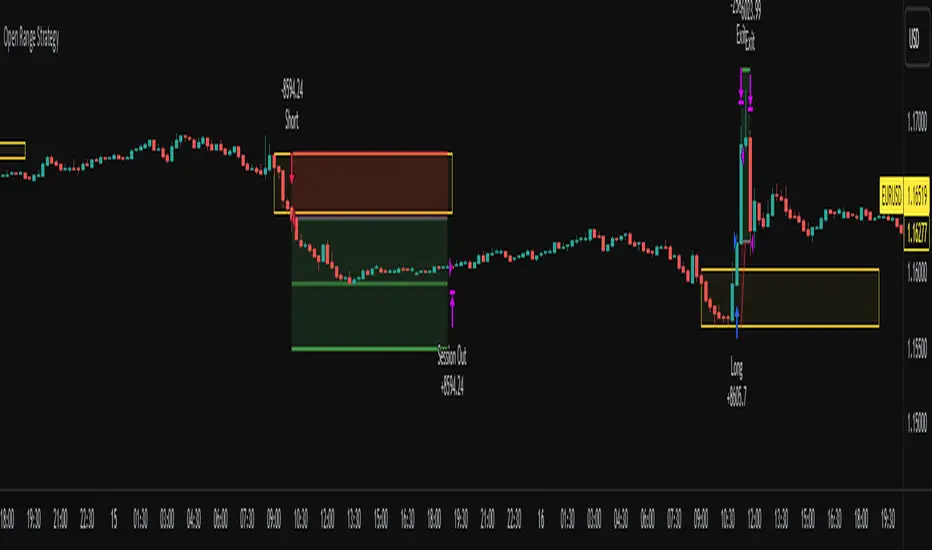

Open Range Breakout Strategy With Multi TakeProfitHello everyone,

For a while, I’ve been wanting to develop new scripts, but I couldn’t decide what to create. Eventually, I came up with the idea of coding traditional and well-known trading strategies—while adding modern features such as multi–take profit options. For the first strategy in this series, I chose the Open Range Strategy .

For those unfamiliar with it, the Open Range Strategy is a trading approach where you define a specific time period at the beginning of a trading session—such as the first 15 minutes, 30 minutes, or 1 hour—and mark the highest and lowest prices within that range. These levels then act as reference points for potential breakouts: if the price breaks above the range, it may signal a long entry; if it breaks below, it may indicate a short entry. This method is popular among day traders for capturing early momentum in the market.

Since this strategy is generally used as an intraday strategy , I added a Trade Session feature. This allows you to define the exact time window during which trades can be opened. Once the session ends, all positions are automatically closed, ensuring trades remain within your chosen intraday period.

Even though it’s a relatively simple concept, I’ve come across many different variations of it. That’s why I created a highly customizable project. Under the Session Settings, you can select the time window you want to define as your range. Whether it’s the first 15-minute candle or the entire first hour, the choice is entirely yours.

For stop-loss placement, there are two different options:

Middle of the Range – The stop loss is placed at the midpoint between the high and low of the defined range, offering a balanced buffer for both bullish and bearish setups.

Top/Bottom of the Range – The stop loss is placed just beyond the range’s high for short trades or just below the range’s low for long trades, providing a more conservative risk approach.

I’ve always been a big fan of the multi take-profit feature, so I added two different take-profit targets to this project. Take profits are calculated based on a Risk-to-Reward Ratio, which you can adjust in the settings. You can also set different position sizes for each target, allowing you to scale out of trades in a way that suits your strategy.

The result is a flexible, user-friendly strategy script that brings together a classic approach with modern risk management tools—ready to be tailored to your trading style

ZapTeam Pro Strategy v6 — EMA The Pro Strategy v6 script is a versatile trading strategy for TradingView that combines trend indicators, filters, and levels.

Main features:

EMA 21, EMA 50, EMA 200 — trend detection and entry signals via EMA crossovers.

Ichimoku Cloud (optional) — trend filtering and price position relative to the cloud.

ETH Dominance filter (optional) — filters trades based on Ethereum dominance (ETH.D).

ATR Stop-Loss — dynamic stop-loss based on volatility.

Two take-profits (TP1 and TP2) with optional 50/50 split.

Dynamic Fibonacci Levels — automatic or manual swings, with 1.272 and 1.618 extensions.

Custom S/R Levels — user-defined support/resistance levels.

Level lines extend across the chart and automatically adjust when zooming or panning.

Designed for trading in trending market conditions on any timeframe.

The strategy calculates position size based on percentage risk per equity.

[Stratégia] VWAP Mean Magnet v9 (Simple Alert)This strategy is specifically designed for a ranging (sideways-moving) Bitcoin market.

A trade is only opened and signaled on the chart if all three of the following conditions are met simultaneously at the close of a candle:

Zone Entry

The price must cross into the signal zone: the red band for a Short (sell) position, or the green band for a Long (buy) position.

RSI Confirmation

The RSI indicator must also confirm the signal. For a Short, it must go above 65 (overbought condition). For a Long, it must fall below 25 (oversold condition).

Volume Filter

The volume on the entry candle cannot be excessively high. This safety filter is designed to prevent trades during risky, high-momentum breakouts.

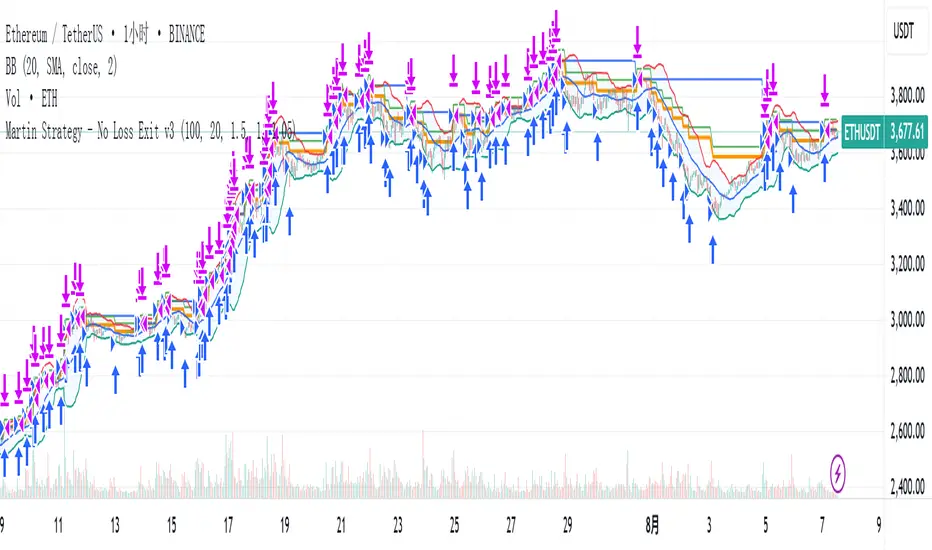

Martin Strategy - No Loss Exit v3Martin Strategy - No Loss Exit v3Martin Strategy - No Loss Exit v3Martin Strategy - No Loss Exit v3

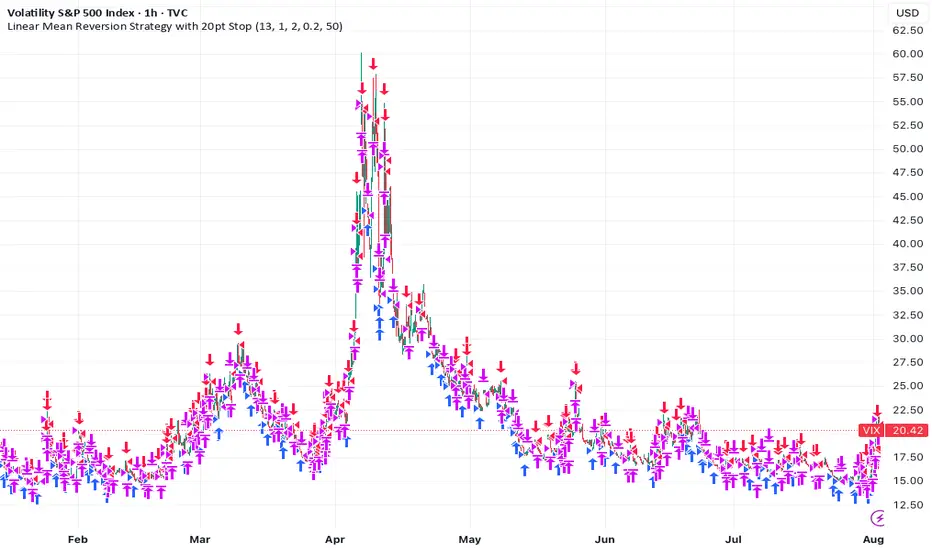

Linear Mean Reversion Strategy📘 Strategy Introduction: Linear Mean Reversion with Fixed Stop

This strategy implements a simple yet powerful mean reversion model that assumes price tends to oscillate around a dynamic average over time. It identifies statistically significant deviations from the moving average using a z-score, and enters trades expecting a return to the mean.

🧠 Core Logic:

A z-score is calculated by comparing the current price to its moving average, normalized by standard deviation, over a user-defined half-life window.

Trades are entered when the z-score crosses a threshold (e.g., ±1), signaling overbought or oversold conditions.

The strategy exits positions either when price reverts back near the mean (z-score close to 0), or if a fixed stop loss of 100 points is hit, whichever comes first.

⚙️ Key Features:

Dynamic mean and volatility estimation using moving average and standard deviation

Configurable z-score thresholds for entry and exit

Position size scaling based on z-score magnitude

Fixed stop loss to control risk and avoid prolonged drawdowns

🧪 Use Case:

Ideal for range-bound markets or assets that exhibit stationary behavior around a mean, this strategy is especially useful on assets with mean-reverting characteristics like currency pairs, ETFs, or large-cap stocks. It is best suited for traders looking for short-term reversions rather than long-term trends.