Jace's Raff ChannelJust a basic, no-frills, Raff Regression channel. You can adjust the regression length and provide a starting point offset.

Regressions

Lorentzian Length Adaptive Moving Average [LLAMA] Adaptation of "Machine Learning: Lorentzian Classification" by

Gradient color by base on work by

LLAMA: A regime-aware adaptive moving average that bends with the market.

Start with a problem traders know:

Traditional moving averages are either too slow (EMA200) or too fast (EMA9)

Adaptive MAs exist, but they often hug price too tightly or smooth too much, failing to balance bias and tactics

LLAMA uses a Lorentzian distance function to adapt its length dynamically. Instead of a fixed smoothing window, it stretches or contracts depending on market conditions. This distortion reduces lag while still providing a clear bias line.

The indicator looks back at recent bars and measures how similar they are using a Lorentzian distance (a log‑scaled absolute difference). It keeps track of the “nearest neighbors” — bars that most resemble the current regime. Each neighbor carries a label (long, short, neutral) based on simple price comparisons. By averaging these labels, LLAMA predicts whether the market is leaning bullish or bearish. That prediction is then mapped into a dynamic length between and .

Bullish bias -> length stretches toward max (smoother, more stable).

Bearish bias -> length contracts toward min (snappier, more reactive).

During breakouts, LLAMA tightens and comes into contact with bars, giving actionable signals. During chop, it stretches to avoid false triggers. It covers both ends of the spectrum (bias and tactics) in one line, something static MA's can't do.

Think of LLAMA as a lens that bends with the market:

Wide lens (max length) for big picture bias.

Narrow lens (min length) for tactical precision.

The "Lorentzian Loop" is the math that decides when to widen or narrow.

R Dominante by Mata (CRT Madre + CRT Interior)Dominant Range (Green + Red + Outstanding Lines)

This script automatically identifies the dominant parent candle (CRT – Candle Range Theory) and draws its range with a green box. It also allows you to create independent red parent candles that function autonomously.

Main Features:

Main Green Box: Represents the dominant parent candle, following the actual CRT:

It is activated and remains active while the price reaches the extremes.

It is only invalidated if there is a close outside the range.

It is automatically deactivated when it reaches both extremes (high and low).

Independent Red Box: Detects ranges independent of the green box and is deactivated when both extremes are reached.

Fully Automatic: No manual range adjustments required.

Configuration: Adjust the transparency of the boxes and the maximum number of bars to review.

Recommended Use:

Ideal for traders who apply Candle Range Theory (CRT).

Allows for clear identification of dominant and secondary ranges.

Useful for determining touch points of extremes and planning strategic entries and exits.

EPS Trendline (Fundamentals Insight by Mazhar Karimi)Overview

This indicator visualizes a company’s Earnings Per Share (EPS) data directly on the chart—pulled from TradingView’s fundamental database—and applies a dynamic linear regression trendline to highlight the long-term direction of earnings growth or decline.

It’s designed to help investors and quantitative traders quickly see how the company’s profitability (EPS) has evolved over time and whether it’s trending upward (growth), flat (stagnant), or downward (decline).

How it Works

Uses request.financial() to fetch EPS data (Diluted or Basic).

You can select whether to use TTM (Trailing Twelve Months), FQ (Fiscal Quarter), or FY (Fiscal Year) data.

The script fits a regression line (using ta.linreg) over a configurable window to visualize the underlying EPS trend.

Updates automatically when new financial data is released.

Inputs

EPS Period: Choose between FQ / FY / TTM

Use Diluted EPS: Toggle to compare Diluted vs. Basic EPS

Regression Window: Adjust how many bars are used to fit the trendline

Interpretation Tips

A rising trendline indicates earnings momentum and potential investor confidence.

A flat or declining trendline may warn of profitability slowdowns.

Combine with price action or valuation ratios (like P/E) for deeper analysis.

Works best on stocks or ETFs with fundamental data (not available for crypto or FX).

Suggestions / Use Cases

Pair with Price/Earnings ratio indicators to evaluate valuation vs. fundamentals.

Use in conjunction with earnings release events for context.

Ideal for long-term investors, swing traders, or fundamental quants tracking financial health trends.

Future Enhancements (Planned Ideas)

🔹 Option to display multiple regression lines (short-term and long-term)

🔹 Support for comparing multiple tickers’ EPS in the same pane

🔹 Integration with Net Income, Revenue, or Free Cash Flow trends

🔹 Add a “Rate of Change” signal for momentum-based EPS analysis

BB SPY Mean Reversion Investment StrategySummary

Mean reversion first, continuation second. This strategy targets equities and ETFs on daily timeframes. It waits for price to revert from a Bollinger location with candle and EMA agreement, then manages risk with ATR based exits. Uniqueness comes from two elements working together. One, an adaptive band multiplier driven by volatility of volatility that expands or contracts the envelope as conditions change. Two, a bias memory that re arms the same direction after any stop, target, or time exit until a true opposite signal appears. Add it to a clean chart, use the markers and levels, and select on bar close for conservative alerts. Shapes can move while the bar is open and settle on close.

Scope and intent

• Markets. Currently adapted for SPY, needs to be optimized for other assets

• Timeframes. Daily primary. Other frames are possible but not the default

• Default demo. SPY on daily

• Purpose. Trade mean reversion entries that can chain into a longer swing by splitting holds into ATR or time segments

Originality and usefulness

• Novelty. Adaptive band width from volatility of volatility plus a persistent bias array that keeps the original direction alive across sequential entries until an opposite setup is confirmed

• Failure modes mitigated. False starts in chop are reduced by candle color and EMA location. Missed continuation after a take profit or stop is addressed by the re arm engine. Oversized envelopes during quiet regimes are avoided by the adaptive multiplier

• Testability. Every module has Inputs and visible levels so users can see why a suggestion appears

• Portable yardstick. All risk and targets are expressed in ATR units

Method overview in plain language

The engine measures where price sits relative to Bollinger bands, confirms with candle color and EMA location, requires ADX for shorts(in our case long close since we use it currently as long only), and optionally requires a trend or mean reversion regime using band width percent rank and basis slope. Risk uses ATR for stop, target, and optional breakeven. A small array stores the last confirmed direction. While flat, the engine keeps a pending order in that direction. The array flips only when a true opposite setup appears.

Base measures

• Range basis. True Range smoothed over a user defined ATR Length

• Return basis. Not required

Components

• Bollinger envelope. SMA length and standard deviation multiplier. Entry is based on cross of close through the band with location bias

• Candle and EMA filter. Close relative to open and close relative to EMA align direction

• ADX gate for shorts. Requires minimum trend strength for short trades

• Adaptive multiplier. Band width scales using volatility of volatility so envelopes breathe with conditions

• Regime gate optional. Band width percent rank and basis slope identify trend or mean reversion regimes

• Risk manager. ATR stop, ATR target, optional breakeven, optional time exit

• Bias memory. Array stores last confirmed direction and re arms entries while flat

Fusion rule

Minimum satisfied gates count style. All required gates must be true. Optional gates are controlled in Inputs. Bias memory never overrides an opposite confirmed setup.

Signal rule

• Long setup when close crosses up through the lower band, the bar closes green, and close is above the long EMA

• Short setup when close crosses down through the upper band, the bar closes red, close is below the short EMA, and ADX is above the minimum

• While flat the model keeps a pending order in the stored direction until a true opposite setup appears

• IN LONG or IN SHORT describes states between entry and exit

What you will see on the chart

• Markers for Long and Short setups

• Exit markers from ATR or time rules

• Reference levels for entry, stop, and target

• Bollinger bands and optional adaptive bands

Inputs with guidance

Setup

• Signal timeframe. Uses the chart timeframe

• Invert direction optional. Flips long and short

Logic

• BB Length. Typical 10 to 50. Higher smooths more

• BB Mult. Typical 1.0 to 2.5. Higher widens entries

• EMA Length long. Typical 10 to 50

• EMA Length short. Typical 5 to 30

• ADX Minimum for short. Typical 15 to 35

Filters

• Regime Type. none or trend or mean reversion

• Rank Lookback. Typical 100 to 300

• Basis Slope Length and Threshold. Larger values reduce false trends

Risk

• ATR Length. Typical 10 to 21

• ATR Stop Mult. Typical 1.0 to 3.0

• ATR Take Profit Mult. Typical 2.0 to 5.0

• Breakeven Trigger R. Move stop to entry after the chosen multiple

• Time Exit. Minimum bars and extension when profit exceeds a fraction of ATR

Bias and rearm

• Bias flips kept. Array depth

• Keep rearm when flat. Maintain a pending order while flat

UI

• Show markers and levels. Clean defaults

Usage recipes

Alerts update in real time and can change while the bar forms. Select on bar close for conservative workflows.

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• If any higher timeframe calls are enabled, request.security uses lookahead off

• Commission 0.03 percent

• Slippage 3 ticks

• Default order size method Percent of equity with value 5

• Pyramiding 0

• Process orders on close On

• Bar magnifier Off

• Recalculate after order is filled Off

• Calc on every tick Off

Realism and responsible publication

No performance claims. Costs and fills vary by venue. Shapes can move intrabar and settle on close. Strategies use standard candles only.

Honest limitations and failure modes

High impact releases and thin liquidity can break assumptions. Gap heavy symbols may require larger ATR. Very quiet regimes can reduce contrast in the mean reversion signal. If stop and target can both be touched inside one bar, outcome follows the TradingView order model for that bar path.

Regimes with extreme one sided trend and very low volatility can reduce mean reversion edges. Results vary by symbol and venue. Past results never guarantee future outcomes.

Open source reuse and credits

None.

Backtest realism

Costs are realistic for liquid equities. Sizing does not exceed five percent per trade by default. Any departure should be justified by the user.

If you got any questions please le me know

Hybrid Linear Regression Channel with Fibonacci LevelsHow to Use the LRC Fib Hybrid Indicator (Detailed Guide)

1. Read the Trend

2.The thick blue line is the linear regression midline.

If it’s sloping upward → uptrend (favor longs).

If sloping downward → downtrend (favor shorts).

The gray channel bounds are ±2 standard deviations (adjustable).

3. Understand Fibonacci Levels

Fib lines are projected parallel to the regression slope using the channel width as 100%:

Red dashed lines (0.0 to 0.786): Support zones in uptrends.

Blue dashed line (0.5): Midline/neutral.

Green dashed lines (1.0 to 2.618): Resistance zones in downtrends.

Strongest levels: 0.618 (support) and 1.618 (resistance).

4. Buy Signal (Long Entry)

Triggered when:

Midline is rising (uptrend confirmed).

Price crosses above a red Fib level (0.0–0.786).

Volume > 20-period average (if confirmation enabled).

Action:

Enter long on the green triangle (▲).

Stop Loss: Below the lower gray channel or recent swing low.

Take Profit: At 1.0, 1.272, or 1.618 green Fibs.

5. Sell Signal (Short Entry)

Triggered when:

Midline is falling (downtrend).

Price crosses below a green Fib level (1.272–2.618).

Volume > average.

Action:

Enter short on the red triangle (▼).

Stop Loss: Above the upper gray channel.

Take Profit: At 1.0, 0.786, or 0.618 red Fibs.

6. Use the Info Table (Bottom-Right)

Shows live prices of all Fib levels, current trend ("Up"/"Down"), and signal status ("BUY"/"SELL"/"None").

7. Customize via Settings (Gear Icon)

Regression Length: 50–200 (shorter = faster response).

Std Dev Multiplier: 1.5–3.0 (tighter/wider channel).

Toggle Fibs: Hide unused levels to declutter.

Volume Confirmation: Turn off for pure price action.

8. Set Alerts

Right-click chart → Add Alert → Select "Buy Signal" or "Sell Signal" → Enable popup/email/webhook.

9. Best Practices

Best in trending markets (avoid chop).

Wait for volume spike on bounce.

Combine with higher timeframe bias.

Use 0.618/1.618 as primary reversal zones.

This indicator gives you adaptive trend, precise entries, volume filter, and dynamic targets — all in one clean overlay.

Henry's MA & RSProviding 10 21 50 200 MA and RS rating based on S&P 500, basically for US stocks. Enjoy!

NSR - Dynamic Linear Regression ChannelOverview

The NSR - Dynamic Linear Regression Channel is a powerful overlay indicator that plots a dynamic regression-based channel around price action. Unlike static channels, this tool continuously recalculates the linear regression trendline from a user-defined starting point and builds upper and lower boundaries using a combination of standard deviation and maximum price deviations (highs/lows).

It visually separates "Premium" (overvalued) and "Discount" (undervalued) zones relative to the regression trend — ideal for mean-reversion, breakout, or trend-following strategies.

Key Features

Dynamic Regression Line Calculates slope, intercept, and average using full lookback from a reset point.

Adaptive Channel Width Combines standard deviation of residuals with max high/low deviations for robust boundaries.

Auto-Reset on Breakout Channel resets when price closes beyond upper/lower band twice in direction of trend .

Visual Zones Blue shaded = Premium (resistance zone)

Red shaded = Discount (support zone)

Real-Time Updates Live channel extends with each bar; historical channels preserved on reset.

How It Works

Regression Calculation

Uses all bars since last reset to compute the best-fit line:

y = intercept + slope × bar_position

Deviation Bands

Statistical : Standard deviation of price from regression line

Structural : Maximum distance from highs to line (upper) and lows to line (lower)

Final band = Regression Line ± (Deviation Input × StdDev)

Channel Reset Logic

Resets when:

Price closes above upper band twice in an uptrend (slope > 0)

OR closes below lower band twice in a downtrend (slope < 0)

Prevents overextension and adapts to new trends.

Visual Output

Active channel updates in real-time

Completed channels saved as historical reference (up to 500 lines/boxes)

Input Parameters

Deviation (2.0) - Multiplier for standard deviation to set channel width

Premium Color - blue color for upper (resistance) zone

Discount Color - red color for lower (support) zone

Best Use Cases

Mean Reversion - Buy near lower band in uptrend, sell near upper band

Breakout Trading - Enter on confirmed close beyond band + volume

Trend Confirmation - Use slope direction + price position in channel

Stop Loss / Take Profit - Place stops beyond opposite band

Pro Tips

Use on higher timeframes (4H, Daily) for cleaner regression fits

Combine with volume or momentum to filter false breakouts

Lower Deviation (e.g., 1.5) for tighter, more responsive channels

Watch channel resets — they often mark significant trend shifts

Why Use DLRC?

"Most channels are static. This one evolves with the market."

The NSR-DLRC gives you a mathematically sound, visually intuitive way to see:

Where price should be (regression)

Where it has been (deviation extremes)

When the trend is breaking structure

Perfect for traders who want regression-based precision without rigid assumptions.

Add to chart → Watch price dance within the evolving trend corridor.

Dual Harmonic-based AHR DCA (Default :BTC-ETH)A panel indicator designed for dual-asset BTC/ETH DCA (Dollar Cost Averaging) decisions.

It is inspired by the Chinese community indicator "AHR999" proposed by “Jiushen”.

How to use:

Lower HM-based AHR → cheaper (potential buy zone).

Higher HM-based AHR → more expensive (potential risk zone).

Higher than Risk Threshold → consider to sell, but not suitable for DCA.

When both AHR lines are below the Risk threshold → buy the cheaper one (or split if similar).

If one AHR is above Risk → buy the other asset.

If both are above Risk → simulation shows “STOP (both risk)”.

Not limited to BTC/ETH — you can freely change symbols in the input panel

to build any dual-asset DCA pair you want (e.g., BTC/BNB, ETH/SOL, etc.).

What you’ll see:

Two lines: AHR BTC (HM) and AHR ETH (HM)

Two dashed lines: OppThreshold (green) and RiskThreshold (red)

Colored fill showing which asset is cheaper (BTC or ETH)

Buy markers:

- B = Buy BTC

- E = Buy ETH

- D = Dual (split budget)

Top-right table: prices, AHRs, thresholds, qOpp/qRisk%, simulation, P&L

Labels showing last-bar AHR values

Core idea:

Use an AHR based on Harmonic Moving Average (HM) — a ratio that measures how “cheap or expensive” price is relative to both its short-term mean and long-term trend.

The original AHR999 used SMA and was designed for BTC only.

This indicator extends it with cross-exchange percentile mapping, allowing the empirical “opportunity/risk” zones of the AHR999 (on Bitstamp) to adapt automatically to the current market pair.

The indicator derives two adaptive thresholds:

OppThreshold – opportunity zone

RiskThreshold – risk zone

These thresholds are compared with the current HM-based AHR of BTC and ETH to decide which asset is cheaper, and whether it is good to DCA or not, or considering to sell(When it in risk area).

This version uses

Display base: Binance (default: perpetual) with HM-based AHR

Percentile base: Bitstamp spot SMA-AHR (complete, stable history)

Rolling window: 2920 daily bars (~8 years) for percentile tracking

Concept summary

AHR measures the ratio of price to its long-term regression and short-term mean.

HM replaces SMA to better reflect equal-fiat-cost DCA behavior.

Cross-exchange percentile mapping (Bitstamp → Binance) keeps thresholds consistent with the original AHR999 interpretation.

Recommended settings (1D):

DCA length (harmonic): 200

Log-regression lookback: 1825 (≈5 years)

Rolling window: 2920 (≈8 years)

Reference thresholds: 0.45 / 1.20 (AHR999 empirical priors)

Tie split tolerance (ΔAHR): 0.05

Daily budget: 15 USDT (simulation)

All display options can be toggled: table, markers, labels, etc.

Notes:

When the rolling window is filled (2920 bars by default), thresholds are first calculated and then visually backfilled as left-extended lines.

The “buy markers” and “decision table” are light simulations without fees or funding costs — for rhythm and relative analysis, not backtesting.

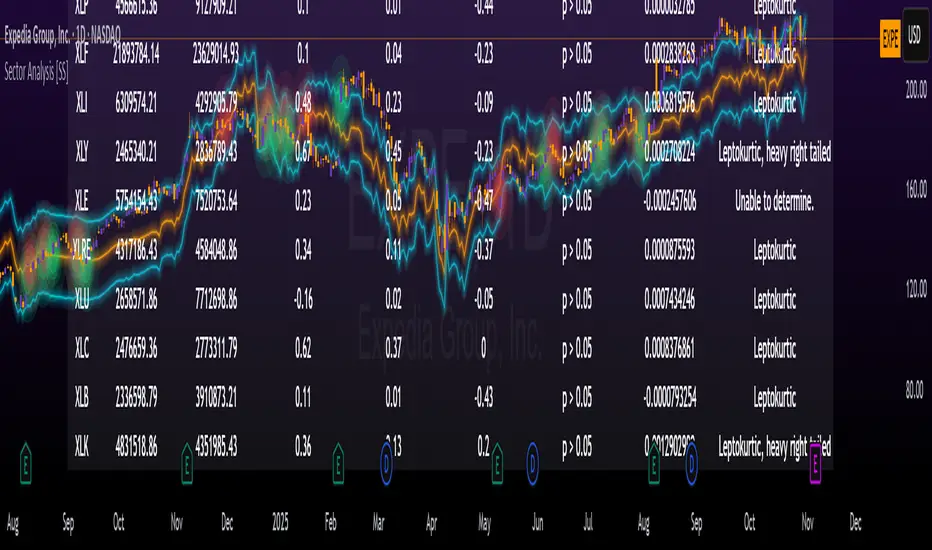

Sector Analysis [SS]Introducing the most powerful sector analysis tool/indicator available, to date, in Pine!

This is a whopper indicator, so be sure to read carefully to ensure you understand its applications and uses!

First of all, because this is a whopper, let's go over the key functional points of the indicator.

The indicator compares the 11 main sector ETFs against whichever ticker you are looking at.

The functions include the following:

Ability to pull technicals from the sectors, such as RSI, Stochastic and Z-Score;

Ability to look at the correlation of the sector ETF to the current ticker you are looking at.

Ability to calculate the R2 value between the ticker you are looking at and each sector.

The ability to run a Two Tailed T-Test against the log returns of the Ticker of interest and the Sector (to analyze statistically significant returns between sectors/tickers).

The ability to analyze the distribution of returns across all sector ETFs.

The ability to pull buying and selling volume across all sector ETFs.

The ability to create an integrated moving average using a sector ETF to predict the expected close range of a ticker of interest.

These are the highlight functions. Below, I will go more into them, what they mean and how to use them.

Pulling Technicals

This is pretty straight forward. You can pull technicals, such as RSI, Stochastic and Z-Score from all the sector ETFs and view them in a table.

See below for the example:

Pulling Correlation

In order to see which sector your ticker of interest follows more closely, we need to look first at correlation and then at R2.

The correlation will look at the immediate relationship over a specified time. A highly positive value, indicates a strong, symbiotic relationship, which the sector and the ticker follow each other. This would be represented by a correlation of 0.8 or higher.

A strong negative correlation, such as -0.8 or lower, indicates that the sector and the ticker are completely opposite. When one goes up, the other goes down and vice versa.

You can adjust your correlation assessment length directly in the settings menu:

If you want to use a sector ETF to find the expected range for a ticker of interest, it is important to locate the highest, POSITIVE, correlation value. Here are the results for MSFT at a correlation lookback of 200:

In this example, we can see the best relationship is with the ETF XLK.

Analysis of R2

R2 is an important metric. It essentially measures how much of the variance between 2 tickers are explained by a simple, linear relationship.

A high R2 means that a huge degree of variance can be explained between the 2 tickers. A low R2 means that it cannot and that the 2 tickers are likely not integrated or closely related.

In general, if you want to use the sector ETF to find the mean and trading range and identify over-valuation/over-extension and under-extension statistically, you need to see both a high correlation and a high R-Squared. These 2 metrics should be analyzed together.

Let's take a look at MSFT:

Here, despite the correlation implying that XLK was the ticker we should use to analyze, when we look at the R Squared, we see actually, we should be using XLI.

XLI has a strong positive relationship with MSFT, albeit a bit less than XLK, but the R2 is solid, > 0.9, indicating the XLI explains much of MSFT's variance.

Two Tailed T-Test

A two tailed T-test analyzes whether there is a statistically significant difference between 2 different groups, or in our case, tickers.

The T-Test is conducted on the log returns of the ticker of interest and the sector. You then can see the P value results, whether it is significant or not. Let's look at MSFT again:

Looking at this, we can see there is no statistically significant difference in returns between MSFT and any of the sectors.

We can also see the SMA of the log returns for more detailed comparison.

If we were to observe a significant finding on the T-Test metrics, this would indicate that one sector either outperforms or underperforms your ticker to a statistically significant degree! If you stumble upon this, you would check the average log returns to compare against the average returns of your ticker of interest, to see whether there is better performance or worse performance from the sector ETF vs. your ticker of interest.

Analyzing the Distribution

The indicator will also analyze the distribution of returns.

This is an interesting option as it can help you ascertain risk. Normally distributed returns imply mean reverting behavviour. Deviations from that imply trending behaviour with higher risk expectancy. If we look at the distribution statistics currently over the last 200 trading days, here are the results:

Here, we can see all show signs of trending, as none of the returns are normally distributed. The highest risk sectors are XLK and XLY.

Why are they the highest risk?

Because the indicator has found a heavy right tailed distribution, indicated sudden and erratic mean reversion/losses are possible.

Creating an MA

Now for the big bonus of the indicator!

The indicator can actually create a regression based range from closely correlated sectors, so you can see, in sectors that are strongly correlated to your ticker, whether your ticker is over-bought, oversold or has mean reverted.

Let's look at MSFT using XLI, our previously identified sector with a high correlation and high R2 value:

The results are pretty impressive.

You can see that MSFT has rode the mean of the sector on the daily timeframe for quite some time. Each time it over extended itself above the sector implied range, it mean reverted.

Currently, if you were to trade based on Pairs or statistics, MSFT is no trade as it is currently trading at its sector mean.

If you are a visual person, you can have the indicator plot the mean reversion points directly:

Green represents a bullish mean reversion and red a bearish mean reversion.

Concluding Remarks

If you like pair trading, following the link between sectors and tickers or want a more objective way to determine whether a ticker is over-bought or oversold, this indicator can help you.

In addition to doing this, the indicator can provide risk insights into different sectors by looking at the distribution, as well as identify under-performing sectors or tickers.

It can also shed light on sectors that may be technically over-bought or oversold by looking at Z-Score, stochastics and RSI.

Its a whopper and I really hope you find it helpful and useful!

Thanks everyone for reading and checking this out!

Safe trades!

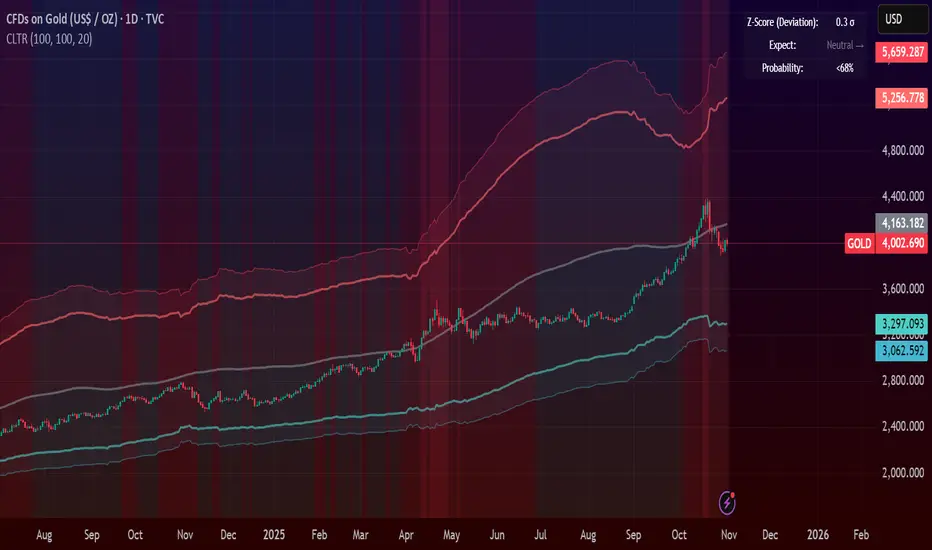

Central Limit Theorem Reversion IndicatorDear TV community, let me introduce you to the first-ever Central Limit Theorem indicator on TradingView.

The Central Limit Theorem is used in statistics and it can be quite useful in quant trading and understanding market behaviors.

In short, the CLT states: "When you take repeated samples from any population and calculate their averages, those averages will form a normal (bell curve) distribution—no matter what the original data looks like."

In this CLT indicator, I use statistical theory to identify high-probability mean reversion opportunities in the markets. It calculates statistical confidence bands and z-scores to identify when price movements deviate significantly from their expected distribution, signaling potential reversion opportunities with quantifiable probability levels.

Mathematical Foundation

The Central Limit Theorem (CLT) says that when you average many data points together, those averages will form a predictable bell-curve pattern, even if the original data is completely random and unpredictable (which often is in the markets). This works no matter what you're measuring, and it gets more reliable as you use more data points.

Why using it for trading?

Individual price movements seem random and chaotic, but when we look at the average of many price movements, we can actually predict how they should behave statistically. This lets us spot when prices have moved "too far" from what's normal—and those extreme moves tend to snap back (mean reversion).

Key Formula:

Z = (X̄ - μ) / (σ / √n)

Where:

- X̄ = Sample mean (average return over n periods)

- μ = Population mean (long-term expected return)

- σ = Population standard deviation (volatility)

- n = Sample size

- σ/√n = Standard error of the mean

How I Apply CLT

Step 1: Calculate Returns

Measures how much price changed from one bar to the next (using logarithms for better statistical properties)

Step 2: Average Recent Returns

Takes the average of the last n returns (e.g., last 100 bars). This is your "sample mean."

Step 3: Find What's "Normal"

Looks at historical data to determine: a) What the typical average return should be (the long-term mean) and b) How volatile the market usually is (standard deviation)

Step 4: Calculate Standard Error

Determines how much sample averages naturally vary. Larger samples = smaller expected variation.

Step 5: Calculate Z-Score

Measures how unusual the current situation is.

Step 6: Draw Confidence Bands

Converts these statistical boundaries into actual price levels on your chart, showing where price is statistically expected to stay 95% and 99% of the time.

Interpretation & Usage

The Z-Score:

The z-score tells you how statistically unusual the current price deviation is:

|Z| < 1.0 → Normal behavior, no action

|Z| = 1.0 to 1.96 → Moderate deviation, watch closely

|Z| = 1.96 to 2.58 → Significant deviation (95%+), consider entry

|Z| > 2.58 → Extreme deviation (99%+), high probability setup

The Confidence Bands

- Upper Red Bands: 95% and 99% overbought zones → Expect mean reversion downward as the price is not likely to cross these lines.

- Center Gray Line: Statistical expectation (fair value)

- Lower Blue Bands: 95% and 99% oversold zones → Expect mean reversion upward

Trading Logic:

- When price exceeds the upper 95% band (z-score > +1.96), there's only a 5% probability this is random noise → Strong sell/short signal

- When price falls below the lower 95% band (z-score < -1.96), there's a 95% statistical expectation of upward reversion → Strong buy/long signal

Background Gradient

The background color provides real-time visual feedback:

- Blue shades: Oversold conditions, expect upward reversion

- Red shades: Overbought conditions, expect downward reversion

- Intensity: Darker colors indicate stronger statistical significance

Trading Strategy Examples

Hypothetically, this is how the indicator could be used:

- Long: Z-score < -1.96 (below 95% confidence band)

- Short: Z-score > +1.96 (above 95% confidence band)

- Take profit when price returns to center line (Z ≈ 0)

Input Parameters

Sample Size (n) - Default: 100

Lookback Period (m) - Default: 100

You can also create alerts based on the indicator.

Final notes:

- The indicator uses logarithmic returns for better statistical properties

- Converts statistical bands back to price space for practical use

- Adaptive volatility: Bands automatically widen in high volatility, narrow in low volatility

- No repainting: yay! All calculations use historical data only

Feedback is more than welcome!

Henri

NLR-ADX Divergence Strategy Triple-ConfirmedHow it works

Builds a cleaner DMI/ADX

Recomputes classic +DI, −DI, ADX over a user-set length.

Then “non-linear regresses” each series toward a mean (your choice: dynamic EMA of the series or a fixed Static Mid like 50).

The further a value is from the mean, the stronger the pull (controlled by alphaMin/alphaMax and the γ exponent), giving smoother, more stable DI/ADX lines with less whipsaw.

Optional EMA smoothing on top of that.

Lock in values at confirmed pivots

Uses price pivots (left/right bars) to confirm swing lows and highs.

When a pivot confirms, the script captures (“freezes”) the current +DI, −DI, and ADX values at that bar and stores them. This avoids later drift from smoothing/EMAs.

Check for triple divergence

For a bullish setup (potential long):

Price makes a Lower Low vs. a prior pivot low,

+DI is higher than before (bulls quietly stronger),

−DI is lower (bears weakening),

ADX is lower (trend fatigue).

For a bearish setup (potential short)

Price makes a Higher High,

+DI is lower, −DI is higher,

ADX is lower.

Adds a “no-intersection” sanity check: between the two pivots, the live series shouldn’t snake across the straight line connecting endpoints. This filters messy, low-quality structures.

Trade logic

On a valid triple-confirm, places a strategy.entry (Long for bullish, Short for bearish) and optionally labels the bar (BUY or SELL with +DI/−DI/ADX arrows).

Simple flip behavior: if you’re long and a new short signal prints (or vice versa), it closes the open side and flips.

Key inputs you can tweak

Custom DMI Settings

DMI Length — base length for DI/ADX.

Non-Linear Regression Model

Mean Reference — EMA(series) (dynamic) or Static mid (e.g., 50).

Dynamic Mean Length & Deviation Scale Length — govern the mean and scale used for regression.

Min/Max Regression & Non-Linearity Exponent (γ) — how strongly values are pulled toward the mean (stronger when far away).

Divergence Engine

Pivot Left/Right Bars — how strict the swing confirmation is (larger = more confirmation, more delay).

Min Bars Between Pivots — avoids comparing “near-duplicate” swings.

Max Historical Pivots to Store — memory cap.

Rolling Correlation vs Another Symbol (SPY Default)This indicator visualizes the rolling correlation between the current chart symbol and another selected asset, helping traders understand how closely the two move together over time.

It calculates the Pearson correlation coefficient over a user-defined period (default 22 bars) and plots it as a color-coded line:

• Green line → positive correlation (move in the same direction)

• Red line → negative correlation (move in opposite directions)

• A gray dashed line marks the zero level (no correlation).

The background highlights periods of strong relationship:

• Light green when correlation > +0.7 (strong positive)

• Light red when correlation < –0.7 (strong negative)

Use this tool to quickly spot diversification opportunities, confirm hedges, or understand how assets interact during different market regimes.

VWAP Composites📊 VWAP Composite - Advanced Multi-Period Volume Weighted Average Price Indicator

═══════════════════════════════════════════════════════════════════

🎯 OVERVIEW

VWAP Composite is an advanced volume-weighted average price (VWAP) indicator that goes beyond traditional single-period VWAP calculations by offering composite multi-period analysis and unprecedented customization. This indicator solves a common problem traders face: traditional VWAP resets at arbitrary intervals (session start, day, week), but significant price action and volume accumulation often spans multiple periods. VWAP Composite allows you to anchor VWAP calculations to any timeframe—or combine multiple periods into a single composite VWAP—giving you a true representation of average price weighted by volume across the exact periods that matter to your analysis.

═══════════════════════════════════════════════════════════════════

⚙️ HOW IT WORKS - CALCULATION METHODOLOGY

📌 CORE VWAP CALCULATION

The indicator calculates VWAP using the standard volume-weighted formula:

• Typical Price = (High + Low + Close) / 3

• VWAP = Σ(Typical Price × Volume) / Σ(Volume)

This calculation is performed across user-defined time periods, ensuring each bar's contribution to the average is proportional to its trading volume.

📌 STANDARD DEVIATION BANDS

The indicator calculates volume-weighted standard deviation to measure price dispersion around the VWAP:

• Variance = Σ / Σ(Volume)

• Standard Deviation = √Variance

• Upper Band = VWAP + (StdDev × Multiplier)

• Lower Band = VWAP - (StdDev × Multiplier)

These bands help identify overbought/oversold conditions relative to the volume-weighted mean, with high-volume price excursions having greater impact on band width than low-volume moves.

📌 COMPOSITE PERIOD METHODOLOGY (Auto Mode)

Unlike traditional VWAP that resets at fixed intervals, Auto Mode creates composite VWAPs by combining the current period with N previous periods:

• Period Span = 1: Current period only (standard VWAP behavior)

• Period Span = 2: Current period + 1 previous period combined

• Period Span = 3: Current period + 2 previous periods combined

• And so on...

Example: A 3-period Weekly composite VWAP calculates from the start of 2 weeks ago through the current week's end, creating a single VWAP that represents 21 days of continuous price and volume data. This provides context about where price stands relative to the volume-weighted average over multiple weeks, not just the current week.

═══════════════════════════════════════════════════════════════════

🔧 KEY FEATURES & ORIGINALITY

✅ DUAL OPERATING MODES

1️⃣ MANUAL MODE (5 Independent VWAPs)

Define up to 5 separate VWAP calculations with custom start/end times:

• Perfect for anchoring VWAP to specific events (earnings, Fed announcements, major reversals)

• Each VWAP has independent color settings for lines and deviation band backgrounds

• Individual control over calculation extension and visual extension (explained below)

• Useful for tracking multiple institutional accumulation/distribution zones simultaneously

2️⃣ AUTO MODE (Composite Period VWAP)

Automatically calculates VWAP across combined time periods:

• Supported periods: Daily, Weekly, Monthly, Quarterly, Yearly

• Configurable period span (1-20 periods)

• Always up-to-date, recalculates on each new bar

• Ideal for systematic analysis across consistent timeframes

✅ DUAL EXTENSION SYSTEM (Manual Mode Innovation)

Most VWAP indicators only offer "on/off" for extending calculations. This indicator provides two distinct extension options:

🔹 EXTEND CALCULATION TO CURRENT BAR

When enabled, continues including new bars in the VWAP calculation after the defined end time. The VWAP value updates dynamically as new volume enters the market.

Use case: You anchored VWAP to a major low 3 weeks ago. You want the VWAP to continue evolving with new volume data to track ongoing institutional positioning.

🔹 EXTEND VISUAL LINE ONLY

When enabled (and calculation extension is disabled), projects the "frozen" VWAP value forward as a reference line. The VWAP value remains fixed at what it was at the end time, but the line and deviation bands visually extend to current price.

Use case: You want to see how price is behaving relative to the VWAP that existed at a specific point in time (e.g., "Where is price now vs. the 5-day VWAP that existed at last Friday's close?").

This dual system gives you unprecedented control over whether you're tracking a "living" VWAP that incorporates new data or using historical VWAP levels as static reference points.

✅ CUSTOMIZABLE STANDARD DEVIATION BANDS

• Adjustable multiplier (0.1 to 5.0)

• Independent background colors with opacity control for each VWAP

• Dashed band lines for easy visual distinction from main VWAP

• Bands extend when visual extension is enabled, maintaining zone visibility

✅ COMPREHENSIVE LABELING SYSTEM

Each VWAP displays:

• Current VWAP value

• Upper deviation band value (High)

• Lower deviation band value (Low)

• Extension status indicator (Calc Extended / Visual Extended)

• Color-coded for quick identification

═══════════════════════════════════════════════════════════════════

📖 HOW TO USE THIS INDICATOR

🎯 SCENARIO 1: EVENT-ANCHORED VWAP (Manual Mode)

Use case: A stock gaps down 15% on earnings and you want to track where institutions are positioning during the recovery.

Setup:

1. Switch to Manual Mode

2. Enable VWAP 1

3. Set Start Time to the earnings gap bar

4. Set End Time to current time (or leave far in future)

5. Enable "Extend Calculation to Current Bar"

6. Watch how price respects the VWAP as a dynamic support/resistance

Interpretation:

• Price above VWAP = buyers in control since the event

• Price testing VWAP from above = potential support

• Volume-weighted standard deviation bands show normal price range

• Price outside bands = potential exhaustion/mean reversion setup

🎯 SCENARIO 2: MULTI-WEEK INSTITUTIONAL ACCUMULATION ZONE (Auto Mode)

Use case: You trade swing setups and want to identify where institutions have been accumulating over the past 3 weeks.

Setup:

1. Switch to Auto Mode

2. Select "Weekly" period type

3. Set Period Span to 3

4. Enable standard deviation bands

Interpretation:

• 3-week composite VWAP shows the true average institutional entry

• Price bouncing off VWAP repeatedly = strong support (institutions defending their average)

• Price breaking below VWAP on high volume = potential distribution

• Deviation bands contracting = consolidation; expanding = volatility increase

🎯 SCENARIO 3: COMPARING MULTIPLE TIME HORIZONS (Manual Mode)

Use case: You want to see short-term vs medium-term vs long-term VWAP alignments.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Last 5 trading days (blue)

3. VWAP 2: Last 10 trading days (orange)

4. VWAP 3: Last 20 trading days (purple)

5. Enable "Extend Calculation" for all

6. Set different background colors for visual separation

Interpretation:

• All VWAPs aligned upward = strong trend across all timeframes

• Price between VWAPs = finding equilibrium between different trader timeframes

• Short-term VWAP crossing long-term VWAP = momentum shift

• Price rejecting at higher-timeframe VWAP = that timeframe's traders defending their average

🎯 SCENARIO 4: HISTORICAL VWAP REFERENCE LEVELS (Manual Mode)

Use case: You want to see where the 1-month VWAP was at each month-end as static reference levels.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Set to last month's start/end dates

3. VWAP 2: Set to 2 months ago start/end dates

4. VWAP 3: Set to 3 months ago start/end dates

5. Disable "Extend Calculation"

6. Enable "Extend Visual Line Only"

Interpretation:

• Each VWAP represents the volume-weighted average for that complete month

• These become static support/resistance levels

• Price returning to old monthly VWAPs = institutional memory/gap fill behavior

• Useful for identifying longer-term value areas

═══════════════════════════════════════════════════════════════════

🎨 CUSTOMIZATION OPTIONS

GENERAL SETTINGS

• Show/hide labels

• Line style: Solid, Dashed, or Dotted

• Standard deviation multiplier (impacts band width)

• Toggle standard deviation bands on/off

MANUAL MODE (Per VWAP)

• Custom start and end times

• Line color picker

• Background color picker (with transparency control)

• Extend calculation option

• Extend visual option

• Show/hide individual VWAPs

AUTO MODE

• Period type selection (Daily/Weekly/Monthly/Quarterly/Yearly)

• Period span (1-20 periods)

• Line color

• Background color (with transparency control)

═══════════════════════════════════════════════════════════════════

💡 TRADING APPLICATIONS

✓ Mean Reversion: Use deviation bands to identify stretched prices likely to return to VWAP

✓ Trend Confirmation: Price sustained above VWAP = bullish bias; below = bearish bias

✓ Support/Resistance: VWAP often acts as dynamic S/R, especially on higher volume periods

✓ Institutional Positioning: Multi-day/week VWAPs show where large players have established positions

✓ Entry Timing: Wait for pullbacks to VWAP in trending markets

✓ Stop Placement: Use VWAP ± standard deviation as volatility-adjusted stop levels

✓ Breakout Confirmation: Breakouts from consolidation with price reclaiming VWAP = stronger signal

✓ Multi-Timeframe Analysis: Compare short vs long-period VWAPs to gauge momentum alignment

═══════════════════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

• The indicator redraws on each bar to maintain accurate visual representation (uses `barstate.islast`)

• Maximum lookback is limited to 5000 bars for performance optimization

• Time range calculations work across all timeframes but are most effective on intraday to daily charts

• Standard deviation bands assume volume-weighted distribution; extreme events may violate assumptions

• Auto mode always calculates to current bar; use Manual mode for fixed historical periods

═══════════════════════════════════════════════════════════════════

This indicator is open-source. Feel free to examine the code, learn from it, and adapt it to your needs.

Midnight Lines for Tokyo, London, New Yorkممتاز 👌 إليك **تعريفًا محدثًا وكاملًا للمؤشر باللغتين العربية والإنجليزية**، مع إدراج توضيح دقيق لتعامل المؤشر مع **تغيّر التوقيت الصيفي والشتوي (DST)** في لندن ونيويورك:

---

## 🇬🇧 **English Description (with DST behavior)**

**Indicator name:** *Midnight Lines for Tokyo, London, and New York*

**Purpose:**

This indicator automatically draws **vertical lines** on the chart at **midnight (00:00)** for the three major global trading sessions:

* **Tokyo**

* **London**

* **New York**

### 🔹 How it works:

1. The script checks each candle’s time using the built-in TradingView time zone function:

* `"Asia/Tokyo"`

* `"Europe/London"`

* `"America/New_York"`

2. When it detects **00:00** in any of these zones, it draws:

* A **vertical dotted line** that extends from the top to the bottom of the chart.

* A **label** at the top with the session name (e.g., “Tokyo Midnight”).

3. Each session has its own color for clarity:

* **Blue** → Tokyo Midnight

* **Green** → London Midnight

* **Red** → New York Midnight

### 🕒 Automatic Daylight Saving Time (DST) Adjustment:

The indicator automatically adapts to **Daylight Saving Time changes** in both **London** and **New York**:

* When London switches between **GMT and GMT+1**, the midnight line shifts automatically to remain accurate.

* When New York switches between **EST and EDT**, the script also updates accordingly.

* Tokyo does **not** observe DST, so its timing stays constant year-round.

### 🎯 Purpose:

Helps traders visually track the start of each new trading day in the major sessions and analyze:

* Session overlaps (e.g., London–New York overlap)

* Session-based trading strategies

* Price movement behavior at each new day open

---

## 🇸🇦 **الوصف بالعربية (مع إدراج تغير التوقيت)**

**اسم المؤشر:** خطوط منتصف الليل لجلسات طوكيو، لندن، ونيويورك

**الهدف:**

يقوم هذا المؤشر تلقائيًا برسم **خطوط عمودية** على الرسم البياني عند **منتصف الليل (00:00)** لكل من الجلسات الثلاث الرئيسية:

* **جلسة طوكيو**

* **جلسة لندن**

* **جلسة نيويورك**

### 🔹 كيفية العمل:

1. يستخدم المؤشر دوال TradingView لحساب الوقت الفعلي لكل مدينة:

* `"Asia/Tokyo"` لطوكيو

* `"Europe/London"` للندن

* `"America/New_York"` لنيويورك

2. عند وصول الساعة إلى **00:00** بتوقيت أي مدينة، يرسم المؤشر:

* **خطًا عموديًا متقطعًا** يمتد من أعلى إلى أسفل الرسم البياني.

* **تسمية (Label)** أعلى الخط باسم الجلسة (مثل “Tokyo Midnight”).

3. كل جلسة لها لون مختلف:

* **أزرق** → منتصف طوكيو

* **أخضر** → منتصف لندن

* **أحمر** → منتصف نيويورك

### 🕒 التعامل مع تغيّر التوقيت الصيفي والشتوي (DST):

يتكيّف المؤشر تلقائيًا مع تغيّر التوقيت في لندن ونيويورك:

* عندما تنتقل لندن بين **التوقيت الشتوي (GMT)** و**التوقيت الصيفي (GMT+1)**، يتحرك الخط تلقائيًا ليبقى في الساعة 00:00 المحلية.

* وعندما تنتقل نيويورك بين **EST** و**EDT**، يتم تعديل الخط كذلك تلقائيًا.

* أما طوكيو فلا تعتمد التوقيت الصيفي، لذا يبقى وقتها ثابتًا دائمًا على الساعة **00:00 JST**.

### 🎯 الفائدة:

يساعد المتداولين على تحديد **بداية كل جلسة تداول رئيسية**، ومراقبة:

* **تداخل الجلسات** مثل لندن ونيويورك

* **تحركات السعر عند بداية اليوم الجديد**

* **استراتيجيات التداول الزمنية حسب الجلسة**

---

mean reversion Spread Z-Score Your main "actor" is the Blue Line 🔵 (the Z-Score). It tells you if your spread is "expensive" or "cheap" compared to its average.

The other lines are your action zones.

Here is how to read the signals:

Scenario 1: SELL the Spread (The spread is TOO EXPENSIVE)

• ENTRY Signal: The Blue Line 🔵 moves up and crosses the Red Line 🔴 (at +1.8).

• Meaning: MNQ has become far too expensive compared to MES. The rubber band is stretched too far upwards.

• Your Action (Sell):

• ✅ SELL MNQ

• ✅ BUY MES

• EXIT Signal: The Blue Line 🔵 comes back down and crosses the Dotted Red Line (at +0.5).

• Meaning: The rubber band is back to normal. It's time to take your profits.

• Your Action (Close):

• ✅ BUY BACK your MNQ

• ✅ SELL your MES

Scenario 2: BUY the Spread (The spread is TOO CHEAP)

• ENTRY Signal: The Blue Line 🔵 moves down and crosses the Green Line 🟢 (at -1.8).

• Meaning: MNQ has become far too cheap compared to MES. The rubber band is stretched too far downwards.

• Your Action (Buy):

• ✅ BUY MNQ

• ✅ SELL MES

• EXIT Signal: The Blue Line 🔵 moves back up and crosses the Dotted Green Line (at -0.5).

• Meaning: The rubber band is back to normal. It's time to take your profits.

• Your Action (Close):

• ✅ SELL your MNQ

• ✅ BUY BACK your MES

In summary:

• Blue Line 🔵 touches Red Line 🔴 = Sell the spread.

• Blue Line 🔵 touches Green Line 🟢 = Buy the spread.

Liquidaciones BTCUSDT.PAllows you to manually record liquidation prices for both short and long positions, which are then displayed on the chart:

Orange: Short liquidations

Blue: Long liquidations

Optionally, a specific liquidation price can be highlighted to indicate higher-volume liquidations

Note: All liquidation prices must be entered manually.

Smooth Theil-SenI wanted to build a Theil-Sen estimator that could run on more than one bar and produce smoother output than the standard implementation. Theil-Sen regression is a non-parametric method that calculates the median slope between all pairs of points in your dataset, which makes it extremely robust to outliers. The problem is that median operations produce discrete jumps, especially when you're working with limited sample sizes. Every time the median shifts from one value to another, you get a step change in your regression line, which creates visual choppiness that can be distracting even though the underlying calculations are sound.

The solution I ended up going with was convolving a Gaussian kernel around the center of the sorted lists to get a more continuous median estimate. Instead of just picking the middle value or averaging the two middle values when you have an even sample size, the Gaussian kernel weights the values near the center more heavily and smoothly tapers off as you move away from the median position. This creates a weighted average that behaves like a median in terms of robustness but produces much smoother transitions as new data points arrive and the sorted list shifts.

There are variance tradeoffs with this approach since you're no longer using the pure median, but they're minimal in practice. The kernel weighting stays concentrated enough around the center that you retain most of the outlier resistance that makes Theil-Sen useful in the first place. What you gain is a regression line that updates smoothly instead of jumping discretely, which makes it easier to spot genuine trend changes versus just the statistical noise of median recalculation. The smoothness is particularly noticeable when you're running the estimator over longer lookback periods where the sorted list is large enough that small kernel adjustments have less impact on the overall center of mass.

The Gaussian kernel itself is a bell curve centered on the median position, with a standard deviation you can tune to control how much smoothing you want. Tighter kernels stay closer to the pure median behavior and give you more discrete steps. Wider kernels spread the weighting further from the center and produce smoother output at the cost of slightly reduced outlier resistance. The default settings strike a balance that keeps the estimator robust while removing most of the visual jitter.

Running Theil-Sen on multiple bars means calculating slopes between all pairs of points across your lookback window, sorting those slopes, and then applying the Gaussian kernel to find the weighted center of that sorted distribution. This is computationally more expensive than simple moving averages or even standard linear regression, but Pine Script handles it well enough for reasonable lookback lengths. The benefit is that you get a trend estimate that doesn't get thrown off by individual spikes or anomalies in your price data, which is valuable when working with noisy instruments or during volatile periods where traditional regression lines can swing wildly.

The implementation maintains sorted arrays for both the slope calculations and the final kernel weighting, which keeps everything organized and makes the Gaussian convolution straightforward. The kernel weights are precalculated based on the distance from the center position, then applied as multipliers to the sorted slope values before summing to get the final smoothed median slope. That slope gets combined with an intercept calculation to produce the regression line values you see plotted on the chart.

What this really demonstrates is that you can take classical statistical methods like Theil-Sen and adapt them with signal processing techniques like kernel convolution to get behavior that's more suited to real-time visualization. The pure mathematical definition of a median is discrete by nature, but financial charts benefit from smooth, continuous lines that make it easier to track changes over time. By introducing the Gaussian kernel weighting, you preserve the core robustness of the median-based approach while gaining the visual smoothness of methods that use weighted averages. Whether that smoothness is worth the minor variance tradeoff depends on your use case, but for most charting applications, the improved readability makes it a good compromise.

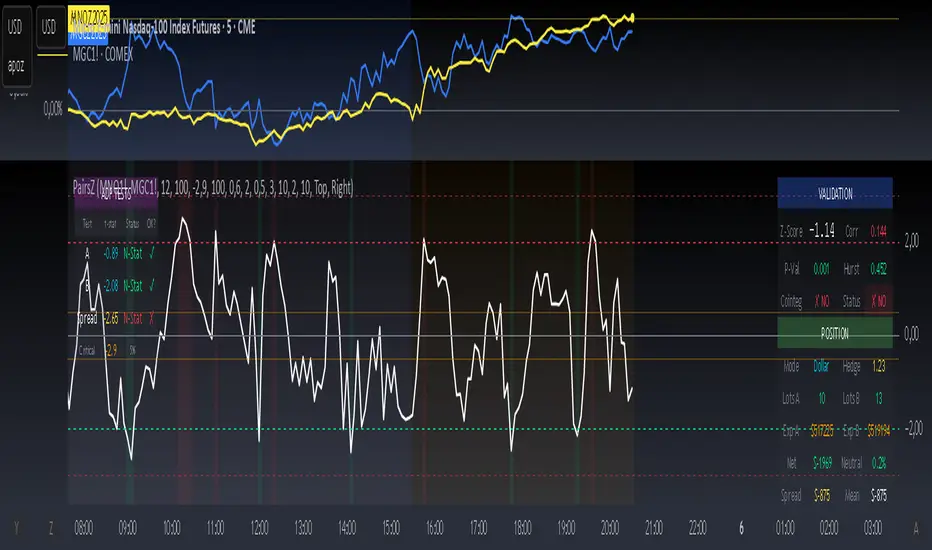

Spread Trading Z-ScoreIndicator: Z-Score Spread Indicator

Description

The "Z-Score Spread Indicator" is a powerful tool for traders employing mean-reversion strategies on the spread between two financial assets (e.g., futures contracts like MNQ and MES). This indicator calculates and plots the Z-score of the price spread, indicating how far the current spread deviates from its historical mean. It features customizable entry and exit thresholds with adjustable offsets, along with an estimated p-value displayed in a table to assess statistical significance.

Key Features

Asset Selection: Allows users to select two asset symbols (e.g., CME_MINI:MNQ1! and CME_MINI:MES1!) via customizable inputs.

Z-Score Calculation: Computes the Z-score based on the spread’s simple moving average and standard deviation over a user-defined lookback period.

Customizable Thresholds with Offset: Offers adjustable base entry and exit thresholds, with an optional offset to fine-tune trading levels, plotted as horizontal lines.

P-Value Estimation: Provides an approximate p-value to evaluate the statistical significance of the Z-score, displayed in a table anchored to the top-left corner.

Visual Representation: Plots the Z-score with a zero line and threshold lines for intuitive interpretation.

Adjustable Parameters

Asset A Symbol: Symbol for Asset A (default: CME_MINI:MNQ1!).

Asset B Symbol: Symbol for Asset B (default: CME_MINI:MES1!).

Z-Score Lookback: Lookback period for Z-score calculation (default: 40, minimum 2).

Base Entry Threshold: Threshold for entry signals (default: 1.8, adjustable with a step of 0.1).

Base Exit Threshold: Threshold for exit signals (default: 0.5, adjustable with a step of 0.1).

Threshold Offset (+/-): Offset to adjust entry and exit thresholds symmetrically (default: 0.0, range -5.0 to 5.0, step 0.1).

Usage

Add the indicator to your chart via the "Indicators" tab.

Customize the parameters based on your preferred assets and trading strategy (lookback period, thresholds, offset).

Observe the Z-score plot and threshold lines (red for short entry, green for long entry, orange dotted for exits) to identify potential trade setups.

Check the p-value table in the top-left corner to assess the statistical significance of the current Z-score.

Use this data to inform mean-reversion trading decisions, ideally in conjunction with other indicators.

Notes

A Z-score above the entry threshold (positive) or below the negative entry threshold suggests a potential short or long entry, respectively. Exits are signaled when the Z-score crosses the exit thresholds.

The p-value is an approximation based on the normal distribution; a value below 0.05 typically indicates statistical significance, but further validation is recommended.

The indicator uses a simple spread (Asset A - Asset B) without volatility adjustments; consider pairing it with a lots calculator for hedging.

Limitations

The p-value is an approximation and may not reflect advanced statistical tests (e.g., ADF) due to Pine Script constraints.

No automatic trading signals are generated; it provides data for manual analysis.

Author

Developed by grogusama, October 15, 2025, 07:29 PM CEST.

VBE Pro - Advanced Volatility Bands with Zero Lag & PredictionVBE Pro: Zero-Lag Predictive Bands

A next-gen volatility envelope that blends zero-lag smoothing with forward-looking volatility models (EWMA/GARCH/HAR/ML) to keep bands tight in calm markets, responsive in shocks, and adaptive across regimes.

What it does

Builds volatility from multiple methods (ATR, StDev, Parkinson, Garman-Klass, Rogers-Satchell, Yang-Zhang).

Projects near-term vol with your choice of predictor, then blends it via a weight slider.

Applies zero-lag smoothing (ZLEMA/ZLMA/DEMA/TEMA/HMA/JMA/Ehlers/Kalman/T3) to cut delay without over-shoot.

Auto-adapts band width by regime (high/low/normal) and can expand dynamically with price acceleration.

Optional displacement to align with your execution style.

On-chart

Upper/Lower zero-lag bands with optional fill.

Middle line (ZL-smoothed source).

Regime-tinted background (High/Low).

Displacement marker (if used).

Compact top-right info table: current vs predicted vol, regime, squeeze, multiplier, methods, ZL gain, est. lag reduction.

Signals & Alerts

Break↑ / Break↓ when price crosses the bands.

Vol↑ / Vol↓ expansion/contraction sequences.

“Squeeze” when band width compresses vs its ZL average.

“ZL” marker when significant zero-lag is active.

Prediction divergence ⚠ when projected vol deviates > threshold.

Built-in alertconditions for all of the above.

Quick start

Method: ATR or Hybrid for robustness.

Smoothing: ZLEMA, length 5–8, ZL gain 2–3 (push higher only if you accept more projection).

Bands: Multiplier 2.0, Adaptive on, Dynamic off to start.

Prediction: EWMA, weight 0.25–0.35. Move to GARCH in mean-reverty tapes; HAR-RV for mixed regimes.

Regime lookback: 50.

Liquidity Index with Advanced Statistical NormalizationLiquidity Index with Advanced Statistical Normalization

An open-source TradingView indicator for analyzing global liquidity cycles using robust statistical methods

Overview

This Pine Script indicator combines multiple macroeconomic data sources to construct a composite liquidity index that tracks global financial conditions. It employs advanced statistical techniques typically found in quantitative finance research, adapted for real-time charting.

Key Features

📊 Multi-Source Data Integration

- Federal Reserve Components: Fed Funds Rate, Reverse Repo (RRP), Treasury General Account (TGA)

- PBOC Components: China M2 Money Stock adjusted by CNY/USD exchange rate

- Volatility Index: MOVE Index (bond market volatility)

🔬 Advanced Statistical Methods

1. Theil-Sen Estimator: Robust trend detection resistant to outliers

2. Triple Normalization:

- Z-score normalization

- MAD (Median Absolute Deviation) normalization

- Quantile normalization via inverse normal CDF

3. Multi-Timeframe Analysis: Short (8-bar) and long (34-bar) windows with blended composite

📈 Signal Processing

- Log-transformation for non-linear relationships

- Smoothing via customizable SMA

- Composite signal averaging across normalization methods

Why This Approach?

Traditional liquidity indicators often suffer from:

- Sensitivity to outliers in economic data

- Assumption of normal distributions

- Single-timeframe bias

This script addresses these issues by:

- Using median-based robust statistics (Theil-Sen, MAD)

- Applying multiple normalization techniques

- Blending short and long-term perspectives

Customization Options

short_length // Short window (default: 8)

long_length // Long window (default: 34)

show_short // Display short composite

show_long // Display long composite

show_blended // Display blended signal

smoothing_length // SMA smoothing period (default: 10)

How to Use

1. Liquidity Expansion (positive values): Risk-on environment, favorable for asset prices

2. Liquidity Contraction (negative values): Risk-off environment, potential market stress

3. Divergences: Compare indicator direction vs. price action for early warnings

Potential Improvements

Community members are encouraged to enhance:

- Additional data sources (ECB balance sheet, BOJ operations, etc.)

- Alternative normalization methods (robust scaling, rank transformation)

- Machine learning integration (LSTM forecasting, regime detection)

- Alert conditions for liquidity inflection points

- Volatility-adjusted weighting schemes

Technical Notes

- Uses request.security() for multi-symbol data fetching

- All calculations handle missing data via nz() functions

- Median-based statistics computed via array operations

- Custom inverse CDF approximation (no external libraries required)

Contributing

This is a foundation for liquidity analysis. Potential extensions:

- LLM Integration: Use language models to parse Fed/PBOC meeting minutes and adjust weights dynamically

- Sentiment Layer: Incorporate crypto funding rates or options skew

- Adaptive Parameters: Auto-tune window lengths based on market regime

- Cross-Asset Validation: Backtest signals against BTC, equities, bonds

---

License: Open source - modify and redistribute freelyDisclaimer: For educational purposes only. Not financial advice.

Bitcoin Power Law Corridor + Z-score

This script visualizes the long-term Bitcoin Power Law Corridor, a conceptual model originally discussed by Harold Christopher Burger, and enhances it with a logarithmic Z-Score framework.

The indicator plots Bitcoin’s long-term regression curve together with estimated resistance and support bands based on power-law relationships between price and time since inception.

The added Z-Score expresses the statistical distance between price and the central regression line, using logarithmic scaling:

Z ≈ 0 → price near its long-term fair-value trajectory.

Z ≈ +2 → price near the lower corridor boundary (historically undervalued region).

Z ≈ −2 → price near the upper corridor boundary (historically overheated region).

This indicator is designed for visual and educational purposes only.

It should not be considered financial advice, a predictive model, or a signal provider.

Users should always combine this tool with other forms of technical, fundamental, and sentiment analysis to confirm confluence before making any decision.

EMA+MACD动态0轴主图动态MACD,EMA55作为当前周期动态0轴使用。EMA13作为小4倍周期动态0轴。当前周期DIF线穿越0轴标记+MACD金死叉标记。

The main chart dynamic MACD and EMA55 are used as the dynamic 0-axis for the current cycle. EMA13 is used as the dynamic 0- axis for the smaller 4x cycle. The current cycle's DIF line has crossed the 0-axis, marked with a "+" sign indicating a golden cross on the MACD.