Aurum DCX AVE Gold and Silver StrategySummary in one paragraph

Aurum DCX AVE is a volatility break strategy for gold and silver on intraday and swing timeframes. It aligns a new Directional Convexity Index with an Adaptive Volatility Envelope and an optional USD/DXY bias so trades appear only when direction quality and expansion agree. It is original because it fuses three pieces rarely combined in one model for metals: a convexity aware trend strength score, a percentile based envelope that widens with regime heat, and an intermarket DXY filter.

Scope and intent

• Markets. Gold and silver futures or spot, other liquid commodities, major indices

• Timeframes. Five minutes to one day. Defaults to 30min for swing pace

• Default demo used in this publication. TVC:GOLD on 30m

• Purpose. Enter confirmed volatility breaks while muting chop using regime heat and USD bias

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. DCX combines DI strength with path efficiency and curvature. AVE blends ATR with a high TR percentile and widens with DCX heat. DXY adds an intermarket bias

• Failure mode addressed. False starts inside compression and unconfirmed breakouts during USD swings

• Testability. Each component has a named input. Entry names L and S are visible in the list of trades

• Portable yardstick. Weekly ATR for stops and R multiples for targets

• Open source. Method and implementation are disclosed for community review

Method overview in plain language

You score direction quality with DCX, size an adaptive envelope with a blend of ATR and a high TR percentile, and only allow breaks that clear the band while DCX is above a heat threshold in the same direction. An optional DXY filter favors long when USD weakens and short when USD strengthens. Orders are bracketed with a Weekly ATR stop and an R multiple target, with optional trailing to the envelope.

Base measures

• Range basis. True Range and ATR over user windows. A high TR percentile captures expansion tails used by AVE

• Return basis. Not required

Components

• Directional Convexity Index DCX. Measures directional strength with DX, multiplies by path efficiency, blends a curvature term from acceleration, scales to 0 to 100, and uses a rise window

• Adaptive Volatility Envelope AVE. Midline ALMA or HMA or EMA plus bands sized by a blend of ATR and a high TR percentile. The blend weight follows volatility of volatility. Band width widens with DCX heat

• DXY Bias optional. Daily EMA trend of DXY. Long bias when USD weakens. Short bias when USD strengthens

• Risk block. Initial stop equals Weekly ATR times a multiplier. Target equals an R multiple of the initial risk. Optional trailing to AVE band

Fusion rule

• All gates must pass. DCX above threshold and rising. Directional lead agrees. Price breaks the AVE band in the same direction. DXY bias agrees when enabled

Signal rule

• Long. Close above AVE upper and DCX above threshold and DCX rising and plus DI leads and DXY bias is bearish

• Short. Close below AVE lower and DCX above threshold and DCX falling and minus DI leads and DXY bias is bullish

• Exit and flip. Bracket exit at stop or target. Optional trailing to AVE band

Inputs with guidance

Setup

• Symbol. Default TVC:GOLD (Correlation Asset for internal logic)

• Signal timeframe. Blank follows the chart

• Confirm timeframe. Default 1 day used by the bias block

Directional Convexity Index

• DCX window. Typical 10 to 21. Higher filters more. Lower reacts earlier

• DCX rise bars. Typical 3 to 6. Higher demands continuation

• DCX entry threshold. Typical 15 to 35. Higher avoids soft moves

• Efficiency floor. Typical 0.02 to 0.06. Stability in quiet tape

• Convexity weight 0..1. Typical 0.25 to 0.50. Higher gives curvature more influence

Adaptive Volatility Envelope

• AVE window. Typical 24 to 48. Higher smooths more

• Midline type. ALMA or HMA or EMA per preference

• TR percentile 0..100. Typical 75 to 90. Higher favors only strong expansions

• Vol of vol reference. Typical 0.05 to 0.30. Controls how much the percentile term weighs against ATR

• Base envelope mult. Typical 1.4 to 2.2. Width of bands

• Regime adapt 0..1. Typical 0.6 to 0.95. How much DCX heat widens or narrows the bands

Intermarket Bias

• Use DXY bias. Default ON

• DXY timeframe. Default 1 day

• DXY trend window. Typical 10 to 50

Risk

• Risk percent per trade. Reporting field. Keep live risk near one to two percent

• Weekly ATR. Default 14. Basis for stops

• Stop ATR weekly mult. Typical 1.5 to 3.0

• Take profit R multiple. Typical 1.5 to 3.0

• Trail with AVE band. Optional. OFF by default

Properties visible in this publication

• Initial capital. 20000

• Base currency. USD

• request.security lookahead off everywhere

• Commission. 0.03 percent

• Slippage. 5 ticks

• Default order size method percent of equity with value 3% of the total capital available

• Pyramiding 0

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Strategies use standard candles for signals and orders only

Honest limitations and failure modes

• Economic releases and thin liquidity can break assumptions behind the expansion logic

• Gap heavy symbols may prefer a longer ATR window

• Very quiet regimes can reduce signal contrast. Consider higher DCX thresholds or wider bands

• Session time follows the exchange of the chart and can change symbol to symbol

• Symbol sensitivity is expected. Use the gates and length inputs to find stable settings

Open source reuse and credits

• None

Mode

Public open source. Source is visible and free to reuse within TradingView House Rules

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Algorithm

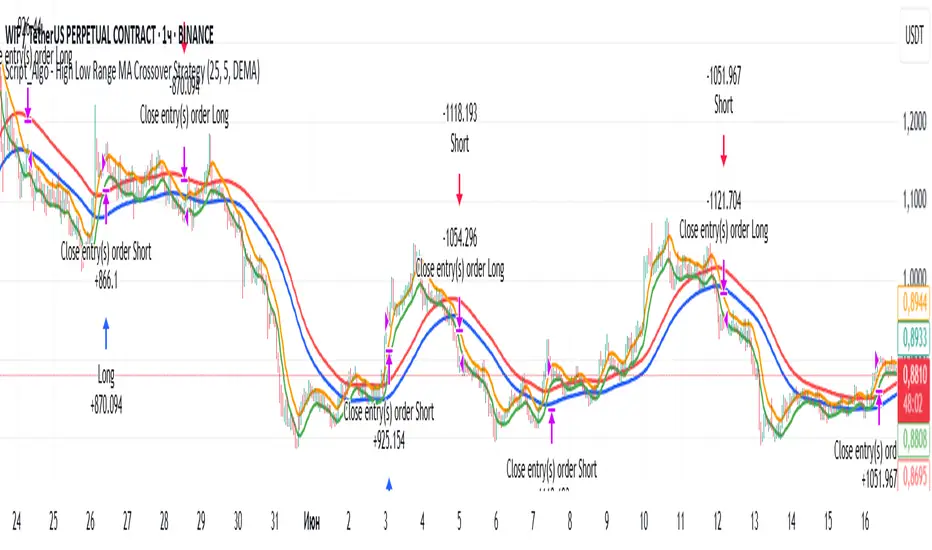

Script_Algo - High Low Range MA Crossover Strategy🎯 Core Concept

This strategy uses modified moving averages crossover, built on maximum and minimum prices, to determine entry and exit points in the market. A key advantage of this strategy is that it avoids most false signals in trendless conditions, which is characteristic of traditional moving average crossover strategies. This makes it possible to improve the risk/reward ratio and, consequently, the strategy's profitability.

📊 How the Strategy Works

Main Mechanism

The strategy builds 4 moving averages:

Two senior MAs (on high and low) with a longer period

Two junior MAs (on high and low) with a shorter period

Buy signal 🟢: when the junior MA of lows crosses above the senior MA of highs

Sell signal 🔴: when the junior MA of highs crosses below the senior MA of lows

As seen on the chart, it was potentially possible to make 9X on the WIFUSDT cryptocurrency pair in just a year and a half. However, be careful—such results may not necessarily be repeated in the future.

Special Feature

Position closing priority ❗: if an opposite signal arrives while a position is open, the strategy first closes the current position and only then opens a new one

⚙️ Indicator Settings

Available Moving Average Types

EMA - Exponential MA

SMA - Simple MA

SSMA - Smoothed MA

WMA - Weighted MA

VWMA - Volume Weighted MA

RMA - Adaptive MA

DEMA - Double EMA

TEMA - Triple EMA

Adjustable Parameters

Senior MA Length - period for long-term moving averages

Junior MA Length - period for short-term moving averages

✅ Advantages of the Strategy

🛡️ False Signal Protection - using two pairs of modified MAs reduces the number of false entries

🔄 Configuration Flexibility - ability to choose MA type and calculation periods

⚡ Automatic Switching - the strategy automatically closes the current position when receiving an opposite signal

📈 Visual Clarity - all MAs are displayed on the chart in different colors

⚠️ Disadvantages and Risks

📉 Signal Lag - like all MA-based strategies, it may provide delayed signals during sharp movements

🔁 Frequent Switching - in sideways markets, it may lead to multiple consecutive position openings/closings

📊 Requires Optimization - optimal parameters need to be selected for different instruments and timeframes

💡 Usage Recommendations

Backtest - test the strategy's performance on historical data

Optimize Parameters - select MA periods suitable for the specific trading instrument

Use Filters - add additional filters to confirm signals

Manage Risks - always use stop-loss and take-profit orders.

You can safely connect to the exchange via webhook and enjoy trading.

Good luck and profits to everyone!!

iMoku (Ichimoku Complete Tool) - The Quant Science iMoku™ is a professional all-in-one solution for the famous Ichimoku Kinko Hyo indicator.

The algorithm includes:

1. Backtesting spot

2. Visual tool

3. Auto-trading functions

With iMoku you can test four different strategies.

Strategy 1: Cross Tenkan Sen - Kijun Sen

A long position is opened with 100% of the invested capital ($1000) when "Tenkan Sen" crossover "Kijun Sen".

Closing the long position on the opposite condition.

There are 3 different strength signals for this strategy: weak, normal, strong.

Weak : the signal is weak when the condition is true and the price is above the 'Kumo'

Normal : the signal is normal when the condition is true and the price is within the 'Kumo'

Strong : the signal is strong when the condition is true and the price is below the 'Kumo'

Strategy 2: Cross Price - Kijun Sen

A long position is opened with 100% of the invested capital ($1000) when the price crossover the 'Kijun Sen'.

Closing the long position on the opposite condition.

There are 3 different strength signals for this strategy: weak, normal, strong.

Weak : the signal is weak when the condition is true and the price is above the 'Kumo'

Normal : the signal is normal when the condition is true and the price is inside the 'Kumo'

Strong : the signal is strong when the condition is true and the price is below the 'Kumo'

Strategy 3: Kumo Breakout

A long position is opened with 100% of the invested capital ($1000) when the price breakup the 'Kumo'.

Closing the long position with a percentage stop loss and take profit on the invested capital.

Strategy 4: Kumo Twist

A long position is opened with 100% of the invested capital ($1000) when the 'Kumo' goes from negative to positive (called "Twist").

Closing the long position on the opposite condition.

There are 2 different strength signals for this strategy: weak, and strong.

Weak : the signal is weak when the condition is true and the price is above the 'Kumo'

Strong : the signal is strong when the condition is true and the price is below the 'Kumo'

This script is compliant with algorithmic trading.

You can use this script with trading terminals such as 3Commas or CryptoHopper. Connecting this script is very easy.

1. Enter the user interface

2. Select and activate a strategy

3. Copy your bot's links into the dedicated fields

4. Create and activate alert

Disclaimer: algorithmic trading involves risk, the user should consider aspects such as slippage, liquidity and costs when evaluating an asset. The Quant Science is not responsible for any kind of damage resulting from use of this script. By using this script you take all the responsibilities and risks.

GRID SPOT TRADING ALGORITHM - GRID BOT TRADING STRATEGYGRID SPOT TRADING ALGORITHM : LONG ONLY STRATEGY OPEN SOURCE

This is a long only strategy for spot assets.

HOW IT WORKS

Grid trading is a trading strategy where an investor creates a so-called "price grid". The basic idea of the strategy is to repeatedly buy at the pre-specified price and then wait for the price to rise above that level and then sell the position (and vice versa with shorting or hedging).

FEATURES

Grids: This algorithm has a total of 10 grids.

Take profit: The trader can increase or decrease the distance between the grids from the User Interface panel, the distance between one grid and another represents the take profit.

Management: The algorithm buys 10% of the capital every time the price breaks down a grid and sells during a rise to the next higher grid. The initial capital is invested in 10 sizes which represent 10% of the capital per trade.

Stop Loss: The algorithm knows no stop loss as long as it is not activated from the User Interface panel. By activating the stop loss from the User Interface panel the algorithm will insert a close condition on all trades which will be calculated from the last lower grid.

Trades: Trades are opened only if the price is within the grid. If the market leaves the grid the algorithm will not buy new positions or sell new positions.

Optimal market conditions: The favorable market for this algorithm is the sideways market.

LIMITATIONS OF THE MODEL

The trader must take into account that this is a static model. It only works perfectly well if the market is in a sideways phase and incurs heavy losses if the market takes a downward trend. The model is unusable for an uptrend. The trader must therefore carefully analyze the market where he intends to use this strategy, making sure that the price is in a sideways phase.

USES

Indispensable research and backtesting tool for those using bots for their investments. The algorithm produces a backtesting of the strategy for past history. It is used by professional traders to understand if this strategy has been profitable on a market and what parameters to use for bots using this strategy (Kucoin, Binance etc.).

If you would like to develop your own algorithm with customized conditions based on a grid strategy, please contact us.

If you need help in using this tool, please contact us without hesitation.

DMI + HMA - No Risk ManagementDMI (Directional Movement Index) and HMA (Hull Moving Average)

The DMI and HMA make a great combination, The DMI will gauge the market direction, while the HMA will add confirmation to the trend strength.

What is the DMI?

The DMI is an indicator that was developed by J. Welles Wilder in 1978. The Indicator was designed to identify in which direction the price is moving. This is done by comparing previous highs and lows and drawing 2 lines.

1. A Positive movement line

2. A Negative movement line

A third line can be added, which would be known as the ADX line or Average Directional Index. This can also be used to gauge the strength in which direction the market is moving.

When the Positive movement line (DI+) is above the Negative movement line (DI-) there is more upward pressure. Ofcourse visa versa, when the DI- is above the DI+ that would indicate more downwards pressure.

Want to know more about HMA? Check out one of our other published scripts

What is this strategy doing?

We are first waiting for the DMI to cross in our favoured direction, after that, we wait for the HMA to signal the entry. Without both conditions being true, no trade will be made.

Long Entries

1. DI+ crosses above DI-

2. HMA line 1 is above HMA line 2

Short Entries

1. DI- Crosses above DI+

2. HMA line 1 is below HMA lilne 2

Its as simple as that.

Conclusion

While this strategy does have its downsides, that can be reduced by adding some risk manegment into the script. In general the trade profitability is above average, And the max drawdown is at a minimum.

The settings have been optimised to suite BTCUSDT PERP markets. Though with small adjustments it can be used on many assets!

Hull Crossover Strategy no TP or SLWhat is it?

A simple yet effective strategy ran on the 30m chart.

This is a basic idea that can be expanded on using different indicator to either add signals or filter out certain bad signals!

The strategy consists of 1 fast moving average and 1 slow moving average.

Both of these moving averages are the Hull Moving Average

What is the Hull Moving Average?

The Hull Moving Average ( HMA ) is a directional trend indicator.

It captures the current market conditions and uses recent price action to determine if conditions are bullish or bearish relative to historical data.

The Hull is different from traditional trend indicators like the EMA and the SMA .

It is designed to reduce the lag often associated with other MAs by providing a faster signal on a smoother visual plane.

How it works?

When the fast HMA crosses over the slow HMA , we initiate a long signal, and

when the fast HMA crosses under the slow HMA , we initiate a short signal.

Conclusion

The power of simplicity is what makes this such a great core to use to build onto making something even better!

The results were optimised to suit the most common market conditions seen today.

******** Not financial advice! ********

Ichimoku Cloud Strategy Long Only [Bitduke]Slightly modificated and optimized for Pine Script 4.0, Ichimoku Cloud Strategy which, suddenly, good suitable for the several crypto assets.

Details:

Enter position when conversion line crosses base line up, and close it when the opposite happens.

Additional condition for open / close the trade is lagging span, it should be higher than cloud to open position and below - to close it.

Backtesting:

Backtested on SOLUSDT ( FTX, Binance )

+150% for 2021 year, 8% dd

+191% for all time, 32% dd

Disadvantages:

- Small number of trades

- Need to vary parameters for different coins (not very robust)

Should be tested carefully for other coins / stock market. Different parameters could be needed or even algo modifications.

Strategy doesn't repaint.

GMS: RSI StrategyThis is just a basic RSI strategy that it easy to use and quite comprehensive so you can quickly test out an idea based on RSI.

- I made it comprehensive in that you can select long, short, or both.

- There is a simple moving average trend filter. You can filter for trades above, below, or don't include it at all.

- The exit is based on a simple moving average.

The source code should be open if you want to see it or modify it for your own project. I hope it helps!

Andre

Global Market Signals

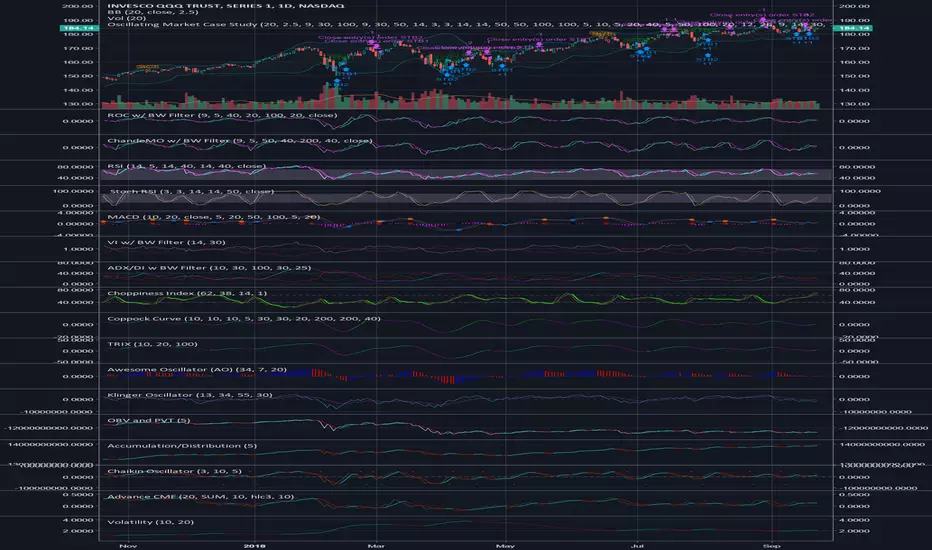

Oscillating Market Case StudyThis is a little something I created to analyze the market. Ultimately, I wanted to create something that could encapsulate the entire market as best as possible. The idea was simple, use technical analysis to create cases that would indicate entry positions and exit positions for long positions initially. After completing that, I decided to add a few shorting cases.

A combination of 25-30 indicators were used to create this, and the indicators were modified with a filter to create a smoothed overlay.

So here's the breakdown:

- 10 total cases: 7 long, 3 short

- The 7 long cases are broken down into three categories; long term, medium term, short term

- Short Term: OC1, OC2, STB1, STB2

- Medium Term: STB1, STB2

- Long Term: LTB1

- Shorting Cases: SC1, SC2, SC3

- The cases are both plotted as text and entry orders; this can be toggled on and off through the format menu.

I suggest you use the format menu to get the most out of this script. The menu consists of toggles to turn of the plots and/or the entries. It's pretty self explanatory. Use it to keep the chart cleared and concise so you only visualise the cases that you need.

Personally, the cases that have worked the best for me are:

- Long Cases: OC1, OC2, STB2, LTB1

- Shorting Cases: SC2, SC3

I kept this description as short as possible, but please feel free to reach out if you have any questions.

Pretty much, use the cases and see if it works for you.

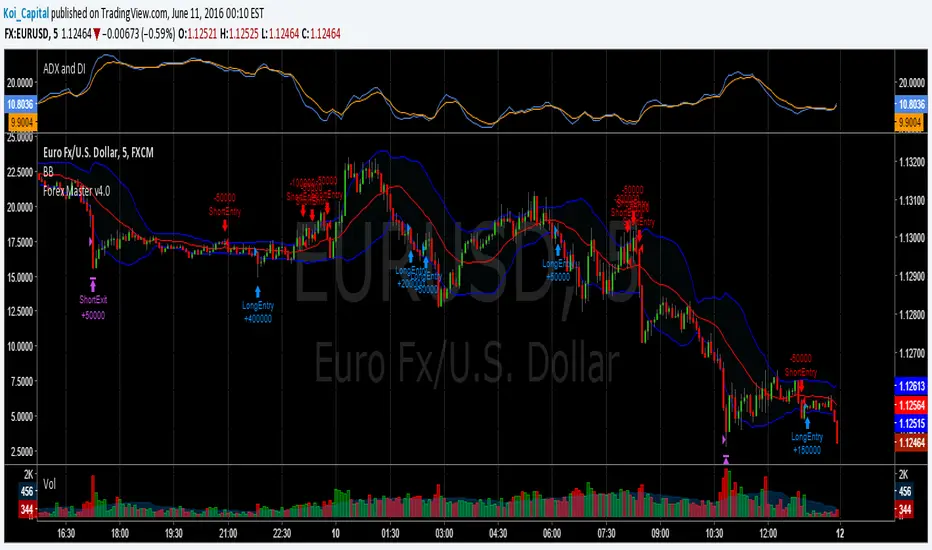

Forex Master v4.0 (EUR/USD Mean-Reversion Algorithm)DESCRIPTION

Forex Master v4.0 is a mean-reversion algorithm currently optimized for trading the EUR/USD pair on the 5M chart interval. All indicator inputs use the period's closing price and all trades are executed at the open of the period following the period where the trade signal was generated.

There are 3 main components that make up Forex Master v4.0:

I. Trend Filter

The algorithm uses a version of the ADX indicator as a trend filter to trade only in certain time periods where price is more likely to be range-bound (i.e., mean-reverting). This indicator is composed of a Fast ADX and a Slow ADX, both using the same look-back period of 50. However, the Fast ADX is smoothed with a 6-period EMA and the Slow ADX is smoothed with a 12-period EMA. When the Fast ADX is above the Slow ADX, the algorithm does not trade because this indicates that price is likelier to trend, which is bad for a mean-reversion system. Conversely, when the Fast ADX is below the Slow ADX, price is likelier to be ranging so this is the only time when the algorithm is allowed to trade.

II. Bollinger Bands

When allowed to trade by the Trend Filter, the algorithm uses the Bollinger Bands indicator to enter long and short positions. The Bolliger Bands indicator has a look-back period of 20 and a standard deviation of 1.5 for both upper and lower bands. When price crosses over the lower band, a Long Signal is generated and a long position is entered. When price crosses under the upper band, a Short Signal is generated and a short position is entered.

III. Money Management

Rule 1 - Each trade will use a limit order for a fixed quantity of 50,000 contracts (0.50 lot). The only exception is Rule

Rule 2 - Order pyramiding is enabled and up to 10 consecutive orders of the same signal can be executed (for example: 14 consecutive Long Signals are generated over 8 hours and the algorithm sends in 10 different buy orders at various prices for a total of 350,000 contracts).

Rule 3 - Every order will include a bracket with both TP and SL set at 50 pips (note: the algorithm only closes the current open position and does not enter the opposite trade once a TP or SL has been hit).

Rule 4 - When a new opposite trade signal is generated, the algorithm sends in a larger order to close the current open position as well as open a new one (for example: 14 consecutive Long Signals are generated over 8 hours and the algorithm sends in 10 different buy orders at various prices for a total of 350,000 contracts. A Short Signal is generated shortly after the 14th Long Signal. The algorithm then sends in a sell order for 400,000 contracts to close the 350,000 contracts long position and open a new short position of 50,000 contracts).

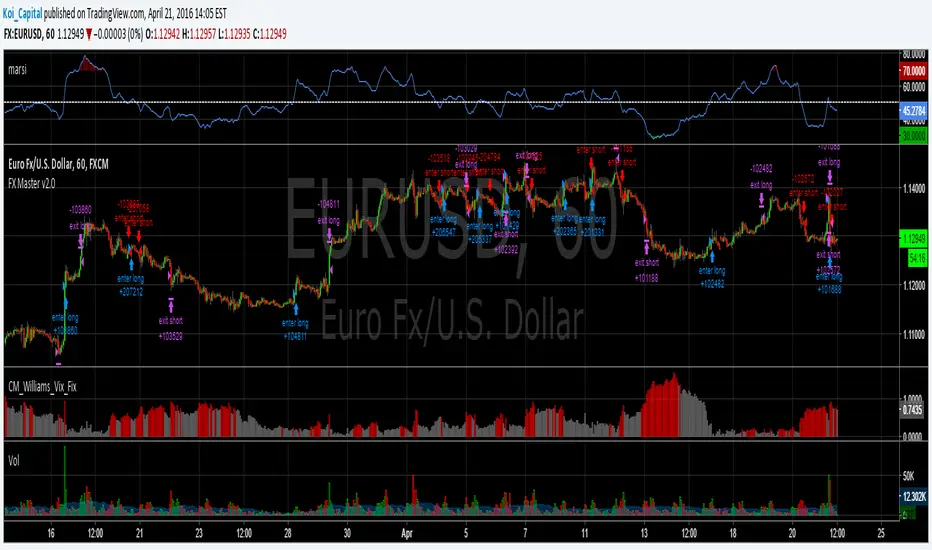

Forex Master v2.0 (EUR/USD)This is version 2 of my Forex Master algorithm originally posted here:

BACKTEST CONDITIONS:

Initial equity = $100,000 (no leverage)

Order size = 100% of equity

Pyramiding = disabled

TRADING RULES:

Long entry = EMA5(RSI20) cross> 50

Profit limit = 50 pips

Stop loss = 50 pips

Short entry = EMA5(RSI20) cross< 50

Profit limit = 50 pips

Stop loss = 50 pips

Long entry = Short exit

Short entry = long exit

DISCLAIMER: None of my ideas and posts are investment advice. Past performance is not an indication of future results. This strategy was constructed with the benefit of hindsight and its future performance cannot be guaranteed.

SPY Master v1.0This is a simple swing trading algorithm that uses a fast RSI-EMA to trigger buy/cover signals and a slow RSI-EMA to trigger sell/short signals for SPY, an xchange-traded fund for the S&P 500.

The idea behind this strategy follows the premise that most profitable momentum trades usually occur during periods when price is trending up or down. Periods of flat price actions are usually where most unprofitable trades occur. Because we cannot predict exactly when trending periods will occur, the algorithm basically bets money on all trade opportunities during all market conditions. Despite an accuracy rate of only 40%, the algorithm's asymmetric risk/reward profile allows the average winner to be 2x the average loser. The end result is a positive (profitable) net payout.

TRADING RULES:

Buy/Cover = EMA3(RSI2) cross> 50

Sell/Short = EMA5(RSI2) cross< 50

BACKTEST SETTINGS:

- Period = March 2011 - Present

- Initial capital = $10,000

- Dividends excluded

- Trading costs excluded

PERFORMANCE COMPARISON:

There are 657 trades, which means 1,314 orders. Assuming each order costs $2 (what I pay for at Interactive Brokers), total trading costs should be $2,628.

-SPY (buy & hold) = 132.73 ---> 193.22 = +45.57% (dividends excluded)

-SPY Master v1.0 = $12,649 - $2,628 = $10,021 = +100.21%

DISCLAIMER: None of my ideas and posts are investment advice. Past performance is not an indication of future results. This strategy was constructed with the benefit of hindsight and its future performance cannot be guaranteed.

Simple RSI-MA Algo Beats DOW By Huge Margin Over Past 100 Years!This simple RSI-MA long/short algorithm beats the Dow by a FREAKING HUGE margin over the past century (excluding dividends and trading costs).

The algorithm uses a fast SMA of the RSI as a buy/cover signal and a slow SMA of the RSI as a sell/short signal.

Backtest period = 09/17/1916 - 11/02/2015

Dow = 98 --> 17,830 = +18,094% = 5.38% CAGR

Algorithm = net profit + open P/L = +43,349% = 6.31% CAGR

Notice how the algorithm dodged both the 30s' Great Depression and the 2008 Crisis. Pretty cool huh? :)

ALGORITHM'S FORMULA (use weekly chart):

Buy/Cover = MA10(RSI10) cross> 50

Sell/Short = MA50(RSI10) cross< 50

STRATEGY TESTER'S SETTINGS:

- Initial cash = $10,000

- Pyramiding disabled

- Re-investment enabled (order size = 100% of equity )

- Trade re-calculations disabled

DISCLAIMER: None of my ideas and posts are investment advice. Past performance is not an indication of future results. This strategy was constructed with the benefit of hindsight and its future performance cannot be guaranteed.