Volume Weighted LR Standard DeviationThis indicator analyzes market character by decomposing total volatility into three distinct, interpretable components based on a Linear Regression model.

Key Features:

Three-Component Volatility Decomposition: The indicator separates volatility based on the 'Estimate Bar Statistics' option.

Standard Mode (Estimate Bar Statistics = OFF): Calculates volatility based on the selected Source (dies führt hauptsächlich zu 'Trend'- und 'Residual'-Volatilität).

Decomposition Mode (Estimate Bar Statistics = ON): The indicator uses a statistical model ('Estimator') to calculate within-bar volatility. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead). This separates volatility into:

Trend Volatility (Green/Red): Volatility explained by the regression's slope (Momentum).

Residual Volatility (Yellow): Volatility from price oscillating around the regression line (Mean-Reversion).

Within-Bar Volatility (Blue): Volatility from the high-low range of each bar (Noise/Choppiness).

Dual Display Modes: The indicator offers two modes to visualize this decomposition:

Absolute Mode: Displays the total standard deviation as a stacked area chart, partitioned by the variance ratio of the three components.

Normalized Mode: Displays the direct variance ratio (proportion) of each component relative to the total (0-1), ideal for identifying the dominant market character.

Calculation Options:

Normalization: An optional 'Normalize Volatility' setting calculates an Exponential Regression Curve (log-space), making the analysis suitable for growth assets.

Volume Weighting: An option (Volume weighted) applies volume weighting to all regression and volatility calculations.

Multi-Component Pivot Detection: Includes a pivot detector that identifies significant turning points (highs and lows) in both the Total Volatility and the Trend Volatility Ratio. (Note: These pivots are only plotted when 'Plot Mode' is set to 'Absolute').

Note on Confirmation (Lag): Pivot signals are confirmed using a lookback method. A pivot is only plotted after the Pivot Right Bars input has passed, which introduces an inherent lag.

Multi-Timeframe (MTF) Capability:

MTF Volatility Lines: The volatility lines can be calculated on a higher timeframe, with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Pivot detection (Calculate Pivots) is disabled if a Higher Timeframe (HTF) is selected.

Integrated Alerts: Includes 9 comprehensive alerts for:

Volatility character changes (e.g., 'Character Change from Noise to Trend').

Dominant character emerging (e.g., 'Bullish Trend Character Emerging').

Total Volatility pivot (High/Low) detection.

Trend Volatility pivot (High/Low) detection.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

ความผันผวน

Volume Weighted Standard DeviationThis indicator calculates the Standard Deviation and decomposes total volatility into its core components, allowing to analyze the underlying character of the market.

Key Features:

Volatility Decomposition: The indicator separates volatility based on the 'Estimate Bar Statistics' option.

Standard Mode (Estimate Bar Statistics = OFF): Calculates a simple (Volume-Weighted) Standard Deviation of the selected Source.

Decomposition Mode (Estimate Bar Statistics = ON): The indicator uses a statistical model ('Estimator') to calculate within-bar volatility (choppiness, noise) and between-bar volatility (trending moves). (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead).

Dual Display Modes: The indicator offers two modes to visualize this information:

Absolute Mode: Plots the total standard deviation as a stacked area chart, showing the proportional contribution of the 'Between' and 'Within' components.

Normalized Mode: Plots the direct ratio of each component's variance (from 0 to 1), making it easy to identify which character is dominant.

Calculation Options: The volatility calculation can be optionally Volume weighted. An optional Normalize Volatility setting performs the calculation in logarithmic space, making volatility comparable across different price scales.

Volatility Pivot Detection: Includes a built-in pivot detector that identifies significant turning points (highs and lows) in the total volatility line. (Note: This is only visible in 'Absolute Mode').

Note on Confirmation (Lag): Pivot signals are confirmed using a lookback method. A pivot is only plotted after the Pivot Right Bars input has passed, which introduces an inherent lag.

Multi-Timeframe (MTF) Capability:

MTF Volatility Lines: The volatility lines can be calculated on a higher timeframe, with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Pivot detection (Calculate Pivots) is disabled if a Higher Timeframe (HTF) is selected.

Integrated Alerts: Includes 6 alerts for:

Volatility character changes (e.g., 'Trend Character Emerging', 'Character Change from Trend to Choppy').

Volatility pivot (high or low) detection.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Volume Weighted Average True RangeThis indicator calculates a customizable version of the Average True Range (ATR), a tool for measuring market volatility. It enhances the standard ATR with volume weighting, a dual-smoothing process, normalization, and volatility pivot detection.

Key Features:

Volume Weighting: An option (Volume weighted) allows for volume to be incorporated into the volatility calculation. This provides a measure of "volume-adjusted" volatility that is more responsive to significant market activity.

Dual Smoothing Process: For noise reduction, the indicator employs a two-stage smoothing process. It first calculates a smoothed True Range (TR) over a user-defined period (TR Length) before applying the final ATR moving average (ATR Length & ATR Smooth).

Normalization (Percentage Volatility): An optional 'Normalize' mode calculates the ATR as a percentage of the price. This allows for consistent volatility comparison across different assets and over long time periods.

Volatility Pivot Detection: The indicator includes a built-in pivot detector that identifies significant turning points (highs and lows) in the ATR line itself, signaling potential shifts in volatility.

Note on Confirmation (Lag): Pivot signals are confirmed using a lookback method. A pivot is only plotted after the Pivot Right Bars input has passed. This is essential for ensuring the signal is non-repainting but introduces an inherent lag.

Multi-Timeframe (MTF) Capability:

MTF ATR Line: The ATR line itself can be calculated on a different timeframe, with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Pivot detection (Calculate Pivots) is disabled if a Higher Timeframe (HTF) is selected.

Integrated Alerts: Includes alerts that trigger when a new volatility pivot (high or low) is detected in the ATR line.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Chaikin Money FlowThis indicator provides an implementation of the classic Chaikin Money Flow (CMF), a volume-weighted oscillator designed to measure money flow pressure. It is enhanced with a customizable signal line and a built-in divergence detection engine.

Key Features:

Full Divergence Suite (Class A, B, C): The primary feature is the integrated divergence engine. It automatically detects and plots all three major types of divergences:

Regular (A): Signals potential trend reversals.

Hidden (B): Signals potential trend continuations.

Exaggerated (C): Signals weakness at double tops/bottoms.

Divergence Filtering and Visualization:

Price Tolerance Filter: Divergence detection is enhanced with a percentage-based price tolerance (pivPrcTol) to filter out insignificant market noise, leading to more robust signals.

Persistent Visualization: Divergence markers are plotted for the entire duration of the signal and are visually anchored to the CMF level of the confirming pivot.

Customizable Signal Line: Includes an optional moving average of the CMF, which serves as a signal line. The type of MA (Signal Smoothing) and its length can be customized. This signal line can also be optionally volume-weighted (Volume weighted).

Note on Confirmation (Lag): Divergence signals rely on a pivot confirmation method to ensure they do not repaint.

The Start of a- divergence is only detected after the confirming pivot is fully formed (a delay based on Pivot Right Bars).

The End of a divergence is detected either instantly (if the signal is invalidated by price action) or with a delay (when a new, non-divergent pivot is confirmed).

Multi-Timeframe (MTF) Capability:

MTF CMF & Signal Lines: The CMF and its signal line can be calculated on a higher timeframe, with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Divergence detection engine (pivDiv) is disabled if a timeframe other than the chart's timeframe is selected. Divergences are only calculated on the active chart timeframe.

Integrated Alerts: Includes 16 comprehensive alerts for:

The start and end of all 6 divergence types.

The CMF crossing its signal line.

The CMF crossing the zero line.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Volume Weighted Bollinger BandsThis indicator provides a customizable version of Bollinger Bands, enhanced with optional volume weighting and a method for decomposing market volatility.

Key Features:

Volatility Decomposition: The indicator's primary feature is its ability to separate total volatility, controlled by the 'Estimate Bar Statistics' option.

Standard Mode (Estimate Bar Statistics = OFF): The indicator functions as a customizable Bollinger Band. It calculates the standard deviation of the user-selected Source and plots a single set of bands.

Decomposition Mode (Estimate Bar Statistics = ON): The indicator uses a statistical model ('Estimator') to calculate within-bar volatility. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead). This mode displays two sets of bands:

Inner Bands: Show only the contribution of the 'between-bar' volatility.

Outer Bands: Show the total volatility (the sum of between-bar and within-bar components).

Customizable Construction: The indicator is a hybrid:

Basis Line: The central line is calculated using a selectable Moving Average type (e.g., EMA, SMA, WMA).

Volume Weighting: An option (Volume weighted) allows for volume to be incorporated into the calculation of both the basis MA and the volatility decomposition.

Logarithmic Scaling: An optional 'Normalize' mode calculates the bands on a logarithmic scale. This results in bands that maintain a constant percentage distance from the basis, suitable for analyzing exponential markets.

Multi-Timeframe (MTF) Engine: The indicator includes an MTF conversion block. When a Higher Timeframe (HTF) is selected, advanced options become available: Fill Gaps handles data gaps, and Wait for timeframe to close prevents repainting by ensuring the indicator only updates when the HTF bar closes.

Integrated Alerts: Includes a full set of built-in alerts for the source price crossing over or under the central MA line and the outermost calculated volatility band.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Firex Data Trade 5* SetupIdentifies Boring, Quiet, No Supply / No Demand candles. "

+ "Highlights potential 5★ setups for trading confirmation when price breaks candle highs/lows. "

+ "Helps traders spot low-volume turning points and breakout opportunities

Volume Weighted Keltner ChannelThis indicator provides a customizable implementation of Keltner Channels (KC), a volatility-based envelope designed to identify trend direction and potential reversal or breakout zones. It allows deep control over its core components and calculation methods.

Key Features:

Customizable Components: This implementation allows for full control over the channel's construction:

Basis Line: Choose from a wide range of moving average types (e.g., EMA, SMA, WMA) for the central line.

Volatility Bands: Select the volatility measure used to construct the bands: Average True Range (ATR), True Range (TR), or bar Range (High-Low).

Volume Weighting: An option (Volume weighted) allows for volume to be incorporated into the calculation of both the basis moving average and the selected volatility measure (e.g., creating a Volume-Weighted ATR). This makes the channel more responsive to moves backed by high market participation.

Logarithmic Scaling: The indicator includes an optional 'Normalize' mode that calculates the channel on a logarithmic scale. This creates bands that represent a constant percentage distance from the basis, making it a suitable tool for analyzing long-term trends in exponential markets.

Multi-Timeframe (MTF) Engine: The indicator includes an MTF conversion block. When a Higher Timeframe (HTF) is selected, advanced options become available: Fill Gaps handles data gaps, and Wait for timeframe to close prevents repainting by ensuring the indicator only updates when the HTF bar closes.

Integrated Alerts: Includes a full set of built-in alerts for the source price crossing over or under the upper band, lower band, and the central basis line.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Crypto Futures Basis Tracker (Annualized)🧩 What is Basis Arbitrage

Basis arbitrage is a market-neutral trading strategy that exploits the price difference between a cryptocurrency’s spot and its futures markets.

When futures trade above spot (called contango), traders can buy spot and short futures, locking in a potential yield.

When futures trade below spot (backwardation), the reverse applies — short spot and go long futures.

The yield earned (or cost paid) by holding this position until expiry is called the basis. Expressing it as an annualized percentage allows comparison across different contract maturities.

⚙️ How the Indicator Works

This tool calculates the annualized basis for up to 10 cryptocurrency futures against a chosen spot price.

You select one spot symbol (e.g., BITSTAMP:BTCUSD) and up to 10 futures symbols (e.g., DERIBIT:BTCUSD07X2025, DERIBIT:BTCUSD14X2025, etc.).

The script automatically computes the days-to-expiry (DTE) and the annualized basis for each future.

A table displays for each contract: symbol, expiry date, DTE, last price, and annualized basis (%) — making it easy to compare the forward curve across maturities.

⚠️ Risks and Limitations

While basis arbitrage is often considered low-risk, it’s not risk-free:

Funding and financing costs can erode returns, especially when borrowing or using leverage.

Exchange or counterparty risk — if one leg of the trade fails (e.g., exchange default, margin liquidation), the hedge breaks.

Execution and timing risk — the basis can tighten or invert before both legs are opened.

Liquidity differences — thin futures may have large bid-ask spreads or slippage.

Use this indicator for analysis and monitoring, not as an automated trading signal.

Disclaimer: Please remember that past performance may not be indicative of future results. Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting. This post and the script don't provide any financial advice.

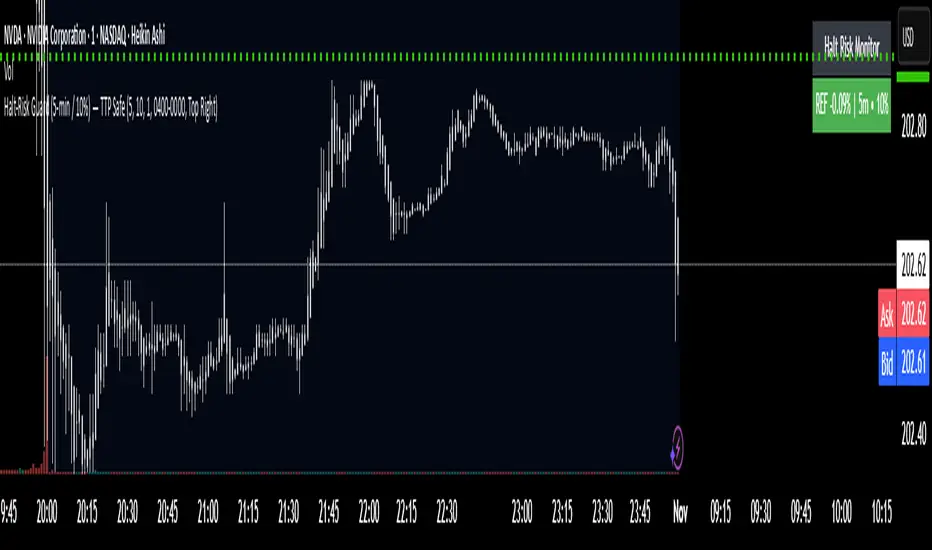

Halt-Risk Guard (5-min / 10%) — TTP Safe🛑 Halt-Risk Guard (5-min / 10%) — TTP Safe

Stay clear of halts, invalidations, and over-extended moves.

🔍 Overview

The Halt-Risk Guard helps traders avoid sudden invalidations by monitoring price velocity over the past X minutes (default: 5 min) and flagging when moves exceed a configurable threshold (default: 10%).

Originally built to meet Trade The Pool (TTP) risk-management rules — where even non-halted 10% moves can void trades — this tool provides a clear, visual warning system and optional entry blocker.

⚙️ Key Features

✅ Halt-Risk Detection – Calculates both reference-based and swing-based (high↔low) percentage change over the chosen lookback period.

✅ TTP Safe Mode – “Swing mode” captures extreme volatility spikes that may invalidate trades even when the market stays open.

✅ Entry Blocker (optional) – Automatically greys candles and dims the background during risky conditions to prevent impulsive entries.

✅ Customisable Positioning – Move the on-chart info box to any corner of your chart (Top Left / Top Right / Bottom Left / Bottom Right).

✅ Clean Alerts –

⚠️ At/Above Threshold

✅ Back to Safe

⛔ Entry Blocker Active

✅ Visual Table Display – Compact dashboard shows current % move, lookback window, and threshold with intuitive green/red status.

✅ Strategy-Ready Output – A hidden 0/1 plot lets you block or filter trades in automated systems.

⚡ How It Works

Monitors the selected symbol using your chosen computation timeframe (recommended 1-minute).

Evaluates either:

REF mode: Close-to-close change over the lookback window.

SWING mode: High-to-low range within the same window.

If the move ≥ Threshold %, the script highlights a halt-risk condition and optionally activates the entry blocker.

🎨 Recommended Settings

Lookback: 5 minutes

Threshold: 10 %

Swing mode: ON (TTP-safe)

Computation timeframe: 1 minute

Entry blocker: ON

Dim background: ON

🧠 Use Cases

TTP and other prop-firm evaluations enforcing price-movement limits.

Volatility-based scalping systems to avoid chasing extended candles.

Strategy filters for algorithmic entries (e.g. pause trading during halt-risk windows).

⚠️ Disclaimer

This tool provides visual and alert-based guidance only. It does not guarantee compliance with any specific firm’s rules or eliminate trading risk. Always verify thresholds and rules with your broker or evaluation provider.

Volatility Resonance CandlesVolatility Resonance Candles visualize the dynamic interaction between price acceleration, volatility, and volume energy.

They’re designed to reveal moments when volatility expansion and directional momentum resonate — often preceding strong directional moves or reversals.

🔬 Concept

Traditional candles display direction and range, but they miss the energetic structure of volatility itself.

This indicator introduces a resonance model, where ATR ratio, price acceleration, and volume intensity combine to form a composite signal.

* ATR Resonance: compares short-term vs. long-term volatility

* Acceleration: captures the rate of price change

* Volume Energy: reinforces the move’s significance

When these components align, the candle color “resonates” — brighter, more intense candles signal stronger volatility–momentum coupling.

⚙️ Features

* Adaptive Scaling

Normalizes energy intensity dynamically across a user-defined lookback period, ensuring consistency in changing market conditions.

* Power-Law Transformation

Optional non-linear scaling (gamma) emphasizes higher-energy events while keeping low-intensity noise visually subdued.

* Divergence Mode

When enabled, colors can invert to highlight energy divergence from candle direction (e.g., bearish pressure during bullish closes).

* Customizable Styling

Full control over bullish/bearish base colors, transparency scaling, and threshold sensitivity.

🧠 Interpretation

* Bright / High-Intensity Candles → Strong alignment of volatility and directional energy.

Often signals the resonant phase of a move — acceleration backed by volatility expansion and volume participation.

* Dim / Low-Intensity Candles → Energy dispersion or consolidation.

These typically mark quiet zones, pauses, or inefficient volatility.

* Opposite-Colored Candles (if divergence mode on) → Potential inflection zones or hidden stress in the trend structure.

⚠️ Disclaimer

This script is for educational purposes only.

It does not constitute financial advice, and past performance is not indicative of future results. Always do your own research and test strategies before making trading decisions.

Murrey Math SMA up to 32s Murrey Math SMA up to 32s is a highly advanced Pine Script v5 indicator that combines Murrey Math Lines (MML) with a customizable moving average (MA) — including a non-repainting Rolling VWAP (RVWAP) — and dynamic color-coded support/resistance bands up to 1/32 subdivisions. It projects octave-based geometric price levels (like Gann) centered on your chosen MA, with adaptive scaling, angle-based trend coloring, and absolute/extended MML bands. Includes 1/8, 1/16, and 1/32 grid lines, shaded zones, labels, and a live increment display.Core FeaturesFeature

Description

MA Types

SMA, VWMA, VWAP, Period VWAP, RVWAP (rolling VWAP over fixed or adaptive time window)

Murrey Math Grid

Auto-scaled 0/8 to 8/8 + extensions (±3/8), with 1/16 & 1/32 subdivisions

Dynamic Coloring

Bands colored by MA slope angle (bullish/bearish) or absolute MML shift

RVWAP Engine

Non-repainting volume-weighted average over user-defined or adaptive time steps

Wick Filtering

Optional ignore wicks for cleaner MML framing

Resolution Support

Works with higher timeframe data via request.security()

Key Use Cases Use Case

How to Use

1. Precision Support & Resistance

Treat 4/8 (mid) as pivot, 0/8 & 8/8 as extremes. Price often reverses or accelerates at these levels.

2. Mean Reversion Trades

Buy near 0/8–1/8 (oversold), sell near 7/8–8/8 (overbought) when MA is flat or sloping mildly.

3. Trend Continuation

When MA angle > threshold and price breaks 5/8, expect move to 8/8. Confirm with volume.

4. Breakout Entries

Watch for close beyond 8/8 or 0/8 + MA angle steep → strong momentum breakout.

5. Scalping with 1/32 Grid

Use 1/32 lines as micro-targets in ranging markets or after news spikes.

6. Volume-Weighted Fair Value

RVWAP = true average price paid over time → anchor for institutional fair value.

Visual Layout (MA-Centered)

+3/8 ───┐

+2/8 ───┤ ← Strong resistance

+1/8 ───┤

8/8 ███┤ ← Overbought (red zone)

7/8 ───┤

6/8 ███┤

5/8 ───┤

4/8 ███┤ ← Midline (pivot)

3/8 ───┤

2/8 ███┤

1/8 ───┤

0/8 ███┤ ← Oversold (green zone)

-1/8 ───┤

-2/8 ───┤

-3/8 ───┘

Shaded: 0/8–1/8 (buy), 7/8–8/8 (sell), 3/8–5/8 (neutral/consolidation)

MA Line: Orange (RVWAP) or hidden

Labels: Bottom, 1/4, Mid, 3/4, Top (offset to the right)

Table: Shows current Increment size

Best For Swing & scalp traders on stocks, forex, crypto

Volume-based strategies (RVWAP shines in high-volume moves)

Gann/Murrey Math enthusiasts wanting automation + modern MA anchoring

Uptrick: Volume Weighted BandsIntroduction

This indicator, Uptrick: Volume Weighted Bands, overlays dynamic, volume-informed trend channels directly on the chart. By fusing price and volume data through volume-weighted and exponential moving averages, the script forms a core trend line with adaptive bandwidth controlled by volatility. It is designed to help traders identify trend direction, breakout entries, and extended conditions that may warrant take-profits or pullback re-entries.

Overview

The Volume Weighted Bands system is built around a trend line calculated by averaging a Volume Weighted Moving Average (VWMA) and an Exponential Moving Average (EMA), both over a configurable lookback period. This hybrid trend baseline is then smoothed further and expanded into dynamic upper and lower bands using an Average True Range (ATR) multiplier. These bands adapt with market volatility and shift color based on prevailing price action, helping traders quickly identify bullish, bearish, or neutral conditions.

Originality and Unique Features

This script introduces originality by blending both price and volume in the core trend calculation, a technique that is more responsive than traditional moving average bands. Its multi-mode visualization (cloud, single-band, or line-only), combined with selective buy/sell signals, makes it flexible for discretionary and algorithmic strategies alike. Optional modules for take-profit signals based on z-score deviation and RSI slope, as well as buy-back detection logic with cooldown filters, offer practical tools for managing trades beyond simple entries.

Explanation of Inputs

Every user input in this script is included to give the trader control over behavior and visual presentation:

Trend Length (len): Defines the lookback window for both the VWMA and EMA, controlling the sensitivity of the core trend baseline. A lower value makes the bands more reactive, while a higher value smooths out short-term noise.

Extra Smoothing (smoothLen): Applies an additional EMA to the blended VWMA/EMA average. This second-level smoothing ensures the central trend line reacts gradually to shifts in price.

Band Width (ATR Multiplier) (bandMult): Multiplies the ATR to create the width of the upper and lower bands around the trend line. Larger values widen the bands, capturing more volatility, while smaller values narrow them.

ATR Length (atrLen): Sets the length of the ATR used in calculating band width and signal offsets. Longer values produce smoother band boundaries.

Show Buy/Sell Signals (showSignals): Toggles the primary crossover/crossunder entry signals, which are labeled when the close crosses the upper or lower band.

Visual Mode (visualMode): Allows selection between three display modes:

--> Cloud: Shows both bands and the central trend line with a shaded background.

--> Single Band: Displays only the active (upper or lower) band depending on trend state, with gradient fill to price.

--> Line Only: Shows only the trend line for a minimal visual profile.

Take Profit Signals (enableTP): Enables a z-score-based profit-taking signal system. Signals occur when price deviates significantly from the trend line and RSI confirms exhaustion.

TP Z-Score Threshold (tpThreshold): Sets the z-score deviation required to trigger a take-profit signal. Higher values reduce the frequency of signals, focusing on more extreme moves.

Re-Entries (enableBuyBack): Enables logic to signal when price reverts into the band after an initial breakout, suggesting a possible re-entry or pullback setup.

Buy Back Cooldown (bars) (buyBackCooldown): Defines a minimum bar count before a new buy-back signal is allowed, preventing rapid retriggering in choppy conditions.

Buy Offset and Sell Offset: Hidden inputs used to vertically adjust the placement of the Buy ("𝓤𝓹") and Sell ("𝓓𝓸𝔀𝓷") labels relative to the bands. These use ATR units to maintain proportionality across different instruments and timeframes.

Take-Profit Signal Module

The take-profit module uses a z-score of the distance between price and the trend line to detect extended conditions. In bullish trends, a signal appears when price is well above the band and RSI indicates exhaustion; the opposite applies for bearish conditions. A boolean flag is used to prevent retriggering until RSI resets. These signals are plotted with minimalist “X” markers near recent highs or lows, based on whether the market is extended upward or downward.

Re-Entry Logic

The re-entry system identifies instances where price momentarily dips or spikes into the opposite band but closes back inside, implying a continuation of the prevailing trend. This module can be particularly useful for traders managing entries after brief pullbacks. A built-in cooldown period helps filter out noise and prevents signal overloading during fast markets. Visual markers are shown as upward or downward arrows near the relevant candle wicks.

How to Use This Indicator

The basic usage of this indicator follows a directional, signal-driven approach. When a buy signal appears, it suggests entering a long position. The recommended stop loss placement is below the lower band, allowing for some breathing space to accommodate natural volatility. As the position progresses, take partial profits—typically 10% to 15% of the position—each time a take-profit signal (marked with an "X") is shown on the chart.

An optional feature is the buy-back signal, which can be used to re-enter after partial exits or missed entries. Utilizing this can help reduce losses during false breakouts or trend reversals by scaling in more gradually. However, it also means that in strong, clean trends, the full position may not be captured from the start, potentially reducing the total return. It is up to the trader to decide whether to enter fully on the initial signal or incrementally using buy-backs.

When a sell signal appears, the strategy advises fully exiting any long positions and immediately switching to a short position. The short trade follows the same logic: place your stop loss above the upper band with some margin, and again, take partial profits at each take-profit signal.

Visual Presentation and Signal Labels

All signals are plotted with clean, minimal labels that avoid clutter, and are color-coded using a custom palette designed to remain clear across light and dark chart themes. Bullish trends are marked in teal and bearish trends in magenta. Candles and wicks are also colored accordingly to align price action with the detected trend state. Buy and sell entries are marked with "𝓤𝓹" and "𝓓𝓸𝔀𝓷" labels.

Summary

In summary, the Uptrick: Volume Weighted Bands indicator provides a versatile, visually adaptive trend and volatility tool that can serve multiple styles of trading. Through its integration of price, volume, and volatility, along with modular take-profit and buy-back signaling, it aims to provide actionable structure across a range of market conditions.

Disclaimer

This indicator is for educational purposes only. Trading involves risk, and past performance does not guarantee future results. Always test strategies before applying them in live markets.

AMF PG Strategy v2.3AMF PG Strategy v2.3

1. Core Philosophy: Filtered and Volatility-Aware Trend Following

"AMF PG Strategy" is an advanced trend-following system designed to adapt to the dynamic nature of modern markets. The strategy's core philosophy is not just to follow the trend but also to wait for the right conditions to enter the market.

This is not a "black box." It is a rules-based framework that gives the user full control over various market filters. By requiring multiple conditions to be met simultaneously, the strategy aims to filter out low-quality signals and focus only on high-probability trend opportunities.

2. Core Engine: AMF PG Trend Following

At the heart of the strategy is a proprietary, volatility-aware trend-following mechanism called AMF PG (Praetorian Guard). This engine operates as follows:

Dynamic Bands: Creates a dynamic upper and lower band around the price that is constantly recalculated. The width of these bands is not fixed; It dynamically adjusts based on recent market volatility, volume flow, and price expansion. This adaptive structure allows the strategy to adapt to both calm and high-volatility markets.

Entry Signals: A buy signal is triggered when the price rises above the upper band. A sell signal is triggered when the price falls below the lower band. However, these signals are executed only when all the active filters described below give the green light.

Trailing Stop-Loss: When a position is entered, the opposite band automatically acts as a trailing stop-loss level. For example, when a buy position is opened, the lower band follows the price as a stop-loss. This allows for profit retention and trend continuation.

3. Multi-Layered Filter System: Understanding the Market

The power of this strategy comes from its modular filter system, which allows the user to filter market conditions based on their own analysis. Each filter can be enabled or disabled individually in the settings:

Filter 1: Trend Strength (ADX Filter): This filter confirms whether there is a strong trend in the market. It uses the ADX (Average Directional Index) indicator and only allows trades if the ADX value is above a certain threshold. This helps avoid trading in weak or directionless markets. It also confirms the direction of the trend by checking the position of the DMI (+DI and -DI) lines.

Filter 2: Sideways Market (Chop Index Filter): This filter determines whether the market is excessively choppy or directionless. Using the Chop Index, this filter aims to protect against fakeouts by blocking trades when the market is highly indecisive.

Filter 3: Market Structure (Hurst Exponent Filter): This is one of the strategy's most advanced filters. It analyzes the current market behavior using the Hurst Exponent. This mathematical tool attempts to determine whether a market tends to trend (permanent), tends to revert to the mean (anti-permanent), or moves randomly. This filter ensures that signals are generated only when market structure supports trending trades.

4. Risk Management: Maximum Drawdown Protection

This strategy includes a built-in capital protection mechanism. Users can specify the percentage of their capital they will tolerate to decline from its peak. If the strategy's capital reaches this set drawdown limit, the protection feature is activated, closing all open positions and preventing new trades from being opened. This acts as an emergency brake to protect capital against unexpected market conditions.

5. Automation Ready: Customizable Webhook Alerts

The strategy is designed for traders who want to automate their signals. From the Settings menu, you can configure custom alert messages in JSON format, compatible with third-party automation services (via Webhooks).

6. Strategy Backtest Information

Please note that past performance is not indicative of future results. The published chart and performance report were generated on the 4-hour timeframe of the BTCUSD pair with the following settings:

Test Period: January 1, 2016 - October 31, 2025

Default Position Size: 15% of Capital

Pyramiding: Closed

Commission: 0.0008

Slippage: 2 ticks (Please enter the slippage you used in your own tests)

Testing Approach: The published test includes 423 trades and is statistically significant. It is strongly recommended that you test on different assets and timeframes for your own analysis. The default settings are a template and should be adjusted by the user for their own analysis.

Sector Relative StrengthThis indicator measures a stock's Real Relative Strength against its sector benchmark, helping you identify stocks that are outperforming or underperforming their sector peers.

The concept is based on the Real Relative Strength methodology popularized by the r/realdaytrading community.

Unlike traditional relative strength calculations that simply compare price ratios, this indicator uses a more sophisticated approach that accounts for volatility through ATR (Average True Range), providing a normalized view of true relative performance.

Key Features

Automatic Sector Detection

Automatically detects your stock's sector using TradingView's built-in sector classification

Maps to the appropriate SPDR Sector ETF (XLK, XLF, XLV, XLY, XLP, XLI, XLE, XLU, XLB, XLC)

Supports all 20 TradingView sectors

Sector ETF Mappings

The indicator automatically compares your stock against:

Technology: XLK (Technology Services, Electronic Technology)

Financials: XLF (Finance sector)

Healthcare: XLV (Health Technology, Health Services)

Consumer Discretionary: XLY (Retail Trade, Consumer Services, Consumer Durables)

Consumer Staples: XLP (Consumer Non-Durables)

Industrials: XLI (Producer Manufacturing, Industrial Services, Transportation, Commercial Services)

Energy: XLE (Energy Minerals)

Utilities: XLU

Materials: XLB (Non-Energy Minerals, Process Industries)

Communications: XLC

Default: SPY (for Miscellaneous or unclassified sectors)

Customizable Settings

Comparison Mode: Choose between automatic sector comparison or custom symbol

Length: Adjustable lookback period (default: 12)

Smoothing: Apply moving average to reduce noise (default: 3)

Visual Clarity

Green line: Stock is outperforming its sector

Red line: Stock is underperforming its sector

Zero baseline: Clear reference point for performance

Clean info box: Shows which ETF you're comparing against

How It Works

The indicator calculates relative strength using the following methodology:

Rolling Price Change: Measures the price movement over the specified length for both the stock and its sector ETF

ATR Normalization: Uses Average True Range to normalize for volatility differences

Power Index: Calculates the sector's strength relative to its volatility

Real Relative Strength: Compares the stock's performance against the sector's power index

Smoothing: Applies a moving average to reduce single-candle spikes

Formula:

Power Index = (Sector Price Change) / (Sector ATR)

RRS = (Stock Price Change - Power Index × Stock ATR) / Stock ATR

Smoothed RRS = SMA(RRS, Smoothing Length)

Candlestick StrengthThis indicator quantifies the “energy” of each candlestick by combining its height (high–low span), trading volume, and internal structure (body vs. wick proportions). It provides a numeric measure of how strongly each candle contributes to market momentum, allowing traders to distinguish meaningful price action from indecision or noise.

Concept

Every candlestick represents a short-term contest between buyers and sellers. Large candles with significant volume indicate strong market participation, while small or low-volume candles suggest hesitation or absorption. Candlestick Strength captures this by calculating a normalized measure of each candle’s energy relative to recent activity, making it comparable across different market conditions and timeframes.

The indicator also analyzes the candle’s internal structure:

The body reflects net directional movement.

The wicks represent back-and-forth price traversal within the candle. Because wick movement does not fully contribute to directional momentum, it is weighted at half the body’s contribution. This ensures the indicator emphasizes sustained directional pressure while still acknowledging rejection or absorption.

Interpretation

High values indicate candles with energy above recent averages — suggesting expanding momentum and strong directional intent.

Average values reflect typical candle activity, representing neutral or steady market behavior.

Low values suggest weak candles — either the market is pausing, consolidating, or momentum is fading.

The outputs are displayed as a symmetric histogram: bullish candle energy is shown in green above zero, bearish energy in red below zero, with ±1 reference lines marking the normalized average energy level.

Usage

Combine with trend analysis, swing highs/lows, or volume-weighted averages to validate breakouts or trend continuation.

Monitor for divergence between price movement and candle energy to identify exhaustion, absorption, or potential reversals.

Filter out false momentum signals caused by narrow-range or low-volume candles.

Adaptable across timeframes: normalized energy allows comparison between small and large timeframe candles.

Vandan V2Vandan V2 is an automated trend-following strategy for NASDAQ E-mini Futures (NQ1!).

It uses multi-timeframe momentum and volatility filters to identify high-probability entries.

Includes dynamic risk management and trailing logic optimized for intraday trading.

ATR x Trend x Volume SignalsATR x Trend x Volume Signals is a multi-factor indicator that combines volatility, trend, and volume analysis into one adaptive framework. It is designed for traders who use technical confluence and prefer clear, rule-based setups.

🎯 Purpose

This tool identifies high-probability market moments when volatility structure (ATR), momentum direction (CCI-based trend logic), and volume expansion all align. It helps filter out noise and focus on clean, actionable trade conditions.

⚙️ Structure

The indicator consists of three main analytical layers:

1️⃣ ATR Trailing Stop – calculates two adaptive ATR lines (fast and slow) that define volatility context, trend bias, and potential reversal points.

2️⃣ Trend Indicator (CCI + ATR) – uses a CCI-based logic combined with ATR smoothing to determine the dominant trend direction and reduce false flips.

3️⃣ Volume Analysis – evaluates volume deviations from their historical average using standard deviation. Bars are highlighted as medium, high, or extra-high volume depending on intensity.

💡 Signal Logic

A Buy Signal (green) appears when all of the following are true:

• The ATR (slow) line is green.

• The Trend Indicator is blue.

• A bullish candle closes above both the ATR (slow) and the Trend Indicator.

• The candle shows medium, high, or extra-high volume.

A Sell Signal (red) appears when:

• The ATR (slow) line is red.

• The Trend Indicator is red.

• A bearish candle closes below both the ATR (slow) and the Trend Indicator.

• The candle shows medium, high, or extra-high volume.

Only one signal can appear per ATR trend phase. A new signal is generated only after the ATR direction changes.

❌ Exit Logic

Exit markers are shown when price crosses the slow ATR line. This behavior simulates a trailing stop exit. The exit is triggered one bar after entry to prevent same-bar exits.

⏰ Session Filter

Signals are generated only between the user-defined session start and end times (default: 14:00–18:00 chart time). This allows the trader to limit signal generation to active trading hours.

💬 Practical Use

It is recommended to trade with a fixed risk-reward ratio such as 1 : 1.5. Stop-loss placement should be beyond the slow ATR line and adjusted gradually as the trade develops.

For better confirmation, the Trend Indicator timeframe should be higher than the chart timeframe (for example: trading on 1 min → set Trend Indicator timeframe to 15 min; trading on 5 min → set to 1 hour).

🧠 Main Features

• Dual ATR volatility structure (fast and slow)

• CCI-based trend direction filtering

• Volume deviation heatmap logic

• Time-restricted signal generation

• Dynamic trailing-stop exit system

• Non-repainting logic

• Fully optimized for Pine Script v6

📊 Usage Tip

Best results are achieved when combining this indicator with additional technical context such as support-resistance, higher-timeframe confirmation, or market structure analysis.

📈 Credits

Inspired by:

• ATR Trailing Stop by Ceyhun

• Trend Magic by Kivanc Ozbilgic

• Heatmap Volume by xdecow

Volume Sentiment Breakout Channels [AlgoAlpha]🟠 OVERVIEW

This tool visualizes breakout zones based on volume sentiment within dynamic price channels . It identifies high-impact consolidation areas, quantifies buy/sell dominance inside those zones, and then displays real-time shifts in sentiment strength. When the market breaks above or below these sentiment-weighted channels, traders can interpret the event as a change in conviction, not just a technical breakout.

🟠 CONCEPTS

The script builds on two layers of logic:

Channel Detection : A volatility-based algorithm locates price compression areas using normalized highs and lows over a defined lookback. These “boxes” mark accumulation or distribution ranges.

Volume Sentiment Profiling : Each channel is internally divided into small bins, where volume is aggregated and signed by candle direction. This produces a granular sentiment map showing which levels are dominated by buyers or sellers.

When a breakout occurs, the script clears the previous box and forms a new one, letting traders visually track transitions between phases of control. The colored gradients and text updates continuously reflect the internal bias—green for net-buying, red for net-selling—so you can see conviction strength at a glance.

🟠 FEATURES

Volume-weighted sentiment map inside each box, with gradient color intensity proportional to participation.

Dynamic text display of current and overall sentiment within each channel.

Real-time trail lines to show active bullish/bearish trend extensions after breakout.

🟠 USAGE

Setup : Add the script to your chart and enable Strong Closes Only if you prefer cleaner breakouts. Use shorter normalization length (e.g., 50–80) for fast markets; longer (100–200) for smoother transitions.

Read Signals : Transparent boxes mark active sentiment channels. Green gradients show buy-side dominance, red shows sell-side. The middle dashed line is the equilibrium of the channel. “▲” appears when price breaks upward, “▼” when it breaks downward.

Understanding Sentiment : The sentiment profile can be used to show the probability of the price moving up or down at respective price levels.

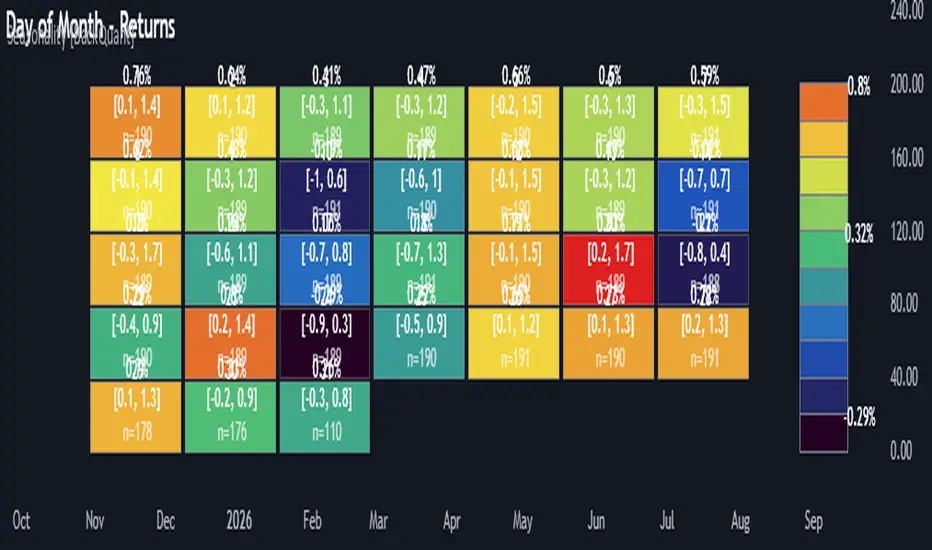

Multi-Mode Seasonality Map [BackQuant]Multi-Mode Seasonality Map

A fast, visual way to expose repeatable calendar patterns in returns, volatility, volume, and range across multiple granularities (Day of Week, Day of Month, Hour of Day, Week of Month). Built for idea generation, regime context, and execution timing.

What is “seasonality” in markets?

Seasonality refers to statistically repeatable patterns tied to the calendar or clock, rather than to price levels. Examples include specific weekdays tending to be stronger, certain hours showing higher realized volatility, or month-end flow boosting volumes. This tool measures those effects directly on your charted symbol.

Why seasonality matters

It’s orthogonal alpha: timing edges independent of price structure that can complement trend, mean reversion, or flow-based setups.

It frames expectations: when a session typically runs hot or cold, you size and pace risk accordingly.

It improves execution: entering during historically favorable windows, avoiding historically noisy windows.

It clarifies context: separating normal “calendar noise” from true anomaly helps avoid overreacting to routine moves.

How traders use seasonality in practice

Timing entries/exits : If Tuesday morning is historically weak for this asset, a mean-reversion buyer may wait for that drift to complete before entering.

Sizing & stops : If 13:00–15:00 shows elevated volatility, widen stops or reduce size to maintain constant risk.

Session playbooks : Build repeatable routines around the hours/days that consistently drive PnL.

Portfolio rotation : Compare seasonal edges across assets to schedule focus and deploy attention where the calendar favors you.

Why Day-of-Week (DOW) can be especially helpful

Flows cluster by weekday (ETF creations/redemptions, options hedging cadence, futures roll patterns, macro data releases), so DOW often encodes a stable micro-structure signal.

Desk behavior and liquidity provision differ by weekday, impacting realized range and slippage.

DOW is simple to operationalize: easy rules like “fade Monday afternoon chop” or “press Thursday trend extension” can be tested and enforced.

What this indicator does

Multi-mode heatmaps : Switch between Day of Week, Day of Month, Hour of Day, Week of Month .

Metric selection : Analyze Returns , Volatility ((high-low)/open), Volume (vs 20-bar average), or Range (vs 20-bar average).

Confidence intervals : Per cell, compute mean, standard deviation, and a z-based CI at your chosen confidence level.

Sample guards : Enforce a minimum sample size so thin data doesn’t mislead.

Readable map : Color palettes, value labels, sample size, and an optional legend for fast interpretation.

Scoreboard : Optional table highlights best/worst DOW and today’s seasonality with CI and a simple “edge” tag.

How it’s calculated (under the hood)

Per bar, compute the chosen metric (return, vol, volume %, or range %) over your lookback window.

Bucket that metric into the active calendar bin (e.g., Tuesday, the 15th, 10:00 hour, or Week-2 of month).

For each bin, accumulate sum , sum of squares , and count , then at render compute mean , std dev , and confidence interval .

Color scale normalizes to the observed min/max of eligible bins (those meeting the minimum sample size).

How to read the heatmap

Color : Greener/warmer typically implies higher mean value for the chosen metric; cooler implies lower.

Value label : The center number is the bin’s mean (e.g., average % return for Tuesdays).

Confidence bracket : Optional “ ” shows the CI for the mean, helping you gauge stability.

n = sample size : More samples = more reliability. Treat small-n bins with skepticism.

Suggested workflows

Pick the lens : Start with Analysis Type = Returns , Heatmap View = Day of Week , lookback ≈ 252 trading days . Note the best/worst weekdays and their CI width.

Sanity-check volatility : Switch to Volatility to see which bins carry the most realized range. Use that to plan stop width and trade pacing.

Check liquidity proxy : Flip to Volume , identify thin vs thick windows. Execute risk in thicker windows to reduce slippage.

Drill to intraday : Use Hour of Day to reveal opening bursts, lunchtime lulls, and closing ramps. Combine with your main strategy to schedule entries.

Calendar nuance : Inspect Week of Month and Day of Month for end-of-month, options-cycle, or data-release effects.

Codify rules : Translate stable edges into rules like “no fresh risk during bottom-quartile hours” or “scale entries during top-quartile hours.”

Parameter guidance

Analysis Period (Days) : 252 for a one-year view. Shorten (100–150) to emphasize the current regime; lengthen (500+) for long-memory effects.

Heatmap View : Start with DOW for robustness, then refine with Hour-of-Day for your execution window.

Confidence Level : 95% is standard; use 90% if you want wider coverage with fewer false “insufficient data” bins.

Min Sample Size : 10–20 helps filter noise. For Hour-of-Day on higher timeframes, consider lowering if your dataset is small.

Color Scheme : Choose a palette with good mid-tone contrast (e.g., Red-Green or Viridis) for quick thresholding.

Interpreting common patterns

Return-positive but low-vol bins : Favorable drift windows for passive adds or tight-stop trend continuation.

Return-flat but high-vol bins : Opportunity for mean reversion or breakout scalping, but manage risk accordingly.

High-volume bins : Better expected execution quality; schedule size here if slippage matters.

Wide CI : Edge is unstable or sample is thin; treat as exploratory until more data accumulates.

Best practices

Revalidate after regime shifts (new macro cycle, liquidity regime change, major exchange microstructure updates).

Use multiple lenses: DOW to find the day, then Hour-of-Day to refine the entry window.

Combine with your core setup signals; treat seasonality as a filter or weight, not a standalone trigger.

Test across assets/timeframes—edges are instrument-specific and may not transfer 1:1.

Limitations & notes

History-dependent: short histories or sparse intraday data reduce reliability.

Not causal: a hot Tuesday doesn’t guarantee future Tuesday strength; treat as probabilistic bias.

Aggregation bias: changing session hours or symbol migrations can distort older samples.

CI is z-approximate: good for fast triage, not a substitute for full hypothesis testing.

Quick setup

Use Returns + Day of Week + 252d to get a clean yearly map of weekday edge.

Flip to Hour of Day on intraday charts to schedule precise entries/exits.

Keep Show Values and Confidence Intervals on while you calibrate; hide later for a clean visual.

The Multi-Mode Seasonality Map helps you convert the calendar from an afterthought into a quantitative edge, surfacing when an asset tends to move, expand, or stay quiet—so you can plan, size, and execute with intent.