Line Regression Intercept Strategy Linear Regression Intercept is one of the indicators calculated by using the

Linear Regression technique. Linear regression indicates the value of the Y

(generally the price) when the value of X (the time series) is 0. Linear

Regression Intercept is used along with the Linear Regression Slope to create

the Linear Regression Line. The Linear Regression Intercept along with the Slope

creates the Regression line.

WARNING:

- This script to change bars colors.

Strategy

Chande Forecast Oscillator Backtest The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Chande Forecast Oscillator Strategy The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.

WARNING:

- This script to change bars colors.

Center Of Gravity Backtest The indicator is based on moving averages. On the basis of these, the

"center" of the price is calculated, and price channels are also constructed,

which act as corridors for the asset quotations.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

ETH/BTC MMAs Daytrade strategy 15min UT 0.05% feesPlayed around with Moving Averages, with the goal to bounce on trendlines and trend reversals.

Time Unit : 15 min

Candle Type : Heikin Ashi

Commission : 0.05% on trades (Binance fees)

Initial capital : 1k €

Do you think this could work?

Center Of Gravity Strategy The indicator is based on moving averages. On the basis of these, the

"center" of the price is calculated, and price channels are also constructed,

which act as corridors for the asset quotations.

My Ichimoku indicator & Strategyhello I'm a beginner in trading, but I try to learn how to code strategies.

I recoded the Ichimoku indicator, and created my personnal strategy based on it.

The backtesting is done from 1/1/2017 to today in 45 min Time Unit for candles, with a 1 000 € equity.

The trades are all Long Entries and Exits with no pyramiding, no short trades at all.

/!\ Exchanges commission fees are not calculated and can in reality easily divide by 2 the total profit (am I right guys?) /!\

A buy signal is triggered upon these conditions:

- close is above the Kuma (cloud)

AND

- close crosses over Kijunsen AND Kijunsen is not flat (calculated with rising and falling with input "Kijunsen Lag")

OR

- Close crosses over ChikouSpan AND there was a sell signal in the last 8 candles

Sell signal is the same but reversed.

I appreciate your feedback ! Maybe I will update this later if I get better results.

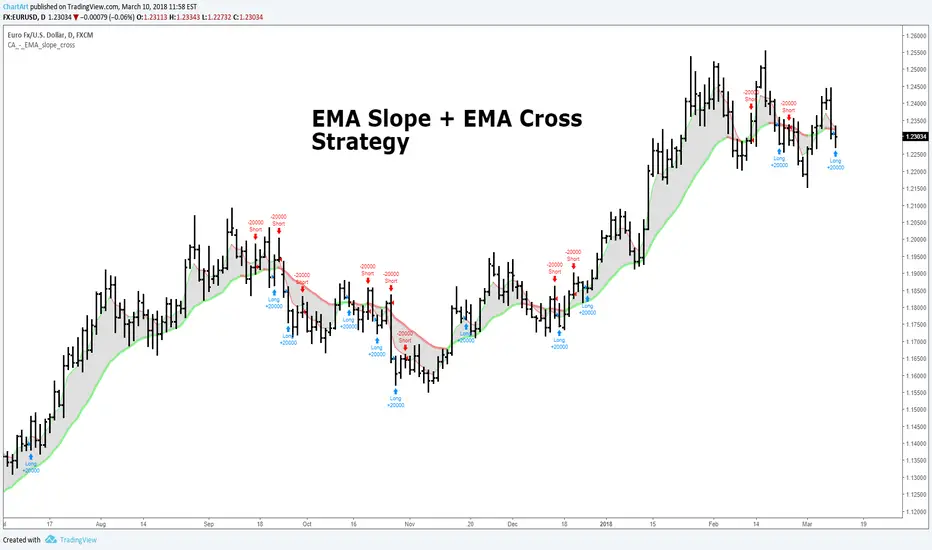

EMA Slope + EMA Cross Strategy (by ChartArt)This strategy uses divergences between three exponential moving averages and their slope directions as well as crosses between the price and these moving averages to switch between a long or short position. The strategy is non-stop in the market and always either long or short.

In addition the moving averages and price bars are colored depending if they are trending up or down.

The strategy was created for the "EURUSD" daily timeframe.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

XPloRR MA-Trailing-Stop StrategyXPloRR MA-Trailing-Stop Strategy

Long term MA-Trailing-Stop strategy with Adjustable Signal Strength to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the fast buy EMA (blue) crossing over the slow buy SMA curve (orange) and the fast buy EMA has a certain up strength.

My sell strategy is triggered by either one of these conditions:

the EMA(6) of the close value is crossing under the trailing stop value (green) or

the fast sell EMA (navy) is crossing under the slow sell SMA curve (red) and the fast sell EMA has a certain down strength.

The trailing stop value (green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between the high and low values.

The scripts shows a lot of graphical information:

The close value is shown in light-green. When the close value is lower then the buy value, the close value is shown in light-red. This way it is possible to evaluate the virtual losses during the trade.

the trailing stop value is shown in dark-green. When the sell value is lower then the buy value, the last color of the trade will be red (best viewed when zoomed)(in the example, there are 2 trades that end in gain and 2 in loss (red line at end))

the EMA and SMA values for both buy and sell signals are shown as a line

the buy and sell(close) signals are labeled in blue

How to use this strategy?

Every stock has it's own "DNA", so first thing to do is tune the right parameters to get the best strategy values voor EMA , SMA, Strength for both buy and sell and the Trailing Stop (#ATR).

Look in the strategy tester overview to optimize the values Percent Profitable and Net Profit (using the strategy settings icon, you can increase/decrease the parameters)

Then keep using these parameters for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Important : optimizing these parameters is no guarantee for future winning trades!

Here are the parameters:

Fast EMA Buy: buy trigger when Fast EMA Buy crosses over the Slow SMA Buy value (use values between 10-20)

Slow SMA Buy: buy trigger when Fast EMA Buy crosses over the Slow SMA Buy value (use values between 30-100)

Minimum Buy Strength: minimum upward trend value of the Fast SMA Buy value (directional coefficient)(use values between 0-120)

Fast EMA Sell: sell trigger when Fast EMA Sell crosses under the Slow SMA Sell value (use values between 10-20)

Slow SMA Sell: sell trigger when Fast EMA Sell crosses under the Slow SMA Sell value (use values between 30-100)

Minimum Sell Strength: minimum downward trend value of the Fast SMA Sell value (directional coefficient)(use values between 0-120)

Trailing Stop (#ATR): the trailing stop value as a multiple of the ATR(15) value (use values between 2-20)

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now) compared to the Buy&Hold Strategy(=do nothing):

BEKB(Bekaert): EMA-Buy=12, SMA-Buy=44, Strength-Buy=65, EMA-Sell=12, SMA-Sell=55, Strength-Sell=120, Stop#ATR=20

NetProfit: 996%, #Trades: 6, %Profitable: 83%, Buy&HoldProfit: 78%

BAR(Barco): EMA-Buy=16, SMA-Buy=80, Strength-Buy=44, EMA-Sell=12, SMA-Sell=45, Strength-Sell=82, Stop#ATR=9

NetProfit: 385%, #Trades: 7, %Profitable: 71%, Buy&HoldProfit: 55%

AAPL(Apple): EMA-Buy=12, SMA-Buy=45, Strength-Buy=40, EMA-Sell=19, SMA-Sell=45, Strength-Sell=106, Stop#ATR=8

NetProfit: 6900%, #Trades: 7, %Profitable: 71%, Buy&HoldProfit: 2938%

TNET(Telenet): EMA-Buy=12, SMA-Buy=45, Strength-Buy=27, EMA-Sell=19, SMA-Sell=45, Strength-Sell=70, Stop#ATR=14

NetProfit: 129%, #Trade

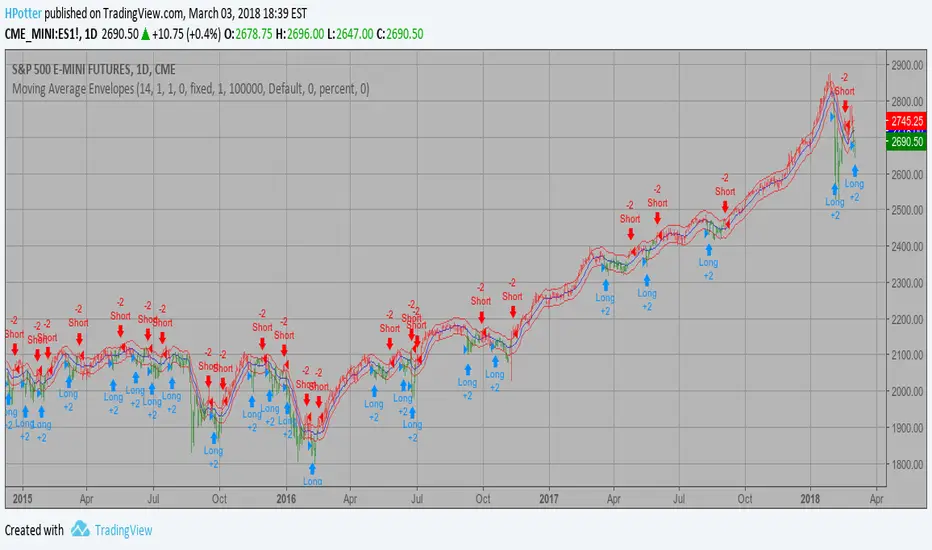

Moving Average Envelopes Backtest Moving Average Envelopes are percentage-based envelopes set above and

below a moving average. The moving average, which forms the base for

this indicator, can be a simple or exponential moving average. Each

envelope is then set the same percentage above or below the moving average.

This creates parallel bands that follow price action. With a moving average

as the base, Moving Average Envelopes can be used as a trend following indicator.

However, this indicator is not limited to just trend following. The envelopes

can also be used to identify overbought and oversold levels when the trend is

relatively flat.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Moving Average Envelopes Moving Average Envelopes are percentage-based envelopes set above and

below a moving average. The moving average, which forms the base for

this indicator, can be a simple or exponential moving average. Each

envelope is then set the same percentage above or below the moving average.

This creates parallel bands that follow price action. With a moving average

as the base, Moving Average Envelopes can be used as a trend following indicator.

However, this indicator is not limited to just trend following. The envelopes

can also be used to identify overbought and oversold levels when the trend is

relatively flat.

WARNING:

- This script to change bars colors.

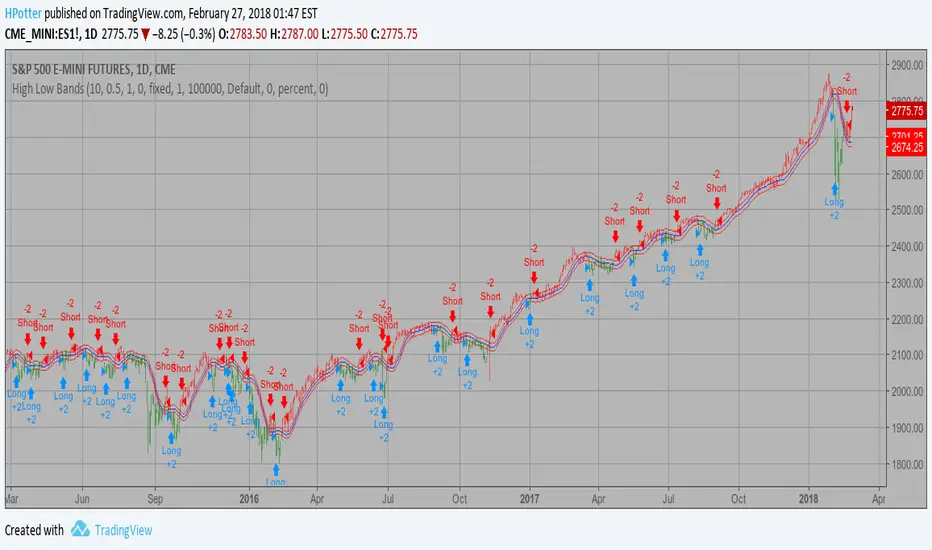

High Low Bands Backtest As the name suggests, High low bands are two bands surrounding the underlying’s

price. These bands are generated from the triangular moving averages calculated

from the underlying’s price. The triangular moving average is, in turn, shifted

up and down by a fixed percentage. The bands, thus formed, are termed as High

low bands. The main theme and concept of High low bands is based upon the triangular

moving average.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

High Low Bands Strategy As the name suggests, High low bands are two bands surrounding the underlying’s

price. These bands are generated from the triangular moving averages calculated

from the underlying’s price. The triangular moving average is, in turn, shifted

up and down by a fixed percentage. The bands, thus formed, are termed as High

low bands. The main theme and concept of High low bands is based upon the triangular

moving average.

WARNING:

- This script to change bars colors.

Rainbow StrategyThe strategy is based on the following idea:

www.youtube.com

Not a fan of this but no script was present to show this idea's performance.

Best suitable for the 1-minute chart. You can change the ema values as per your needs.

For Tips to continue :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Fractal Chaos Oscillator Backtest The value of Fractal Chaos Oscillator is calculated as the difference between

the most subtle movements of the market. In general, its value moves between

-1.000 and 1.000. The higher the value of the Fractal Chaos Oscillator, the

more one can say that it follows a certain trend – an increase in prices trend,

or a decrease in prices trend.

Being an indicator expressed in a numeric value, traders say that this is an

indicator that puts a value on the trendiness of the markets. When the FCO reaches

a high value, they initiate the “buy” operation, contrarily when the FCO reaches a

low value, they signal the “sell” action. This is an excellent indicator to use in

intra-day trading.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Fractal Chaos Oscillator Strategy The value of Fractal Chaos Oscillator is calculated as the difference between

the most subtle movements of the market. In general, its value moves between

-1.000 and 1.000. The higher the value of the Fractal Chaos Oscillator, the

more one can say that it follows a certain trend – an increase in prices trend,

or a decrease in prices trend.

Being an indicator expressed in a numeric value, traders say that this is an

indicator that puts a value on the trendiness of the markets. When the FCO reaches

a high value, they initiate the “buy” operation, contrarily when the FCO reaches a

low value, they signal the “sell” action. This is an excellent indicator to use in

intra-day trading.

WARNING:

- This script to change bars colors.

Fractal Chaos Bands Backtest The FCB indicator looks back in time depending on the number of time periods trader selected

to plot the indicator. The upper fractal line is made by plotting stock price highs and the

lower fractal line is made by plotting stock price lows. Essentially, the Fractal Chaos Bands

show an overall panorama of the price movement, as they filter out the insignificant fluctuations

of the stock price.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Vdub FX SniperVX3 / Strategy Alerts BetaThis is nothing other than a simple alert script I created for Vdub FX Sniper VX3 / Strategy by Vdubus

Thank you to WillowGoLightly for coming to me with the idea.

Change Log:

Removed plots & layover

Added a simple alert indicator to match original

Be sure to give Vdubus a big thanks!

Original Sniper Script by Vdubus:

Disclaimer: I have never used this indicator or alert script. There may be several unknown bugs. If found, please feel free to comment below and I will attempt to fix them. Use at your own risk.

Fractal Chaos Bands Strategy Stock market moves in a highly chaotic way, but at a larger scale, the movements

follow a certain pattern that can be applied to shorter or longer periods of time

and we can use Fractal Chaos Bands Indicator to identify those patterns. Basically,

the Fractal Chaos Bands Indicator helps us to identify whether the stock market is

trending or not. When a market is trending, the bands will have a slope and if market

is not trending the bands will flatten out. As the slope of the bands decreases, it

signifies that the market is choppy, insecure and variable. As the graph becomes more

and more abrupt, be it going up or down, the significance is that the market becomes

trendy, or stable. Fractal Chaos Bands Indicator is used similarly to other bands-indicator

(Bollinger bands for instance), offering trading opportunities when price moves above or

under the fractal lines.

The FCB indicator looks back in time depending on the number of time periods trader selected

to plot the indicator. The upper fractal line is made by plotting stock price highs and the

lower fractal line is made by plotting stock price lows. Essentially, the Fractal Chaos Bands

show an overall panorama of the price movement, as they filter out the insignificant fluctuations

of the stock price.

WARNING:

- This script to change bars colors.

Ichimoku Kumo Twist Strategy with Presets [Krypt]A simple strategy for testing Ichimoku settings used in the following indicator:

Philakone 55 EMA Swing Trading StrategyThis strategy was inspired by Philkone Crypto's "Lesson 12: Let's Learn Advanced 55 EMA Strategy" video.

steemit.com

Supports Buy and Sell Condition alerts and displays arrows on the chart.