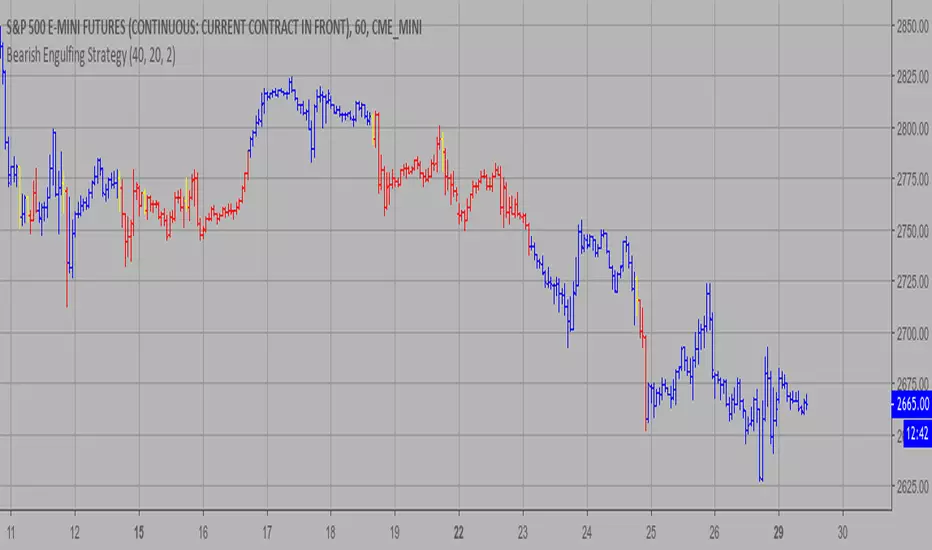

Bearish Engulfing Strategy This is a bearish candlestick reversal pattern formed by two candlesticks.

Following an uptrend, the first candlestick is a up candlestick which is

followed by a down candlestick which has a long real body that engulfs or

contains the real body of the prior bar. The Engulfing pattern is the reverse

of the Harami pattern.

WARNING:

- This script to change bars colors.

Strategy!

Doji strategyThis is a simple strategy based on Doji star candlestick.

It places two orders: buy stop at doji star high or previous candle high and sell stop at doji star low or previous candle low.

Exit rules are with take profit and fixed stop loss or take profit and stop loss at doji min or max.

This strategy works very well with high time frames like Daily and Weekly because those are without noise in doji formation.

Each currency pair has its own optimal setting for TP and SL: it's up to user find the best ones.

I could implement SL based on ATR, maybe in next revision.

Please use comment section for any feedback.

Next improvement (only to whom is interested to this script and follows me): study with alerts on multiple tickers all at one. Leave a comment if you want to have access to study.

(H-L)/C Histogram Strategy This histogram displays (high-low)/close

Can be applied to any time frame.

WARNING:

- This script to change bars colors.

CMO & WMA Strategy ver 2.0 This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

Trend Trader Bands Strategy This is plots the indicator developed by Andrew Abraham

in the Trading the Trend article of TASC September 1998

It was modified, result values wass averages.

And draw two bands above and below TT line.

Trend Trader AVR Strategy This is plots the indicator developed by Andrew Abraham

in the Trading the Trend article of TASC September 1998

It was modified, result values wass averages.

SimpleMA smoothed crossover strategyExperimental simple Bot script for ETH/USD 1 hour chart. welcome to test on other pairs. put feedback in comments.

This is a crossbreed between SMA and HULLMA

[Strategy] CCI EMA scalping [DEV]Recommended timeframe: 5M or higher

Based on EMA crosses and CCI levels.

Take profit can be also at Pivot levels like Daily/Weekly

Stop loss should be between 12-15 pips.

This strategy is still under development!

Real Price for Heikin Ashi ChartsThe indicator is in the top left of the screen! That's all there is, by design.

This is a super simple indicator that allows you to see what the real price of a candle was when using Heikin Ashi charts, while not cluttering up your screen.

HA charts are a great way to help those who can be spooked by the chaos of the markets (I'm one!), but they have a big drawback in that the price you see on a HA candle is often significantly different from the real price that you would trade on. This brings issues of unrealistic expectations of profits/losses, and also makes back testing a strategy very difficult. I still wouldn't recommend ever using TradingView's "strategy" tool when using HA charts, but using this indicator you can do accurate manual back tests.

There's nothing plotted on the screen given that there's no real point in it, but you can make the lines appear if you wish - just go into settings and change the transparency.

The order of the numbers on the indicator match the OHLC (Open, High, Low, Close) format.

There's also settings to turn off one or more of the OHLC values, simply open the settings and go to Inputs. This could be useful for some people, as the High and Low values of HA candles are the same as regular candles. Only the Open and Close are different.

Any queries let me know.

DreamsDefined

Complete Trend Trading System [Fhenry0331]This system was designed for the beginner trader to make money swing trading. Your losses will be small and your gains will be mostly large. You will show consistent profit. Period.

The system works on any security you like to trade. I used GBPUSD as an example because of the up swing and down swing it had recently. I tried to put as much information of how the system works in the chart. Hope it helps and is not to cluttered.

I will reiterate how the system works here: Everything is based off of closed price.

Legend

Uptrend: Buy

Green bar: initial start of an uptrend or uptrend continuing. Place order above that bar. If the initial bar does not stray too far from the MVWAP , I will place orders above subsequent bars if no filled occurred.

If initial start of the trend is missed, I will wait for the pullback. A pullback is a close below the MVWAP, and a close above the EMA (Low), RSI is above 50. Orders are placed above the pullback bars with plotted char "B" and also plotted green triangle up. Again orders are placed above those bars. the bars do not notate automatic buys. Don't chase anything. You will miss the initial bar on something because of news or earnings and it rocket up. Just wait, it will pullback. If it doesn't, to hell with it, on to the next.

Take profits: In the indicator you will see "T." That notates to take some profits. It is a suggestion. I was always told to take profits into spikes, as well as you can never lose money if you take profits. Up to you if you want to scale out and take the suggested profits or not.

Exit Completely: In an uptrend, close your entire position on bars colored yellow or red. (Again, closed bars)

In uptrend bars colored orange and black, do nothing, they are just pullback bars. Look for the buy pullback signal, then follow pullback buy rules for an uptrend.

Downtrend: Short

Red bar: initial start of a downtrend or downtrend continuing. Place order below the bar. If the initial bar does not stray too far fro the MVWAP, place orders below subsequent bars.

If initial start on the downtrend is missed, wait for the pullback. A pullback is a close above the MVWAP, and close below the EMA(Low). RSI is below 50. Orders are placed below the pullback bars with the plotted char "S" and also plotted red triangle. Again those bars are not automatic shorts, orders are placed below them. Don't chase anything. Wait for price to come into your plan. The idea FOMO is the stupidest thing ever, how can you miss out on something when it is always there. The market is always there and something will come into your zone. Chill.

"T": same as in uptrend, suggestion to take some profits.

Exit Completely: In a downtrend, close your entire position on bars colored orange or green.

In downtrend you will see bars colored yellow and black, do nothing, they are pullback bars. Look for the pullback short signal and follow pullback short rules.

If you have any questions get at me. Take a look at it on what you trade. Flip it through different securities.

Best of luck in all you do.

P.S. You should not take a trade right before earnings. You should also exit a trade right before earnings.

VB Strategy

VB Indicator

VB Indicator PRO (with Alarm function)

With this strategy, you can test VB indicator.

This strategy use entry and close price

entry price = (high price + low price) / 2

close price = (high price + low price) / 2

이 전략으로 VB 지표에 대해 테스트할 수 있습니다.

이 전략의 진입가와 청산가는 아래와 같이 설정합니다.

진입가 = (고점+저점) / 2

청산가 = (고점+저점) / 2

ATR Trailing Stop Bands Strategy [R] Originally based on a script by HPotter for an ATR Trailing Stop, which itself was based on an article by Sylvain Vervoort, but I adapted it to add Bands, to add extra optional Wick Protection, and have now made it a Strategy. It's not great for entries/exits, but as a Trailing Stop that can let winners ride, it's great.

Ema cross strat / Turtle Trading This is just a simple EMA cross strategy which is meant to be similar to Turtle Trading Strategy.

It uses in default 4 Hour 21 / 10 EMA to long or short. This is not perfect but in the long run it will profit. Works best in bull market.

LINK TO ALERT :

Ergotic MACD Strategy [forked from HPotter]Ergotic MACD Strategy forked from HPotter

In addition to this fine script you will find some additional features:

- Backtester

- Alerts

- Filters: RSI, MFI, Price trend

- Trailing Stop Loss

- Other minor adjustments

Trend Reversal Alerts Strategy [4H/3M]This is advanced version of T-R.A.S with better logic adapted for 4hour / 3month timeframes

Trend Reversal Alerts Strategy [Advanced]This is a hourly version of T-R.A.S

It's better for houry timeframes : 2h, 3h, 4h, 6h, 12h, 1d, 4d ; otherwise use version for weekly

Strong Potential Asset Strategy (EMA + EMA)During experiments with the market, I found out that simple strategy is the best solution. However, I decided to bring some of my ideas on the 2 MA strategy.

- Instead of SMA - there will be 2 EMA, so the strategy will be more sensitive to the latest data;

- There is an option, which regulates the difference between those 2 EMAs, this should protect us from false trend enter;

- There is an option "Exit tolerance", which regulates how much could be the difference between 2 EMAs after crossover. This supposed to protect us from the false trend exit.

Hope this will be helpful :)

Absolute Price Oscillator (APO) Strategy 2.0 The Absolute Price Oscillator displays the difference between two exponential

moving averages of a security's price and is expressed as an absolute value.

How this indicator works

APO crossing above zero is considered bullish, while crossing below zero is bearish.

A positive indicator value indicates an upward movement, while negative readings

signal a downward trend.

Divergences form when a new high or low in price is not confirmed by the Absolute Price

Oscillator (APO). A bullish divergence forms when price make a lower low, but the APO

forms a higher low. This indicates less downward momentum that could foreshadow a bullish

reversal. A bearish divergence forms when price makes a higher high, but the APO forms a

lower high. This shows less upward momentum that could foreshadow a bearish reversal.

WARNING:

- This script to change bars colors.

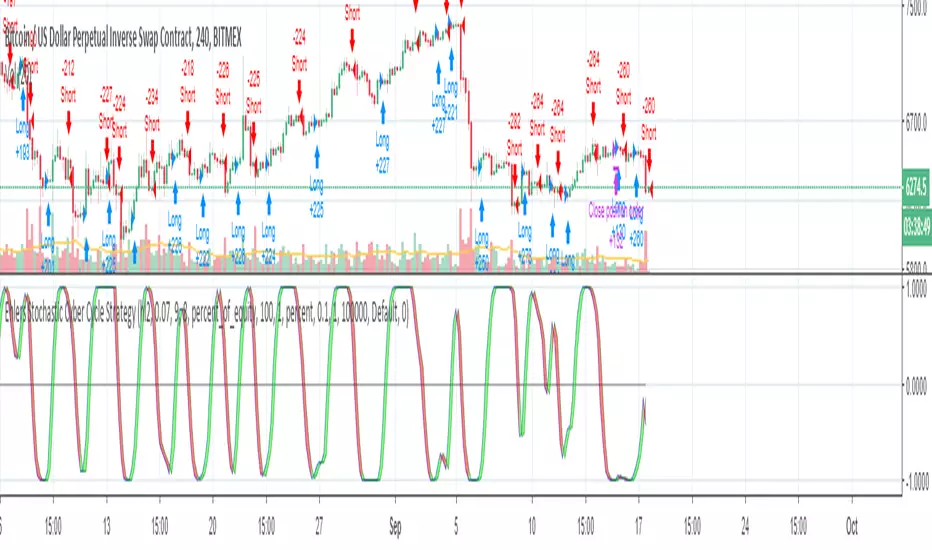

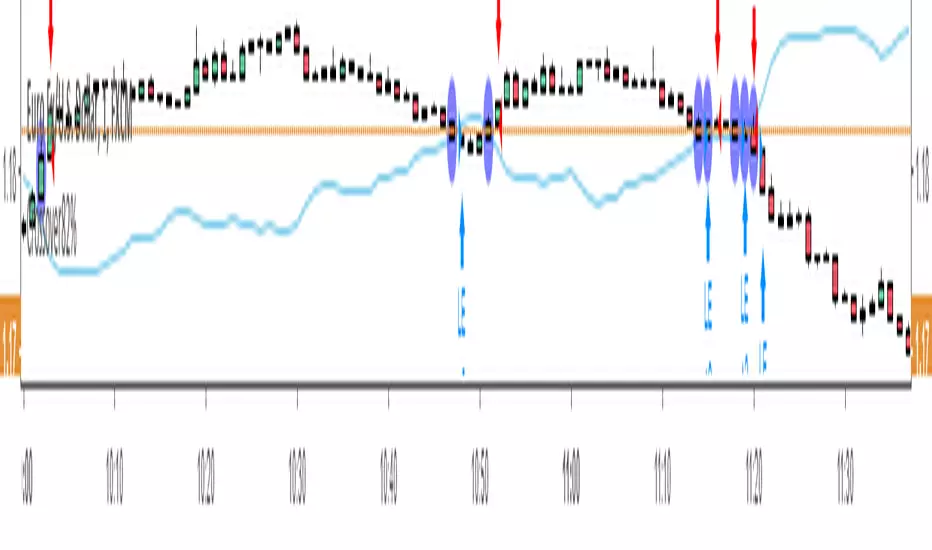

Ehlers Fisher Stochastic Relative Vigor Index StrategyBy John Ehlers from his book "Cybernetic Analysis for Stocks and Futures".

Ehlers Stochastic Cyber Cycle StrategyBy John Ehlers from his book "Cybernetic Analysis for Stocks and Futures".