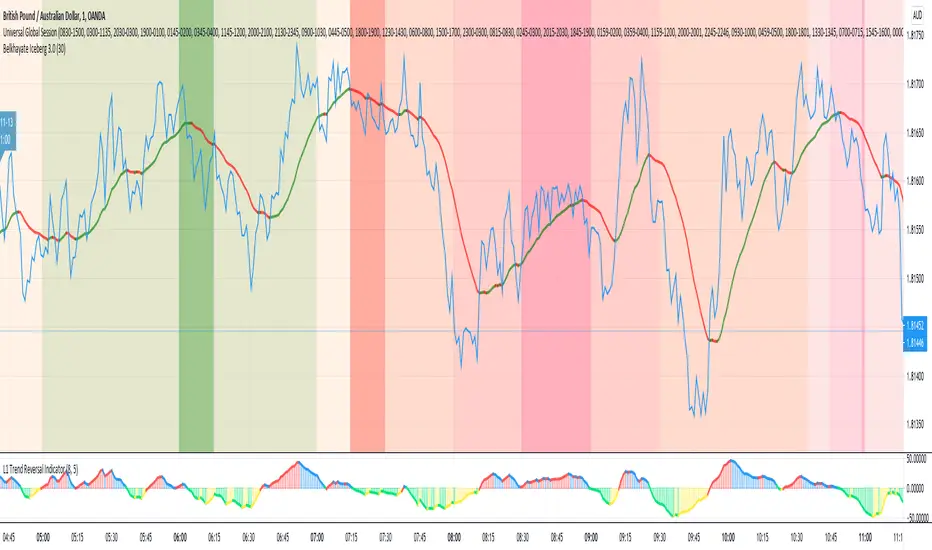

Universal Global SessionUniversal Global Session

This Script combines the world sessions of: Stocks, Forex, Bitcoin Kill Zones, strategic points, all configurable, in a single Script, to capitalize the opening and closing times of global exchanges as investment assets, becoming an Universal Global Session .

It is based on the great work of @oscarvs ( BITCOIN KILL ZONES v2 ) and the scripts of @ChrisMoody. Thank you Oscar and Chris for your excellent judgment and great work.

At the end of this writing you can find all the internet references of the extensive documentation that I present here. To maximize your benefits in the use of this Script, I recommend that you read the entire document to create an objective and practical criterion.

All the hours of the different exchanges are presented at GMT -6. In Market24hClock you can adjust it to your preferences.

After a deep investigation I have been able to show that the different world sessions reveal underlying investment cycles, where it is possible to find sustained changes in the nominal behavior of the trend before the passage from one session to another and in the natural overlaps between the sessions. These underlying movements generally occur 15 minutes before the start, close or overlap of the session, when the session properly starts and also 15 minutes after respectively. Therefore, this script is designed to highlight these particular trending behaviors. Try it, discover your own conclusions and let me know in the notes, thank you.

Foreign Exchange Market Hours

It is the schedule by which currency market participants can buy, sell, trade and speculate on currencies all over the world. It is open 24 hours a day during working days and closes on weekends, thanks to the fact that operations are carried out through a network of information systems, instead of physical exchanges that close at a certain time. It opens Monday morning at 8 am local time in Sydney —Australia— (which is equivalent to Sunday night at 7 pm, in New York City —United States—, according to Eastern Standard Time), and It closes at 5pm local time in New York City (which is equivalent to 6am Saturday morning in Sydney).

The Forex market is decentralized and driven by local sessions, where the hours of Forex trading are based on the opening range of each active country, becoming an efficient transfer mechanism for all participants. Four territories in particular stand out: Sydney, Tokyo, London and New York, where the highest volume of operations occurs when the sessions in London and New York overlap. Furthermore, Europe is complemented by major financial centers such as Paris, Frankfurt and Zurich. Each day of forex trading begins with the opening of Australia, then Asia, followed by Europe, and finally North America. As markets in one region close, another opens - or has already opened - and continues to trade in the currency market. The seven most traded currencies in the world are: the US dollar, the euro, the Japanese yen, the British pound, the Australian dollar, the Canadian dollar, and the New Zealand dollar.

Currencies are needed around the world for international trade, this means that operations are not dominated by a single exchange market, but rather involve a global network of brokers from around the world, such as banks, commercial companies, central banks, companies investment management, hedge funds, as well as retail forex brokers and global investors. Because this market operates in multiple time zones, it can be accessed at any time except during the weekend, therefore, there is continuously at least one open market and there are some hours of overlap between the closing of the market of one region and the opening of another. The international scope of currency trading means that there are always traders around the world making and satisfying demands for a particular currency.

The market involves a global network of exchanges and brokers from around the world, although time zones overlap, the generally accepted time zone for each region is as follows:

Sydney 5pm to 2am EST (10pm to 7am UTC)

London 3am to 12 noon EST (8pm to 5pm UTC)

New York 8am to 5pm EST (1pm to 10pm UTC)

Tokyo 7pm to 4am EST (12am to 9am UTC)

Trading Session

A financial asset trading session refers to a period of time that coincides with the daytime trading hours for a given location, it is a business day in the local financial market. This may vary according to the asset class and the country, therefore operators must know the hours of trading sessions for the securities and derivatives in which they are interested in trading. If investors can understand market hours and set proper targets, they will have a much greater chance of making a profit within a workable schedule.

Kill Zones

Kill zones are highly liquid events. Many different market participants often come together and perform around these events. The activity itself can be event-driven (margin calls or option exercise-related activity), portfolio management-driven (asset allocation rebalancing orders and closing buy-in), or institutionally driven (larger players needing liquidity to complete the size) or a combination of any of the three. This intense cross-current of activity at a very specific point in time often occurs near significant technical levels and the established trends emerging from these events often persist until the next Death Zone approaches or enters.

Kill Zones are evolving with time and the course of world history. Since the end of World War II, New York has slowly invaded London's place as the world center for commercial banking. So much so that during the latter part of the 20th century, New York was considered the new center of the financial universe. With the end of the cold war, that leadership appears to have shifted towards Europe and away from the United States. Furthermore, Japan has slowly lost its former dominance in the global economic landscape, while Beijing's has increased dramatically. Only time will tell how these death zones will evolve given the ever-changing political, economic, and socioeconomic influences of each region.

Financial Markets

New York

New York (NYSE Chicago, NASDAQ)

7:30 am - 2:00 pm

It is the second largest currency platform in the world, followed largely by foreign investors as it participates in 90% of all operations, where movements on the New York Stock Exchange (NYSE) can have an immediate effect (powerful) on the dollar, for example, when companies merge and acquisitions are finalized, the dollar can instantly gain or lose value.

A. Complementary Stock Exchanges

Brazil (BOVESPA - Brazilian Stock Exchange)

07:00 am - 02:55 pm

Canada (TSX - Toronto Stock Exchange)

07:30 am - 02:00 pm

New York (NYSE - New York Stock Exchange)

08:30 am - 03:00 pm

B. North American Trading Session

07:00 am - 03:00 pm

(from the beginning of the business day on NYSE and NASDAQ, until the end of the New York session)

New York, Chicago and Toronto (Canada) open the North American session. Characterized by the most aggressive trading within the markets, currency pairs show high volatility. As the US markets open, trading is still active in Europe, however trading volume generally decreases with the end of the European session and the overlap between the US and Europe.

C. Strategic Points

US main session starts in 1 hour

07:30 am

The euro tends to drop before the US session. The NYSE, CHX and TSX (Canada) trading sessions begin 1 hour after this strategic point. The North American session begins trading Forex at 07:00 am.

This constitutes the beginning of the overlap of the United States and the European market that spans from 07:00 am to 10:35 am, often called the best time to trade EUR / USD, it is the period of greatest liquidity for the main European currencies since it is where they have their widest daily ranges.

When New York opens at 07:00 am the most intense trading begins in both the US and European markets. The overlap of European and American trading sessions has 80% of the total average trading range for all currency pairs during US business hours and 70% of the total average trading range for all currency pairs during European business hours. The intersection of the US and European sessions are the most volatile overlapping hours of all.

Influential news and data for the USD are released between 07:30 am and 09:00 am and play the biggest role in the North American Session. These are the strategically most important moments of this activity period: 07:00 am, 08:00 am and 08:30 am.

The main session of operations in the United States and Canada begins

08:30 am

Start of main trading sessions in New York, Chicago and Toronto. The European session still overlaps the North American session and this is the time for large-scale unpredictable trading. The United States leads the market. It is difficult to interpret the news due to speculation. Trends develop very quickly and it is difficult to identify them, however trends (especially for the euro), which have developed during the overlap, often turn the other way when Europe exits the market.

Second hour of the US session and last hour of the European session

09:30 am

End of the European session

10:35 am

The trend of the euro will change rapidly after the end of the European session.

Last hour of the United States session

02:00 pm

Institutional clients and very large funds are very active during the first and last working hours of almost all stock exchanges, knowing this allows to better predict price movements in the opening and closing of large markets. Within the last trading hours of the secondary market session, a pullback can often be seen in the EUR / USD that continues until the opening of the Tokyo session. Generally it happens if there was an upward price movement before 04:00 pm - 05:00 pm.

End of the trade session in the United States

03:00 pm

D. Kill Zones

11:30 am - 1:30 pm

New York Kill Zone. The United States is still the world's largest economy, so by default, the New York opening carries a lot of weight and often comes with a huge injection of liquidity. In fact, most of the world's marketable assets are priced in US dollars, making political and economic activity within this region even more important. Because it is relatively late in the world's trading day, this Death Zone often sees violent price swings within its first hour, leading to the proven adage "never trust the first hour of trading in America. North.

---------------

London

London (LSE - London Stock Exchange)

02:00 am - 10:35 am

Britain dominates the currency markets around the world, and London is its main component. London, a central trading capital of the world, accounts for about 43% of world trade, many Forex trends often originate from London.

A. Complementary Stock Exchange

Dubai (DFM - Dubai Financial Market)

12:00 am - 03:50 am

Moscow (MOEX - Moscow Exchange)

12:30 am - 10:00 am

Germany (FWB - Frankfurt Stock Exchange)

01:00 am - 10:30 am

Afríca (JSE - Johannesburg Stock Exchange)

01:00 am - 09:00 am

Saudi Arabia (TADAWUL - Saudi Stock Exchange)

01:00 am - 06:00 am

Switzerland (SIX - Swiss Stock Exchange)

02:00 am - 10:30 am

B. European Trading Session

02:00 am - 11:00 am

(from the opening of the Frankfurt session to the close of the Order Book on the London Stock Exchange / Euronext)

It is a very liquid trading session, where trends are set that start during the first trading hours in Europe and generally continue until the beginning of the US session.

C. Middle East Trading Session

12:00 am - 06:00 am

(from the opening of the Dubai session to the end of the Riyadh session)

D. Strategic Points

European session begins

02:00 am

London, Frankfurt and Zurich Stock Exchange enter the market, overlap between Europe and Asia begins.

End of the Singapore and Asia sessions

03:00 am

The euro rises almost immediately or an hour after Singapore exits the market.

Middle East Oil Markets Completion Process

05:00 am

Operations are ending in the European-Asian market, at which time Dubai, Qatar and in another hour in Riyadh, which constitute the Middle East oil markets, are closing. Because oil trading is done in US dollars, and the region with the trading day coming to an end no longer needs the dollar, consequently, the euro tends to grow more frequently.

End of the Middle East trading session

06:00 am

E. Kill Zones

5:00 am - 7:00 am

London Kill Zone. Considered the center of the financial universe for more than 500 years, Europe still has a lot of influence in the banking world. Many older players use the European session to establish their positions. As such, the London Open often sees the most significant trend-setting activity on any trading day. In fact, it has been suggested that 80% of all weekly trends are set through the London Kill Zone on Tuesday.

F. Kill Zones (close)

2:00 pm - 4:00 pm

London Kill Zone (close).

---------------

Tokyo

Tokyo (JPX - Tokyo Stock Exchange)

06:00 pm - 12:00 am

It is the first Asian market to open, receiving most of the Asian trade, just ahead of Hong Kong and Singapore.

A. Complementary Stock Exchange

Singapore (SGX - Singapore Exchange)

07:00 pm - 03:00 am

Hong Kong (HKEx - Hong Kong Stock Exchange)

07:30 pm - 02:00 am

Shanghai (SSE - Shanghai Stock Exchange)

07:30 pm - 01:00 am

India (NSE - India National Stock Exchange)

09:45 pm - 04:00 am

B. Asian Trading Session

06:00 pm - 03:00 am

From the opening of the Tokyo session to the end of the Singapore session

The first major Asian market to open is Tokyo which has the largest market share and is the third largest Forex trading center in the world. Singapore opens in an hour, and then the Chinese markets: Shanghai and Hong Kong open 30 minutes later. With them, the trading volume increases and begins a large-scale operation in the Asia-Pacific region, offering more liquidity for the Asian-Pacific currencies and their crosses. When European countries open their doors, more liquidity will be offered to Asian and European crossings.

C. Strategic Points

Second hour of the Tokyo session

07:00 pm

This session also opens the Singapore market. The commercial dynamics grows in anticipation of the opening of the two largest Chinese markets in 30 minutes: Shanghai and Hong Kong, within these 30 minutes or just before the China session begins, the euro usually falls until the same moment of the opening of Shanghai and Hong Kong.

Second hour of the China session

08:30 pm

Hong Kong and Shanghai start trading and the euro usually grows for more than an hour. The EUR / USD pair mixes up as Asian exporters convert part of their earnings into both US dollars and euros.

Last hour of the Tokyo session

11:00 pm

End of the Tokyo session

12:00 am

If the euro has been actively declining up to this time, China will raise the euro after the Tokyo shutdown. Hong Kong, Shanghai and Singapore remain open and take matters into their own hands causing the growth of the euro. Asia is a huge commercial and industrial region with a large number of high-quality economic products and gigantic financial turnover, making the number of transactions on the stock exchanges huge during the Asian session. That is why traders, who entered the trade at the opening of the London session, should pay attention to their terminals when Asia exits the market.

End of the Shanghai session

01:00 am

The trade ends in Shanghai. This is the last trading hour of the Hong Kong session, during which market activity peaks.

D. Kill Zones

10:00 pm - 2:00 am

Asian Kill Zone. Considered the "Institutional" Zone, this zone represents both the launch pad for new trends as well as a recharge area for the post-American session. It is the beginning of a new day (or week) for the world and as such it makes sense that this zone often sets the tone for the remainder of the global business day. It is ideal to pay attention to the opening of Tokyo, Beijing and Sydney.

--------------

Sidney

Sydney (ASX - Australia Stock Exchange)

06:00 pm - 12:00 am

A. Complementary Stock Exchange

New Zealand (NZX - New Zealand Stock Exchange)

04:00 pm - 10:45 pm

It's where the global trading day officially begins. While it is the smallest of the megamarkets, it sees a lot of initial action when markets reopen Sunday afternoon as individual traders and financial institutions are trying to regroup after the long hiatus since Friday afternoon. On weekdays it constitutes the end of the current trading day where the change in the settlement date occurs.

B. Pacific Trading Session

04:00 pm - 12:00 am

(from the opening of the Wellington session to the end of the Sydney session)

Forex begins its business hours when Wellington (New Zealand Exchange) opens local time on Monday. Sydney (Australian Stock Exchange) opens in 2 hours. It is a session with a fairly low volatility, configuring itself as the calmest session of all. Strong movements appear when influential news is published and when the Pacific session overlaps the Asian Session.

C. Strategic Points

End of the Sydney session

12:00 am

---------------

Conclusions

The best time to trade is during overlaps in trading times between open markets. Overlaps equate to higher price ranges, creating greater opportunities.

Regarding press releases (news), it should be noted that these in the currency markets have the power to improve a normally slow trading period. When a major announcement is made regarding economic data, especially when it goes against the predicted forecast, the coin can lose or gain value in a matter of seconds. In general, the more economic growth a country produces, the more positive the economy is for international investors. Investment capital tends to flow to countries that are believed to have good growth prospects and subsequently good investment opportunities, leading to the strengthening of the country's exchange rate. Also, a country that has higher interest rates through its government bonds tends to attract investment capital as foreign investors seek high-yield opportunities. However, stable economic growth and attractive yields or interest rates are inextricably intertwined. It's important to take advantage of market overlaps and keep an eye out for press releases when setting up a trading schedule.

References:

www.investopedia.com

www.investopedia.com

www.investopedia.com

www.investopedia.com

market24hclock.com

market24hclock.com

ค้นหาในสคริปต์สำหรับ "电力行业+股票+11年涨幅"

Back to zero: Understanding seriestype: pine series basic example

time required: 10 minutes

level: medium (need to know the "array" data variable as a generic programming concept, basic Pine syntax)

tl;dr how variables and series work in Pine

Pine is an array/vector language. That's something that twists how it behaves, and how we have to think about it. A lot of misunderstandings come from forgetting this fact. This example tries to clear that concept.

First, you need to know what an array is, and how it works in a programmig language. Also, having javascript under your belt helps too. If you don't, google "javascript array basic tutorial" is your friend :)

So, in pine arrays are called "series". Every variable is an array with values for each candle in the chart. if we do:

myVar = true

this is not a constant. It is a series of values for each candle, { true, true,....., true }

In practice, the result is the same, but we can access each of the values in the series, like myVar{0}, myVar{7}, myVar{anyNumber}....

Again, it is not a constant, since you can access/modify the each value individually

so, lets show it:

plot (myVar, clolor = gray)

this plots an horizontal line of value 1 ( 1 is equal to true ) so it's all good.

On to a more usual series:

tipicalSeries = close > open ? true : false

plot(tipicalSeries, color= blue)

This gives the expected result, a tipical up and down line with values at 1 or 0. Naturally, "tipicalSeries" is an array, the "ups" and "downs" are all stored under the same variable, indexed by the candles.

In Pine, the ZERO position in the array is the last one, which corresponds to the last candle on the right. Say you have a chart with 12 candles. The close would be the closing value of what we intuitively think as first candle, the one on the left. then close ... and so on.... until close , the value of the "last" candle, the one on the right. It actually helps to start thinking of the positions backwards, counting down to zero, rocket launch style :)

And back to our series. The myVar will also be the same size, from myVar to myVar .

When we do some operation with them, something simple like

if ( myVar == tipicalSeries)

what is really happening is that internally, Pine is checking each of the indexes, as in myVar == tipicalSeries , myVar == tipicalSeries .... myVar == tipicalSeries

And we can store that stuff to check it. simply:

result = (myVar == tipicalSeries) ? true : false //yes, this is the same as tipicalSeries, but we're not in a boolean logic tut ;)

plot (result)

The reason we can plot the result is that it is an array, not a single value. The example indicator i provide shows a plot where the values are obtained from different places in the array, this line here:

mySeries3 = mySeries2 and mySeries1

this creates a series that is the result of the PREVIOUS values stored (the zero index is the one most at the right, or the "current" one), which here just causes a shift in the plotted line by one candle.

Go ahead, grab a copy of my code, try to change the indexes and see the results. Understanding this stuff is critical to go deeper into Pine :)

ICT Macro Slot Algo Event📊 Overview

A powerful multi-timeframe trading indicator that combines Institutional Macro Session Tracking identify optimal trading windows throughout the day. This tool helps traders align with institutional flow patterns and algorithmic activity across major sessions.

🎯 Key Features

1. Macro Algo Event Sessions

Tracks 6 key institutional time windows during NY Session:

NY Sweep (08:50-09:10) - Opening balance flows

Silver Bullet #1 (09:50-10:10) - First major macro move

Silver Bullet #2 (10:50-11:10) - Second chance/retest opportunity

Lunch Macro (11:50-12:10) - Mid-day repositioning

Post-Lunch Rebalance (13:10-13:40) - Post-lunch adjustments

NY Closing Macros (15:15-15:45) - End-of-day flows

ICT Macro Slot Algo Event📊 Overview

A powerful multi-timeframe trading indicator that combines Institutional Macro Session Tracking to identify optimal trading windows throughout the day. This tool helps traders align with institutional flow patterns and algorithmic activity across major sessions.

🎯 Key Features

1. Macro Algo Event Sessions

Tracks 6 key institutional time windows during NY Session:

NY Sweep (08:50-09:10) - Opening balance flows

Silver Bullet #1 (09:50-10:10) - First major macro move

Silver Bullet #2 (10:50-11:10) - Second chance/retest opportunity

Lunch Macro (11:50-12:10) - Mid-day repositioning

Post-Lunch Rebalance (13:10-13:40) - Post-lunch adjustments

NY Closing Macros (15:15-15:45) - End-of-day flows

Bifurcation Zone - CAEBifurcation Zone — Cognitive Adversarial Engine (BZ-CAE)

Bifurcation Zone — CAE (BZ-CAE) is a next-generation divergence detection system enhanced by a Cognitive Adversarial Engine that evaluates both sides of every potential trade before presenting signals. Unlike traditional divergence indicators that show every price-oscillator disagreement regardless of context, BZ-CAE applies comprehensive market-state intelligence to identify only the divergences that occur in favorable conditions with genuine probability edges.

The system identifies structural bifurcation points — critical junctures where price and momentum disagree, signaling potential reversals or continuations — then validates these opportunities through five interconnected intelligence layers: Trend Conviction Scoring , Directional Momentum Alignment , Multi-Factor Exhaustion Modeling , Adversarial Validation , and Confidence Scoring . The result is a selective, context-aware signal system that filters noise and highlights high-probability setups.

This is not a "buy the arrow" indicator. It's a decision support framework that teaches you how to read market state, evaluate divergence quality, and make informed trading decisions based on quantified intelligence rather than hope.

What Sets BZ-CAE Apart: Technical Architecture

The Problem With Traditional Divergence Indicators

Most divergence indicators operate on a simple rule: if price makes a higher high and RSI makes a lower high, show a bearish signal. If price makes a lower low and RSI makes a higher low, show a bullish signal. This creates several critical problems:

Context Blindness : They show counter-trend signals in powerful trends that rarely reverse, leading to repeated losses as you fade momentum.

Signal Spam : Every minor price-oscillator disagreement generates an alert, overwhelming you with low-quality setups and creating analysis paralysis.

No Quality Ranking : All signals are treated identically. A marginal divergence in choppy conditions receives the same visual treatment as a high-conviction setup at a major exhaustion point.

Single-Sided Evaluation : They ask "Is this a good long?" without checking if the short case is overwhelmingly stronger, leading you into obvious bad trades.

Static Configuration : You manually choose RSI 14 or Stochastic 14 and hope it works, with no systematic way to validate if that's optimal for your instrument.

BZ-CAE's Solution: Cognitive Adversarial Intelligence

BZ-CAE solves these problems through an integrated five-layer intelligence architecture:

1. Trend Conviction Score (TCS) — 0 to 1 Scale

Most indicators check if ADX is above 25 to determine "trending" conditions. This binary approach misses nuance. TCS is a weighted composite metric:

Formula : 0.35 × normalize(ADX, 10, 35) + 0.35 × structural_strength + 0.30 × htf_alignment

Structural Strength : 10-bar SMA of consecutive directional bars. Captures persistence — are bulls or bears consistently winning?

HTF Alignment : Multi-timeframe EMA stacking (20/50/100/200). When all EMAs align in the same direction, you're in institutional trend territory.

Purpose : Quantifies how "locked in" the trend is. When TCS exceeds your threshold (default 0.80), the system knows to avoid counter-trend trades unless other factors override.

Interpretation :

TCS > 0.85: Very strong trend — counter-trading is extremely high risk

TCS 0.70-0.85: Strong trend — favor continuation, require exhaustion for reversals

TCS 0.50-0.70: Moderate trend — context matters, both directions viable

TCS < 0.50: Weak/choppy — reversals more viable, range-bound conditions

2. Directional Momentum Alignment (DMA) — ATR-Normalized

Formula : (EMA21 - EMA55) / ATR14

This isn't just "price above EMA" — it's a regime-aware momentum gauge. The same $100 price movement reads completely differently in high-volatility crypto versus low-volatility forex. By normalizing with ATR, DMA adapts its interpretation to current market conditions.

Purpose : Quantifies the directional "force" behind current price action. Positive = bullish push, negative = bearish push. Magnitude = strength.

Interpretation :

DMA > 0.7: Strong bullish momentum — bearish divergences risky

DMA 0.3 to 0.7: Moderate bullish bias

DMA -0.3 to 0.3: Balanced/choppy conditions

DMA -0.7 to -0.3: Moderate bearish bias

DMA < -0.7: Strong bearish momentum — bullish divergences risky

3. Multi-Factor Exhaustion Modeling — 0 to 1 Probability

Single-metric exhaustion detection (like "RSI > 80") misses complex market states. BZ-CAE aggregates five independent exhaustion signals:

Volume Spikes : Current volume versus 50-bar average

2.5x average: 0.25 weight

2.0x average: 0.15 weight

1.5x average: 0.10 weight

Divergence Present : The fact that a divergence exists contributes 0.30 weight — structural momentum disagreement is itself an exhaustion signal.

RSI Extremes : Captures oscillator climax zones

RSI > 80 or < 20: 0.25 weight

RSI > 75 or < 25: 0.15 weight

Pin Bar Detection : Identifies rejection candles (2:1 wick-to-body ratio, indicating failed breakout attempts): 0.15 weight

Extended Runs : Consecutive bars above/below EMA20 without pullback

30+ bars: 0.15 weight (market hasn't paused to consolidate)

Total exhaustion score is the sum of all applicable weights, capped at 1.0.

Purpose : Detects when strong trends become vulnerable to reversal. High exhaustion can override trend filters, allowing counter-trend trades at genuine turning points that basic indicators would miss.

Interpretation :

Exhaustion > 0.75: High probability of climax — yellow background shading alerts you visually

Exhaustion 0.50-0.75: Moderate overextension — watch for confirmation

Exhaustion < 0.50: Fresh move — trend can continue, counter-trend trades higher risk

4. Adversarial Validation — Game Theory Applied to Trading

This is BZ-CAE's signature innovation. Before approving any signal, the engine quantifies BOTH sides of the trade simultaneously:

For Bullish Divergences , it calculates:

Bull Case Score (0-1+) :

Distance below EMA20 (pullback quality): up to 0.25

Bullish EMA alignment (close > EMA20 > EMA50): 0.25

Oversold RSI (< 40): 0.25

Volume confirmation (> 1.2x average): 0.25

Bear Case Score (0-1+) :

Price below EMA50 (structural weakness): 0.30

Very oversold RSI (< 30, indicating knife-catching): 0.20

Differential = Bull Case - Bear Case

If differential < -0.10 (default threshold), the bear case is dominating — signal is BLOCKED or ANNOTATED.

For Bearish Divergences , the logic inverts (Bear Case vs Bull Case).

Purpose : Prevents trades where you're fighting obvious strength in the opposite direction. This is institutional-grade risk management — don't just evaluate your trade, evaluate the counter-trade simultaneously.

Why This Matters : You might see a bullish divergence at a local low, but if price is deeply below major support EMAs with strong bearish momentum, you're catching a falling knife. The adversarial check catches this and blocks the signal.

5. Confidence Scoring — 0 to 1 Quality Assessment

Every signal that passes initial filters receives a comprehensive quality score:

Formula :

0.30 × normalize(TCS) // Trend context

+ 0.25 × normalize(|DMA|) // Momentum magnitude

+ 0.20 × pullback_quality // Entry distance from EMA20

+ 0.15 × state_quality // ADX + alignment + structure

+ 0.10 × divergence_strength // Slope separation magnitude

+ adversarial_bonus (0-0.30) // Your side's advantage

Purpose : Ranks setup quality for filtering and position sizing decisions. You can set a minimum confidence threshold (default 0.35) to ensure only quality setups reach your chart.

Interpretation :

Confidence > 0.70: Premium setup — consider increased position size

Confidence 0.50-0.70: Good quality — standard size

Confidence 0.35-0.50: Acceptable — reduced size or skip if conservative

Confidence < 0.35: Marginal — blocked in Filtering mode, annotated in Advisory mode

CAE Operating Modes: Learning vs Enforcement

Off : Disables all CAE logic. Raw divergence pipeline only. Use for baseline comparison.

Advisory : Shows ALL signals regardless of CAE evaluation, but annotates signals that WOULD be blocked with specific warnings (e.g., "Bull: strong downtrend (TCS=0.87)" or "Adversarial bearish"). This is your learning mode — see CAE's decision logic in action without missing educational opportunities.

Filtering : Actively blocks low-quality signals. Only setups that pass all enabled gates (Trend Filter, Adversarial Validation, Confidence Gating) reach your chart. This is your live trading mode — trust the system to enforce discipline.

CAE Filter Gates: Three-Layer Protection

When CAE is enabled, signals must pass through three independent gates (each can be toggled on/off):

Gate 1: Strong Trend Filter

If TCS ≥ tcs_threshold (default 0.80)

And signal is counter-trend (bullish in downtrend or bearish in uptrend)

And exhaustion < exhaustion_required (default 0.50)

Then: BLOCK signal

Logic: Don't fade strong trends unless the move is clearly overextended

Gate 2: Adversarial Validation

Calculate both bull case and bear case scores

If opposing case dominates by more than adv_threshold (default 0.10)

Then: BLOCK signal

Logic: Avoid trades where you're fighting obvious strength in the opposite direction

Gate 3: Confidence Gating

Calculate composite confidence score (0-1)

If confidence < min_confidence (default 0.35)

Then: In Filtering mode, BLOCK signal; in Advisory mode, ANNOTATE with warning

Logic: Only take setups with minimum quality threshold

All three gates work together. A signal must pass ALL enabled gates to fire.

Visual Intelligence System

Bifurcation Zones (Supply/Demand Blocks)

When a divergence signal fires, BZ-CAE draws a semi-transparent box extending 15 bars forward from the signal pivot:

Demand Zones (Bullish) : Theme-colored box (cyan in Cyberpunk, blue in Professional, etc.) labeled "Demand" — marks where smart money likely placed buy orders as price diverged at the low.

Supply Zones (Bearish) : Theme-colored box (magenta in Cyberpunk, orange in Professional) labeled "Supply" — marks where smart money likely placed sell orders as price diverged at the high.

Theory : Divergences represent institutional disagreement with the crowd. The crowd pushed price to an extreme (new high or low), but momentum (oscillator) is waning, indicating smart money is taking the opposite side. These zones mark order placement areas that become future support/resistance.

Use Cases :

Exit targets: Take profit when price returns to opposite-side zone

Re-entry levels: If price returns to your entry zone, consider adding

Stop placement: Place stops just beyond your zone (below demand, above supply)

Auto-Cleanup : System keeps the last 20 zones to prevent chart clutter.

Adversarial Bar Coloring — Real-Time Market Debate Heatmap

Each bar is colored based on the Bull Case vs Bear Case differential:

Strong Bull Advantage (diff > 0.3): Full theme bull color (e.g., cyan)

Moderate Bull Advantage (diff > 0.1): 50% transparency bull

Neutral (diff -0.1 to 0.1): Gray/neutral theme

Moderate Bear Advantage (diff < -0.1): 50% transparency bear

Strong Bear Advantage (diff < -0.3): Full theme bear color (e.g., magenta)

This creates a real-time visual heatmap showing which side is "winning" the market debate. When bars flip from cyan to magenta (or vice versa), you're witnessing a shift in adversarial advantage — a leading indicator of potential momentum changes.

Exhaustion Shading

When exhaustion score exceeds 0.75, the chart background displays a semi-transparent yellow highlight. This immediate visual warning alerts you that the current move is at high risk of reversal, even if trend indicators remain strong.

Visual Themes — Six Aesthetic Options

Cyberpunk : Cyan/Magenta/Yellow — High contrast, neon aesthetic, excellent for dark-themed trading environments

Professional : Blue/Orange/Green — Corporate color palette, suitable for presentations and professional documentation

Ocean : Teal/Red/Cyan — Aquatic palette, calming for extended monitoring sessions

Fire : Orange/Red/Coral — Warm aggressive colors, high energy

Matrix : Green/Red/Lime — Code aesthetic, homage to classic hacker visuals

Monochrome : White/Gray — Minimal distraction, maximum focus on price action

All visual elements (signal markers, zones, bar colors, dashboard) adapt to your selected theme.

Divergence Engine — Core Detection System

What Are Divergences?

Divergences occur when price action and momentum indicators disagree, creating structural tension that often resolves in a change of direction:

Regular Divergence (Reversal Signal) :

Bearish Regular : Price makes higher high, oscillator makes lower high → Potential trend reversal down

Bullish Regular : Price makes lower low, oscillator makes higher low → Potential trend reversal up

Hidden Divergence (Continuation Signal) :

Bearish Hidden : Price makes lower high, oscillator makes higher high → Downtrend continuation

Bullish Hidden : Price makes higher low, oscillator makes lower low → Uptrend continuation

Both types can be enabled/disabled independently in settings.

Pivot Detection Methods

BZ-CAE uses symmetric pivot detection with separate lookback and lookforward periods (default 5/5):

Pivot High : Bar where high > all highs within lookback range AND high > all highs within lookforward range

Pivot Low : Bar where low < all lows within lookback range AND low < all lows within lookforward range

This ensures structural validity — the pivot must be a clear local extreme, not just a minor wiggle.

Divergence Validation Requirements

For a divergence to be confirmed, it must satisfy:

Slope Disagreement : Price slope and oscillator slope must move in opposite directions (for regular divs) or same direction with inverted highs/lows (for hidden divs)

Minimum Slope Change : |osc_slope| > min_slope_change / 100 (default 1.0) — filters weak, marginal divergences

Maximum Lookback Range : Pivots must be within max_lookback bars (default 60) — prevents ancient, irrelevant divergences

ATR-Normalized Strength : Divergence strength = min(|price_slope| × |osc_slope| × 10, 1.0) — quantifies the magnitude of disagreement in volatility context

Regular divergences receive 1.0× weight; hidden divergences receive 0.8× weight (slightly less reliable historically).

Oscillator Options — Five Professional Indicators

RSI (Relative Strength Index) : Classic overbought/oversold momentum indicator. Best for: General purpose divergence detection across all instruments.

Stochastic : Range-bound %K momentum comparing close to high-low range. Best for: Mean reversion strategies and range-bound markets.

CCI (Commodity Channel Index) : Measures deviation from statistical mean, auto-normalized to 0-100 scale. Best for: Cyclical instruments and commodities.

MFI (Money Flow Index) : Volume-weighted RSI incorporating money flow. Best for: Volume-driven markets like stocks and crypto.

Williams %R : Inverse stochastic looking back over period, auto-adjusted to 0-100. Best for: Reversal detection at extremes.

Each oscillator has adjustable length (2-200, default 14) and smoothing (1-20, default 1). You also set overbought (50-100, default 70) and oversold (0-50, default 30) thresholds.

Signal Timing Modes — Understanding Repainting

BZ-CAE offers two timing policies with complete transparency about repainting behavior:

Realtime (1-bar, peak-anchored)

How It Works :

Detects peaks 1 bar ago using pattern: high > high AND high > high

Signal prints on the NEXT bar after peak detection (bar_index)

Visual marker anchors to the actual PEAK bar (bar_index - 1, offset -1)

Signal locks in when bar CONFIRMS (closes)

Repainting Behavior :

On the FORMING bar (before close), the peak condition may change as new prices arrive

Once bar CLOSES (barstate.isconfirmed), signal is locked permanently

This is preview/early warning behavior by design

Best For :

Active monitoring and immediate alerts

Learning the system (seeing signals develop in real-time)

Responsive entry if you're watching the chart live

Confirmed (lookforward)

How It Works :

Uses Pine Script's built-in ta.pivothigh() and ta.pivotlow() functions

Requires full pivot validation period (lookback + lookforward bars)

Signal prints pivot_lookforward bars after the actual peak (default 5-bar delay)

Visual marker anchors to the actual peak bar (offset -pivot_lookforward)

No Repainting Behavior

Best For :

Backtesting and historical analysis

Conservative entries requiring full confirmation

Automated trading systems

Swing trading with larger timeframes

Tradeoff :

Delayed entry by pivot_lookforward bars (typically 5 bars)

On a 5-minute chart, this is a 25-minute delay

On a 4-hour chart, this is a 20-hour delay

Recommendation : Use Confirmed for backtesting to verify system performance honestly. Use Realtime for live monitoring only if you're actively watching the chart and understand pre-confirmation repainting behavior.

Signal Spacing System — Anti-Spam Architecture

Even after CAE filtering, raw divergences can cluster. The spacing system enforces separation:

Three Independent Filters

1. Min Bars Between ANY Signals (default 12):

Prevents rapid-fire clustering across both directions

If last signal (bull or bear) was within N bars, block new signal

Ensures breathing room between all setups

2. Min Bars Between SAME-SIDE Signals (default 24, optional enforcement):

Prevents bull-bull or bear-bear spam

Separate tracking for bullish and bearish signal timelines

Toggle enforcement on/off

3. Min ATR Distance From Last Signal (default 0, optional):

Requires price to move N × ATR from last signal location

Ensures meaningful price movement between setups

0 = disabled, 0.5-2.0 = typical range for enabled

All three filters work independently. A signal must pass ALL enabled filters to proceed.

Practical Guidance :

Scalping (1-5m) : Any 6-10, Same-side 12-20, ATR 0-0.5

Day Trading (15m-1H) : Any 12, Same-side 24, ATR 0-1.0

Swing Trading (4H-D) : Any 20-30, Same-side 40-60, ATR 1.0-2.0

Dashboard — Real-Time Control Center

The dashboard (toggleable, four corner positions, three sizes) provides comprehensive system intelligence:

Oscillator Section

Current oscillator type and value

State: OVERBOUGHT / OVERSOLD / NEUTRAL (color-coded)

Length parameter

Cognitive Engine Section

TCS (Trend Conviction Score) :

Current value with emoji state indicator

🔥 = Strong trend (>0.75)

📊 = Moderate trend (0.50-0.75)

〰️ = Weak/choppy (<0.50)

Color: Red if above threshold (trend filter active), yellow if moderate, green if weak

DMA (Directional Momentum Alignment) :

Current value with emoji direction indicator

🐂 = Bullish momentum (>0.5)

⚖️ = Balanced (-0.5 to 0.5)

🐻 = Bearish momentum (<-0.5)

Color: Green if bullish, red if bearish

Exhaustion :

Current value with emoji warning indicator

⚠️ = High exhaustion (>0.75)

🟡 = Moderate (0.50-0.75)

✓ = Low (<0.50)

Color: Red if high, yellow if moderate, green if low

Pullback :

Quality of current distance from EMA20

Values >0.6 are ideal entry zones (not too close, not too far)

Bull Case / Bear Case (if Adversarial enabled):

Current scores for both sides of the market debate

Differential with emoji indicator:

📈 = Bull advantage (>0.2)

➡️ = Balanced (-0.2 to 0.2)

📉 = Bear advantage (<-0.2)

Last Signal Metrics Section (New Feature)

When a signal fires, this section captures and displays:

Signal type (BULL or BEAR)

Bars elapsed since signal

Confidence % at time of signal

TCS value at signal time

DMA value at signal time

Purpose : Provides a historical reference for learning. You can see what the market state looked like when the last signal fired, helping you correlate outcomes with conditions.

Statistics Section

Total Signals : Lifetime count across session

Blocked Signals : Count and percentage (filter effectiveness metric)

Bull Signals : Total bullish divergences

Bear Signals : Total bearish divergences

Purpose : System health monitoring. If blocked % is very high (>60%), filters may be too strict. If very low (<10%), filters may be too loose.

Advisory Annotations

When CAE Mode = Advisory, this section displays warnings for signals that would be blocked in Filtering mode:

Examples:

"Bull spacing: wait 8 bars"

"Bear: strong uptrend (TCS=0.87)"

"Adversarial bearish"

"Low confidence 32%"

Multiple warnings can stack, separated by " | ". This teaches you CAE's decision logic transparently.

How to Use BZ-CAE — Complete Workflow

Phase 1: Initial Setup (First Session)

Apply BZ-CAE to your chart

Select your preferred Visual Theme (Cyberpunk recommended for visibility)

Set Signal Timing to "Confirmed (lookforward)" for learning

Choose your Oscillator Type (RSI recommended for general use, length 14)

Set Overbought/Oversold to 70/30 (standard)

Enable both Regular Divergence and Hidden Divergence

Set Pivot Lookback/Lookforward to 5/5 (balanced structure)

Enable CAE Intelligence

Set CAE Mode to "Advisory" (learning mode)

Enable all three CAE filters: Strong Trend Filter , Adversarial Validation , Confidence Gating

Enable Show Dashboard , position Top Right, size Normal

Enable Draw Bifurcation Zones and Adversarial Bar Coloring

Phase 2: Learning Period (Weeks 1-2)

Goal : Understand how CAE evaluates market state and filters signals.

Activities :

Watch the dashboard during signals :

Note TCS values when counter-trend signals fail — this teaches you the trend strength threshold for your instrument

Observe exhaustion patterns at actual turning points — learn when overextension truly matters

Study adversarial differential at signal times — see when opposing cases dominate

Review blocked signals (orange X-crosses):

In Advisory mode, you see everything — signals that would pass AND signals that would be blocked

Check the advisory annotations to understand why CAE would block

Track outcomes: Were the blocks correct? Did those signals fail?

Use Last Signal Metrics :

After each signal, check the dashboard capture of confidence, TCS, and DMA

Journal these values alongside trade outcomes

Identify patterns: Do confidence >0.70 signals work better? Does your instrument respect TCS >0.85?

Understand your instrument's "personality" :

Trending instruments (indices, major forex) may need TCS threshold 0.85-0.90

Choppy instruments (low-cap stocks, exotic pairs) may work best with TCS 0.70-0.75

High-volatility instruments (crypto) may need wider spacing

Low-volatility instruments may need tighter spacing

Phase 3: Calibration (Weeks 3-4)

Goal : Optimize settings for your specific instrument, timeframe, and style.

Calibration Checklist :

Min Confidence Threshold :

Review confidence distribution in your signal journal

Identify the confidence level below which signals consistently fail

Set min_confidence slightly above that level

Day trading : 0.35-0.45

Swing trading : 0.40-0.55

Scalping : 0.30-0.40

TCS Threshold :

Find the TCS level where counter-trend signals consistently get stopped out

Set tcs_threshold at or slightly below that level

Trending instruments : 0.85-0.90

Mixed instruments : 0.80-0.85

Choppy instruments : 0.75-0.80

Exhaustion Override Level :

Identify exhaustion readings that marked genuine reversals

Set exhaustion_required just below the average

Typical range : 0.45-0.55

Adversarial Threshold :

Default 0.10 works for most instruments

If you find CAE is too conservative (blocking good trades), raise to 0.15-0.20

If signals are still getting caught in opposing momentum, lower to 0.07-0.09

Spacing Parameters :

Count bars between quality signals in your journal

Set min bars ANY to ~60% of that average

Set min bars SAME-SIDE to ~120% of that average

Scalping : Any 6-10, Same 12-20

Day trading : Any 12, Same 24

Swing : Any 20-30, Same 40-60

Oscillator Selection :

Try different oscillators for 1-2 weeks each

Track win rate and average winner/loser by oscillator type

RSI : Best for general use, clear OB/OS

Stochastic : Best for range-bound, mean reversion

MFI : Best for volume-driven markets

CCI : Best for cyclical instruments

Williams %R : Best for reversal detection

Phase 4: Live Deployment

Goal : Disciplined execution with proven, calibrated system.

Settings Changes :

Switch CAE Mode from Advisory to Filtering

System now actively blocks low-quality signals

Only setups passing all gates reach your chart

Keep Signal Timing on Confirmed for conservative entries

OR switch to Realtime if you're actively monitoring and want faster entries (accept pre-confirmation repaint risk)

Use your calibrated thresholds from Phase 3

Enable high-confidence alerts: "⭐ High Confidence Bullish/Bearish" (>0.70)

Trading Discipline Rules :

Respect Blocked Signals :

If CAE blocks a trade you wanted to take, TRUST THE SYSTEM

Don't manually override — if you consistently disagree, return to Phase 2/3 calibration

The block exists because market state failed intelligence checks

Confidence-Based Position Sizing :

Confidence >0.70: Standard or increased size (e.g., 1.5-2.0% risk)

Confidence 0.50-0.70: Standard size (e.g., 1.0% risk)

Confidence 0.35-0.50: Reduced size (e.g., 0.5% risk) or skip if conservative

TCS-Based Management :

High TCS + counter-trend signal: Use tight stops, quick exits (you're fading momentum)

Low TCS + reversal signal: Use wider stops, trail aggressively (genuine reversal potential)

Exhaustion Awareness :

Exhaustion >0.75 (yellow shading): Market is overextended, reversal risk is elevated — consider early exit or tighter trailing stops even on winning trades

Exhaustion <0.30: Continuation bias — hold for larger move, wide trailing stops

Adversarial Context :

Strong differential against you (e.g., bullish signal with bear diff <-0.2): Use very tight stops, consider skipping

Strong differential with you (e.g., bullish signal with bull diff >0.2): Trail aggressively, this is your tailwind

Practical Settings by Timeframe & Style

Scalping (1-5 Minute Charts)

Objective : High frequency, tight stops, quick reversals in fast-moving markets.

Oscillator :

Type: RSI or Stochastic (fast response to quick moves)

Length: 9-11 (more responsive than standard 14)

Smoothing: 1 (no lag)

OB/OS: 65/35 (looser thresholds ensure frequent crossings in fast conditions)

Divergence :

Pivot Lookback/Lookforward: 3/3 (tight structure, catch small swings)

Max Lookback: 40-50 bars (recent structure only)

Min Slope Change: 0.8-1.0 (don't be overly strict)

CAE :

Mode: Advisory first (learn), then Filtering

Min Confidence: 0.30-0.35 (lower bar for speed, accept more signals)

TCS Threshold: 0.70-0.75 (allow more counter-trend opportunities)

Exhaustion Required: 0.45-0.50 (moderate override)

Strong Trend Filter: ON (still respect major intraday trends)

Adversarial: ON (critical for scalping protection — catches bad entries quickly)

Spacing :

Min Bars ANY: 6-10 (fast pace, many setups)

Min Bars SAME-SIDE: 12-20 (prevent clustering)

Min ATR Distance: 0 or 0.5 (loose)

Timing : Realtime (speed over precision, but understand repaint risk)

Visuals :

Signal Size: Tiny (chart clarity in busy conditions)

Show Zones: Optional (can clutter on low timeframes)

Bar Coloring: ON (helps read momentum shifts quickly)

Dashboard: Small size (corner reference, not main focus)

Key Consideration : Scalping generates noise. Even with CAE, expect lower win rate (45-55%) but aim for favorable R:R (2:1 or better). Size conservatively.

Day Trading (15-Minute to 1-Hour Charts)

Objective : Balance quality and frequency. Standard divergence trading approach.

Oscillator :

Type: RSI or MFI (proven reliability, volume confirmation with MFI)

Length: 14 (industry standard, well-studied)

Smoothing: 1-2

OB/OS: 70/30 (classic levels)

Divergence :

Pivot Lookback/Lookforward: 5/5 (balanced structure)

Max Lookback: 60 bars

Min Slope Change: 1.0 (standard strictness)

CAE :

Mode: Filtering (enforce discipline from the start after brief Advisory learning)

Min Confidence: 0.35-0.45 (quality filter without being too restrictive)

TCS Threshold: 0.80-0.85 (respect strong trends)

Exhaustion Required: 0.50 (balanced override threshold)

Strong Trend Filter: ON

Adversarial: ON

Confidence Gating: ON (all three filters active)

Spacing :

Min Bars ANY: 12 (breathing room between all setups)

Min Bars SAME-SIDE: 24 (prevent bull/bear clusters)

Min ATR Distance: 0-1.0 (optional refinement, typically 0.5-1.0)

Timing : Confirmed (1-bar delay for reliability, no repainting)

Visuals :

Signal Size: Tiny or Small

Show Zones: ON (useful reference for exits/re-entries)

Bar Coloring: ON (context awareness)

Dashboard: Normal size (full visibility)

Key Consideration : This is the "sweet spot" timeframe for BZ-CAE. Market structure is clear, CAE has sufficient data, and signal frequency is manageable. Expect 55-65% win rate with proper execution.

Swing Trading (4-Hour to Daily Charts)

Objective : Quality over quantity. High conviction only. Larger stops and targets.

Oscillator :

Type: RSI or CCI (robust on higher timeframes, smooth longer waves)

Length: 14-21 (capture larger momentum swings)

Smoothing: 1-3

OB/OS: 70/30 or 75/25 (strict extremes)

Divergence :

Pivot Lookback/Lookforward: 5/5 or 7/7 (structural purity, major swings only)

Max Lookback: 80-100 bars (broader historical context)

Min Slope Change: 1.2-1.5 (require strong, undeniable divergence)

CAE :

Mode: Filtering (strict enforcement, premium setups only)

Min Confidence: 0.40-0.55 (high bar for entry)

TCS Threshold: 0.85-0.95 (very strong trend protection — don't fade established HTF trends)

Exhaustion Required: 0.50-0.60 (higher bar for override — only extreme exhaustion justifies counter-trend)

Strong Trend Filter: ON (critical on HTF)

Adversarial: ON (avoid obvious bad trades)

Confidence Gating: ON (quality gate essential)

Spacing :

Min Bars ANY: 20-30 (substantial separation)

Min Bars SAME-SIDE: 40-60 (significant breathing room)

Min ATR Distance: 1.0-2.0 (require meaningful price movement)

Timing : Confirmed (purity over speed, zero repaint for swing accuracy)

Visuals :

Signal Size: Small or Normal (clear markers on zoomed-out view)

Show Zones: ON (important HTF levels)

Bar Coloring: ON (long-term trend awareness)

Dashboard: Normal or Large (comprehensive analysis)

Key Consideration : Swing signals are rare but powerful. Expect 2-5 signals per month per instrument. Win rate should be 60-70%+ due to stringent filtering. Position size can be larger given confidence.

Dashboard Interpretation Reference

TCS (Trend Conviction Score) States

0.00-0.50: Weak/Choppy

Emoji: 〰️

Color: Green/cyan

Meaning: No established trend. Range-bound or consolidating. Both reversal and continuation signals viable.

Action: Reversals (regular divs) are safer. Use wider profit targets (market has room to move). Consider mean reversion strategies.

0.50-0.75: Moderate Trend

Emoji: 📊

Color: Yellow/neutral

Meaning: Developing trend but not locked in. Context matters significantly.

Action: Check DMA and exhaustion. If DMA confirms trend and exhaustion is low, favor continuation (hidden divs). If exhaustion is high, reversals are viable.

0.75-0.85: Strong Trend

Emoji: 🔥

Color: Orange/warning

Meaning: Well-established trend with persistence. Counter-trend is high risk.

Action: Require exhaustion >0.50 for counter-trend entries. Favor continuation signals. Use tight stops on counter-trend attempts.

0.85-1.00: Very Strong Trend

Emoji: 🔥🔥

Color: Red/danger (if counter-trading)

Meaning: Locked-in institutional trend. Extremely high risk to fade.

Action: Avoid counter-trend unless exhaustion >0.75 (yellow shading). Focus exclusively on continuation opportunities. Momentum is king here.

DMA (Directional Momentum Alignment) Zones

-2.0 to -1.0: Strong Bearish Momentum

Emoji: 🐻🐻

Color: Dark red

Meaning: Powerful downside force. Sellers are in control.

Action: Bullish divergences are counter-momentum (high risk). Bearish divergences are with-momentum (lower risk). Size down on longs.

-0.5 to 0.5: Neutral/Balanced

Emoji: ⚖️

Color: Gray/neutral

Meaning: No strong directional bias. Choppy or consolidating.

Action: Both directions have similar probability. Focus on confidence score and adversarial differential for edge.

1.0 to 2.0: Strong Bullish Momentum

Emoji: 🐂🐂

Color: Bright green/cyan

Meaning: Powerful upside force. Buyers are in control.

Action: Bearish divergences are counter-momentum (high risk). Bullish divergences are with-momentum (lower risk). Size down on shorts.

Exhaustion States

0.00-0.50: Fresh Move

Emoji: ✓

Color: Green

Meaning: Trend is healthy, not overextended. Room to run.

Action: Counter-trend trades are premature. Favor continuation. Hold winners for larger moves. Avoid early exits.

0.50-0.75: Mature Move

Emoji: 🟡

Color: Yellow

Meaning: Move is aging. Watch for signs of climax.

Action: Tighten trailing stops on winning trades. Be ready for reversals. Don't add to positions aggressively.

0.75-0.85: High Exhaustion

Emoji: ⚠️

Color: Orange

Background: Yellow shading appears

Meaning: Move is overextended. Reversal risk elevated significantly.

Action: Counter-trend reversals are higher probability. Consider early exits on with-trend positions. Size up on reversal divergences (if CAE allows).

0.85-1.00: Critical Exhaustion

Emoji: ⚠️⚠️

Color: Red

Background: Yellow shading intensifies

Meaning: Climax conditions. Reversal imminent or underway.

Action: Aggressive reversal trades justified. Exit all with-trend positions. This is where major turns occur.

Confidence Score Tiers

0.00-0.30: Low Quality

Color: Red

Status: Blocked in Filtering mode

Action: Skip entirely. Setup lacks fundamental quality across multiple factors.

0.30-0.50: Moderate Quality

Color: Yellow/orange

Status: Marginal — passes in Filtering only if >min_confidence

Action: Reduced position size (0.5-0.75% risk). Tight stops. Conservative profit targets. Skip if you're selective.

0.50-0.70: High Quality

Color: Green/cyan

Status: Good setup across most quality factors

Action: Standard position size (1.0-1.5% risk). Normal stops and targets. This is your bread-and-butter trade.

0.70-1.00: Premium Quality

Color: Bright green/gold

Status: Exceptional setup — all factors aligned

Visual: Double confidence ring appears

Action: Consider increased position size (1.5-2.0% risk, maximum). Wider stops. Larger targets. High probability of success. These are rare — capitalize when they appear.

Adversarial Differential Interpretation

Bull Differential > 0.3 :

Visual: Strong cyan/green bar colors

Meaning: Bull case strongly dominates. Buyers have clear advantage.

Action: Bullish divergences favored (with-advantage). Bearish divergences face headwind (reduce size or skip). Momentum is bullish.

Bull Differential 0.1 to 0.3 :

Visual: Moderate cyan/green transparency

Meaning: Moderate bull advantage. Buyers have edge but not overwhelming.

Action: Both directions viable. Slight bias toward longs.

Differential -0.1 to 0.1 :

Visual: Gray/neutral bars

Meaning: Balanced debate. No clear advantage either side.

Action: Rely on other factors (confidence, TCS, exhaustion) for direction. Adversarial is neutral.

Bear Differential -0.3 to -0.1 :

Visual: Moderate red/magenta transparency

Meaning: Moderate bear advantage. Sellers have edge but not overwhelming.

Action: Both directions viable. Slight bias toward shorts.

Bear Differential < -0.3 :

Visual: Strong red/magenta bar colors

Meaning: Bear case strongly dominates. Sellers have clear advantage.

Action: Bearish divergences favored (with-advantage). Bullish divergences face headwind (reduce size or skip). Momentum is bearish.

Last Signal Metrics — Post-Trade Analysis

After a signal fires, dashboard captures:

Type : BULL or BEAR

Bars Ago : How long since signal (updates every bar)

Confidence : What was the quality score at signal time

TCS : What was trend conviction at signal time

DMA : What was momentum alignment at signal time

Use Case : Post-trade journaling and learning.

Example: "BULL signal 12 bars ago. Confidence: 68%, TCS: 0.42, DMA: -0.85"

Analysis : This was a bullish reversal (regular div) with good confidence, weak trend (TCS), but strong bearish momentum (DMA). The bet was that momentum would reverse — a counter-momentum play requiring exhaustion confirmation. Check if exhaustion was high at that time to justify the entry.

Track patterns:

Do your best trades have confidence >0.65?

Do low-TCS signals (<0.50) work better for you?

Are you more successful with-momentum (DMA aligned with signal) or counter-momentum?

Troubleshooting Guide

Problem: No Signals Appearing

Symptoms : Chart loads, dashboard shows metrics, but no divergence signals fire.

Diagnosis Checklist :

Check dashboard oscillator value : Is it crossing OB/OS levels (70/30)? If oscillator stays in 40-60 range constantly, it can't reach extremes needed for divergence detection.

Are pivots forming? : Look for local swing highs/lows on your chart. If price is in tight consolidation, pivots may not meet lookback/lookforward requirements.

Is spacing too tight? : Check "Last Signal" metrics — how many bars since last signal? If <12 and your min_bars_ANY is 12, spacing filter is blocking.

Is CAE blocking everything? : Check dashboard Statistics section — what's the blocked signal count? High blocks indicate overly strict filters.

Solutions :

Loosen OB/OS Temporarily :

Try 65/35 to verify divergence detection works

If signals appear, the issue was threshold strictness

Gradually tighten back to 67/33, then 70/30 as appropriate

Lower Min Confidence :

Try 0.25-0.30 (diagnostic level)

If signals appear, filter was too strict

Raise gradually to find sweet spot (0.35-0.45 typical)

Disable Strong Trend Filter Temporarily :

Turn off in CAE settings

If signals appear, TCS threshold was blocking everything

Re-enable and lower TCS_threshold to 0.70-0.75

Reduce Min Slope Change :

Try 0.7-0.8 (from default 1.0)

Allows weaker divergences through

Helpful on low-volatility instruments

Widen Spacing :

Set min_bars_ANY to 6-8

Set min_bars_SAME_SIDE to 12-16

Reduces time between allowed signals

Check Timing Mode :

If using Confirmed, remember there's a pivot_lookforward delay (5+ bars)

Switch to Realtime temporarily to verify system is working

Realtime has no delay but repaints

Verify Oscillator Settings :

Length 14 is standard but might not fit all instruments

Try length 9-11 for faster response

Try length 18-21 for slower, smoother response

Problem: Too Many Signals (Signal Spam)

Symptoms : Dashboard shows 50+ signals in Statistics, confidence scores mostly <0.40, signals clustering close together.

Solutions :

Raise Min Confidence :

Try 0.40-0.50 (quality filter)

Blocks bottom-tier setups

Targets top 50-60% of divergences only

Tighten OB/OS :

Use 70/30 or 75/25

Requires more extreme oscillator readings

Reduces false divergences in mid-range

Increase Min Slope Change :

Try 1.2-1.5 (from default 1.0)

Requires stronger, more obvious divergences

Filters marginal slope disagreements

Raise TCS Threshold :

Try 0.85-0.90 (from default 0.80)

Stricter trend filter blocks more counter-trend attempts

Favors only strongest trend alignment

Enable ALL CAE Gates :

Turn on Trend Filter + Adversarial + Confidence

Triple-layer protection

Blocks aggressively — expect 20-40% reduction in signals

Widen Spacing :

min_bars_ANY: 15-20 (from 12)

min_bars_SAME_SIDE: 30-40 (from 24)

Creates substantial breathing room

Switch to Confirmed Timing :

Removes realtime preview noise

Ensures full pivot validation

5-bar delay filters many false starts

Problem: Signals in Strong Trends Get Stopped Out

Symptoms : You take a bullish divergence in a downtrend (or bearish in uptrend), and it immediately fails. Dashboard showed high TCS at the time.

Analysis : This is INTENDED behavior — CAE is protecting you from low-probability counter-trend trades.

Understanding :

Check Last Signal Metrics in dashboard — what was TCS when signal fired?

If TCS was >0.85 and signal was counter-trend, CAE correctly identified it as high risk

Strong trends rarely reverse cleanly without major exhaustion

Your losses here are the system working as designed (blocking bad odds)

If You Want to Override (Not Recommended) :

Lower TCS_threshold to 0.70-0.75 (allows more counter-trend)

Lower exhaustion_required to 0.40 (easier override)

Disable Strong Trend Filter entirely (very risky)

Better Approach :

TRUST THE FILTER — it's preventing costly mistakes

Wait for exhaustion >0.75 (yellow shading) before counter-trending strong TCS

Focus on continuation signals (hidden divs) in high-TCS environments

Use Advisory mode to see what CAE is blocking and learn from outcomes

Problem: Adversarial Blocking Seems Wrong

Symptoms : You see a divergence that "looks good" visually, but CAE blocks with "Adversarial bearish/bullish" warning.

Diagnosis :

Check dashboard Bull Case and Bear Case scores at that moment

Look at Differential value

Check adversarial bar colors — was there strong coloring against your intended direction?

Understanding :

Adversarial catches "obvious" opposing momentum that's easy to miss

Example: Bullish divergence at a local low, BUT price is deeply below EMA50, bearish momentum is strong, and RSI shows knife-catching conditions

Bull Case might be 0.20 while Bear Case is 0.55

Differential = -0.35, far beyond threshold

Block is CORRECT — you'd be fighting overwhelming opposing flow

If You Disagree Consistently

Review blocked signals on chart — scroll back and check outcomes

Did those blocked signals actually work, or did they fail as adversarial predicted?

Raise adv_threshold to 0.15-0.20 (more permissive, allows closer battles)

Disable Adversarial Validation temporarily (diagnostic) to isolate its effect

Use Advisory mode to learn adversarial patterns over 50-100 signals

Remember : Adversarial is conservative BY DESIGN. It prevents "obvious" bad trades where you're fighting strong strength the other way.

Problem: Dashboard Not Showing or Incomplete

Solutions :

Toggle "Show Dashboard" to ON in settings

Try different dashboard sizes (Small/Normal/Large)

Try different positions (Top Left/Right, Bottom Left/Right) — might be off-screen

Some sections require CAE Enable = ON (Cognitive Engine section won't appear if CAE is disabled)

Statistics section requires at least 1 lifetime signal to populate

Check that visual theme is set (dashboard colors adapt to theme)

Problem: Performance Lag, Chart Freezing

Symptoms : Chart loading is slow, indicator calculations cause delays, pinch-to-zoom lags.

Diagnosis : Visual features are computationally expensive, especially adversarial bar coloring (recalculates every bar).

Solutions (In Order of Impact) :

Disable Adversarial Bar Coloring (MOST EXPENSIVE):

Turn OFF "Adversarial Bar Coloring" in settings

This is the single biggest performance drain

Immediate improvement

Reduce Vertical Lines :

Lower "Keep last N vertical lines" to 20-30

Or set to 0 to disable entirely

Moderate improvement

Disable Bifurcation Zones :

Turn OFF "Draw Bifurcation Zones"

Reduces box drawing calculations

Moderate improvement

Set Dashboard Size to Small :

Smaller dashboard = fewer cells = less rendering

Minor improvement

Use Shorter Max Lookback :

Reduce max_lookback to 40-50 (from 60+)

Fewer bars to scan for divergences

Minor improvement

Disable Exhaustion Shading :

Turn OFF "Show Market State"

Removes background coloring calculations

Minor improvement

Extreme Performance Mode :

Disable ALL visual enhancements

Keep only triangle markers

Dashboard Small or OFF

Use Minimal theme if available

Problem: Realtime Signals Repainting

Symptoms : You see a signal appear, but on next bar it disappears or moves.

Explanation :

Realtime mode detects peaks 1 bar ago: high > high AND high > high

On the FORMING bar (before close), this condition can change as new prices arrive

Example: At 10:05, high (10:04 bar) was 100, current high is 99 → peak detected

At 10:05:30, new high of 101 arrives → peak condition breaks → signal disappears

At 10:06 (bar close), final high is 101 → no peak at 10:04 anymore → signal gone permanently

This is expected behavior for realtime responsiveness. You get preview/early warning, but it's not locked until bar confirms.

Solutions :

Use Confirmed Timing :

Switch to "Confirmed (lookforward)" mode

ZERO repainting — pivot must be fully validated

5-bar delay (pivot_lookforward)

What you see in history is exactly what would have appeared live

Accept Realtime Repaint as Tradeoff :

Keep Realtime mode for speed and alerts

Understand that pre-confirmation signals may vanish

Only trade signals that CONFIRM at bar close (check barstate.isconfirmed)

Use for live monitoring, NOT for backtesting

Trade Only After Confirmation :

In Realtime mode, wait 1 full bar after signal appears before entering

If signal survives that bar close, it's locked

This adds 1-bar delay but removes repaint risk

Recommendation : Use Confirmed for backtesting and conservative trading. Use Realtime only for active monitoring with full understanding of preview behavior.

Risk Management Integration

BZ-CAE is a signal generation system, not a complete trading strategy. You must integrate proper risk management:

Position Sizing by Confidence

Confidence 0.70-1.00 (Premium) :

Risk: 1.5-2.0% of account (MAXIMUM)

Reasoning: High-quality setup across all factors

Still cap at 2% — even premium setups can fail

Confidence 0.50-0.70 (High Quality) :

Risk: 1.0-1.5% of account

Reasoning: Standard good setup

Your bread-and-butter risk level

Confidence 0.35-0.50 (Moderate Quality) :

Risk: 0.5-1.0% of account

Reasoning: Marginal setup, passes minimum threshold

Reduce size or skip if you're selective

Confidence <0.35 (Low Quality) :

Risk: 0% (blocked in Filtering mode)

Reasoning: Insufficient quality factors

System protects you by not showing these

Stop Placement Strategies

For Reversal Signals (Regular Divergences) :

Place stop beyond the divergence pivot plus buffer

Bullish : Stop below the divergence low - 1.0-1.5 × ATR

Bearish : Stop above the divergence high + 1.0-1.5 × ATR

Reasoning: If price breaks the pivot, divergence structure is invalidated

For Continuation Signals (Hidden Divergences) :

Place stop beyond recent swing in opposite direction

Bullish continuation : Stop below recent swing low (not the divergence pivot itself)

Bearish continuation : Stop above recent swing high

Reasoning: You're trading with trend, allow more breathing room

ATR-Based Stops :

1.5-2.0 × ATR is standard

Scale by timeframe:

Scalping (1-5m): 1.0-1.5 × ATR (tight)

Day trading (15m-1H): 1.5-2.0 × ATR (balanced)

Swing (4H-D): 2.0-3.0 × ATR (wide)

Never Use Fixed Dollar/Pip Stops :

Markets have different volatility

50-pip stop on EUR/USD ≠ 50-pip stop on GBP/JPY

Always normalize by ATR or pivot structure

Profit Targets and Scaling

Primary Target :

2-3 × ATR from entry (minimum 2:1 reward-risk)

Example : Entry at 100, ATR = 2, stop at 97 (1.5 × ATR) → target at 106 (3 × ATR) = 2:1 R:R

Scaling Out Strategy :

Take 50% off at 1.5 × ATR (secure partial profit)

Move stop to breakeven

Trail remaining 50% with 1.0 × ATR trailing stop

Let winners run if trend persists

Targets by Confidence :

High Confidence (>0.70) : Aggressive targets (3-4 × ATR), trail wider (1.5 × ATR)

Standard Confidence (0.50-0.70) : Normal targets (2-3 × ATR), standard trail (1.0 × ATR)

Low Confidence (0.35-0.50) : Conservative targets (1.5-2 × ATR), tight trail (0.75 × ATR)

Use Bifurcation Zones :

If opposite-side zone is visible on chart (from previous signal), use it as target

Example : Bullish signal at 100, prior supply zone at 110 → use 110 as target

Zones mark institutional resistance/support

Exhaustion-Based Exits :

If you're in a trade and exhaustion >0.75 develops (yellow shading), consider early exit

Market is overextended — reversal risk is high

Take profit even if target not reached

Trade Management by TCS

High TCS + Counter-Trend Trade (Risky) :

Use very tight stops (1.0-1.5 × ATR)

Conservative targets (1.5-2 × ATR)

Quick exit if trade doesn't work immediately

You're fading momentum — respect it

Low TCS + Reversal Trade (Safer) :

Use wider stops (2.0-2.5 × ATR)

Aggressive targets (3-4 × ATR)

Trail with patience

Genuine reversal potential in weak trend

High TCS + Continuation Trade (Safest) :

Standard stops (1.5-2.0 × ATR)

Very aggressive targets (4-5 × ATR)

Trail wide (1.5-2.0 × ATR)

You're with institutional momentum — let it run

Educational Value — Learning Machine Intelligence

BZ-CAE is designed as a learning platform, not just a tool:

Advisory Mode as Teacher

Most indicators are binary: signal or no signal. You don't learn WHY certain setups are better.

BZ-CAE's Advisory mode shows you EVERY potential divergence, then annotates the ones that would be blocked in Filtering mode with specific reasons:

"Bull: strong downtrend (TCS=0.87)" teaches you that TCS >0.85 makes counter-trend very risky

"Adversarial bearish" teaches you that the opposing case was dominating

"Low confidence 32%" teaches you that the setup lacked quality across multiple factors

"Bull spacing: wait 8 bars" teaches you that signals need breathing room

After 50-100 signals in Advisory mode, you internalize the CAE's decision logic. You start seeing these factors yourself BEFORE the indicator does.

Dashboard Transparency

Most "intelligent" indicators are black boxes — you don't know how they make decisions.

BZ-CAE shows you ALL metrics in real-time:

TCS tells you trend strength

DMA tells you momentum alignment

Exhaustion tells you overextension

Adversarial shows both sides of the debate

Confidence shows composite quality

You learn to interpret market state holistically, a skill applicable to ANY trading system beyond this indicator.

Divergence Quality Education

Not all divergences are equal. BZ-CAE teaches you which conditions produce high-probability setups:

Quality divergence : Regular bullish div at a low, TCS <0.50 (weak trend), exhaustion >0.75 (overextended), positive adversarial differential, confidence >0.70

Low-quality divergence : Regular bearish div at a high, TCS >0.85 (strong uptrend), exhaustion <0.30 (not overextended), negative adversarial differential, confidence <0.40

After using the system, you can evaluate divergences manually with similar intelligence.

Risk Management Discipline

Confidence-based position sizing teaches you to adjust risk based on setup quality, not emotions:

Beginners often size all trades identically

Or worse, size UP on marginal setups to "make up" for losses

BZ-CAE forces systematic sizing: premium setups get larger size, marginal setups get smaller size

This creates a probabilistic approach where your edge compounds over time.

What This Indicator Is NOT

Complete transparency about limitations and positioning:

Not a Prediction System