Combo Strategy 123 Reversal and ADXR This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Secon strategy

The Average Directional Movement Index Rating (ADXR) measures the strength

of the Average Directional Movement Index (ADX). It's calculated by taking

the average of the current ADX and the ADX from one time period before

(time periods can vary, but the most typical period used is 14 days).

Like the ADX, the ADXR ranges from values of 0 to 100 and reflects strengthening

and weakening trends. However, because it represents an average of ADX, values

don't fluctuate as dramatically and some analysts believe the indicator helps

better display trends in volatile markets.

WARNING:

- For purpose educate only

- This script to change bars colors.

ค้นหาในสคริปต์สำหรับ "the strat"

Combo Backtest 123 Reversal and Accelerator Oscillator (AC) This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Accelerator Oscillator has been developed by Bill Williams

as the development of the Awesome Oscillator. It represents the

difference between the Awesome Oscillator and the 5-period moving

average, and as such it shows the speed of change of the Awesome

Oscillator, which can be useful to find trend reversals before the

Awesome Oscillator does.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategies 123 Reversal and Accelerator Oscillator (AC) This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Accelerator Oscillator has been developed by Bill Williams

as the development of the Awesome Oscillator. It represents the

difference between the Awesome Oscillator and the 5-period moving

average, and as such it shows the speed of change of the Awesome

Oscillator, which can be useful to find trend reversals before the

Awesome Oscillator does.

WARNING:

- This script to change bars colors.

Combo Backtest 123 Reversal and Absolute Price Oscillator (APO) This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Secon strategy

The Absolute Price Oscillator displays the difference between two exponential

moving averages of a security's price and is expressed as an absolute value.

How this indicator works

APO crossing above zero is considered bullish, while crossing below zero is bearish.

A positive indicator value indicates an upward movement, while negative readings

signal a downward trend.

Divergences form when a new high or low in price is not confirmed by the Absolute Price

Oscillator (APO). A bullish divergence forms when price make a lower low, but the APO

forms a higher low. This indicates less downward momentum that could foreshadow a bullish

reversal. A bearish divergence forms when price makes a higher high, but the APO forms a

lower high. This shows less upward momentum that could foreshadow a bearish reversal.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategies 123 Reversal and Absolute Price Oscillator This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Secon strategy

The Absolute Price Oscillator displays the difference between two exponential

moving averages of a security's price and is expressed as an absolute value.

How this indicator works

APO crossing above zero is considered bullish, while crossing below zero is bearish.

A positive indicator value indicates an upward movement, while negative readings

signal a downward trend.

Divergences form when a new high or low in price is not confirmed by the Absolute Price

Oscillator (APO). A bullish divergence forms when price make a lower low, but the APO

forms a higher low. This indicates less downward momentum that could foreshadow a bullish

reversal. A bearish divergence forms when price makes a higher high, but the APO forms a

lower high. This shows less upward momentum that could foreshadow a bearish reversal.

WARNING:

- This script to change bars colors.

Combo Strategies 123 Reversal and 3-Bar-Reversal-Pattern This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Secon strategy

This startegy based on 3-day pattern reversal described in "Are Three-Bar

Patterns Reliable For Stocks" article by Thomas Bulkowski, presented in

January,2000 issue of Stocks&Commodities magazine.

That pattern conforms to the following rules:

- It uses daily prices, not intraday or weekly prices;

- The middle day of the three-day pattern has the lowest low of the three days, with no ties allowed;

- The last day must have a close above the prior day's high, with no ties allowed;

- Each day must have a nonzero trading range.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategies 123 Reversal and 3-Bar-Reversal-Pattern This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Secon strategy

This startegy based on 3-day pattern reversal described in "Are Three-Bar

Patterns Reliable For Stocks" article by Thomas Bulkowski, presented in

January,2000 issue of Stocks&Commodities magazine.

That pattern conforms to the following rules:

- It uses daily prices, not intraday or weekly prices;

- The middle day of the three-day pattern has the lowest low of the three days, with no ties allowed;

- The last day must have a close above the prior day's high, with no ties allowed;

- Each day must have a nonzero trading range.

WARNING:

- This script to change bars colors.

Combo Backtest 123 Reversal and 2/20 EMA This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Secon strategy

This indicator plots 2/20 exponential moving average. For the Mov

Avg X 2/20 Indicator, the EMA bar will be painted when the Alert criteria is met.

Please, use it only for learning or paper trading. Do not for real trading.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategies 123 Reversal and 2/20 EMA This is combo strategies for get

a cumulative signal. Result signal will return 1 if two strategies

is long, -1 if all strategies is short and 0 if signals of strategies is not equal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Secon strategy

This indicator plots 2/20 exponential moving average. For the Mov

Avg X 2/20 Indicator, the EMA bar will be painted when the Alert criteria is met.

Please, use it only for learning or paper trading. Do not for real trading.

XPloRR MA-Trailing-Stop StrategyXPloRR MA-Trailing-Stop Strategy

Long term MA-Trailing-Stop strategy with Adjustable Signal Strength to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the fast buy EMA (blue) crossing over the slow buy SMA curve (orange) and the fast buy EMA has a certain up strength.

My sell strategy is triggered by either one of these conditions:

the EMA(6) of the close value is crossing under the trailing stop value (green) or

the fast sell EMA (navy) is crossing under the slow sell SMA curve (red) and the fast sell EMA has a certain down strength.

The trailing stop value (green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between the high and low values.

The scripts shows a lot of graphical information:

The close value is shown in light-green. When the close value is lower then the buy value, the close value is shown in light-red. This way it is possible to evaluate the virtual losses during the trade.

the trailing stop value is shown in dark-green. When the sell value is lower then the buy value, the last color of the trade will be red (best viewed when zoomed)(in the example, there are 2 trades that end in gain and 2 in loss (red line at end))

the EMA and SMA values for both buy and sell signals are shown as a line

the buy and sell(close) signals are labeled in blue

How to use this strategy?

Every stock has it's own "DNA", so first thing to do is tune the right parameters to get the best strategy values voor EMA , SMA, Strength for both buy and sell and the Trailing Stop (#ATR).

Look in the strategy tester overview to optimize the values Percent Profitable and Net Profit (using the strategy settings icon, you can increase/decrease the parameters)

Then keep using these parameters for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Important : optimizing these parameters is no guarantee for future winning trades!

Here are the parameters:

Fast EMA Buy: buy trigger when Fast EMA Buy crosses over the Slow SMA Buy value (use values between 10-20)

Slow SMA Buy: buy trigger when Fast EMA Buy crosses over the Slow SMA Buy value (use values between 30-100)

Minimum Buy Strength: minimum upward trend value of the Fast SMA Buy value (directional coefficient)(use values between 0-120)

Fast EMA Sell: sell trigger when Fast EMA Sell crosses under the Slow SMA Sell value (use values between 10-20)

Slow SMA Sell: sell trigger when Fast EMA Sell crosses under the Slow SMA Sell value (use values between 30-100)

Minimum Sell Strength: minimum downward trend value of the Fast SMA Sell value (directional coefficient)(use values between 0-120)

Trailing Stop (#ATR): the trailing stop value as a multiple of the ATR(15) value (use values between 2-20)

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now) compared to the Buy&Hold Strategy(=do nothing):

BEKB(Bekaert): EMA-Buy=12, SMA-Buy=44, Strength-Buy=65, EMA-Sell=12, SMA-Sell=55, Strength-Sell=120, Stop#ATR=20

NetProfit: 996%, #Trades: 6, %Profitable: 83%, Buy&HoldProfit: 78%

BAR(Barco): EMA-Buy=16, SMA-Buy=80, Strength-Buy=44, EMA-Sell=12, SMA-Sell=45, Strength-Sell=82, Stop#ATR=9

NetProfit: 385%, #Trades: 7, %Profitable: 71%, Buy&HoldProfit: 55%

AAPL(Apple): EMA-Buy=12, SMA-Buy=45, Strength-Buy=40, EMA-Sell=19, SMA-Sell=45, Strength-Sell=106, Stop#ATR=8

NetProfit: 6900%, #Trades: 7, %Profitable: 71%, Buy&HoldProfit: 2938%

TNET(Telenet): EMA-Buy=12, SMA-Buy=45, Strength-Buy=27, EMA-Sell=19, SMA-Sell=45, Strength-Sell=70, Stop#ATR=14

NetProfit: 129%, #Trade

XPloRR MA-Buy ATR-Trailing-Stop Long Term Strategy Beating B&HXPloRR MA-Buy ATR-MA-Trailing-Stop Strategy

Long term MA Trailing Stop strategy to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the EMA(blue) crossing over the SMA curve(orange).

My sell strategy is triggered by another EMA(lime) of the close value crossing the trailing stop(green) value.

The trailing stop value(green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between high and low values.

Every stock has it's own "DNA", so first thing to do is find the right parameters to get the best strategy values voor EMA, SMA and Trailing Stop.

Then keep using these parameter for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Here are the parameters:

Exponential MA: buy trigger when crossing over the SMA value (use values between 11-50)

Simple MA: buy trigger when EMA crosses over the SMA value (use values between 20 and 200)

Stop EMA: sell trigger when Stop EMA of close value crosses under the trailing stop value (use values between 8 and 16)

Trailing Stop #ATR: defines the trailing stop value as a multiple of the ATR(15) value

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now):

BAR(Barco): EMA=11, SMA=82, StopEMA=12, Stop#ATR=9

Buy&HoldProfit: 45.82%, NetProfit: 294.7%, #Trades:8, %Profit:62.5%, ProfitFactor: 12.539

AAPL(Apple): EMA=12, SMA=45, StopEMA=12, Stop#ATR=6

Buy&HoldProfit: 2925.86%, NetProfit: 4035.92%, #Trades:10, %Profit:60%, ProfitFactor: 6.36

BEKB(Bekaert): EMA=12, SMA=42, StopEMA=12, Stop#ATR=7

Buy&HoldProfit: 81.11%, NetProfit: 521.37%, #Trades:10, %Profit:60%, ProfitFactor: 2.617

SOLB(Solvay): EMA=12, SMA=63, StopEMA=11, Stop#ATR=8

Buy&HoldProfit: 43.61%, NetProfit: 151.4%, #Trades:8, %Profit:75%, ProfitFactor: 3.794

PHIA(Philips): EMA=11, SMA=80, StopEMA=8, Stop#ATR=10

Buy&HoldProfit: 56.79%, NetProfit: 198.46%, #Trades:6, %Profit:83.33%, ProfitFactor: 23.07

I am very curious to see the parameters for your stocks and please make suggestions to improve this strategy.

Alpha - Multi-Asset Adaptive Trading Strategy# Alpha - Multi-Asset Adaptive Trading Strategy

Overview

Alpha is a comprehensive trading strategy that combines multiple technical analysis components with pre-optimized settings for over 70 different trading instruments across cryptocurrencies, forex, and stocks. The strategy employs an adaptive approach using modified trend detection algorithms, dynamic support/resistance zones, and multi-timeframe confirmation.

Key Features & Originality

1. Adaptive Trend Detection System

- Modified trend-following algorithm with amplitude-based channel deviation

- Dynamic channel width adjustment based on ATR (Average True Range)

- Dual-layer trend confirmation using both price action and momentum indicators

2. Pre-Configured Asset Optimization

The strategy includes carefully backtested parameter sets for:

- **Cryptocurrencies**: BTC, ETH, and 40+ altcoin pairs

- **Forex Pairs**: Major and minor currency pairs

- **Stocks**: TSLA, AAPL, GOOG

- **Commodities**: Gold, Silver, Platinum

- Each configuration is optimized for specific timeframes (5m, 15m, 30m, 45m, 1h)

3. Advanced Risk Management

- Multiple take profit levels (4 targets with customizable position sizing)

- Dynamic stop-loss options (ATR-based or percentage-based)

- Position size allocation across profit targets (default: 30%, 30%, 30%, 10%)

4. Multi-Timeframe Analysis Dashboard

- Real-time analysis across 4 configurable timeframes

- Comprehensive performance metrics display

- Visual representation of current market conditions

5. Market Condition Filtering

- RSI-based trend strength filtering

- ATR-based volatility filtering

- Sideways market detection to avoid choppy conditions

- Customizable filter combinations (ATR only, RSI only, both, or disabled)

How to Use

Initial Setup

1. **Select Asset Configuration**: Choose your trading pair from the "Strategies" dropdown menu

2. **Enable Strategy**: Enter "Alpha" in the code confirmation field

3. **Adjust Timeframe**: Match your chart timeframe to the selected strategy configuration

Parameter Customization

- **Trendline Settings**: Adjust amplitude and channel deviation for sensitivity

- **TP/SL Method**: Choose between ATR-based or percentage-based targets

- **Filtering Options**: Select appropriate market filters for your trading style

- **Backtest Period**: Set the number of days for strategy testing (max 60)

Signal Interpretation

- **BUY/SELL Labels**: Primary entry signals based on trend changes

- **Support/Resistance Zones**: Visual zones showing key price levels

- **Dashboard**: Real-time display of position status, targets, and performance metrics

Important Considerations

Limitations and Warnings

- **Backtesting Period**: Results shown are based on historical data from the specified backtest period

- **No Guarantee**: Past performance does not guarantee future results

- **Market Conditions**: Strategy performance varies with market volatility and trending conditions

- **Repainting**: Some signals may repaint if "Wait For Confirmed Bar" is disabled

Risk Warnings

- The pre-configured settings are starting points and may require adjustment for current market conditions

- Always use appropriate position sizing and risk management

- Test thoroughly on demo accounts before live trading

- Monitor and adjust parameters regularly as market dynamics change

Technical Components

Core Indicators Used

- Modified trend detection with amplitude-based channels

- RSI (Relative Strength Index) for momentum confirmation

- ATR (Average True Range) for volatility measurement

- Support/Resistance detection using pivot points

- Bollinger Band variant for trend confirmation

Alert Functionality

The strategy includes comprehensive alert options for:

- Entry signals (long and short)

- Take profit levels (TP1, TP2, TP3, TP4)

- Stop loss triggers

- Integration with trading bots via webhook messages

Recommended Usage

Best Practices

1. Start with the pre-configured settings for your chosen asset

2. Run backtests over different time periods to verify performance

3. Use the dashboard to monitor real-time strategy performance

4. Adjust filters based on current market conditions

5. Always use stop losses and proper risk management

Timeframe Recommendations

- **Short-Term**: Use 5m, 15m configurations for scalping

- **Mid-Term**: Use 30m, 45m configurations for day trading

- **Long-Term**: Use 1h configurations for swing trading

Updates and Support

The strategy parameters are regularly reviewed and optimized. Users should periodically check for updates to ensure they have the latest configurations.

Disclaimer

This strategy is for educational and informational purposes only. Trading involves substantial risk of loss. Users should conduct their own research and consider their financial situation before trading. The author is not responsible for any trading losses incurred using this strategy.

BOCS Channel Scalper Indicator - Mean Reversion Alert System# BOCS Channel Scalper Indicator - Mean Reversion Alert System

## WHAT THIS INDICATOR DOES:

This is a mean reversion trading indicator that identifies consolidation channels through volatility analysis and generates alert signals when price enters entry zones near channel boundaries. **This indicator version is designed for manual trading with comprehensive alert functionality.** Unlike automated strategies, this tool sends notifications (via popup, email, SMS, or webhook) when trading opportunities occur, allowing you to manually review and execute trades. The system assumes price will revert to the channel mean, identifying scalp opportunities as price reaches extremes and preparing to bounce back toward center.

## INDICATOR VS STRATEGY - KEY DISTINCTION:

**This is an INDICATOR with alerts, not an automated strategy.** It does not execute trades automatically. Instead, it:

- Displays visual signals on your chart when entry conditions are met

- Sends customizable alerts to your device/email when opportunities arise

- Shows TP/SL levels for reference but does not place orders

- Requires you to manually enter and exit positions based on signals

- Works with all TradingView subscription levels (alerts included on all plans)

**For automated trading with backtesting**, use the strategy version. For manual control with notifications, use this indicator version.

## ALERT CAPABILITIES:

This indicator includes four distinct alert conditions that can be configured independently:

**1. New Channel Formation Alert**

- Triggers when a fresh BOCS channel is identified

- Message: "New BOCS channel formed - potential scalp setup ready"

- Use this to prepare for upcoming trading opportunities

**2. Long Scalp Entry Alert**

- Fires when price touches the long entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "LONG scalp signal at 24731.75 | TP: 24743.2 | SL: 24716.5"

**3. Short Scalp Entry Alert**

- Fires when price touches the short entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "SHORT scalp signal at 24747.50 | TP: 24735.0 | SL: 24762.75"

**4. Any Entry Signal Alert**

- Combined alert for both long and short entries

- Use this if you want a single alert stream for all opportunities

- Message: "BOCS Scalp Entry: at "

**Setting Up Alerts:**

1. Add indicator to chart and configure settings

2. Click the Alert (⏰) button in TradingView toolbar

3. Select "BOCS Channel Scalper" from condition dropdown

4. Choose desired alert type (Long, Short, Any, or Channel Formation)

5. Set "Once Per Bar Close" to avoid false signals during bar formation

6. Configure delivery method (popup, email, webhook for automation platforms)

7. Save alert - it will fire automatically when conditions are met

**Alert Message Placeholders:**

Alerts use TradingView's dynamic placeholder system:

- {{ticker}} = Symbol name (e.g., NQ1!)

- {{close}} = Current price at signal

- {{plot_1}} = Calculated take profit level

- {{plot_2}} = Calculated stop loss level

These placeholders populate automatically, creating detailed notification messages without manual configuration.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This indicator is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Indicator**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the indicator ideal for active day traders who want continuous alert opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased signal frequency also means higher potential commission costs and requires disciplined trade selection when acting on alerts.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The indicator normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The indicator uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The indicator tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The indicator uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. Visual markers (arrows and labels) appear on chart, and configured alerts fire immediately.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents alert spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long alert will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The indicator includes a multi-timeframe ATR filter to avoid alerts during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while viewing 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Alerts enabled

- If ATR < threshold: No alerts fire

This prevents notifications during dead zones where mean reversion is unreliable due to insufficient price movement. The ATR status is displayed in the info table with visual confirmation (✓ or ✗).

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. These levels are displayed as visual lines with labels and included in alert messages for reference when manually placing orders.

### Stop Loss Placement:

Stop losses are calculated just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. SL levels are displayed on chart and included in alert notifications as suggested stop placement.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

## INPUT PARAMETERS:

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long alert generation on/off

- **Enable Short Scalps**: Toggle short alert generation on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between alerts (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for alert enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time indicator status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Long Color**: Customize long signal color (default: darker green for readability)

- **Short Color**: Customize short signal color (default: red)

- **TP/SL Colors**: Customize take profit and stop loss line colors

- **Line Length**: Visual length of TP/SL reference lines (5-200 bars)

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short alerts

- **TP/SL reference lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing channel status, last signal, entry/TP/SL prices, risk/reward ratio, and ATR filter status

- **Visual confirmation** when alerts fire via on-chart markers synchronized with notifications

## HOW TO USE:

### For 1-3 Minute Scalping with Alerts (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars to reduce alert spam

- **Alert Setup**: Configure "Any Entry Signal" for combined long/short notifications

- **Execution**: When alert fires, verify chart visuals, then manually place limit order at entry zone with provided TP/SL levels

### For 5-15 Minute Day Trading with Alerts:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- **Alert Setup**: Configure separate "Long Scalp Entry" and "Short Scalp Entry" alerts if you trade directionally based on bias

- **Execution**: Review channel structure on alert, confirm ATR filter shows ✓, then enter manually

### For 30-60 Minute Swing Scalping with Alerts:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- **Alert Setup**: Use "New Channel Formation" to prepare for setups, then "Any Entry Signal" for execution alerts

- **Execution**: Larger timeframes allow more analysis time between alert and entry

### Webhook Integration for Semi-Automation:

- Configure alert webhook URL to connect with platforms like TradersPost, TradingView Paper Trading, or custom automation

- Alert message includes all necessary order parameters (direction, entry, TP, SL)

- Webhook receives structured data when signal fires

- External platform can auto-execute based on alert payload

- Still maintains manual oversight vs full strategy automation

## USAGE CONSIDERATIONS:

- **Manual Discipline Required**: Alerts provide opportunities but execution requires judgment. Not all alerts should be taken - consider market context, trend, and channel quality

- **Alert Timing**: Alerts fire on bar close by default. Ensure "Once Per Bar Close" is selected to avoid false signals during bar formation

- **Notification Delivery**: Mobile/email alerts may have 1-3 second delay. For immediate execution, use desktop popups or webhook automation

- **Cooldown Necessity**: Without cooldown, rapidly touching price action can generate excessive alerts. Start with 3-bar cooldown and adjust based on alert volume

- **ATR Filter Impact**: Enabling ATR filter dramatically reduces alert count but improves quality. Track filter status in info table to understand when you're receiving fewer alerts

- **Commission Awareness**: High alert frequency means high potential trade count. Calculate if your commission structure supports frequent scalping before acting on all alerts

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features are not included in this indicator version. Multi-timeframe ATR requires higher-tier TradingView subscription for request.security() functionality on timeframes below chart timeframe.

## KNOWN LIMITATIONS:

- **Indicator does not execute trades** - alerts are informational only; you must manually place all orders

- **Alert delivery depends on TradingView infrastructure** - delays or failures possible during platform issues

- **No position tracking** - indicator doesn't know if you're in a trade; you must manage open positions independently

- **TP/SL levels are reference only** - you must manually set these on your broker platform; they are not live orders

- **Immediate touch entry can generate many alerts** in choppy zones without adequate cooldown

- **Channel deletion at 10-tick breaks** may be too aggressive or lenient depending on instrument tick size

- **ATR filter from lower timeframes** requires TradingView Premium/Pro+ for request.security()

- **Mean reversion logic fails** in strong breakout scenarios - alerts will fire but trades may hit stops

- **No partial closing capability** - full position management is manual; you determine scaling out

- **Alerts do not account for gaps** or overnight price changes; morning alerts may be stale

## RISK DISCLOSURE:

Trading involves substantial risk of loss. This indicator provides signals for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Mean reversion strategies can experience extended drawdowns during trending markets. Alerts are not guaranteed to be profitable and should be combined with your own analysis. Stop losses may not fill at intended levels during extreme volatility or gaps. Never trade with capital you cannot afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Always verify alerts against current market conditions before executing trades manually.

## ACKNOWLEDGMENT & CREDITS:

This indicator is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based alert generation, comprehensive alert condition system with customizable notifications, multi-timeframe ATR volatility filtering, cooldown period for alert management, dual TP methods (fixed points vs channel percentage), visual TP/SL reference lines, and real-time status monitoring table. This indicator version is specifically designed for manual traders who prefer alert-based decision making over automated execution.

Extremum Range MA Crossover Strategy1. Principle of Work & Strategy Logic ⚙️📈

Main idea: The strategy tries to catch the moment of a breakout from a price consolidation range (flat) and the start of a new trend. It combines two key elements:

Moving Average (MA) 📉: Acts as a dynamic support/resistance level and trend filter.

Range Extremes (Range High/Low) 🔺🔻: Define the borders of the recent price channel or consolidation.

The strategy does not attempt to catch absolute tops and bottoms. Instead, it enters an already formed move after the breakout, expecting continuation.

Type: Trend-following, momentum-based.

Timeframes: Works on different TFs (H1, H4, D), but best suited for H4 and higher, where breakouts are more meaningful.

2. Justification of Indicators & Settings ⚙️

A. Moving Average (MA) 📊

Why used: Core of the strategy. It smooths price fluctuations and helps define the trend. The price (via extremes) must cross the MA → signals a potential trend shift or strengthening.

Parameters:

maLength = 20: Default length (≈ one trading month, 20-21 days). Good balance between sensitivity & smoothing.

Lower TF → reduce (10–14).

Higher TF → increase (50).

maSource: Defines price source (default = Close). Alternatives (HL2, HLC3) → smoother, less noisy MA.

maType: Default = EMA (Exponential MA).

Why EMA? Faster reaction to recent price changes vs SMA → useful for breakout strategies.

Other options:

SMA 🟦 – classic, slowest.

WMA 🟨 – weights recent data stronger.

HMA 🟩 – near-zero lag, but “nervous,” more false signals.

DEMA/TEMA 🟧 – even faster & more sensitive than EMA.

VWMA 🔊 – volume-weighted.

ZLEMA ⏱ – reduced lag.

👉 Choice = tradeoff between speed of reaction & false signals.

B. Range Extremes (Previous High/Low) 📏

Why used: Define borders of recent trading range.

prevHigh = local resistance.

prevLow = local support.

Break of these levels on close = trigger.

Parameters:

lookbackPeriod = 5: Searches for highest high / lowest low of last 5 candles. Very recent range.

Higher value (10–20) → wider, stronger ranges but rarer signals.

3. Entry & Exit Rules 🎯

Long signals (BUY) 🟢📈

Condition (longCondition): Previous Low crosses MA from below upwards.

→ Price bounced from the bottom & strong enough to push range border above MA.

Execution: Auto-close short (if any) → open long.

Short signals (SELL) 🔴📉

Condition (shortCondition): Previous High crosses MA from above downwards.

→ Price rejected from the top, upper border failed above MA.

Execution: Auto-close long (if any) → open short.

Exit conditions 🚪

Exit Long (exitLongCondition): Close below prevLow.

→ Uptrend likely ended, range shifts down.

Exit Short (exitShortCondition): Close above prevHigh.

→ Downtrend likely ended, range shifts up.

⚠️ Important: Exit = only on candle close beyond extremes (not just wick).

4. Trading Settings ⚒️

overlay = true → indicators shown on chart.

initial_capital = 10000 💵.

default_qty_type = strategy.cash, default_qty_value = 100 → trades fixed $100 per order (not lots). Can switch to % of equity.

commission_type = strategy.commission.percent, commission_value = 0.1 → default broker fee = 0.1%. Adjust for your broker!

slippage = 3 → slippage = 3 ticks. Adjust to asset liquidity.

currency = USD.

margin_long = 100, margin_short = 100 → no leverage (100% margin).

5. Visualization on Chart 📊

The strategy draws 3 lines:

🔵 MA line (thickness 2).

🔴 Previous High (last N candles).

🟢 Previous Low (last N candles).

Also: entry/exit arrows & equity curve shown in backtest.

Disclaimer ⚠️📌

Risk Warning: This description & code are for educational purposes only. Not financial advice. Trading (Forex, Stocks, Crypto) carries high risk and may lead to full capital loss. You trade at your own risk.

Testing: Always backtest & demo test first. Past results ≠ future profits.

Responsibility: Author of this strategy & description is not responsible for your trading decisions or losses.

Hazel nut BB Strategy, volume base- lite versionHazel nut BB Strategy, volume base — lite version

Having knowledge and information in financial markets is only useful when a trader operates with a well-defined trading strategy. Trading strategies assist in capital management, profit-taking, and reducing potential losses.

This strategy is built upon the core principle of supply and demand dynamics. Alongside this foundation, one of the widely used technical tools — the Bollinger Bands — is employed to structure a framework for profit management and risk control.

In this strategy, the interaction of these tools is explained in detail. A key point to note is that for calculating buy and sell volumes, a lower timeframe function is used. When applied with a tick-level resolution, this provides the most precise measurement of buyer/seller flows. However, this comes with a limitation of reduced historical depth. Users should be aware of this trade-off: if precise tick-level data is required, shorter timeframes should be considered to extend historical coverage .

The strategy offers multiple configuration options. Nevertheless, it should be treated strictly as a supportive tool rather than a standalone trading system. Decisions must integrate personal analysis and other instruments. For example, in highly volatile assets with narrow ranges, it is recommended to adjust profit-taking and stop-loss percentages to smaller values.

◉ Volume Settings

• Buyer and seller volume (up/down volume) are requested from a lower timeframe, with an option to override the automatic resolution.

• A global lookback period is applied to calculate moving averages and cumulative sums of buy/sell/delta volumes.

• Ratios of buyers/sellers to total volume are derived both on the current bar and across the lookback window.

◉ Bollinger Band

• Bands are computed using configurable moving averages (SMA, EMA, RMA, WMA, VWMA).

• Inputs allow control of length, standard deviation multiplier, and offset.

• The basis, upper, and lower bands are plotted, with a shaded background between them.

◉ Progress & Proximity

• Relative position of the price to the Bollinger basis is expressed as percentages (qPlus/qMinus).

• “Near band” conditions are triggered when price progress toward the upper or lower band exceeds a user-defined threshold (%).

• A signed score (sScore) represents how far the close has moved above or below the basis relative to band width.

◉ Info Table

• Optional compact table summarizing:

• - Upper/lower band margins

• - Buyer/seller volumes with moving averages

• - Delta and cumulative delta

• - Buyer/seller ratios per bar and across the window

• - Money flow values (buy/sell/delta × price) for bar-level and summed periods

• The table is neutral-colored and resizable for different chart layouts.

◉ Zone Event Gate

• Tracks entry into and exit from “near band” zones.

• Arming logic: a side is armed when price enters a band proximity zone.

• Trigger logic: on exit, a trade event is generated if cumulative buyer or seller volume dominates over a configurable window.

◉ Trading Logic

• Orders are placed only on zone-exit events, conditional on volume dominance.

• Position sizing is defined as a fixed percentage of strategy equity.

• Long entries occur when leaving the lower zone with buyer dominance; short entries occur when leaving the upper zone with seller dominance.

◉ Exit Rules

• Open positions are managed by a strict priority sequence:

• 1. Stop-loss (% of entry price)

• 2. Take-profit (% of entry price)

• 3. Opposite-side event (zone exit with dominance in the other direction)

• Stop-loss and take-profit levels are configurable

◉ Notes

• This lite version is intended to demonstrate the interaction of Bollinger Bands and volume-based dominance logic.

• It provides a framework to observe how price reacts at band boundaries under varying buy/sell pressure, and how zone exits can be systematically converted into entry/exit signals.

When configuring this strategy, it is essential to carefully review the settings within the Strategy Tester. Ensure that the chosen parameters and historical data options are correctly aligned with the intended use. Accurate back testing depends on applying proper configurations for historical reference. The figure below illustrates sample result and configuration type.

Strat Failed 2-Up/2-Down Scanner v2**Strat Failed 2-Up/2-Down Scanner**

The Strat Failed 2-Up/2-Down Scanner is designed for traders using The Strat methodology, developed by Rob Smith, to identify key reversal patterns in any market and timeframe. This indicator detects two specific candlestick patterns: Failed 2-Up (bearish) and Failed 2-Down (bullish), which signal potential reversals when a directional move fails to follow through.

**What It Does**

- **Failed 2-Up**: Identifies a bearish candle where the low and high are higher than the previous candle’s low and high, but the close is below the open, indicating a failed attempt to continue an uptrend. These are marked with a red candlestick, a red downward triangle above the bar, and a table entry.

- **Failed 2-Down**: Identifies a bullish candle where the high and low are lower than the previous candle’s high and low, but the close is above the open, signaling a failed downtrend. These are marked with a green candlestick, a green upward triangle below the bar, and a table entry.

- A table in the top-right corner displays the signal type ("Failed 2-Up" or "Failed 2-Down") and the ticker symbol for quick reference.

- Alerts are provided for both patterns, making the indicator compatible with TradingView’s screener for automated scanning.

**How It Works**

The indicator analyzes each candlestick’s high, low, and close relative to the previous candle:

- Failed 2-Up: `low > low `, `high > high `, `close < open`.

- Failed 2-Down: `high < high `, `low < low `, `close > open`.

When these conditions are met, the indicator applies visual markers (colored bars and triangles) and updates the signal table. Alert conditions trigger notifications for integration with TradingView’s alert system.

**How to Use**

1. Apply the indicator to any chart (stocks, forex, crypto, etc.) on any timeframe (e.g., 1-minute, hourly, daily).

2. Monitor the chart for red (Failed 2-Up) or green (Failed 2-Down) candlesticks with corresponding triangles.

3. Check the top-right table for the latest signal and ticker.

4. Set alerts by selecting “Failed 2-Up Detected” or “Failed 2-Down Detected” in TradingView’s alert menu to receive notifications (e.g., via email or app).

5. Use the signals to identify potential reversal setups in conjunction with other Strat-based analysis, such as swing levels or time-based strategies.

**Originality**

Unlike other Strat indicators that may focus on swing levels or complex candlestick combinations, this scanner specifically targets Failed 2-Up and Failed 2-Down patterns with clear, minimalist visualizations (bars, triangles, table) and robust alert functionality. Its simplicity makes it accessible for both novice and experienced traders using The Strat methodology.

**Ideal For**

Day traders, swing traders, and scalpers looking to capitalize on reversal signals in trending or ranging markets. The indicator is versatile for any asset class and timeframe, enhancing trade decision-making with The Strat’s pattern-based approach.

AltCoin & MemeCoin Index Correlation [Eddie_Bitcoin]🧠 Philosophy of the Strategy

The AltCoin & MemeCoin Index Correlation Strategy by Eddie_Bitcoin is a carefully engineered trend-following system built specifically for the highly volatile and sentiment-driven world of altcoins and memecoins.

This strategy recognizes that crypto markets—especially niche sectors like memecoins—are not only influenced by individual price action but also by the relative strength or weakness of their broader sector. Hence, it attempts to improve the reliability of trading signals by requiring alignment between a specific coin’s trend and its sector-wide index trend.

Rather than treating each crypto asset in isolation, this strategy dynamically incorporates real-time dominance metrics from custom indices (OTHERS.D and MEME.D) and combines them with local price action through dual exponential moving average (EMA) crossovers. Only when both the asset and its sector are moving in the same direction does it allow for trade entries—making it a confluence-based system rather than a single-signal strategy.

It supports risk-aware capital allocation, partial exits, configurable stop loss and take profit levels, and a scalable equity-compounding model.

✅ Why did I choose OTHERS.D and MEME.D as reference indices?

I selected OTHERS.D and MEME.D because they offer a sector-focused view of crypto market dynamics, especially relevant when trading altcoins and memecoins.

🔹 OTHERS.D tracks the market dominance of all cryptocurrencies outside the top 10 by market cap.

This excludes not only BTC and ETH, but also major stablecoins like USDT and USDC, making it a cleaner indicator of risk appetite across true altcoins.

🔹 This is particularly useful for detecting "Altcoin Season"—periods where capital rotates away from Bitcoin and flows into smaller-cap coins.

A rising OTHERS.D often signals the start of broader altcoin rallies.

🔹 MEME.D, on the other hand, captures the speculative behavior of memecoin segments, which are often driven by retail hype and social media activity.

It's perfect for timing momentum shifts in high-risk, high-reward tokens.

By using these indices, the strategy aligns entries with broader sector trends, filtering out noise and increasing the probability of catching true directional moves, especially in phases of capital rotation and altcoin risk-on behavior.

📐 How It Works — Core Logic and Execution Model

At its heart, this strategy employs dual EMA crossover detection—one pair for the asset being traded and one pair for the selected market index.

A trade is only executed when both EMA crossovers agree on the direction. For example:

Long Entry: Coin's fast EMA > slow EMA and Index's fast EMA > slow EMA

Short Entry: Coin's fast EMA < slow EMA and Index's fast EMA < slow EMA

You can disable the index filter and trade solely based on the asset’s trend just to make a comparison and see if improves a classic EMA crossover strategy.

Additionally, the strategy includes:

- Adaptive position sizing, based on fixed capital or current equity (compound mode)

- Take Profit and Stop Loss in percentage terms

- Smart partial exits when trend momentum fades

- Date filtering for precise backtesting over specific timeframes

- Real-time performance stats, equity tracking, and visual cues on chart

⚙️ Parameters & Customization

🔁 EMA Settings

Each EMA pair is customizable:

Coin Fast EMA: Default = 47

Coin Slow EMA: Default = 50

Index Fast EMA: Default = 47

Index Slow EMA: Default = 50

These control the sensitivity of the trend detection. A wider spread gives smoother, slower entries; a narrower spread makes it more responsive.

🧭 Index Reference

The correlation mechanism uses CryptoCap sector dominance indexes:

OTHERS.D: Dominance of all coins EXCLUDING Top 10 ones

MEME.D: Dominance of all Meme coins

These are dynamically calculated using:

OTHERS_D = OTHERS_cap / TOTAL_cap * 100

MEME_D = MEME_cap / TOTAL_cap * 100

You can select:

Reference Index: OTHERS.D or MEME.D

Or disable the index reference completely (Don't Use Index Reference)

💰 Position Sizing & Risk Management

Two capital allocation models are supported:

- Fixed % of initial capital (default)

- Compound profits, which scales positions as equity grows

Settings:

- Compound profits?: true/false

- % of equity: Between 1% and 200% (default = 10%)

This is critical for users who want to balance growth with risk.

🎯 Take Profit / Stop Loss

Customizable thresholds determine automatic exits:

- TakeProfit: Default = 99999 (disabled)

- StopLoss: Default = 5 (%)

These exits are percentage-based and operate off the entry price vs. current close.

📉 Trend Weakening Exit (Scale Out)

If the position is in profit but the trend weakens (e.g., EMA color signals trend loss), the strategy can partially close a configurable portion of the position:

- Scale Position on Weak Trend?: true/false

- Scaled Percentage: % to close (default = 65%)

This feature is useful for preserving profits without exiting completely.

📆 Date Filter

Useful for segmenting performance over specific timeframes (e.g., bull vs bear markets):

- Filter Date Range of Backtest: ON/OFF

- Start Date and End Date: Custom time range

OTHER PARAMETERS EXPLANATION (Strategy "Properties" Tab):

- Initial Capital is set to 100 USD

- Commission is set to 0.055% (The ones I have on Bybit)

- Slippage is set to 3 ticks

- Margin (short and long) are set to 0.001% to avoid "overspending" your initial capital allocation

📊 Visual Feedback and Debug Tools

📈 EMA Trend Visualization

The slow EMA line is dynamically color-coded to visually display the alignment between the asset trend and the index trend:

Lime: Coin and index both bullish

Teal: Only coin bullish

Maroon: Only index bullish

Red: Both bearish

This allows for immediate visual confirmation of current trend strength.

💬 Real-Time PnL Labels

When a trade closes, a label shows:

Previous trade return in % (first value is the effective PL)

Green background for profit, Red for losses.

📑 Summary Table Overlay

This table appears in a corner of the chart (user-defined) and shows live performance data including:

Trade direction (yellow long, purple short)

Emojis: 💚 for current profit, 😡 for current loss

Total number of trades

Win rate

Max drawdown

Duration in days

Current trade profit/loss (absolute and %)

Cumulative PnL (absolute and %)

APR (Annualized Percentage Return)

Each metric is color-coded:

Green for strong results

Yellow/orange for average

Red/maroon for poor performance

You can select where this appears:

Top Left

Top Right

Bottom Left

Bottom Right (default)

📚 Interpretation of Key Metrics

Equity Multiplier: How many times initial capital has grown (e.g., “1.75x”)

Net Profit: Total gains including open positions

Max Drawdown: Largest peak-to-valley drop in strategy equity

APR: Annualized return calculated based on equity growth and days elapsed

Win Rate: % of profitable trades

PnL %: Percentage profit on the most recent trade

🧠 Advanced Logic & Safety Features

🛑 “Don’t Re-Enter” Filter

If a trade is closed due to StopLoss without a confirmed reversal, the strategy avoids re-entering in that same direction until conditions improve. This prevents false reversals and repetitive losses in sideways markets.

🧷 Equity Protection

No new trades are initiated if equity falls below initial_capital / 30. This avoids overleveraging or continuing to trade when capital preservation is critical.

Keep in mind that past results in no way guarantee future performance.

Eddie Bitcoin

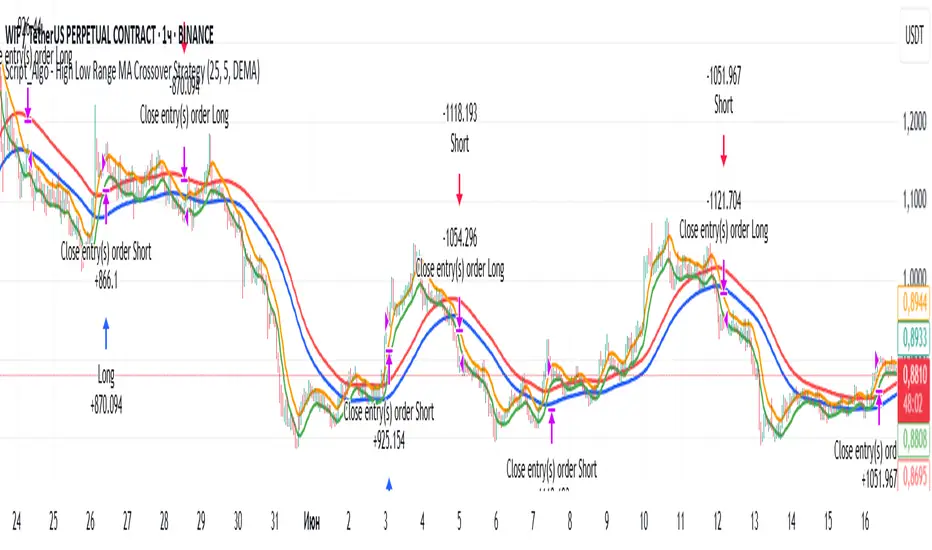

Script_Algo - High Low Range MA Crossover Strategy🎯 Core Concept

This strategy uses modified moving averages crossover, built on maximum and minimum prices, to determine entry and exit points in the market. A key advantage of this strategy is that it avoids most false signals in trendless conditions, which is characteristic of traditional moving average crossover strategies. This makes it possible to improve the risk/reward ratio and, consequently, the strategy's profitability.

📊 How the Strategy Works

Main Mechanism

The strategy builds 4 moving averages:

Two senior MAs (on high and low) with a longer period

Two junior MAs (on high and low) with a shorter period

Buy signal 🟢: when the junior MA of lows crosses above the senior MA of highs

Sell signal 🔴: when the junior MA of highs crosses below the senior MA of lows

As seen on the chart, it was potentially possible to make 9X on the WIFUSDT cryptocurrency pair in just a year and a half. However, be careful—such results may not necessarily be repeated in the future.

Special Feature

Position closing priority ❗: if an opposite signal arrives while a position is open, the strategy first closes the current position and only then opens a new one

⚙️ Indicator Settings

Available Moving Average Types

EMA - Exponential MA

SMA - Simple MA

SSMA - Smoothed MA

WMA - Weighted MA

VWMA - Volume Weighted MA

RMA - Adaptive MA

DEMA - Double EMA

TEMA - Triple EMA

Adjustable Parameters

Senior MA Length - period for long-term moving averages

Junior MA Length - period for short-term moving averages

✅ Advantages of the Strategy

🛡️ False Signal Protection - using two pairs of modified MAs reduces the number of false entries

🔄 Configuration Flexibility - ability to choose MA type and calculation periods

⚡ Automatic Switching - the strategy automatically closes the current position when receiving an opposite signal

📈 Visual Clarity - all MAs are displayed on the chart in different colors

⚠️ Disadvantages and Risks

📉 Signal Lag - like all MA-based strategies, it may provide delayed signals during sharp movements

🔁 Frequent Switching - in sideways markets, it may lead to multiple consecutive position openings/closings

📊 Requires Optimization - optimal parameters need to be selected for different instruments and timeframes

💡 Usage Recommendations

Backtest - test the strategy's performance on historical data

Optimize Parameters - select MA periods suitable for the specific trading instrument

Use Filters - add additional filters to confirm signals

Manage Risks - always use stop-loss and take-profit orders.

You can safely connect to the exchange via webhook and enjoy trading.

Good luck and profits to everyone!!

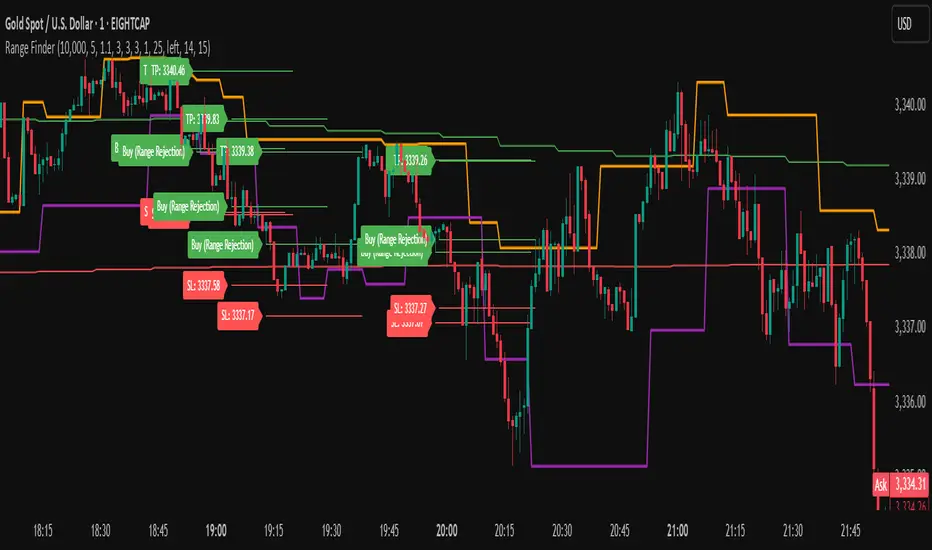

Range FinderRange Finder Strategy for TradingView

Overview

The Range Finder Strategy is a sophisticated trading system designed for forex and cryptocurrency markets, leveraging dynamic range detection, wick-based rejection patterns, and EMA confluence to execute high-probability trades. This strategy identifies key price ranges using pivot points and triggers trades when price rejects from these boundaries with significant wick formations, aligning with the broader market trend as confirmed by EMA crossovers. It incorporates robust risk management, customizable parameters, and visual aids for clear trade visualization, making it suitable for both manual and automated trading on platforms like Bitget via webhook alerts.

Strategy Components

1. Dynamic Range Detection

Pivot Points: The strategy identifies range boundaries using pivot highs and lows, calculated with a user-defined Pivot Length (default: 5 bars left/right). These pivots mark significant swing points, defining the upper (range high) and lower (range low) boundaries of the price range.

Visualization: The range high is plotted as an orange line, and the range low as a purple line, using a broken line style (plot.style_linebr) to show only confirmed pivot levels, providing a clear visual of the trading range.

2. Wick-Based Rejection Pattern

Wick Detection: The strategy looks for rejection candles at the range boundaries, characterized by significant wicks. A wick is considered valid if its size is at least the user-defined Wick to Body Ratio (default: 1.1, or 10% larger than the candle body).

Sell Signal: Triggered when the high exceeds the range high, the candle closes bearish (close < open), and the upper wick meets the ratio requirement.

Buy Signal: Triggered when the low falls below the range low, the candle closes bullish (close > open), and the lower wick meets the ratio requirement.

Purpose: These wicks indicate strong rejection at key levels, often signaling a reversal back into the range, providing high-probability entry points.

3. EMA Trend Confirmation

EMA Calculation: Uses two Exponential Moving Averages (EMAs) calculated on a user-selectable timeframe (default: 5-minute):

EMA 200: Long-term trend indicator (plotted in red).

EMA 50: Short-term trend indicator (plotted in green).

Crossover Logic:

A bullish trend is confirmed when the EMA 50 crosses above the EMA 200 (ema_trend_up = true).

A bearish trend is confirmed when the EMA 50 crosses below the EMA 200 (ema_trend_down = true).

Confluence Requirement: Trades are only executed when the wick rejection aligns with the EMA trend (e.g., sell signals require close < ema200 and bearish trend; buy signals require close > ema200 and bullish trend).

4. Risk Management

Position Sizing: Calculated based on the user-defined Account Balance (default: $10,000) and Risk Per Trade (default: 2%). The position size is determined as risk_amount / stop_distance, where stop_distance is derived from the Average True Range (ATR, default period: 14).

Stop Loss (SL): Set using an ATR-based multiplier (SL Multiplier, default: 9.0). For sells, SL is placed above the high; for buys, below the low.

Take Profit (TP): Set using an ATR-based multiplier (TP Multiplier, default: 6.0) scaled by the Risk:Reward Ratio (default: 6.0), ensuring a favorable reward-to-risk profile.

Example: For a $10,000 account with 2% risk, if ATR is 0.5, the position size is 400 units, with SL and TP dynamically adjusted to market volatility.

5. Trade Execution

Sell Entry: Triggered on a wick rejection above the range high, with bearish EMA confluence (ema_trend_down and close < ema200). Enters a short position with calculated SL and TP.

Buy Entry: Triggered on a wick rejection below the range low, with bullish EMA confluence (ema_trend_up and close > ema200). Enters a long position with calculated SL and TP.

Exit Logic: Uses strategy.exit to set SL and TP levels, closing trades when either is hit.

6. Visual Feedback

Lines and Labels: Upon trade entry, the strategy plots:

Red SL line and label (e.g., "SL: 123.45").

Green TP line and label (e.g., "TP: 120.00").

Entry line (red for sell, green for buy) labeled with "Sell (Range Rejection)" or "Buy (Range Rejection)".

Customization: Users can adjust the Line Length (default: 25 bars) for how long lines persist and Label Position (left or right) for optimal chart visibility.

7. Alert Conditions

Webhook Integration: Generates alerts for Bitget webhook integration, providing JSON-formatted messages with trade details (action, contracts, market position, size, price, symbol, and timestamp).

Usage: Traders can set up automated trading by connecting these alerts to trading bots or platforms supporting webhooks.

Pivot Distance Strategy# Multi-Timeframe Pivot Distance Strategy

## Core Innovation & Originality

This strategy revolutionizes moving average crossover trading by applying MA logic to **pivot distance relationships** instead of raw price data. Unlike traditional MA crossovers that react to price changes, this system reacts to **structural momentum changes** in how current price relates to recent significant pivot levels, creating earlier signals with fewer false positives.

## Methodology & Mathematical Foundation

### Pivot Distance Oscillator

The strategy calculates:

- **High Pivot Percentage**: (Current Close / Last Pivot High) × 100

- **Low Pivot Percentage**: (Last Pivot Low / Current Close) × 100

- **Pivot Distance**: High Pivot Percentage - Low Pivot Percentage

This creates a standardized oscillator measuring market structure compression/expansion regardless of asset price or volatility.

### Multi-Timeframe Filter

Higher timeframe analysis provides directional bias:

- **HTF Long** → Allow long entries, force short exits

- **HTF Short** → Allow short entries, force long exits

- **HTF Squeeze** → Block all entries, force all exits

## Signal Generation Methods

### Method 1: Dual MA Crossover (Primary/Default)

**Fast MA (14 EMA)** and **Slow MA (50 SMA)** applied to pivot distance values:

- **Long Signal**: Fast MA crosses above Slow MA (accelerating bullish pivot momentum)

- **Short Signal**: Fast MA crosses below Slow MA (accelerating bearish pivot momentum)

**Key Advantage**:

- Traditional: Fast MA(price) crosses Slow MA(price) - reacts to price changes

- This Strategy: Fast MA(pivot distance) crosses Slow MA(pivot distance) - reacts to structural changes

- Result: Earlier signals, better trend identification, fewer ranging market whipsaws

### Method 2: MA Cross Zero

- **Long**: Pivot Distance MA crosses above zero

- **Short**: Pivot Distance MA crosses below zero

### Method 3: Pivot Distance Breakout (Squeeze-Based)

Uses dynamic threshold envelopes to detect compression/expansion cycles:

- **Long**: Distance breaks above dynamic breakout threshold after squeeze

- **Short**: Distance breaks below negative breakout threshold after squeeze

**Note**: Only the Breakout method uses threshold envelopes; MA Cross modes operate without them for cleaner signals.

## Risk Management Integration

- **ATR-Based Stops**: Entry ± (ATR × Multiplier) for stops/targets

- **Trailing Stops**: Dynamic adjustment based on profit thresholds

- **Cooldown System**: Prevents overtrading after stop-loss exits

## How to Use

### Setup (Default: MA Cross MA)

1. **Strategy Logic**: "MA Cross MA" for structural momentum signals

2. **MA Settings**: 14 EMA (fast) / 50 SMA (slow) - both adjustable

3. **Multi-Timeframe**: Enable HTF for trend alignment

4. **Risk Management**: ATR stop loss, ATR take profit

### Signal Interpretation

- **Blue/Purple lines**: Fast/Slow MAs of pivot distance

- **Green/Red histogram**: Positive/negative pivot distance

- **Triangle markers**: MA crossover entry signals

- **HTF display**: Shows higher timeframe bias (top-left)

### Trade Management

- **Entry**: Clean MA crossover with HTF alignment

- **Exit**: Opposite crossover, HTF change, or risk management triggers

## Unique Advantages

1. **Structural vs Price Momentum**: Captures market structure changes rather than just price movement, naturally filtering noise

2. **Multi-Modal Flexibility**: Three signal methods for different market conditions or strategies

3. **Timeframe Alignment**: HTF filtering improves win rates by preventing counter-trend trades

The Barking Rat LiteMomentum & FVG Reversion Strategy

The Barking Rat Lite is a disciplined, short-term mean-reversion strategy that combines RSI momentum filtering, EMA bands, and Fair Value Gap (FVG) detection to identify short-term reversal points. Designed for practical use on volatile markets, it focuses on precise entries and ATR-based take profit management to balance opportunity and risk.

Core Concept

This strategy seeks potential reversals when short-term price action shows exhaustion outside an EMA band, confirmed by momentum and FVG signals:

EMA Bands:

Parameters used: A 20-period EMA (fast) and 100-period EMA (slow).

Why chosen:

- The 20 EMA is sensitive to short-term moves and reflects immediate momentum.

- The 100 EMA provides a slower, structural anchor.

When price trades outside both bands, it often signals overextension relative to both short-term and medium-term trends.

Application in strategy:

- Long entries are only considered when price dips below both EMAs, identifying potential undervaluation.

- Short entries are only considered when price rises above both EMAs, identifying potential overvaluation.

This dual-band filter avoids counter-trend signals that would occur if only a single EMA was used, making entries more selective..

Fair Value Gap Detection (FVG):

Parameters used: The script checks for dislocations using a 12-bar lookback (i.e. comparing current highs/lows with values 12 candles back).

Why chosen:

- A 12-bar displacement highlights significant inefficiencies in price structure while filtering out micro-gaps that appear every few bars in high-volatility markets.

- By aligning FVG signals with candle direction (bullish = close > open, bearish = close < open), the strategy avoids random gaps and instead targets ones that suggest exhaustion.

Application in strategy:

- Bullish FVGs form when earlier lows sit above current highs, hinting at downward over-extension.

- Bearish FVGs form when earlier highs sit below current lows, hinting at upward over-extension.

This gives the strategy a structural filter beyond simple oscillators, ensuring signals have price-dislocation context.

RSI Momentum Filter:

Parameters used: 14-period RSI with thresholds of 80 (overbought) and 20 (oversold).

Why chosen:

- RSI(14) is a widely recognized momentum measure that balances responsiveness with stability.

- The thresholds are intentionally extreme (80/20 vs. the more common 70/30), so the strategy only engages at genuine exhaustion points rather than frequent minor corrections.

Application in strategy:

- Longs trigger when RSI < 20, suggesting oversold exhaustion.

- Shorts trigger when RSI > 80, suggesting overbought exhaustion.

This ensures entries are not just technically valid but also backed by momentum extremes, raising conviction.

ATR-Based Take Profit:

Parameters used: 14-period ATR, with a default multiplier of 4.

Why chosen:

- ATR(14) reflects the prevailing volatility environment without reacting too much to outliers.

- A multiplier of 4 is a pragmatic compromise: wide enough to let trades breathe in volatile conditions, but tight enough to enforce disciplined exits before mean reversion fades.

Application in strategy:

- At entry, a fixed target is set = Entry Price ± (ATR × 4).

- This target scales automatically with volatility: narrower in calm periods, wider in explosive markets.

By avoiding discretionary exits, the system maintains rule-based discipline.

Visual Signals on Chart

Blue “▲” below candle: Potential long entry

Orange/Yellow “▼” above candle: Potential short entry

Green “✔️”: Trade closed at ATR take profit

Blue (20 EMA) & Orange (100 EMA) lines: Dynamic channel reference

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 28, 2025 — Aug 17, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Lite strategy is very selective, filtering out over 90% of market noise. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods.

The strategy generates a sizeable number of trades, reducing reliance on a single outcome.

Combined with conservative filters, the 25% setting offers a balance between aggression and control.

Users are strongly encouraged to customize this to suit their risk profile.

What makes Barking Rat Lite valuable