NY, Asia & London Session Lines + NY First HourEUR/USD last session OHLC Asia + London and first hour NY. defaults to last session if market closed. publishing to save for my self, nothing groundbreaking

ค้นหาในสคริปต์สำหรับ "session"

ASR - Average Session Range [KasTrades]This indicator displays the Average Session Range based on the session of your choice.

You can turn the tables off if you don't want to see a table version of the ASR levels. There is also a momentum table showing the current momentum, which you can also turn off.

VWAP Session and NY CashAuto Anchored VWAPs with Label options

Session starts at 1800 EST

Cash Open or NY Session starts 0930 EST

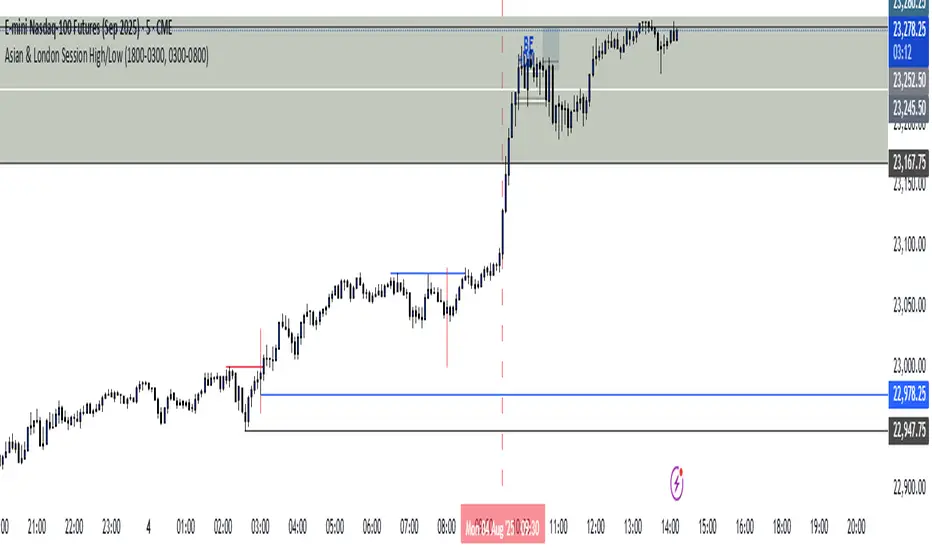

Asian & London Session High/Low (NEW)Marks out asian session high and low, london session high and low, so you dont have to, these levels are crucial to your trading, so use this indicator

Asian & London Session High/LowMarks out asian session high and low, aswell as london session high and low, this makes it easier for you to have crucial key levels on your chart at all times

Timed Reversion Markers (Custom Session Alerts)This script plots vertical histogram markers at specific intraday time points defined by the user. It is designed for traders who follow time-based reversion or breakout setups tied to predictable market behavior at key clock times, such as institutional opening moves, midday reversals, or end-of-day volatility.

Unlike traditional price-action indicators, this tool focuses purely on time-based triggers, a technique often used in time cycle analysis, market internals, and volume-timing strategies.

The indicator includes eight fully customizable time inputs, allowing users to mark any intraday minute with precision using a decimal hour format (for example, 9.55 for 9:55 AM). Each input is automatically converted into hour and minute format, and a visual histogram marker is plotted once per day at that exact time.

Example use cases:

Mark institutional session opens (e.g., 9:30, 10:00, 15:30)

Time-based mean reversion or volatility windows

Backtest recurring time-based reactions

Highlight algorithmic spike zones

The vertical plots serve as non-intrusive, high-contrast visual markers for scalping setups, session analysis, and decision-making checkpoints. All markers are displayed at the top of the chart without interfering with price candles.

Cumulative Weighted Change (Session) with 14 MAThis indicator provides the session weighted cumulative change of the Magnificent 7(AAPL META GOOG AMZN MSFT NVDA TSLA), it is weighted according to their market capitalization and size in relation to size of the market. The bar to bar current change is plotted by the fast line that begins its calculations at the start of each daily session, the smoother(slower) line is the 14 period Volume Weighted Moving Average of the cumulative change.

I use this in conjunction with a timeframe continuity indicator in order to weed out invalid signals, I have one that I have recently published. I use this to trade futures and index stock options, since the 7 tickers that this indicator is built off of are the biggest force that moves markets this ends up acting as an alpha indicator if you can find a consistent and reliable way to weed out false signals.

Happy Trading!

-Drgzzz

Daily Session Fibonacci LevelsPlots automatic Fibonacci retracement levels based on the current session high and low.

Levels for the prior and current session can be toggled on/off.

Optional: Toggle to show the Fibonacci Level labels.

Allows for customizable levels and colors; toggles for individual levels.

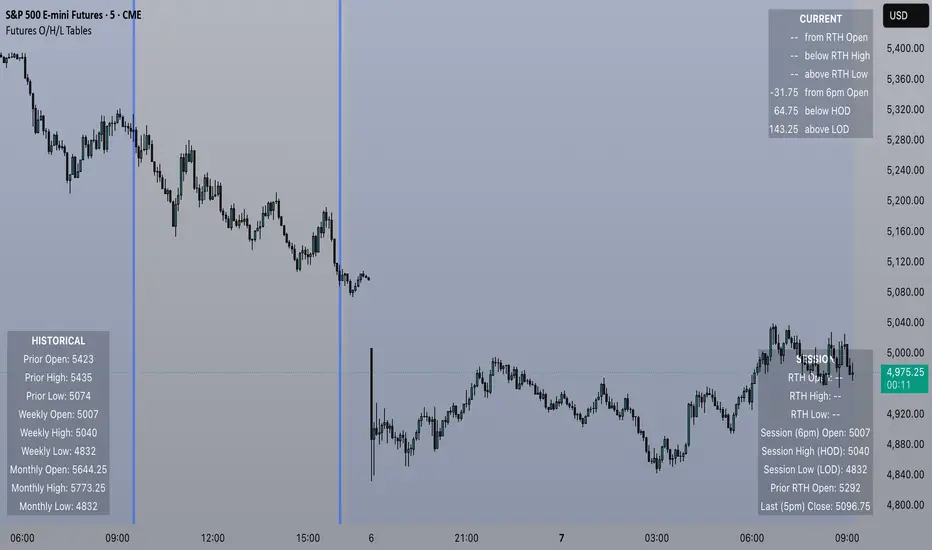

Futures Open/High/Low TablesAdds (up to) 3 tables to a chart, displaying Open/High/Low data for today (RTH and extended hours), yesterday, and the current week / month -- to help with intraday analysis of a futures ticker.

The tables only appear on intraday charts (5min, 30min, etc). On a Daily/Weekly/etc chart they are not calculated or shown.

In addition to Open/High/Low, the "Current" table in the top-right shows a live measurement of # of points from the open, the RTH open, and the highs/lows.

Lastly, the 9:30am ET open and the 4pm RTH close are by default marked with a shaded background (on intraday charts) for easy visual reference, and also to help with adjusting the session time to accommodate time zone issues if they occur.

Tested on ES in Eastern Time Zone, but should work on any futures instrument and any time zone by adjusting the Session Time setting.

Electronic Trading Hours Session/CandlesThis indicator visually distinguishes the electronic trading session, spanning from the prior day's close (e.g., 5:00 PM EST) through the overnight period until the next day's opening bell (e.g., 9:30 AM EST).

It can be customized to highlight this period with a shaded zone or colored candles depending on the trader’s preference.

The overnight levels that create the opening range gap often act as critical zones of liquidity.

The indicator provides a clear visual cue of potential price magnets that smart money (institutional traders) may target during the opening bell session to trigger liquidity sweeps.

Jerusalem Session Weekday MarkingJerusalem Session Weekday Marking

This indicator applies a background color to each trading day based on the Jerusalem time zone (Asia/Jerusalem). It's a simple, no-frills tool for traders operating in markets that follow a Sunday-Thursday business week.

How It Works:

Monday to Thursday → Red background (Regular trading days)

Friday to Sunday → Green background (Weekend/non-standard trading days)

Background coloring applies to the entire day (not just session hours).

Why Use This?

Designed for traders focusing on Middle Eastern, Israeli, and Forex markets.

Helps differentiate trading days at a glance in a market where Friday-Saturday weekends are standard.

Works automatically with Jerusalem timezone, no manual adjustments needed.

🚀 Simple, effective, and useful for traders who care about local trading schedules. 🚀

Monday Session High/LowThis script tracks and draw the High and the Low for Monday session across the whole week period.

Many crypto traders use the high and low extremes for Monday session as an confluence on how the price action during the week reacts against it.

EMA/Session/ATR/LotSizeSeveral indicators combined

1. 6 Exponential Moving Averages - Identifying the trend direction or using EMAs as a dynamic support/resistance.

2. Session on Chart - Highlighting session for day trading. London, New York, Tokyo, and Sydney.

3. Average True Range - display the Average True Range on recent price to calculate the volatility.

4. Lot Size Calculator - to calculate lot size based on account balance, risk per trade, atr stop-loss, and art multiplier.

5. ATRX - ATRX is an indicator that gives the value of the (close price - EMA 27)/ATR (14)

It tells how strong the trend is compared to its volatility

According to AJ. BANK FTMO Trader Thailand, if the value of ATRX is between 2X-3X or -2X-3X, you should consider trading using climax zone on timeframe H1.

If the ATRX is more than 3X or less than -3X but does not exceed 4X or -4X, you should consider trading using timeframe M15 in the climax zone.

However, if the ATRX exceeds 4X or -4X, use M5 instead.

Hourly Bias on BTC in Bullish USA Session “Green Eagle”Name: Hourly Bias on BTC in Bullish USA Session

Category: Hourly Bias

Operating mode: Spot, only long

Trades duration: Intraday, 11 bars

Timeframe: 1H

Suggested usage: When the market is compressed, USA session has a bullish bias.

Entry: enter Long at 15:00 on specific days of the week. There is a volatility filter based on ATR which identifies compression.

Exit: exit at a pre-defined time at 01:00

Usage:

⁃ It can be useful to use alerts or webhooks to automate this strategy.

⁃ This is a core system that can be improved in different ways (e.g. Stop-loss, take-profit, position sizing) or studying more the behaviour in the specific days of the week or short when is red.

Configuration:

- N/A

Backtesting

⁃ Exchange: BINANCE

⁃ Pair: BTCUSDT

⁃ Timeframe: 1H

⁃ Fee 0.075%

⁃ Slippage 2

- Start : 2019-01-06

We decided to release this free BTC strategy.

How you or we can improve? Source code is open so share your ideas!

Trade Session If you are trading intraday. It is sometimes helpful to see

the boundaries of your time period. This script was created

for this. It highlights your trading session in the background.

You can specify this interval in the settings in hh:mm-hh:mm

session start and stop, respectively.

Fide AI - High/low SessionDraw the high and low of the specific session until the start the session again.

Ignore Extended Session CodeLooking at the extended session is awesome and can certainly give you an edge on trading the open of a market. If you're more of a technical trader, though, you run into the problem of the extended session data throwing your indicators off. To fix that, use the code below as a template for whatever indicators you use.

3-Session ORB (SGT) + 15m EMA200 Trend Dashboard (v6)3-Session ORB (SGT) + 15m EMA200 Trend Dashboard (v6)

PD Location Screener (NY Session)Scan only for DISCOUNT or PREMIUM

Ignore everything at equilibrium

Then apply:

Liquidity sweep

Displacement

FVG / OB

One trade. Done.

Dual Session VWAPs by GK snipervwaps automatically

for london

new york session

easy

will remove automatically next day

ICT 7/8/9am lines NY session + 7.30/8.30/9.30 linesThis script show the 7, 8, 9 AM NY session lines, together with the 7.30, 8.30 and 9.30AM lines, like ICT teaches in the 2024 Mentorship, lesson 2.

Feel free to use it!