Multi-timeframe Moving Average Overlay w/ Sentiment Table🔍 Overview

This indicator overlays selected moving averages (MA) from multiple timeframes directly onto the chart and provides a dynamic sentiment table that summarizes the relative bullish or bearish alignment of short-, mid-, and long-term moving averages.

It supports seven moving average types — including traditional and advanced options like DEMA, TEMA, and HMA — and provides visual feedback via table highlights and alerts when strong momentum alignment is detected.

This tool is designed to support traders who rely on multi-timeframe analysis for trend confirmation, momentum filtering, and high-probability entry timing.

⚙️ Core Features

Multi-Timeframe MA Overlay:

Plot moving averages from 1-minute, 5-minute, 1-hour, 1-day, 1-week, and 1-month timeframes on the same chart for visual trend alignment.

Customizable MA Type:

Choose from:

EMA (Exponential Moving Average)

SMA (Simple Moving Average)

DEMA (Double EMA)

TEMA (Triple EMA)

WMA (Weighted MA)

VWMA (Volume-Weighted MA)

HMA (Hull MA)

Adjustable MA Length:

Change the length of all moving averages globally to suit your strategy (e.g. 9, 21, 50, etc.).

Sentiment Table:

Visually track trend sentiment across four key zones (Hourly, Daily, Weekly, Monthly). Each is based on the relative positioning of short-term and long-term MAs.

Sentiment Symbols Explained:

↑↑↑: Strong bullish momentum (short-term MAs stacked above longer-term MAs)

↑↑ / ↑: Moderate bullish bias

↓↓↓: Strong bearish momentum

↓↓ / ↓: Moderate bearish bias

Table Customization:

Choose the table’s position on the chart (bottom right, top right, bottom left, top left).

Style Customization:

Display MA lines as standard Line or Stepline format.

Color Customization:

Individual colors for each timeframe MA line for visual clarity.

Built-in Alerts:

Receive alerts when strong bullish (↑↑↑) or bearish (↓↓↓) sentiment is detected on any timeframe block.

📈 Use Cases

1. Trend Confirmation:

Use sentiment alignment across multiple timeframes to confirm the overall trend direction before entering a trade.

2. Entry Timing:

Wait for a shift from neutral to strong bullish or bearish sentiment to time entries during pullbacks or breakouts.

3. Momentum Filtering:

Only trade in the direction of the dominant multi-timeframe trend. For example, ignore long setups when all sentiment blocks show bearish alignment.

4. Swing & Intraday Scalping:

Use hourly and daily sentiment zones for swing trades, or rely on 1m/5m MAs for precise scalping decisions in fast-moving markets.

5. Strategy Layering:

Combine this overlay with support/resistance, RSI, or volume-based signals to enhance decision-making with multi-timeframe context.

⚠️ Important Notes

Lower-timeframe values (1m, 5m) may appear static on higher-timeframe charts due to resolution limits in TradingView. This is expected behavior.

The indicator uses MA stacking, not crossover events, to determine sentiment.

ค้นหาในสคริปต์สำหรับ "scalping"

Pullback SARPullback SAR - Parabolic SAR with Pullback Detection

Description: The "Pullback SAR" is an advanced indicator built on the classic Parabolic SAR but with additional functionality for detecting pullbacks. It helps identify moments when the price pulls back from the main trend, offering potential entry signals. Perfect for traders looking to enter the market after a correction.

Key Features:

SAR (Parabolic SAR): The Parabolic SAR indicator is used to determine potential trend reversal points. It marks levels where the price could reverse its direction.

Pullback Detection: The indicator catches periods when the price moves away from the main trend and then returns, which may suggest a re-entry opportunity.

Long and Short Signals: Once a pullback in the direction of the main trend is identified, the indicator generates signals that could be used to open positions.

Simple and Clear Construction: The indicator is based on the classic SAR, with added pullback detection logic to enhance the accuracy of the signals.

Parameters:

Start (SAR Step): Determines the initial step for the SAR calculation, which controls the rate of change in the indicator at the beginning.

Increment (SAR Increment): Defines the maximum step size for SAR, allowing traders to adjust the indicator’s sensitivity to market volatility.

Max Value (SAR Max): Sets the upper limit for the SAR value, controlling its volatility.

Usage:

Swing Trading: Ideal for swing strategies, aiming to capture larger price moves while maintaining a safe margin.

Scalping: Due to its precise pullback detection, it can also be used in scalping, especially when the price quickly returns to the main trend.

Risk Management: The combination of SAR and pullback detection allows traders to adjust their positions according to changing market conditions.

Special Notes:

Adjusting Parameters: Depending on the market and trading style, users can adjust the SAR parameters (Start, Increment, Max Value) to fit their needs.

Combination with Other Indicators: It's recommended to use the indicator alongside other technical analysis tools (e.g., EMA, RSI) to enhance the accuracy of the signals.

Link to the script: This open-source version of the indicator is available on TradingView, enabling full customization and adjustments to meet your personal trading strategy. Share your experiences and suggestions!

[TehThomas] - ICT Inversion Fair value Gap (IFVG) The Inversion Fair Value Gap (IFVG) indicator is a powerful tool designed for traders who utilize ICT (Inner Circle Trader) strategies. It focuses on identifying and displaying Inversion Fair Value Gaps, which are critical zones that emerge when traditional Fair Value Gaps (FVGs) are invalidated by price action. These gaps represent key areas where price often reacts, making them essential for identifying potential reversals, trend continuations, and liquidity zones.

What Are Inversion Fair Value Gaps?

Inversion Fair Value Gaps occur when price revisits a traditional FVG and breaks through it, effectively flipping its role in the market. For example:

A bullish FVG that is invalidated becomes a bearish zone, often acting as resistance.

A bearish FVG that is invalidated transforms into a bullish zone, serving as support.

These gaps are significant because they often align with institutional trading activity. They highlight areas where large orders have been executed or where liquidity has been targeted. Understanding these gaps provides traders with a deeper insight into market structure and helps them anticipate future price movements with greater accuracy.

Why This Strategy Works

The IFVG concept is rooted in ICT principles, which emphasize liquidity dynamics, market inefficiencies, and institutional order flow. Traditional FVGs represent imbalances in price action caused by gaps between candles. When these gaps are invalidated, they become inversion zones that can act as magnets for price. These zones frequently serve as high-probability areas for price reversals or trend continuations.

This strategy works because it aligns with how institutional traders operate. Inversion gaps often mark areas of interest for "smart money," making them reliable indicators of potential market turning points. By focusing on these zones, traders can align their strategies with institutional behavior and improve their overall trading edge.

How the Indicator Works

This indicator simplifies the process of identifying and tracking IFVGs by automating their detection and visualization on the chart. It scans the chart in real-time to identify bullish and bearish FVGs that meet user-defined thresholds for inversion. Once identified, these gaps are dynamically displayed on the chart with distinct colors for bullish and bearish zones.

The indicator also tracks whether these gaps are mitigated or broken by price action. When an IFVG is broken, it extends the zone for a user-defined number of bars to visualize its potential role as a new support or resistance level. Additionally, alerts can be enabled to notify traders when new IFVGs form or when existing ones are broken, ensuring timely decision-making in fast-moving markets.

Key Features

Automatic Detection: The indicator automatically identifies bullish and bearish IFVGs based on user-defined thresholds.

Dynamic Visualization: It displays IFVGs directly on the chart with customizable colors for easy differentiation.

Real-Time Updates: The status of each IFVG is updated dynamically based on price action.

Zone Extensions: Broken IFVGs are extended to visualize their potential as support or resistance levels.

Alerts: Notifications can be set up to alert traders when key events occur, such as the formation or breaking of an IFVG.

These features make the tool highly efficient and reduce the need for manual analysis, allowing traders to focus on execution rather than tedious chart work.

Benefits of Using This Indicator

The IFVG indicator offers several advantages that make it an indispensable tool for ICT traders. By automating the detection of inversion gaps, it saves time and reduces errors in analysis. The clearly defined zones improve risk management by providing precise entry points, stop-loss levels, and profit targets based on market structure.

This tool is also highly versatile and adapts seamlessly across different timeframes. Whether you’re scalping lower timeframes or swing trading higher ones, it provides actionable insights tailored to your trading style. Furthermore, by aligning your strategy with institutional logic, you gain a significant edge in anticipating market movements.

Practical Applications

This indicator can be used across various trading styles:

Scalping: Identify quick reversal points on lower timeframes using real-time alerts.

Day Trading: Use inversion gaps as key levels for intraday support/resistance or trend continuation setups.

Swing Trading: Analyse higher timeframes to identify major inversion zones that could act as critical turning points in larger trends.

By integrating this tool into your trading routine, you can streamline your analysis process and focus on executing high-probability setups.

Conclusion

The Inversion Fair Value Gap (IFVG) indicator is more than just a technical analysis tool—it’s a strategic ally for traders looking to refine their edge in the markets. By automating the detection and tracking of inversion gaps based on ICT principles, it simplifies complex market analysis while maintaining accuracy and depth. Whether you’re new to ICT strategies or an experienced trader seeking greater precision, this indicator will elevate your trading game by aligning your approach with institutional behavior.

If you’re serious about improving your trading results while saving time and effort, this tool is an essential addition to your toolkit. It provides clarity in chaotic markets, enhances precision in trade execution, and ensures you never miss critical opportunities in your trading journey.

__________________________________________

Thanks for your support!

If you found this idea helpful or learned something new, drop a like 👍 and leave a comment, I’d love to hear your thoughts! 🚀

Make sure to follow me for more price action insights, free indicators, and trading strategies. Let’s grow and trade smarter together! 📈

Multi-Timeframe Confluence IndicatorThe Multi-Timeframe Confluence Indicator strategically combines multiple timeframes with technical tools like EMA and RSI to provide robust, high-probability trading signals. This combination is grounded in the principles of technical analysis and market behavior, tailored for traders across all styles—whether intraday, swing, or positional.

1. The Power of Multi-Timeframe Confluence

Markets are influenced by participants operating on different time horizons:

• Intraday traders act on short-term price fluctuations.

• Swing traders focus on intermediate trends lasting days or weeks.

• Position traders aim to capture multi-month or long-term trends.

By aligning signals from a higher timeframe (macro trend) with a lower timeframe (micro trend), the indicator ensures that short-term entries are in harmony with the broader market direction. This multi-timeframe approach significantly reduces false signals caused by temporary market noise or counter-trend moves.

Example: A bullish trend on the daily chart (higher timeframe) combined with a bullish RSI and EMA alignment on the 15-minute chart (lower timeframe) provides a stronger confirmation than relying on the 15-minute chart alone.

2. Why EMA and RSI Are Essential

Each element of the indicator serves a unique role in ensuring accuracy and reliability:

• EMA (Exponential Moving Average):

• A dynamic trend filter that adjusts quickly to price changes.

• On the higher timeframe, it establishes the overall trend direction (e.g., bullish or bearish).

• On the lower timeframe, it identifies precise entry/exit zones within the trend.

• RSI (Relative Strength Index):

• Adds a momentum-based perspective, confirming whether a trend is backed by strong buying or selling pressure.

• Ensures that signals occur in areas of strength (RSI > 55 for bullish signals, RSI < 45 for bearish signals), filtering out weak or uncertain price movements.

By combining EMA (trend) and RSI (momentum), the indicator delivers confluence-based validation, where both trend and momentum align, making signals more reliable.

3. Cooldown Period for Signal Optimization

Trading in choppy or sideways markets often leads to overtrading and false signals. The cooldown period ensures that once a signal is generated, subsequent signals are suppressed for a defined number of bars. This prevents traders from entering low-probability trades during indecisive market phases, improving overall signal quality.

Example: After a bullish confluence signal, the cooldown period prevents a bearish signal from being triggered prematurely if the market enters a temporary retracement.

4. Use Cases Across Trading Styles

This indicator caters to various trading styles, each benefiting from the confluence of timeframes and technical elements:

• Intraday Trading:

• Use a 1-hour chart as the higher timeframe and a 5-minute chart as the lower timeframe.

• Benefit: Align intraday entries with the hourly trend for higher win rates.

• Swing Trading:

• Use a daily chart as the higher timeframe and a 1-hour chart as the lower timeframe.

• Benefit: Capture multi-day moves while avoiding counter-trend entries.

• Scalping:

• Use a 30-minute chart as the higher timeframe and a 1-minute chart as the lower timeframe.

• Benefit: Enhance scalping efficiency by ensuring short-term trades align with broader intraday trends.

• Position Trading:

• Use a weekly chart as the higher timeframe and a daily chart as the lower timeframe.

• Benefit: Time long-term entries more precisely, maximizing profit potential.

5. Robustness Through Customization

The indicator allows traders to customize:

• Timeframes for higher and lower analysis.

• EMA lengths for trend filtering.

• RSI settings for momentum confirmation.

• Cooldown periods to adapt to market volatility.

This flexibility ensures that the indicator can be tailored to suit individual trading preferences, market conditions, and asset classes, making it a comprehensive tool for any trading strategy.

Why This Mashup Stands Out

The Multi-Timeframe Confluence Indicator is more than a sum of its parts. It leverages:

• EMA’s ability to identify trends, combined with RSI’s insight into momentum, ensuring each signal is well-supported.

• A multi-timeframe perspective that incorporates both macro and micro trends, filtering out noise and improving reliability.

• A cooldown mechanism that prevents overtrading, a common pitfall for traders in volatile markets.

This integration results in a powerful, adaptable indicator that provides actionable, high-confidence signals, reducing uncertainty and enhancing trading performance across all styles.

EBL - Enigma BOS Logic Select Higher Time FrameThe "EBL – Enigma BOS Logic" is a unique multi-timeframe trading indicator designed for traders who rely on structured price action and key level retests to find high-probability trade opportunities. This indicator automates the identification of significant price levels on a higher timeframe, plots them across all lower timeframes, and provides actionable signals (buy/sell) when price retests those levels. It is ideal for traders who focus on lower timeframes for precise entries while using higher timeframe structure for trend confirmation.

How the Indicator Works

Key Level Detection:

The indicator allows the user to select a key level timeframe (e.g., 1H, 4H, Daily, Weekly). It then identifies Break of Structure (BOS) levels on the selected timeframe.

When a bullish-to-bearish or bearish-to-bullish reversal is detected on the selected timeframe, the corresponding high or low of the reversal candle is stored as a key level.

These key levels are plotted as horizontal lines on all lower timeframes, helping the trader visualize critical support and resistance zones across multiple timeframes.

Retest Confirmation:

Once a key level is established, the indicator continuously monitors the price action on lower timeframes.

If the price touches or crosses a key level, it is considered a retest, and an alert is generated.

The indicator plots a retest marker (customizable as a circle or diamond) at the exact price level where the retest occurred, providing a clear visual cue for the trader.

Trading Signals:

When a retest is detected, a table is displayed on the chart with the following information:

The trading pair.

The signal direction (Buy/Sell).

The price at which the retest occurred.

This table gives traders instant insight into actionable opportunities, making it easier to focus on live market conditions without missing critical retests.

Key Features

Multi-Timeframe Analysis: The indicator focuses on a higher timeframe selected by the user, ensuring that only the most relevant key levels are plotted for lower timeframe trading.

Dynamic Retest Signals: It dynamically identifies when price retests a key level and provides both visual markers and real-time alerts.

Customizable Retest Markers: Users can customize the retest marker's shape (circle/diamond) and color to suit their preferences.

Signal Table: A built-in table displays clear buy or sell signals when retests occur, ensuring that traders have all the necessary information at a glance.

Alerts: The indicator supports real-time alerts for retests, helping traders stay informed even when they are not actively monitoring the chart.

How to Use the Indicator

Select a Key Level Timeframe:

In the input settings, choose a higher timeframe (e.g., 4H or Daily) to define key levels.

The indicator will calculate Break of Structure (BOS) levels on the selected timeframe and plot them as horizontal lines across all lower timeframes.

Monitor Lower Timeframes for Retests:

Switch to a lower timeframe (e.g., 15m, 5m) to wait for price to approach the key levels plotted by the indicator.

When a retest occurs, observe the signal table and retest marker for actionable trade signals.

Act on Buy/Sell Signals:

Use the information provided by the signal table to make trading decisions.

For a buy signal, wait for bullish confirmation (e.g., price holding above the retested level).

For a sell signal, wait for bearish confirmation (e.g., price holding below the retested level).

Trading Concepts and Underlying Logic

The indicator is based on the Break of Structure (BOS) concept, a core principle in price action trading. BOS levels represent points where the market shifts its trend direction, making them critical zones for potential reversals or continuations.

By focusing on higher timeframe BOS levels, the indicator helps traders align their lower timeframe entries with the overall market trend.

The concept of retests is used to confirm the validity of a key level. A retest occurs when the price returns to a previously identified BOS level, offering a high-probability entry point.

Use Cases

Scalping: Traders who prefer lower timeframe scalping can use the indicator to align their trades with higher timeframe key levels, increasing the likelihood of successful trades.

Swing Trading: Swing traders can use the indicator to identify key reversal zones on higher timeframes and plan their trades accordingly.

Intraday Trading: Intraday traders can benefit from the real-time alerts and signals generated by the indicator, ensuring they never miss critical retests during active trading hours.

Conclusion

The "EBL – Enigma BOS Logic" is a powerful tool for traders who want to enhance their price action trading by focusing on key levels and retests across multiple timeframes. By automating the identification of BOS levels and providing clear retest signals, it helps traders make more informed and confident trading decisions. Whether you are a scalper, intraday trader, or swing trader, this indicator offers valuable insights to improve your trading performance.

Multi-Timeframe Stochastic Alert [tradeviZion]# Multi-Timeframe Stochastic Alert : Complete User Guide

## 1. Introduction

### What is the Multi-Timeframe Stochastic Alert?

The Multi-Timeframe Stochastic Alert is an advanced technical analysis tool that helps traders identify potential trading opportunities by analyzing momentum across multiple timeframes. It combines the power of the stochastic oscillator with multi-timeframe analysis to provide more reliable trading signals.

### Key Features and Benefits

- Simultaneous analysis of 6 different timeframes

- Advanced alert system with customizable conditions

- Real-time visual feedback with color-coded signals

- Comprehensive data table with instant market insights

- Motivational trading messages for psychological support

- Flexible theme support for comfortable viewing

### How it Can Help Your Trading

- Identify stronger trends by confirming momentum across multiple timeframes

- Reduce false signals through multi-timeframe confirmation

- Stay informed of market changes with customizable alerts

- Make more informed decisions with comprehensive market data

- Maintain trading discipline with clear visual signals

## 2. Understanding the Display

### The Stochastic Chart

The main chart displays three key components:

1. ** K-Line (Fast) **: The primary stochastic line (default color: green)

2. ** D-Line (Slow) **: The signal line (default color: red)

3. ** Reference Lines **:

- Overbought Level (80): Upper dashed line

- Middle Line (50): Center dashed line

- Oversold Level (20): Lower dashed line

### The Information Table

The table provides a comprehensive view of stochastic readings across all timeframes. Here's what each column means:

#### Column Explanations:

1. ** Timeframe **

- Shows the time period for each row

- Example: "5" = 5 minutes, "15" = 15 minutes, etc.

2. ** K Value **

- The fast stochastic line value (0-100)

- Higher values indicate stronger upward momentum

- Lower values indicate stronger downward momentum

3. ** D Value **

- The slow stochastic line value (0-100)

- Helps confirm momentum direction

- Crossovers with K-line can signal potential trades

4. ** Status **

- Shows current momentum with symbols:

- ▲ = Increasing (bullish)

- ▼ = Decreasing (bearish)

- Color matches the trend direction

5. ** Trend **

- Shows the current market condition:

- "Overbought" (above 80)

- "Bullish" (above 50)

- "Bearish" (below 50)

- "Oversold" (below 20)

#### Row Explanations:

1. ** Title Row **

- Shows "🎯 Multi-Timeframe Stochastic"

- Indicates the indicator is active

2. ** Header Row **

- Contains column titles

- Dark blue background for easy reading

3. ** Timeframe Rows **

- Six rows showing different timeframe analyses

- Each row updates independently

- Color-coded for easy trend identification

4. **Message Row**

- Shows rotating motivational messages

- Updates every 5 bars

- Helps maintain trading discipline

### Visual Indicators and Colors

- ** Green Background **: Indicates bullish conditions

- ** Red Background **: Indicates bearish conditions

- ** Color Intensity **: Shows strength of the signal

- ** Background Highlights **: Appear when alert conditions are met

## 3. Core Settings Groups

### Stochastic Settings

These settings control the core calculation of the stochastic oscillator.

1. ** Length (Default: 14) **

- What it does: Determines the lookback period for calculations

- Higher values (e.g., 21): More stable, fewer signals

- Lower values (e.g., 8): More sensitive, more signals

- Recommended:

* Day Trading: 8-14

* Swing Trading: 14-21

* Position Trading: 21-30

2. ** Smooth K (Default: 3) **

- What it does: Smooths the main stochastic line

- Higher values: Smoother line, fewer false signals

- Lower values: More responsive, but more noise

- Recommended:

* Day Trading: 2-3

* Swing Trading: 3-5

* Position Trading: 5-7

3. ** Smooth D (Default: 3) **

- What it does: Smooths the signal line

- Works in conjunction with Smooth K

- Usually kept equal to or slightly higher than Smooth K

- Recommended: Keep same as Smooth K for consistency

4. ** Source (Default: Close) **

- What it does: Determines price data for calculations

- Options: Close, Open, High, Low, HL2, HLC3, OHLC4

- Recommended: Stick with Close for most reliable signals

### Timeframe Settings

Controls the multiple timeframes analyzed by the indicator.

1. ** Main Timeframes (TF1-TF6) **

- TF1 (Default: 10): Shortest timeframe for quick signals

- TF2 (Default: 15): Short-term trend confirmation

- TF3 (Default: 30): Medium-term trend analysis

- TF4 (Default: 30): Additional medium-term confirmation

- TF5 (Default: 60): Longer-term trend analysis

- TF6 (Default: 240): Major trend confirmation

Recommended Combinations:

* Scalping: 1, 3, 5, 15, 30, 60

* Day Trading: 5, 15, 30, 60, 240, D

* Swing Trading: 15, 60, 240, D, W, M

2. ** Wait for Bar Close (Default: true) **

- What it does: Controls when calculations update

- True: More reliable but slightly delayed signals

- False: Faster signals but may change before bar closes

- Recommended: Keep True for more reliable signals

### Alert Settings

#### Main Alert Settings

1. ** Enable Alerts (Default: true) **

- Master switch for all alert notifications

- Toggle this off when you don't want any alerts

- Useful during testing or when you want to focus on visual signals only

2. ** Alert Condition (Options) **

- "Above Middle": Bullish momentum alerts only

- "Below Middle": Bearish momentum alerts only

- "Both": Alerts for both directions

- Recommended:

* Trending Markets: Choose direction matching the trend

* Ranging Markets: Use "Both" to catch reversals

* New Traders: Start with "Both" until you develop a specific strategy

3. ** Alert Frequency **

- "Once Per Bar": Immediate alerts during the bar

- "Once Per Bar Close": Alerts only after bar closes

- Recommended:

* Day Trading: "Once Per Bar" for quick reactions

* Swing Trading: "Once Per Bar Close" for confirmed signals

* Beginners: "Once Per Bar Close" to reduce false signals

#### Timeframe Check Settings

1. ** First Check (TF1) **

- Purpose: Confirms basic trend direction

- Alert Triggers When:

* For Bullish: Stochastic is above middle line (50)

* For Bearish: Stochastic is below middle line (50)

* For Both: Triggers in either direction based on position relative to middle line

- Settings:

* Enable/Disable: Turn first check on/off

* Timeframe: Default 5 minutes

- Best Used For:

* Quick trend confirmation

* Entry timing

* Scalping setups

2. ** Second Check (TF2) **

- Purpose: Confirms both position and momentum

- Alert Triggers When:

* For Bullish: Stochastic is above middle line AND both K&D lines are increasing

* For Bearish: Stochastic is below middle line AND both K&D lines are decreasing

* For Both: Triggers based on position and direction matching current condition

- Settings:

* Enable/Disable: Turn second check on/off

* Timeframe: Default 15 minutes

- Best Used For:

* Trend strength confirmation

* Avoiding false breakouts

* Day trading setups

3. ** Third Check (TF3) **

- Purpose: Confirms overall momentum direction

- Alert Triggers When:

* For Bullish: Both K&D lines are increasing (momentum confirmation)

* For Bearish: Both K&D lines are decreasing (momentum confirmation)

* For Both: Triggers based on matching momentum direction

- Settings:

* Enable/Disable: Turn third check on/off

* Timeframe: Default 30 minutes

- Best Used For:

* Major trend confirmation

* Swing trading setups

* Avoiding trades against the main trend

Note: All three conditions must be met simultaneously for the alert to trigger. This multi-timeframe confirmation helps reduce false signals and provides stronger trade setups.

#### Alert Combinations Examples

1. ** Conservative Setup **

- Enable all three checks

- Use "Once Per Bar Close"

- Timeframe Selection Example:

* First Check: 15 minutes

* Second Check: 1 hour (60 minutes)

* Third Check: 4 hours (240 minutes)

- Wider gaps between timeframes reduce noise and false signals

- Best for: Swing trading, beginners

2. ** Aggressive Setup **

- Enable first two checks only

- Use "Once Per Bar"

- Timeframe Selection Example:

* First Check: 5 minutes

* Second Check: 15 minutes

- Closer timeframes for quicker signals

- Best for: Day trading, experienced traders

3. ** Balanced Setup **

- Enable all checks

- Use "Once Per Bar"

- Timeframe Selection Example:

* First Check: 5 minutes

* Second Check: 15 minutes

* Third Check: 1 hour (60 minutes)

- Balanced spacing between timeframes

- Best for: All-around trading

### Visual Settings

#### Alert Visual Settings

1. ** Show Background Color (Default: true) **

- What it does: Highlights chart background when alerts trigger

- Benefits:

* Makes signals more visible

* Helps spot opportunities quickly

* Provides visual confirmation of alerts

- When to disable:

* If using multiple indicators

* When preferring a cleaner chart

* During manual backtesting

2. ** Background Transparency (Default: 90) **

- Range: 0 (solid) to 100 (invisible)

- Recommended Settings:

* Clean Charts: 90-95

* Multiple Indicators: 85-90

* Single Indicator: 80-85

- Tip: Adjust based on your chart's overall visibility

3. ** Background Colors **

- Bullish Background:

* Default: Green

* Indicates upward momentum

* Customizable to match your theme

- Bearish Background:

* Default: Red

* Indicates downward momentum

* Customizable to match your theme

#### Level Settings

1. ** Oversold Level (Default: 20) **

- Traditional Setting: 20

- Adjustable Range: 0-100

- Usage:

* Lower values (e.g., 10): More conservative

* Higher values (e.g., 30): More aggressive

- Trading Applications:

* Potential bullish reversal zone

* Support level in uptrends

* Entry point for long positions

2. ** Overbought Level (Default: 80) **

- Traditional Setting: 80

- Adjustable Range: 0-100

- Usage:

* Lower values (e.g., 70): More aggressive

* Higher values (e.g., 90): More conservative

- Trading Applications:

* Potential bearish reversal zone

* Resistance level in downtrends

* Exit point for long positions

3. ** Middle Line (Default: 50) **

- Purpose: Trend direction separator

- Applications:

* Above 50: Bullish territory

* Below 50: Bearish territory

* Crossing 50: Potential trend change

- Trading Uses:

* Trend confirmation

* Entry/exit trigger

* Risk management level

#### Color Settings

1. ** Bullish Color (Default: Green) **

- Used for:

* K-Line (Main stochastic line)

* Status symbols when trending up

* Trend labels for bullish conditions

- Customization:

* Choose colors that stand out

* Match your trading platform theme

* Consider color blindness accessibility

2. ** Bearish Color (Default: Red) **

- Used for:

* D-Line (Signal line)

* Status symbols when trending down

* Trend labels for bearish conditions

- Customization:

* Choose contrasting colors

* Ensure visibility on your chart

* Consider monitor settings

3. ** Neutral Color (Default: Gray) **

- Used for:

* Middle line (50 level)

- Customization:

* Should be less prominent

* Easy on the eyes

* Good background contrast

### Theme Settings

1. **Color Theme Options**

- Dark Theme (Default):

* Dark background with white text

* Optimized for dark chart backgrounds

* Reduces eye strain in low light

- Light Theme:

* Light background with black text

* Better visibility in bright conditions

- Custom Theme:

* Use your own color preferences

2. ** Available Theme Colors **

- Table Background

- Table Text

- Table Headers

Note: The theme affects only the table display colors. The stochastic lines and alert backgrounds use their own color settings.

### Table Settings

#### Position and Size

1. ** Table Position **

- Options:

* Top Right (Default)

* Middle Right

* Bottom Right

* Top Left

* Middle Left

* Bottom Left

- Considerations:

* Chart space utilization

* Personal preference

* Multiple monitor setups

2. ** Text Sizes **

- Title Size Options:

* Tiny: Minimal space usage

* Small: Compact but readable

* Normal (Default): Standard visibility

* Large: Enhanced readability

* Huge: Maximum visibility

- Data Size Options:

* Recommended: One size smaller than title

* Adjust based on screen resolution

* Consider viewing distance

3. ** Empowering Messages **

- Purpose:

* Maintain trading discipline

* Provide psychological support

* Remind of best practices

- Rotation:

* Changes every 5 bars

* Categories include:

- Market Wisdom

- Strategy & Discipline

- Mindset & Growth

- Technical Mastery

- Market Philosophy

## 4. Setting Up for Different Trading Styles

### Day Trading Setup

1. **Timeframes**

- Primary: 5, 15, 30 minutes

- Secondary: 1H, 4H

- Alert Settings: "Once Per Bar"

2. ** Stochastic Settings **

- Length: 8-14

- Smooth K/D: 2-3

- Alert Condition: Match market trend

3. ** Visual Settings **

- Background: Enabled

- Transparency: 85-90

- Theme: Based on trading hours

### Swing Trading Setup

1. ** Timeframes **

- Primary: 1H, 4H, Daily

- Secondary: Weekly

- Alert Settings: "Once Per Bar Close"

2. ** Stochastic Settings **

- Length: 14-21

- Smooth K/D: 3-5

- Alert Condition: "Both"

3. ** Visual Settings **

- Background: Optional

- Transparency: 90-95

- Theme: Personal preference

### Position Trading Setup

1. ** Timeframes **

- Primary: Daily, Weekly

- Secondary: Monthly

- Alert Settings: "Once Per Bar Close"

2. ** Stochastic Settings **

- Length: 21-30

- Smooth K/D: 5-7

- Alert Condition: "Both"

3. ** Visual Settings **

- Background: Disabled

- Focus on table data

- Theme: High contrast

## 5. Troubleshooting Guide

### Common Issues and Solutions

1. ** Too Many Alerts **

- Cause: Settings too sensitive

- Solutions:

* Increase timeframe intervals

* Use "Once Per Bar Close"

* Enable fewer timeframe checks

* Adjust stochastic length higher

2. ** Missed Signals **

- Cause: Settings too conservative

- Solutions:

* Decrease timeframe intervals

* Use "Once Per Bar"

* Enable more timeframe checks

* Adjust stochastic length lower

3. ** False Signals **

- Cause: Insufficient confirmation

- Solutions:

* Enable all three timeframe checks

* Use larger timeframe gaps

* Wait for bar close

* Confirm with price action

4. ** Visual Clarity Issues **

- Cause: Poor contrast or overlap

- Solutions:

* Adjust transparency

* Change theme settings

* Reposition table

* Modify color scheme

### Best Practices

1. ** Getting Started **

- Start with default settings

- Use "Both" alert condition

- Enable all timeframe checks

- Wait for bar close

- Monitor for a few days

2. ** Fine-Tuning **

- Adjust one setting at a time

- Document changes and results

- Test in different market conditions

- Find your optimal timeframe combination

- Balance sensitivity with reliability

3. ** Risk Management **

- Don't trade against major trends

- Confirm signals with price action

- Use appropriate position sizing

- Set clear stop losses

- Follow your trading plan

4. ** Regular Maintenance **

- Review settings weekly

- Adjust for market conditions

- Update color scheme for visibility

- Clean up chart regularly

- Maintain trading journal

## 6. Tips for Success

1. ** Entry Strategies **

- Wait for all timeframes to align

- Confirm with price action

- Use proper position sizing

- Consider market conditions

2. ** Exit Strategies **

- Trail stops using indicator levels

- Take partial profits at targets

- Honor your stop losses

- Don't fight the trend

3. ** Psychology **

- Stay disciplined with settings

- Don't override system signals

- Keep emotions in check

- Learn from each trade

4. ** Continuous Improvement **

- Record your trades

- Review performance regularly

- Adjust settings gradually

- Stay educated on markets

[ETH] Optimized Trend Strategy - Lorenzo SuperScalpStrategy Title: Optimized Trend Strategy - Lorenzo SuperScalp

Description:

The Optimized Trend Strategy is a comprehensive trading system tailored for Ethereum (ETH) and optimized for the 15-minute timeframe but adaptable to various timeframes. This strategy utilizes a combination of technical indicators—RSI, Bollinger Bands, and MACD—to identify and act on price trends efficiently, providing traders with actionable buy and sell signals based on market conditions.

Key Features:

Multi-Indicator Approach:

RSI (Relative Strength Index): Identifies overbought and oversold conditions to time market entries and exits.

Bollinger Bands: Acts as a dynamic support and resistance level, helping to pinpoint precise entry and exit zones.

MACD (Moving Average Convergence Divergence): Detects momentum changes through bullish and bearish crossovers.

Signal Conditions:

Buy Signal:

RSI is below 45 (indicating an oversold condition).

Price is near or below the lower Bollinger Band.

MACD bullish crossover occurs.

Sell Signal:

RSI is above 55 (indicating an overbought condition).

Price is near or above the upper Bollinger Band.

MACD bearish crossunder occurs.

Trade Execution Logic:

Long Trades: Opened when a buy signal flashes. If there’s an open short position, it is closed before opening a long.

Short Trades: Opened when a sell signal flashes. If there’s an open long position, it is closed before opening a short.

The strategy also ensures a minimum number of bars between consecutive trades to avoid rapid trading in choppy conditions.

Pyramiding Support:

Up to 3 consecutive trades in the same direction are allowed, enabling traders to scale into positions based on strong signals.

Visual Indicators:

RSI Levels: Dotted lines at 45 and 55 for quick reference to oversold and overbought levels.

Buy and Sell Signals: Visual markers on the chart indicate where trades are executed, ensuring clarity on entry and exit points.

Best Used For:

Swing Trading & Scalping: While optimized for the 15-minute timeframe, this strategy works across various timeframes, making it suitable for both short-term scalping and swing trading.

Crypto Trading: Tailored for Ethereum but effective for other cryptocurrencies due to its dynamic indicator setup.

ADX with Donchian Channels

The "ADX with Donchian Channels" indicator combines the Average Directional Index (ADX) with Donchian Channels to provide traders with a powerful tool for identifying trends and potential breakouts.

Features:

Average Directional Index (ADX):

The ADX is used to quantify the strength of a trend. It helps traders determine whether a market is trending or ranging.

Adjustable parameters for ADX smoothing and DI length allow traders to fine-tune the sensitivity of the trend strength measurement.

Donchian Channels on ADX:

Donchian Channels are applied directly to the ADX values to highlight the highest high and lowest low of the ADX over a specified period.

The upper and lower Donchian Channels can signal potential trend breakouts when the ADX value moves outside these bounds.

The middle Donchian Channel provides a reference for the average trend strength.

Visualization:

The indicator plots the ADX line in red to clearly display the trend strength.

The upper and lower Donchian Channels are plotted in blue, with a green middle line to represent the average.

The area between the upper and lower Donchian Channels is filled with a blue shade to visually emphasize the range of ADX values.

Default Settings for Scalping:

Donchian Channel Length: 10

Standard Deviation Multiplier: 1.58

ADX Length: 2

ADX Smoothing Length: 2

These default settings are optimized for scalping, offering a quick response to changes in trend strength and potential breakout signals. However, traders can adjust these settings to suit different trading styles and market conditions.

How to Use:

Trend Strength Identification: Use the ADX line to identify the strength of the current trend. Higher ADX values indicate stronger trends.

Breakout Signals: Monitor the ADX value in relation to the Donchian Channels. A breakout above the upper channel or below the lower channel can signal a potential trend continuation or reversal.

Range Identification: The filled area between the Donchian Channels provides a visual representation of the ADX range, helping traders identify when the market is ranging or trending.

This indicator is designed to enhance your trading strategy by combining trend strength measurement with breakout signals, making it a versatile tool for various market conditions.

BTC Correlation multiframesBTC Correlation indicator for scalping. Shows real-time correlation between the current asset and Bitcoin across three timeframes (30m, 1H, 4H), regardless of the chart timeframe you're viewing.

Green indicates strong positive correlation (asset follows BTC), yellow shows independence (ideal for scalping without BTC influence), and red indicates inverse correlation. Perfect for quick identification of whether your scalping target is moving independently from Bitcoin's price action.

The indicator compares percentage changes of the current candle in each timeframe, providing instant visual feedback on correlation strength through color-coded values.

Stabilized HMA ScalperStabilized HMA Scalper / Stab. HMA 2.0

Stabilized HMA Scalper is a visual trend-structure overlay indicator designed to highlight directional momentum, trend alignment, and market state through a combination of adaptive moving averages and contextual visual cues.

The indicator blends a Hull Moving Average (HMA) for responsiveness with an ALMA-based baseline filter to stabilize trend interpretation and reduce noise. The result is a clean, visually expressive framework for reading market structure directly on the price chart.

Core Design Philosophy

This script is built around trend confirmation and state visualization, not prediction or automation.

All elements are calculated on confirmed bar closes and do not repaint.

The indicator focuses on three analytical dimensions:

1. Dual Moving Average Structure

Hull Moving Average (HMA)

Acts as the primary momentum curve.

Designed for fast reaction to directional changes.

Slope behavior is used to infer momentum expansion or contraction.

ALMA Baseline Filter

Provides a stabilizing reference for broader trend context.

Helps distinguish directional movement from short-term fluctuations.

Used as a structural filter rather than a trigger mechanism.

2. Trend State Visualization

When HMA slope and price position relative to the ALMA baseline align, the indicator visually highlights the active market state:

Bullish alignment: upward momentum with supportive structure

Bearish alignment: downward momentum with confirming structure

Neutral / range: mixed conditions or transitional phases

A dynamic gradient fill between HMA and ALMA visually reinforces this alignment, offering an immediate understanding of trend strength and continuity.

3. Visual Markers & Labels

Discrete chart markers may appear at moments when momentum structure transitions into a new aligned state.

These markers are contextual annotations, intended to draw attention to changes in trend conditions rather than to provide standalone decisions.

They are based solely on historical price data and are fully non-repainting.

Dashboard

An optional on-chart dashboard summarizes the current market state classification (Bullish / Bearish / Range) based on the internal trend logic.

Position and size are fully configurable.

Designed for at-a-glance situational awareness.

Reflects the same logic used in the chart visuals.

Usage Disclaimer

This indicator is provided for technical analysis and educational purposes only.

It does not generate financial advice or guarantee outcomes and should be used as part of a broader analytical workflow.

RSI Chebyshev Pro with Goldilocks Fractals - NR [NPR21]RSI Chebyshev Pro with Goldilocks Fractals - Non-Repaint

CHART INFORMATION

Instrument: /MNQ (Micro E-mini Nasdaq-100 Futures)

Timeframe: 2-minute

Indicator: RSI Chebyshev Pro with Goldilocks Fractals - NR

THE PROBLEM

Standard RSI is too choppy and noisy – it whipsaws all over the place in volatile markets like futures, giving false oversold/overbought signals that burn you on entries. I was sick of missing real reversals or getting stopped out on fakeouts. I wanted something smoother that still catches the big momentum shifts without lagging too much, plus actual market structure to make it more reliable for quick trades.

WHAT MAKES THIS UNIQUE

Unlike basic RSI indicators that use simple moving average smoothing, this combines several advanced techniques that aren't commonly found together:

1. Chebyshev Type I Filtering - Signal processing mathematics (not basic EMAs) that kills noise while keeping real swings sharp. Most RSI smoothing just blurs everything - this keeps responsiveness without the chop.

2. MAMA Adaptive Period - The moving average adapts to actual market cycles using the MESA algorithm, not fixed periods that lag in changing conditions.

3. RSI Pivot Fractals - These aren't price fractals slapped onto RSI. The fractals detect pivots directly on RSI values at extreme levels, with signals appearing back at the exact pivot bar (not current bar), showing you where the actual reversal happened.

4. True Non-Repainting Implementation - Signals appear delayed BUT locked at the historical pivot location forever. What you see in backtests is exactly what appeared live - no vanishing signals, no shifting.

5. All-in-One Integration - Instead of running 3-4 separate indicators (RSI + fractals + patterns + smoothing), everything works together in a single, optimized calculation with confluence built in.

This isn't just RSI with some Williams Fractals thrown on top - it's a complete rethink of how to identify high-probability RSI reversals using signal processing and adaptive algorithms.

ORIGIN & ENHANCEMENTS

Original Source: ChartPrime RSI Chebyshev indicator

Converted & Enhanced by: NPR21

What I Added:

✅ Converted to Pine Script v6 - Made this available to TradingView traders

✅ Goldilocks Fractals - RSI alone doesn't tell you about price structure. These fractals nail those "just right" pivot points where highs/lows confirm. I kept seeing RSI extremes that reversed hard when they lined up with fractals - this was the missing piece for confluence.

✅ 100% Non-Repainting - I've been burned by repainters. You'd backtest something, looks amazing, then live it vanishes or shifts. Lost real money on that. This is rock-solid: signals show delayed but once they're there, they're locked forever. Makes backtesting trustworthy.

✅ Candlestick Patterns - Engulfing, Morning Star, Evening Star detection for confluence

✅ Customizable Visuals - BUY/SELL labels, multiple display styles, full color/size control

✅ Complete Alert System - Get notified on all signal types

HOW IT WORKS

Chebyshev Filtering:

Like putting noise-canceling on your RSI – smooths out jittery ups and downs from random price spikes without flattening into useless lag. It's signal processing math that keeps important swings sharp while killing BS noise. Way better than simple EMA smoothing that blurs everything.

The Components:

Ultra-Smooth RSI - Chebyshev Type I filtering + adaptive MAMA algorithm

Goldilocks Fractals - Pivot detection confirmed after N bars (default 5)

Pattern Recognition - Detects Engulfing, Morning/Evening Star patterns

Visual Styles - Candle Trend (hollow green/solid red) or traditional candles

SIGNAL DELAY vs REPAINTING

✅ THIS HAS SIGNAL DELAY (GOOD) - NOT REPAINTING (BAD)

Signal Delay:

Signals appear after N bars (default 5 bar delay)

Once visible, NEVER disappears or moves

Perfect for backtesting - 100% reliable

What you see in history is what you'd see live

Why the Delay:

To confirm a pivot, we need to see price didn't go lower/higher in the next N bars. This confirmation makes signals reliable. The delay is the price for trustworthy signals.

Want faster? Drop Fractal Periods to 2-3 (more signals, less confirmation).

HOW I TRADE IT

My /MNQ Scalping (1-3 min charts):

LONG: BUY label appears (down fractal + maybe morning star/engulfing) → Check RSI crossing up from oversold (<30) → Confirm with volume → Long with stop below fractal low → Target 1-2R

SHORT: SELL label (up fractal + maybe evening star) → RSI from overbought → Short with stop above

Filter: Only longs in uptrends (watch the MA). Exit partials if momentum fades.

Best Timeframes: 1-5 min for futures scalping. Works on 15 min for swings but for pure scalping, stay under 5 min in high-vol sessions.

SETTINGS I USE

Standard Setup:

Length: 24, Smoothing: 3

Auto MA: ON, Multiplier: 1-2

Fractal Periods: 5 (good confirmation)

Choppy Days:

Smoothing to 5

Aggressive:

Fractal Periods to 3

Pro Tip: Pair with volume or price EMA. Love when fractal BUY + engulfing bull align. Use Candle Trend style. Test on demo first.

KEY SETTINGS

RSI: Length (24), Smoothing (3), Auto MA, Style (Candle/Candle Trend)

Fractals: Periods (5 = more reliable, 3 = faster/riskier), Label colors/sizes, Offsets

Alerts: All signals fire only on confirmed, non-repainting events

DISCLAIMERS

⚠️ Tool, not a complete system - use proper risk management

⚠️ Signals have delay for reliability - not for instant entries

⚠️ Best with price action, volume, other analysis

⚠️ Test on demo before live trading

Questions? Comment below!

NPR21

RSI Chebyshev Pro with Goldilocks Fractals - NR [NPR21]RSI Chebyshev Pro with Goldilocks Fractals - Non-Repaint

----------------------------------------------------------------------------------------------------------------------

CHART INFORMATION

Instrument: /MNQ (Micro E-mini Nasdaq-100 Futures)

Timeframe: 2-minute

Indicator: RSI Chebyshev Pro with Goldilocks Fractals - NR

----------------------------------------------------------------------------------------------------------------------

THE PROBLEM

Standard RSI is too choppy and noisy – it whipsaws all over the place in volatile markets like futures, giving false oversold/overbought signals that burn you on entries. I was sick of missing real reversals or getting stopped out on fakeouts. I wanted something smoother that still catches the big momentum shifts without lagging too much, plus actual market structure to make it more reliable for quick trades.

WHAT MAKES THIS UNIQUE

Unlike basic RSI indicators that use simple moving average smoothing, this combines several advanced techniques that aren't commonly found together:

1. Chebyshev Type I Filtering - Signal processing mathematics (not basic EMAs) that kills noise while keeping real swings sharp. Most RSI smoothing just blurs everything - this keeps responsiveness without the chop.

2. MAMA Adaptive Period - The moving average adapts to actual market cycles using the MESA algorithm, not fixed periods that lag in changing conditions.

3. RSI Pivot Fractals - These aren't price fractals slapped onto RSI. The fractals detect pivots directly on RSI values at extreme levels, with signals appearing back at the exact pivot bar (not current bar), showing you where the actual reversal happened.

4. True Non-Repainting Implementation - Signals appear delayed BUT locked at the historical pivot location forever. What you see in backtests is exactly what appeared live - no vanishing signals, no shifting.

5. All-in-One Integration - Instead of running 3-4 separate indicators (RSI + fractals + patterns + smoothing), everything works together in a single, optimized calculation with confluence built in.

This isn't just RSI with some Williams Fractals thrown on top - it's a complete rethink of how to identify high-probability RSI reversals using signal processing and adaptive algorithms.

ORIGIN & ENHANCEMENTS

Original Source: ChartPrime RSI Chebyshev indicator

Converted & Enhanced by: NPR21

What I Added:

✅ Converted to Pine Script v6 - Made this available to TradingView traders

✅ Goldilocks Fractals - RSI alone doesn't tell you about price structure. These fractals nail those "just right" pivot points where highs/lows confirm. I kept seeing RSI extremes that reversed hard when they lined up with fractals - this was the missing piece for confluence.

✅ 100% Non-Repainting - I've been burned by repainters. You'd backtest something, looks amazing, then live it vanishes or shifts. Lost real money on that. This is rock-solid: signals show delayed but once they're there, they're locked forever. Makes backtesting trustworthy.

✅ Candlestick Patterns - Engulfing, Morning Star, Evening Star detection for confluence

✅ Customizable Visuals - BUY/SELL labels, multiple display styles, full color/size control

✅ Complete Alert System - Get notified on all signal types

HOW IT WORKS

Chebyshev Filtering:

Like putting noise-canceling on your RSI – smooths out jittery ups and downs from random price spikes without flattening into useless lag. It's signal processing math that keeps important swings sharp while killing BS noise. Way better than simple EMA smoothing that blurs everything.

The Components:

Ultra-Smooth RSI - Chebyshev Type I filtering + adaptive MAMA algorithm

Goldilocks Fractals - Pivot detection confirmed after N bars (default 5)

Pattern Recognition - Detects Engulfing, Morning/Evening Star patterns

Visual Styles - Candle Trend (hollow green/solid red) or traditional candles

SIGNAL DELAY vs REPAINTING

✅ THIS HAS SIGNAL DELAY (GOOD) - NOT REPAINTING (BAD)

Signal Delay:

Signals appear after N bars (default 5 bar delay)

Once visible, NEVER disappears or moves

Perfect for backtesting - 100% reliable

What you see in history is what you'd see live

Why the Delay:

To confirm a pivot, we need to see price didn't go lower/higher in the next N bars. This confirmation makes signals reliable. The delay is the price for trustworthy signals.

Want faster? Drop Fractal Periods to 2-3 (more signals, less confirmation).

HOW I TRADE IT

My /MNQ Scalping (1-3 min charts):

LONG: BUY label appears (down fractal + maybe morning star/engulfing) → Check RSI crossing up from oversold (<30) → Confirm with volume → Long with stop below fractal low → Target 1-2R

SHORT: SELL label (up fractal + maybe evening star) → RSI from overbought → Short with stop above

Filter: Only longs in uptrends (watch the MA). Exit partials if momentum fades.

Best Timeframes: 1-5 min for futures scalping. Works on 15 min for swings but for pure scalping, stay under 5 min in high-vol sessions.

SETTINGS I USE

Standard Setup:

Length: 24, Smoothing: 3

Auto MA: ON, Multiplier: 1-2

Fractal Periods: 5 (good confirmation)

Choppy Days:

Smoothing to 5

Aggressive:

Fractal Periods to 3

Pro Tip: Pair with volume or price EMA. Love when fractal BUY + engulfing bull align. Use Candle Trend style. Test on demo first.

KEY SETTINGS

RSI: Length (24), Smoothing (3), Auto MA, Style (Candle/Candle Trend)

Fractals: Periods (5 = more reliable, 3 = faster/riskier), Label colors/sizes, Offsets

Alerts: All signals fire only on confirmed, non-repainting events

DISCLAIMERS

⚠️ Tool, not a complete system - use proper risk management

⚠️ Signals have delay for reliability - not for instant entries

⚠️ Best with price action, volume, other analysis

⚠️ Test on demo before live trading

Questions? Comment below!

NPR21

RSI Chebyshev Pro with Goldilocks Fractals - NR [NPR21]RSI Chebyshev Pro with Goldilocks Fractals - Non-Repaint

==================================================================================

**CHART INFORMATION**

The example chart shown displays:

- Instrument: /MNQ (Micro E-mini Nasdaq-100 Futures)

- Timeframe: 2-minute

- Indicator: RSI Chebyshev Pro with Goldilocks Fractals - NR

==================================================================================

═════════════════════════════════════════════════════════════

THE PROBLEM

Standard RSI is too choppy and noisy – it whipsaws all over the place in volatile markets like futures, giving false oversold/overbought signals that burn you on entries. I was sick of missing real reversals or getting stopped out on fakeouts. I wanted something smoother that still catches the big momentum shifts without lagging too much, plus actual market structure to make it more reliable for quick trades.

═════════════════════════════════════════════════════════════

WHAT MAKES THIS UNIQUE

Unlike basic RSI indicators that use simple moving average smoothing, this combines several advanced techniques that aren't commonly found together:

1. Chebyshev Type I Filtering - Signal processing mathematics (not basic EMAs) that kills noise while keeping real swings sharp. Most RSI smoothing just blurs everything - this keeps responsiveness without the chop.

2. MAMA Adaptive Period - The moving average adapts to actual market cycles using the MESA algorithm, not fixed periods that lag in changing conditions.

3. RSI Pivot Fractals - These aren't price fractals slapped onto RSI. The fractals detect pivots directly on RSI values at extreme levels, with signals appearing back at the exact pivot bar (not current bar), showing you where the actual reversal happened.

4. True Non-Repainting Implementation - Signals appear delayed BUT locked at the historical pivot location forever. What you see in backtests is exactly what appeared live - no vanishing signals, no shifting.

5. All-in-One Integration - Instead of running 3-4 separate indicators (RSI + fractals + patterns + smoothing), everything works together in a single, optimized calculation with confluence built in.

This isn't just RSI with some Williams Fractals thrown on top - it's a complete rethink of how to identify high-probability RSI reversals using signal processing and adaptive algorithms.

═════════════════════════════════════════════════════════════

ORIGIN & ENHANCEMENTS

Original Source: ChartPrime RSI Chebyshev indicator

Converted & Enhanced by: NPR21

What I Added:

✅ Converted to Pine Script v6 - Made this available to TradingView traders

✅ Goldilocks Fractals - RSI alone doesn't tell you about price structure. These fractals nail those "just right" pivot points where highs/lows confirm. I kept seeing RSI extremes that reversed hard when they lined up with fractals - this was the missing piece for confluence.

✅ 100% Non-Repainting - I've been burned by repainters. You'd backtest something, looks amazing, then live it vanishes or shifts. Lost real money on that. This is rock-solid: signals show delayed but once they're there, they're locked forever. Makes backtesting trustworthy.

✅ Candlestick Patterns - Engulfing, Morning Star, Evening Star detection for confluence

✅ Customizable Visuals - BUY/SELL labels, multiple display styles, full color/size control

✅ Complete Alert System - Get notified on all signal types

═════════════════════════════════════════════════════════════

HOW IT WORKS

Chebyshev Filtering:

Like putting noise-canceling on your RSI – smooths out jittery ups and downs from random price spikes without flattening into useless lag. It's signal processing math that keeps important swings sharp while killing BS noise. Way better than simple EMA smoothing that blurs everything.

The Components:

Ultra-Smooth RSI - Chebyshev Type I filtering + adaptive MAMA algorithm

Goldilocks Fractals - Pivot detection confirmed after N bars (default 5)

Pattern Recognition - Detects Engulfing, Morning/Evening Star patterns

Visual Styles - Candle Trend (hollow green/solid red) or traditional candles

═════════════════════════════════════════════════════════════

SIGNAL DELAY vs REPAINTING

✅ THIS HAS SIGNAL DELAY (GOOD) - NOT REPAINTING (BAD)

Signal Delay:

Signals appear after N bars (default 5 bar delay)

Once visible, NEVER disappears or moves

Perfect for backtesting - 100% reliable

What you see in history is what you'd see live

Why the Delay:

To confirm a pivot, we need to see price didn't go lower/higher in the next N bars. This confirmation makes signals reliable. The delay is the price for trustworthy signals.

Want faster? Drop Fractal Periods to 2-3 (more signals, less confirmation).

════════════════════════════════════════════════════════════

HOW I TRADE IT

My /MNQ Scalping (1-3 min charts):

LONG: BUY label appears (down fractal + maybe morning star/engulfing) → Check RSI crossing up from oversold (<30) → Confirm with volume → Long with stop below fractal low → Target 1-2R

SHORT: SELL label (up fractal + maybe evening star) → RSI from overbought → Short with stop above

Filter: Only longs in uptrends (watch the MA). Exit partials if momentum fades.

Best Timeframes: 1-5 min for futures scalping. Works on 15 min for swings but for pure scalping, stay under 5 min in high-vol sessions.

═════════════════════════════════════════════════════════════

SETTINGS I USE

Standard Setup:

Length: 24, Smoothing: 3

Auto MA: ON, Multiplier: 1-2

Fractal Periods: 5 (good confirmation)

Choppy Days: Smoothing to 5

Aggressive: Fractal Periods to 3

Pro Tip: Pair with volume or price EMA. Love when fractal BUY + engulfing bull align. Use Candle Trend style. Test on demo first.

═════════════════════════════════════════════════════════════

KEY SETTINGS

RSI: Length (24), Smoothing (3), Auto MA, Style (Candle/Candle Trend)

Fractals: Periods (5 = more reliable, 3 = faster/riskier), Label colors/sizes, Offsets

Alerts: All signals fire only on confirmed, non-repainting events

═════════════════════════════════════════════════════════════

DISCLAIMERS

⚠️ Tool, not a complete system - use proper risk management

⚠️ Signals have delay for reliability - not for instant entries

⚠️ Best with price action, volume, other analysis

⚠️ Test on demo before live trading

═════════════════════════════════════════════════════════════

Questions? Comment below!

NPR21

Weekend Hunter Ultimate v6.2 Weekend Hunter Ultimate v6.2 - Automated Crypto Weekend Trading System

OVERVIEW:

Specialized trading strategy designed for cryptocurrency weekend markets (Saturday-Sunday) when institutional traders are typically offline and market dynamics differ significantly from weekdays. Optimized for 15-minute timeframe execution with multi-timeframe confluence analysis.

KEY FEATURES:

- Weekend-Only Trading: Automatically activates during configurable weekend hours

- Dynamic Leverage: 5-20x leverage adjusted based on market safety and signal confidence

- Multi-Timeframe Analysis: Combines 4H trend, 1H momentum, and 15M execution

- 10 Pre-configured Crypto Pairs: BTC, ETH, LINK, XRP, DOGE, SOL, AVAX, PEPE, TON, POL

- Position & Risk Management: Max 4 concurrent positions, -30% account protection

- Smart Trailing Stops: Protects profits when approaching targets

RISK MANAGEMENT:

- Maximum daily loss: 5% (configurable)

- Maximum weekend loss: 15% (configurable)

- Per-position risk: Capped at 120-156 USDT

- Emergency stops for flash crashes (8% moves)

- Consecutive loss protection (4 losses = pause)

TECHNICAL INDICATORS:

- CVD (Cumulative Volume Delta) divergence detection

- ATR-based dynamic stop loss and take profit

- RSI, MACD, Bollinger Bands confluence

- Volume surge confirmation (1.5x average)

- Weekend liquidity adjustments

INTEGRATION:

- Designed for Bybit Futures (0.075% taker fee)

- WunderTrading webhook compatibility via JSON alerts

- Minimum position size: 120 USDT (Bybit requirement)

- Initial capital: $500 recommended

TARGET METRICS:

- Win rate target: 65%

- Average win: 5.5%

- Average loss: 1.8%

- Risk-reward ratio: ~3:1

IMPORTANT DISCLAIMERS:

- Past performance does not guarantee future results

- Leveraged trading carries substantial risk of loss

- Weekend crypto markets have 13% of normal liquidity

- Not suitable for traders who cannot afford to lose their entire investment

- Requires continuous monitoring and adjustment

USAGE:

1. Apply to 15-minute charts only

2. Configure weekend hours for your timezone

3. Set up webhook alerts for automation

4. Monitor performance table in top-right corner

5. Adjust parameters based on your risk tolerance

This is an experimental strategy for educational purposes. Always test with small amounts first and never invest more than you can afford to lose completely.

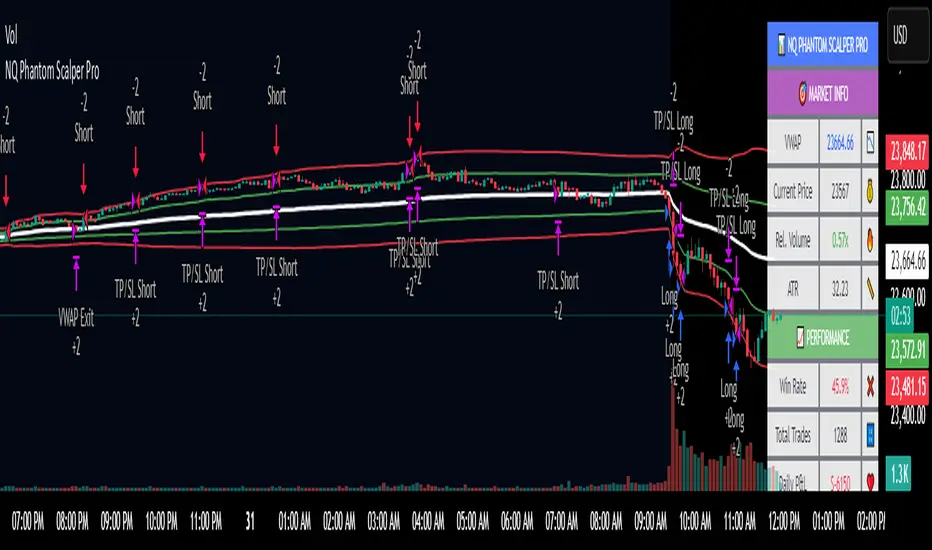

NQ Phantom Scalper Pro# 👻 NQ Phantom Scalper Pro

**Advanced VWAP Mean Reversion Strategy with Volume Confirmation**

## 🎯 Strategy Overview

The NQ Phantom Scalper Pro is a sophisticated mean reversion strategy designed specifically for Nasdaq 100 (NQ) futures scalping. This strategy combines Volume Weighted Average Price (VWAP) bands with intelligent volume spike detection to identify high-probability reversal opportunities during optimal market hours.

## 🔧 Key Features

### VWAP Band System

- **Dynamic VWAP Bands**: Automatically adjusting standard deviation bands based on intraday volatility

- **Multiple Band Levels**: Configurable Band #1 (entry trigger) and Band #2 (profit target reference)

- **Flexible Anchoring**: Choose from Session, Week, Month, Quarter, or Year-based VWAP calculations

### Volume Intelligence

- **Volume Spike Detection**: Only triggers entries when volume exceeds SMA by configurable multiplier

- **Relative Volume Display**: Real-time volume strength indicator in info panel

- **Optional Volume Filter**: Can be disabled for testing alternative setups

### Advanced Time Management

- **12-Hour Format**: User-friendly time inputs (9 AM - 4 PM default)

- **Lunch Filter**: Automatically avoids low-liquidity lunch period (12-2 PM)

- **Visual Time Zones**: Color-coded background for active/inactive periods

- **Market Hours Focus**: Optimized for peak NQ trading sessions

### Smart Risk Management

- **ATR-Based Stops**: Volatility-adjusted stop losses using Average True Range

- **Dual Exit Strategy**: VWAP mean reversion + fixed profit targets

- **Adjustable Risk-Reward**: Configurable target ratio to opposite VWAP band

- **Position Sizing**: Percentage-based equity allocation

### Optional Trend Filter

- **EMA Trend Alignment**: Optional trend filter to avoid counter-trend trades

- **Configurable Period**: Adjustable EMA length for trend determination

- **Toggle Functionality**: Enable/disable based on market conditions

## 📊 How It Works

### Entry Logic

**Long Entries**: Triggered when price touches lower VWAP band + volume spike during active hours

**Short Entries**: Triggered when price touches upper VWAP band + volume spike during active hours

### Exit Strategy

1. **VWAP Mean Reversion**: Early exit when price returns to VWAP center line

2. **Profit Target**: Fixed target based on percentage to opposite VWAP band

3. **Stop Loss**: ATR-based protective stop

### Visual Elements

- **VWAP Center Line**: Blue line showing volume-weighted fair value

- **Green Bands**: Entry trigger levels (Band #1)

- **Red Bands**: Extended levels for target reference (Band #2)

- **Orange EMA**: Trend filter line (when enabled)

- **Background Colors**: Yellow (lunch), Gray (after hours), Clear (active trading)

- **Info Panel**: Real-time metrics display

## ⚙️ Recommended Settings

### Timeframes

- **Primary**: 1-5 minute charts for scalping

- **Validation**: Test on 15-minute for swing applications

### Market Conditions

- **Best Performance**: Ranging/choppy markets with good volume

- **Trend Markets**: Enable trend filter to avoid counter-trend trades

- **High Volatility**: Increase ATR multiplier for stops

### Session Optimization

- **Pre-Market**: Generally avoided (low volume)

- **Morning Session**: 9:30 AM - 12:00 PM (high activity)

- **Lunch Period**: 12:00 PM - 2:00 PM (filtered by default)

- **Afternoon Session**: 2:00 PM - 4:00 PM (good volume)

- **After Hours**: Generally avoided (wide spreads)

## ⚠️ Risk Disclaimer

This strategy is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Trading futures involves substantial risk of loss and is not suitable for all investors. Users should:

- Thoroughly backtest on historical data

- Start with small position sizes

- Understand the risks of leveraged trading

- Consider transaction costs and slippage

- Never risk more than you can afford to lose

## 📈 Performance Tips

1. **Volume Threshold**: Adjust volume multiplier based on average NQ volume patterns

2. **Band Sensitivity**: Modify band multipliers for different volatility regimes

3. **Time Filters**: Customize trading hours based on your timezone and preferences

4. **Trend Alignment**: Use trend filter during strong directional markets

5. **Risk Management**: Always maintain consistent position sizing and risk parameters

**Version**: 6.0 Compatible

**Asset**: Optimized for NASDAQ 100 Futures (NQ)

**Style**: Mean Reversion Scalping

**Frequency**: High-Frequency Trading Ready

Reflexivity Resonance Factor (RRF) - Quantum Flow Reflexivity Resonance Factor (RRF) – Quantum Flow

See the Feedback Loops. Anticipate the Regime Shift.

What is the RRF – Quantum Flow?

The Reflexivity Resonance Factor (RRF) – Quantum Flow is a next-generation market regime detector and energy oscillator, inspired by George Soros’ theory of reflexivity and modern complexity science. It is designed for traders who want to visualize the hidden feedback loops between market perception and participation, and to anticipate explosive regime shifts before they unfold.

Unlike traditional oscillators, RRF does not just measure price momentum or volatility. Instead, it models the dynamic feedback between how the market perceives itself (perception) and how it acts on that perception (participation). When these feedback loops synchronize, they create “resonance” – a state of amplified reflexivity that often precedes major market moves.

Theoretical Foundation

Reflexivity: Markets are not just driven by external information, but by participants’ perceptions and their actions, which in turn influence future perceptions. This feedback loop can create self-reinforcing trends or sudden reversals.

Resonance: When perception and participation align and reinforce each other, the market enters a high-energy, reflexive state. These “resonance” events often mark the start of new trends or the climax of existing ones.

Energy Field: The indicator quantifies the “energy” of the market’s reflexivity, allowing you to see when the crowd is about to act in unison.

How RRF – Quantum Flow Works

Perception Proxy: Measures the rate of change in price (ROC) over a configurable period, then smooths it with an EMA. This models how quickly the market’s collective perception is shifting.

Participation Proxy: Uses a fast/slow ATR ratio to gauge the intensity of market participation (volatility expansion/contraction).

Reflexivity Core: Multiplies perception and participation to model the feedback loop.

Resonance Detection: Applies Z-score normalization to the absolute value of reflexivity, highlighting when current feedback is unusually strong compared to recent history.

Energy Calculation: Scales resonance to a 0–100 “energy” value, visualized as a dynamic background.

Regime Strength: Tracks the percentage of bars in a lookback window where resonance exceeded the threshold, quantifying the persistence of reflexive regimes.

Inputs:

🧬 Core Parameters

Perception Period (pp_roc_len, default 14): Lookback for price ROC.

Lower (5–10): More sensitive, for scalping (1–5min).

Default (14): Balanced, for 15min–1hr.

Higher (20–30): Smoother, for 4hr–daily.

Perception Smooth (pp_smooth_len, default 7): EMA smoothing for perception.

Lower (3–5): Faster, more detail.

Default (7): Balanced.

Higher (10–15): Smoother, less noise.

Participation Fast (prp_fast_len, default 7): Fast ATR for immediate volatility.

5–7: Scalping.

7–10: Day trading.

10–14: Swing trading.

Participation Slow (prp_slow_len, default 21): Slow ATR for baseline volatility.

Should be 2–4x fast ATR.

Default (21): Works with fast=7.

⚡ Signal Configuration

Resonance Window (res_z_window, default 50): Z-score lookback for resonance normalization.

20–30: More reactive.

50: Medium-term.

100+: Very stable.

Primary Threshold (rrf_threshold, default 1.5): Z-score level for “Active” resonance.

1.0–1.5: More signals.

1.5: Balanced.

2.0+: Only strong signals.

Extreme Threshold (rrf_extreme, default 2.5): Z-score for “Extreme” resonance.

2.5: Major regime shifts.

3.0+: Only the most extreme.

Regime Window (regime_window, default 100): Lookback for regime strength (% of bars with resonance spikes).

Higher: More context, slower.

Lower: Adapts quickly.

🎨 Visual Settings

Show Resonance Flow (show_flow, default true): Plots the main resonance line with glow effects.

Show Signal Particles (show_particles, default true): Circular markers at active/extreme resonance points.