MACD Liquidity Tracker Strategy [Quant Trading]MACD Liquidity Tracker Strategy

Overview

The MACD Liquidity Tracker Strategy is an enhanced trading system that transforms the traditional MACD indicator into a comprehensive momentum-based strategy with advanced visual signals and risk management. This strategy builds upon the original MACD Liquidity Tracker System indicator by TheNeWSystemLqtyTrckr , converting it into a fully automated trading strategy with improved parameters and additional features.

What Makes This Strategy Original

This strategy significantly enhances the basic MACD approach by introducing:

Four distinct system types for different market conditions and trading styles

Advanced color-coded histogram visualization with four dynamic colors showing momentum strength and direction

Integrated trend filtering using 9 different moving average types

Comprehensive risk management with customizable stop-loss and take-profit levels

Multiple alert systems for entry signals, exits, and trend conditions

Flexible signal display options with customizable entry markers

How It Works

Core MACD Calculation

The strategy uses a fully customizable MACD configuration with traditional default parameters:

Fast MA : 12 periods (customizable, minimum 1, no maximum limit)

Slow MA : 26 periods (customizable, minimum 1, no maximum limit)

Signal Line : 9 periods (customizable, now properly implemented and used)

Cryptocurrency Optimization : The strategy's flexible parameter system allows for significant optimization across different crypto assets. Traditional MACD settings (12/26/9) often generate excessive noise and false signals in volatile crypto markets. By using slower, more smoothed parameters, traders can capture meaningful momentum shifts while filtering out market noise.

Example - DOGE Optimization (45/80/290 settings) :

• Performance : Optimized parameters yielding exceptional backtesting results with 29,800% PnL

• Why it works : DOGE's high volatility and social sentiment-driven price action benefits from heavily smoothed indicators

• Timeframes : Particularly effective on 30-minute and 4-hour charts for swing trading

• Logic : The very slow parameters filter out noise and capture only the most significant trend changes

Other Optimizable Cryptocurrencies : This parameter flexibility makes the strategy highly effective for major altcoins including SUI, SEI, LINK, Solana (SOL) , and many others. Each crypto asset can benefit from custom parameter tuning based on its unique volatility profile and trading characteristics.

Four Trading System Types

1. Normal System (Default)

Long signals : When MACD line is above the signal line

Short signals : When MACD line is below the signal line

Best for : Swing trading and capturing longer-term trends in stable markets

Logic : Traditional MACD crossover approach using the signal line

2. Fast System

Long signals : Bright Blue OR Dark Magenta (transparent) histogram colors

Short signals : Dark Blue (transparent) OR Bright Magenta histogram colors

Best for : Scalping and high-volatility markets (crypto, forex)

Logic : Leverages early momentum shifts based on histogram color changes

3. Safe System

Long signals : Only Bright Blue histogram color (strongest bullish momentum)

Short signals : All other colors (Dark Blue, Bright Magenta, Dark Magenta)

Best for : Risk-averse traders and choppy markets

Logic : Prioritizes only the strongest bullish signals while treating everything else as bearish

4. Crossover System

Long signals : MACD line crosses above signal line

Short signals : MACD line crosses below signal line

Best for : Precise timing entries with traditional MACD methodology

Logic : Pure crossover signals for more precise entry timing

Color-Coded Histogram Logic

The strategy uses four distinct colors to visualize momentum:

🔹 Bright Blue : MACD > 0 and rising (strong bullish momentum)

🔹 Dark Blue (Transparent) : MACD > 0 but falling (weakening bullish momentum)

🔹 Bright Magenta : MACD < 0 and falling (strong bearish momentum)

🔹 Dark Magenta (Transparent) : MACD < 0 but rising (weakening bearish momentum)

Trend Filter Integration

The strategy includes an advanced trend filter using 9 different moving average types:

SMA (Simple Moving Average)

EMA (Exponential Moving Average) - Default

WMA (Weighted Moving Average)

HMA (Hull Moving Average)

RMA (Running Moving Average)

LSMA (Least Squares Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

VIDYA (Variable Index Dynamic Average)

Default Settings : 50-period EMA for trend identification

Visual Signal System

Entry Markers : Blue triangles (▲) below candles for long entries, Magenta triangles (▼) above candles for short entries

Candle Coloring : Price candles change color based on active signals (Blue = Long, Magenta = Short)

Signal Text : Optional "Long" or "Short" text inside entry triangles (toggleable)

Trend MA : Gray line plotted on main chart for trend reference

Parameter Optimization Examples

DOGE Trading Success (Optimized Parameters) :

Using 45/80/290 MACD settings with 50-period EMA trend filter has shown exceptional results on DOGE:

Performance : Backtesting results showing 29,800% PnL demonstrate the power of proper parameter optimization

Reasoning : DOGE's meme-driven volatility and social sentiment spikes create significant noise with traditional MACD settings

Solution : Very slow parameters (45/80/290) filter out social media-driven price spikes while capturing only major momentum shifts

Optimal Timeframes : 30-minute and 4-hour charts for swing trading opportunities

Result : Exceptionally clean signals with minimal false entries during DOGE's characteristic pump-and-dump cycles

Multi-Crypto Adaptability :

The same optimization principles apply to other major cryptocurrencies:

SUI : Benefits from smoothed parameters due to newer coin volatility patterns

SEI : Requires adjustment for its unique DeFi-related price movements

LINK : Oracle news events create price spikes that benefit from noise filtering

Solana (SOL) : Network congestion events and ecosystem developments need smoothed detection

General Rule : Higher volatility coins typically benefit from very slow MACD parameters (40-50 / 70-90 / 250-300 ranges)

Key Input Parameters

System Type : Choose between Fast, Normal, Safe, or Crossover (Default: Normal)

MACD Fast MA : 12 periods default (no maximum limit, consider 40-50 for crypto optimization)

MACD Slow MA : 26 periods default (no maximum limit, consider 70-90 for crypto optimization)

MACD Signal MA : 9 periods default (now properly utilized, consider 250-300 for crypto optimization)

Trend MA Type : EMA default (9 options available)

Trend MA Length : 50 periods default (no maximum limit)

Signal Display : Both, Long Only, Short Only, or None

Show Signal Text : True/False toggle for entry marker text

Trading Applications

Recommended Use Cases

Momentum Trading : Capitalize on strong directional moves using the color-coded system

Trend Following : Combine MACD signals with trend MA filter for higher probability trades

Scalping : Use "Fast" system type for quick entries in volatile markets

Swing Trading : Use "Normal" or "Safe" system types for longer-term positions

Cryptocurrency Trading : Optimize parameters for individual crypto assets (e.g., 45/80/290 for DOGE, custom settings for SUI, SEI, LINK, SOL)

Market Suitability

Volatile Markets : Forex, crypto, indices (recommend "Fast" system or smoothed parameters)

Stable Markets : Stocks, ETFs (recommend "Normal" or "Safe" system)

All Timeframes : Effective from 1-minute charts to daily charts

Crypto Optimization : Each major cryptocurrency (DOGE, SUI, SEI, LINK, SOL, etc.) can benefit from custom parameter tuning. Consider slower MACD parameters for noise reduction in volatile crypto markets

Alert System

The strategy provides comprehensive alerts for:

Entry Signals : Long and short entry triangle appearances

Exit Signals : Position exit notifications

Color Changes : Individual histogram color alerts

Trend Conditions : Price above/below trend MA alerts

Strategy Parameters

Default Settings

Initial Capital : $1,000

Position Size : 100% of equity

Commission : 0.1%

Slippage : 3 points

Date Range : January 1, 2018 to December 31, 2069

Risk Management (Optional)

Stop Loss : Disabled by default (customizable percentage-based)

Take Profit : Disabled by default (customizable percentage-based)

Short Trades : Disabled by default (can be enabled)

Important Notes and Limitations

Backtesting Considerations

Uses realistic commission (0.1%) and slippage (3 points)

Default position sizing uses 100% equity - adjust based on risk tolerance

Stop-loss and take-profit are disabled by default to show raw strategy performance

Strategy does not use lookahead bias or future data

Risk Warnings

Past performance does not guarantee future results

MACD-based strategies may produce false signals in ranging markets

Consider combining with additional confluences like support/resistance levels

Test thoroughly on demo accounts before live trading

Adjust position sizing based on your risk management requirements

Technical Limitations

Strategy does not work on non-standard chart types (Heikin Ashi, Renko, etc.)

Signals are based on close prices and may not reflect intraday price action

Multiple rapid signals in volatile conditions may result in overtrading

Credits and Attribution

This strategy is based on the original "MACD Liquidity Tracker System" indicator created by TheNeWSystemLqtyTrckr . This strategy version includes significant enhancements:

Complete strategy implementation with entry/exit logic

Addition of the "Crossover" system type

Proper implementation and utilization of the MACD signal line

Enhanced risk management features

Improved parameter flexibility with no artificial maximum limits

Additional alert systems for comprehensive trade management

The original indicator's core color logic and visual system have been preserved while expanding functionality for automated trading applications.

ค้นหาในสคริปต์สำหรับ "range"

Daily Bias on 5 minutes Reversal StrategyThis strategy combines higher-timeframe bias (daily and 1-hour) with 5-minute reversal signals to identify intraday trades. It aims to capitalize on false breakouts of the previous day's high/low, with strict risk management (Strict position sizing, max risk cap, and R:R enforcement), Avoids Over-Trading (1 trade/day rule prevents chasing), SL buffer adapts to volatility.

#1. This strategy does not utilize indicators. We will use the daily (D) price range and look for breakout attempts and rejections at the extreme points on the lower time frame (1h). If rejection occurs, it establishes our bias (bullish or bearish). For final confirmation, we move to the 5-minute timeframe to observe attempts to retest that daily price range. If significant rejection occurs again, that becomes our entry point.

#2. When rejection occurs, the 1-hour candle may form a new extreme point (low/high). Therefore, we will no longer use the daily price range as our trade exit point but instead the new extreme level established after the breakout attempt and price rejection.

To prevent premature trade exits, we also add an SL buffer using ATR while still capping the maximum acceptable risk per trade (as a percentage). Take profit is calculated using a risk-to-reward ratio, with a default setting of 1.5x.

#3. Key Input Parameters

a. Timeframes :

1. Daily TF ((Anchor for daily high/low (default: D).)

2. 1H Bias TF (Bias confirmation timeframe (default: 60))

3. Execution TF (Entry signal timeframe (default: 5, should match chart).

b. Trade Management

1. SL Buffer ATR Multiplier (Buffer beyond swing low/high (default: 6.0))

2. Min ATR Threshold (Minimum buffer size (default: 1.0))

3. Risk Reward Ratio (TP distance multiplier (default: 1.5))

4. Max Risk Allowed (Max risk % of entry (default: 3.0%))

Lookback Bars for SL Bars for swing low/high (default: 60))

c. Break Thresholds

1. 1H Candle Break Threshold (ATR multiplier for 1H break (default: 0.75))

2. 5M Candle Break Threshold (ATR multiplier for 5M break (default: 0.5))

Gabriel's Price Action Strategy🧠 Gabriel's Price Action Strategy — Smart Signal Sequence with Dynamic Risk Control

Created by: OneWallStreetQuant

Strategy Type: Momentum-based Sequence Logic + Smart Volume & RSI Filters

Ideal For: Intraday scalping, swing trading, and momentum trend entries on stocks, forex, crypto, indices.

🚀 Overview

Gabriel's Price Action Strategy is a multi-layered, logic-driven trading system that combines:

✅ Candle Sequence Detection: Detects persistent bullish/bearish momentum using a smart configurable sequence of green/red candles.

✅ Structure Break Filtering: Prevents entries if recent price invalidates the momentum setup (e.g., a red candle breaks a bullish low).

✅ Custom Volume Engine: Integrates a hybrid tick-volume model using Negative/Positive Volume Index (NVI-PVI) to identify smart money flows.

✅ Advanced RSI Logic: Uses Jurik RSX for accurate oversold/overbought filtering.

✅ Optional MTF Trend Filter: Validates trend direction using a slope-based Jurik MA on higher timeframes.

✅ MPT-Based DMI Filter: Adds pyramid entries only during strong trend phases, based on Gain/Pain ratios and Ulcer-index smoothed ADX.

✅ Risk Management: ATR-based SL/TP and fully customizable trailing logic for both profit and stop-loss.

📈 Entry Logic

Trades are triggered only when:

A minimum number of recent candles are bullish/bearish (Min Green/Red Candles)

Structure has not been broken by opposite price action (optional)

Relative volume exceeds average (optional)

RSI is below overbought or above oversold (optional)

MTF slope is aligned with trend direction (optional)

💡 Key Features

Custom Candle Logic: Detects momentum shifts using a tunable lookback window (up to 50 bars).

Smart Volume Filtering: Volume is intelligently estimated using tick-based ranges and NVI-PVI deltas.

Risk Management Built-in: Set your ATR length, SL/TP multipliers, and dynamic trailing offsets with full control.

Scorecard System: A built-in scoring engine evaluates Win Rate, Drawdown, Sharpe Ratio, Recovery Factor, and Profit Factor — visualized on chart as a label.

Backtest-Friendly: Includes date range toggles, bar-magnifier support, and optimized execution on every tick.

📊 Strategy Scorecard (Label)

Automatically calculates:

✅ Total Trades

✅ Win Rate (%)

✅ Net Profit

✅ Profit Factor

✅ Expected Payoff

✅ Max & Avg Drawdown

✅ Recovery Factor

✅ Sharpe Ratio

✅ VaR (95%)

Plus, assigns a normalized score from 0 to 100 for evaluating overall robustness.

⚙️ Customization

Every module — from entry filters to pyramiding and trailing logic — is fully configurable:

Volume Filters ✅

RSI Filters ✅

Structure Break Checks ✅

HTF Jurik MA & Slope Threshold ✅

Multi-Timeframe Mode ✅

Backtest Score Visualization ✅

⚠️ Notes

Enable bar magnifier and calc on every tick for best accuracy.

On early bars, signal logic may delay until enough candles are available.

Best paired with assets showing directional volatility (SPY, BTC, ETH, Gold, etc.).

Ideally paired on trending timeframes such as M1, M5, M15, M30, 1HR, 4 Hourly, Daily, Weekly, Monthly, etc.

ICT Bread and Butter Sell-SetupICT Bread and Butter Sell-Setup – TradingView Strategy

Overview:

The ICT Bread and Butter Sell-Setup is an intraday trading strategy designed to capitalize on bearish market conditions. It follows institutional order flow and exploits liquidity patterns within key trading sessions—London, New York, and Asia—to identify high-probability short entries.

Key Components of the Strategy:

🔹 London Open Setup (2:00 AM – 8:20 AM NY Time)

The London session typically sets the initial directional move of the day.

A short-term high often forms before a downward push, establishing the daily high.

🔹 New York Open Kill Zone (8:20 AM – 10:00 AM NY Time)

The New York Judas Swing (a temporary rally above London’s high) creates an opportunity for short entries.

Traders fade this move, anticipating a sell-off targeting liquidity below previous lows.

🔹 London Close Buy Setup (10:30 AM – 1:00 PM NY Time)

If price reaches a higher timeframe discount array, a retracement higher is expected.

A bullish order block or failure swing signals a possible reversal.

The risk is set just below the day’s low, targeting a 20-30% retracement of the daily range.

🔹 Asia Open Sell Setup (7:00 PM – 2:00 AM NY Time)

If institutional order flow remains bearish, a short entry is taken around the 0-GMT Open.

Expect a 15-20 pip decline as the Asian range forms.

Strategy Rules:

📉 Short Entry Conditions:

✅ New York Judas Swing occurs (price moves above London’s high before reversing).

✅ Short entry is triggered when price closes below the open.

✅ Stop-loss is set 10 pips above the session high.

✅ Take-profit targets liquidity zones on higher timeframes.

📈 Long Entry (London Close Reversal):

✅ Price reaches a higher timeframe discount array between 10:30 AM – 1:00 PM NY Time.

✅ A bullish order block confirms the reversal.

✅ Stop-loss is set 10 pips below the day’s low.

✅ Take-profit targets 20-30% of the daily range retracement.

📉 Asia Open Sell Entry:

✅ Price trades slightly above the 0-GMT Open.

✅ Short entry is taken at resistance, targeting a quick 15-20 pip move.

Why Use This Strategy?

🚀 Institutional Order Flow Tracking – Aligns with smart money concepts.

📊 Precise Session Timing – Uses market structure across London, New York, and Asia.

🎯 High-Probability Entries – Focuses on liquidity grabs and engineered stop hunts.

📉 Optimized Risk Management – Defined stop-loss and take-profit levels.

This strategy is ideal for traders looking to trade with institutions, fade liquidity grabs, and capture high-probability short setups during the trading day. 📉🔥

Universal Strategy | QuantEdgeBIntroducing the Universal Strategy by QuantEdgeB

The Universal Strategy | QuantEdgeB is a dynamic, multi-indicator strategy designed to operate across various asset classes with precision and adaptability. This cutting-edge system utilizes four sophisticated methodologies, each integrating advanced trend-following, volatility filtering, and normalization techniques to provide robust signals. Its modular architecture and customizable features ensure suitability for diverse market conditions, empowering traders with data-driven decision-making tools. Its adaptability to different price behaviors and volatility levels makes it a robust and versatile tool, equipping traders with data-driven confidence in their market decisions.

_______

1. Core Methodologies and Features

1️⃣ DEMA ATR

Strength : Fast responsiveness to trend shifts.

The double exponential moving average is inherently aggressive, designed to reduce lag and quickly identify early signs of trend reversals or breakout opportunities. ATR bands add a volatility-sensitive layer, dynamically adjusting the breakout thresholds to match current market conditions, ensuring it remains responsive while filtering out noise

How It Fits :

This indicator is the first responder, providing early signals of potential trend shifts. While its aggressiveness can result in quick entries, it may occasionally overreact in noisy markets. This is where the smoother indicators step in to confirm signals.

2️⃣ Gaussian - VIDYA ATR (Variable Index Dynamic Average)

Strength : Smooth, adaptive trend identification.

Unlike DEMA, VIDYA adapts to market volatility through its standard deviation-based formula, making it smoother and less reactive to short-term fluctuations. ATR filtering ensures the indicator remains effective in volatile markets by dynamically adjusting its sensitivity.

How It Fits :

The smoother complement to DEMA ATR, VIDYA ATR filters out false signals from minor price movements. It provides confirmation for the trends identified by DEMA ATR, ensuring entries are based on robust, sustained price movements.

3️⃣ VIDYA Loop Trend Scoring

Strength : Historical trend scoring for consistent momentum detection.

This module evaluates the relative strength of trends by comparing the current VIDYA value to its historical values over a defined range. The loop mechanism provides a trend confidence score, quantifying the momentum behind price movements.

How It Fits :

VIDYA For-Loop adds a quantitative measure of trend strength, ensuring that trades are backed by sustained momentum. It balances the early signals from DEMA ATR and the smoothness of VIDYA ATR by providing a statistical check on the underlying trend.

4️⃣ Median SD with Normalization

Strength : Precision in breakout detection and market normalization.

The Median price serves as a robust baseline for detecting breakouts and reversals.

SD bands expand dynamically during periods of high volatility, making the indicator particularly effective for spotting strong trends or breakout opportunities. Normalization ensures the indicator adapts seamlessly across different assets and timeframes, providing consistent performance.

How It Fits :

The Median SD module provides final confirmation by focusing on price breakouts and market normalization. While the other indicators focus on momentum and trend strength, Median SD emphasizes precision, ensuring entries align with significant price movements rather than random fluctuations.

_______

2. How The Single Components Work Together

1️⃣ Balance of Speed and Smoothness :

The strategy blends quick responsiveness (DEMA ATR) with smooth and adaptive confirmation (VIDYA ATR & For-Loop), ensuring timely reactions without overreacting to market fluctuations. Median SD with Normalization refines breakout detection and stabilizes performance across assets using statistical anchors like price median and standard deviation.

Adaptability to Market Dynamics:

2️⃣ Adaptability to Market Dynamics :

The indicators complement each other seamlessly in trending markets, with the DEMA ATR and Median SD with Normalization quickly identifying shifts and confirming sustained momentum. In volatile or choppy markets, normalization and SD bands work together to filter out noise and reduce false signals, ensuring precise entries and exits. Meanwhile, the For-Loop scoring and Gaussian-Filtered VIDYA ATR focus on providing smoother, more reliable trend detection, offering consistent performance regardless of market conditions.

_______

3. Scoring and Signal Confirmation

The Universal Strategy consolidates signals from all four methodologies, calculating a Trend Probability Index (TPI). The four core indicators operate independently but contribute to a unified TPI, enabling highly adaptive behavior across asset classes.

- Each methodology generates a trend score: 1 for bullish trends, -1 for bearish trends.

- The TPI averages the scores, creating a unified signal.

- Long Position: Triggered when the TPI exceeds the long threshold (default: 0).

- Short Position: Triggered when the TPI falls below the short threshold (default: 0).

The strategy’s customizable settings allow traders to tailor its behavior to different market conditions—whether smoother trends in low-volatility assets or quick reaction to high-volatility breakouts. The long and short thresholds can be fine-tuned to match a trader’s risk tolerance and preferences.

_______

4. Use Cases:

The Universal Strategy | QuantEdgeB is designed to excel across a wide range of trading scenarios, thanks to its modular architecture and adaptability. Whether you're navigating trending, volatile, or range-bound markets, this strategy offers robust tools to enhance your decision-making. Below are the key use cases for its application:

1️⃣ Trend Trading

The strategy’s Gaussian-Filtered DEMA ATR and VIDYA ATR modules are perfect for identifying and riding sustained trends.

Ideal For: Traders looking to capture long-term momentum or position trades.

2️⃣ Breakout and Volatility-Based Strategies

With its Median SD with Normalization, the strategy excels in detecting volatility breakouts and significant price movements.

Ideal For: Traders aiming to capitalize on sudden market movements, especially in assets like cryptocurrencies and commodities.

3️⃣ Momentum and Strength Assessment

By generating a trend confidence score, the VIDYA For-Loop quantifies momentum strength—helping traders distinguish temporary spikes from sustainable trends.

Ideal For: Swing traders and those focusing on momentum-driven setups.

4️⃣ Adaptability Across Multiple Assets

The strategy’s robust framework ensures it performs consistently across different assets and timeframes.

Ideal For: Traders managing diverse portfolios or shifting between asset classes.

5️⃣ Backtesting and Optimization

Built-in backtesting and equity visualization tools make this strategy ideal for testing and refining parameters in real-world conditions.

• How It Helps: The strategy equity curve and metrics table offer a clear picture of performance, helping traders identify optimal settings for their chosen market and timeframe.

• Ideal For: Traders focused on rigorous testing and long-term optimization.

_______

5. Signal Composition Table:

This table presents a real-time breakdown of each indicator’s trend score (+1 bullish, -1 bearish) alongside the final aggregated signal. By visualizing the contribution of each methodology, traders gain greater transparency, confidence, and clarity in identifying long or short opportunities.

6. Customized Settings:

1️⃣ General Inputs

• Strategy Long Threshold (Lu): 0

• Strategy Short Threshold (Su): 0

2️⃣ Gaussian Filter

• Gaussian Length (len_FG): 4

• Gaussian Source (src_FG): close

• Gaussian Sigma (sigma_FG): 2.0

3️⃣ DEMA ATR

• DEMA Length (len_D): 30

• DEMA Source (src_D): close

• ATR Length (atr_D): 14

• ATR Multiplier (mult_D): 1.0

4️⃣ VIDYA ATR

• VIDYA Length (len_V1): 9

• SD Length (len_VHist1): 30

• ATR Length (atr_V): 14

• ATR Multiplier (mult_V): 1.7

5️⃣ VIDYA For-Loop

• VIDYA Length (len_V2): 2

• SD Length (len_VHist2): 5

• VIDYA Source (src_V2): close

• Start Loop (strat_loop): 1

• End Loop (end_loop): 60

• Long Threshold (long_t): 40

• Short Threshold (short_t): 8

6️⃣ Median SD

• Median Length (len_m): 24

• Normalized Median Length (len_msd): 50

• SD Length (SD_len): 32

• Long SD Weight (w1): 0.98

• Short SD Weight (w2): 1.02

• Long Normalized Smooth (smooth_long): 1

• Short Normalized Smooth (smooth_short): 1

Conclusion

The Universal Strategy | QuantEdgeB is a meticulously crafted, multi-dimensional trading system designed to thrive across diverse market conditions and asset classes. By combining Gaussian-Filtered DEMA ATR, VIDYA ATR, VIDYA For-Loop, and Median SD with Normalization, this strategy provides a seamless balance between speed, smoothness, and adaptability. Each component complements the others, ensuring traders benefit from early responsiveness, trend confirmation, momentum scoring, and breakout precision.

Its modular structure ensures versatility across trending, volatile, and consolidating markets. Whether applied to equities, forex, commodities, or crypto, it delivers data-driven precision while minimizing reliance on randomness, reinforcing confidence in decision-making.

With built-in backtesting tools, traders can rigorously evaluate performance under real-world conditions, while customization options allow fine-tuning for specific market dynamics and individual trading styles.

Why It Stands Out

The Universal Strategy | QuantEdgeB isn’t just a trading algorithm—it’s a comprehensive framework that empowers traders to make confident, informed decisions in the face of ever-changing market conditions. Its emphasis on precision, reliability, and transparency makes it a powerful tool for both professional and retail traders seeking consistent performance and enhanced risk management.

_______

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Kernel Regression Envelope with SMI OscillatorThis script combines the predictive capabilities of the **Nadaraya-Watson estimator**, implemented by the esteemed jdehorty (credit to him for his excellent work on the `KernelFunctions` library and the original Nadaraya-Watson Envelope indicator), with the confirmation strength of the **Stochastic Momentum Index (SMI)** to create a dynamic trend reversal strategy. The core idea is to identify potential overbought and oversold conditions using the Nadaraya-Watson Envelope and then confirm these signals with the SMI before entering a trade.

**Understanding the Nadaraya-Watson Envelope:**

The Nadaraya-Watson estimator is a non-parametric regression technique that essentially calculates a weighted average of past price data to estimate the current underlying trend. Unlike simple moving averages that give equal weight to all past data within a defined period, the Nadaraya-Watson estimator uses a **kernel function** (in this case, the Rational Quadratic Kernel) to assign weights. The key parameters influencing this estimation are:

* **Lookback Window (h):** This determines how many historical bars are considered for the estimation. A larger window results in a smoother estimation, while a smaller window makes it more reactive to recent price changes.

* **Relative Weighting (alpha):** This parameter controls the influence of different time frames in the estimation. Lower values emphasize longer-term price action, while higher values make the estimator more sensitive to shorter-term movements.

* **Start Regression at Bar (x\_0):** This allows you to exclude the potentially volatile initial bars of a chart from the calculation, leading to a more stable estimation.

The script calculates the Nadaraya-Watson estimation for the closing price (`yhat_close`), as well as the highs (`yhat_high`) and lows (`yhat_low`). The `yhat_close` is then used as the central trend line.

**Dynamic Envelope Bands with ATR:**

To identify potential entry and exit points around the Nadaraya-Watson estimation, the script uses **Average True Range (ATR)** to create dynamic envelope bands. ATR measures the volatility of the price. By multiplying the ATR by different factors (`nearFactor` and `farFactor`), we create multiple bands:

* **Near Bands:** These are closer to the Nadaraya-Watson estimation and are intended to identify potential immediate overbought or oversold zones.

* **Far Bands:** These are further away and can act as potential take-profit or stop-loss levels, representing more extreme price extensions.

The script calculates both near and far upper and lower bands, as well as an average between the near and far bands. This provides a nuanced view of potential support and resistance levels around the estimated trend.

**Confirming Reversals with the Stochastic Momentum Index (SMI):**

While the Nadaraya-Watson Envelope identifies potential overextended conditions, the **Stochastic Momentum Index (SMI)** is used to confirm a potential trend reversal. The SMI, unlike a traditional stochastic oscillator, oscillates around a zero line. It measures the location of the current closing price relative to the median of the high/low range over a specified period.

The script calculates the SMI on a **higher timeframe** (defined by the "Timeframe" input) to gain a broader perspective on the market momentum. This helps to filter out potential whipsaws and false signals that might occur on the current chart's timeframe. The SMI calculation involves:

* **%K Length:** The lookback period for calculating the highest high and lowest low.

* **%D Length:** The period for smoothing the relative range.

* **EMA Length:** The period for smoothing the SMI itself.

The script uses a double EMA for smoothing within the SMI calculation for added smoothness.

**How the Indicators Work Together in the Strategy:**

The strategy enters a long position when:

1. The closing price crosses below the **near lower band** of the Nadaraya-Watson Envelope, suggesting a potential oversold condition.

2. The SMI crosses above its EMA, indicating positive momentum.

3. The SMI value is below -50, further supporting the oversold idea on the higher timeframe.

Conversely, the strategy enters a short position when:

1. The closing price crosses above the **near upper band** of the Nadaraya-Watson Envelope, suggesting a potential overbought condition.

2. The SMI crosses below its EMA, indicating negative momentum.

3. The SMI value is above 50, further supporting the overbought idea on the higher timeframe.

Trades are closed when the price crosses the **far band** in the opposite direction of the trade. A stop-loss is also implemented based on a fixed value.

**In essence:** The Nadaraya-Watson Envelope identifies areas where the price might be deviating significantly from its estimated trend. The SMI, calculated on a higher timeframe, then acts as a confirmation signal, suggesting that the momentum is shifting in the direction of a potential reversal. The ATR-based bands provide dynamic entry and exit points based on the current volatility.

**How to Use the Script:**

1. **Apply the script to your chart.**

2. **Adjust the "Kernel Settings":**

* **Lookback Window (h):** Experiment with different values to find the smoothness that best suits the asset and timeframe you are trading. Lower values make the envelope more reactive, while higher values make it smoother.

* **Relative Weighting (alpha):** Adjust to control the influence of different timeframes on the Nadaraya-Watson estimation.

* **Start Regression at Bar (x\_0):** Increase this value if you want to exclude the initial, potentially volatile, bars from the calculation.

* **Stoploss:** Set your desired stop-loss value.

3. **Adjust the "SMI" settings:**

* **%K Length, %D Length, EMA Length:** These parameters control the sensitivity and smoothness of the SMI. Experiment to find settings that work well for your trading style.

* **Timeframe:** Select the higher timeframe you want to use for SMI confirmation.

4. **Adjust the "ATR Length" and "Near/Far ATR Factor":** These settings control the width and sensitivity of the envelope bands. Smaller ATR lengths make the bands more reactive to recent volatility.

5. **Customize the "Color Settings"** to your preference.

6. **Observe the plots:**

* The **Nadaraya-Watson Estimation (yhat)** line represents the estimated underlying trend.

* The **near and far upper and lower bands** visualize potential overbought and oversold zones based on the ATR.

* The **fill areas** highlight the regions between the near and far bands.

7. **Look for entry signals:** A long entry is considered when the price touches or crosses below the lower near band and the SMI confirms upward momentum. A short entry is considered when the price touches or crosses above the upper near band and the SMI confirms downward momentum.

8. **Manage your trades:** The script provides exit signals when the price crosses the far band. The fixed stop-loss will also close trades if the price moves against your position.

**Justification for Combining Nadaraya-Watson Envelope and SMI:**

The combination of the Nadaraya-Watson Envelope and the SMI provides a more robust approach to identifying potential trend reversals compared to using either indicator in isolation. The Nadaraya-Watson Envelope excels at identifying potential areas where the price is overextended relative to its recent history. However, relying solely on the envelope can lead to false signals, especially in choppy or volatile markets. By incorporating the SMI as a confirmation tool, we add a momentum filter that helps to validate the potential reversals signaled by the envelope. The higher timeframe SMI further helps to filter out noise and focus on more significant shifts in momentum. The ATR-based bands add a dynamic element to the entry and exit points, adapting to the current market volatility. This mashup aims to leverage the strengths of each indicator to create a more reliable trading strategy.

ETH Signal 15m

This strategy uses the Supertrend indicator combined with RSI to generate buy and sell signals, with stop loss (SL) and take profit (TP) conditions based on ATR (Average True Range). Below is a detailed explanation of each part:

1. General Information BINANCE:ETHUSDT.P

Strategy Name: "ETH Signal 15m"

Designed for use on the 15-minute time frame for the ETH pair.

Default capital allocation is 15% of total equity for each trade.

2. Backtest Period

start_time and end_time: Define the start and end time of the backtest period.

start_time = 2024-08-01: Start date of the backtest.

end_time = 2054-01-01: End date of the backtest.

The strategy will only run when the current time falls within this specified range.

3. Supertrend Indicator

Supertrend is a trend-following indicator that provides buy or sell signals based on the direction of price changes.

factor = 2.76: The multiplier used in the Supertrend calculation (increasing this value makes the Supertrend less sensitive to price movements).

atrPeriod = 12: Number of periods used to calculate ATR.

Output:

direction: Determines the buy/sell direction based on Supertrend.

If direction decreases, it signals a buy (Long).

If direction increases, it signals a sell (Short).

4. RSI Indicator

RSI (Relative Strength Index) is a momentum indicator, often used to identify overbought or oversold conditions.

rsiLength = 12: Number of periods used to calculate RSI.

rsiOverbought = 70: RSI level considered overbought.

rsiOversold = 30: RSI level considered oversold.

5. Entry Conditions

Long Entry:

Supertrend gives a buy signal (ta.change(direction) < 0).

RSI must be below the overbought level (rsi < rsiOverbought).

Short Entry:

Supertrend gives a sell signal (ta.change(direction) > 0).

RSI must be above the oversold level (rsi > rsiOversold).

The strategy will only execute trades if the current time is within the backtest period (in_date_range).

6. Stop Loss (SL) and Take Profit (TP) Conditions

ATR (Average True Range) is used to calculate the distance for Stop Loss and Take Profit based on price volatility.

atr = ta.atr(atrPeriod): ATR is calculated using 12 periods.

Stop Loss and Take Profit are calculated as follows:

Long Trade:

Stop Loss: Set at close - 4 * atr (current price minus 4 times the ATR).

Take Profit: Set at close + 2 * atr (current price plus 2 times the ATR).

Short Trade:

Stop Loss: Set at close + 4 * atr (current price plus 4 times the ATR).

Take Profit: Set at close - 2.237 * atr (current price minus 2.237 times the ATR).

Summary:

This strategy enters a Long trade when the Supertrend indicates an upward trend and RSI is not in the overbought region. Conversely, a Short trade is entered when Supertrend signals a downtrend, and RSI is not oversold.

The trade is exited when the price reaches the Stop Loss or Take Profit levels, which are determined based on price volatility (ATR).

Disclaimer:

The content provided in this strategy is for informational and educational purposes only. It is not intended as financial, investment, or trading advice. Trading in cryptocurrency, stocks, or any financial markets involves significant risk, and you may lose more than your initial investment. Past performance is not indicative of future results, and no guarantee of profit can be made. You should consult with a professional financial advisor before making any investment decisions. The creator of this strategy is not responsible for any financial losses or damages incurred as a result of following this strategy. All trades are executed at your own risk.

Bollinger Bands Enhanced StrategyOverview

The common practice of using Bollinger bands is to use it for building mean reversion or squeeze momentum strategies. In the current script Bollinger Bands Enhanced Strategy we are trying to combine the strengths of both strategies types. It utilizes Bollinger Bands indicator to buy the local dip and activates trailing profit system after reaching the user given number of Average True Ranges (ATR). Also it uses 200 period EMA to filter trades only in the direction of a trend. Strategy can execute only long trades.

Unique Features

Trailing Profit System: Strategy uses user given number of ATR to activate trailing take profit. If price has already reached the trailing profit activation level, scrip will close long trade if price closes below Bollinger Bands middle line.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Major Trend Filter: Strategy utilizes 100 period EMA to take trades only in the direction of a trend.

Flexible Risk Management: Users can choose number of ATR as a stop loss (by default = 1.75) for trades. This is flexible approach because ATR is recalculated on every candle, therefore stop-loss readjusted to the current volatility.

Methodology

First of all, script checks if currently price is above the 200-period exponential moving average EMA. EMA is used to establish the current trend. Script will take long trades on if this filtering system showing us the uptrend. Then the strategy executes the long trade if candle’s low below the lower Bollinger band. To calculate the middle Bollinger line, we use the standard 20-period simple moving average (SMA), lower band is calculated by the substruction from middle line the standard deviation multiplied by user given value (by default = 2).

When long trade executed, script places stop-loss at the price level below the entry price by user defined number of ATR (by default = 1.75). This stop-loss level recalculates at every candle while trade is open according to the current candle ATR value. Also strategy set the trailing profit activation level at the price above the position average price by user given number of ATR (by default = 2.25). It is also recalculated every candle according to ATR value. When price hit this level script plotted the triangle with the label “Strong Uptrend” and start trail the price at the middle Bollinger line. It also started to be plotted as a green line.

When price close below this trailing level script closes the long trade and search for the next trade opportunity.

Risk Management

The strategy employs a combined and flexible approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined ATR stop loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 1.75*ATR drop from the entry point, but it can be adjusted according to the trader's preferences.

There is no fixed take profit, but strategy allows user to define user the ATR trailing profit activation parameter. By default, this stop-loss is set to a 2.25*ATR growth from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Bollinger bangs indicator to open long trades in the local dips. If price reached the lower band there is a high probability of bounce. Here is an issue: during the strong downtrend price can constantly goes down without any significant correction. That’s why we decided to use 200-period EMA as a trend filter to increase the probability of opening long trades during major uptrend only.

Usually, Bollinger Bands indicator is using for mean reversion or breakout strategies. Both of them have the disadvantages. The mean reversion buys the dip, but closes on the return to some mean value. Therefore, it usually misses the major trend moves. The breakout strategies usually have the issue with too high buy price because to have the breakout confirmation price shall break some price level. Therefore, in such strategies traders need to set the large stop-loss, which decreases potential reward to risk ratio.

In this strategy we are trying to combine the best features of both types of strategies. Script utilizes ate ATR to setup the stop-loss and trailing profit activation levels. ATR takes into account the current volatility. Therefore, when we setup stop-loss with the user-given number of ATR we increase the probability to decrease the number of false stop outs. The trailing profit concept is trying to add the beat feature from breakout strategies and increase probability to stay in trade while uptrend is developing. When price hit the trailing profit activation level, script started to trail the price with middle line if Bollinger bands indicator. Only when candle closes below the middle line script closes the long trade.

Backtest Results

Operating window: Date range of backtests is 2020.10.01 - 2024.07.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -9.78%

Maximum Single Profit: +25.62%

Net Profit: +6778.11 USDT (+67.78%)

Total Trades: 111 (48.65% win rate)

Profit Factor: 2.065

Maximum Accumulated Loss: 853.56 USDT (-6.60%)

Average Profit per Trade: 61.06 USDT (+1.62%)

Average Trade Duration: 76 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Advanced Trend Strategy [BITsPIP]The BITsPIP team is super excited to share our latest trading gem with you all. We're all about diving deep and ensuring our strategies can stand the test of time. So, we invite you to join us in exploring the awesome potential of this new strategy and really put it through its pace with some deep backtesting. This isn't just another strategy; it boasts a profit factor hovering around 1.5 across over 1000 trades, which is quite an achievement. Consider integrating it with your trading bots to further enhance your trading efficiency and profit generation. Curious? Ask for trial access or drop by our website for more details.

I. Deep Backtesting

We're all in on transparency and solid results, which is why we didn't stop at 100... or even 500 trades. We went over 1000, making sure this strategy is as robust as they come. No flimsy forecasts or sneaky repainting here. Just good, solid strategy that's ready for the real deal. Curious about the details? Check out our detailed backtesting screenshot for the BINANCE:BTCUSDT in a 5-minute timeframe. It's all about giving you the clear picture.

#No Overfitting

#No Repainting

Backtesting Screenshot

II. Algorithmic Trading

Thinking of trading as a manual game? Think again! Manual trading is a bit like rolling the dice - fun, but kind of risky if you're aiming for consistent wins. Instead, why not lean into the future with algorithmic trading? It's all about trusting the market's rhythm over the long term. By integrating your strategy with a trading bot, you can enjoy peace of mind, rest easy, and keep those emotional trades at bay.

III) Applications

Dive into the Advanced Trend Strategy, your versatile tool for navigating the market's waters. This strategy shines in under an hour timeframes, offering adaptability across stocks, commodities, forex, and cryptocurrencies. Initially fine-tuned for low-volatility cryptos like BINANCE:BTCUSDT , its default settings are a solid starting point.

But here's where your expertise comes into play. Each market beats to its own drum, necessitating nuanced adjustments to stop loss and take profit settings. This customization is key to maximizing the strategy's effectiveness in your chosen arena.

IV) Strategy's Logic

The Advanced Trend Strategy is a powerhouse, blending the precision of Hull Suite, RSI, and our unique trend detector technique. At its core, it’s designed for savvy risk management, aiming to lock in substantial profits while steering clear of minor market ripples. It utilizes stop-loss and take-profit thresholds to form a profit channel, providing a safety net for each trade. This is a trend-following strategy at heart, where these profit channels play a critical role in maximizing returns by securing positions within these "warranty channels."

1. Trend-Following

The market's complexity, influenced by countless factors, makes small movements seem almost chaotic. Yet, the principle of #Trend-Following shines in less volatile markets in long term. The strategy excels by pinpointing the ideal moments to enter the market, coupled with refined risk management to secure profits. It’s tailored for you, the individual trader, enabling you to ride the waves of market trends upwards or downwards.

2. Risk Management

A key facet of the strategy is its emphasis on pragmatic risk management. Traders are empowered to establish practical stop-loss and take-profit levels, tailoring these crucial parameters to the specific market they are engaging in. This customization is instrumental in optimizing long-term profitability, ensuring that the strategy adapts fluidly to the unique characteristics and volatility patterns of different trading environments.

V) Strategy's Input Settings and Default Values

1. Alerts

The strategy comes equipped with a flexible alert system designed to keep you informed and ready to act. Within the settings, you’ll find options to configure order/exit and comment/alert messages to your preference. This feature is particularly useful for staying on top of the strategy’s activities without constant manual oversight.

2. Hull Suite

i. Hull Suite Length: Designed for capturing long-term trends, the Hull Suite Length is configured at 1000. Functioning comparably to moving averages, the Hull Suite features upper and lower bands. Currently, it is set to 1000.

ii. Length Multiplier: It's advisable to maintain a minimal value for the Length Multiplier, prioritizing the optimization of the Hull Suite Length. Presently, it is set to 1.

3. RSI Indicator

i. The RSI is a widely recognized tool in trading. Adapt the oversold and overbought thresholds to better match the specifics of your market for optimal results.

4. StopLoss and TakeProfit

i. StopLoss and TakeProfit Settings: Two distinct approaches are available. Semi-Automatic StopLoss/TakeProfit Setting and Manual StopLoss/TakeProfit Setting. The Semi-Automatic mode streamlines the process by allowing you to input values for a 5-minute timeframe, subsequently auto-adjusting these values across various timeframes, both lower and higher. Conversely, the Manual mode offers full control, enabling you to meticulously define TakeProfit values for each individual timeframe.

ii. TakeProfit Threshold # and TakeProfit Value #: Imagine this mechanism as an ascending staircase. Each step represents a range, with the lower boundary (TakeProfit Value) designed to close the trade upon being reached, and the upper boundary (TakeProfit Threshold) upon being hit, propelling the trade to the next level, and forming a new range. This stair-stepping approach enhances risk management and increases profitability. The pre-set configurations are tailored for $BINANCE:BTCUSDT. It's advisable to devote time to tailoring these settings to your specific market, aiming to achieve optimal results based on backtesting.

iii. StopLoss Value: In line with its name, this value marks the limit of loss you're prepared to accept should the market trend go against your expectations. It's crucial to note that once your asset reaches the first TakeProfit range, the initial StopLoss value becomes obsolete, supplanted by the first TakeProfit Value. The default StopLoss value is pegged at 1.6(%), a figure worth considering in your trading strategy.

VI) Entry Conditions

The primary signal for entry is generated by our custom trend detection mechanism and hull suite values (ascending/descending). This is supported by additional indicators acting as confirmation.

VII) Exit Conditions

The strategy stipulates exit conditions primarily governed by stop loss and take profit parameters. On infrequent occasions, if the trend lacks confirmation post-entry, the strategy mandates an exit upon the issuance of a reverse signal (whether confirmed or unconfirmed) by the strategy itself.

BITsPIP

Octopus Nest Strategy Hello Fellas,

Hereby, I come up with a popular strategy from YouTube called Octopus Nest Strategy. It is a no repaint, lower timeframe scalping strategy utilizing PSAR, EMA and TTM Squeeze.

The strategy considers these market factors:

PSAR -> Trend

EMA -> Trend

TTM Squeeze -> Momentum and Volatility by incorporating Bollinger Bands and Keltner Channels

Note: As you can see there is a potential improvement by incorporating volume.

What's Different Compared To The Original Strategy?

I added an option which allows users to use the Adaptive PSAR of @loxx, which will hopefully improve results sometimes.

Signals

Enter Long -> source above EMA 100, source crosses above PSAR and TTM Squeeze crosses above 0

Enter Short -> source below EMA 100, source crosses below PSAR and TTM Squeeze crosses below 0

Exit Long and Exit Short are triggered from the risk management. Thus, it will just exit on SL or TP.

Risk Management

"High Low Stop Loss" and "Automatic High Low Take Profit" are used here.

High Low Stop Loss: Utilizes the last high for short and the last low for long to calculate the stop loss level. The last high or low gets multiplied by the user-defined multiplicator and if no recent high or low was found it uses the backup multiplier.

Automatic High Low Take Profit: Utilizes the current stop loss level of "High Low Stop Loss" and gets calculated by the user-defined risk ratio.

Now, follows the bunch of knowledge for the more inexperienced readers.

PSAR: Parabolic Stop And Reverse; Developed by J. Welles Wilders and a classic trend reversal indicator.

The indicator works most effectively in trending markets where large price moves allow traders to capture significant gains. When a security’s price is range-bound, the indicator will constantly be reversing, resulting in multiple low-profit or losing trades.

TTM Squeeze: TTM Squeeze is a volatility and momentum indicator introduced by John Carter of Trade the Markets (now Simpler Trading), which capitalizes on the tendency for price to break out strongly after consolidating in a tight trading range.

The volatility component of the TTM Squeeze indicator measures price compression using Bollinger Bands and Keltner Channels. If the Bollinger Bands are completely enclosed within the Keltner Channels, that indicates a period of very low volatility. This state is known as the squeeze. When the Bollinger Bands expand and move back outside of the Keltner Channel, the squeeze is said to have “fired”: volatility increases and prices are likely to break out of that tight trading range in one direction or the other. The on/off state of the squeeze is shown with small dots on the zero line of the indicator: red dots indicate the squeeze is on, and green dots indicate the squeeze is off.

EMA: Exponential Moving Average; Like a simple moving average, but with exponential weighting of the input data.

Don't forget to check out the settings and keep it up.

Best regards,

simwai

---

Credits to:

@loxx

@Bjorgum

@Greeny

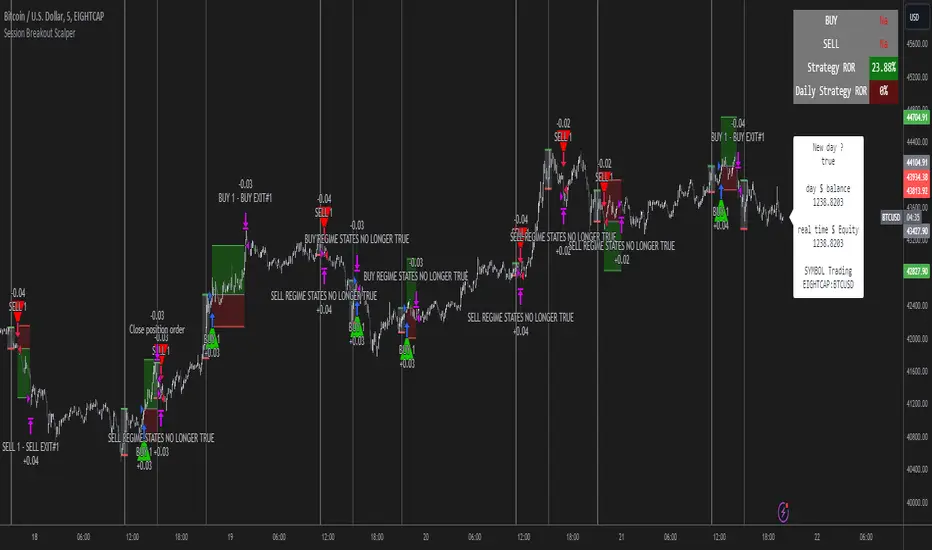

Session Breakout Scalper Trading BotHi Traders !

Introduction:

I have recently been exploring the world of automated algorithmic trading (as I prefer more objective trading strategies over subjective technical analysis (TA)) and would like to share one of my automation compatible (PineConnecter compatible) scripts “Session Breakout Scalper”.

The strategy is really simple and is based on time conditional breakouts although has more ”relatively” advanced optional features such as the regime indicators (Regime Filters) that attempt to filter out noise by adding more confluence states and the ATR multiple SL that takes into account volatility to mitigate the down side risk of the trade.

What is Algorthmic Trading:

Firstly what is algorithmic trading? Algorithmic trading also known as algo-trading, is a method of using computer programs (in this case pine script) to execute trades based on predetermined rules and instructions (this trading strategy). It's like having a robot trader who follows a strict set of commands to buy and sell assets automatically, without any human intervention.

Important Note:

For Algorithmic trading the strategy will require you having an essential TV subscription at the minimum (so that you can set alerts) plus a PineConnecter subscription (scroll down to the .”How does the strategy send signals” headings to read more)

The Strategy Explained:

Is the Time input true ? (this can be changed by toggling times under the “TRADE MEDIAN TIMES” group for user inputs).

Given the above is true the strategy waits x bars after the session and then calculates the highest high (HH) to lowest low (LL) range. For this box to form, the user defined amount of bars must print after the session. The box is symmetrical meaning the HH and LL are calculated over a lookback that is equal to the sum of user defined bars before and after the session (+ 1).

The Strategy then simultaneously defines the HH as the buy level (green line) and the LL as the sell level (red line). note the strategy will set stop orders at these levels respectively.

Enter a buy if price action crosses above the HH, and then cancel the sell order type (The opposite is true for a stop order).

If the momentum based regime filters are true the strategy will check for the regime / regimes to be true, if the regime if false the strategy will exit the current trade, as the regime filter has predicted a slowing / reversal of momentum.

The image below shows the strategy executing these trading rules ( Regime filters, "Trades on chart", "Signal & Label" and "Quantity" have been omitted. "Strategy label plots" has been switched to true)

Other Strategy Rules:

If a new session (time session which is user defined) is true (blue vertical line) and the strategy is currently still in a trade it will exit that trade immediately.

It is possible to also set a range of percentage gain per day that the strategy will try to acquire, if at any point the strategy’s profit is within the percentage range then the position / trade will be exited immediately (This can be changed in the “PERCENT DAY GAIN” group for user inputs)

Stops and Targets:

The strategy has either static (fixed) or variable SL options. TP however is only static. The “STRAT TP & TP” group of user inputs is responsible for the SL and TP values (quoted in pips). Note once the ATR stop is set to true the SL values in the above group no longer have any affect on the SL as expected.

What are the Regime Filters:

The Larry Williams Large Trade Index (LWLTI): The Larry Williams Large Trade Index (LWTI) is a momentum-based technical indicator developed by iconic trader Larry Williams. It identifies potential entries and exits for trades by gauging market sentiment, particularly the buying and selling pressure from large market players. Here's a breakdown of the LWTI:

LWLTI components and their interpretation:

Oscillator: It oscillates between 0 and 100, with 50 acting as the neutral line.

Sentiment Meter: Values above 75 suggest a bearish market dominated by large selling, while readings below 25 indicate a bullish market with strong buying from large players.

Trend Confirmation: Crossing above 75 during an uptrend and below 25 during a downtrend confirms the trend's continuation.

The Andean Oscillator (AO) : The Andean Oscillator is a trend and momentum based indicator designed to measure the degree of variations within individual uptrends and downtrends in the prices.

Regime Filter States:

In trading, a regime filter is a tool used to identify the current state or "regime" of the market.

These Regime filters are integrated within the trading strategy to attempt to lower risk (equity volatility and/or draw down). The regime filters have different states for each market order type (buy and sell). When the regime filters are set to true, if these regime states fail to be true the trade is exited immediately.

For Buy Trades:

LWLTI positive momentum state: Quotient of the lagged trailing difference and the ATR > 50

AO positive momentum state: Bull line > Bear line (signal line is omitted)

For Sell Trades:

LWLTI negative momentum stat: Quotient of the lagged trailing difference and the ATR < 50

AO negative momentum state: Bull line < Bear line (signal line is omitted)

How does the Strategy Send Signals:

The strategy triggers a TV alert (you will neet to set a alert first), TV then sends a HTTP request to the automation software (PineConnecter) which receives the request and then communicates to an MT4/5 EA to automate the trading strategy.

For the strategy to send signals you must have the following

At least a TV essential subscription

This Script added to your chart

A PineConnecter account, which is paid and not free. This will provide you with the expert advisor that executes trades based on these strategies signals.

For more detailed information on the automation process I would recommend you read the PineConnecter documentation and FAQ page.

Dashboard:

This Dashboard (top right by defualt) lists some simple trading statistics and also shows when a trade is live.

Important Notice:

- USE THIS STRATEGY AT YOUR OWN RISK AND ALWAYS DO YOUR OWN RESEARCH & MANUAL BACKTESTING !

- THE STRATEGY WILL NOT EXHIBIT THE BACKTEST PERFORMANCE SEEN BELOW IN ALL MARKETS !

London BreakOut ClassicHey there, this is my first time publishing a strategy. The strategy is based on the London Breakout Idea, an incredibly popular concept with abundant information available online.

Let me summarize the London Breakout Strategy in a nutshell: It involves identifying key price levels based on the Tokyo Session before the London Session starts. Typically, these key levels are the high and low of the previous Tokyo session. If a breakout occurs during the London session, you simply follow the trend.

The purpose of this code

After conducting my research, I came across numerous posts, videos, and articles discussing the London Breakout Strategy. I aimed to automatically test it myself to verify whether the claims made by these so-called trading gurus are accurate or not. Consequently, I wrote this script to gain an understanding of how this strategy would perform if I were to follow its basic settings blindly.

Explanation of drawings on the chart:

Red or Green Box: A box is drawn on our chart displaying the exact range of the Tokyo trading session. This box is colored red if the trend during the session was downward and green if it was upward. The box is always drawn between the high and the low between 0:00 AM and 7:00 AM UTC. You can change the settings via the Inputs "Session time Tokyo" & "Session time zone".

Green Background: The green background represents the London trading session. My code allows us to make entries only during this time. If we haven't entered a trade, any pending orders are canceled. I've also programmed a timeout at 11 pm to ensure every trade is closed before the new Tokyo session begins.

Red Line: The red line is automatically placed in the middle of our previous Tokyo range. This line acts as our stop loss. If we cross this line after entering a trade but before reaching our take profit, we'll be stopped out.

When do we enter a trade?

We wait for a candle body to close outside of the previous Tokyo range to enter a trade with the opening of the next candle. We only enter one trade per day.

Where do we put our Take Profit?

The code calculates the exact distance between our entry point and the stop loss. We are trading a risk-reward ratio of 1:1 by default, meaning our take profit is always the same number of pips away from our entry as the stop loss. The Stop Loss is always defined by the red line on the chart. You can change the risk-reward ratio via the inputs setting "CRV", to see how the result changes.

What is the purpose of this script?

I wanted to backtest the London breakout strategy to see how it actually works. Therefore, I wrote this code so that everybody can test it for themselves. You can change the settings and see how the result changes. Typically, you should test this strategy on forex markets and on either 1Min, 5 Min, or 15 Min timeframe.

What are the results?

Over the last 3-6 months (over 100 trades), trading the strategy with my default settings hasn't proven to be very successful. Consequently, I do not recommend trading this strategy blindly. The purpose of this code is to provide you with a foundation for the London Breakout Strategy, allowing you to modify and enhance it according to your preferences. If you're contemplating whether to give it a try, you can assess the results from the past months by using this code as a starting point.

Captain Backtest Model [TFO]Created by @imjesstwoone and @mickey1984, this trade model attempts to capture the expansion from the 10:00-14:00 EST 4h candle using just 3 simple steps. All of the information presented in this description has been outlined by its creators, all I did was translate it to Pine Script. All core settings of the trade model may be edited so that users can test several variations, however this description will cover its default, intended behavior using NQ 5m as an example.

Step 1 is to identify our Price Range. In this case, we are concerned with the highest high and the lowest low created from 6:00-10:00 EST.

Step 2 is to wait for either the high or low of said range to be taken out. Whichever side gets taken first determines the long/short bias for the remainder of the Trade Window (i.e. if price takes the range high, bias is long, and vice versa). Bias must be determined by 11:15 EST, otherwise no trades will be taken. This filter is intended to weed out "choppy" trading days.

Step 3 is to wait for a retracement and enter with a close through the previous candle's high (if long biased) or low (if short biased). There are a couple toggleable criteria that we use to define a retracement; one is checking for opposite close candles that indicate a pullback; another is checking if price took the previous candle's low (if long biased) or high (if short biased).

This trade model was initially tested for index futures, particularly ES and NQ, using a 5m chart, however this indicator allows us to backtest any symbol on any timeframe. Creators @imjesstwoone and @mickey1984 specified a 5 point stop loss on ES and a 25 point stop loss on NQ with their testing.

I've personally found some success in backtesting NQ 5m using a 25 point stop loss and 75 point profit target (3:1 R). Enabling the Use Fixed R:R parameter will ensure that these stops and targets are utilized, otherwise it will enter and hold the position until the close of the Trade Window.

Volatility Compression Breakout - LeafAlgo Pro StrategyThe Volatility Compression Breakout strategy is designed to identify periods of low volatility followed by potential breakout opportunities in the market. It aims to capture moments when the price consolidates within a narrow range, indicating a decrease in volatility, and anticipates a subsequent expansion in price movement. This strategy is based on our indicator of the same name (), but differs by offering many more options for the band/channel type and trend filters in addition to implementing the ability to use this strategy with algorithmic plug-ins (see details at the bottom).

This strategy features six types of bands/channels and five types of trend filters, for a total of 30 combinations. The six band/channel types are the Adaptive Gaussian MA channel (based on the Adaptive Gaussian MA that we previously published ()), standard Bollinger Bands, smoothed Bollinger Bands (basis is an EMA of the typical Bollinger Basis), Keltner Channels, a Quadratic Regression Channel (based on the channel that we previously published in the LeafAlgo Pro indicator ()), and Volatility-Based Mean Reversion Bands (). The five trend filters include an EMA, SMA, Weighted MA, McGinley Dynamic, and the Adaptive Gaussian MA itself.

Examples of the different band/channel types (all with EMA as the trend filter):

Adaptive Gaussian MA Channel:

Bollinger Bands:

Smoothed Bollinger Bands:

Keltner Channels:

Quadratic Regression Channel:

Volatility-Based Mean Reversion Bands:

Examples of the different trend filters (all with Keltner Channels):

EMA:

SMA:

WMA:

McGinley Dynamic:

Adaptive Gaussian MA:

How the Long/Short Entry Signals are Calculated:

A breakout signal upwards, accompanied by a long entry, is created when the high is greater than the secondary upper band (the upper band plus a standard deviation or with a multiplier, depending on which band/channel type is selected), the latest close is above the trend filter line, and the previous close was below the trend filter line. A break downwards, accompanied by a short entry, is created when the low is below the secondary lower band, the close is below the trend filter line, and the previous close was above the trend filter line. These conditions, along with a confirmed barstate, make up the strategy entry signals.

Coloration:

When the close price is above both the middle/basis and the trend filter, the bars are colored lime green, indicating a potential bullish market sentiment. When the close price is positioned above the basis but below the trend filter, or below the basis but above the trend filter, the bars are colored yellow, signifying a neutral or indecisive market condition. Conversely, when the close price falls below both the basis and the trend filter, the bars are colored fuchsia, suggesting a potential bearish market sentiment. Additionally, the coloration of the middle/basis line and the trend filter provides further visual cues for assessing the trend. When the close price is above the basis, the line is colored lime green, indicating a bullish trend. Conversely, when the close price is below the basis, the line is colored fuchsia, highlighting a bearish trend. Similarly, the trend line is colored lime green when the close price is above it, representing a bullish trend, and fuchsia when the close price is below it, indicating a bearish trend. The fill between the primary and secondary upper bands is colored lime and the fill between the primary and secondary lower bands is colored fuchsia. These colorations can be toggled on/off in the strategy settings menu.

How Changing Parameters Can Be Beneficial:

Modifying the parameters allows you to adapt the indicator to different market conditions and trading styles. For example, with Keltner Channels, increasing the compression period can help identify broader volatility patterns and major market shifts. On the other hand, decreasing the compression period provides more precise and timely signals for short-term traders. Adjusting the compression multiplier affects the width of the Keltner Channels. Higher multipliers increase the breakout threshold, filtering out smaller price movements and providing more reliable signals during significant market shifts. Lower multipliers make the indicator more sensitive to smaller price ranges, generating more frequent but potentially less reliable signals.

Changing the type of trend filter can drastically change your results. Test out each trend filter type and determine which one will work best for your purposes. Further, the MA periods in the trend filter settings can help you align your trades with the prevailing market direction. Increasing the period smoothes out the trend, filtering out shorter-term fluctuations and focusing on more sustained moves. Decreasing the period allows for quicker responses to changes in trend, capturing shorter-term price swings.

By adjusting the parameters and incorporating additional analysis techniques, you can customize the strategy to suit your trading style and preferences. However, it is crucial to exercise caution, conduct thorough analysis, and practice proper risk management to increase the likelihood of successful trades. Remember that no strategy can guarantee profits, and continuous learning and adaptation are key to long-term trading success.

Take Profit/Stop Loss Settings:

Take profit, stop loss, and trailing percentages are also included, found at the bottom of the Input tab under “TT and TTP” as well as “Stop Loss”. The take profit and stop loss levels will be reflected as green and red lines respectively on the chart as they occur. Make sure to understand the TP/SL ratio that you desire before use, as the desired hit rate/profitability percentage will be affected accordingly. The option for adding in a trailing stop has also been included, with options to choose between an ATR-based trail or a percentage-based trail. This strategy does NOT guarantee future returns. Apply caution in trading regardless of discretionary or algorithmic. Understand the concepts of risk/reward and the intricacies of each strategy choice before utilizing them in your personal trading.

Profitview/Pineconnector Settings:

If you wish to utilize Profitview’s automation system, find the included “Profitview Settings” under the Input tab of the strategy settings menu. If not, skip this section entirely as it can be left blank. Options will be “OPEN LONG TITLE”, “OPEN SHORT TITLE”, “CLOSE LONG TITLE”, and “CLOSE SHORT TITLE”. If you wished to trade SOL, for example, you would put “SOL LONG”, “SOL SHORT”, “SOL CLOSE LONG”, and “SOL CLOSE SHORT” in these areas. Within your Profitview extension, ensure that your Alerts all match these titles. To set an alert for use with Profitview, go to the “Alerts” tab in TradingView, then create an alert. Make sure that your desired asset and timeframe are currently displayed on your screen when creating the alert. Under the “Condition” option of the alert, select the strategy, then select the expiration time. If using TradingView Premium, this can be open-ended. Otherwise, select your desired expiration time and date. This can be updated whenever desired to ensure the strategy does not expire. Under “Alert actions”, nothing necessarily needs to be selected unless so desired. Leave the “Alert name” option empty. For the “Message”, delete the generated message and replace it with {{strategy.order.alert_message}} and nothing else. If using Pineconnector, follow the same directions for setting up an alert, but use the ",buy,,risk=" syntax as noted in the tooltips.

Additional Sample Settings (for ETHUSDT-Binance 45M):

Band/Channel Type - Keltner Channels (Compression Period of 20, Multiplier of 1.8x)

Trend Filter - WMA (50 length, no offset, close as the source)

TP/SL - 3.0% TP / 2.0% SL, 0.005 trailed TP, no trailed SL

Wunder Volatility botWunder Volatility bot

We have used the Average True Range (ATR) in many of its trading versions.

1. ATR with MA. This indicator includes the ATR as well as the simple moving average, which helps to restore the expected market.

2. We apply percentage based ATR to determine how volatile the market is and whether to buy or sell at that time. For trading, we will filter the market and make trades only within the specified range. This range will adjust depending on the asset, so you will need to change the settings if you are trading multiple assets.