The ICT Ultimate Grid | MarketMaverisk GroupThe ICT Ultimate Grid | MarketMaverisk Group

This script is a fully customizable checklist based on ICT (Inner Circle Trader) concepts. It helps traders validate entry conditions across three timeframes:

LTP (Long-Term), ITP (Intermediate-Term), and STP (Short-Term).

⸻

✅ Purpose & Utility:

Instead of generating simple buy/sell signals, this tool assists traders in making structured, confirmation-based decisions. It presents a visual checklist with 11 customizable columns—each can be individually toggled for each timeframe and displays ✅ or ❌ confirmation status.

⸻

🧠 Confirmation Structure:

The checklist covers the following core elements from the ICT methodology:

• ERL⇔IRL and IRL⇔ERL (presented as special confirmations below the table)

• DOL – Drow On liqudity Level

• PD – permium or discuant

• SMT – Smart Money Trap / Inter-market Divergence

• CSD – Change in State of dlivery

• MSS – Market Structure Shift

• MMXM – Market maker (buy or sell) model

• FVG – Fair Value Gap

• OB – Order Block

• BRK.B – breker Block

Each item can be enabled or disabled for LTP, ITP, and STP individually.

⸻

📊 Visual Design:

• Clean, compact table displayed in the top-right corner of the chart.

• Clear color scheme (✅ Green = Confirmed, ❌ Red = Not Confirmed, Grey = Hidden/Disabled).

• Timeframes are stacked row-wise (LTP, ITP, STP).

• Inputs allow fine-grained control over what elements are shown in each timeframe.

• Additional rows are used to confirm:

• HTF Key Level

• Direction: Reversal ↩️ or Continuation 🔂

• Bias: Bullish 🔼 or Bearish 🔽

⸻

📈 Use Case:

This tool is ideal for traders who follow:

• ICT-based trading approaches

• Market structure + Liquidity analysis

• Day trading, scalping, or swing setups

• Confirmation-based entries after higher-timeframe alignment

⸻

⚙️ Recommended Timeframe Settings:

• LTP = D1 or 4H

• ITP = 1H or 15min

• STP = 5min or 3min or 1min

• Session time: Best used between 02:00 and 05:00 on london killzone & 08:00 and 12:00 on New york killzone in New York timezone (UTC -5)

(you can customize this in strategy version)

⸻

🛠 Technical Note:

This version is an indicator and does not generate signals or alerts by itself. For full automation, a strategy version is also available upon request.

⸻

Let me know if you’d like me to also write a “strategy description” or help you prepare the public chart layout 📊 to make your publish clean and attractivE

ค้นหาในสคริปต์สำหรับ "market structure"

TTM Scalper AlertTTM Scalper Alert — Real-Time Pivot Detector

Description:

This is a custom implementation of the classic TTM Scalper Alert, adapted to show early pivot detection and trend structure tracking in real-time. The script identifies potential highs and lows before the full pivot confirmation—giving traders an early edge—and removes outdated signals once pivots are confirmed.

It supports two levels of detection:

Fast Alert Pivots : Identified after Alert Period candles confirm a local reversal.

Confirmed Pivots : Validated only after Pivot Period candles on both sides ensure a true swing high/low.

How It Works:

Fast Detection (Early Pivots):

Detected after Alert Period (AP) candles. These are provisional signals, shown as triangle labels (▲▼) near current price. Only the latest signal is shown; previous fast pivots are deleted to avoid clutter.

Confirmed Pivots:

Detected with a full lookback of Pivot Period (PP) on both sides of the candle. Shown using plotshape with triangle markers (▲▼). Serve as anchors for price structure analysis (HH-HL or LL-LH tracking).

Custom Source Option:

Users can choose to base pivots on High/Low or Close/Open range. Helps adjust sensitivity depending on volatility or bar structure.

How to Interpret:

Trend & Market Structure:

Use Confirmed Pivots (plotshapes) to analyze market structure:

HH → HL: Uptrend

LL → LH: Downtrend

Watch for breaks in structure for possible reversals

Early Alerts:

The floating labels (▲▼) represent early warnings of a potential pivot. Use them to anticipate:

Short-term exhaustion

Quick scalping entries

Divergence setups

Inputs:

Source : Choose from High/Low or Close/Open — affects how pivots are calculated

Alert Period : How fast the script detects an early reversal pattern (used for entry timing)

Pivot Period : How many candles before/after to confirm a full pivot (used for structural analysis)

Best For:

Traders who follow price action and structure

Scalpers and intraday traders who want early signals

Anyone using pivot highs/lows for confluence with other tools (like RSI divergence, Bollinger Bands, VWAP, etc.)

Pro Tips:

Combine this with:

Trend Magic or Supertrend for directional bias

Volume spike filters to confirm reversal intent

RSI/CCI divergence to strengthen reversal pivots

Adjust Alert Period to tune early signal sensitivity (lower = faster but noisier)

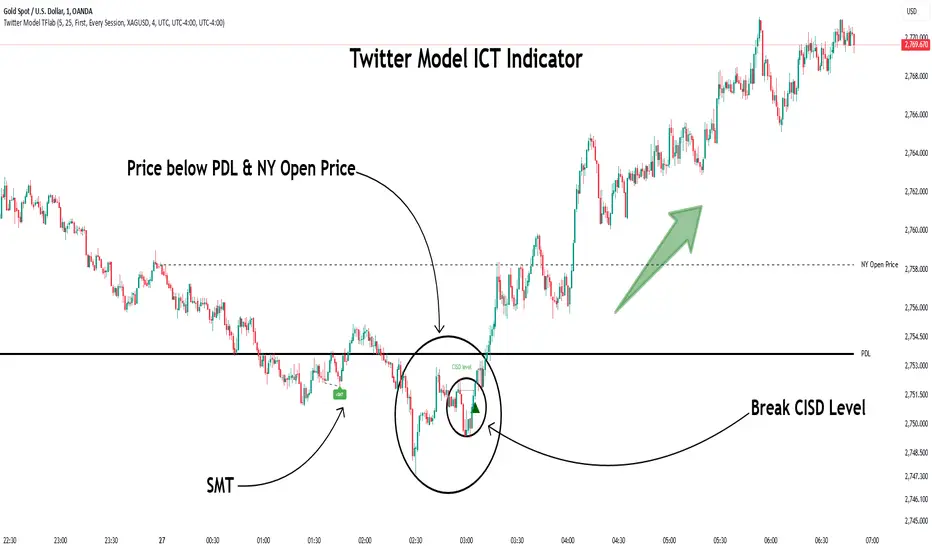

Twitter Model ICT [TradingFinder] MMXM ERL D + FVG + M15 MSS/SMT🔵 Introduction

The Twitter Model ICT is a trading approach based on ICT (Inner Circle Trader) models, focusing on price movement between external and internal liquidity in lower timeframes. This model integrates key concepts such as Market Structure Shift (MSS), Smart Money Technique (SMT) divergence, and CISD level break to identify precise entry points in the market.

The primary goal of this model is to determine key liquidity levels, such as the previous day’s high and low (PDH/PDL) and align them with the Fair Value Gap (FVG) in the 1-hour timeframe. The overall strategy involves framing trades around the 1H FVG and using the M15 Market Structure Shift (MSS) for entry confirmation.

The Twitter Model ICT is designed to utilize external liquidity levels, such as PDH/PDL, as key entry zones. The model identifies FVG in the 1-hour timeframe, which acts as a magnet for price movement. Additionally, traders confirm entries using M15 Market Structure Shift (MSS) and SMT divergence.

Bullish Twitter Model :

In a bullish setup, the price sweeps the previous day’s low (PDL), and after confirming reversal signals, buys are executed in internal liquidity zones. Conversely, in a bearish setup, the price sweeps the previous day’s high (PDH), and after confirming weakness signals, sells are executed.

Bearish Twitter Model :

In short setups, entries are only executed above the Midnight Open, while in long setups, entries are taken below the Midnight Open. Adhering to these principles allows traders to define precise entry and exit points and analyze price movement with greater accuracy based on liquidity and market structure.

🔵 How to Use

The Twitter Model ICT is a liquidity-based trading strategy that analyzes price movements relative to the previous day’s high and low (PDH/PDL) and Fair Value Gap (FVG). This model is applicable in both bullish and bearish directions and utilizes the 1-hour (1H) and 15-minute (M15) timeframes for entry confirmation.

The price first sweeps an external liquidity level (PDH or PDL) and then provides an entry opportunity based on Market Structure Shift (MSS) and SMT divergence. Additionally, the entry should be positioned relative to the Midnight Open, meaning long entries should occur below the Midnight Open and short entries above it.

🟣 Bullish Twitter Model

In a bullish setup, the price first sweeps the previous day’s low (PDL) and reaches an external liquidity level. Then, in the 1-hour timeframe (1H), a bullish Fair Value Gap (FVG) forms, which serves as the price target.

To confirm the entry, a Market Structure Shift (MSS) in the 15-minute timeframe (M15) should be observed, signaling a trend reversal to the upside. Additionally, SMT divergence with correlated assets can indicate weakness in selling pressure.

Under these conditions, a long position is taken below the Midnight Open, with a stop-loss placed at the lowest point of the recent bearish move. The price target for this trade is the FVG in the 1-hour timeframe.

🟣 Bearish Twitter Model

In a bearish setup, the price first sweeps the previous day’s high (PDH) and reaches an external liquidity level. Then, in the 1-hour timeframe (1H), a bearish Fair Value Gap (FVG) is identified, serving as the trade target.

To confirm entry, a Market Structure Shift (MSS) in the 15-minute timeframe (M15) should form, signaling a trend shift to the downside. If an SMT divergence is present, it can provide additional confirmation for the trade.

Once these conditions are met, a short position is taken above the Midnight Open, with a stop-loss placed at the highest level of the recent bullish move. The trade's price target is the FVG in the 1-hour timeframe.

🔵 Settings

Bar Back Check : Determining the return of candles to identify the CISD level.

CISD Level Validity : CISD level validity period based on the number of candles.

Daily Position : Determines whether only the first signal of the day is considered or if signals are evaluated throughout the entire day.

Session : Specifies in which trading sessions the indicator will be active.

Second Symbol : This setting allows you to select another asset for comparison with the primary asset. By default, "XAUUSD" (Gold) is set as the second symbol, but you can change it to any currency pair, stock, or cryptocurrency. For example, you can choose currency pairs like EUR/USD or GBP/USD to identify divergences between these two assets.

Divergence Fractal Periods : This parameter defines the number of past candles to consider when identifying divergences. The default value is 2, but you can change it to suit your preferences. This setting allows you to detect divergences more accurately by selecting a greater number of candles.

The indicator allows displaying sessions based on various time zones. The user can select one of the following options :

UTC (Coordinated Universal Time)

Local Time of the Session

User’s Local Time

Show Open Price : Displays the New York market opening price.

Show PDH / PDL : Displays the previous day’s high and low to identify potential entry points.

Show SMT Divergence : Displays lines and labels for bullish ("+SMT") and bearish ("-SMT") divergences.

🔵 Conclusion

The Twitter Model ICT is an effective approach for analyzing and executing trades in financial markets, utilizing a combination of liquidity principles, market structure, and SMT confirmations to identify optimal entry and exit points.

By analyzing the previous day’s high and low (PDH/PDL), Fair Value Gaps (FVG), and Market Structure Shift (MSS) in the 1H and M15 timeframes, traders can pinpoint liquidity-driven trade opportunities. Additionally, considering the Midnight Open level helps traders avoid random entries and ensures better trade placement.

By applying this model, traders can interpret market movements based on liquidity flow and structural changes, allowing them to fine-tune their trading decisions with higher precision. Ultimately, the Twitter Model ICT provides a structured and logical approach for traders who seek to trade based on liquidity behavior and trend shifts in the market.

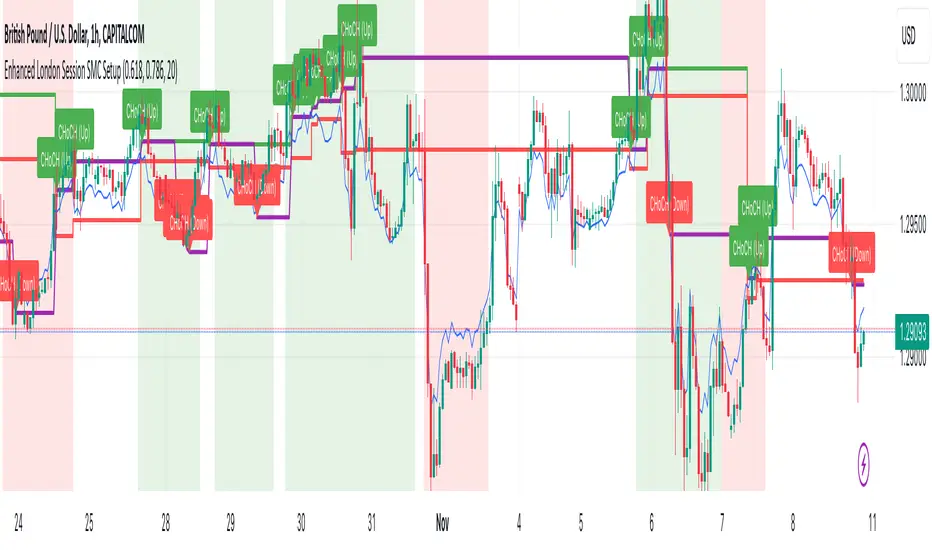

Enhanced London Session SMC SetupEnhanced London Session SMC Setup Indicator

This Pine Script-based indicator is designed for traders focusing on the London trading session, leveraging smart money concepts (SMC) to identify potential trading opportunities in the GBP/USD currency pair. The script uses multiple techniques such as Order Block Detection, Imbalance (Fair Value Gap) Analysis, Change of Character (CHoCH) detection, and Fibonacci retracement levels to aid in market structure analysis, providing a well-rounded approach to trade setups.

Features:

London Session Highlight:

The indicator visually marks the London trading session (from 08:00 AM to 04:00 PM UTC) on the chart using a blue background, signaling when the high-volume, high-impulse moves tend to occur, helping traders focus their analysis on this key session.

Order Block Detection:

Identifies significant impulse moves that may form order blocks (supply and demand zones). Order blocks are areas where institutions have executed large orders, often leading to price reversals or continuation. The indicator plots the high and low of these order blocks, providing key levels to monitor for potential entries.

Imbalance (Fair Value Gap) Detection:

Detects and highlights price imbalances or fair value gaps (FVG) where the market has moved too quickly, creating a gap in price action. These areas are often revisited by price, offering potential trade opportunities. The upper and lower bounds of the imbalance are visually marked for easy reference.

Change of Character (CHoCH) Detection:

This feature identifies potential trend reversals by detecting significant changes in market character. When the price action shifts from bullish to bearish or vice versa, a CHoCH signal is triggered, and the corresponding level is marked on the chart. This can help traders catch trend reversals at key levels.

Fibonacci Retracement Levels:

The script calculates and plots the key Fibonacci retracement levels (0.618 and 0.786 by default) based on the highest and lowest points over a user-defined swing lookback period. These levels are commonly used by traders to identify potential pullback zones where price may reverse or find support/resistance.

Directional Bias Based on Market Structure:

The indicator provides a market structure analysis by comparing the current highs and lows to the previous periods' highs and lows. This helps in identifying whether the market is in a bullish or bearish state, providing a clear directional bias for trade setups.

Alerts:

The indicator comes with built-in alert conditions to notify the trader when an order block, imbalance, CHoCH, or other significant price action event is detected, ensuring timely action can be taken.

Ideal Usage:

Timeframe: Suitable for intraday trading, particularly focusing on the London session (08:00 AM to 04:00 PM UTC).

Currency Pair: Specifically designed for GBP/USD but can be adapted to other pairs with similar market behavior.

Trading Strategy: Best used in conjunction with a price action strategy, focusing on the key levels identified (order blocks, FVG, CHoCH) and using Fibonacci retracement levels for precision entries.

Target Audience: Ideal for traders who follow smart money concepts (SMC) and are looking for a structured approach to identify high-probability setups during the London session.

Fib and Slope Trend Detector [EWT] + MTF Dashboard🚀 Overview

The Momentum Structure Trend Detector is a sophisticated trend-following tool that combines Price Velocity (Slope) with Market Structure (Fibonacci) to identify high-probability trend reversals and continuations.

Unlike traditional indicators that rely heavily on lagging moving averages, this script analyzes the speed of price action in real-time. It operates on the core principle of market structure: Impulse moves are fast and steep, while corrections are slow and shallow.

🧠 The Logic: Physics Meets Market Structure

This indicator determines the trend direction by calculating the Slope (Velocity) of price swings.

ZigZag Calculation: It first identifies market swings (Highs and Lows) using a standard pivot detection algorithm.

Slope Calculation: It calculates the velocity of every completed leg using the formula: $Slope = \frac{|Price Change|}{|Time Duration|}$.

Trend Definition:

Uptrend : If the previous Up-move was fast (Impulse) and the subsequent Down-move is slower (Correction), the market is primed for an uptrend.

Downtrend : If the previous Down-move was fast (Impulse) and the subsequent Up-move is slower (Correction), the market is primed for a downtrend.

🔥 Key Features

1. Aggressive Real-Time Detection (No Lag)

Most structure indicators wait for a "Higher High" to confirm a trend, which often leads to late entries. This script uses an Aggressive Live Slope calculation:

It compares the current developing slope of the live price action against the slope of the previous completed leg.

Result: As soon as the current move becomes "steeper" (faster) than the previous correction, the trend flips immediately. This allows you to catch the "meat" of the move before a new pivot is even confirmed.

2. Fibonacci Validity Filter

Momentum alone isn't enough; we need structural integrity.

The script calculates the 78.6% Retracement level of the impulse leg.

If a correction moves deeper than this Fibonacci limit (on a closing basis), the trend structure is considered "broken" or "invalid," and the indicator switches to a Neutral state. This filters out choppy/ranging markets.

3. Multi-Timeframe (MTF) Dashboard

A customizable dashboard on the chart allows for fractal analysis. You can view the trend state (UP/DOWN/NEUTRAL) across 9 different timeframes (1m to 1M) simultaneously.

Green Row : Uptrend

Red Row : Downtrend

Gray : Neutral/Indeterminate

4. Smart Visuals

Background Colo r: Changes dynamically (Teal for Bullish, Red for Bearish, Gray for Neutral) to give you an instant read of the market state.

Slope Labels : Displays the calculated numeric slope on the chart, helping you visualize the momentum difference between impulse and corrective waves.

Invalidation Levels : Automatically plots the invalidation line (Stop Loss level) based on the market structure.

🛠️ Settings & Inputs

Strategy Settings

Pivot Deviation Length : Sensitivity of the ZigZag calculation (Default: 5). Lower numbers = more sensitive to small swings.

Max Retracement % : The Fibonacci limit for a valid correction (Default: 78.6%).

Min Bars for Live Calc : To prevent noise, the script waits for this many bars after a pivot before calculating the "Live Slope" (Default: 3).

Dashboard Settings

Show Dashboard : Toggle the table on/off.

Timeframe Toggles : Enable/Disable specific timeframes (1m, 5m, 15m, 30m, 1H, 4H, 1D, 1W, 1M) to suit your trading style.

🎯 How to Use

Wait for Background Change : When the background turns Teal, it indicates that a corrective pullback has ended and a new impulse with high velocity has begun.

Check Invalidation : Look at the plotted Stop Loss Level. If price closes below this line, the trade idea is invalid.

Confirm with Dashboard : Use the table to ensure the higher timeframes (e.g., 1H, 4H) align with your current chart's direction for higher probability setups.

Disclaimer : This tool is designed for trend analysis and educational purposes. Past performance (momentum) is not indicative of future results. Always manage your risk.

Dynamic S&R Projector [Polarity Flip]Support and Resistance should not be static. It should tell a story.

Most traders clutter their charts with manually drawn lines, often forgetting which ones were important or which timeframe they came from. This indicator automates the entire process of identifying market structure, adapting dynamically to your trading style while using Volume Price Analysis (VPA) to separate "Smart Money" levels from random noise.

It combines three professional concepts into one tool: Multi-Timeframe Projection, Volume Strength Filtering, and Live Polarity Flipping.

Who is this for?

Day Traders: Project Daily levels onto your 1-minute or 5-minute charts. Stop trading in a vacuum; see the walls before you hit them.

Swing Traders: Project Weekly levels onto your Daily chart to find major trend reversals.

Investors: Project Monthly levels to identify multi-year accumulation zones.

Core Features

1. Smart Timeframe (Auto-Detection) No more toggling settings. The indicator detects what chart you are viewing and automatically projects the next significant Higher Timeframe (HTF) structure:

Viewing Intraday (< Daily)? → Projects Daily Pivots.

Viewing Daily? → Projects Weekly Pivots.

Viewing Weekly? → Projects Monthly Pivots.

2. VPA Strength Filtering (The "Truth" Serum) Not all levels are equal. This script grades every pivot based on the volume activity at the moment it was formed:

Thick Solid Line: Formed on High Volume (>1.5x Average). This is an "Institutional Level." Expect hard bounces.

Thin Dashed Line: Formed on Low Volume. This is a weak structure.

3. Live Polarity Flip (Support ↔ Resistance) The script monitors price action in real-time to respect the "Principle of Polarity."

Wick Protection: The color change is based strictly on the Candle Close. If price wicks through a level but closes back inside, the line retains its original color (rejecting the fakeout).

The Flip: Once price successfully closes past a level, the color instantly flips (Red becomes Green, or Green becomes Red) to indicate the new market state.

How to Trade This Indicator (Example Strategies)

Strategy A: The "Concrete Wall" Bounce (Day & Swing) Identify a Thick Green Line below the current price. This represents a Strong HTF Support defended by institutional volume.

Action: Set Limit Buy orders at the line or wait for a bullish reversal candle (Hammer) to form at the touch.

Strategy B: The "Paper Wall" Breakout (Momentum) Identify price approaching a Thin Dashed Red Line (Weak Resistance).

Action: Since this level lacks volume backing, do not fade it. Look for a breakout setup as price is likely to slice through easily.

Strategy C: The "Flip & Retest" (Trend Following) Watch for a Thick Red Line to turn Green. This means resistance has been conquered.

Action: Wait for price to pull back to this new Green line. If it holds (the line stays Green), enter long. You are now using the "roof" as a "floor."

Settings Guide

Calculation Mode:

Auto (Higher TF): The recommended "Smart" mode described above.

Use Current Chart: Finds pivots on the exact timeframe you are viewing (good for scalping structure).

Fixed Manual: Locks the projection to a specific timeframe (e.g., always show Daily).

Pivot Lookback (Sensitivity):

Default (10/10): Balances major and minor structure.

Higher (20/20): Shows only the most critical major market turns.

Max Number of Lines: Limits how many historical levels are shown to keep your chart clean.

***********************************************************************************************

Disclaimer: This tool is for educational purposes and decision support. Past volume and price action do not guarantee future results. Always manage your risk.

Liquidity Sweep + BOS Retest System — Prop Firm Edition🟦 Liquidity Sweep + BOS Retest System — Prop Firm Edition

A High-Probability Smart Money Strategy Built for NQ, ES, and Funding Accounts

🚀 Overview

The Liquidity Sweep + BOS Retest System (Prop Firm Edition) is a precision-engineered SMC strategy built specifically for prop firm traders. It mirrors institutional liquidity behavior and combines it with strict account-safe entry rules to help traders pass and maintain funding accounts with consistency.

Unlike typical indicators, this system waits for three confirmations — liquidity sweep, displacement, and a clean retest — before executing any trade. Every component is optimized for low drawdown, high R:R, and prop-firm-approved risk management.

Whether you’re trading Apex, TakeProfitTrader, FFF, or OneUp Trader, this system gives you a powerful mechanical framework that keeps you within rules while identifying the market’s highest-probability reversal zones.

🔥 Key Features

1. Liquidity Sweep Detection (Stop Hunt Logic)

Automatically identifies when price clears a previous swing high/low with a sweep confirmation candle.

✔ Filters noise

✔ Eliminates early entries

✔ Locks onto true liquidity grabs

2. Automatic Break of Structure (BOS) Confirmation

Price must show true displacement by breaking structure opposite the sweep direction.

✔ Confirms momentum shift

✔ Removes fake reversals

✔ Ensures institutional intent

3. Precision Retest Entry Model

The strategy enters only when price retests the BOS level at premium/discount pricing.

✔ Zero chasing

✔ Extremely tight stop loss placement

✔ Prop-firm-friendly controlled risk

4. Built-In Risk & Trade Management

SL set at swept liquidity

TP set by user-defined R:R multiplier

Optional session filter (NY Open by default)

One trade at a time (no pyramiding)

Automatically resets logic after each trade

This prevents overtrading — the #1 cause of evaluation and account breaches.

5. Designed for Prop Firm Futures Trading

This script is optimized for:

Trailing/static drawdown accounts

Micro contract precision

Funding evaluations

Low-risk, high-probability setups

Structured, rule-based execution

It reduces randomness and emotional trading by automating the highest-quality SMC sequence.

🎯 The Trading Model Behind the System

Step 1 — Liquidity Sweep

Price must take out a recent high/low and close back inside structure.

This confirms stop-hunting behavior and marks the beginning of a potential reversal.

Step 2 — BOS (Break of Structure)

Price must break the opposite side swing with a displacement candle. This validates a directional shift.

Step 3 — Retest Entry

The system waits for price to retrace into the BOS level and signal continuation.

This creates optimal R:R entry with minimal drawdown.

📈 Best Markets

NQ (NASDAQ Futures) – Highly recommended

ES, YM, RTY

Gold (XAUUSD)

FX majors

Crypto (with high volatility)

Works best on 1m, 2m, 5m, or 15m depending on your trading style.

🧠 Why Traders Love This System

✔ No signals until all confirmations align

✔ Reduces overtrading and emotional decisions

✔ Follows market structure instead of random indicators

✔ Perfect for maintaining long-term funded accounts

✔ Built around institutional-grade concepts

✔ Makes your trading consistent, calm, and rules-based

⚙️ Recommended Settings

Session: 06:30–08:00 MST (NY Open)

R:R: 1.5R – 3R

Contracts: Start with 1–2 micros

Markets: NQ for best structure & volume

📦 What’s Included

Complete strategy logic

All plots, labels, sweep markers & BOS alerts

BOS retest entry automation

Session filtering

Stop loss & take profit system

Full SMC logic pipeline

🏁 Summary

The Liquidity Sweep + BOS Retest System is a complete, prop-firm-ready, structure-based strategy that automates one of the cleanest and most reliable SMC entry models. It is designed to keep you safe, consistent, and rule-compliant while capturing premium institutional setups.

If you want to trade with confidence, discipline, and prop-firm precision — this system is for you.

Good Luck -BG

Pivot Regime Anchored VWAP [CHE] Pivot Regime Anchored VWAP — Detects body-based pivot regimes to classify swing highs and lows, anchoring volume-weighted average price lines directly at higher highs and lower lows for adaptive reference levels.

Summary

This indicator identifies shifts between top and bottom regimes through breakouts in candle body highs and lows, labeling swing points as higher highs, lower highs, lower lows, or higher lows. It then draws anchored volume-weighted average price lines starting from the most recent higher high and lower low, providing dynamic support and resistance that evolve with volume flow. These anchored lines differ from standard volume-weighted averages by resetting only at confirmed swing extremes, reducing noise in ranging markets while highlighting momentum shifts in trends.

Motivation: Why this design?

Traders often struggle with static reference lines that fail to adapt to changing market structures, leading to false breaks in volatile conditions or missed continuations in trends. By anchoring volume-weighted average price calculations to body pivot regimes—specifically at higher highs for resistance and lower lows for support—this design creates reference levels tied directly to price structure extremes. This approach addresses the problem of generic moving averages lagging behind swing confirmations, offering a more context-aware tool for intraday or swing trading.

What’s different vs. standard approaches?

- Baseline reference: Traditional volume-weighted average price indicators compute a running total from session start or fixed periods, often ignoring price structure.

- Architecture differences:

- Regime detection via body breakout logic switches between high and low focus dynamically.

- Anchoring limited to confirmed higher highs and lower lows, with historical recalculation for accurate line drawing.

- Polyline rendering rebuilds only on the last bar to manage performance.

- Practical effect: Charts show fewer, more meaningful lines that start at swing points, making it easier to spot confluences with structure breaks rather than cluttered overlays from continuous calculations.

How it works (technical)

The indicator first calculates the maximum and minimum of each candle's open and close to define body highs and lows. It then scans a lookback window for the highest body high and lowest body low. A top regime triggers when the body high from the lookback period exceeds the window's highest, and a bottom regime when the body low falls below the window's lowest. These regime shifts confirm pivots only when crossing from one state to the other.

For top pivots, it compares the new body high against the previous swing high: if greater, it marks a higher high and anchors a new line; otherwise, a lower high. The same logic applies inversely for bottom pivots. Anchored lines use cumulative price-volume products and volumes from the anchor bar onward, subtracting prior cumulatives to isolate the segment. On pivot confirmation, it loops backward from the current bar to the anchor, computing and storing points for the line. New points append as bars advance, ensuring the line reflects ongoing volume weighting.

Initialization uses persistent variables to track the last swing values and anchor bars, starting with neutral states. Data flows from regime detection to pivot classification, then to anchoring and point accumulation, with lines rendered globally on the final bar.

Parameter Guide

Pivot Length — Controls the lookback window for detecting body breakouts, influencing pivot frequency and sensitivity to recent action. Shorter values catch more pivots in choppy conditions; longer smooths for major swings. Default: 30 (bars). Trade-offs/Tips: Min 1; for intraday, try 10–20 to reduce lag but watch for noise; on daily, 50+ for stability.

Show Pivot Labels — Toggles display of text markers at swing points, aiding quick identification of higher highs, lower highs, lower lows, or higher lows. Default: true. Trade-offs/Tips: Disable in multi-indicator setups to declutter; useful for backtesting structure.

HH Color — Sets the line and label color for higher high anchored lines, distinguishing resistance levels. Default: Red (solid). Trade-offs/Tips: Choose contrasting hues for dark/light themes; pair with opacity for fills if added later.

LL Color — Sets the line and label color for lower low anchored lines, distinguishing support levels. Default: Lime (solid). Trade-offs/Tips: As above; green shades work well for bullish contexts without overpowering candles.

Reading & Interpretation

Higher high labels and red lines indicate potential resistance zones where volume weighting begins at a new swing top, suggesting sellers may defend prior highs. Lower low labels and lime lines mark support from a fresh swing bottom, with the line's slope reflecting buyer commitment via volume. Lower highs or higher lows appear as labels without new anchors, signaling possible range-bound action. Line proximity to price shows overextension; crosses may hint at regime shifts, but confirm with volume spikes.

Practical Workflows & Combinations

- Trend following: Enter longs above a rising lower low anchored line after higher low confirmation; filter with rising higher highs for uptrends. Use line breaks as trailing stops.

- Exits/Stops: In downtrends, exit shorts below a higher high line; set aggressive stops above it for scalps, conservative below for swings. Pair with momentum oscillators for divergence.

- Multi-asset/Multi-TF: Defaults suit forex/stocks on 1H–4H; on crypto 15M, shorten length to 15. Scale colors for dark themes; combine with higher timeframe anchors for confluence.

Behavior, Constraints & Performance

Closed-bar logic ensures pivots confirm after the lookback period, with no repainting on historical bars—live bars may adjust until regime shift. No higher timeframe calls, so minimal repaint risk beyond standard delays. Resources include a 2000-bar history limit, label/polyline caps at 200/50, and loops for historical point filling (up to current bar count from anchor, typically under 500 iterations). Known limits: In extreme gaps or low-volume periods, anchors may skew; lines absent until first pivots.

Sensible Defaults & Quick Tuning

Start with the 30-bar length for balanced pivot detection across most assets. For too-frequent pivots in ranges, increase to 50 for fewer signals. If lines lag in trends, reduce to 20 and enable labels for visual cues. In low-volatility assets, widen color contrasts; test on 100-bar history to verify stability.

What this indicator is—and isn’t

This is a structure-aware visualization layer for anchoring volume-weighted references at swing extremes, enhancing manual analysis of regimes and levels. It is not a standalone signal generator or predictive model—always integrate with broader context like order flow or news. Use alongside risk management and position sizing, not as isolated buy/sell triggers.

Many thanks to LuxAlgo for the original script "McDonald's Pattern ". The implementation for body pivots instead of wicks uses a = max(open, close), b = min(open, close) and then highest(a, length) / lowest(b, length). This filters noise from the wicks and detects breakouts over/under bodies. Unusual and targeted, super innovative.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

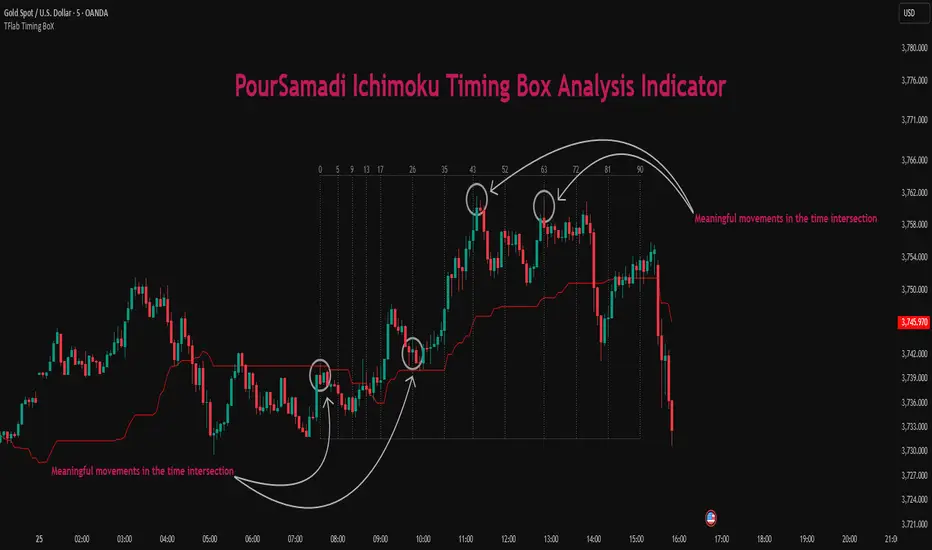

Ichimoku PourSamadi Signal [TradingFinder] KijunSen Magic Number🔵 Introduction

The Ichimoku Kinko Hyo system is one of the most comprehensive market analysis tools ever created. Developed by Goichi Hosoda, a Japanese journalist in the 1930s, its purpose was to allow traders to recognize the balance between price, time, and momentum at a single glance. (In Japanese, Ichimoku literally means “one look.”)

At the core of the system lie five key components: Tenkan-sen (Conversion Line), Kijun-sen (Baseline), Chikou Span (Lagging Line), and the two leading spans, Senkou Span A and Senkou Span B, which together form the well-known Kumo or cloud representing both temporal structure and equilibrium zones in the market.

Although Ichimoku is commonly used to identify trends and support/resistance levels, a deeper layer of time philosophy exists within it. Ichimoku was not designed solely for price analysis but equally for time analysis.

In the classical model, the numerical cycles 9, 26, 52 reflect the natural rhythm of the market originally based on the Tokyo Stock Exchange’s trading schedule in the 1930s.

These values repeat across the system’s calculations, forming the foundation of Ichimoku’s time symmetry where price and time ultimately seek equilibrium.

In recent years, modern analysts have explored new approaches to extract time-based turning points from Ichimoku’s structure. One such approach is the analysis of flat segments on the Kijun-sen and Senkou B lines.

Whenever one of these lines remains flat for a period, it signals temporary balance between buyers and sellers; when the flat breaks, the market exits equilibrium and a new cycle begins.

This indicator is built precisely upon that philosophy. Following the timing methodology introduced by M.A. Poursamadi, the focus shifts away from price signals and line crossovers toward identifying flat periods on Kijun-sen (period 52) as time anchors.

From the first candle that changes the line’s slope, the tool begins a temporal count using a fixed sequence of key numbers: 5, 9, 13, 17, 26, 35, 43, 52, 63, 72, 81, 90.

Derived from both classical Ichimoku cycles and empirical testing, these numbers mark potential timing nodes where a market wave may end, a correction may begin, or a new leg may form.

Thus, this method serves not merely as another Ichimoku tool but as a temporal metronome for market structure a way to visualize moments when the market is ready to change rhythm, often before candles reveal it.

🔵 How to Use

The Kijun Timing BoX is built entirely on Ichimoku’s concept of time analysis.

Its core idea is that within every flat segment of the Kijun-sen, the market enters a temporary balance between opposing forces.

When that flat breaks, a new time cycle begins. From that first breakout candle, the indicator starts counting forward through the predefined time sequence(5, 9, 13, 17, 26, 35, 43, 52, 63, 72, 81, 90).

This counting framework creates a temporal map of market behavior, where each number represents an area where meaningful price fluctuations often occur.

A “meaningful fluctuation” does not necessarily imply reversal or continuation; rather, it marks a moment when the market’s internal energy balance shifts, typically visible as noticeable reactions on lower timeframes.

🟣 Identifying the Anchor Point

The first step is recognizing a valid flat zone on the Kijun-sen.

When this line remains flat for several candles and then changes slope, the indicator marks that bar as the Anchor, initiating the time count.

From that point onward, vertical gray lines appear at each interval in the key-number sequence, visualizing the time nodes ahead.

🟣 Reading the Timing Lines

Each numbered line represents a timing node a temporal point where a change in price rhythm is statistically more likely to occur.

At these nodes, the market may :

Enter a consolidation or minor correction phase.

Develop range-bound movement.

Or simply alter the speed and intensity of its move.

These behaviors do not imply a specific direction; they only highlight zones where time-based activity tends to cluster, giving traders a clearer view of cyclical rhythm.

🟣 Applying Time Analysis

The indicator’s primary use is to observe temporal order, not to predict price direction.

By tracking the distance between Anchors and the reactions that appear near major timing lines, traders can empirically identify each market’s characteristic rhythm—its own time DNA.

For example, one asset may consistently show significant fluctuations around the 13- and 26-bar marks,while another might react closer to 9 or 52. Recognizing such patterns helps traders understand how long typical cycles last before new phases of volatility emerge.

🟣 Combining with Other Tools

The indicator does not generate buy/sell signals on its own.

Its best use is in combination with price- or structure-based methods, to see whether meaningful price reactions occur around the same timing nodes.

In practice, it helps distinguish structured time-based fluctuations from random, noise-driven moves an insight often overlooked in conventional market analysis.

🔵 Settings

🟣 Logical Settings

KijunSen Period : Defines the baseline period used for timing analysis. Default = 52. It is the main line for detecting flats and generating time anchors.

Flat Event Filter : Controls how flat segments are validated before triggering a new timing event.

All : Every flat triggers a new Timing Box.

Automatic : Only flats longer than the historical average are used (recommended).

Custom : User manually defines the minimum flat length via Custom Count.

Update Timing Analysis BoX Per Event : If enabled, a new Timing Box is drawn each time a new flat event occurs. If disabled, the box completes its 90-bar window before refreshing.

🟣 Ichimoku Settings

TenkanSen Period : Defines the period for the Conversion Line (Tenkan-sen). Default = 9.

KijunSen Period : Sets the standard Ichimoku baseline (not the timing line). Default = 26.

Span B Period : Defines the period for Senkou Span B, the slower cloud boundary. Default = 52.

Shift Lines : Offsets cloud projection into the future. Default = 26.

🟣 Display Settings

Users can show or hide all Ichimoku lines Tenkan-sen, Kijun-sen, Chikou Span, Span A, and Span B as well as the Ichimoku Cloud.

They can also customize the color of each element to match personal chart preferences and improve visibility.

🔵 Conclusion

This analytical approach transforms Ichimoku’s time philosophy into a visual and measurable framework. A flat Kijun-sen represents a moment of market equilibrium; when its slope shifts, a new temporal cycle begins.

The purpose is not to forecast price direction but to highlight periods when meaningful fluctuations are more likely to develop.

Through this perspective, traders can observe the hidden rhythm of market time and expand their analysis beyond price into a broader time-cycle dimension.

Ultimately, the method revives Ichimoku’s original principle: the market can only be truly understood through the simultaneous harmony of price, time, and balance.

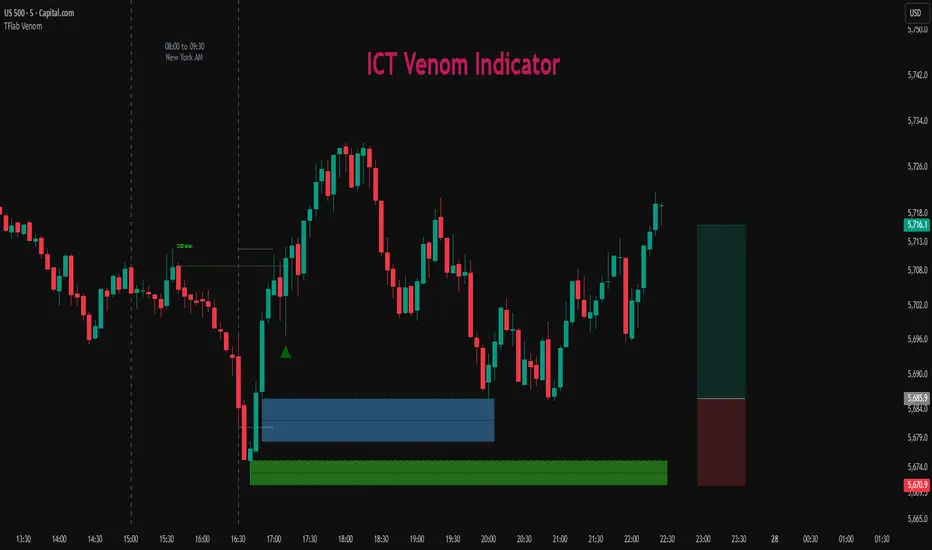

ICT Venom Trading Model [TradingFinder] SMC NY Session 2025SetupIntroduction

The ICT Venom Model is one of the most advanced strategies in the ICT framework, designed for intraday trading on major US indices such as US100, US30, and US500. This model is rooted in liquidity theory, time and price dynamics, and institutional order flow.

The Venom Model focuses on detecting Liquidity Sweeps, identifying Fair Value Gaps (FVG), and analyzing Market Structure Shifts (MSS). By combining these ICT core concepts, traders can filter false breakouts, capture sharp reversals, and align their entries with the real institutional liquidity flow during the New York Session.

Key Highlights of ICT Venom Model :

Intraday focus : Optimized for US indices (US100, US30, US500).

Time element : Critical window is 08:00–09:30 AM (Venom Box).

Liquidity sweep logic : Price grabs liquidity at 09:30 AM open.

Confirmation tools : MSS, CISD, FVG, and Order Blocks.

Dual setups : Works in both Bullish Venom and Bearish Venom conditions.

At its core, the ICT Venom Strategy is a framework that explains how institutional players manipulate liquidity pools by engineering false breakouts around the initial range of the market. Between 08:00 and 09:30 AM New York time, a range called the “Venom Box” is formed.

This range acts as a trap for retail traders, and once the 09:30 AM market open occurs, price usually sweeps either the high or the low of this box to collect stop-loss liquidity. After this liquidity grab, the market often reverses sharply, giving birth to a classic Bullish Venom Setup or Bearish Venom Setup

The Venom Model (ICT Venom Trading Strategy) is not just a pattern recognition tool but a precise institutional trading model based on time, liquidity, and market structure. By understanding the Initial Balance Range, watching for Liquidity Sweeps, and entering trades from FVG zones or Order Blocks, traders can anticipate market reversals with high accuracy. This strategy is widely respected among ICT followers because it offers both risk management discipline and clear entry/exit conditions. In short, the Venom Model transforms liquidity manipulation into actionable trading opportunities.

Bullish Setup :

Bearish Setup :

🔵 How to Use

The ICT Venom Model is applied by observing price behavior during the early hours of the New York session. The first step is to define the Initial Range, also called the Venom Box, which is formed between 08:00 and 09:30 AM EST. This range marks the high and low points where institutional traders often create traps for retail participants. Once the official market opens at 09:30 AM, price usually sweeps either the top or bottom of this box to collect liquidity.

After this liquidity grab, the market tends to reverse in alignment with the true directional bias. To confirm the setup, traders look for signals such as a Market Structure Shift (MSS), Change in State of Delivery (CISD), or the appearance of a Fair Value Gap (FVG). These elements validate the reversal and provide precise levels for trade execution.

🟣 Bullish Setup

In a Bullish Venom Setup, the market first sweeps the low of the Venom Box after 09:30 AM, triggering sell-side liquidity collection. This downward move is often sharp and deceptive, designed to stop out retail long positions and attract new sellers. Once liquidity is taken, the market typically shifts direction, forming an MSS or CISD that signals a reversal to the upside.

Traders then wait for price to retrace into a Fair Value Gap or a demand-side Order Block created during the reversal leg. This retracement offers the ideal entry point for long positions. Stop-loss placement should be just below the liquidity sweep low, while profit targets are set at the Venom Box high and, if momentum continues, at higher session or daily highs.

🟣 Bearish Setup

In a Bearish Venom Setup, the process is similar but reversed. After the Initial Range is defined, if price breaks above the Venom Box high following the 09:30 AM open, it signals a false breakout designed to collect buy-side liquidity. This move usually traps eager buyers and clears out stop-losses above the high.

After the liquidity sweep, confirmation comes through an MSS or CISD pointing to a reversal downward. At this stage, traders anticipate a retracement into a Fair Value Gap or a supply-side Order Block formed during the reversal. Short entries are taken within this zone, with stop-loss positioned just above the liquidity sweep high. The logical profit targets include the Venom Box low and, in stronger bearish momentum, deeper session or daily lows.

🔵 Settings

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

CISD : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

🔵 Conclusion

The ICT Venom Model is more than just a reversal setup; it is a complete intraday trading framework that blends liquidity theory, time precision, and market structure analysis. By focusing on the Initial Range between 08:00 and 09:30 AM New York time and observing how price reacts at the 09:30 AM open, traders can identify liquidity sweeps that reveal institutional intentions.

Whether in a Bullish Venom Setup or a Bearish Venom Setup, the model allows for precise entries through Fair Value Gaps (FVGs) and Order Blocks, while maintaining clear risk management with well-defined stop-loss and target levels.

Ultimately, the ICT Venom Model provides traders with a structured way to filter false moves and align their trades with institutional order flow. Its strength lies in transforming liquidity manipulation into actionable opportunities, giving intraday traders an edge in timing, accuracy, and consistency. For those who master its logic, the Venom Model becomes not only a strategy for entry and exit, but also a deeper framework for understanding how liquidity truly drives price in the New York session.

Apex Edge - MTF Confluence PanelApex Edge – MTF Confluence Panel

Description:

The Apex Edge – MTF Confluence Panel is a powerful multi-timeframe analysis tool built to streamline trade decision-making by aggregating key confluences across three user-defined timeframes. The panel visually presents the state of five core market signals—Trend, Momentum, Sweep, Structure, and Trap—alongside a unified Score column that summarizes directional bias with clarity.

Traders can customize the number of bullish/bearish conditions required to trigger a score signal, allowing the tool to be tailored for both conservative and aggressive trading styles. This script is designed for those who value a clean, structured, and objective approach to identifying market alignment—whether scalping or swing trading.

How it Works:

Across each of the three selected timeframes, the panel evaluates:

Trend: Based on a user-configurable Hull Moving Average (HMA), the script compares price relative to trend to determine bullish, bearish, or neutral bias.

Momentum: Uses OBV (On-Balance Volume) with volume spike detection to identify bursts of strong buying or selling pressure.

Sweep: Detects potential liquidity grabs by identifying price rejections beyond prior swing highs/lows. A break below a previous low with reversal signals bullish intent (and vice versa for bearish).

Structure: Uses dynamic pivot-based logic to identify market structure breaks (BOS) beyond recent confirmed swing levels.

Trap: Flags potential false moves by measuring RSI overbought/oversold signal clusters combined with minimal price movement—highlighting exhaustion or deceptive breaks.

Score: A weighted consensus of the above components. The number of required confluences to trigger a score (default: 3) can be set by the user via input, offering flexibility in signal sensitivity.

Why It’s Useful for Traders:

Quick Decision-Making: The color-coded panel provides instant visual feedback on whether confluences align across timeframes—ideal for fast-paced environments like scalping or high-volatility news sessions.

Multi-Timeframe Confidence: Helps eliminate guesswork by confirming whether higher and lower timeframe conditions support your trade idea.

Customizability: Adjustable confluence threshold means traders can fine-tune how sensitive the system is—more signals for faster entries, stricter confluence for higher conviction trades.

Built-In Alerts: Automated alerts for score alignment, trap detection, and liquidity sweeps allow traders to stay informed even when away from the screen.

Strategic Edge: Supports directional bias confirmation and trade filtering with logic designed to mimic professional decision-making workflows.

Features:

Clean, real-time confluence table across three user-selected timeframes

Configurable score sensitivity via “Minimum Confluences for Score” input

Cell-based colour coding for at-a-glance trade direction

Built-in alerts for score alignment, traps, and sweep triggers

Note - This Indicator works great in sync with Apex Edge - Session Sweep Pro

Useful levels for TP = previous session high/low boxes or fib levels.

⚠️ Disclaimer:

This script is for informational and educational purposes only and should not be considered financial advice. Always perform your own due diligence and practice proper risk management when trading.

Institutional Support/Resistance Locator🏛️ Institutional Support/Resistance Locator

Overview

The Institutional Support/Resistance Locator identifies high-probability demand and supply zones based on strong price rejection, large candle bodies, and elevated volume . These zones are commonly targeted or defended by institutional participants, helping traders anticipate potential reversal or continuation areas.

⸻

How It Works

The indicator uses a confluence of conditions to detect zones:

• Large Body Candles: Body size must exceed the moving average body size multiplied by a user-defined factor.

• High Volume: Volume must exceed the moving average volume by a configurable multiplier.

• Wick Rejection: Candles must show strong upper or lower wicks indicating aggressive rejection.

• If all criteria are met:

• Bullish candles form a Demand Zone.

• Bearish candles form a Supply Zone.

Each zone is plotted for a customizable number of future bars, representing areas where institutions may re-engage with the market.

⸻

Key Features

• ✅ Highlights institutional demand and supply areas dynamically

• ✅ Customizable sensitivity: body, volume, wick, padding, and zone extension

• ✅ Zones plotted as translucent regions with auto-expiry

• ✅ Works across all timeframes and markets

⸻

How to Use

• Trend Traders: Use demand zones for potential bounce entries in uptrends, and supply zones for pullback short entries in downtrends.

• Range Traders: Use zones as potential reversal points inside sideways market structures.

• Scalpers & Intraday Traders: Combine with volume or price action near zones for refined entries.

Always validate zone reactions with supporting indicators or price behavior.

⸻

Why This Combination?

The combination of wick rejection, volume confirmation, and large candle structure is designed to reflect footprints of smart money. Rather than relying on fixed pivots or subjective zones, this logic adapts to the current market context with statistically grounded conditions.

⸻

Why It’s Worth Using

This tool offers traders a structured way to interpret institutional activity on charts without relying on guesswork. By plotting potential high-impact areas, it helps improve reaction time.

⸻

Note :

• This script is open-source and non-commercial.

• No performance guarantees or unrealistic claims are made.

• It is intended for educational and analytical purposes only.

FVG, Swing, Target, D/W/M High Low Detector Basic by Trader Riaz"FVG, Swing, Target, D/W/M High Low Detector Basic by Trader Riaz " is a powerful TradingView indicator designed to enhance your trading strategy by identifying key market structures and levels. This all-in-one tool detects Fair Value Gaps (FVGs), Swing Highs/Lows, and previous Day, Previous Week, and Previous Month Highs/Lows, helping traders make informed decisions with ease.

Key Features:

Bullish & Bearish FVG Detection: Highlights Fair Value Gaps with customizable colors, labels, and extension options.

Swing Highs & Lows: Automatically detects and marks Swing Highs and Lows with adjustable display settings and extensions.

Next Target Levels: Identifies potential price targets based on market direction (rising or falling).

Daily, Weekly, and Monthly High/Low Levels: Displays previous day, week, and month highs/lows with customizable colors.

Customizable Settings: Fully adjustable inputs for colors, number of levels to display, and extension periods.

Clean Visuals: Intuitive and non-intrusive design with dashed lines, labels, and tooltips for better chart readability.

This indicator is ideal for traders looking to identify key price levels, improve market structure analysis, and enhance their trading strategies.

Happy Trading,

Trader Riaz

ICT FVG & Swing Detector Basic by Trader RiazICT FVG & Swing Detector Basic by Trader Riaz

Unlock Precision Trading with the Ultimate Fair Value Gap (FVG) and Swing Detection Tool!

Developed by Trader Riaz , the ICT FVG and Swing Detector Basic is a powerful Pine Script indicator designed to help traders identify key market structures with ease. Whether you're a day trader, swing trader, or scalper, this indicator provides actionable insights by detecting Bullish and Bearish Fair Value Gaps (FVGs) and Swing Highs/Lows on any timeframe. Perfect for trading forex, stocks, crypto, and more on TradingView!

Key Features:

1: Bullish and Bearish FVG Detection

- Automatically identifies Bullish FVGs (highlighted in green) and Bearish FVGs (highlighted in red) to spot potential reversal or continuation zones.

- Displays FVGs as shaded boxes with a dashed midline at 70% opacity, making it easy to see the midpoint of the gap for precise entries and exits.

- Labels are placed inside the FVG boxes at the extreme right for clear visibility.

2: Customizable FVG Display

- Control the number of Bullish and Bearish FVGs displayed on the chart with user-defined inputs (fvg_bull_count and fvg_bear_count).

- Toggle the visibility of Bullish and Bearish FVGs with simple checkboxes (show_bull_fvg and show_bear_fvg) to declutter your chart.

3: Swing High and Swing Low Detection

- Detects Swing Highs (blue lines) and Swing Lows (red lines) to identify key market turning points.

- Labels are positioned at the extreme right edge of the lines for better readability and alignment.

- Customize the number of Swing Highs and Lows displayed (swing_high_count and swing_low_count) to focus on the most recent market structures.

4: Fully Customizable Display

- Toggle visibility for Swing Highs and Lows (show_swing_high and show_swing_low) to suit your trading style.

- Adjust the colors of Swing High and Low lines (swing_high_color and swing_low_color) to match your chart preferences.

5: Clean and Efficient Design

- Built with Pine Script v6 for optimal performance on TradingView.

- Automatically removes older FVGs and Swing points when the user-defined count is exceeded, keeping your chart clean and focused.

- Labels are strategically placed to avoid clutter while providing clear information.

Why Use This Indicator?

Precision Trading: Identify high-probability setups with FVGs and Swing points, commonly used in Smart Money Concepts (SMC) and Institutional Trading strategies.

User-Friendly: Easy-to-use inputs allow traders of all levels to customize the indicator to their needs.

Versatile: Works on any market (Forex, Stocks, Crypto, Commodities) and timeframe (1M, 5M, 1H, 4H, Daily, etc.).

Developed by Trader Riaz: Backed by the expertise of Trader Riaz, a seasoned trader dedicated to creating tools that empower the TradingView community.

How to Use:

- Add the Custom FVG and Swing Detector to your chart on TradingView.

- Adjust the input settings to control the number of FVGs and Swing points displayed.

- Toggle visibility for Bullish/Bearish FVGs and Swing Highs/Lows as needed.

- Use the identified FVGs and Swing points to plan your trades, set stop-losses, and target key levels.

Ideal For:

- Traders using Smart Money Concepts (SMC), Price Action, or Market Structure strategies.

- Those looking to identify liquidity grabs, imbalances, and trend reversals.

- Beginners and advanced traders seeking a reliable tool to enhance their technical analysis.

Happy trading!

paranimonipobre

Chart Description: Buy Low, Sell High with Market Structure

This chart utilizes a dynamic trading strategy based on Bollinger Bands, RSI, and market structure analysis to identify high-probability buy and sell signals while aligning with prevailing trends.

Key Elements:

Bollinger Bands:

The upper (red) and lower (green) bands define volatility boundaries based on standard deviations.

The middle line (blue) represents the 20-period simple moving average.

Market Structure:

Swing highs (red triangles labeled "SH") and swing lows (green triangles labeled "SL") are identified to analyze the trend.

Background colors indicate trend direction:

Green Background: Uptrend (Higher Lows).

Red Background: Downtrend (Lower Highs).

RSI Indicator:

Shown in a separate pane, with overbought (red) at 70 and oversold (green) at 30.

Helps confirm signal validity by identifying momentum extremes.

Buy and Sell Signals:

Buy Signals (Green):

Triggered when the price crosses above the lower Bollinger Band, RSI is oversold (<30), and the market is in an uptrend.

Displayed as green "BUY" labels below bars.

Sell Signals (Red):

Triggered when the price crosses below the upper Bollinger Band, RSI is overbought (>70), and the market is in a downtrend.

Displayed as red "SELL" labels above bars.

How to Use:

Trend Identification:

Follow market structure analysis to determine the current trend direction.

Trade only in the direction of the trend (e.g., buy in an uptrend, sell in a downtrend).

Signal Confirmation:

Look for signals aligning with Bollinger Bands, RSI levels, and market structure.

Ignore signals that conflict with the trend to avoid false entries.

Market Conditions:

Best suited for trending markets with clear higher lows or lower highs.

Signals in choppy or sideways markets may require additional confirmation.

Trading IQ - ICT LibraryLibrary "ICTlibrary"

Used to calculate various ICT related price levels and strategies. An ongoing project.

Hello Coders!

This library is meant for sourcing ICT related concepts. While some functions might generate more output than you require, you can specify "Lite Mode" as "true" in applicable functions to slim down necessary inputs.

isLastBar(userTF)

Identifies the last bar on the chart before a timeframe change

Parameters:

userTF (simple int) : the timeframe you wish to calculate the last bar for, must be converted to integer using 'timeframe.in_seconds()'

Returns: bool true if bar on chart is last bar of higher TF, dalse if bar on chart is not last bar of higher TF

necessaryData(atrTF)

returns necessaryData UDT for historical data access

Parameters:

atrTF (float) : user-selected timeframe ATR value.

Returns: logZ. log return Z score, used for calculating order blocks.

method gradBoxes(gradientBoxes, idColor, timeStart, bottom, top, rightCoordinate)

creates neon like effect for box drawings

Namespace types: array

Parameters:

gradientBoxes (array) : an array.new() to store the gradient boxes

idColor (color)

timeStart (int) : left point of box

bottom (float) : bottom of box price point

top (float) : top of box price point

rightCoordinate (int) : right point of box

Returns: void

checkIfTraded(tradeName)

checks if recent trade is of specific name

Parameters:

tradeName (string)

Returns: bool true if recent trade id matches target name, false otherwise

checkIfClosed(tradeName)

checks if recent closed trade is of specific name

Parameters:

tradeName (string)

Returns: bool true if recent closed trade id matches target name, false otherwise

IQZZ(atrMult, finalTF)

custom ZZ to quickly determine market direction.

Parameters:

atrMult (float) : an atr multiplier used to determine the required price move for a ZZ direction change

finalTF (string) : the timeframe used for the atr calcuation

Returns: dir market direction. Up => 1, down => -1

method drawBos(id, startPoint, getKeyPointTime, getKeyPointPrice, col, showBOS, isUp)

calculates and draws Break Of Structure

Namespace types: array

Parameters:

id (array)

startPoint (chart.point)

getKeyPointTime (int) : the actual time of startPoint, simplystartPoint.time

getKeyPointPrice (float) : the actual time of startPoint, simplystartPoint.price

col (color) : color of the BoS line / label

showBOS (bool) : whether to show label/line. This function still calculates internally for other ICT related concepts even if not drawn.

isUp (bool) : whether BoS happened during price increase or price decrease.

Returns: void

method drawMSS(id, startPoint, getKeyPointTime, getKeyPointPrice, col, showMSS, isUp, upRejections, dnRejections, highArr, lowArr, timeArr, closeArr, openArr, atrTFarr, upRejectionsPrices, dnRejectionsPrices)

calculates and draws Market Structure Shift. This data is also used to calculate Rejection Blocks.

Namespace types: array

Parameters:

id (array)

startPoint (chart.point)

getKeyPointTime (int) : the actual time of startPoint, simplystartPoint.time

getKeyPointPrice (float) : the actual time of startPoint, simplystartPoint.price

col (color) : color of the MSS line / label

showMSS (bool) : whether to show label/line. This function still calculates internally for other ICT related concepts even if not drawn.

isUp (bool) : whether MSS happened during price increase or price decrease.

upRejections (array)

dnRejections (array)

highArr (array) : array containing historical highs, should be taken from the UDT "necessaryData" defined above

lowArr (array) : array containing historical lows, should be taken from the UDT "necessaryData" defined above

timeArr (array) : array containing historical times, should be taken from the UDT "necessaryData" defined above

closeArr (array) : array containing historical closes, should be taken from the UDT "necessaryData" defined above

openArr (array) : array containing historical opens, should be taken from the UDT "necessaryData" defined above

atrTFarr (array) : array containing historical atr values (of user-selected TF), should be taken from the UDT "necessaryData" defined above

upRejectionsPrices (array) : array containing up rejections prices. Is sorted and used to determine selective looping for invalidations.

dnRejectionsPrices (array) : array containing down rejections prices. Is sorted and used to determine selective looping for invalidations.

Returns: void

method getTime(id, compare, timeArr)

gets time of inputted price (compare) in an array of data

this is useful when the user-selected timeframe for ICT concepts is greater than the chart's timeframe

Namespace types: array

Parameters:

id (array) : the array of data to search through, to find which index has the same value as "compare"

compare (float) : the target data point to find in the array

timeArr (array) : array of historical times

Returns: the time that the data point in the array was recorded

method OB(id, highArr, signArr, lowArr, timeArr, sign)

store bullish orderblock data

Namespace types: array

Parameters:

id (array)

highArr (array) : array of historical highs

signArr (array) : array of historical price direction "math.sign(close - open)"

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

sign (int) : orderblock direction, -1 => bullish, 1 => bearish

Returns: void

OTEstrat(OTEstart, future, closeArr, highArr, lowArr, timeArr, longOTEPT, longOTESL, longOTElevel, shortOTEPT, shortOTESL, shortOTElevel, structureDirection, oteLongs, atrTF, oteShorts)

executes the OTE strategy

Parameters:

OTEstart (chart.point)

future (int) : future time point for drawings

closeArr (array) : array of historical closes

highArr (array) : array of historical highs

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

longOTEPT (string) : user-selected long OTE profit target, please create an input.string() for this using the example below

longOTESL (int) : user-selected long OTE stop loss, please create an input.string() for this using the example below

longOTElevel (float) : long entry price of selected retracement ratio for OTE

shortOTEPT (string) : user-selected short OTE profit target, please create an input.string() for this using the example below

shortOTESL (int) : user-selected short OTE stop loss, please create an input.string() for this using the example below

shortOTElevel (float) : short entry price of selected retracement ratio for OTE

structureDirection (string) : current market structure direction, this should be "Up" or "Down". This is used to cancel pending orders if market structure changes

oteLongs (bool) : input.bool() for whether OTE longs can be executed

atrTF (float) : atr of the user-seleceted TF

oteShorts (bool) : input.bool() for whether OTE shorts can be executed

@exampleInputs

oteLongs = input.bool(defval = false, title = "OTE Longs", group = "Optimal Trade Entry")

longOTElevel = input.float(defval = 0.79, title = "Long Entry Retracement Level", options = , group = "Optimal Trade Entry")

longOTEPT = input.string(defval = "-0.5", title = "Long TP", options = , group = "Optimal Trade Entry")

longOTESL = input.int(defval = 0, title = "How Many Ticks Below Swing Low For Stop Loss", group = "Optimal Trade Entry")

oteShorts = input.bool(defval = false, title = "OTE Shorts", group = "Optimal Trade Entry")

shortOTElevel = input.float(defval = 0.79, title = "Short Entry Retracement Level", options = , group = "Optimal Trade Entry")

shortOTEPT = input.string(defval = "-0.5", title = "Short TP", options = , group = "Optimal Trade Entry")

shortOTESL = input.int(defval = 0, title = "How Many Ticks Above Swing Low For Stop Loss", group = "Optimal Trade Entry")

Returns: void (0)

displacement(logZ, atrTFreg, highArr, timeArr, lowArr, upDispShow, dnDispShow, masterCoords, labelLevels, dispUpcol, rightCoordinate, dispDncol, noBorders)

calculates and draws dispacements

Parameters:

logZ (float) : log return of current price, used to determine a "significant price move" for a displacement

atrTFreg (float) : atr of user-seleceted timeframe

highArr (array) : array of historical highs

timeArr (array) : array of historical times

lowArr (array) : array of historical lows

upDispShow (int) : amount of historical upside displacements to show

dnDispShow (int) : amount of historical downside displacements to show

masterCoords (map) : a map to push the most recent displacement prices into, useful for having key levels in one data structure

labelLevels (string) : used to determine label placement for the displacement, can be inside box, outside box, or none, example below

dispUpcol (color) : upside displacement color

rightCoordinate (int) : future time for displacement drawing, best is "last_bar_time"

dispDncol (color) : downside displacement color

noBorders (bool) : input.bool() to remove box borders, example below

@exampleInputs

labelLevels = input.string(defval = "Inside" , title = "Box Label Placement", options = )

noBorders = input.bool(defval = false, title = "No Borders On Levels")

Returns: void

method getStrongLow(id, startIndex, timeArr, lowArr, strongLowPoints)

unshift strong low data to array id

Namespace types: array

Parameters:

id (array)

startIndex (int) : the starting index for the timeArr array of the UDT "necessaryData".

this point should start from at least 1 pivot prior to find the low before an upside BoS

timeArr (array) : array of historical times

lowArr (array) : array of historical lows

strongLowPoints (array) : array of strong low prices. Used to retrieve highest strong low price and see if need for

removal of invalidated strong lows

Returns: void

method getStrongHigh(id, startIndex, timeArr, highArr, strongHighPoints)

unshift strong high data to array id

Namespace types: array

Parameters:

id (array)

startIndex (int) : the starting index for the timeArr array of the UDT "necessaryData".

this point should start from at least 1 pivot prior to find the high before a downside BoS

timeArr (array) : array of historical times

highArr (array) : array of historical highs

strongHighPoints (array)

Returns: void

equalLevels(highArr, lowArr, timeArr, rightCoordinate, equalHighsCol, equalLowsCol, liteMode)

used to calculate recent equal highs or equal lows

Parameters:

highArr (array) : array of historical highs

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

rightCoordinate (int) : a future time (right for boxes, x2 for lines)

equalHighsCol (color) : user-selected color for equal highs drawings

equalLowsCol (color) : user-selected color for equal lows drawings

liteMode (bool) : optional for a lite mode version of an ICT strategy. For more control over drawings leave as "True", "False" will apply neon effects

Returns: void

quickTime(timeString)

used to quickly determine if a user-inputted time range is currently active in NYT time

Parameters:

timeString (string) : a time range

Returns: true if session is active, false if session is inactive

macros(showMacros, noBorders)

used to calculate and draw session macros

Parameters:

showMacros (bool) : an input.bool() or simple bool to determine whether to activate the function

noBorders (bool) : an input.bool() to determine whether the box anchored to the session should have borders

Returns: void

po3(tf, left, right, show)

use to calculate HTF po3 candle

@tip only call this function on "barstate.islast"

Parameters:

tf (simple string)

left (int) : the left point of the candle, calculated as bar_index + left,

right (int) : :the right point of the candle, calculated as bar_index + right,

show (bool) : input.bool() whether to show the po3 candle or not

Returns: void

silverBullet(silverBulletStratLong, silverBulletStratShort, future, userTF, H, L, H2, L2, noBorders, silverBulletLongTP, historicalPoints, historicalData, silverBulletLongSL, silverBulletShortTP, silverBulletShortSL)

used to execute the Silver Bullet Strategy

Parameters:

silverBulletStratLong (simple bool)

silverBulletStratShort (simple bool)

future (int) : a future time, used for drawings, example "last_bar_time"

userTF (simple int)

H (float) : the high price of the user-selected TF

L (float) : the low price of the user-selected TF

H2 (float) : the high price of the user-selected TF

L2 (float) : the low price of the user-selected TF

noBorders (bool) : an input.bool() used to remove the borders from box drawings

silverBulletLongTP (series silverBulletLevels)

historicalPoints (array)

historicalData (necessaryData)

silverBulletLongSL (series silverBulletLevels)

silverBulletShortTP (series silverBulletLevels)

silverBulletShortSL (series silverBulletLevels)

Returns: void

method invalidFVGcheck(FVGarr, upFVGpricesSorted, dnFVGpricesSorted)

check if existing FVGs are still valid

Namespace types: array

Parameters:

FVGarr (array)

upFVGpricesSorted (array) : an array of bullish FVG prices, used to selective search through FVG array to remove invalidated levels

dnFVGpricesSorted (array) : an array of bearish FVG prices, used to selective search through FVG array to remove invalidated levels

Returns: void (0)

method drawFVG(counter, FVGshow, FVGname, FVGcol, data, masterCoords, labelLevels, borderTransp, liteMode, rightCoordinate)

draws FVGs on last bar

Namespace types: map

Parameters:

counter (map) : a counter, as map, keeping count of the number of FVGs drawn, makes sure that there aren't more FVGs drawn

than int FVGshow

FVGshow (int) : the number of FVGs to show. There should be a bullish FVG show and bearish FVG show. This function "drawFVG" is used separately

for bearish FVG and bullish FVG.

FVGname (string) : the name of the FVG, "FVG Up" or "FVG Down"

FVGcol (color) : desired FVG color

data (FVG)

masterCoords (map) : a map containing the names and price points of key levels. Used to define price ranges.

labelLevels (string) : an input.string with options "Inside", "Outside", "Remove". Determines whether FVG labels should be inside box, outside,

or na.

borderTransp (int)

liteMode (bool)

rightCoordinate (int) : the right coordinate of any drawings. Must be a time point.

Returns: void

invalidBlockCheck(bullishOBbox, bearishOBbox, userTF)

check if existing order blocks are still valid

Parameters:

bullishOBbox (array) : an array declared using the UDT orderBlock that contains bullish order block related data