Kaufman's Efficiency Ratio Strategy [KL]I recently published an indicator called "Kaufman's Efficiency Ratio Indicator". In the description of that script, I hypothesized about how the Efficiency Ratio could be applied to identify bullish moves in instances where price had already gone up steeply, but rests for a while, allowing for entry in expectation that price will continually rise. I decided to test out this idea with Pinescript.

About Kaufman's Efficiency Ratio ("ER")

ER was developed by a systematic trader by the name of Perry J. Kaufman.

Formula

The formula is:

= A divided by B,

where:

A = Current closing price minus the closing price at the start of the lookback period

B = Sum of differences between closing prices (in absolute terms) of consecutive bars over the lookback period

How this strategy enters a trade (Long):

- code: entry_signal_long = ER > 0 and ER_is_mid

- meaning: when ER is positive, strategy assumes price has risen. Usually ER value begins high (red), and unless it is a false move, then it should stay positive. This strategy will patiently wait until ER drops to medium (yellow), and then place a trade.

- how low/medium/high is dynamically determined: Refer to the description of my other script("Kaufman's Efficiency Ratio Indicator") for details. Trying to keep this as short as possible.

How this strategy exits a trade (Long):

- when price hits stop limit; stop limit is based on low of bars, trails upward based on ATR

- included a feature called "tightening TSL", which tries to reduce the stop-buffer during periods of high volatility implied by ER (very experimental, opening the floor for suggestions on how this can be improved)

ค้นหาในสคริปต์สำหรับ "implied"

CryptoSignalScanner - MACD Multiple Time FramesDESCRIPTION:

After receiving some multiple request to provide a MACD indicator that displays multiple timeframes at the same time I created this simple script.

You can use this script for free and adjust it as much you like.

With this script you can plot 6 MACD lines & 6 Signal lines.

• Current Timeframe MACD Line

• Current Timeframe Signal Line

• 15 minute candle MACD Line

• 15 minute candle Signal Line

• 30 minute candle MACD Line

• 30 minute candle Signal Line

• 1 hour candle MACD Line

• 1 hour candle Signal Line

• 2 hour candle MACD Line

• 2 hour candle Signal Line

• 4 hour candle MACD Line

• 4 hour candle Signal Line

HOW TO USE:

• When multiple MACD lines on an uptrend are grouped together it is time to SELL.

• When multiple MACD lines on a downtrend are grouped together it is time to BUY.

• The higher to length of the MACD lines the stronger the BUY/SELL signal.

FEATURES:

• You can show/hide the preferred MACD lines.

• You can show/hide the preferred Signal lines.

How MACD works

The MACD indicator is generated by subtracting two exponential moving averages (EMAs) to create the main line (MACD line), which is then used to calculate another EMA that represents the signal line. In addition, there is the MACD histogram, which is calculated based on the differences between those two lines. The histogram, along with the other two lines, fluctuates above and below a center line, which is also known as the zero line.

The MACD indicator consists of three elements moving around the zero line:

• The MACD line. By default the MACD line is calculated by subtracting the 26-day EMA from the 12-day EMA.

MACD line = 12d EMA - 26d EMA

• The signal line. By default the signal line is calculated from a 9-day EMA of the MACD line.

Signal line = 9d EMA of MACD line

• Histogram. The histogram is nothing more than a visual record of the relative movements of the MACD line and the signal line.

It is simply calculated as: MACD line - signal line

REMARKS:

• This advice is NOT financial advice.

• We do not provide personal investment advice and we are not a qualified licensed investment advisor.

• All information found here, including any ideas, opinions, views, predictions, forecasts, commentaries, suggestions, or stock picks, expressed or implied herein, are for informational, entertainment or educational purposes only and should not be construed as personal investment advice.

• We will not and cannot be held liable for any actions you take as a result of anything you read here.

• We only provide this information to help you make a better decision.

• While the information provided is believed to be accurate, it may include errors or inaccuracies.

Good Luck,

SEOCO

Volume using Candle RangeAnother way of finding out a rough estimate of the volume or how much bulls or bears were in control using only the range of the candlesticks in relation to the closing price. If the close is in the higher range zone then the volume is said to have been positive, if the close is in the lower range zone then the volume is said to have been negative. The close is compared to the midpoint of the candle to see how far from the midpoint the close was.

The columns bars show how far each candlestick's close price is to the midpoint of its high and low. It's possible for the column bar to be a different color than the candlestick itself if the close was above or below the midpoint. An average line is shown that takes the average of a given length amount of column bars. There is an option to show the absolute value only of the columns and the average line.

This is based on an idea I found about candlestick range bars implying volume. This is an attempt to put that theory into practice and to see if there's any truth to it. It's not exactly volume and may not always look like it, and it does not show how many trades took place but instead tries to use price in relation to the high and low range.

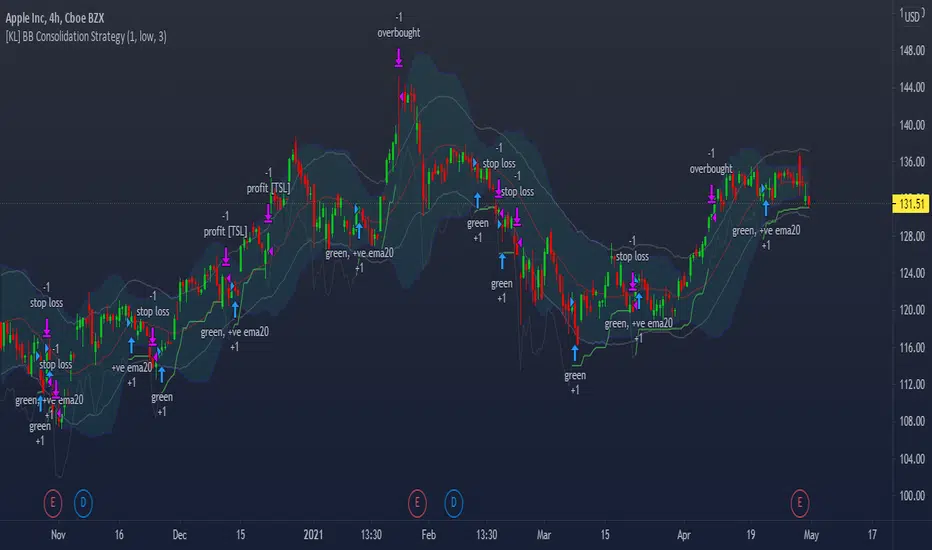

[KL] Bollinger Bands Consolidation StrategyThis strategy will enter into long position based on the volatility of prices implied by indicators of (a) Bollinger bands, and (b) ATR.

Application of Bollinger bands ("BOLL")

Using plain vanilla settings for BOLL (i.e. 20 period moving average, and 2 standard deviations of closing prices), we are interested to know about the shape of the area that is bounded by the upper and lower bands.

In theory, consolidation happens when volatility of price decreases. Visually speaking, this is represented by the narrowing of the upper/lower bands. This strategy considers the narrowing of BOLL bands as the primary indicator for long-entry.

Application of ATRs (as confirmations)

Firstly, to confirm that BOLL bands are narrowing (as mentioned above), the ATR at a potential point of entry is compared against the standard deviation of prices over BOLL's lookback periods. Once again, visualizing the shape of BOLL bands during consolidation, we assume the lines begin to squeeze when the distance between the center line and upper/lower band is less than two current ATRs.

Secondly, this strategy looks into the moving average of ATRs to assure that prices are not too choppy when entering into market. If the moving average of ATR decreases at a point in time such that all the above conditions are met, then we can assert that the volatility of price is decreasing.

Thirdly, ATR is used for determining the size of our trailing stop loss. We will keep the multiplier fixed at two.

MOVE/VXTLT CorrelationMany know of the VIX for equity trading. Yet, many are unaware that there is the same kind of volatility measure for trading bonds, called the MOVE Index.

"The Merrill Lynch Option Volatility Estimate (MOVE) Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options which are weighted on the 2, 5, 10, and 30 year contracts."

With this script one can see the the correlation and divergences between bonds and its volatility measure to make educated decisions in trading or hedging.

The idea of this script comes from NicTheMajestic.

GBTC holdings USD market valueThis script estimates GBTC bitcoins per share, rather than hardcoding as in other scripts. Its result is an estimate of GBTC holdings USD market value.

Per share bitcoin estimates are adjusted by 2.0% / 365 per day from 2019 year end holdings. Calendar year 2019 ending bitcoins and shares were 261,192 bitcoins and 269,445,300 shares. From the 2019 Form 10-K: 'The Trust’s only ordinary recurring expense is the Sponsor’s Fee. The Sponsor’s Fee accrues daily in U.S. dollars at an annual rate of 2.0% of the Bitcoin Holdings.. The Sponsor’s Fee is payable in Bitcoins to the Sponsor monthly in arrears.'

No attempt is made to account for leap years.

Per share bitcoin estimate is converted to USD market value by multiplying by the simple average BTCUSD price at Coinbase and Bitstamp. Grayscale uses the TradeBlock XBX index, a volume weighted average of Coinbase Pro, Kraken, LMAX Digital and Bitstamp prices.

Spot checks vs archive.org captures of daily bitcoins per share and the chart on Grayscale's site:

The estimate for market close January 22 2021 is 0.00094899 bitcoins per share, the published datum on Grayscale's web site was 0.00094898. The estimate matches at 20:30 rather than at 16:00.

The estimate for December 31 2018 is 0.000988965 vs a published 0.00098895.

The estimate for December 29 2017 market value is $14.58 vs $14.65.

The estimate for December 30 2016 market value is $0.99 vs $0.98.

The estimate for January 4 2016 market value is $0.46 vs $0.45.

No estimates before 2016.

The default style is to draw a blue line with two thirds transparency outside market hours and for first/last minutes of trading, switching to daily or greater periodicity hides this.

No warranty is expressed or implied , I am not a lawyer, etc etc etc.

This is not investing advice . Always do your own due diligence .

Normalized Volatility IndicatorFrom an article by Rajesh Kayakkal:

"Early bear phase signals can help you get out of the market before it turns down. This indicator tells you how.

There are many ways to identify the trend of a financial market, the most common being the 200-day exponential moving average (Ema). When price is trending down below the 200-day Ema, the market is believed to be in a bear phase. If the market is trending up above the 200-day Ema, it is considered to be in a bull phase.

Since every indicator fails at times, I wanted to find other indicators to confirm a trend. In my quest for another indicator to determine the trend for the financial markets, I found the Cboe Volatility Index (Vix) to be a good indicator of the market direction. The Vix is calculated from the weighted average of the implied volatilities of various options on the Standard & Poor’s 500 index futures.

J. Welles Wilder’s average true range can also give an indication of the financial market trends; that is, when the market is in a bull phase, the average true range narrows, and when it is in a bear phase, the average true range expands. The normalized volatility indicator (Nvi) is based on this behavior.

Normalized volatility indicator (Nvi)

Average true range (Atr) varies depending on time. But how do we determine the phase of the financial market with Atr? Perhaps some type of ratio could give us a clue. A ratio presents a relationship of a quantity with respect to another. I did some research based on a ratio of the 64-day average true range and the end-of-day value of equity indexes such as the Standard & Poor’s 500 (Spx). I selected the 64-day period since it is close to the average number of trading days in a quarter. The ratio of the 64-day average true range and closing price does discount seasonal variations in the average true range and gives a single number that can be used to compare volatility of an instrument across many decades. I call this ratio the normalized volatility indicator.

I found an interesting correlation between Nvi and cycles of major equity market indexes. The formula for the Nvi is:

Nvi = 64 - Day average true range/End-of-day price * 100

The NVI gave advanced signals before the cyclical bear phase of SPX commenced in October 2000 and was almost on the spot with the bull phase that began in 2003 and the current secular bear market cycle, which started in November 2007."

Includes options to show inverse NVI and change the ATR length and smoothing.

Volatility Rainbow [Nic]What is this

The volatility rainbow tracks divergences in a security and its volatility index. This can be used to identify periods of heightened implied (future) risk.

About Volatility

The volatility is calculated by looking at put / call ratios. When VIX goes up it means that puts are outpacing calls. This is a bearish signal.

About Correlation

When the security goes up while the VIX goes up, the divergence on the plot will increase and turn a color. This should be a warning.

Colors

RED - DIA

BLUE - SPX

GREEN - IWM

GOLD - GLD

YELLOW - QQQ

ORANGE - TLT

White- VVIX

Related

Volatility Prism [Nic]What is this

The volatility rainbow tracks divergences in a security and its volatility index. This can be used to identify periods of heightened implied (future) risk.

About Volatility

The volatility is calculated by looking at put / call ratios. When VIX goes up it means that puts are outpacing calls. This is a bearish signal.

About Correlation

When the security goes up while the VIX goes up, the divergence on the plot will increase and turn a color. This should be a warning.

Volatility Rainbow

This is a similar indicator, but this one merges all signals into a single line.

VIX MTF MomentumSweet little momentum gadget to track the VIX Index.

What is the VIX?

The CBOE S&P 500 Volatility Index (VIX) is known as the 'Fear Index' which can measure how worried traders are that the S&P 500 might suddenly drop within the next 30 days.

When the VIX starts moving higher, it is telling you that traders are getting nervous. When the VIX starts moving lower, it is telling you that traders are gaining confidence.

VIX calculation?

The Chicago Board of Options Exchange Market Volatility Index (VIX) is a measure of implied volatility (Of the S&P 500 securities options), based on the prices of a basket of S&P 500 Index options with 30 days to expiration.

How to use:

If VIX Momentum is above 0 (RED) traders are getting nervous.

If VIX Momentum is below 0 (GREEN) traders are gaining confidence.

Follow to get updates and new scripts: www.tradingview.com

Risk RangeThis indicator creates risk ranges using implied volatility (VIX) or historical volatility, skewness ( Cboe SKEW or estimate ) and kurtosis.

Realized Variables for Options ComparisonThese variables can be used in comparison with the implied volatility of options.

Variables:

Realized Volatility

mathematical notation lowercase 'sigma'

Realized Variance

mathematical notation lowercase 'sigma' squared

Realized Beta

mathematical notation lowercase 'beta'

Timeframes:

Yearly = 250 or 365

Quarterly = 50 or 90

Monthly = 20 or 30

Important Note:

Options Contract Expiry = barmerge.lookahead_on

"Merge strategy for the requested data position. Requested barset is merged with current barset in the order of sorting bars by their opening time. This merge strategy can lead to undesirable effect of getting data from "future" on calculation on history. This is unacceptable in backtesting strategies, but can be useful in indicators."

[ All other timeframes barmerge.lookahead is disabled.

CryptoSignalScanner - Advanced Moving Averages - Cross & RainbowDESCRIPTION:

With this script you can plot 6 moving averages.

You can decide which Moving Average you want to show or hide.

For every plot you can decide to display the Simple Moving Average ( SMA ) or Exponential Moving Average ( EMA ).

It provides CrossOver and CrossUnder labels when loading the script. Those labels you can show or hide.

You have the possibility to show or hide the rainbow colors. This rainbow function gives you a clear view of the current trend.

HOW TO USE:

• When one Moving Average crosses above another Moving Average it signals an uptrend.

• When one Moving Average crosses below another Moving Average it signals a downtrend.

• The higher to length of the Moving Average the stronger the trend.

FEATURES:

• You can show/hide the preferred Moving Averages.

• You can set the length, type and source for every Moving Average.

• You can show/hide the rainbow colors.

• You can show/hide the CrossUp labels.

• You can show/hide the CrossDown labels.

• You can set alerts for every Moving Average.

• Etc...

DEFAULT SETTINGS:

• MA1 => EMA5

• MA2 => EMA10

• MA3 => EMA20

• MA4 => SMA50

• MA5 => SMA100

• MA6 => SMA200

Simple Moving Average vs. Exponential Moving Average:

SMA and EMA are calculated differently. The exponential moving average ( EMA ) focuses more on recent prices than on a long series of data points, as the simple moving average required.

The calculation makes the EMA quicker to react to price changes and the SMA react slower. That is the main difference between the two.

One is not necessarily better than another. It comes down to personal preference. Plot an EMA and SMA of the same length on a chart and see which one helps you make better trading decisions.

Moving Average Trading Strategies:

The first strategy is a price crossover, when the price crosses above or below a moving average, it signals a potential change in trend.

The second strategy applies when one moving averages crosses another moving average.

• When the short-term MA crosses above the long-term MA, it signals a buy signal.

• When the short-term MA crosses below the long-term MA, it signals a sell signal.

REMARKS:

• This advice is NOT financial advice.

• We do not provide personal investment advice and we are not a qualified licensed investment advisor.

• All information found here, including any ideas, opinions, views, predictions, forecasts, commentaries, suggestions, or stock picks, expressed or implied herein, are for informational, entertainment or educational purposes only and should not be construed as personal investment advice.

• We will not and cannot be held liable for any actions you take as a result of anything you read here.

• We only provide this information to help you make a better decision.

• While the information provided is believed to be accurate, it may include errors or inaccuracies.

If you like this script please donate some coins to share your appreciation.

Good Luck,

SEOCO

Volatility SkewThis indicator measure the historical skew of actual volatility for an individual security. It measure the volatility of up moves versus down moves over the period and gives a ratio. When the indicator is greater than one, it indicators that volatility is greater to the upside, when it is below 1 it indicates that volatility is skewed to the downside.

This is not comparable to the SKEW index, since that measures the implied volatility across option strikes, rather than using historical volatility.

Roofing Filter [DW]This is an experimental study built on the concept of using roofing filters on price data proposed by John Ehlers.

Roofing filters are a type of bandpass filter conventionally used in HF radio receivers in the first IF stage to limit the frequency spectrum passed on to later stages in the receiver.

The goal in applying roofing filters to a price signal is to simultaneously attenuate high frequency noise and low frequency distortion to pass an oscillating signal with a nearly zero mean for analysis and/or further calculation.

In this study, there are three filter types to choose from:

-> Ehlers Roofing Filter, which passes data through a 2 pole high pass filter, then through a Super Smoother filter.

-> Gaussian Roofing Filter, which passes data through a 2 pole Gaussian high pass filter, then through a 2 pole Gaussian low pass filter.

-> Butterworth Roofing Filter, which passes data through a 2 pole Butterworth high pass filter, then through a 2 pole Butterworth low pass filter.

Each filter type has different amplitude and delay characteristics, so play around with each type and see which response suits your needs best.

There is an option to normalize the scale of the output as well. The normalization process in this script is computed by comparing positive and negative outputs to the filter's moving RMS value.

The resulting oscillator can be fed through numerous conventional indicators including Stochastic Oscillator, RSI, CCI, etc. to generate smoother, less distorted indicators for a clearer view of turning points.

Alternatively, it can also act as an indicator itself, as implied by the corresponding color scheme included in the script.

Although roofing filters are not conventionally used in the analysis of market data, applying such spectral analysis techniques may prove to be quite useful for the design of more efficient indicators and more reliable predictions.

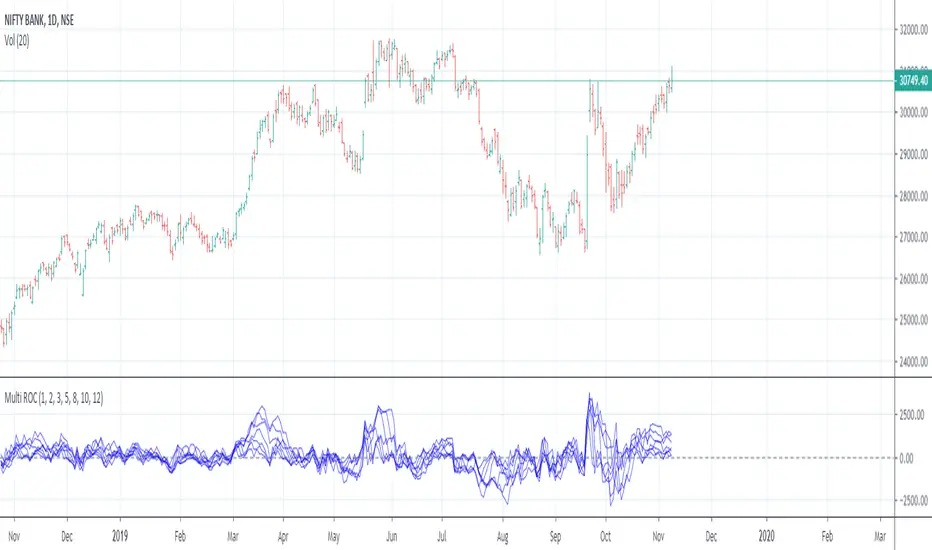

Multiple Rate Of ChangeConvergence of Multiple period Rates of Change near the Zero line shows contraction in volatility.

Soon we can expect expansion in volatility.

Ideal strategy would be to buy ATM Straddles when different period ROCs converge near Zero line.

(Also check implied volatility of options before going for this strategy)

Multistep AutocorrelationAutocorrelation, also known as serial correlation, is the correlation of a signal with a delayed copy of itself as a function of delay. Informally, it is the similarity between observations as a function of the time lag between them. The analysis of autocorrelation is a mathematical tool for finding repeating patterns, such as the presence of a periodic signal obscured by noise, or identifying the missing fundamental frequency in a signal implied by its harmonic frequencies. It is often used in signal processing for analyzing functions or series of values, such as time domain signals.

This multistep autocorrelation function calculates the correlation of roc (rate of change) between an asset at t and t-1 as well as the correlation of the same asset at t and t-4. The output is an average of the two.

If both outputs show a positive correlation, the color will be green.

If only one shows a positive correlation, the color will be yellow.

If neither show a positive correlation, the color will be red.

This indicator can be useful as a filter for strategy entry logic (only enter on strong correlation and the strategy entry condition), or as standalone confirmation of strength in a specific direction. It can also be used to filter chop.

Another potential usecase would be as a variable in regression applications.

Enjoy!

(JS)S&P 500 Volatility Oscillator For Options 2.0I am going to start taking requests to open source my indicators and they will also be updated to Version 4 of Pinescript.

I added some features to the original code such the ability to smooth the oscillator and select the look back periods for the historical volatility.

Link to original:

Original post:

"The idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX ). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX ) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility . (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M ) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX , SPY , even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Feb 17, 2019

Release Notes: Cosmetic update for a much cleaner look:

-Replaced the "HIGH IV" with a simlple "H"

-Now the white line is constantly showing you the relationship between VIX and VIX3M - when VIX is greater than VIX3M the background still goes red

-However, now when VIX drops below Historical Volatility, the background is bright green

-When both above are true - it's dark green

-The Average True Range on the bottom is now a series of crosses"

Casey's Parabolic SARI whipped together this script after having listened to Hyperwave with Sawcruhteez and Tyler Jenks in the evening on July 3, 2019. They felt that the existing Parabolic SAR was not doing its calculations properly, and they hoped that someone might help them correct this. So I tried my hand at it, learning Pine as I went. I don't know if this script works properly (so don't use it!), but it does show a trend change on the weekly this week as it apparently should. I'm making the script public so that Sawcruhteez and Tyler Jenks can take a look at it.

MIT License

Copyright (c) 2019 Casey Bowman

Permission is hereby granted, free of charge, to any person obtaining a copy

of this software and associated documentation files (the "Software"), to deal

in the Software without restriction, including without limitation the rights

to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

copies of the Software, and to permit persons to whom the Software is

furnished to do so, subject to the following conditions:

The above copyright notice and this permission notice shall be included in all

copies or substantial portions of the Software.

THE SOFTWARE IS PROVIDED "AS IS", WITHOUT WARRANTY OF ANY KIND, EXPRESS OR

IMPLIED, INCLUDING BUT NOT LIMITED TO THE WARRANTIES OF MERCHANTABILITY,

FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT. IN NO EVENT SHALL THE

AUTHORS OR COPYRIGHT HOLDERS BE LIABLE FOR ANY CLAIM, DAMAGES OR OTHER

LIABILITY, WHETHER IN AN ACTION OF CONTRACT, TORT OR OTHERWISE, ARISING FROM,

OUT OF OR IN CONNECTION WITH THE SOFTWARE OR THE USE OR OTHER DEALINGS IN THE

SOFTWARE.

Percentage OscillatorUsing momentum calculations on multiple time frames and adding everything together into 4 separate directions:

1- green: the strength and momentum in +45 to +90 degrees angle

2- blue: the strength and momentum in 0 to +45 degrees angle

3- orange: the strength and momentum in 0 to -45 degrees angle

4- red: the strength and momentum in -45 to -90 degrees angle

Single parameter to control the size of the largest moving window.

Uptrend is green with orange corrections

Downtrend is red with blue corrections

When downtrend turns into uptrend, blue becomes green

When uptrend turns into downtrend, orange becomes red

The natural cycle of the market is RED->BLUE->GREEN->ORANGE and so on, you will see the cycle repeats itself 3 times before a break up\down. The strength of the movement depends on the height and width of all the waves that created the 3 cycle movement (reminds Elliot in an oscillatory representation)

The script is provided as is, there are no trading strategies implied or recommended.

Feel free to PM with questions

Daily Deviations (Self Input Version)

Plots the standard deviation resistance/support levels.

Input the previous settlement price and the implied volatility.

credit to u/UberBotMan and u/Living_Granger for the idea and formulas

(preview example is using settlement of 2420 and IV of 11)

ST_Trend_ReversalSTRONG TREND REVERSAL INDICATOR

The code is the percentage difference between the spot price of a given financial asset and its 200-day MA of that period. My standard setup is Daily, and I think it's got very good predictive power at that timeframe.

It can be read in two ways:

1. Values extremely above or below the 200-period MA present chances of buying/selling agains the prevailing trend.

2. Values closely above or below the 200-period MA are make-or-break market periods, where a medium-term trend becomes evident. Breaks above or below the MA are associated with strong chances of directional movements. But it's not fool-proof as false breaks have become commonplace nowadays.

Other way to use it is as confirmation of breakdowns: For example, an asset that loses its 200-day MA and then can't rally above it becomes exposed to steep losses afterwards.

It's also helpful to use in volatility trading: the closer the asset goes to its MA, the lower goes implied vol, and thus better opportiunities to be long volatility on those occasions where direction is hard to predict.

STRI = close/(200dMA)

Values over 100 indicate percentage premiums of spot vs its moving average.

Values below indicate percentage discounts of spot vs its moving average.