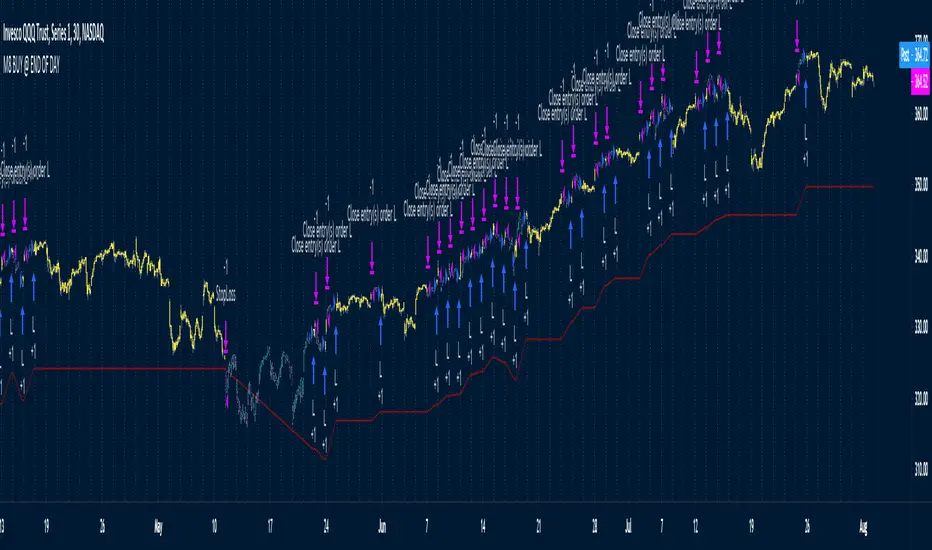

M8 BUY @ END OF DAYI've read a couple of times at a couple of different places that most of the move in the market happens after hours, meaning during non-standard trading hours.

After-market and pre-market hours and have seen data presented showing that systems which bought just before end normal market hours and sold the next morning had really amazing resutls.

But when testing those I found the results to be quite poor compared to the pretty graphs I saw, and after much tweaking and trying different ideas I gave up on the idea until I recently decided to try a new position management system.

The System

Buys at the end of the trading day before the close

Sells the next morning at the open IF THE CLOSE OF THE CURRENT BAR IS HIGHER THAN THE ENTRY PRICE

When the current price is not higher, the system will keep the position open until it EITHER gets stops out or closes on profit <<< this is WHY it has the high win %

The system has a high win ratio because it will keep that one position open until it either reaches profit or stops out

This "system" of waiting, and keeping the trade open, actually turned out to be a fantastic way to kind of put the complete trading strategy in a kind of limbo mode. It either waits for market failure or for a profit.

I don't really care about win % at all, almost always high win % ratio systems are just nonsense. What I look for is a PF -- profit factor of 1.5 or above, and a relatively smooth equity curve. -- This has both.

The Stop Loss setting is set @ .95, meaning a 5% stop loss. The Red Line on the chart is the stop loss line.

There is no set profit target -- it simply takes what the market gives.

Non-Repainting System

This does use a 200D Simple Moving Average as a filter. Like a Green Light / Red Light traffic light, the system will only trade long when the price is above its 200 Moving average.

Here is the code: "F1 = close > sma(security(syminfo.tickerid, "D", close ), MarketFilterLen) // HIGH OF OLD DATA -- SO NO REPAINTING"

I use "close ", so that's data from two days ago, it's fixed, confirmed, non-repainting data from the higher timeframe.

-- I would only suggest using this on direction tickers like SPY, QQQ, SSO, TQQQ, market sectors with additional filters in place.

ค้นหาในสคริปต์สำหรับ "ha溢价率"

Portfolio Backtester Engine█ OVERVIEW

Portfolio Backtester Engine (PBTE). This tool will allow you to backtest strategies across multiple securities at once. Allowing you to easier understand if your strategy is robust. If you are familiar with the PineCoders backtesting engine , then you will find this indicator pleasant to work with as it is an adaptation based on that work. Much of the functionality has been kept the same, or enhanced, with some minor adjustments I made on the account of creating a more subjectively intuitive tool.

█ HISTORY

The original purpose of the backtesting engine (`BTE`) was to bridge the gap between strategies and studies . Previously, strategies did not contain the ability to send alerts, but were necessary for backtesting. Studies on the other hand were necessary for sending alerts, but could not provide backtesting results . Often, traders would have to manage two separate Pine scripts to take advantage of each feature, this was less than ideal.

The `BTE` published by PineCoders offered a solution to this issue by generating backtesting results under the context of a study(). This allowed traders to backtest their strategy and simultaneously generate alerts for automated trading, thus eliminating the need for a separate strategy() script (though, even converting the engine to a strategy was made simple by the PineCoders!).

Fast forward a couple years and PineScript evolved beyond these issues and alerts were introduced into strategies. The BTE was not quite as necessary anymore, but is still extremely useful as it contains extra features and data not found under the strategy() context. Below is an excerpt of features contained by the BTE:

"""

More than `40` built-in strategies,

Customizable components,

Coupling with your own external indicator,

Simple conversion from Study to Strategy modes,

Post-Exit analysis to search for alternate trade outcomes,

Use of the Data Window to show detailed bar by bar trade information and global statistics, including some not provided by TV backtesting,

Plotting of reminders and generation of alerts on in-trade events.

"""

Before I go any further, I want to be clear that the BTE is STILL a good tool and it is STILL very useful. The Portfolio Backtesting Engine I am introducing is only a tangental advancement and not to be confused as a replacement, this tool would not have been possible without the `BTE`.

█ THE PROBLEM

Most strategies built in Pine are limited by one thing. Data. Backtesting should be a rigorous process and researchers should examine the performance of their strategy across all market regimes; that includes, bullish and bearish markets, ranging markets, low volatility and high volatility. Depending on your TV subscription The Pine Engine is limited to 5k-20k historical bars available for backtesting, which can often leave the strategy results wanting. As a general rule of thumb, strategies should be tested across a quantity of historical bars which will allow for at least 100 trades. In many cases, the lack of historical bars available for backtesting and frequency of the strategy signals produces less than 100 trades, rendering your strategy results inconclusive.

█ THE SOLUTION

In order to be confident that we have a robust strategy we must test it across all market regimes and we must have over 100 trades. To do this effectively, researchers can use the Portfolio Backtesting Engine (PBTE).

By testing a strategy across a carefully selected portfolio of securities, researchers can now gather 5k-20k historical bars per security! Currently, the PTBE allows up to 5 securities, which amounts to 25k-100k historical bars.

█ HOW TO USE

1 — Add the indicator to your chart.

• Confirm inputs. These will be the most important initial values which you can change later by clicking the gear icon ⚙ and opening up the settings of the indicator.

2 — Select a portfolio.

• You will want to spend some time carefully selecting a portfolio of securities.

• Each security should be uncorrelated.

• The entire portfolio should contain a mix of different market regimes.

You should understand that strategies generally take advantage of one particular type of market regime. (trending, ranging, low/high volatility)

For example, the default RSI strategy is typically advantageous during ranging markets, whereas a typical moving average crossover strategy is advantageous in trending markets.

If you were to use the standard RSI strategy during a trending market, you might be selling when you should be buying.

Similarily, if you use an SMA crossover during a ranging market, you will find that the MA's may produce many false signals.

Even if you build a strategy that is designed to be used only in a trending market, it is still best to select a portfolio of all market regimes

as you will be able to test how your strategy will perform when the market does something unexpected.

3 — Test a built-in strategy or add your own.

• Navigate to gear icon ⚙ (settings) of strategy.

• Choose your options.

• Select a Main Entry Strat and Alternate Entry Strat .

• If you want to add your own strategy, you will need to modify the source code and follow the built-in example.

• You will only need to generate (buy 1 / sell -1/ neutral 0) signals.

• Select a Filter , by default these are all off.

• Select an Entry Stop - This will be your stop loss placed at the trade entry.

• Select Pyamiding - This will allow you to stack positions. By default this is off.

• Select Hard Exits - You can also think of these as Take Profits.

• Let the strategy run and take note of the display tables results.

• Portfolio - Shows each security.

• The strategy runs on each asset in your portfolio.

• The initial capital is equally distributed across each security.

So if you have 5 securities and a starting capital of 100,000$ then each security will run the strategy starting with 20,000$

The total row will aggregate the results on a bar by bar basis showing the total results of your initial capital.

• Net Profit (NP) - Shows profitability.

• Number of Trades (#T) - Shows # of trades taken during backtesting period.

• Typically will want to see this number greater than 100 on the "Total" row.

• Average Trade Length (ATL) - Shows average # of days in a trade.

• Maximum Drawdown (MD ) - Max peak-to-valley equity drawdown during backtesting period.

• This number defines the minimum amount of capital required to trade the system.

• Typically, this shouldn’t be lower than 34% and we will want to allow for at least 50% beyond this number.

• Maximum Loss (ML) - Shows largest loss experienced on a per-trade basis.

• Normally, don’t want to exceed more than 1-2 % of equity.

• Maximum Drawdown Duration (MDD) - The longest duration of a drawdown in equity prior to a new equity peak.

• This number is important to help us psychologically understand how long we can expect to wait for a new peak in account equity.

• Maximum Consecutive Losses (MCL) - The max consecutive losses endured throughout the backtesting period.

• Another important metric for trader psychology, this will help you understand how many losses you should be prepared to handle.

• Profit to Maximum Drawdown (P:MD) - A ratio for the average profit to the maximum drawdown.

• The higher the ratio is, the better. Large profits and small losses contribute to a good PMD.

• This metric allows us to examine the profit with respect to risk.

• Profit Loss Ratio (P:L) - Average profit over the average loss.

• Typically this number should be higher in trend following systems.

• Mean reversion systems show lower values, but compensate with a better win %.

• Percent Winners (% W) - The percentage of winning trades.

• Trend systems will usually have lower win percentages, since statistically the market is only trending roughly 30% of the time.

• Mean reversion systems typically should have a high % W.

• Time Percentage (Time %) - The amount of time that the system has an open position.

• The more time you are in the market, the more you are exposed to market risk, not to mention you could be using that money for something else right?

• Return on Investment (ROI) - Your Net Profit over your initial investment, represented as a percentage.

• You want this number to be positive and high.

• Open Profit (OP) - If the strategy has any open positions, the floating value will be represented here.

• Trading Days (TD) - An important metric showing how many days the strategy was active.

• This is good to know and will be valuable in understanding how long you will need to run this strategy in order to achieve results.

█ FEATURES

These are additional features that extend the original `BTE` features.

- Portfolio backtesting.

- Color coded performance results.

- Circuit Breakers that will stop trading.

- Position reversals on exit. (Simulating the function of always in the market. Similar to strategy.entry functionality)

- Whipsaw Filter

- Moving Average Filter

- Minimum Change Filter

- % Gain Equity Exit

- Popular strategies, (MACD, MA cross, supertrend)

Below are features that were excluded from the original `BTE`

- 2 stage in-trade stops with kick-in rules (This was a subjective decision to remove. I found it to be complex and thwarted my use of the `BTE` for some time.)

- Simple conversion from Study to Strategy modes. (Not possible with multiple securities)

- Coupling with your own external indicator (Not really practical to use with multiple securities, but could be used if signals were generated based on some indicator which was not based on the current chart)

- Use of the Data Window to show detailed bar by bar trade information and global statistics.

- Post Exit Analysis.

- Plotting of reminders and generation of alerts on in-trade events.

- Alerts (These may be added in the future by request when I find the time.)

█ THANKS

The whole PineCoders team for all their shared knowledge and original publication of the BTE and Richard Weismann for his ideas on building robust strategies.

═════════════════════════════════════════════════════════════════════════

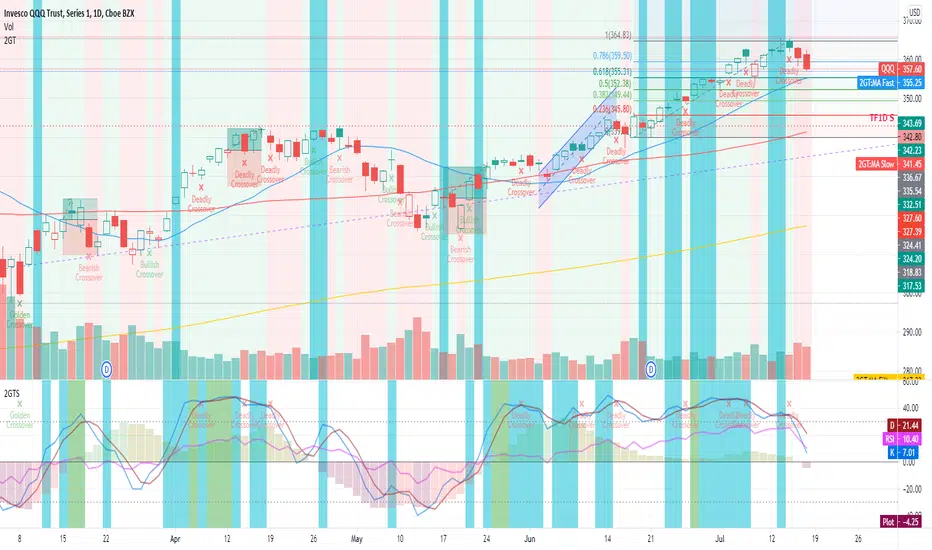

2nd Grade StrategyThis is a strategy to complement the 2GT indicator. It utilises the same rules as 2GT.

This is comprises of multiple popularly used indicators to help decide on whether to go long or short. This indicator will overlay the MA lines and background colours on your chart.

The heikin-ashi colour will be shown as the background colour. This will help you identify a trend more easily while using bars, candles, hollow candles, etc. When the background is green, it means that it is a green HA and vice versa.

The blue MA line is for showing the short-term trend. The red MA line is for showing the medium-term trend. You can select the moving average flavour of your choice in the settings.

The yellow MA line is the long-term trend that is mainly used as a filter to indicate bullish/bearish trend. The MA type for this filter can be different from the short/mid term MA.

This indicator will also show Stochastic crossovers (GC, DC, BC) on the chart. This will help to always keep your eye on the chart candles.

In the settings, you can also turn on/off bullish/bearish signals.

Rules for bullish signals on this indicator:-

1. MA: Blue > Red > Yellow (FastMA > SlowMA > FilterMA)

2. Stochastic: K > D and both are heading upwards

3. 2nd Green HA

When 2 out of the 3 rules are met, the candle background will be Aqua in colour. When all 3 rules are met, the candle background will be Green .

Rules for bearish signals on this indicator:-

1. MA: Yellow > Red > Blue (FilterMA > SlowMA > FastMA)

2. Stochastic: D > K and both are heading downwards

3. 2nd Red HA

When 2 out of the 3 rules are met, the candle background will be Orange in colour. When all 3 rules are met, the candle background will be Red .

Do note that you can hide any of these elements in via the settings.

If you find this useful, do smash the LIKE and FOLLOW button.

WSLM

2nd Grade TechniqueThis is comprises of multiple popularly used indicators to help decide on whether to go long or short. This indicator will overlay the MA lines and background colours on your chart.

The heikin-ashi colour will be shown as the background colour. This will help you identify a trend more easily while using bars, candles, hollow candles, etc. When the background is green, it means that it is a green HA and vice versa.

The blue MA line is for showing the short-term trend. The red MA line is for showing the medium-term trend. You can select the moving average flavour of your choice in the settings.

The yellow MA line is the long-term trend that is mainly used as a filter to indicate bullish/bearish trend. The MA type for this filter can be different from the short/mid term MA.

This indicator will also show Stochastic crossovers (GC, DC, BC) on the chart. This will help to always keep your eye on the chart candles.

In the settings, you can also turn on/off bullish/bearish signals.

Rules for bullish signals on this indicator:-

1. MA: Blue > Red > Yellow (FastMA > SlowMA > FilterMA)

2. Stochastic: K > D and both are heading upwards

3. 2nd Green HA

When 2 out of the 3 rules are met, the candle background will be Aqua in colour. When all 3 rules are met, the candle background will be Green .

Rules for bearish signals on this indicator:-

1. MA: Yellow > Red > Blue (FilterMA > SlowMA > FastMA)

2. Stochastic: D > K and both are heading downwards

3. 2nd Red HA

When 2 out of the 3 rules are met, the candle background will be Orange in colour. When all 3 rules are met, the candle background will be Red .

Do note that you can show/hide any of these elements via the settings.

If you find this useful, do smash the LIKE and FOLLOW button.

WSLM

Decision point boxes [LM]Hello traders,

I would like to introduce you decision point boxes study. The idea is the same as the pivots looking left and right some count of candles that has to be either up or down candle the only difference from pivots is that I'm only looking for consecutive up or down candle and in between them one candle that is oposite stance than surounding also candle has to have by default 50% or greater of wicks than body which mean market has done some decission at this candle.

Example of up candles and decision down candle:

Example of down candles a decision up candle:

Hope you will enjoy it

Support and Resistance by CainKellyeCheck out my automatic support and resistance indicator that uses the EMA of price change * relative volume as the bases of pivot search.

It also tells the strength of the support and resistance lines calculated using a 4 times quicker EMA and using its distance from the slower one.

The strongest plotted line has the maximum opacity and the weakest has the minimum opacity inside the given range.

This calculation results in an organic detection of the support and resistance prices.

You can set the distance range in percentage you want to have lines calculated around the current price.

You can set the lines gravity distance inside which they are snapped together: the stronger line pulls the weaker to it by using strength weighted average for the new price value.

You can increase the minimum opacity value in case you only see few lines (but the maximum is 15)

You can change the used price for the lines to Close or High/Low but recommended is to use the average of those two (default)

The distances multiplier helps to get a birds eye view easily when using 4H (or higher) chart and a separate one to use on Daily / Weekly / Monthly for even broader view.

Lines and labels are drawn near the candles so you are still able to zoom in.

Labels are not drawn when their line is barely visible (transparency >= 80)

This indicator has been refined on the 15 minute and 1 hour charts of BTC and other cryptos but it works well in smaller volatility markets as well if the distances are adjusted accordingly.

Single Prints - Session Initial BalancesDisclaimer: Expose yourself to the knowledge of different trading methods. If you are unaware of what a Single Print is then do some research and broaden your knowledge.

This indicator has only been tested on BTCUSDT Binance pair. This indicator is meant to be used on the 30 minute timeframe to highlight Single Prints.

The calculations are base on 0000 UTC and what Single Prints are created during that day.

Single Prints

Single Prints are where prices moves to fast through an area (on a 30 minute timeframe), in the case of this indicator in $50 intervals, where the price has not yet cross back past, represented as orange lines. If you were viewing this on a Time Price Opportunity Chart (TPO) each $50 would be represented as a square with a letter in it. If price has only been through that area once, within that 24 hour period, then it is called a Single Print. If however the Single Print is on the lower wick of the candle it is called a Buying Tail and on the Upper Wick a Selling Tail.

Single Prints leave low volume nodes with liquidity gaps, these inefficient moves tend to get filled, and we can seek trading opportunities once they get filled, or we can also enter before they get filled and use these single prints as targets.

Single Prints are a sign of emotional buying or selling as very little time was spent at those levels and thus there is no value there.

The endpoints of single print sections are considered to be potential support or resistance points and or get filled (like a CME gap).

The above is only a very short summary, to understand Single Prints, Buying Tails and Selling Tails more please do your own research (DYOR).

References:

Trading Riot Volume Profile - Website

TOROS TPO Charts Explained - Youtube

Session Boxes

Session Boxes are the high and low of that markets session before the new market session opens. I used the data from the website Trading Hours for the time input.

White box – Start of day UTC 0000 to Market Close UTC 2000

Purple box – Asia Start UTC 0130 to London Start UTC 0700

Yellow box – London Start UTC 0700 to New York Start UTC 1330

Blue box – New York Start UTC 1330 to Market Close UTC 2000

Red box – Market Close UTC 2000 to End of day UTC 2359

References:

Trading Hours - Website

Initial Balance

The Initial Balance is the market range between the high and low of the first hour of trading for the market. In the case of crypto when is the Initial Balance if it is 24/7.

Context of Initial Balance:

The Initial Balance is traditionally the range of prices transacted in the first hour of trade. Many regard the Initial Balance as a significant range because, especially for the index futures which are tied to the underlying stocks, orders entered overnight or before the open are typically executed prior to the end of the first hour of trade. Some use it to understand how the rest of the day may develop, while others use it as a span of time to avoid trading altogether because of its potential volatility.

For this indicator I have coded the Initial Balance time as below:

White Box - To appear for the first hour of the day 0000 to 0100 UTC .

Purple Box - To appear for the first hour of the day 0130 to 0230 UTC .

Yellow Box - To appear for the first hour of the day 0700 to 0800 UTC .

Blue Box - To appear for the first hour of the day 1330 to 1430 UTC .

Red Box - To appear for the first hour of the day 2000 to 2100 UTC .

The diagram above shows some examples:

How price (white arrows) retraces the single prints.

How price (red arrows) uses the single prints as S/R.

References:

Not Hard Trading – Website

My Pivots Initial Balance - Website

Thanks go to:

StackOverFlow Bjorn Mistiaen

Trading View user mvs1231

Please message me if you have any feedback/questions.

I am looking at developing this indicator further in the future.

Moving Average and PerformanceThis indicator combines several tools that are used daily for analysis:

The performance of the action we are seeing.

The percentage of retracement the stock has made from its all time high.

Possibility of using up to four exponential or simple moving averages in the length we want.

It allows to see or not the levels of four moving averages in daily temporality.

This indicator is unique since it allows you to see in real time the performance of the Stock or ETF that is being analyzed, which allows you to make a timely decision for short, medium or long-term investments.

If you are doing scalping, swing, or intraday trading, you can see the retracement it has made from the ATH (3, 5, 10 or 13%) which can become Supports or Resistances where the price can rebound, Likewise, the levels of the moving averages in 1D temporality can be observed at the same time, which are usually dynamic supports or resistances and it can also be observed in the same temporality of the chart four moving averages that the trader can configure in the length that you deem convenient to improve your analysis and make decisions as quickly as possible.

Este indicador es único ya que permite ver en tiempo real el rendimiento de la Acción o ETF que se está analizando, lo cual permite tomar una decisión oportuna para las inversiones a corto, mediano o largo plazo.

Si se está haciendo trading tipo scalping, swing, o intradía, se puede observar el retroceso que ha hecho desde el ATH (3, 5, 10 o 13%) el cual puede convertirse en Soportes o Resistencias en donde el precio puede hacer rebotes, así mismo se pueden estar observando al mismo tiempo los niveles de las medias móviles en temporalidad de 1D, los cuales usualmente son Soportes o resistencias dinámicas y también se puede observar en la misma temporalidad del gráfico cuatro medias móviles que el trader puede configurar en la longitud que crea conveniente para mejorar su análisis y tomar decisiones lo más rápido posible.

Volume Play This is going to be my first published indicator on Trading View. Thanks for TradingView for providing us this great platform And thanks for all of those who helps me to built this indicator and share there ideas.I cannot mention everyone name here believe me that list going to be huge.Everyone’s idea and help is much appreciated.This is how our TradingView community is growing day by day with kindness and knowledge. Every time I take so much from community in form knowledge that every time somewhere I feel that I also need to do something for community and finally day arrived .A gift from my side to community.A gift of indicator-VOLUME PLAY

This volume based indicator has High Relative Volume bar Background, Low Relative Volume bar background ,Volume Labels of Buying volume, Selling volume and Total volume count with percentage, Highest Volume in Percentage and Highest 5x volume count and 10x volume count of bar.Plus I have did column scaling to take Down pan input so you can switch pane or add in existing pane without any major problem And all this works on any time frame. Isn’t it good idea?

This indicator displays the volume of each session in a similar manner of the default volume indicator.However it add on the last bar Green and Red bar colours. Green means buying is more than selling and Red means selling is more than buying.On top of Some bar If number appears That means that’s volume is highest multiple volume of 5 and if number appears with label means highest multiple volume of 10.So simple without label volume counts means 5x and with label means 10x.

Now some of bars has background colour of Mint green , Pastel red and White.That’s highlight high relative volume bars with a highly buying activity range in Green and high relative volume bars with a highly selling activity range in Red And white background is low relative volume for that timeframe bar.

I am kind of person who don’t keep show indicator value enable all time.So it’s come in mind why not plot this values without enabling it.So I decided to show this values of buying, selling and total volumes on top near middle pane.Interesting thing is that I made a label with the help of pine script Table feature.Thanks a lot to Pine Team to add this new great feature! It’s great alternative for labels feature.Because of this feature I am able to locate buying, selling and total volume at right place where in most of scenario it will adjust.

Please note that all values are estimate.It’s not accurate.I show volumes in K,M form.Plus with volume I also try to show Buying And Selling volume in percentage form to get rough idea about what’s going on in instrument.Idea is to get better view of volume by splitting it into Buying , Selling and Total volume.This allows you to see are the bulls or bears in-control in relation to the overall Volume.

By default this indicator overlay is false but you can move this indicator pane to existing upper or lower pane.It will help to save space as well.If combine with two indicator at same pane then it will create two value scale at right side.So you will not loose any indicators values.By default I used 50% of vertical space in indicator scale factor.

I tried to make this indicator as accurate as inbuilt volume indicator with added extra feature.The main aim of indicator to get Idea of volume role in that symbol with that specific timeframe.Result might not be accurate but I expect somewhat nearby to accurate.

Kept source code open purposely for learners of pine script. Please avoid misuse or selling of this indicator.Remember Sharing Is Caring. If someone has suggestions or any addition then please comment below.Wishing you all abundance of health, wealth, and prosperity.

After all its all about VOLUME PLAY.

Disclaimer:-This indicator is not meant for buy or sell signals.This post and the script don’t provide any financial advice. This indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

[francrypto® strategy] 4 EMAs, P.SAR & Vol.Prof. (by kv4coins)(ENG)

This script consists of my own strategy for cryptocurrency (but can be adapted very well for stocks, forex, etc.)

Is a combination of:

- Four Exponentials Moving Average (EMA), configurables: by defect are 10, 21, 55 and 200 periods in yellow, aqua, orange and blue each of them

- Parabolic SAR System (PSAR), configurable

- Volume Profile (that has been developed by kv4coins - he has already authorized me to use it under the same OSS Licence Terms: MPL 2.0), configurable: with another default values and bilingual support for Spanish (SPA)

How it works

1) It is always better to detect specifics candlesticks or patrons: doji , pinbar or inverted pinbar , engulfing bars , morning star or evening star , harami , twizzer bottom or top , etc.

2) The 10 and 21 periods EMA help to identify the short-term behavior

3) The 55 periods EMA can be used like a support or resistance in medium-term, as 200 periods EMA in very long-term

4) It will convenient search for a double cross (10 & 21) or a triple cross (10, 21 & 55) to determine the medium-term change Downtrend to UpTrend (or viceversa)

5) Confirm the change patron with the Parabolic SAR and then identify potencials purchases or sales

6) Use Volume profile to detect potential supports or resistances areas, in order to set stop limit/loss and take profit orders.

Hope this helps!

Cheers,

FRANCRYPTO®

–––––– 0 ––––––

(ESP)

Este script consiste en mi propia estrategia para criptomonedas (pero puede adaptarse muy bien para acciones, forex, etc.)

Es la combinación de:

1) Cuatro Medias Móviles Exponenciales (EMA), configurables: por defecto son de 10, 21, 55 y 200 períodos en amarillo, turquesa, naranja y azul cada una de ellas

2) Sistema Parabolic SAR (PSAR), configurable

3) Perfil de Volumen (que fuera desarrollado por kv4coins - que ya me ha autorizado a su uso bajo las mismas condiciones de la Licencia OSS: MPL 2.0), configurable: con otros valores por defecto y soporte bilingüe para Español (SPA)

Cómo funciona

1) Siempre va a resultar mejor detectar velas japonesas específicas o patrones: doji , martillos o martillos invertidos , velas envolventes , patrón amanecer o atardecer , harami , velas gemelas , etcétera

2) La EMA de 10 y 21 períodos ayudan a identificar el comportamiento de corto plazo

3) La EMA de 55 períodos puede ser usada como un soporte o resistencia de mediano plazo, como así también, la EMA de 200 períodos en el muy largo plazo

4) Será conveniente buscar un doble cruce (10 & 21) o un triple cruce (10, 21 & 55) para determinar un cambio de la tendencia de mediano plazo de bajista hacia alcista (o viceversa)

5) Confirmá el patrón de cambio con la Parabólica de SAR y entonces identificá potenciales compras o ventas

6) Usá el perfil de volumen para detectar las potenciales zonas de soporte o resistencia, principalmente para establecer ordenes stop limit/loss o take profit.

¡Espero que pueda serles de utilidad!

Saludos,

FRANCRYPTO®

MA DerivativesMA Derivatives basicly using Ichimoku Cloud and some additional moving averages for traders.

A. ICHIMOKU

Tenkan-sen (Conversion Line): (9-period high + 9-period low)/2

On a daily chart , this line is the midpoint of the 9-day high-low range, which is almost two weeks.

Kijun-sen (Base Line): (26-period high + 26-period low)/2

On a daily chart , this line is the midpoint of the 26-day high-low range, which is almost one month.

Senkou Span A (Leading Span A): (Conversion Line + Base Line)/2

This is the midpoint between the Conversion Line and the Base Line. The Leading Span A forms one of the two Cloud boundaries. It is referred to as “Leading” because it is plotted 26 periods in the future and forms the faster Cloud boundary.

Senkou Span B (Leading Span B): (52-period high + 52-period low)/2

On the daily chart , this line is the midpoint of the 52-day high-low range, which is a little less than 3 months. The default calculation setting is 52 periods, but it can be adjusted. This value is plotted 26 periods in the future and forms the slower Cloud boundary.

Chikou Span: Represents the closing price and is plotted 26 days back.

Kumo Cloud: Kumo cloud between Senkuo Span A and Senkou Span B lines. It can be green or red. Color can be change with the trend.

You can use Ichimoku for buy&sell strategy

For Buying Strategy

- Tenkansen (Conversion Line) should crossover Kijunsen (Base line) above the highest line of cloud

- Price should be above the highest line of cloud

- Chikouspan should be above the cloud

For Selling Strategy

- Kijunsen (Base Line) should crossover Tenkansen (Conversion Line) below the lowest line of cloud

- Price should be below the lowest line of cloud

- Chikouspan should be below the cloud

B. SIMPLE MOVING AVERAGES

The indicator has some of Simple Moving Averages

It includes:

-Simple Moving Average 50

-Simple Moving Average 100

-Simple Moving Average 200

C. EXPONENTIAL MOVING AVERAGES

The indicator has some of Simple Moving Averages

It includes:

-Exponential Moving Average 9

-Exponential Moving Average 21

-Exponential Moving Average 50

D. BOLLINGER BAND

Bollinger Bands are a type of price envelope developed by John BollingerOpens in a new window. (Price envelopes define upper and lower price range levels.) Bollinger Bands are envelopes plotted at a standard deviation level above and below a simple moving average of the price. Because the distance of the bands is based on standard deviation, they adjust to volatility swings in the underlying price.

Bollinger Bands use 2 parameters, Period and Standard Deviations, StdDev. The default values are 20 for period, and 2 for standard deviations, although you may customize the combinations.

Bollinger bands help determine whether prices are high or low on a relative basis. They are used in pairs, both upper and lower bands and in conjunction with a moving average. Further, the pair of bands is not intended to be used on its own. Use the pair to confirm signals given with other indicators.

How this indicator works

When the bands tighten during a period of low volatility, it raises the likelihood of a sharp price move in either direction. This may begin a trending move. Watch out for a false move in opposite direction which reverses before the proper trend begins.

When the bands separate by an unusual large amount, volatility increases and any existing trend may be ending.

Prices have a tendency to bounce within the bands' envelope, touching one band then moving to the other band. You can use these swings to help identify potential profit targets. For example, if a price bounces off the lower band and then crosses above the moving average, the upper band then becomes the profit target.

Price can exceed or hug a band envelope for prolonged periods during strong trends. On divergence with a momentum oscillator, you may want to do additional research to determine if taking additional profits is appropriate for you.

A strong trend continuation can be expected when the price moves out of the bands. However, if prices move immediately back inside the band, then the suggested strength is negated.

Calculation

First, calculate a simple moving average. Next, calculate the standard deviation over the same number of periods as the simple moving average. For the upper band, add the standard deviation to the moving average. For the lower band, subtract the standard deviation from the moving average.

Typical values used:

Short term: 10 day moving average, bands at 1.5 standard deviations. (1.5 times the standard dev. +/- the SMA)

Medium term: 20 day moving average, bands at 2 standard deviations.

Long term: 50 day moving average, bands at 2.5 standard deviations.

E. ADJUSTABLE MOVING AVERAGES

And this script has also 2 adjustable moving average

- 1 Adjustable Simple Moving Average

- 1 Adjustable Exponential Moving Average

You can just change the length for using this tool.

MashumeHullTV█ OVERVIEW

This plots the Hull Moving Average Turning Points and Concavity

with the addition of colored segments representing concavity and turning points: maxima, minima and inflection.

a fast way to determine the trend direction and possible reversals based on concavity of the trend

Dark Green: Concave Up but HMA decreasing. The 'mood' has changed and the declining trend of the HMA is slowing. Possible trend change to Uptrend soon

Light Green: Concave up and HMA increasing. Price is increasing, and since the curve is still concave up, it is accelerating upward. Uptrend

Orange: Concavity is now downward, and though price is still increasing, the rate has slowed, perhaps the mood has become less enthusiastic. Possible trend change to Downtrend soon

Red: Concave down and HMA decreasing. Downtrend

Buy signals generated when Hull turns from Dark Green -> Light Green

Sell signals generated when Hull turns from Orange -> Red

To best determine if this is a entry point or a trend reversal, it is recommended to use in conjunction with the QQEMoMoTV indicator

█ FEATURES

Calculations

Calculates the concavity of the Hull Moving Average comparing the Hull concavity of the current bar to the previous bar and displays the concavity in the form of 4 different colors.

Note: may cause repainting, so recommended to use with another indicator such as the QQEMoMoTV indicator to confirm signals.

Calculates divergence between the calculated HMA and the actual price and displays this in the Divergence Label.

Calculates the local minima, maxima and inflection points with the ability to display these as auto support/resistance lines.

Inputs

You can use the script's inputs to configure:

• Calculation Source (default HL2)

• HMA Length (default 21)

• Lookback (default 2)

• Whether to show Auto Support/Resist Lines

• Whether to show Buy/Sell Arrows

• Whether to show Divergence Label

• Whether to extend Local Auto Support/Resist Lines

Alerts

Buy Signal alert based on HMA crossing above MA_Min/Hull Support, when Hull turns from Dark Green -> Light Green, Bullish

Sell Signal alert based on HMA crossing below MA_Max/Hull Resistance, when Hull turns from Orange -> Red, Bearish

Experimental support for applying the indicator to higher time frames

eg. charting the hourly MashumeHull indicator on 15 min chart. See the commented code to access this feature

█ CREDITS

Original Author: Seth Urion (Mashume)

Feature upgrades and usage: Xiuying

Converted to Tradingview by: Machdragon

Digital Nivesh Out of Range Trade IndicatorThis indicator is for intraday with the basic logic that any script will always trade in its range.

So , if any script moves away from its range, it will try to come back to its normal range movement.

Suppose average movement of any share is 100 points, and share has moved more than 150 points there is high probability that it will move in opposite direction in order to have average movement of price of 100.

For Stocks please use average period as 15 days for index 30 days.

If share price(YELLOW LINE) moves away from higher or lower blue line, then with the help of volume confirmation a trade can be initiated in opposite direction.

Please note direction needs to be opposite of what has happened in the day.

for eg. upper blue line could be broken , in both situation i.e.. share price is rising or falling,

so if share price is rising and upper blue line is broken:

Bearsish trade can be initiated with the help of price action n volume.

if share price has falledn and upper blue is broken:

Bullish trade can be initiated with the help of volume n price action confirmation.

Baus BandsThe Baus Bands are a simplified version of another one of my trend following indicators, the Neapolitan Bands. This version only shows the trend trading zones in green and red. An additional 21 EMA with an ATR band was added as part of my own trend trading rules using these bands.

How do I read this indicator?

Is the blue band between and not touching the green or red clouds? The condition is ranging.

Is the blue band touching the green cloud? The condition is a bullish trend.

Is the blue band touching the red cloud? The condition is a bearish trend.

The trend trading rules are exactly the same as the default Neapolitans, but include an extra condition.

A trend has started once 2 conditions are met:

Price has entered either trending cloud.

The 21 EMA ATR band in blue is within the same cloud.

With those conditions met, if you expect the trend to continue, trade pull-backs to the blue band in the direction of the trending cloud.

Isn't this just a 21 EMA trading pull-backs strategy?

No. The 21 EMA alone is not sufficient in my opinion to define a range or trend technically. Always buying the 21 EMA pull-back, especially in a range, is not a great strategy by itself unless you've already identified price as trending. Baus Bands adds that trend identification.

Why make this?

Baus Bands show the conditions I personally use for catching trends and identifying ranges with these indicators, and shows only the information I use.

What's the purpose of the ATR band around the 21 EMA?

Sometimes price will open and close below the 21 EMA and cause some technical analysts will say the trend is over. I added the ATR specifically to get a volatility based, upper and lower bound range around the 21 EMA. that way I have an acceptable price range where price could move past the 21 EMA and still keep a trend valid using similar rules. I then saw that so long this ATR band (not the 21 EMA itself) was touching those trending clouds, then the trend has a good chance of continuing as long as that was true.

72s Strat: Backtesting Adaptive HMA+ pt.1This is a follow up to my previous publication of Adaptive HMA+ few months ago, as a mean to provide some kind of initial backtesting tools. Which can be use to explore many possible strategies, optimise its settings to better conform user's pair/tf, and hopefully able to help tweaking your general strategy.

If you haven't read the study or use the indicator, kindly go here first to get the overall idea.

The first strategy introduce in this backtest is one most basic already described in the study; buy/sell is when movement is there and everything is on the right side; When RSI has turned to other side, we can use it as exit point (if in profit of course, else just let it hit our TP/SL, why would we exit before profit). Also, base on RSI when we make entry, we can further differentiate type of signals. --Please check all comments in code directly where the signals , entries , and exits section are.

Second additional strategy to check; is when we also use second faster Adaptive HMA+ for exit. So this is like a double orders on a signal but with different exit-rule (/more on this on snapshots below). Alternatively, you can also work the code so to only use this type of exit.

There's also an additional feature which you can enable its visuals, the Distance Zone , is to help measuring price distance to our xHMA+. It's just a simple atr based envelope really, I already put the sample code in study's comment section, but better gonna update it there directly for non-coder too, after this.

In this sample I use Lot for order quantity size just because that's what I use on my broker. Also what few friends use while we forward-testing it since the study is published, so we also checked/compared each profit/loss report by real number. To use default or other unit of measurement, change the entry code accordingly.

If you change your order size, you should also change the commission in Properties Tab. My broker commission is 5 USD per order/lot, so in there with example order size 0.1 lot I put commission 0.5$ per order (I'll put 2.5$ for 0.5 lot, 10$ for 2 lot, and so on). Crypto usually has higher charge. --It is important that you should fill it base on your broker.

SETTINGS

I'm trying to keep it short. Please explore it further again. (Beginner should also first get acquaintance with terms use here.)

ORDERS:

Base Minimum Profit Before Exit:

The number is multiplier of ongoing ATR. Means that when basic exit condition is met, algo will check whether you're already in minimum profit or not, if not, let it still run to TP or SL, or until it meets subsequent exit condition, then it will check again.

Default Target Profit:

Multiplier of ATR at signal. If reached before any eligible exit condition is met, exit TP.

Base StopLoss Point:

You can change directly in code to use other like ATR Trailing SL, fix percent SL, or whatever. In the sample, 4 options provided.

Maximum StopLoss:

This is like a safety-net, that if at some point your chosen SL point from input above happens to be exceeding this maximum input that you can tolerate, then this max point is the one will be use as SL.

Activate 2nd order...:

The additional doubling of certain buy/sell with different exits as described above. If enable, you should also set pyramiding to at least: 2. If not, it does nothing.

ADAPTIVE HMA+ PERIOD

Many users already have their own settings for these. So in here I only sample the default as first presented in the study. Make it to your adaptive.

MARKET MOVEMENT

(1) Now you can check in realtime how much slope degree is best to define your specific pair/tf is out of congestion (yellow) area. And (2) also able to check directly what ATR lengths are more suitable defining your pair's volatility.

DISTANCE ZONE

Distance Multiplier. Each pair/tf has its own best distance zone (in xHMA+ perspective). The zone also determine whether a signal should appear or not. (Or what type of signal, if you wanna go more detail in constructing your strategy)

USAGE

(Provided you already have your own comfortable settings for minimum-maximum period of Adaptive HMA+. Best if you already have backtested it manually too and/or apply as an add-on to your working strategy)

1. In our experiences, first most important to define is both elements in the Market Movement Settings . These also tend to be persistent for whole season since it's kinda describing that pair/tf overall behaviour. Don't worry if you still get a low Profit Factor here, but by tweaking you should start to see positive changes in one of Max Drawdown and Net Profit, or Percent Profitable.

2. Afterwards, find your pair/tf Distance Zone . When optimising this, what we seek is just a "not to bad" equity curves to start forming. At least Max Drawdown should lessen more. Doesn't have to be great already, but should be better, no red in Net Profit.

3. Then go manage the "Trailing Minimum Profit", TP, SL, and max SL.

4. Repeat 1,2,3. 👻

5. Manage order size, commission, and/or enable double-order (need pyramiding) if you like. Check if your equity can handle max drawdown before margin call.

6. After getting an acceptable backtest result, go to List of Trades tab and find the biggest loss or when many sequencing loss in a row happened. Click on it to go to exact point on chart, observe why the signal failed and get at least general idea how it can be prevented . The rest is yours, you should know your pair/tf more than other.

You can also re-explore your minimum-maximum period for both Major and minor xHMA+.

Keep in mind that all numbers in Setting are conceptually in a form of range . You don't want to get superb equity curves but actually a "fragile" , means one can easily turn it to disaster just by changing only a fraction in one/two of the setting.

---

If you just wanna test the strength of the indicator alone, you can disable "Use StopLoss" temporarily while optimising settings.

Using no SL might be tempting in overall result data in some cases, but NOTE: It is not recommended to not using SL, don't forget that we deliberately enter when it's in high volatility. If want to add flexibility or trading for long-term, just maximise your SL. ie.: chose SL Point>ATR only and set it maximum. (Check your max drawdown after this).

I think this is quite important specially for beginners, so here's an example; Hypothetically in below scenario, because of some settings, the buy order after the loss sell signal didn't appear. Let's say if our initial capital only 1000$ using leverage and order size 0,5 lot (risky position sizing already), moreover if this happens at the beginning of your trading season, that's half of account gone already in one trade . Your max SL should've made you exit after that pumping bar.

The Trailing Minimum Profit is actually look like this. Search in the code if you want to plot it. I just don't like too many lines on chart.

To maximise profit we can try enabling double-order. The only added rule coded is: RSI should rising when buy and falling when sell. 2nd signal will appears above or below default buy/sell signal. (Of course it's also prone to double-loss, re-check your max drawdown after. Profit factor play its part in here for a long run). Snapshot in comparison:

Two default sell signals on left closed at RSI exit, the additional sell signal closed later on when price crossover minor xHMA+. On buy side, price haven't met our minimum profit when first crossunder minor xHMA+. If later on we hit SL on this "+buy" signal, at least we already profited from default buy signal. You can also consider/treat this as multiple TP points.

For longer-term trading, what you need to maximise is the Minimum Profit , so it won't exit whenever an exit condition happened, it can happen several times before reaching minimum profit. Hopefully this snapshot can explain:

Notice in comparison default sell and buy signal now close in average after 3 days. What's best is when we also have confirmation from higher TF. It's like targeting higher TF by entering from smaller TF.

As also mention in the study, we can still experiment via original HMA by putting same value for minimum-maximum period setting. This is experimental EU 1H with Major xHMA+: 144-144, Flat market 13, Distance multiplier 3.6, with 2nd order activated.

Kiwi was a bit surprising for me. It's flat market is effectively below 6, with quite far distance zone of 3.5. Probably because I'm using big numbers in adaptive period.

---

The result you see in strategy tester report below for EURUSD 15m is using just default settings you see in code, as follow:

0,1 lot for each order (which is the smallest allowed by my broker).

No pyramiding. Commission: 0.5 usd per order. Slippage: 3

Opening position is only using basic strategy #1 (RSI exit). Additional exit not activated.

Minimum Profit: 1. TP: 3.

SL use: Half-distance zone. Max SL: 4.5.

Major xHMA+: 172-233. minor xHMA+: 89-121

Distance Zone Multiplier: 2.7

RSI: Standard 14.

(From our forward-testing, the difference we get from net profit is because of the spread, our entry isn't exactly at the close/open price. Not so much though, but not the same. If somebody can direct me to any example where we can code our entry via current bid/ask price, that would be awesome!)

It's already a long post (sorry), think I'm gonna pause here. Check out the code :)

---

DISCLAIMER: Past performance is no guarantee of future results , and so on.. you know the drill ;)

Please read whole description first before using, don't take 1-2 paragraph and claim it's the whole logic, you are responsible of your own actions and understanding.

Crypto Bands with ToolsThis indicator has 3 bands

1. Upper Band

2. Middle Band

3. Lower Band

1. Upper Band

Average of Moving Average of the Close (add Standard Deviations) and Highest price reached in the prior period

2. Middle Band

Average of upper and middle bands. And middle band also has BUY-SELL function. If middle band is blue you can BUY and if the middle band colored red you can SELL

3. Lower Band

Average of Moving Average of the Close(subtract Standard Deviations) and Lowest price reached in the prior period

Upper and Lower bands can be used for BUY&SELL strategy.

You can buy when price touches the lower band

You can sell when price touches the upper band

Indicator can work with long and short positions aswell

As you can see when price touches the lower band you can be LONG

and when the price touches the upper band you can be SHORT

When stock prices continually touch the upper DMR Band, the prices are thought to be overbought; conversely, when they continually touch the lower band, prices are thought to be oversold, triggering a buy signal. When using DMR Bands, designate the upper and lower bands as price targets.

indicator has ichimoku and some moving averages for checking the support and resistances.

Alpha & BetaHow to use Alpha(α)?

If Alpha is positive the stock outperforms, if the value is negative means the stock underperforms.

α < 0: The investment has earned too little for its risk (or, was too risky for the return)

α = 0: The investment has earned a return adequate for the risk taken

α > 0: The investment has a return in excess of the reward for the assumed risk

How to use Beta(β)?

β = 1: Exactly as volatile as the index

β > 1: More volatile than the index

β < 1 > 0: Less volatile than the index

β = 0: Uncorrelated to the index

β < 0: Negatively correlated to the index

β > 2: Trending stock

Higher the β higher risk/reward

Example: If the beta is 1.1, the share price is like to move by 10% more than the index

Trading Tip

Choose a stock with Alpha greater than 0 and Beta greater than 1.9 for intraday in 5min timeframe for long positions

Remember that such stocks will have high risk and high reward

Shortlist stocks with Beta greater than 1.9 for next day in 5min timeframe

Directional Movement Index and ADXDMI (ADX) consists of three indicators that measure a trend’s strength and direction. Three lines compose the Direction Movement Index (DMI): ADX (white/gray line), DI+ (green line), and DI- (orange line). The Average Directional Index (ADX) line shows the strength of the trend. The higher the ADX value, the stronger the trend. The ADX line is white when it has a positive slope, otherwise it is gray.

The Plus Direction Indicator (DI+) and Minus Direction Indicator (DI-) show the current price direction. When the DI+ is above DI-, the current price momentum is up. When the DI- is above DI+, the current price momentum is down.

Trend detection: When the background has a bluish color there is an upward trend, and when the background has a reddish color there is a downward trend.

Includes an information panel that shows the current value and trend of some well-known indicators.

Zweig Market Breadth Thrust Indicator StrategyThe Breadth Thrust Indicator is a technical indicator which determines market momentum, signaling the start of a potential new bull market.

The Breadth Thrust Indicator was developed by Martin Zweig, an American stock investor, financial analyst, and investment adviser. According to Zweig, the concept is based on the principle that the sudden change of money in the investment markets elevates stocks and signals increased liquidity. In other words, this indicator is all about how quickly the NYSE's advancing and declining numbers go from poor to great in a compressed time period.

A "Thrust" indicates that the stock market has rapidly changed from an oversold condition to one of strength, but has not yet become overbought. This is very rare and has happened only a few times. Dr . Zweig also points out that most bull markets begin with a Breadth Thrust.

More info can be found at www.investopedia.com

I have inspired by indicator introduced in TradingView by LazyBear and adopted the logic from there. Thanks LazyBear !!!

Though indicator signals the new Bull market, but I have not found much information how to use it in daily market. So I had come up with a strategy, which would allow us to trade SPY, QQQ , AMEX and securities under these markets.

I have used MA setting as 65 (since Zweig indicator setting was 10 days , based on that I set 65 for Hourly chart ... 10d x 6.5 Hrs = 65 in my startegy). You have to change this setting if you change the timeframe. Also , note that this strategy is for Stock Market only.

Strategy Rule/Settings

===================

Select the market type based on your security symbol.

SPY => use NYSE

QQQ => use NASDAQ

any other security => check exchange it was listed and select the corresponding market.

if you dont know , use COMBINED option

BUY

====

when indicator cross 0.40 from below

Note:

1. see how well it picks the bottoms ... example : Nov 2020 ....

2. setting 0.45 is also produces good results , only thing is you get more signals.

EXIT

=====

Exit when indicator cross down from 0.60 . I have used RSI (5) for partial exits. These two are available in settings

Close the whole position when indicator crossing down 0.40

STOP LOSS

=========

defaulted to 5%

Please Note , I have tested SPY , QQQ on Horly chart with MA 65. You need to chnage the MA setting based on your time frame and check the results.

WARNING

========

For the use of educational purposes only

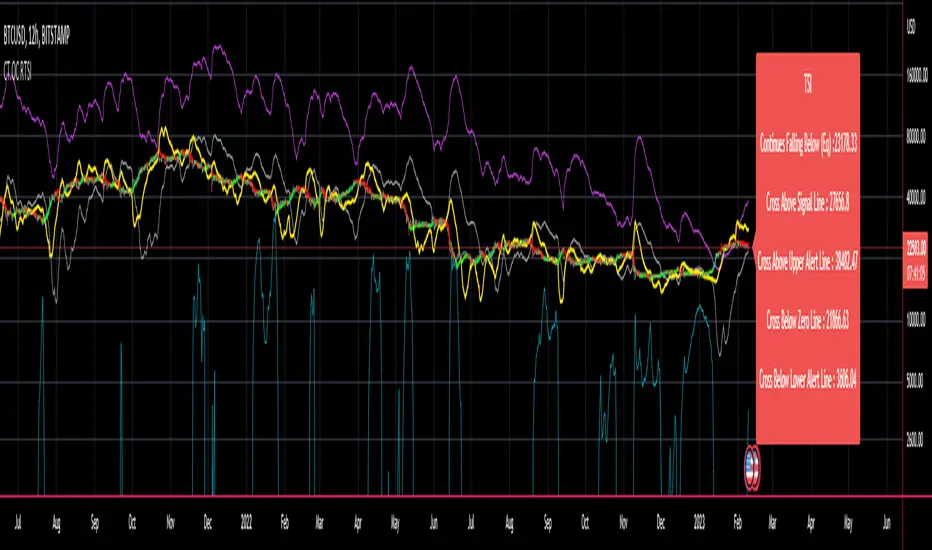

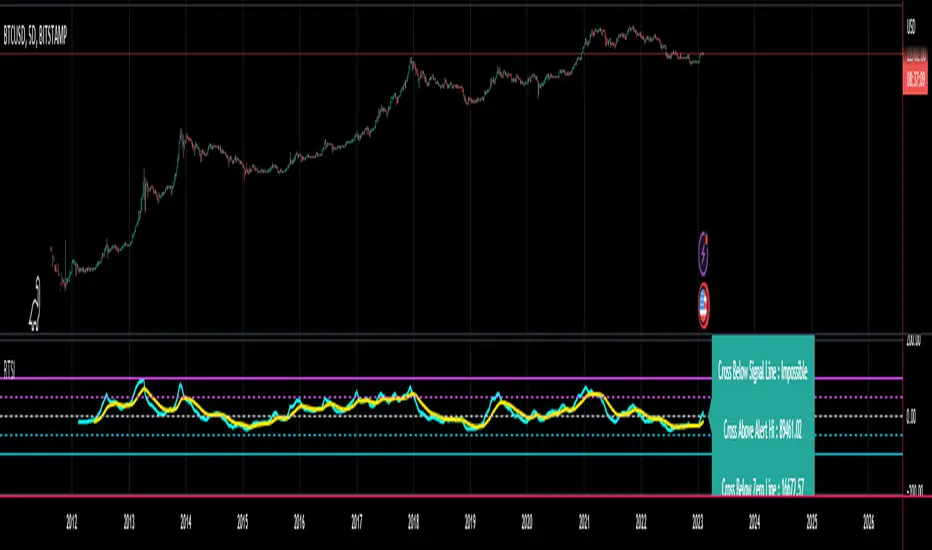

CT Reverse True Strength Indicator On ChartIntroducing the Caretakers “On Chart” Reverse True Strength Index.

According to Wikipedia….

“The True Strength Index (TSI) is a technical indicator used in the analysis of financial markets that attempts to show both trend direction and overbought/oversold conditions. It was first published William Blau in 1991.

The indicator uses moving averages of the underlying momentum of a financial instrument.

Momentum is considered a leading indicator of price movements, and a moving average characteristically lags behind price.

The TSI combines these characteristics to create an indication of price and direction more in sync with market turns than either momentum or moving average.”

The TSI has a normal range of values between +100 and -100.

Traditionally traders and analysts will consider:

Positives values above 25 to indicate an “overbought” condition

Negative values below -25 to indicate an “oversold” condition

I have reverse engineered the True Strength Index formula to derive 2 new functions.

1) The reverse TSI function is dual purpose which can be used to calculate….

The chart price at which the TSI will reach a particular TSI scale value.

The chart price at which the TSI will equal its previous value.

2) The reverse TSI signal cross function can be used to calculate the chart price at which the TSI will cross its signal line.

I have employed these functions here to return the price levels where the True Strength Index would equal :

Upper alert level ( default 25 )

Zero-Line

Lower alert level ( default -25 )

Previous TSI (eq) value

TSI signal line

In this “On Chart” version of the reverse True Strength Index the crossover levels are displayed both as lines on the chart and via an optional info-box with choice of user selected info.

Chart Line Colors

Upper alert level... ( Fuchsia )

Zero-Line............ ( White )

Lower alert level... ( Aqua )

TSI (eq)...............( TSI (eq) > close..Orange, TSI (eq) < close..Lime )

TSI signal line........( Signal Cross Line > Close..Aqua, Signal Cross Line < Close..Fuchsia )

How to interpret the displayed prices returned from the TSI scale zero line and upper and lower alert levels.

Closing exactly at the given price will cause the True Strength Index value to equal the scale value.

Closing above the given price will cause the True Strength Index to cross above the scale value.

Closing below the given price will cause the True Strength Index to cross below the scale value.

How to interpret the displayed price returned from the TSI (eq)

Closing exactly at the price will cause the True Strength Index value to equal the previous TSI value.

Closing above the price will cause the True Strength Index value to increase.

Closing below the price will cause the True Strength Index value to decrease.

How to interpret the displayed price returned from the TSI signal line crossover.

Closing exactly at the given price will cause the True Strength Index value to equal the signal line.

Closing above the given price will cause the True Strength Index to cross above the signal line.

Closing below the given price will cause the True Strength Index to cross below the signal line.

Common methods to derive signals from the TSI :

Zero-line crossovers

When the CMO crosses above the zero-line, a buy signal is generated.

When the CMO crosses below the zero-line, a sell signal is generated.

“Overbought” and “Oversold” crossovers

When the SMI crosses below -25 and then moves back above it, a buy signal is generated.

When the SMI crosses above +25 and then moves back below it, a sell signal is generated.

What Does the True Strength Index (TSI) Tell You?

The indicator is primarily used to identify overbought and oversold conditions in an asset's price, spot divergence, identify trend direction and changes via the zero-line, and highlight short-term price momentum with signal line crossovers.

Since the TSI is based on price movements, oversold and overbought levels will vary by the asset being traded. Some stocks may reach +30 and -30 before tending to see price reversals, while another stock may reverse near +20 and -20.

Mark extreme TSI levels, on the asset being traded, to see where overbought and oversold is. Being oversold doesn't necessarily mean it is time to buy, and when an asset is overbought it doesn't necessarily mean it is time to sell. Traders will typically watch for other signals to trigger a trade decision. For example, they may wait for the price or TSI to start dropping before selling in overbought territory. Alternatively, they may wait for a signal line crossover.

Signal Line Crossovers

The true strength index has a signal line, which is usually a seven- to 13-period EMA of the TSI line. A signal line crossover occurs when the TSI line crosses the signal line. When the TSI crosses above the signal line from below, that may warrant a long position. When the TSI crosses below the signal line from above, that may warrant selling or short selling.

Signal line crossovers occur frequently, so should be utilized only in conjunction with other signals from the TSI. For example, buy signals may be favoured when the TSI is above the zero-line. Or sell signals may be favoured when the TSI is in overbought territory.

Zero-line Crossovers

The zero-line crossover is another signal the TSI generates. Price momentum is positive when the indicator is above zero and negative when it is below zero. Some traders use the zero-line for a directional bias. For example, a trader may decide only to enter a long position if the indicator is above its zero-line. Conversely, the trader would be bearish and only consider short positions if the indicator's value is below zero.

Breakouts and Divergence

Traders can use support and resistance levels created by the true strength index to identify breakouts and price momentum shifts. For instance, if the indicator breaks below a trendline, the price may see continued selling.

Divergence is another tool the TSI provides. If the price of an asset is moving higher, while the TSI is dropping, that is called bearish divergence and could result in a downside price move. If the TSI is rising while the price is falling, that could signal higher prices to come. This is called bullish divergence.

Divergence is a poor timing signal, so it should only be used in conjunction with other signals generated by the TSI or other technical indicators.

The Difference Between the True Strength Index (TSI) and the Moving Average Convergence Divergence (MACD) Indicator.

The TSI is smoothing price changes to create a technical oscillator. The moving average convergence divergence (MACD) indicator is measuring the separation between two moving averages. Both indicators are used in similar ways for trading purposes, yet they are not calculated the same and will provide different signals at different times.

The Limitations of Using the True Strength Index (TSI)

Many of the signals provided by the TSI will be false signals. That means the price action will be different than expected following a trade signal. For example, during an uptrend, the TSI may cross below the zero-line several times, but then the price proceeds higher even though the TSI indicates momentum has shifted down.

Signal line crossovers also occur so frequently that they may not provide a lot of trading benefit. Such signals need to be heavily filtered based on other elements of the indicator or through other forms of analysis. The TSI will also sometimes change direction without price changing direction, resulting in trade signals that look good on the TSI but continue to lose money based on price.

Divergence also tends to unreliable on the indicator. Divergence can last so long that it provides little insight into when a reversal will actually occur. Also, divergence isn't always present when price reversals actually do occur.

The TSI should only be used in conjunction with other forms of analysis, such as price action analysis and other technical indicators.

This is not financial advice, use at your own risk.

CT Reverse True Strength IndicatorIntroducing the Caretakers Reverse True Strength Index.

According to Wikipedia….

“The True Strength Index (TSI) is a technical indicator used in the analysis of financial markets that attempts to show both trend direction and overbought/oversold conditions. It was first published William Blau in 1991.

The indicator uses moving averages of the underlying momentum of a financial instrument.

Momentum is considered a leading indicator of price movements, and a moving average characteristically lags behind price.

The TSI combines these characteristics to create an indication of price and direction more in sync with market turns than either momentum or moving average.”

The TSI has a normal range of values between +100 and -100.

Traditionally traders and analysts will consider:

Positives values above 25 to indicate an “overbought” condition

Negative values below -25 to indicate an “oversold” condition

I have reverse engineered the True Strength Index formula to derive 2 new functions.

The reverse TSI function is dual purpose which can be used to calculate….

The chart price at which the TSI will reach a particular TSI scale value.

The chart price at which the TSI will equal its previous value.

The reverse TSI signal cross function can be used to calculate the chart price at which the TSI will cross its signal line.

I have employed these functions here to return the price levels where the True Strength Index would equal :

Upper alert level ( default 25 )

Zero-Line

Lower alert level ( default -25 )

Previous TSI (eq) value.

TSI signal line

These crossover levels are displayed via an optional info-box with choice of user selected info.

How to interpret the displayed prices returned from the TSI scale zero line and upper and lower alert levels.

Closing exactly at the given price will cause the True Strength Index value to equal the scale value.

Closing above the given price will cause the True Strength Index to cross above the scale value.

Closing below the given price will cause the True Strength Index to cross below the scale value.

How to interpret the displayed price returned from the TSI (eq)

Closing exactly at the price will cause the True Strength Index value to equal the previous TSI value.

Closing above the price will cause the True Strength Index value to increase.

Closing below the price will cause the True Strength Index value to decrease.

How to interpret the displayed price returned from the TSI signal line crossover.

Closing exactly at the given price will cause the True Strength Index value to equal the signal line.

Closing above the given price will cause the True Strength Index to cross above the signal line.

Closing below the given price will cause the True Strength Index to cross below the signal line.

Common methods to derive signals from the TSI :

Zero-line crossovers

When the CMO crosses above the zero-line, a buy signal is generated.

When the CMO crosses below the zero-line, a sell signal is generated.

“Overbought” and “Oversold” crossover

When the SMI crosses below -25 and then moves back above it, a buy signal is generated.

When the SMI crosses above +25 and then moves back below it, a sell signal is generated.

What Does the True Strength Index (TSI) Tell You?

The indicator is primarily used to identify overbought and oversold conditions in an asset's price, spot divergence, identify trend direction and changes via the zero-line, and highlight short-term price momentum with signal line crossovers.

Since the TSI is based on price movements, oversold and overbought levels will vary by the asset being traded. Some stocks may reach +30 and -30 before tending to see price reversals, while another stock may reverse near +20 and -20.

Mark extreme TSI levels, on the asset being traded, to see where overbought and oversold is. Being oversold doesn't necessarily mean it is time to buy, and when an asset is overbought it doesn't necessarily mean it is time to sell. Traders will typically watch for other signals to trigger a trade decision. For example, they may wait for the price or TSI to start dropping before selling in overbought territory. Alternatively, they may wait for a signal line crossover.

Signal Line Crossovers

The true strength index has a signal line, which is usually a seven- to 13-period EMA of the TSI line. A signal line crossover occurs when the TSI line crosses the signal line. When the TSI crosses above the signal line from below, that may warrant a long position. When the TSI crosses below the signal line from above, that may warrant selling or short selling.

Signal line crossovers occur frequently, so should be utilized only in conjunction with other signals from the TSI. For example, buy signals may be favoured when the TSI is above the zero-line. Or sell signals may be favoured when the TSI is in overbought territory.

Zero-line Crossovers

The zero-line crossover is another signal the TSI generates. Price momentum is positive when the indicator is above zero and negative when it is below zero. Some traders use the zero-line for a directional bias. For example, a trader may decide only to enter a long position if the indicator is above its zero-line. Conversely, the trader would be bearish and only consider short positions if the indicator's value is below zero.

Breakouts and Divergence

Traders can use support and resistance levels created by the true strength index to identify breakouts and price momentum shifts. For instance, if the indicator breaks below a trendline, the price may see continued selling.

Divergence is another tool the TSI provides. If the price of an asset is moving higher, while the TSI is dropping, that is called bearish divergence and could result in a downside price move. If the TSI is rising while the price is falling, that could signal higher prices to come. This is called bullish divergence.

Divergence is a poor timing signal, so it should only be used in conjunction with other signals generated by the TSI or other technical indicators.

The Difference Between the True Strength Index (TSI) and the Moving Average Convergence Divergence (MACD) Indicator.

The TSI is smoothing price changes to create a technical oscillator. The moving average convergence divergence (MACD) indicator is measuring the separation between two moving averages. Both indicators are used in similar ways for trading purposes, yet they are not calculated the same and will provide different signals at different times.

The Limitations of Using the True Strength Index (TSI)

Many of the signals provided by the TSI will be false signals. That means the price action will be different than expected following a trade signal. For example, during an uptrend, the TSI may cross below the zero-line several times, but then the price proceeds higher even though the TSI indicates momentum has shifted down.

Signal line crossovers also occur so frequently that they may not provide a lot of trading benefit. Such signals need to be heavily filtered based on other elements of the indicator or through other forms of analysis. The TSI will also sometimes change direction without price changing direction, resulting in trade signals that look good on the TSI but continue to lose money based on price.

Divergence also tends to unreliable on the indicator. Divergence can last so long that it provides little insight into when a reversal will actually occur. Also, divergence isn't always present when price reversals actually do occur.

The TSI should only be used in conjunction with other forms of analysis, such as price action analysis and other technical indicators.

This is not financial advice, use at your own risk.

Pi Cycle Top Indicator for BTCUSDThis indicator adds the Pi Cycle Top Indicator for BTCUSD to your chart.

Indicator Overview

The Pi Cycle Top Indicator has historically been effective in picking out the timing of market cycle highs to within 3 days. It uses the 111 day moving average (111DMA) and a newly created multiple of the 350 day moving average, the 350DMA x 2.

For the past three market cycles, when the 111DMA moves up and crosses the 350DMA x 2 we see that it coincides with the price of Bitcoin peaking. It is also interesting to note that 350 / 111 is 3.153, which is very close to Pi = 3.142. In fact, it is the closest we can get to Pi when dividing 350 by another whole number.

It once again demonstrates the cyclical nature of Bitcoin price action over long time frames. Though in this instance it does so with a high degree of accuracy over the past 7 years.

How It Can Be Used

Pi Cycle Top is useful to indicate when the market is very overheated. So overheated that the shorter term moving average, which is the 111 day moving average, has reached a x2 multiple of the 350 day moving average. Historically it has proved advantageous to sell Bitcoin at this time in Bitcoin's price cycles.

Matrix Library (Linear Algebra, incl Multiple Linear Regression)What's this all about?

Ever since 1D arrays were added to Pine Script, many wonderful new opportunities have opened up. There has been a few implementations of matrices and matrix math (most notably by TradingView-user tbiktag in his recent Moving Regression script: ). However, so far, no comprehensive libraries for matrix math and linear algebra has been developed. This script aims to change that.

I'm not math expert, but I like learning new things, so I took it upon myself to relearn linear algebra these past few months, and create a matrix math library for Pine Script. The goal with the library was to make a comprehensive collection of functions that can be used to perform as many of the standard operations on matrices as possible, and to implement functions to solve systems of linear equations. The library implements matrices using arrays, and many standard functions to manipulate these matrices have been added as well.

The main purpose of the library is to give users the ability to solve systems of linear equations (useful for Multiple Linear Regression with K number of independent variables for example), but it can also be used to simulate 2D arrays for any purpose.

So how do I use this thing?

Personally, what I do with my private Pine Script libraries is I keep them stored as text-files in a Libraries folder, and I copy and paste them into my code when I need them. This library is quite large, so I have made sure to use brackets in comments to easily hide any part of the code. This helps with big libraries like this one.

The parts of this script that you need to copy are labeled "MathLib", "ArrayLib", and "MatrixLib". The matrix library is dependent on the functions from these other two libraries, but they are stripped down to only include the functions used by the MatrixLib library.