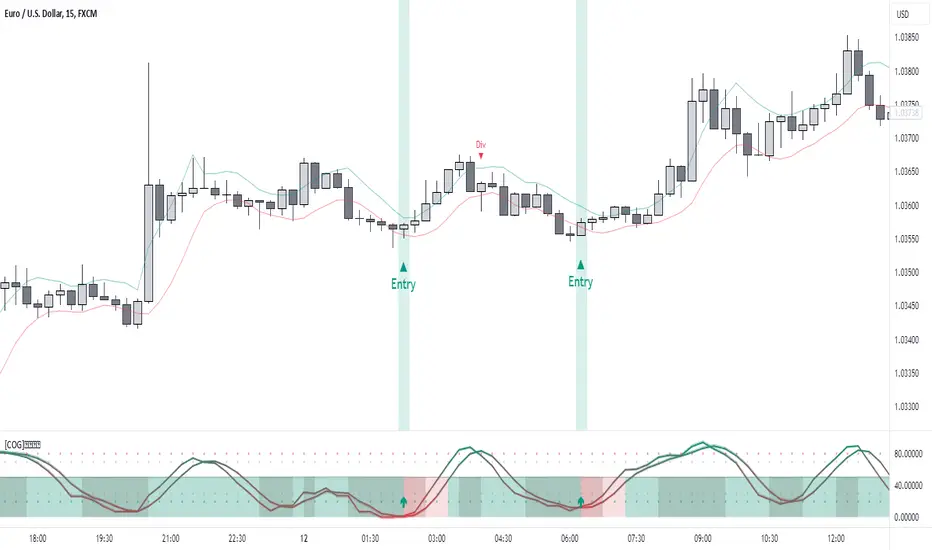

Smart PA Early Entry - Trend StartSmart PA Early Entry Indicator (MACD + FVG + Fibonacci)

This TradingView indicator helps traders spot potential trend reversals early by combining multiple technical tools:

MACD Momentum – Identifies the direction of the trend.

Volume Filter – Confirms strong market participation for reliable signals.

Fair Value Gaps (FVG) – Highlights areas where price may reverse or continue strongly.

Fibonacci Retracement Levels – Pinpoints key support/resistance zones for early entries.

ATR-based Stop Loss – Automatically calculates a dynamic stop-loss based on market volatility.

Trend Start Signals – Alerts only appear on the first candle of a potential trend change to avoid repeated signals.

Visual Labels & Plots – Shows entry price, stop-loss, FVG zones, and Fibonacci levels for easy chart reading.

Ideal for: Intraday and swing traders looking for high-probability entries near trend reversals with clear risk management.

อินดิเคเตอร์ Pine Script®