RifleShooterLibLibrary "RifleShooterLib"

Provides a collection of helper functions in support of the Rifle Shooter Indicators.

Functions support the key components of the Rifle Trade algorithm including

* measuring momentum

* identifying paraboloic price action (to disable the algorthim during such time)

* determine the lookback criteria of X point movement in last N minutes

* processing and navigating between the 23/43/73 levels

* maintaining a status table of algorithm progress

toStrRnd(val, digits)

Parameters:

val (float)

digits (int)

_isValidTimeRange(startTimeInput, endTimeInput)

Parameters:

startTimeInput (string)

endTimeInput (string)

_normalize(_src, _min, _max)

_normalize Normalizes series with unknown min/max using historical min/max.

Parameters:

_src (float) : Source series to normalize

_min (float) : minimum value of the rescaled series

_max (float) : maximum value of the rescaled series

Returns: The series scaled with values between min and max

arrayToSeries(arrayInput)

arrayToSeries Return an array from the provided series.

Parameters:

arrayInput (array) : Source array to convert to a series

Returns: The array as a series datatype

f_parabolicFiltering(_activeCount, long, shooterRsi, shooterRsiLongThreshold, shooterRsiShortThreshold, fiveMinuteRsi, fiveMinRsiLongThreshold, fiveMinRsiShortThreshold, shooterRsiRoc, shooterRsiRocLongThreshold, shooterRsiRocShortThreshold, quickChangeLookbackBars, quckChangeThreshold, curBarChangeThreshold, changeFromPrevBarThreshold, maxBarsToholdParabolicMoveActive, generateLabels)

f_parabolicFiltering Return true when price action indicates a parabolic active movement based on the provided inputs and thresholds.

Parameters:

_activeCount (int)

long (bool)

shooterRsi (float)

shooterRsiLongThreshold (float)

shooterRsiShortThreshold (float)

fiveMinuteRsi (float)

fiveMinRsiLongThreshold (float)

fiveMinRsiShortThreshold (float)

shooterRsiRoc (float)

shooterRsiRocLongThreshold (float)

shooterRsiRocShortThreshold (float)

quickChangeLookbackBars (int)

quckChangeThreshold (int)

curBarChangeThreshold (int)

changeFromPrevBarThreshold (int)

maxBarsToholdParabolicMoveActive (int)

generateLabels (bool)

rsiValid(rsi, buyThreshold, sellThreshold)

rsiValid Returns true if the provided RSI value is withing the associated threshold. For the unused threshold set it to na

Parameters:

rsi (float)

buyThreshold (float)

sellThreshold (float)

squezeBands(source, length)

squezeBands Returns the squeeze bands momentum color of current source series input

Parameters:

source (float)

length (int)

f_momentumOscilator(source, length, transperency)

f_momentumOscilator Returns the squeeze pro momentum value and bar color states of the series input

Parameters:

source (float)

length (int)

transperency (int)

f_getLookbackExtreme(lowSeries, highSeries, lbBars, long)

f_getLookbackExtreme Return the highest high or lowest low over the look back window

Parameters:

lowSeries (float)

highSeries (float)

lbBars (int)

long (bool)

f_getInitialMoveTarget(lbExtreme, priveMoveOffset, long)

f_getInitialMoveTarget Return the point delta required to achieve an initial rifle move (X points over Y lookback)

Parameters:

lbExtreme (float)

priveMoveOffset (int)

long (bool)

isSymbolSupported(sym)

isSymbolSupported Return true if provided symbol is one of the supported DOW Rifle Indicator symbols

Parameters:

sym (string)

getBasePrice(price)

getBasePrice Returns integer portion of provided float

Parameters:

price (float)

getLastTwoDigitsOfPrice(price)

getBasePrice Returns last two integer numerals of provided float value

Parameters:

price (float)

getNextLevelDown(price, lowestLevel, middleLevel, highestLevel)

getNextLevelDown Returns the next level above the provided price value

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

getNextLevelUp(price, lowestLevel, middleLevel, highestLevel)

getNextLevelUp Returns the next level below the provided price value

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

isALevel(price, lowestLevel, middleLevel, highestLevel)

isALevel Returns true if the provided price is onve of the specified levels

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

getClosestLevel(price, lowestLevel, middleLevel, highestLevel)

getClosestLevel Returns the level closest to the price value provided

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

f_fillSetupTableCell(_table, _col, _row, _text, _bgcolor, _txtcolor, _text_size)

f_fillSetupTableCell Helper function to fill a setup table celll

Parameters:

_table (table)

_col (int)

_row (int)

_text (string)

_bgcolor (color)

_txtcolor (color)

_text_size (string)

f_fillSetupTableRow(_table, _row, _col0Str, _col1Str, _col2Str, _bgcolor, _textColor, _textSize)

f_fillSetupTableRow Helper function to fill a setup table row

Parameters:

_table (table)

_row (int)

_col0Str (string)

_col1Str (string)

_col2Str (string)

_bgcolor (color)

_textColor (color)

_textSize (string)

f_addBlankRow(_table, _row)

f_addBlankRow Helper function to fill a setup table row with empty values

Parameters:

_table (table)

_row (int)

f_updateVersionTable(versionTable, versionStr, versionDateStr)

f_updateVersionTable Helper function to fill the version table with provided values

Parameters:

versionTable (table)

versionStr (string)

versionDateStr (string)

f_updateSetupTable(_table, parabolicMoveActive, initialMoveTargetOffset, initialMoveAchieved, shooterRsi, shooterRsiValid, rsiRocEnterThreshold, shooterRsiRoc, fiveMinuteRsi, fiveMinuteRsiValid, requireValid5MinuteRsiForEntry, stallLevelOffset, stallLevelExceeded, stallTargetOffset, recoverStallLevelValid, curBarChangeValid, volumeRoc, volumeRocThreshold, enableVolumeRocForTrigger, tradeActive, entryPrice, curCloseOffset, curSymCashDelta, djiCashDelta, showDjiDelta, longIndicator, fontSize)

f_updateSetupTable Manages writing current data to the setup table

Parameters:

_table (table)

parabolicMoveActive (bool)

initialMoveTargetOffset (float)

initialMoveAchieved (bool)

shooterRsi (float)

shooterRsiValid (bool)

rsiRocEnterThreshold (float)

shooterRsiRoc (float)

fiveMinuteRsi (float)

fiveMinuteRsiValid (bool)

requireValid5MinuteRsiForEntry (bool)

stallLevelOffset (float)

stallLevelExceeded (bool)

stallTargetOffset (float)

recoverStallLevelValid (bool)

curBarChangeValid (bool)

volumeRoc (float)

volumeRocThreshold (float)

enableVolumeRocForTrigger (bool)

tradeActive (bool)

entryPrice (float)

curCloseOffset (float)

curSymCashDelta (float)

djiCashDelta (float)

showDjiDelta (bool)

longIndicator (bool)

fontSize (string)

ค้นหาในสคริปต์สำหรับ "entry"

light_logLight Log - A Defensive Programming Library for Pine Script

Overview

The Light Log library transforms Pine Script development by introducing structured logging and defensive programming patterns typically found in enterprise languages like C#. This library addresses a fundamental challenge in Pine Script: the lack of sophisticated error handling and debugging tools that developers expect when building complex trading systems.

At its core, Light Log provides three transformative capabilities that work together to create more reliable and maintainable code. First, it wraps all native Pine Script types in error-aware containers, allowing values to carry validation state alongside their data. Second, it offers a comprehensive logging system with severity levels and conditional rendering. Third, it includes defensive programming utilities that catch errors early and make code self-documenting.

The Philosophy of Errors as Values

Traditional Pine Script error handling relies on runtime errors that halt execution, making it difficult to build resilient systems that can gracefully handle edge cases. Light Log introduces a paradigm shift by treating errors as first-class values that flow through your program alongside regular data.

When you wrap a value using Light Log's type system, you're not just storing data – you're creating a container that can carry both the value and its validation state. For example, when you call myNumber.INT() , you receive an INT object that contains both the integer value and a Log object that can describe any issues with that value. This approach, inspired by functional programming languages, allows errors to propagate through calculations without causing immediate failures.

Consider how this changes error handling in practice. Instead of a calculation failing catastrophically when it encounters invalid input, it can produce a result object that contains both the computed value (which might be na) and a detailed log explaining what went wrong. Subsequent operations can check has_error() to decide whether to proceed or handle the error condition gracefully.

The Typed Wrapper System

Light Log provides typed wrappers for every native Pine Script type: INT, FLOAT, BOOL, STRING, COLOR, LINE, LABEL, BOX, TABLE, CHART_POINT, POLYLINE, and LINEFILL. These wrappers serve multiple purposes beyond simple value storage.

Each wrapper type contains two fields: the value field v holds the actual data, while the error field e contains a Log object that tracks the value's validation state. This dual nature enables powerful programming patterns. You can perform operations on wrapped values and accumulate error information along the way, creating an audit trail of how values were processed.

The wrapper system includes convenient methods for converting between wrapped and unwrapped values. The extension methods like INT() , FLOAT() , etc., make it easy to wrap existing values, while the from_INT() , from_FLOAT() methods extract the underlying values when needed. The has_error() method provides a consistent interface for checking whether any wrapped value has encountered issues during processing.

The Log Object: Your Debugging Companion

The Log object represents the heart of Light Log's debugging capabilities. Unlike simple string concatenation for error messages, the Log object provides a structured approach to building, modifying, and rendering diagnostic information.

Each Log object carries three essential pieces of information: an error type (info, warning, error, or runtime_error), a message string that can be built incrementally, and an active flag that controls conditional rendering. This structure enables sophisticated logging patterns where you can build up detailed diagnostic information throughout your script's execution and decide later whether and how to display it.

The Log object's methods support fluent chaining, allowing you to build complex messages in a readable way. The write() and write_line() methods append text to the log, while new_line() adds formatting. The clear() method resets the log for reuse, and the rendering methods ( render_now() , render_condition() , and the general render() ) control when and how messages appear.

Defensive Programming Made Easy

Light Log's argument validation functions transform how you write defensive code. Instead of cluttering your functions with verbose validation logic, you can use concise, self-documenting calls that make your intentions clear.

The argument_error() function provides strict validation that halts execution when conditions aren't met – perfect for catching programming errors early. For less critical issues, argument_log_warning() and argument_log_error() record problems without stopping execution, while argument_log_info() provides debug visibility into your function's behavior.

These functions follow a consistent pattern: they take a condition to check, the function name, the argument name, and a descriptive message. This consistency makes error messages predictable and helpful, automatically formatting them to show exactly where problems occurred.

Building Modular, Reusable Code

Light Log encourages a modular approach to Pine Script development by providing tools that make functions more self-contained and reliable. When functions validate their inputs and return wrapped values with error information, they become true black boxes that can be safely composed into larger systems.

The void_return() function addresses Pine Script's requirement that all code paths return a value, even in error handling branches. This utility function provides a clean way to satisfy the compiler while making it clear that a particular code path should never execute.

The static log pattern, initialized with init_static_log() , enables module-wide error tracking. You can create a persistent Log object that accumulates information across multiple function calls, building a comprehensive diagnostic report that helps you understand complex behaviors in your indicators and strategies.

Real-World Applications

In practice, Light Log shines when building sophisticated trading systems. Imagine developing a complex indicator that processes multiple data streams, performs statistical calculations, and generates trading signals. With Light Log, each processing stage can validate its inputs, perform calculations, and pass along both results and diagnostic information.

For example, a moving average calculation might check that the period is positive, that sufficient data exists, and that the input series contains valid values. Instead of failing silently or throwing runtime errors, it can return a FLOAT object that contains either the calculated average or a detailed explanation of why the calculation couldn't be performed.

Strategy developers benefit even more from Light Log's capabilities. Complex entry and exit logic often involves multiple conditions that must all be satisfied. With Light Log, each condition check can contribute to a comprehensive log that explains exactly why a trade was or wasn't taken, making strategy debugging and optimization much more straightforward.

Performance Considerations

While Light Log adds a layer of abstraction over raw Pine Script values, its design minimizes performance impact. The wrapper objects are lightweight, containing only two fields. The logging operations only consume resources when actually rendered, and the conditional rendering system ensures that production code can run with logging disabled for maximum performance.

The library follows Pine Script best practices for performance, using appropriate data structures and avoiding unnecessary operations. The var keyword in init_static_log() ensures that persistent logs don't create new objects on every bar, maintaining efficiency even in real-time calculations.

Getting Started

Adopting Light Log in your Pine Script projects is straightforward. Import the library, wrap your critical values, add validation to your functions, and use Log objects to track important events. Start small by adding logging to a single function, then expand as you see the benefits of better error visibility and code organization.

Remember that Light Log is designed to grow with your needs. You can use as much or as little of its functionality as makes sense for your project. Even simple uses, like adding argument validation to key functions, can significantly improve code reliability and debugging ease.

Transform your Pine Script development experience with Light Log – because professional trading systems deserve professional development tools.

Light Log Technical Deep Dive: Advanced Patterns and Architecture

Understanding Errors as Values

The concept of "errors as values" represents a fundamental shift in how we think about error handling in Pine Script. In traditional Pine Script development, errors are events – they happen at a specific moment in time and immediately interrupt program flow. Light Log transforms errors into data – they become information that flows through your program just like any other value.

This transformation has profound implications. When errors are values, they can be stored, passed between functions, accumulated, transformed, and inspected. They become part of your program's data flow rather than exceptions to it. This approach, popularized by languages like Rust with its Result type and Haskell with its Either monad, brings functional programming's elegance to Pine Script.

Consider a practical example. Traditional Pine Script might calculate a momentum indicator like this:

momentum = close - close

If period is invalid or if there isn't enough historical data, this calculation might produce na or cause subtle bugs. With Light Log's approach:

calculate_momentum(src, period)=>

result = src.FLOAT()

if period <= 0

result.e.write("Invalid period: must be positive", true, ErrorType.error)

result.v := na

else if bar_index < period

result.e.write("Insufficient data: need " + str.tostring(period) + " bars", true, ErrorType.warning)

result.v := na

else

result.v := src - src

result.e.write("Momentum calculated successfully", false, ErrorType.info)

result

Now the function returns not just a value but a complete computational result that includes diagnostic information. Calling code can make intelligent decisions based on both the value and its associated metadata.

The Monad Pattern in Pine Script

While Pine Script lacks the type system features to implement true monads, Light Log brings monadic thinking to Pine Script development. The wrapped types (INT, FLOAT, etc.) act as computational contexts that carry both values and metadata through a series of transformations.

The key insight of monadic programming is that you can chain operations while automatically propagating context. In Light Log, this context is the error state. When you have a FLOAT that contains an error, operations on that FLOAT can check the error state and decide whether to proceed or propagate the error.

This pattern enables what functional programmers call "railway-oriented programming" – your code follows a success track when all is well but can switch to an error track when problems occur. Both tracks lead to the same destination (a result with error information), but they take different paths based on the validity of intermediate values.

Composable Error Handling

Light Log's design encourages composition – building complex functionality from simpler, well-tested components. Each component can validate its inputs, perform its calculation, and return a result with appropriate error information. Higher-level functions can then combine these results intelligently.

Consider building a complex trading signal from multiple indicators:

generate_signal(src, fast_period, slow_period, signal_period) =>

log = init_static_log(ErrorType.info)

// Calculate components with error tracking

fast_ma = calculate_ma(src, fast_period)

slow_ma = calculate_ma(src, slow_period)

// Check for errors in components

if fast_ma.has_error()

log.write_line("Fast MA error: " + fast_ma.e.message, true)

if slow_ma.has_error()

log.write_line("Slow MA error: " + slow_ma.e.message, true)

// Proceed with calculation if no errors

signal = 0.0.FLOAT()

if not (fast_ma.has_error() or slow_ma.has_error())

macd_line = fast_ma.v - slow_ma.v

signal_line = calculate_ma(macd_line, signal_period)

if signal_line.has_error()

log.write_line("Signal line error: " + signal_line.e.message, true)

signal.e := log

else

signal.v := macd_line - signal_line.v

log.write("Signal generated successfully")

else

signal.e := log

signal.v := na

signal

This composable approach makes complex calculations more reliable and easier to debug. Each component is responsible for its own validation and error reporting, and the composite function orchestrates these components while maintaining comprehensive error tracking.

The Static Log Pattern

The init_static_log() function introduces a powerful pattern for maintaining state across function calls. In Pine Script, the var keyword creates variables that persist across bars but are initialized only once. Light Log leverages this to create logging objects that can accumulate information throughout a script's execution.

This pattern is particularly valuable for debugging complex strategies where you need to understand behavior across multiple bars. You can create module-level logs that track important events:

// Module-level diagnostic log

diagnostics = init_static_log(ErrorType.info)

// Track strategy decisions across bars

check_entry_conditions() =>

diagnostics.clear() // Start fresh each bar

diagnostics.write_line("Bar " + str.tostring(bar_index) + " analysis:")

if close > sma(close, 20)

diagnostics.write_line("Price above SMA20", false)

else

diagnostics.write_line("Price below SMA20 - no entry", true, ErrorType.warning)

if volume > sma(volume, 20) * 1.5

diagnostics.write_line("Volume surge detected", false)

else

diagnostics.write_line("Normal volume", false)

// Render diagnostics based on verbosity setting

if debug_mode

diagnostics.render_now()

Advanced Validation Patterns

Light Log's argument validation functions enable sophisticated precondition checking that goes beyond simple null checks. You can implement complex validation logic while keeping your code readable:

validate_price_data(open_val, high_val, low_val, close_val) =>

argument_error(na(open_val) or na(high_val) or na(low_val) or na(close_val),

"validate_price_data", "OHLC values", "contain na values")

argument_error(high_val < low_val,

"validate_price_data", "high/low", "high is less than low")

argument_error(close_val > high_val or close_val < low_val,

"validate_price_data", "close", "is outside high/low range")

argument_log_warning(high_val == low_val,

"validate_price_data", "high/low", "are equal (no range)")

This validation function documents its requirements clearly and fails fast with helpful error messages when assumptions are violated. The mix of errors (which halt execution) and warnings (which allow continuation) provides fine-grained control over how strict your validation should be.

Performance Optimization Strategies

While Light Log adds abstraction, careful design minimizes overhead. Understanding Pine Script's execution model helps you use Light Log efficiently.

Pine Script executes once per bar, so operations that seem expensive in traditional programming might have negligible impact. However, when building real-time systems, every optimization matters. Light Log provides several patterns for efficient use:

Lazy Evaluation: Log messages are only built when they'll be rendered. Use conditional logging to avoid string concatenation in production:

if debug_mode

log.write_line("Calculated value: " + str.tostring(complex_calculation))

Selective Wrapping: Not every value needs error tracking. Wrap values at API boundaries and critical calculation points, but use raw values for simple operations:

// Wrap at boundaries

input_price = close.FLOAT()

validated_period = validate_period(input_period).INT()

// Use raw values internally

sum = 0.0

for i = 0 to validated_period.v - 1

sum += close

Error Propagation: When errors occur early, avoid expensive calculations:

process_data(input) =>

validated = validate_input(input)

if validated.has_error()

validated // Return early with error

else

// Expensive processing only if valid

perform_complex_calculation(validated)

Integration Patterns

Light Log integrates smoothly with existing Pine Script code. You can adopt it incrementally, starting with critical functions and expanding coverage as needed.

Boundary Validation: Add Light Log at the boundaries of your system – where user input enters and where final outputs are produced. This catches most errors while minimizing changes to existing code.

Progressive Enhancement: Start by adding argument validation to existing functions. Then wrap return values. Finally, add comprehensive logging. Each step improves reliability without requiring a complete rewrite.

Testing and Debugging: Use Light Log's conditional rendering to create debug modes for your scripts. Production users see clean output while developers get detailed diagnostics:

// User input for debug mode

debug = input.bool(false, "Enable debug logging")

// Conditional diagnostic output

if debug

diagnostics.render_now()

else

diagnostics.render_condition() // Only shows errors/warnings

Future-Proofing Your Code

Light Log's patterns prepare your code for Pine Script's evolution. As Pine Script adds more sophisticated features, code that uses structured error handling and defensive programming will adapt more easily than code that relies on implicit assumptions.

The type wrapper system, in particular, positions your code to take advantage of potential future features or more sophisticated type inference. By thinking in terms of wrapped values and error propagation today, you're building code that will remain maintainable and extensible tomorrow.

Light Log doesn't just make your Pine Script better today – it prepares it for the trading systems you'll need to build tomorrow.

Library "light_log"

A lightweight logging and defensive programming library for Pine Script.

Designed for modular and extensible scripts, this utility provides structured runtime validation,

conditional logging, and reusable `Log` objects for centralized error propagation.

It also introduces a typed wrapping system for all native Pine values (e.g., `INT`, `FLOAT`, `LABEL`),

allowing values to carry errors alongside data. This enables functional-style flows with built-in

validation tracking, error detection (`has_error()`), and fluent chaining.

Inspired by structured logging patterns found in systems like C#, it reduces boilerplate,

enforces argument safety, and encourages clean, maintainable code architecture.

method INT(self, error_type)

Wraps an `int` value into an `INT` struct with an optional log severity.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The raw `int` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: An `INT` object containing the value and a default Log instance.

method FLOAT(self, error_type)

Wraps a `float` value into a `FLOAT` struct with an optional log severity.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : The raw `float` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `FLOAT` object containing the value and a default Log instance.

method BOOL(self, error_type)

Wraps a `bool` value into a `BOOL` struct with an optional log severity.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

self (bool) : The raw `bool` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `BOOL` object containing the value and a default Log instance.

method STRING(self, error_type)

Wraps a `string` value into a `STRING` struct with an optional log severity.

Namespace types: series string, simple string, input string, const string

Parameters:

self (string) : The raw `string` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `STRING` object containing the value and a default Log instance.

method COLOR(self, error_type)

Wraps a `color` value into a `COLOR` struct with an optional log severity.

Namespace types: series color, simple color, input color, const color

Parameters:

self (color) : The raw `color` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `COLOR` object containing the value and a default Log instance.

method LINE(self, error_type)

Wraps a `line` object into a `LINE` struct with an optional log severity.

Namespace types: series line

Parameters:

self (line) : The raw `line` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `LINE` object containing the value and a default Log instance.

method LABEL(self, error_type)

Wraps a `label` object into a `LABEL` struct with an optional log severity.

Namespace types: series label

Parameters:

self (label) : The raw `label` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `LABEL` object containing the value and a default Log instance.

method BOX(self, error_type)

Wraps a `box` object into a `BOX` struct with an optional log severity.

Namespace types: series box

Parameters:

self (box) : The raw `box` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `BOX` object containing the value and a default Log instance.

method TABLE(self, error_type)

Wraps a `table` object into a `TABLE` struct with an optional log severity.

Namespace types: series table

Parameters:

self (table) : The raw `table` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `TABLE` object containing the value and a default Log instance.

method CHART_POINT(self, error_type)

Wraps a `chart.point` value into a `CHART_POINT` struct with an optional log severity.

Namespace types: chart.point

Parameters:

self (chart.point) : The raw `chart.point` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `CHART_POINT` object containing the value and a default Log instance.

method POLYLINE(self, error_type)

Wraps a `polyline` object into a `POLYLINE` struct with an optional log severity.

Namespace types: series polyline, series polyline, series polyline, series polyline

Parameters:

self (polyline) : The raw `polyline` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `POLYLINE` object containing the value and a default Log instance.

method LINEFILL(self, error_type)

Wraps a `linefill` object into a `LINEFILL` struct with an optional log severity.

Namespace types: series linefill

Parameters:

self (linefill) : The raw `linefill` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `LINEFILL` object containing the value and a default Log instance.

method from_INT(self)

Extracts the integer value from an INT wrapper.

Namespace types: INT

Parameters:

self (INT) : The wrapped INT instance.

Returns: The underlying `int` value.

method from_FLOAT(self)

Extracts the float value from a FLOAT wrapper.

Namespace types: FLOAT

Parameters:

self (FLOAT) : The wrapped FLOAT instance.

Returns: The underlying `float` value.

method from_BOOL(self)

Extracts the boolean value from a BOOL wrapper.

Namespace types: BOOL

Parameters:

self (BOOL) : The wrapped BOOL instance.

Returns: The underlying `bool` value.

method from_STRING(self)

Extracts the string value from a STRING wrapper.

Namespace types: STRING

Parameters:

self (STRING) : The wrapped STRING instance.

Returns: The underlying `string` value.

method from_COLOR(self)

Extracts the color value from a COLOR wrapper.

Namespace types: COLOR

Parameters:

self (COLOR) : The wrapped COLOR instance.

Returns: The underlying `color` value.

method from_LINE(self)

Extracts the line object from a LINE wrapper.

Namespace types: LINE

Parameters:

self (LINE) : The wrapped LINE instance.

Returns: The underlying `line` object.

method from_LABEL(self)

Extracts the label object from a LABEL wrapper.

Namespace types: LABEL

Parameters:

self (LABEL) : The wrapped LABEL instance.

Returns: The underlying `label` object.

method from_BOX(self)

Extracts the box object from a BOX wrapper.

Namespace types: BOX

Parameters:

self (BOX) : The wrapped BOX instance.

Returns: The underlying `box` object.

method from_TABLE(self)

Extracts the table object from a TABLE wrapper.

Namespace types: TABLE

Parameters:

self (TABLE) : The wrapped TABLE instance.

Returns: The underlying `table` object.

method from_CHART_POINT(self)

Extracts the chart.point from a CHART_POINT wrapper.

Namespace types: CHART_POINT

Parameters:

self (CHART_POINT) : The wrapped CHART_POINT instance.

Returns: The underlying `chart.point` value.

method from_POLYLINE(self)

Extracts the polyline object from a POLYLINE wrapper.

Namespace types: POLYLINE

Parameters:

self (POLYLINE) : The wrapped POLYLINE instance.

Returns: The underlying `polyline` object.

method from_LINEFILL(self)

Extracts the linefill object from a LINEFILL wrapper.

Namespace types: LINEFILL

Parameters:

self (LINEFILL) : The wrapped LINEFILL instance.

Returns: The underlying `linefill` object.

method has_error(self)

Returns true if the INT wrapper has an active log entry.

Namespace types: INT

Parameters:

self (INT) : The INT instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the FLOAT wrapper has an active log entry.

Namespace types: FLOAT

Parameters:

self (FLOAT) : The FLOAT instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the BOOL wrapper has an active log entry.

Namespace types: BOOL

Parameters:

self (BOOL) : The BOOL instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the STRING wrapper has an active log entry.

Namespace types: STRING

Parameters:

self (STRING) : The STRING instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the COLOR wrapper has an active log entry.

Namespace types: COLOR

Parameters:

self (COLOR) : The COLOR instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the LINE wrapper has an active log entry.

Namespace types: LINE

Parameters:

self (LINE) : The LINE instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the LABEL wrapper has an active log entry.

Namespace types: LABEL

Parameters:

self (LABEL) : The LABEL instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the BOX wrapper has an active log entry.

Namespace types: BOX

Parameters:

self (BOX) : The BOX instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the TABLE wrapper has an active log entry.

Namespace types: TABLE

Parameters:

self (TABLE) : The TABLE instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the CHART_POINT wrapper has an active log entry.

Namespace types: CHART_POINT

Parameters:

self (CHART_POINT) : The CHART_POINT instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the POLYLINE wrapper has an active log entry.

Namespace types: POLYLINE

Parameters:

self (POLYLINE) : The POLYLINE instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the LINEFILL wrapper has an active log entry.

Namespace types: LINEFILL

Parameters:

self (LINEFILL) : The LINEFILL instance to check.

Returns: True if an error or message is active in the log.

void_return()

Utility function used when a return is syntactically required but functionally unnecessary.

Returns: Nothing. Function never executes its body.

argument_error(condition, function, argument, message)

Throws a runtime error when a condition is met. Used for strict argument validation.

Parameters:

condition (bool) : Boolean expression that triggers the runtime error.

function (string) : Name of the calling function (for formatting).

argument (string) : Name of the problematic argument.

message (string) : Description of the error cause.

Returns: Never returns. Halts execution if the condition is true.

argument_log_info(condition, function, argument, message)

Logs an informational message when a condition is met. Used for optional debug visibility.

Parameters:

condition (bool) : Boolean expression that triggers the log.

function (string) : Name of the calling function.

argument (string) : Argument name being referenced.

message (string) : Informational message to log.

Returns: Nothing. Logs if the condition is true.

argument_log_warning(condition, function, argument, message)

Logs a warning when a condition is met. Non-fatal but highlights potential issues.

Parameters:

condition (bool) : Boolean expression that triggers the warning.

function (string) : Name of the calling function.

argument (string) : Argument name being referenced.

message (string) : Warning message to log.

Returns: Nothing. Logs if the condition is true.

argument_log_error(condition, function, argument, message)

Logs an error message when a condition is met. Does not halt execution.

Parameters:

condition (bool) : Boolean expression that triggers the error log.

function (string) : Name of the calling function.

argument (string) : Argument name being referenced.

message (string) : Error message to log.

Returns: Nothing. Logs if the condition is true.

init_static_log(error_type, message, active)

Initializes a persistent (var) Log object. Ideal for global logging in scripts or modules.

Parameters:

error_type (series ErrorType) : Initial severity level (required).

message (string) : Optional starting message string. Default value of ("").

active (bool) : Whether the log should be flagged active on initialization. Default value of (false).

Returns: A static Log object with the given parameters.

method new_line(self)

Appends a newline character to the Log message. Useful for separating entries during chained writes.

Namespace types: Log

Parameters:

self (Log) : The Log instance to modify.

Returns: The updated Log object with a newline appended.

method write(self, message, flag_active, error_type)

Appends a message to a Log object without a newline. Updates severity and active state if specified.

Namespace types: Log

Parameters:

self (Log) : The Log instance being modified.

message (string) : The text to append to the log.

flag_active (bool) : Whether to activate the log for conditional rendering. Default value of (false).

error_type (series ErrorType) : Optional override for the severity level. Default value of (na).

Returns: The updated Log object.

method write_line(self, message, flag_active, error_type)

Appends a message to a Log object, prefixed with a newline for clarity.

Namespace types: Log

Parameters:

self (Log) : The Log instance being modified.

message (string) : The text to append to the log.

flag_active (bool) : Whether to activate the log for conditional rendering. Default value of (false).

error_type (series ErrorType) : Optional override for the severity level. Default value of (na).

Returns: The updated Log object.

method clear(self, flag_active, error_type)

Clears a Log object’s message and optionally reactivates it. Can also update the error type.

Namespace types: Log

Parameters:

self (Log) : The Log instance being cleared.

flag_active (bool) : Whether to activate the log after clearing. Default value of (false).

error_type (series ErrorType) : Optional new error type to assign. If not provided, the previous type is retained. Default value of (na).

Returns: The cleared Log object.

method render_condition(self, flag_active, error_type)

Conditionally renders the log if it is active. Allows overriding error type and controlling active state afterward.

Namespace types: Log

Parameters:

self (Log) : The Log instance to evaluate and render.

flag_active (bool) : Whether to activate the log after rendering. Default value of (false).

error_type (series ErrorType) : Optional error type override. Useful for contextual formatting just before rendering. Default value of (na).

Returns: The updated Log object.

method render_now(self, flag_active, error_type)

Immediately renders the log regardless of `active` state. Allows overriding error type and active flag.

Namespace types: Log

Parameters:

self (Log) : The Log instance to render.

flag_active (bool) : Whether to activate the log after rendering. Default value of (false).

error_type (series ErrorType) : Optional error type override. Allows dynamic severity adjustment at render time. Default value of (na).

Returns: The updated Log object.

render(self, condition, flag_active, error_type)

Renders the log conditionally or unconditionally. Allows full control over render behavior.

Parameters:

self (Log) : The Log instance to render.

condition (bool) : If true, renders only if the log is active. If false, always renders. Default value of (false).

flag_active (bool) : Whether to activate the log after rendering. Default value of (false).

error_type (series ErrorType) : Optional error type override passed to the render methods. Default value of (na).

Returns: The updated Log object.

Log

A structured object used to store and render logging messages.

Fields:

error_type (series ErrorType) : The severity level of the message (from the ErrorType enum).

message (series string) : The text of the log message.

active (series bool) : Whether the log should trigger rendering when conditionally evaluated.

INT

A wrapped integer type with attached logging for validation or tracing.

Fields:

v (series int) : The underlying `int` value.

e (Log) : Optional log object describing validation status or error context.

FLOAT

A wrapped float type with attached logging for validation or tracing.

Fields:

v (series float) : The underlying `float` value.

e (Log) : Optional log object describing validation status or error context.

BOOL

A wrapped boolean type with attached logging for validation or tracing.

Fields:

v (series bool) : The underlying `bool` value.

e (Log) : Optional log object describing validation status or error context.

STRING

A wrapped string type with attached logging for validation or tracing.

Fields:

v (series string) : The underlying `string` value.

e (Log) : Optional log object describing validation status or error context.

COLOR

A wrapped color type with attached logging for validation or tracing.

Fields:

v (series color) : The underlying `color` value.

e (Log) : Optional log object describing validation status or error context.

LINE

A wrapped line object with attached logging for validation or tracing.

Fields:

v (series line) : The underlying `line` value.

e (Log) : Optional log object describing validation status or error context.

LABEL

A wrapped label object with attached logging for validation or tracing.

Fields:

v (series label) : The underlying `label` value.

e (Log) : Optional log object describing validation status or error context.

BOX

A wrapped box object with attached logging for validation or tracing.

Fields:

v (series box) : The underlying `box` value.

e (Log) : Optional log object describing validation status or error context.

TABLE

A wrapped table object with attached logging for validation or tracing.

Fields:

v (series table) : The underlying `table` value.

e (Log) : Optional log object describing validation status or error context.

CHART_POINT

A wrapped chart point with attached logging for validation or tracing.

Fields:

v (chart.point) : The underlying `chart.point` value.

e (Log) : Optional log object describing validation status or error context.

POLYLINE

A wrapped polyline object with attached logging for validation or tracing.

Fields:

v (series polyline) : The underlying `polyline` value.

e (Log) : Optional log object describing validation status or error context.

LINEFILL

A wrapped linefill object with attached logging for validation or tracing.

Fields:

v (series linefill) : The underlying `linefill` value.

e (Log) : Optional log object describing validation status or error context.

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio

Real-time feedback: Updates performance statistics with each new trade

Visual analytics: Color-coded performance table provides instant visual feedback on strategy health

Integrated risk management: Implements sophisticated take profit mechanisms with 3-step ATR and percentage-based exits

BTCUSD Performance

The table in the upper right corner is a comprehensive performance dashboard showing trading strategy statistics.

Note: While this presentation uses Vegas SuperTrend as the underlying strategy, this is merely an example. The Stats framework can be applied to any trading strategy. The Vegas SuperTrend implementation is included solely to demonstrate how the analytics module integrates with a trading strategy.

⚠️ Timeframe Limitations

Important: TradingView's backtesting engine has a maximum storage limit of 10,000 bars. When using this strategy stats framework on smaller timeframes such as 1-hour or 2-hour charts, you may encounter errors if your backtesting period is too long.

Recommended Timeframe Usage:

Ideal for: 4H, 6H, 8H, Daily charts and above

May cause errors on: 1H, 2H charts spanning multiple years

Not recommended for: Timeframes below 1H with long history

█ Strategy, How it Works: Detailed Explanation

The Strategy Stats framework consists of three primary components: statistical data collection, performance analysis, and visualization.

🔶 Statistical Data Collection

The system maintains several critical data arrays:

equityHistory: Tracks equity curve over time

tradeHistory: Records profit/loss of each trade

predictionSignals: Stores trade direction signals (1 for long, -1 for short)

actualReturns: Records corresponding actual returns from each trade

For each closed trade, the system captures:

float tradePnL = strategy.closedtrades.profit(tradeIndex)

float tradeReturn = strategy.closedtrades.profit_percent(tradeIndex)

int tradeType = entryPrice < exitPrice ? 1 : -1 // Direction

🔶 Performance Metrics Calculation

The framework calculates several key performance metrics:

Information Coefficient (IC):

The correlation between prediction signals and actual returns, measuring forecast skill.

IC = Correlation(predictionSignals, actualReturns)

Where Correlation is the Pearson correlation coefficient:

Correlation(X,Y) = (nΣXY - ΣXY) / √

Sortino Ratio:

Measures risk-adjusted return focusing only on downside risk:

Sortino = (Avg_Return - Risk_Free_Rate) / Downside_Deviation

Where Downside Deviation is:

Downside_Deviation = √

R_i represents individual returns, T is the target return (typically the risk-free rate), and n is the number of observations.

Maximum Drawdown:

Tracks the largest percentage drop from peak to trough:

DD = (Peak_Equity - Trough_Equity) / Peak_Equity * 100

🔶 Time Period Calculation

The system automatically determines the appropriate number of bars to analyze for each timeframe based on the current chart timeframe:

bars_7d = math.max(1, math.round(7 * barsPerDay))

bars_30d = math.max(1, math.round(30 * barsPerDay))

bars_90d = math.max(1, math.round(90 * barsPerDay))

bars_365d = math.max(1, math.round(365 * barsPerDay))

bars_4y = math.max(1, math.round(365 * 4 * barsPerDay))

Where barsPerDay is calculated based on the chart timeframe:

barsPerDay = timeframe.isintraday ?

24 * 60 / math.max(1, (timeframe.in_seconds() / 60)) :

timeframe.isdaily ? 1 :

timeframe.isweekly ? 1/7 :

timeframe.ismonthly ? 1/30 : 0.01

🔶 Visual Representation

The system presents performance data in a color-coded table with intuitive visual indicators:

Green: Excellent performance

Lime: Good performance

Gray: Neutral performance

Orange: Mediocre performance

Red: Poor performance

█ Trade Direction

The Strategy Stats framework supports three trading directions:

Long Only: Only takes long positions when entry conditions are met

Short Only: Only takes short positions when entry conditions are met

Both: Takes both long and short positions depending on market conditions

█ Usage

To effectively use the Strategy Stats framework:

Apply to existing strategies: Add the performance tracking code to any strategy to gain advanced analytics

Monitor multiple timeframes: Use the multi-timeframe analysis to identify performance trends

Evaluate strategy health: Review IC and Sortino ratios to assess predictive power and risk-adjusted returns

Optimize parameters: Use performance data to refine strategy parameters

Compare strategies: Apply the framework to multiple strategies to identify the most effective approach

For best results, allow the strategy to generate sufficient trade history for meaningful statistical analysis (at least 20-30 trades).

█ Default Settings

The default settings have been carefully calibrated for cryptocurrency markets:

Performance Tracking:

Time periods: 7D, 30D, 90D, 1Y, 4Y

Statistical measures: Return, Win%, MaxDD, IC, Sortino Ratio

IC color thresholds: >0.3 (green), >0.1 (lime), <-0.1 (orange), <-0.3 (red)

Sortino color thresholds: >1.0 (green), >0.5 (lime), <0 (red)

Multi-Step Take Profit:

ATR multipliers: 2.618, 5.0, 10.0

Percentage levels: 3%, 8%, 17%

Short multiplier: 1.5x (makes short take profits more aggressive)

Stop loss: 20%

Keltner Channel StrategyOverview

The Keltner Channel Strategy is a powerful trend-following and mean-reversion system that leverages the Keltner Channels, EMA crossovers, and ATR-based stop-losses to optimize trade entries and exits. This strategy has proven to be highly effective, particularly when applied to Gold (XAUUSD) and other commodities with strong trend characteristics.

📈 How It Works

This strategy incorporates two trading approaches: 1️⃣ Keltner Channel Reversal Trades – Identifies overbought and oversold conditions when price touches the outer bands.

2️⃣ Trend Following Trades – Uses the 9 EMA & 21 EMA crossover, with confirmation from the 50 EMA, to enter trades in the direction of the trend.

🔍 Entry & Exit Criteria

📊 Keltner Channel Entries (Reversal Strategy)

✅ Long Entry: When the price crosses below the lower Keltner Band (potential reversal).

✅ Short Entry: When the price crosses above the upper Keltner Band (potential reversal).

⏳ Exit Conditions:

Long positions close when price crosses back above the mid-band (EMA-based).

Short positions close when price crosses back below the mid-band (EMA-based).

📈 Trend Following Entries (Momentum Strategy)

✅ Long Entry: When the 9 EMA crosses above the 21 EMA, and price is above the 50 EMA (bullish momentum).

✅ Short Entry: When the 9 EMA crosses below the 21 EMA, and price is below the 50 EMA (bearish momentum).

⏳ Exit Conditions:

Long positions close when the 9 EMA crosses back below the 21 EMA.

Short positions close when the 9 EMA crosses back above the 21 EMA.

📌 Risk Management & Profit Targeting

ATR-based Stop-Losses:

Long trades: Stop set at 1.5x ATR below entry price.

Short trades: Stop set at 1.5x ATR above entry price.

Take-Profit Levels:

Long trades: Profit target 2x ATR above entry price.

Short trades: Profit target 2x ATR below entry price.

🚀 Why Use This Strategy?

✅ Works exceptionally well on Gold (XAUUSD) due to high volatility.

✅ Combines reversal & trend strategies for improved adaptability.

✅ Uses ATR-based risk management for dynamic position sizing.

✅ Fully automated alerts for trade entries and exits.

🔔 Alerts

This script includes automated TradingView alerts for:

🔹 Keltner Band touches (Reversal signals).

🔹 EMA crossovers (Momentum trades).

🔹 Stop-loss & Take-profit activations.

📊 Ideal Markets & Timeframes

Best for: Gold (XAUUSD), NASDAQ (NQ), Crude Oil (CL), and trending assets.

Recommended Timeframes: 15m, 1H, 4H, Daily.

⚡️ How to Use

1️⃣ Add this script to your TradingView chart.

2️⃣ Select a 15m, 1H, or 4H timeframe for optimal results.

3️⃣ Enable alerts to receive trade notifications in real time.

4️⃣ Backtest and tweak ATR settings to fit your trading style.

🚀 Optimize your Gold trading with this Keltner Channel Strategy! Let me know how it performs for you. 💰📊

Money Flow Indicator (Chaikin Oscillator) with VWAPStrategy Overview

Entry Conditions:

Buy Entry:

The Chaikin Oscillator crosses above the signal line.

The current price is above the VWAP.

Sell Entry:

The Chaikin Oscillator crosses below the signal line.

The current price is below the VWAP.

Exit Conditions:

Profit Taking:

Take profit when a target profit is reached (e.g., a 2% increase from the entry price).

Stop Loss:

Set a stop loss, for example, at a 1% decline from the entry price.

Risk Management:

Manage risk by limiting each trade to no more than 1-2% of the account balance.

Calculate position size based on risk and trade accordingly.

Trend Confirmation:

Use other indicators (like moving averages) to confirm the overall trend and focus trades in the direction of the trend.

In an uptrend, prioritize buy entries; in a downtrend, prioritize sell entries.

Specific Trade Scenarios

Example 1: Buy Entry:

Enter a buy position when the Chaikin Oscillator crosses above the signal line and the price is above the VWAP.

Set a stop loss 1% below the entry price and a profit target 2% above the entry price.

Example 2: Sell Entry:

Enter a sell position when the Chaikin Oscillator crosses below the signal line and the price is below the VWAP.

Set a stop loss 1% above the entry price and a profit target 2% below the entry price.

Additional Considerations

Backtesting: Test this strategy with historical data to evaluate performance and make adjustments as needed.

Market Conditions: Pay attention to market volatility and economic indicators, adjusting the trading strategy flexibly.

Psychological Factors: Avoid emotional decisions and follow clear rules when trading.

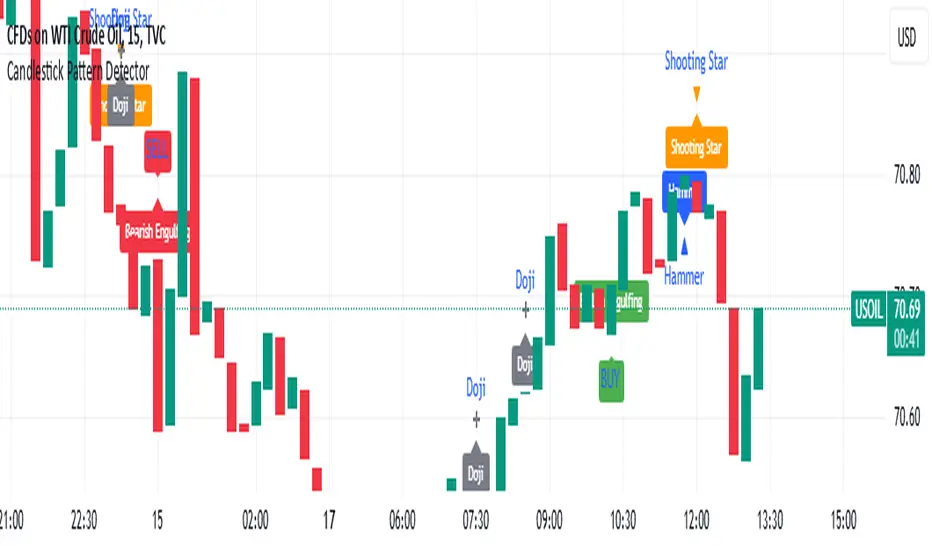

Candlestick Pattern Detector - Vijay PrasadOverview:

This Pine Script v6 indicator is designed to detect and label key candlestick patterns on TradingView charts. It provides real-time visual markers for major bullish and bearish reversal signals, aiding traders in decision-making.

Usefulness:

✅ Saves time by automating candlestick pattern detection.

✅ Reduces manual chart analysis errors.

✅ Works across all markets & timeframes.

✅ Enhances trading strategies with accurate signals.

Candlestick Patterns Recognises:

Bullish Engulfing – A strong bullish reversal pattern.

Bearish Engulfing – Indicates a potential downtrend.

Hammer – Suggests a market bottom or reversal.

Shooting Star – A bearish reversal signal at the top of an uptrend.

Doji – Signals market indecision and possible trend change.

Key Functions:

Automated Pattern Visible

Identifies candlestick patterns dynamically and plots them on the chart.

Visual Labels for Patterns

Labels to indicate specific candlestick formations.

Labels appear only when a valid pattern is detected, avoiding unnecessary clutter.

Buy/Sell Signal

Plots buy signals at bullish patterns and sell signals at bearish patterns.

Helps traders recognize trend reversals and entry/exit points.

Bullish Engulfing Pattern (Green Label)

What it means: A bullish engulfing pattern typically signals a potential reversal from a downtrend to an uptrend. The current candle fully engulfs the previous candle, signaling strong buying interest.

Identifying Candlestick Patterns on the Chart

How to use it:

Entry: Look for a green label (bullish engulfing) at the bottom of the chart. When it appears, consider entering a long position (buy).

Confirmation: To increase reliability, wait for confirmation by observing if price moves above the high of the bullish engulfing candle.

Exit: Exit when the trend shows signs of reversing or take profit at predefined levels (e.g., resistance or a risk-to-reward ratio).

Bearish Engulfing Pattern (Red Label)

What it means: A bearish engulfing pattern is a signal of a potential reversal from an uptrend to a downtrend. The current candle fully engulfs the previous candle, signaling strong selling pressure.

How to use it:

Entry: Look for a red label (bearish engulfing) at the top of the chart. When it appears, consider entering a short position (sell).

Confirmation: Wait for the price to move below the low of the bearish engulfing candle to confirm the bearish trend.

Exit: Close the trade when the price reaches support levels or the trend shows signs of reversing.

Doji Pattern (Blue Circle)

What it means: A Doji candle signals market indecision. It represents a balance between buyers and sellers, often marking a potential reversal or consolidation point.

How to use it:

Entry: If the Doji appears after a strong trend (bullish or bearish), wait for the next candle to break above or below the Doji's high or low. This can signal a continuation or reversal.

Confirmation: You can look for additional indicators like moving averages, RSI, or MACD for confirmation before taking any action.

Exit: Exit when the price shows clear momentum in your entry direction.

Hammer Pattern (Orange Triangle)

What it means: The hammer pattern is a bullish reversal pattern that appears after a downtrend. It suggests that sellers pushed the price down during the session, but buyers managed to push the price back up.

How to use it:

Entry: When a hammer appears, consider entering a long position (buy). The price should move above the hammer's high for confirmation.

Confirmation: Look for strong volume and a follow-up bullish candle to confirm the reversal.

Exit: Set a target based on the next resistance level, or use a trailing stop to lock in profits.

Using Candlestick Patterns with Other Indicators

To increase your chances of success, combine candlestick patterns with other technical indicators.

Here are some ideas:

RSI (Relative Strength Index): Use RSI to check whether the market is overbought or oversold. A bullish engulfing in an oversold market could indicate a stronger buy signal, and a bearish engulfing in an overbought market could indicate a stronger sell signal.

Moving Averages (e.g., 50 EMA, 200 EMA): Confirm trend direction. If the candlestick pattern aligns with the direction of the moving averages, it can give a stronger signal.

MACD (Moving Average Convergence Divergence): Use MACD to confirm momentum and potential trend changes. If a candlestick pattern aligns with a MACD crossover, it strengthens the signal.

Volume: Look for higher-than-average volume when a pattern appears. This can give you additional confirmation that the market is reacting strongly.

Practice and Refine

It's important to practice using the candlestick patterns in a demo account or backtest them to see how they perform under different market conditions. Over time, you can adjust the settings and patterns to fit your trading style and preferences.

CapitalManagementLibrary "CapitalManagement"

TODO: Manage the capital

order_volume(percent_risk, order_entry_price, stop_loss_price)

: Function to calculate order volume according to give risk percent_risk

Parameters:

percent_risk (float)

order_entry_price (float)

stop_loss_price (float)

calculate_takeprofit_price(entry_price, stop_loss_price, risk_reward)

: Function to calculate take profit price according to given risk:reward ratio

Parameters:

entry_price (float)

stop_loss_price (float)

risk_reward (float)

Returns: Return take profit value according to given risk:reward ratio

Ichimoku + RSI + MACD Strategy1. Relative Strength Index (RSI)

Overview:

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is typically used to identify overbought or oversold conditions in a market.

How to Use with Ichimoku:

Long Entry: Look for RSI to be above 30 (indicating it is not oversold) when the price is above the Ichimoku Cloud.

Short Entry: Look for RSI to be below 70 (indicating it is not overbought) when the price is below the Ichimoku Cloud.

2. Moving Average Convergence Divergence (MACD)

Overview:

The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. It consists of the MACD line, signal line, and histogram.

How to Use with Ichimoku:

Long Entry: Enter a long position when the MACD line crosses above the signal line while the price is above the Ichimoku Cloud.

Short Entry: Enter a short position when the MACD line crosses below the signal line while the price is below the Ichimoku Cloud.

Combined Strategy Example

Here’s a brief outline of how to structure a trading strategy using Ichimoku, RSI, and MACD:

Long Entry Conditions:

Price is above the Ichimoku Cloud.

RSI is above 30.

MACD line crosses above the signal line.

Short Entry Conditions:

Price is below the Ichimoku Cloud.

RSI is below 70.

MACD line crosses below the signal line.

Exit Conditions:

Exit long when MACD line crosses below the signal line.

Exit short when MACD line crosses above the signal line.

Mean Reversion Cloud (Ornstein-Uhlenbeck) // AlgoFyreThe Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator detects mean-reversion opportunities by applying the Ornstein-Uhlenbeck process. It calculates a dynamic mean using an Exponential Weighted Moving Average, surrounded by volatility bands, signaling potential buy/sell points when prices deviate.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Adaptive Mean Calculation

🔸Volatility-Based Cloud

🔸Speed of Reversion (θ)

🔶 FUNCTIONALITY

🔸Dynamic Mean and Volatility Bands

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔸Visualization via Table and Plotshapes

🞘 Table Overview

🞘 Plotshapes Explanation

🞘 Code extract

🔶 INSTRUCTIONS

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

🞘 Understanding What to Look For on the Chart

🞘 Possible Entry Signals

🞘 Possible Take Profit Strategies

🞘 Possible Stop-Loss Levels

🞘 Additional Tips

🔸Customize settings

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) is a unique indicator that applies the Ornstein-Uhlenbeck stochastic process to identify mean-reverting behavior in asset prices. Unlike traditional moving average-based indicators, this model uses an Exponentially Weighted Moving Average (EWMA) to calculate the long-term mean, dynamically adjusting to recent price movements while still considering all historical data. It also incorporates volatility bands, providing a "cloud" that visually highlights overbought or oversold conditions. By calculating the speed of mean reversion (θ) through the autocorrelation of log returns, this indicator offers traders a more nuanced and mathematically robust tool for identifying mean-reversion opportunities. These innovations make it especially useful for markets that exhibit range-bound characteristics, offering timely buy and sell signals based on statistical deviations from the mean.

🔸Adaptive Mean Calculation Traditional MA indicators use fixed lengths, which can lead to lagging signals or over-sensitivity in volatile markets. The Mean Reversion Cloud uses an Exponentially Weighted Moving Average (EWMA), which adapts to price movements by dynamically adjusting its calculation, offering a more responsive mean.

🔸Volatility-Based Cloud Unlike simple moving averages that only plot a single line, the Mean Reversion Cloud surrounds the dynamic mean with volatility bands. These bands, based on standard deviations, provide traders with a visual cue of when prices are statistically likely to revert, highlighting potential reversal zones.

🔸Speed of Reversion (θ) The indicator goes beyond price averages by calculating the speed at which the price reverts to the mean (θ), using the autocorrelation of log returns. This gives traders an additional tool for estimating the likelihood and timing of mean reversion, making the signals more reliable in practice.

🔶 FUNCTIONALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator is designed to detect potential mean-reversion opportunities in asset prices by applying the Ornstein-Uhlenbeck stochastic process. It calculates a dynamic mean through the Exponentially Weighted Moving Average (EWMA) and plots volatility bands based on the standard deviation of the asset's price over a specified period. These bands create a "cloud" that represents expected price fluctuations, helping traders to identify overbought or oversold conditions. By calculating the speed of reversion (θ) from the autocorrelation of log returns, the indicator offers a more refined way of assessing how quickly prices may revert to the mean. Additionally, the inclusion of volatility provides a comprehensive view of market conditions, allowing for more accurate buy and sell signals.

Let's dive into the details:

🔸Dynamic Mean and Volatility Bands The dynamic mean (μ) is calculated using the EWMA, giving more weight to recent prices but considering all historical data. This process closely resembles the Ornstein-Uhlenbeck (OU) process, which models the tendency of a stochastic variable (such as price) to revert to its mean over time. Volatility bands are plotted around the mean using standard deviation, forming the "cloud" that signals overbought or oversold conditions. The cloud adapts dynamically to price fluctuations and market volatility, making it a versatile tool for mean-reversion strategies. 🞘 How it works Step one: Calculate the dynamic mean (μ) The Ornstein-Uhlenbeck process describes how a variable, such as an asset's price, tends to revert to a long-term mean while subject to random fluctuations. In this indicator, the EWMA is used to compute the dynamic mean (μ), mimicking the mean-reverting behavior of the OU process. Use the EWMA formula to compute a weighted mean that adjusts to recent price movements. Assign exponentially decreasing weights to older data while giving more emphasis to current prices. Step two: Plot volatility bands Calculate the standard deviation of the price over a user-defined period to determine market volatility. Position the upper and lower bands around the mean by adding and subtracting a multiple of the standard deviation. 🞘 How to calculate Exponential Weighted Moving Average (EWMA)

The EWMA dynamically adjusts to recent price movements:

mu_t = lambda * mu_{t-1} + (1 - lambda) * P_t

Where mu_t is the mean at time t, lambda is the decay factor, and P_t is the price at time t. The higher the decay factor, the more weight is given to recent data.

Autocorrelation (ρ) and Standard Deviation (σ)

To measure mean reversion speed and volatility: rho = correlation(log(close), log(close ), length) Where rho is the autocorrelation of log returns over a specified period.

To calculate volatility:

sigma = stdev(close, length)

Where sigma is the standard deviation of the asset's closing price over a specified length.

Upper and Lower Bands

The upper and lower bands are calculated as follows:

upper_band = mu + (threshold * sigma)

lower_band = mu - (threshold * sigma)

Where threshold is a multiplier for the standard deviation, usually set to 2. These bands represent the range within which the price is expected to fluctuate, based on current volatility and the mean.

🞘 Code extract // Calculate Returns

returns = math.log(close / close )

// Calculate Long-Term Mean (μ) using EWMA over the entire dataset

var float ewma_mu = na // Initialize ewma_mu as 'na'

ewma_mu := na(ewma_mu ) ? close : decay_factor * ewma_mu + (1 - decay_factor) * close

mu = ewma_mu

// Calculate Autocorrelation at Lag 1

rho1 = ta.correlation(returns, returns , corr_length)

// Ensure rho1 is within valid range to avoid errors

rho1 := na(rho1) or rho1 <= 0 ? 0.0001 : rho1

// Calculate Speed of Mean Reversion (θ)

theta = -math.log(rho1)

// Calculate Volatility (σ)

sigma = ta.stdev(close, corr_length)

// Calculate Upper and Lower Bands

upper_band = mu + threshold * sigma

lower_band = mu - threshold * sigma

🔸Visualization via Table and Plotshapes

The table shows key statistics such as the current value of the dynamic mean (μ), the number of times the price has crossed the upper or lower bands, and the consecutive number of bars that the price has remained in an overbought or oversold state.

Plotshapes (diamonds) are used to signal buy and sell opportunities. A green diamond below the price suggests a buy signal when the price crosses below the lower band, and a red diamond above the price indicates a sell signal when the price crosses above the upper band.

The table and plotshapes provide a comprehensive visualization, combining both statistical and actionable information to aid decision-making.

🞘 Code extract // Reset consecutive_bars when price crosses the mean

var consecutive_bars = 0

if (close < mu and close >= mu) or (close > mu and close <= mu)

consecutive_bars := 0

else if math.abs(deviation) > 0

consecutive_bars := math.min(consecutive_bars + 1, dev_length)

transparency = math.max(0, math.min(100, 100 - (consecutive_bars * 100 / dev_length)))

🔶 INSTRUCTIONS

The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator can be set up by adding it to your TradingView chart and configuring parameters such as the decay factor, autocorrelation length, and volatility threshold to suit current market conditions. Look for price crossovers and deviations from the calculated mean for potential entry signals. Use the upper and lower bands as dynamic support/resistance levels for setting take profit and stop-loss orders. Combining this indicator with additional trend-following or momentum-based indicators can improve signal accuracy. Adjust settings for better mean-reversion detection and risk management.

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

Adding the Indicator to the Chart:

Go to your TradingView chart.

Click on the "Indicators" button at the top.

Search for "Mean Reversion Cloud (Ornstein-Uhlenbeck)" in the indicators list.

Click on the indicator to add it to your chart.

Configuring the Indicator:

Open the indicator settings by clicking on the gear icon next to its name on the chart.

Decay Factor: Adjust the decay factor (λ) to control the responsiveness of the mean calculation. A higher value prioritizes recent data.

Autocorrelation Length: Set the autocorrelation length (θ) for calculating the speed of mean reversion. Longer lengths consider more historical data.

Threshold: Define the number of standard deviations for the upper and lower bands to determine how far price must deviate to trigger a signal.

Chart Setup:

Select the appropriate timeframe (e.g., 1-hour, daily) based on your trading strategy.

Consider using other indicators such as RSI or MACD to confirm buy and sell signals.

🞘 Understanding What to Look For on the Chart

Indicator Behavior:

Observe how the price interacts with the dynamic mean and volatility bands. The price staying within the bands suggests mean-reverting behavior, while crossing the bands signals potential entry points.

The indicator calculates overbought/oversold conditions based on deviation from the mean, highlighted by color-coded cloud areas on the chart.

Crossovers and Deviation:

Look for crossovers between the price and the mean (μ) or the bands. A bullish crossover occurs when the price crosses below the lower band, signaling a potential buying opportunity.

A bearish crossover occurs when the price crosses above the upper band, suggesting a potential sell signal.

Deviations from the mean indicate market extremes. A large deviation indicates that the price is far from the mean, suggesting a potential reversal.

Slope and Direction:

Pay attention to the slope of the mean (μ). A rising slope suggests bullish market conditions, while a declining slope signals a bearish market.

The steepness of the slope can indicate the strength of the mean-reversion trend.

🞘 Possible Entry Signals

Bullish Entry:

Crossover Entry: Enter a long position when the price crosses below the lower band with a positive deviation from the mean.

Confirmation Entry: Use additional indicators like RSI (above 50) or increasing volume to confirm the bullish signal.

Bearish Entry:

Crossover Entry: Enter a short position when the price crosses above the upper band with a negative deviation from the mean.

Confirmation Entry: Look for RSI (below 50) or decreasing volume to confirm the bearish signal.

Deviation Confirmation:

Enter trades when the deviation from the mean is significant, indicating that the price has strayed far from its expected value and is likely to revert.

🞘 Possible Take Profit Strategies

Static Take Profit Levels:

Set predefined take profit levels based on historical volatility, using the upper and lower bands as guides.

Place take profit orders near recent support/resistance levels, ensuring you're capitalizing on the mean-reversion behavior.

Trailing Stop Loss: