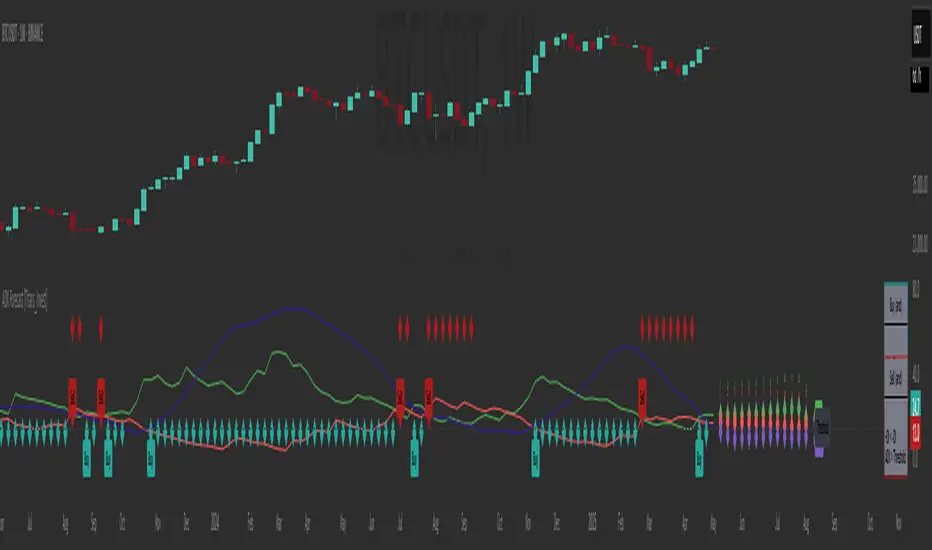

ADX Forecast [Titans_Invest]ADX Forecast

This isn’t just another ADX indicator — it’s the most powerful and complete ADX tool ever created, and without question the best ADX indicator on TradingView, possibly even the best in the world.

ADX Forecast represents a revolutionary leap in trend strength analysis, blending the timeless principles of the classic ADX with cutting-edge predictive modeling. For the first time on TradingView, you can anticipate future ADX movements using scientifically validated linear regression — a true game-changer for traders looking to stay ahead of trend shifts.

1. Real-Time ADX Forecasting

By applying least squares linear regression, ADX Forecast projects the future trajectory of the ADX with exceptional accuracy. This forecasting power enables traders to anticipate changes in trend strength before they fully unfold — a vital edge in fast-moving markets.

2. Unmatched Customization & Precision

With 26 long entry conditions and 26 short entry conditions, this indicator accounts for every possible ADX scenario. Every parameter is fully customizable, making it adaptable to any trading strategy — from scalping to swing trading to long-term investing.

3. Transparency & Advanced Visualization

Visualize internal ADX dynamics in real time with interactive tags, smart flags, and fully adjustable threshold levels. Every signal is transparent, logic-based, and engineered to fit seamlessly into professional-grade trading systems.

4. Scientific Foundation, Elite Execution

Grounded in statistical precision and machine learning principles, ADX Forecast upgrades the classic ADX from a reactive lagging tool into a forward-looking trend prediction engine. This isn’t just an indicator — it’s a scientific evolution in trend analysis.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the ADX, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an ADX time series like this:

Time →

ADX →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted ADX, which can be crossed with the actual ADX to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public ADX with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining ADX with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

ADX Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first ADX indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE ADX❓

The Average Directional Index (ADX) is a technical analysis indicator developed by J. Welles Wilder. It measures the strength of a trend in a market, regardless of whether the trend is up or down.

The ADX is an integral part of the Directional Movement System, which also includes the Plus Directional Indicator (+DI) and the Minus Directional Indicator (-DI). By combining these components, the ADX provides a comprehensive view of market trend strength.

⯁ HOW TO USE THE ADX❓

The ADX is calculated based on the moving average of the price range expansion over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and has three main zones:

• Strong Trend: When the ADX is above 25, indicating a strong trend.

• Weak Trend: When the ADX is below 20, indicating a weak or non-existent trend.

• Neutral Zone: Between 20 and 25, where the trend strength is unclear.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 +DI > -DI

🔹 +DI < -DI

🔹 +DI > ADX

🔹 +DI < ADX

🔹 -DI > ADX

🔹 -DI < ADX

🔹 ADX > Threshold

🔹 ADX < Threshold

🔹 +DI > Threshold

🔹 +DI < Threshold

🔹 -DI > Threshold

🔹 -DI < Threshold

🔹 +DI (Crossover) -DI

🔹 +DI (Crossunder) -DI

🔹 +DI (Crossover) ADX

🔹 +DI (Crossunder) ADX

🔹 +DI (Crossover) Threshold

🔹 +DI (Crossunder) Threshold

🔹 -DI (Crossover) ADX

🔹 -DI (Crossunder) ADX

🔹 -DI (Crossover) Threshold

🔹 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 +DI > -DI

🔸 +DI < -DI

🔸 +DI > ADX

🔸 +DI < ADX

🔸 -DI > ADX

🔸 -DI < ADX

🔸 ADX > Threshold

🔸 ADX < Threshold

🔸 +DI > Threshold

🔸 +DI < Threshold

🔸 -DI > Threshold

🔸 -DI < Threshold

🔸 +DI (Crossover) -DI

🔸 +DI (Crossunder) -DI

🔸 +DI (Crossover) ADX

🔸 +DI (Crossunder) ADX

🔸 +DI (Crossover) Threshold

🔸 +DI (Crossunder) Threshold

🔸 -DI (Crossover) ADX

🔸 -DI (Crossunder) ADX

🔸 -DI (Crossover) Threshold

🔸 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : ADX Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

ค้นหาในสคริปต์สำหรับ "curve"

RSI Full Forecast [Titans_Invest]RSI Full Forecast

Get ready to experience the ultimate evolution of RSI-based indicators – the RSI Full Forecast, a boosted and even smarter version of the already powerful: RSI Forecast

Now featuring over 40 additional entry conditions (forecasts), this indicator redefines the way you view the market.

AI-Powered RSI Forecasting:

Using advanced linear regression with the least squares method – a solid foundation for machine learning - the RSI Full Forecast enables you to predict future RSI behavior with impressive accuracy.

But that’s not all: this new version also lets you monitor future crossovers between the RSI and the MA RSI, delivering early and strategic signals that go far beyond traditional analysis.

You’ll be able to monitor future crossovers up to 20 bars ahead, giving you an even broader and more precise view of market movements.

See the Future, Now:

• Track upcoming RSI & RSI MA crossovers in advance.

• Identify potential reversal zones before price reacts.

• Uncover statistical behavior patterns that would normally go unnoticed.

40+ Intelligent Conditions:

The new layer of conditions is designed to detect multiple high-probability scenarios based on historical patterns and predictive modeling. Each additional forecast is a window into the price's future, powered by robust mathematics and advanced algorithmic logic.

Full Customization:

All parameters can be tailored to fit your strategy – from smoothing periods to prediction sensitivity. You have complete control to turn raw data into smart decisions.

Innovative, Accurate, Unique:

This isn’t just an upgrade. It’s a quantum leap in technical analysis.

RSI Full Forecast is the first of its kind: an indicator that blends statistical analysis, machine learning, and visual design to create a true real-time predictive system.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Full Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔹 RSI (Crossover) MA Forecast

🔹 RSI (Crossunder) MA Forecast

🔹 RSI Forecast 1 > MA Forecast 1

🔹 RSI Forecast 1 < MA Forecast 1

🔹 RSI Forecast 2 > MA Forecast 2

🔹 RSI Forecast 2 < MA Forecast 2

🔹 RSI Forecast 3 > MA Forecast 3

🔹 RSI Forecast 3 < MA Forecast 3

🔹 RSI Forecast 4 > MA Forecast 4

🔹 RSI Forecast 4 < MA Forecast 4

🔹 RSI Forecast 5 > MA Forecast 5

🔹 RSI Forecast 5 < MA Forecast 5

🔹 RSI Forecast 6 > MA Forecast 6

🔹 RSI Forecast 6 < MA Forecast 6

🔹 RSI Forecast 7 > MA Forecast 7

🔹 RSI Forecast 7 < MA Forecast 7

🔹 RSI Forecast 8 > MA Forecast 8

🔹 RSI Forecast 8 < MA Forecast 8

🔹 RSI Forecast 9 > MA Forecast 9

🔹 RSI Forecast 9 < MA Forecast 9

🔹 RSI Forecast 10 > MA Forecast 10

🔹 RSI Forecast 10 < MA Forecast 10

🔹 RSI Forecast 11 > MA Forecast 11

🔹 RSI Forecast 11 < MA Forecast 11

🔹 RSI Forecast 12 > MA Forecast 12

🔹 RSI Forecast 12 < MA Forecast 12

🔹 RSI Forecast 13 > MA Forecast 13

🔹 RSI Forecast 13 < MA Forecast 13

🔹 RSI Forecast 14 > MA Forecast 14

🔹 RSI Forecast 14 < MA Forecast 14

🔹 RSI Forecast 15 > MA Forecast 15

🔹 RSI Forecast 15 < MA Forecast 15

🔹 RSI Forecast 16 > MA Forecast 16

🔹 RSI Forecast 16 < MA Forecast 16

🔹 RSI Forecast 17 > MA Forecast 17

🔹 RSI Forecast 17 < MA Forecast 17

🔹 RSI Forecast 18 > MA Forecast 18

🔹 RSI Forecast 18 < MA Forecast 18

🔹 RSI Forecast 19 > MA Forecast 19

🔹 RSI Forecast 19 < MA Forecast 19

🔹 RSI Forecast 20 > MA Forecast 20

🔹 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔸 RSI (Crossover) MA Forecast

🔸 RSI (Crossunder) MA Forecast

🔸 RSI Forecast 1 > MA Forecast 1

🔸 RSI Forecast 1 < MA Forecast 1

🔸 RSI Forecast 2 > MA Forecast 2

🔸 RSI Forecast 2 < MA Forecast 2

🔸 RSI Forecast 3 > MA Forecast 3

🔸 RSI Forecast 3 < MA Forecast 3

🔸 RSI Forecast 4 > MA Forecast 4

🔸 RSI Forecast 4 < MA Forecast 4

🔸 RSI Forecast 5 > MA Forecast 5

🔸 RSI Forecast 5 < MA Forecast 5

🔸 RSI Forecast 6 > MA Forecast 6

🔸 RSI Forecast 6 < MA Forecast 6

🔸 RSI Forecast 7 > MA Forecast 7

🔸 RSI Forecast 7 < MA Forecast 7

🔸 RSI Forecast 8 > MA Forecast 8

🔸 RSI Forecast 8 < MA Forecast 8

🔸 RSI Forecast 9 > MA Forecast 9

🔸 RSI Forecast 9 < MA Forecast 9

🔸 RSI Forecast 10 > MA Forecast 10

🔸 RSI Forecast 10 < MA Forecast 10

🔸 RSI Forecast 11 > MA Forecast 11

🔸 RSI Forecast 11 < MA Forecast 11

🔸 RSI Forecast 12 > MA Forecast 12

🔸 RSI Forecast 12 < MA Forecast 12

🔸 RSI Forecast 13 > MA Forecast 13

🔸 RSI Forecast 13 < MA Forecast 13

🔸 RSI Forecast 14 > MA Forecast 14

🔸 RSI Forecast 14 < MA Forecast 14

🔸 RSI Forecast 15 > MA Forecast 15

🔸 RSI Forecast 15 < MA Forecast 15

🔸 RSI Forecast 16 > MA Forecast 16

🔸 RSI Forecast 16 < MA Forecast 16

🔸 RSI Forecast 17 > MA Forecast 17

🔸 RSI Forecast 17 < MA Forecast 17

🔸 RSI Forecast 18 > MA Forecast 18

🔸 RSI Forecast 18 < MA Forecast 18

🔸 RSI Forecast 19 > MA Forecast 19

🔸 RSI Forecast 19 < MA Forecast 19

🔸 RSI Forecast 20 > MA Forecast 20

🔸 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Full Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

RSI Forecast [Titans_Invest]RSI Forecast

Introducing one of the most impressive RSI indicators ever created – arguably the best on TradingView, and potentially the best in the world.

RSI Forecast is a visionary evolution of the classic RSI, merging powerful customization with groundbreaking predictive capabilities. While preserving the core principles of traditional RSI, it takes analysis to the next level by allowing users to anticipate potential future RSI movements.

Real-Time RSI Forecasting:

For the first time ever, an RSI indicator integrates linear regression using the least squares method to accurately forecast the future behavior of the RSI. This innovation empowers traders to stay one step ahead of the market with forward-looking insight.

Highly Customizable:

Easily adapt the indicator to your personal trading style. Fine-tune a variety of parameters to generate signals perfectly aligned with your strategy.

Innovative, Unique, and Powerful:

This is the world’s first RSI Forecast to apply this predictive approach using least squares linear regression. A truly elite-level tool designed for traders who want a real edge in the market.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first RSI indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Average Yield InversionDescription:

This script calculates and visualizes the average yield curve spread to identify whether the yield curve is inverted or normal. It takes into account short-term yields (1M, 3M, 6M, 2Y) and long-term yields (10Y, 30Y).

Positive values: The curve is normal, indicating long-term yields are higher than short-term yields. This often reflects economic growth expectations.

Negative values: The curve is inverted, meaning short-term yields are higher than long-term yields, a potential signal of economic slowdown or recession.

Key Features:

Calculates the average spread between long-term and short-term yields.

Displays a clear graph with a zero-line reference for quick interpretation.

Useful for tracking macroeconomic trends and potential market turning points.

This tool is perfect for investors, analysts, and economists who need to monitor yield curve dynamics at a glance.

[Sharpe projection SGM]Dynamic Support and Resistance: Traces adjustable support and resistance lines based on historical prices, signaling new market barriers.

Price Projections and Volatility: Calculates future price projections using moving averages and plots annualized standard deviation-based volatility bands to anticipate price dispersion.

Intuitive Coloring: Colors between support and resistance lines show up or down trends, making it easy to analyze quickly.

Analytics Dashboard: Displays key metrics such as the Sharpe Ratio, which measures average ROI adjusted for asset volatility

Volatility Management for Options Trading: The script helps evaluate strike prices and strategies for options, based on support and resistance levels and projected volatility.

Importance of Diversification: It is necessary to diversify investments to reduce risks and stabilize returns.

Disclaimer on Past Performance: Past performance does not guarantee future results, projections should be supplemented with other analyses.

The script settings can be adjusted according to the specific needs of each user.

The mean and standard deviation are two fundamental statistical concepts often represented in a Gaussian curve, or normal distribution. Here's a quick little lesson on these concepts:

Average

The mean (or arithmetic mean) is the result of the sum of all values in a data set divided by the total number of values. In a data distribution, it represents the center of gravity of the data points.

Standard Deviation

The standard deviation measures the dispersion of the data relative to its mean. A low standard deviation indicates that the data is clustered near the mean, while a high standard deviation shows that it is more spread out.

Gaussian curve

The Gaussian curve or normal distribution is a graphical representation showing the probability of distribution of data. It has the shape of a symmetrical bell centered on the middle. The width of the curve is determined by the standard deviation.

68-95-99.7 rule (rule of thumb): Approximately 68% of the data is within one standard deviation of the mean, 95% is within two standard deviations, and 99.7% is within three standard deviations.

In statistics, understanding the mean and standard deviation allows you to infer a lot about the nature of the data and its trends, and the Gaussian curve provides an intuitive visualization of this information.

In finance, it is crucial to remember that data dispersion can be more random and unpredictable than traditional statistical models like the normal distribution suggest. Financial markets are often affected by unforeseen events or changes in investor behavior, which can result in return distributions with wider standard deviations or non-symmetrical distributions.

The Investment ClockThe Investment Clock was most likely introduced to the general public in a research paper distributed by Merrill Lynch. It’s a simple yet useful framework for understanding the various stages of the US economic cycle and which asset classes perform best in each stage.

The Investment Clock splits the business cycle into four phases, where each phase is comprised of the orientation of growth and inflation relative to their sustainable levels:

Reflation phase (6:01 to 8:59): Growth is sluggish and inflation is low. This phase occurs during the heart of a bear market. The economy is plagued by excess capacity and falling demand. This keeps commodity prices low and pulls down inflation. The yield curve steepens as the central bank lowers short-term rates in an attempt to stimulate growth and inflation. Bonds are the best asset class in this phase.

Recovery phase (9:01 to 11:59): The central bank’s easing takes effect and begins driving growth to above the trend rate. Though growth picks up, inflation remains low because there’s still excess capacity. Rising growth and low inflation are the Goldilocks phase of every cycle. Stocks are the best asset class in this phase.

Overheat phase(12:01 to 2:59): Productivity growth slows and the GDP gap closes causing the economy to bump up against supply constraints. This causes inflation to rise. Rising inflation spurs the central banks to hike rates. As a result, the yield curve begins flattening. With high growth and high inflation, stocks still perform but not as well as in recovery. Volatility returns as bond yields rise and stocks compete with higher yields for capital flows. In this phase, commodities are the best asset class.

Stagflation phase (3:01 to 5:59): GDP growth slows but inflation remains high (sidenote: most bear markets are preceded by a 100%+ increase in the price of oil which drives inflation up and causes central banks to tighten). Productivity dives and a wage-price spiral develops as companies raise prices to protect compressing margins. This goes on until there’s a steep rise in unemployment which breaks the cycle. Central banks keep rates high until they reign in inflation. This causes the yield curve to invert. During this phase, cash is the best asset.

Additional notes from Merrill Lynch:

Cyclicality: When growth is accelerating (12 o'clock), Stocks and Commodities do well. Cyclical sectors like Tech or Steel outperform. When growth is slowing (6 o'clock), Bonds, Cash, and defensives outperform.

Duration: When inflation is falling (9 o'clock), discount rates drop and financial assets do well. Investors pay up for long duration Growth stocks. When inflation is rising (3 o'clock), real assets like Commodities and Cash do best. Pricing power is plentiful and short-duration Value stocks outperform.

Interest Rate-Sensitives: Banks and Consumer Discretionary stocks are interest-rate sensitive “early cycle” performers, doing best in Reflation and Recovery when central banks are easing and growth is starting to recover.

Asset Plays: Some sectors are linked to the performance of an underlying asset. Insurance stocks and Investment Banks are often bond or equity price sensitive, doing well in the Reflation or Recovery phases. Mining stocks are metal price-sensitive, doing well during an Overheat.

About the indicator:

This indicator suggests iShares ETFs for sector rotation analysis. There are likely other ETFs to consider which have lower fees and are outperforming their sector peers.

You may get errors if your chart is set to a different timeframe & ticker other than 1d for symbol/tickers GDPC1 or CPILFESL.

Investment Clock settings are based on a "sustainable level" of growth and inflation, which are each slightly subjective depending on the economist and probably have changed since the last time this indicator was updated. Hence, the sustainable levels are customizable in the settings. When I was formally educated I was trained to use average CPI of 3.1% for financial planning purposes, the default for the indicator is 2.5%, and the Medium article backtested and optimized a 2% sustainable inflation rate. Again, user-defined sustainable growth and rates are slightly subjective and will affect results.

I have not been trained or even had much experience with MetaTrader code, which is how this indicator was originally coded. See the original Medium article that inspired this indicator if you want to audit & compare code.

Hover over info panel for detailed information.

Features: Advanced info panel that performs Investment Clock analysis and offers additional hover info such as sector rotation suggestions. Customizable sustainable levels, growth input, and inflation input. Phase background coloring.

⚠ DISCLAIMER: Not financial advice. Not a trading system. DYOR. I am not affiliated with Medium, Macro Ops, iShares, or Merrill Lynch.

About the Author: I am a patent-holding inventor, a futures trader, a hobby PineScripter, and a former FINRA Registered Representative.

Delta Agnostic Correlation CoefficientVisually see how well a symbol tracks another's movements, without taking price deltas into account.

For example, a 1% move on the index and a 5% move on the target will return a DCC value of 1. An index move of 0.5% on the index and a 10% move on the target will also return a DCC value of 1. The same happens for downward moves.

The SMA value can be set to smooth the curve. A larger value creates a smoother curve.

BTC - Power Law 1.5: Dynamic 50/50 Decay OVERVIEW

Most Bitcoin models treat the asset as if it exists in a vacuum of infinite exponential growth. The classical Power Law (v1.0) was a groundbreaking start, but as Bitcoin matures into a multi-trillion dollar institutional asset, our models must account for the laws of physics and liquidity. The Power Law 1.5: Dynamic 50/50 Decay is a second-generation structural engine. It doesn't just draw a line; it calculates the structural "Center of Gravity" of Bitcoin’s adoption curve while accounting for the natural maturation (decay) of the network’s growth speed.

THE MATHEMATICAL BACKBONE: QUANTILE MEDIAN CALCULATION

The "Fair Value" line (blue) is derived using a Log-Log Linear Regression focused on the 50th percentile (Median). The script first transforms the price and the time (days since the Genesis Block) into a logarithmic scale. It then calculates a power-law constant by finding the Absolute Least Deviation across the entire historical dataset since 2011. Specifically, it uses the formula: Price = 10^(Intercept + Slope * log10(Days)) . To ensure the line is a true median, the script calculates the Median Offset of every historical price point from the raw regression line. By shifting the intercept by this median value, we guarantee that exactly 50% of all weekly bars fall above the curve and 50% fall below it, creating a robust, non-biased structural center.

THE ALPHA SHADOW: DYNAMIC EXPONENT PROJECTION

Unlike standard power-law projections that rely on a static slope, the "Alpha Shadow" (the projection extending from the blue backbone) utilizes a Time-Varying Exponent Model . The model acknowledges that Bitcoin's growth speed—the exponent 'b'—is a decaying function of time, reflecting the diminishing returns of a maturing asset. The script recalculated the Instantaneous Slope on every single bar using the formula: Future_Slope = Initial_Slope - (Decay_Rate * log10(Total_Days_from_Genesis)) . While the Decay Rate (default 0.045) serves as a structural sensitivity constant, its application ensures the growth speed is a dynamic variable rather than a fixed number. Each segment of the dashed green "Shadow" is a unique power-law arc calculated for its specific future time window. This ensures the projection isn't just a straight line drawn on a log chart, but a mathematically tethered curve that "feels" the weight of increasing market capitalization and respects the reality of global liquidity constraints as we approach 2029.

HOW TO READ THE CHART

• The Backbone (Solid Blue): This is the 50/50 Fair Value. When price is below this line, Bitcoin is structurally "cheap." When price is far above it, the asset is in a state of cyclical expansion.

• The Alpha Shadow (Green): This is the mathematical projection of the current curve into 2029. It shows the path of "Fair Value" as the network continues to mature.

• The Regime Audit (Dashboard): A real-time table in the middle-right of your chart provides an audit of the model's integrity, including the current slope (b) and the projected Fair Price for Jan 1, 2029.

WHY THIS IS "FRESH"

Most open-source Power Law scripts on TradingView utilize a Static Linear Regression —calculating a single constant slope that is applied equally to 2011 and 2029. Furthermore, common community models often rely on "Outer Band" fitting (connecting historical cycle peaks to cycle lows). While visually appealing, these methods can be highly sensitive to "Black Swan" outliers and often assume Bitcoin’s growth velocity is a permanent constant.

This script stands out by introducing a Maturation Framework . Instead of fitting to volatile extremes, we anchor the logic to a 50/50 Quantile Median , creating a backbone that is mathematically centered regardless of cyclical noise. By then applying a Dynamic Decay Factor to the growth exponent, we move away from the "static bands" approach and toward a model that respects the physical reality of a maturing, multi-trillion-dollar asset class. This provides a structurally grounded, institutional-grade view of Bitcoin’s trajectory that accounts for the diminishing returns inherent in global adoption.

DISCLAIMER

This script is for educational and macro-analytical purposes only. It does not constitute financial advice. The 2029 projection is a mathematical extrapolation based on historical data and decay constants; it is not a guarantee of future price action.

TAGS

bitcoin, powerlaw, macro, regression, fairvalue, btc, projection, quantitative, math, structural, Rob Maths, robmaths, Rob_Maths

Cup & Handle Finder [theUltimator5]Cup & Handle Finder automatically scans your chart for Cup and Cup & Handle patterns—both bullish and bearish—and draws the structure when it meets quality rules. By default, the pattern detection is extremely strict, so it is very likely that no patterns will plot. This is intentional to reduce noise.

This indicator uses a unique cup detection algorithm that creates an ideal "cup" pattern algorithmically then checks whether or not the chart pattern fits within the ideal pattern with a margin of error that is user defined.

Think of it as two curves - an upper bound and a lower bound. If the chart stays between the upper and lower bound curves (and some other extra checks), it gets identified as a cup.

Once a cup is detected, it starts looking for a handle, which uses a secondary set of criteria. If all the criteria for the handle are met, then the cup and handle is confirmed, and a green arrow plots at the entry point.

If a handle starts to form and then doesn't confirm, a label is plotted that shows it was a failed cup and handle pattern.

If the handle confirms, a label plots that shows it was a confirmed pattern, plus the green arrow.

By default, cup patterns don't plot. You can toggle on cup patterns (cups that didn't continue into a handle pattern)

Key inputs

Minimum / Maximum Lookback: Controls the cup sizes (in bars) the scanner searches.

Breakout Source (Close vs High/Low): Close = stricter; High/Low = more sensitive.

Contained Bar Rate %: Main quality filter. Higher = fewer, cleaner patterns.

Show toggles: Cups, Cup & Handles, Failed Handles, Confirmation Triangles.

Direction filters: Enable Bullish Cups / Enable Bearish Cups.

Colors: Separate styling for bullish/bearish cups, handles, and confirmed/rejected states.

Alerts

Bullish/Bearish Cup Found

Bullish/Bearish Cup & Handle Detected

Bullish/Bearish Cup & Handle Confirmed

Use as a structure/scan tool and pair with your own confirmation and risk management

VX Term StructureThe VX Term Structure Monitor is an advanced visualization tool designed specifically for volatility traders who need to instantly recognize shifts in market structure. By comparing the current VIX Futures Term Structure against the previous trading day's close, this indicator provides a clear, real-time* view of the VIX Spot Index and the next available VX futures contracts. A key visual feature is the "Daily Drift" analysis, which automatically highlights the difference between today's curve (Cyan) and yesterday's curve (Gray/Dashed) with red or green fills, allowing you to immediately spot whether volatility is rising or falling across the term structure.

Unlike standard indicators that rely solely on the Spot price, this script utilizes professional-grade logic to classify market stress into three distinct stages. It identifies a normal Contango environment (Green) when the Front Month (M1) is trading below the Second Month (M2), indicating a calm market where long volatility positions typically suffer from negative roll yield. The system issues a Spot Warning (Orange) if the Spot index overheats and exceeds M1 while the futures curve remains in Contango, often an early signal of building stress. Finally, it detects critical Backwardation (Red) when the futures curve physically inverts (M1 > M2), signaling that market participants are paying a premium for immediate protection.

Usage Note: Due to technical limitations in detecting contract expirations automatically, users must manually select the current "Front Month" contract (e.g., "G (Feb)") in the indicator settings to ensure correct alignment. Users can also configure server-side alerts to trigger specifically when the market flips into Backwardation.

*Note: To view real-time data for VX futures, a paid data subscription to CBOE (CFE) is required on TradingView. Otherwise, the data may be delayed.

Disclaimer: This tool is for educational and informational purposes only and does not constitute financial advice.

Bloomberg Mega Board [v2.5 Fixed]Transform your TradingView chart into a professional-grade command center. Designed for traders who need high-level market awareness without switching tabs, this dashboard provides deep, multi-timeframe analysis across US Sectors, Commodities, Currencies, and Crypto.

Key Features

1. Multi-Asset Paging System Pine Script has a limit of 40 security calls, which usually limits how much data you can see. This script bypasses that limitation using a smart Paging System:

Sectors Page: Tracks the top 10 US Sectors (SPY, XLK, XLF, etc.) & Indices.

Commodities Page: Gold, Silver, Oil, Gas, Copper, Corn, etc.

Currencies Page: Major Forex pairs including DXY, EURUSD, USDJPY.

Crypto Page: Top 10 Cryptocurrencies by volume.

Switch pages instantly via the Settings menu.

2. Smart "News" Headlines Since Pine Script cannot access the live internet for news, this script uses an Algorithmic Headline Generator. It analyzes price action and trend alignment to generate a "Market Status" summary:

Full Bull Trend: Intraday + Daily + Weekly trends are all positive.

Strong Rally: Asset is up significantly (>1.25%) on the day.

Heavy Sell-off: Asset is down significantly (<-1.25%) on the day.

Pullback (Buy?): Daily trend is UP, but Intraday is DOWN (potential entry).

Consolidating: Market is chopping sideways.

3. Timeframe Trend Matrix Monitor momentum across the curve with a single glance. The "Trend" columns are powered by the 5 EMA (Exponential Moving Average):

Intraday: Adapts to your current chart timeframe (e.g., switch your chart to 15m to see the 15m trend).

Daily / Weekly / Monthly: These are hard coded to always show the higher timeframe trend, regardless of what chart you are looking at. Trend is determined by price in relation to it's 5 EMA.

4. "Terminal" Aesthetic

Styled with a dark, high-contrast Bloomberg Terminal look.

Uses Amber tickers and Neon status blocks for rapid visual scanning.

Optimized for Full Screen Mode: Hide your main chart candles to turn your monitor into a dedicated data dashboard.

How to Use

Add the indicator to your chart and move it to "New Lower Indicator" Then repeat 4 times for each dashboard.

Open Settings (the gear icon) and find "Select Page".

Choose your desired market view (e.g., Sectors, Crypto, Currencies, Commodities)

Optional: To replicate the full dashboard look, go to your Chart Settings -> Symbol -> Uncheck "Body" and "Borders" to hide the candles behind the table.

2 hours ago

Release Notes

Transform your TradingView chart into a professional-grade command center. Designed for traders who need high-level market awareness without switching tabs, this dashboard provides deep, multi-timeframe analysis across US Sectors, Commodities, Currencies, and Crypto.

Key Features

1. Multi-Asset Paging System Pine Script has a limit of 40 security calls, which usually limits how much data you can see. This script bypasses that limitation using a smart Paging System:

Sectors Page: Tracks the top 10 US Sectors (SPY, XLK, XLF, etc.) & Indices.

Commodities Page: Gold, Silver, Oil, Gas, Copper, Corn, etc.

Currencies Page: Major Forex pairs including DXY, EURUSD, USDJPY.

Crypto Page: Top 10 Cryptocurrencies by volume.

Switch pages instantly via the Settings menu.

2. Smart "News" Headlines Since Pine Script cannot access the live internet for news, this script uses an Algorithmic Headline Generator. It analyzes price action and trend alignment to generate a "Market Status" summary:

Full Bull Trend: Intraday + Daily + Weekly trends are all positive.

Strong Rally: Asset is up significantly (>1.25%) on the day.

Heavy Sell-off: Asset is down significantly (<-1.25%) on the day.

Pullback (Buy?): Daily trend is UP, but Intraday is DOWN (potential entry).

Consolidating: Market is chopping sideways.

3. Timeframe Trend Matrix Monitor momentum across the curve with a single glance. The "Trend" columns are powered by the 5 EMA (Exponential Moving Average):

Intraday: Adapts to your current chart timeframe (e.g., switch your chart to 15m to see the 15m trend).

Daily / Weekly / Monthly: These are hard coded to always show the higher timeframe trend, regardless of what chart you are looking at. Trend is determined by price in relation to it's 5 EMA.

4. "Terminal" Aesthetic

Styled with a dark, high-contrast Bloomberg Terminal look.

Uses Amber tickers and Neon status blocks for rapid visual scanning.

Optimized for Full Screen Mode: Hide your main chart candles to turn your monitor into a dedicated data dashboard.

How to Use

Add the indicator to your chart and move it to "New Lower Indicator" Then repeat 4 times for each dashboard.

Open Settings (the gear icon) and find "Select Page".

Choose your desired market view (e.g., Sectors, Crypto, Currencies, Commodities)

Optional: To replicate the full dashboard look, go to your Chart Settings -> Symbol -> Uncheck "Body" and "Borders" to hide the candles behind the table.

2 hours ago

Release Notes

Transform your TradingView chart into a professional-grade command center. Designed for traders who need high-level market awareness without switching tabs, this dashboard provides deep, multi-timeframe analysis across US Sectors, Commodities, Currencies, and Crypto.

Key Features

1. Multi-Asset Paging System Pine Script has a limit of 40 security calls, which usually limits how much data you can see. This script bypasses that limitation using a smart Paging System:

Sectors Page: Tracks the top 10 US Sectors (SPY, XLK, XLF, etc.) & Indices.

Commodities Page: Gold, Silver, Oil, Gas, Copper, Corn, etc.

Currencies Page: Major Forex pairs including DXY, EURUSD, USDJPY.

Crypto Page: Top 10 Cryptocurrencies by volume.

Switch pages instantly via the Settings menu.

2. Smart "News" Headlines Since Pine Script cannot access the live internet for news, this script uses an Algorithmic Headline Generator. It analyzes price action and trend alignment to generate a "Market Status" summary:

Full Bull Trend: Intraday + Daily + Weekly trends are all positive.

Strong Rally: Asset is up significantly (>1.25%) on the day.

Heavy Sell-off: Asset is down significantly (<-1.25%) on the day.

Pullback (Buy?): Daily trend is UP, but Intraday is DOWN (potential entry).

Consolidating: Market is chopping sideways.

3. Timeframe Trend Matrix Monitor momentum across the curve with a single glance. The "Trend" columns are powered by the 5 EMA (Exponential Moving Average):

Intraday: Adapts to your current chart timeframe (e.g., switch your chart to 15m to see the 15m trend).

Daily / Weekly / Monthly: These are hard coded to always show the higher timeframe trend, regardless of what chart you are looking at. Trend is determined by price in relation to it's 5 EMA.

4. "Terminal" Aesthetic

Styled with a dark, high-contrast Bloomberg Terminal look.

Uses Amber tickers and Neon status blocks for rapid visual scanning.

Optimized for Full Screen Mode: Hide your main chart candles to turn your monitor into a dedicated data dashboard.

How to Use

Add the indicator to your chart and move it to "New Lower Indicator" Then repeat 4 times for each dashboard.

Open Settings (the gear icon) and find "Select Page".

Choose your desired market view (e.g., Sectors, Crypto, Currencies, Commodities)

Optional: To replicate the full dashboard look, go to your Chart Settings -> Symbol -> Uncheck "Body" and "Borders" to hide the candles behind the table.

2 hours ago

Release Notes

Transform your TradingView chart into a professional-grade command center. Designed for traders who need high-level market awareness without switching tabs, this dashboard provides deep, multi-timeframe analysis across US Sectors, Commodities, Currencies, and Crypto.

Key Features

1. Multi-Asset Paging System Pine Script has a limit of 40 security calls, which usually limits how much data you can see. This script bypasses that limitation using a smart Paging System:

Sectors Page: Tracks the top 10 US Sectors (SPY, XLK, XLF, etc.) & Indices.

Commodities Page: Gold, Silver, Oil, Gas, Copper, Corn, etc.

Currencies Page: Major Forex pairs including DXY, EURUSD, USDJPY.

Crypto Page: Top 10 Cryptocurrencies by volume.

Switch pages instantly via the Settings menu.

2. Smart "News" Headlines Since Pine Script cannot access the live internet for news, this script uses an Algorithmic Headline Generator. It analyzes price action and trend alignment to generate a "Market Status" summary:

Full Bull Trend: Intraday + Daily + Weekly trends are all positive.

Strong Rally: Asset is up significantly (>1.25%) on the day.

Heavy Sell-off: Asset is down significantly (<-1.25%) on the day.

Pullback (Buy?): Daily trend is UP, but Intraday is DOWN (potential entry).

Consolidating: Market is chopping sideways.

3. Timeframe Trend Matrix Monitor momentum across the curve with a single glance. The "Trend" columns are powered by the 5 EMA (Exponential Moving Average):

Intraday: Adapts to your current chart timeframe (e.g., switch your chart to 15m to see the 15m trend).

Daily / Weekly / Monthly: These are hard coded to always show the higher timeframe trend, regardless of what chart you are looking at. Trend is determined by price in relation to it's 5 EMA.

4. "Terminal" Aesthetic

Styled with a dark, high-contrast Bloomberg Terminal look.

Uses Amber tickers and Neon status blocks for rapid visual scanning.

Optimized for Full Screen Mode: Hide your main chart candles to turn your monitor into a dedicated data dashboard.

How to Use

Add the indicator to your chart and move it to "New Lower Indicator" Then repeat 4 times for each dashboard.

Open Settings (the gear icon) and find "Select Page".

Choose your desired market view (e.g., Sectors, Crypto, Currencies, Commodities)

Optional: To replicate the full dashboard look, go to your Chart Settings -> Symbol -> Uncheck "Body" and "Borders" to hide the candles behind the table.

Macro Return ForecastWhen the macro environment was similar, what annualized return did the market usually deliver next?

Before using the indicator, make sure your chart is set to any US-market symbol (SPX, QQQ, DIA, etc.).

This requirement is simple: the indicator pulls macro series from US data (yields, TIPS, credit spreads, breadth of US indices).

Because these series are independent from the chart’s price series, the chart symbol itself does not affect the internal calculations.

Any US symbol works, and the output of the model will be identical as long as you are on a US asset with daily, weekly or monthly timeframe.

The plotted price does not matter: the macro engine is fully exogenous to the chart symbol.

1. What the indicator does relative to selected assets

In the settings you choose which market you want to analyze:

- S&P500

- Nasdaq or NQ100

- Dow Jones

- Russell 2000

- US-wide (VTI)

- S&P500 sectors (XLF, XLY, XLP, etc.)

For each one, the indicator loads:

- Its internal breadth series (percentage of constituents above MA200)

- Its price history to compute forward log-returns at multiple horizons

- Its regime position relative to its own MA200 (for bull/bear filtering)

This means the tool is not tied to the chart symbol you display.

If your chart is SPX but the indicator setting is “S&P500 Technology”, the expected return projection is computed for the Technology sector using its own data, not the chart’s data.

You can therefore:

- Visualize macro-driven expected returns for any major US index or sector.

- Compare how different parts of the market historically reacted to similar macro states.

- Switch assets instantly to see which segment historically behaved better in comparable macro conditions.

The indicator becomes an analyzer of macro sensitivity, not a chart-dependent indicator.

2. Method overview

The model answers a statistical question:

“When macro conditions looked like they do today, what forward annualized return did this asset usually deliver?”

To do this it combines four macro pillars:

- Market breadth of the selected asset

- Yield curve slope (US 10Y minus 2Y)

- US credit spread (high yield minus gov)

- US real rate (TIPS 10Y)

It normalizes each metric into a 0–100 score, groups similar historical states into bins, and examines what the asset did next across six horizons (from ~9 months to ~5 years).

This produces a historical map connecting macro states to realized forward returns.

It is not a forecast model.

It is a conditional-distribution estimator: it tells you what has historically happened from similar setups.

3. Why this produces useful insights on assets

For any chosen asset (SPX, Nasdaq, sectors…), the indicator computes:

- Its forward return distribution in similar macro states.

- How often these states occurred (n).

- Whether the macro environment that preceded positive returns in the past resembles today’s.

- Whether the asset tends to be more sensitive or more resilient than the broad index under given macro configurations.

- Whether a given sector historically benefited from specific yield-curve, credit or real-rate environments.

This lets you answer questions such as:

- Does this sector usually outperform in an inverted yield curve environment?

- Does the Nasdaq historically recover strongly after breadth collapses?

- How did the S&P500 behave historically when real rates were this high?

- Is today’s credit-spread environment typically associated with positive or negative forward returns for this index?

These insights are not predictions but statistical context backed by past market behavior.

4. Why the technique is robust (and why it matters)

The engine uses strict, non-optimistic data processing:

- Winsorization of returns to neutralize extreme outliers without deleting information.

- Shrinkage estimators to avoid overfitting when bins contain few occurrences.

- Adaptive or static bounds for scaling macro indicators, ensuring comparability across cycles.

- Inverse-variance weighting of horizons with penalties for horizon redundancy.

- HAC-style adjustments to reduce autocorrelation bias in return estimation.

Each method aims to prevent artificial inflation of expected-return values and to keep the estimator stable even in unusual macro states.

This produces a result that is not “optimistic”, not curve-fit, not dependent on chart tricks, and not sensitive to isolated historical anomalies.

5. What you get as a user

A single clean line:

Expected Annual Return (%)

This line reflects how the chosen asset historically performed after macro environments similar to today’s.

The color gradient and confidence indicator (n) show the density of comparable episodes in history.

This makes the output extremely simple to read:

- High, stable expectation: historically supportive macro environment.

- Low or negative expectation: historically weaker environments.

- Low confidence: the macro state is rare and historical comparisons are limited.

The tool therefore adds context, not signals.

It helps you understand the environment the asset is currently in, based on how markets behaved in similar conditions across US market history.

LapseBacktestingTableLibrary "LapseBacktestingMetrics"

This library provides a robust set of quantitative backtesting and performance evaluation functions for Pine Script strategies. It’s designed to help traders, quants, and developers assess risk, return, and robustness through detailed statistical metrics — including Sharpe, Sortino, Omega, drawdowns, and trade efficiency.

Built to enhance any trading strategy’s evaluation framework, this library allows you to visualize performance with the quantlapseTable() function, producing an interactive on-chart performance table.

Credit to EliCobra and BikeLife76 for original concept inspiration.

curve(disp_ind)

Retrieves a selected performance curve of your strategy.

Parameters:

disp_ind (simple string): Type of curve to plot. Options include "Equity", "Open Profit", "Net Profit", "Gross Profit".

Returns: (float) Corresponding performance curve value.

cleaner(disp_ind, plot)

Filters and displays selected strategy plots for clean visualization.

Parameters:

disp_ind (simple string): Type of display.

plot (simple float): Strategy plot variable.

Returns: (float) Filtered plot value.

maxEquityDrawDown()

Calculates the maximum equity drawdown during the strategy’s lifecycle.

Returns: (float) Maximum equity drawdown percentage.

maxTradeDrawDown()

Computes the worst intra-trade drawdown among all closed trades.

Returns: (float) Maximum intra-trade drawdown percentage.

consecutive_wins()

Finds the highest number of consecutive winning trades.

Returns: (int) Maximum consecutive wins.

consecutive_losses()

Finds the highest number of consecutive losing trades.

Returns: (int) Maximum consecutive losses.

no_position()

Counts the maximum consecutive bars where no position was held.

Returns: (int) Maximum flat days count.

long_profit()

Calculates total profit generated by long positions as a percentage of initial capital.

Returns: (float) Total long profit %.

short_profit()

Calculates total profit generated by short positions as a percentage of initial capital.

Returns: (float) Total short profit %.

prev_month()

Measures the previous month’s profit or loss based on equity change.

Returns: (float) Monthly equity delta.

w_months()

Counts the number of profitable months in the backtest.

Returns: (int) Total winning months.

l_months()

Counts the number of losing months in the backtest.

Returns: (int) Total losing months.

checktf()

Returns the time-adjusted scaling factor used in Sharpe and Sortino ratio calculations based on chart timeframe.

Returns: (float) Annualization multiplier.

stat_calc()

Performs complete statistical computation including drawdowns, Sharpe, Sortino, Omega, trade stats, and profit ratios.

Returns: (array)

.

f_colors(x, nv)

Generates a color gradient for performance values, supporting dynamic table visualization.

Parameters:

x (simple string): Metric label name.

nv (simple float): Metric numerical value.

Returns: (color) Gradient color value for table background.

quantlapseTable(option, position)

Displays an interactive Performance Table summarizing all major backtesting metrics.

Includes Sharpe, Sortino, Omega, Profit Factor, drawdowns, profitability %, and trade statistics.

Parameters:

option (simple string): Table type — "Full", "Simple", or "None".

position (simple string): Table position — "Top Left", "Middle Right", "Bottom Left", etc.

Returns: (table) On-chart performance visualization table.

This library empowers advanced quantitative evaluation directly within Pine Script®, ideal for strategy developers seeking deeper performance diagnostics and intuitive on-chart metrics.

[boitl] Trendfilter🧭 Trend Filter – Curve View (1D / 1H + M15 Check)

A multi-timeframe trend filter that blends daily, hourly, and 15-minute data into a smooth, color-coded curve displayed in a separate panel.

It visualizes both trend direction and strength while accounting for overextension, providing a reliable “context indicator” for entries and filters.

🔍 Concept

The indicator evaluates three timeframes:

1D (Daily) → SMA200 for long-term trend bias

1H (Hourly) → EMA50 for medium-term confirmation

15M (Intraday) → EMA20 + ATR to detect overextension or mean reversion zones

It computes a continuous trend score between −1 and +1:

+1 → Strong bullish alignment (D1 & H1 both up)

−1 → Strong bearish alignment (D1 & H1 both down)

≈ 0 → Neutral, conflicting, or overextended conditions

The score is smoothed and normalized for a clean visual curve —

green for bullish, red for bearish, with dynamic transparency based on strength.

⚙️ Logic Overview

Timeframe Indicator Purpose

1D SMA200 Long-term trend direction

1H EMA50 Medium-term confirmation

15M EMA20 + ATR Overextension control

Alignment between D1 and H1 defines clear trend bias

Conflicts between them reduce the trend score

M15 overextension (price far from EMA20) softens the signal further

The result is a responsive trend-strength oscillator, ideal for multi-timeframe setups.

🧩 Use Cases

As a trend filter for strategies (e.g. allow entries only if score > 0.3 or < −0.3)

As a visual confirmation of higher-timeframe direction

To avoid trades during conflict or exhaustion

💡 Visualization

Single curve (area plot):

Green = bullish bias

Red = bearish bias

Transparency increases with weaker trend

Background colors:

🟠 Orange → D1/H1 conflict

🔴 Light red → M15 overextension active

Optional: binary alignment line (+1 / 0 / −1) for simplified display

⚙️ Parameters

Proximity to EMA20 (M15) = X×ATR → defines “near” condition

Overextension threshold = X×ATR → sets exhaustion boundary