Entropy (Fiedor/Kontoyiannis) - Part 2 of Fiedor's TheoryThis indicator estimates the Shannon entropy of a price series using a Markov chain model of binary returns, following the approach of Fiedor (2014) and Kontoyiannis (1997).

% of Max shows current entropy as a percentage of its theoretical maximum (1 bit for binary up/down moves).

Percentile ranks the current entropy against historical values in the chosen lookback window.

High entropy suggests price movement is less predictable by frequentist models; low entropy implies more structure and predictability.

Use this as an informational oscillator, not a trading signal.

This is a visualization of Part 1 of Fiedor's Theory. The same entropy logic is already embedded in Part 1 however the second pane is a nice reminder of why it works.

ค้นหาในสคริปต์สำหรับ "binary"

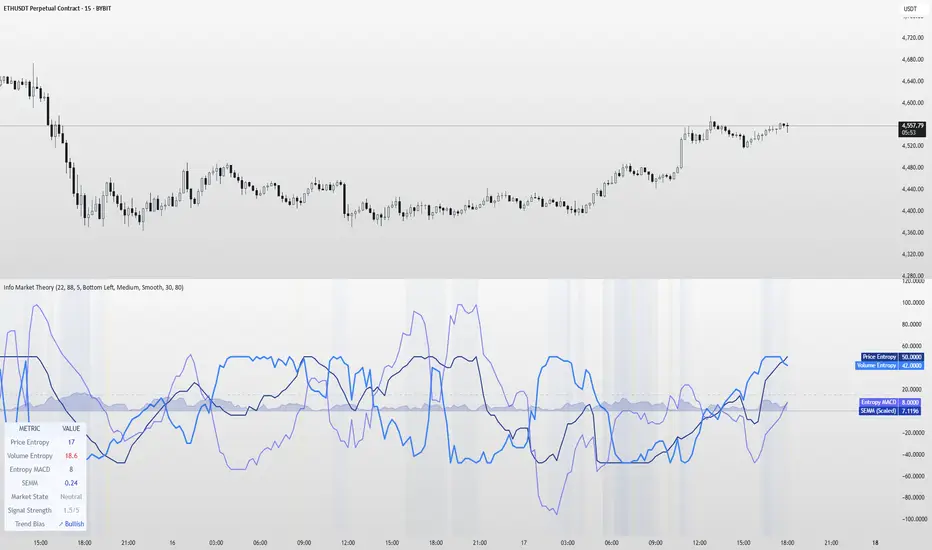

Information Theory Market AnalysisINFORMATION THEORY MARKET ANALYSIS

OVERVIEW

This indicator applies mathematical concepts from information theory to analyze market behavior, measuring the randomness and predictability of price and volume movements through entropy calculations. Unlike traditional technical indicators, it provides insight into market structure and regime changes.

KEY COMPONENTS

Four Main Signals:

• Price Entropy (Deep Blue): Measures randomness in price movements

• Volume Entropy (Bright Blue): Analyzes volume pattern predictability

• Entropy MACD (Purple): Shows relationship between price and volume entropy

• SEMM (Royal Blue): Stochastic Entropy Market Monitor - overall market randomness gauge

Market State Detection:

The indicator identifies seven distinct market states:

• Strong Trending (SEMM < 0.1)

• Weak Trending (0.1-0.2)

• Neutral (0.2-0.3)

• Moderate Random (0.3-0.5)

• High Randomness (0.5-0.8)

• Very Random (0.8-1.0)

• Chaotic (>1.0)

KEY FEATURES

Advanced Analytics:

• Signal Strength Confluence: 0-5 scale measuring alignment of multiple factors

• Entropy Crossovers: Detects shifts between accumulation and distribution phases

• Extreme Readings: Identifies statistical outliers for potential reversals

• Trend Bias Analysis: Directional momentum assessment

Information Dashboard:

• Real-time entropy values and market state

• Signal strength indicator with visual highlighting

• Trend bias with directional arrows

• Color-coded alerts for extreme conditions

Customizable Display:

• Adjustable SEMM scaling (5x to 100x) for optimal visibility

• Multiple line styles: Smooth, Stepped, Dotted

• 9 table positions with 3 size options

• Professional blue color scheme with transparency controls

Comprehensive Alert System - 15 Alert Types Including:

• Extreme entropy readings (price/volume)

• Crossover signals (dominance shifts)

• Market state changes (trending ↔ random)

• High confluence signals (3+ factors aligned)

HOW TO USE

Reading the Signals:

• Entropy Values > ±25: Strong structural signals

• Entropy Values > ±40: Extreme readings, potential reversals

• SEMM < 0.2: Trending market favors directional strategies

• SEMM > 0.5: Random market favors range/scalping strategies

Signal Confluence:

Look for multiple factors aligning:

• Signal Strength ≥ 3.0 for higher probability setups

• Background highlighting indicates confluence

• Table shows real-time strength assessment

Timeframe Optimization:

• Short-term (1m-15m): Entropy Length 14-22, Sensitivity 3-5

• Swing Trading (1H-4H): Default settings optimal

• Position Trading (Daily+): Entropy Length 34-55, Sensitivity 8-12

EDUCATIONAL APPLICATIONS

Market Structure Analysis:

• Understand when markets are trending vs. ranging

• Identify accumulation and distribution phases

• Recognize extreme market conditions

• Measure information content in price movements

Information Theory Concepts:

• Binary entropy calculations applied to financial data

• Probability distribution analysis of returns

• Statistical ranking and percentile analysis

• Momentum-adjusted randomness measurement

TECHNICAL DETAILS

Calculations:

• Uses binary entropy formula: -

• Percentile ranking across multiple timeframes

• Volume-weighted probability distributions

• RSI-adjusted momentum entropy (SEMM)

Customization Options:

• Entropy Length: 5-100 bars (default: 22)

• Average Length: 10-200 bars (default: 88)

• Sensitivity: 1.0-20.0 (default: 5.0, lower = more sensitive)

• SEMM Scaling: 5.0-100.0x (default: 30.0)

IMPORTANT NOTES

Risk Considerations:

• Indicator measures probabilities, not certainties

• High SEMM values (>0.5) suggest increased market randomness

• Extreme readings may persist longer than expected

• Always combine with proper risk management

Educational Purpose:

This indicator is designed for:

• Market structure analysis and education

• Understanding information theory applications in finance

• Developing probabilistic thinking about markets

• Research and analytical purposes

Performance Tips:

• Allow 200+ bars for proper initialization

• Adjust scaling and transparency for optimal visibility

• Use confluence signals for higher probability analysis

• Consider multiple timeframes for comprehensive analysis

DISCLAIMER

This indicator is for educational and analytical purposes. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research and consider your risk tolerance before making trading decisions.

Version: 5.0

Category: Oscillators, Volume, Market Structure

Best For: All timeframes, trending and ranging markets

Complexity: Intermediate to Advanced

Intradayscanner - RvolThis indicator delivers a session-precise Relative Volume (RVol) metric using an advanced, performance-optimized method that goes beyond standard volume-vs-average calculations:

Session-Aligned Cumulative Volume

Tracks intraday volume from each session’s true open using a rolling array of session start bar indices.

Prunes old sessions to maintain high performance even on long history (max_bars_back=5000).

Binary-Search History Lookup

Employs a binary-search algorithm to find the exact bar corresponding to each prior session’s close, accounting for weekends/holidays.

Ensures the N-day average is built from perfectly aligned session volumes rather than simple bar-counts.

Configurable Threshold & Coloring

Computes RVol = (today’s cumulative volume) ÷ (N-day average cumulative volume).

Highlights high-volume conditions when RVol exceeds a user-defined threshold (High Volume Threshold).

Optional line-coloring by price direction (up/down) for immediate visual context.

Background Shading for Volume Spikes

Applies semi-transparent colored backgrounds when RVol > 1 (and above the threshold), making significant volume surges unmissable.

Customizable Lookback & Precision

User inputs for N-day average length, threshold multiplier, and color-by-previous-close toggle.

Designed for up to 5000 bars of history without performance degradation.

TTM Squeeze Value OscillatorThis indicator is specifically designed for use with TradingView's Stock Screener, not for chart analysis. It provides numerical values and binary signals that allow traders to efficiently scan stocks for specific TTM Squeeze conditions, momentum patterns, and EMA alignments.

What It Does

The TTM Squeeze Value Oscillator converts the popular TTM Squeeze indicator into a screenable format by outputting specific numerical values and binary signals (1 or 0) that can be filtered in TradingView's screener tool.

Key Features

1. TTM Squeeze Compression Levels

Value 0: Low Compression (Black) - Bollinger Bands inside outer Keltner Channels

Value 1: Mid Compression (Red) - Bollinger Bands inside middle Keltner Channels

Value 2: High Compression (Orange) - Bollinger Bands inside inner Keltner Channels

Value 3: Squeeze Fired (Green) - Bollinger Bands outside Keltner Channels

2. Momentum Analysis

Four distinct momentum conditions based on TTM Squeeze methodology:

Buy Momentum Increasing - Positive momentum growing stronger

Buy Momentum Decreasing - Positive momentum weakening

Sell Momentum Increasing - Negative momentum growing stronger

Sell Momentum Decreasing - Negative momentum weakening

3. EMA Stacking Analysis

Three EMA alignment patterns using 8, 21, and 48 period EMAs:

EMA Stacked Bullish - 8 EMA > 21 EMA > 48 EMA (uptrend alignment)

EMA Stacked Bearish - 8 EMA < 21 EMA < 48 EMA (downtrend alignment)

EMA Mixed - EMAs not in clear bullish or bearish alignment

4. Consecutive Day Counters

Tracks how many consecutive days each squeeze condition has persisted:

Low Compression Days

Mid Compression Days

High Compression Days

Squeeze Fired Days

5. Combined Signal Analysis

Pre-calculated combinations of squeeze conditions with momentum:

All squeeze levels combined with all four momentum conditions

16 total combined signals for advanced screening

[Kpt-Ahab] Poor Mans Orderflow SimulatorScript Description – Poor Mans Orderflow Simulator

Purpose of the Script

This script simulates a simplified order flow approach ("Poor Man's Orderflow") without access to actual Bid/Ask data. The goal is to detect, quantify, and visualize patterns such as absorption, impulsive moves, and structured re-entry behaviors.

Calculation Logic

Absorption Candles

A candle is classified as "absorption" if:

The ratio of body size to full candle range is below a defined threshold,

Volume is significantly higher than the average of the last N periods,

The candle direction is negative (for long absorption) or positive (for short absorption).

These conditions define a candle with high activity but minimal price movement in the respective direction.

Impulse Candles

A candle is classified as "impulse" if:

The body-to-range ratio is high (indicating a strong directional move),

Volume exceeds the average significantly,

The price closes in the direction of the candle body (bullish or bearish).

Additionally, the average range of previous candles serves as a minimum benchmark for the impulse.

Cluster Detection

A cluster is detected when:

A minimum number of absorption candles is counted within a defined lookback period,

Either the long or short version of the absorption logic is used,

The result is a binary condition: cluster active or inactive.

Entry Signals (Re-entry)

An entry signal is generated when:

One or more absorption candles occurred in the last two bars,

A pullback against the direction of absorption occurs,

The current candle shows a directional move confirmed by a close in the expected direction.

These re-entry signals are evaluated separately for long and short scenarios.

Cluster-Confirmed Signals

A separate signal is generated when a valid re-entry setup occurs while a cluster is active. This represents a combined logic condition.

Alert Logic

The script provides a multi-layer alert framework:

Signal selection (Alertmode):

The user defines which signal type should trigger an alert (e.g. re-entry only, cluster only, combination, or impulse).

Optional filter (Filtermode):

A secondary filter limits alerts to cases where an additional condition (e.g. absorption cluster) is active.

Signal output:

As a simple binary value (+1 / –1) for classic alerts,

Or via an encoded Multibit signal, compatible with other modules in the djmad ecosystem.

These alerts are intended for integration with external systems or for use within platform-native visual or automation features.

Fuzzy SMA Trend Analyzer (experimental)[FibonacciFlux]Fuzzy SMA Trend Analyzer (Normalized): Advanced Market Trend Detection Using Fuzzy Logic Theory

Elevate your technical analysis with institutional-grade fuzzy logic implementation

Research Genesis & Conceptual Framework

This indicator represents the culmination of extensive research into applying fuzzy logic theory to financial markets. While traditional technical indicators often produce binary outcomes, market conditions exist on a continuous spectrum. The Fuzzy SMA Trend Analyzer addresses this limitation by implementing a sophisticated fuzzy logic system that captures the nuanced, multi-dimensional nature of market trends.

Core Fuzzy Logic Principles

At the heart of this indicator lies fuzzy logic theory - a mathematical framework designed to handle imprecision and uncertainty:

// Improved fuzzy_triangle function with guard clauses for NA and invalid parameters.

fuzzy_triangle(val, left, center, right) =>

if na(val) or na(left) or na(center) or na(right) or left > center or center > right // Guard checks

0.0

else if left == center and center == right // Crisp set (single point)

val == center ? 1.0 : 0.0

else if left == center // Left-shoulder shape (ramp down from 1 at center to 0 at right)

val >= right ? 0.0 : val <= center ? 1.0 : (right - val) / (right - center)

else if center == right // Right-shoulder shape (ramp up from 0 at left to 1 at center)

val <= left ? 0.0 : val >= center ? 1.0 : (val - left) / (center - left)

else // Standard triangle

math.max(0.0, math.min((val - left) / (center - left), (right - val) / (right - center)))

This implementation of triangular membership functions enables the indicator to transform crisp numerical values into degrees of membership in linguistic variables like "Large Positive" or "Small Negative," creating a more nuanced representation of market conditions.

Dynamic Percentile Normalization

A critical innovation in this indicator is the implementation of percentile-based normalization for SMA deviation:

// ----- Deviation Scale Estimation using Percentile -----

// Calculate the percentile rank of the *absolute* deviation over the lookback period.

// This gives an estimate of the 'typical maximum' deviation magnitude recently.

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

// ----- Normalize the Raw Deviation -----

// Divide the raw deviation by the estimated 'typical max' magnitude.

normalized_diff = raw_diff / diff_abs_percentile

// ----- Clamp the Normalized Deviation -----

normalized_diff_clamped = math.max(-3.0, math.min(3.0, normalized_diff))

This percentile normalization approach creates a self-adapting system that automatically calibrates to different assets and market regimes. Rather than using fixed thresholds, the indicator dynamically adjusts based on recent volatility patterns, significantly enhancing signal quality across diverse market environments.

Multi-Factor Fuzzy Rule System

The indicator implements a comprehensive fuzzy rule system that evaluates multiple technical factors:

SMA Deviation (Normalized): Measures price displacement from the Simple Moving Average

Rate of Change (ROC): Captures price momentum over a specified period

Relative Strength Index (RSI): Assesses overbought/oversold conditions

These factors are processed through a sophisticated fuzzy inference system with linguistic variables:

// ----- 3.1 Fuzzy Sets for Normalized Deviation -----

diffN_LP := fuzzy_triangle(normalized_diff_clamped, 0.7, 1.5, 3.0) // Large Positive (around/above percentile)

diffN_SP := fuzzy_triangle(normalized_diff_clamped, 0.1, 0.5, 0.9) // Small Positive

diffN_NZ := fuzzy_triangle(normalized_diff_clamped, -0.2, 0.0, 0.2) // Near Zero

diffN_SN := fuzzy_triangle(normalized_diff_clamped, -0.9, -0.5, -0.1) // Small Negative

diffN_LN := fuzzy_triangle(normalized_diff_clamped, -3.0, -1.5, -0.7) // Large Negative (around/below percentile)

// ----- 3.2 Fuzzy Sets for ROC -----

roc_HN := fuzzy_triangle(roc_val, -8.0, -5.0, -2.0)

roc_WN := fuzzy_triangle(roc_val, -3.0, -1.0, -0.1)

roc_NZ := fuzzy_triangle(roc_val, -0.3, 0.0, 0.3)

roc_WP := fuzzy_triangle(roc_val, 0.1, 1.0, 3.0)

roc_HP := fuzzy_triangle(roc_val, 2.0, 5.0, 8.0)

// ----- 3.3 Fuzzy Sets for RSI -----

rsi_L := fuzzy_triangle(rsi_val, 0.0, 25.0, 40.0)

rsi_M := fuzzy_triangle(rsi_val, 35.0, 50.0, 65.0)

rsi_H := fuzzy_triangle(rsi_val, 60.0, 75.0, 100.0)

Advanced Fuzzy Inference Rules

The indicator employs a comprehensive set of fuzzy rules that encode expert knowledge about market behavior:

// --- Fuzzy Rules using Normalized Deviation (diffN_*) ---

cond1 = math.min(diffN_LP, roc_HP, math.max(rsi_M, rsi_H)) // Strong Bullish: Large pos dev, strong pos roc, rsi ok

strength_SB := math.max(strength_SB, cond1)

cond2 = math.min(diffN_SP, roc_WP, rsi_M) // Weak Bullish: Small pos dev, weak pos roc, rsi mid

strength_WB := math.max(strength_WB, cond2)

cond3 = math.min(diffN_SP, roc_NZ, rsi_H) // Weakening Bullish: Small pos dev, flat roc, rsi high

strength_N := math.max(strength_N, cond3 * 0.6) // More neutral

strength_WB := math.max(strength_WB, cond3 * 0.2) // Less weak bullish

This rule system evaluates multiple conditions simultaneously, weighting them by their degree of membership to produce a comprehensive trend assessment. The rules are designed to identify various market conditions including strong trends, weakening trends, potential reversals, and neutral consolidations.

Defuzzification Process

The final step transforms the fuzzy result back into a crisp numerical value representing the overall trend strength:

// --- Step 6: Defuzzification ---

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10 // Use small epsilon instead of != 0.0 for float comparison

fuzzyTrendScore := (strength_SB * STRONG_BULL +

strength_WB * WEAK_BULL +

strength_N * NEUTRAL +

strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1 (strong bearish) to +1 (strong bullish), providing a smooth, continuous evaluation of market conditions that avoids the abrupt signal changes common in traditional indicators.

Advanced Visualization with Rainbow Gradient

The indicator incorporates sophisticated visualization using a rainbow gradient coloring system:

// Normalize score to for gradient function

normalizedScore = na(fuzzyTrendScore) ? 0.5 : math.max(0.0, math.min(1.0, (fuzzyTrendScore + 1) / 2))

// Get the color based on gradient setting and normalized score

final_color = get_gradient(normalizedScore, gradient_type)

This color-coding system provides intuitive visual feedback, with color intensity reflecting trend strength and direction. The gradient can be customized between Red-to-Green or Red-to-Blue configurations based on user preference.

Practical Applications

The Fuzzy SMA Trend Analyzer excels in several key applications:

Trend Identification: Precisely identifies market trend direction and strength with nuanced gradation

Market Regime Detection: Distinguishes between trending markets and consolidation phases

Divergence Analysis: Highlights potential reversals when price action and fuzzy trend score diverge

Filter for Trading Systems: Provides high-quality trend filtering for other trading strategies

Risk Management: Offers early warning of potential trend weakening or reversal

Parameter Customization

The indicator offers extensive customization options:

SMA Length: Adjusts the baseline moving average period

ROC Length: Controls momentum sensitivity

RSI Length: Configures overbought/oversold sensitivity

Normalization Lookback: Determines the adaptive calculation window for percentile normalization

Percentile Rank: Sets the statistical threshold for deviation normalization

Gradient Type: Selects the preferred color scheme for visualization

These parameters enable fine-tuning to specific market conditions, trading styles, and timeframes.

Acknowledgments

The rainbow gradient visualization component draws inspiration from LuxAlgo's "Rainbow Adaptive RSI" (used under CC BY-NC-SA 4.0 license). This implementation of fuzzy logic in technical analysis builds upon Fermi estimation principles to overcome the inherent limitations of crisp binary indicators.

This indicator is shared under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Remember that past performance does not guarantee future results. Always conduct thorough testing before implementing any technical indicator in live trading.

Neural Pulse System [Alpha Extract]Neural Pulse System (NPS)

The Neural Pulse System (NPS) is a custom technical indicator that analyzes price action through a probabilistic lens, offering a dynamic view of bullish and bearish tendencies.

Unlike traditional binary classification models, NPS employs Ordinary Least Squares (OLS) regression with dynamically computed coefficients to produce a smooth probability output ranging from -1 to 1.

Paired with ATR-based bands, this indicator provides an intuitive and volatility-aware approach to trend analysis.

🔶 CALCULATION

The Neural Pulse System utilizes OLS regression to compute probabilities of bullish or bearish price action while incorporating ATR-based bands for volatility context:

Dynamic Coefficients: Coefficients are recalculated in real-time and scaled up to ensure the regression adapts to evolving market conditions.

Ordinary Least Squares (OLS): Uses OLS regression instead of gradient descent for more precise and efficient coefficient estimation.

ATR Bands: Smoothed Average True Range (ATR) bands serve as dynamic boundaries, framing the regression within market volatility.

Probability Output: Instead of a binary result, the output is a continuous probability curve (-1 to 1), helping traders gauge the strength of bullish or bearish momentum.

Formula:

OLS Regression = Line of best fit minimizing squared errors

Probability Signal = Transformed regression output scaled to -1 (bearish) to 1 (bullish)

ATR Bands = Smoothed Average True Range (ATR) to frame price movements within market volatility

🔶 DETAILS

📊 Visual Features:

Probability Curve: Smooth probability signal ranging from -1 (bearish) to 1 (bullish)

ATR Bands: Price action is constrained within volatility bands, preventing extreme deviations

Color-Coded Signals:

Blue to Green: Increasing probability of bullish momentum

Orange to Red: Increasing probability of bearish momentum

Interpretation:

Bullish Bias: Probability output consistently above 0 suggests a bullish trend.

Bearish Bias: Probability output consistently below 0 indicates bearish pressure.

Reversals: Extreme values near -1 or 1, followed by a move toward 0, may signal potential trend reversals.

🔶 EXAMPLES

📌 Trend Identification: Use the probability output to gauge trend direction.

📌Example: On a 1-hour chart, NPS moves from -0.5 to 0.8 as price breaks resistance, signaling a bullish trend.

Reversal Signals: Watch for probability extremes near -1 or 1 followed by a reversal toward 0.

Example: NPS hits 0.9, price touches the upper ATR band, then both retreat—indicating a potential pullback.

📌 Example snapshots:

Volatility Context: ATR bands help assess whether price action aligns with typical market conditions.

Example: During low volatility, the probability signal hovers near 0, and ATR bands tighten, suggesting a potential breakout.

🔶 SETTINGS

Customization Options:

ATR Period – Defines lookback length for ATR calculation (shorter = more responsive, longer = smoother).

ATR Multiplier – Adjusts band width for better volatility capture.

Regression Length – Controls how many bars feed into the coefficient calculation (longer = smoother, shorter = more reactive).

Scaling Factor – Adjusts the strength of regression coefficients.

Output Smoothing – Option to apply a moving average for a cleaner probability curve

MTF Signal XpertMTF Signal Xpert – Detailed Description

Overview:

MTF Signal Xpert is a proprietary, open‑source trading signal indicator that fuses multiple technical analysis methods into one cohesive strategy. Developed after rigorous backtesting and extensive research, this advanced tool is designed to deliver clear BUY and SELL signals by analyzing trend, momentum, and volatility across various timeframes. Its integrated approach not only enhances signal reliability but also incorporates dynamic risk management, helping traders protect their capital while navigating complex market conditions.

Detailed Explanation of How It Works:

Trend Detection via Moving Averages

Dual Moving Averages:

MTF Signal Xpert computes two moving averages—a fast MA and a slow MA—with the flexibility to choose from Simple (SMA), Exponential (EMA), or Hull (HMA) methods. This dual-MA system helps identify the prevailing market trend by contrasting short-term momentum with longer-term trends.

Crossover Logic:

A BUY signal is initiated when the fast MA crosses above the slow MA, coupled with the condition that the current price is above the lower Bollinger Band. This suggests that the market may be emerging from a lower price region. Conversely, a SELL signal is generated when the fast MA crosses below the slow MA and the price is below the upper Bollinger Band, indicating potential bearish pressure.

Recent Crossover Confirmation:

To ensure that signals reflect current market dynamics, the script tracks the number of bars since the moving average crossover event. Only crossovers that occur within a user-defined “candle confirmation” period are considered, which helps filter out outdated signals and improves overall signal accuracy.

Volatility and Price Extremes with Bollinger Bands

Calculation of Bands:

Bollinger Bands are calculated using a 20‑period simple moving average as the central basis, with the upper and lower bands derived from a standard deviation multiplier. This creates dynamic boundaries that adjust according to recent market volatility.

Signal Reinforcement:

For BUY signals, the condition that the price is above the lower Bollinger Band suggests an undervalued market condition, while for SELL signals, the price falling below the upper Bollinger Band reinforces the bearish bias. This volatility context adds depth to the moving average crossover signals.

Momentum Confirmation Using Multiple Oscillators

RSI (Relative Strength Index):

The RSI is computed over 14 periods to determine if the market is in an overbought or oversold state. Only readings within an optimal range (defined by user inputs) validate the signal, ensuring that entries are made during balanced conditions.

MACD (Moving Average Convergence Divergence):

The MACD line is compared with its signal line to assess momentum. A bullish scenario is confirmed when the MACD line is above the signal line, while a bearish scenario is indicated when it is below, thus adding another layer of confirmation.

Awesome Oscillator (AO):

The AO measures the difference between short-term and long-term simple moving averages of the median price. Positive AO values support BUY signals, while negative values back SELL signals, offering additional momentum insight.

ADX (Average Directional Index):

The ADX quantifies trend strength. MTF Signal Xpert only considers signals when the ADX value exceeds a specified threshold, ensuring that trades are taken in strongly trending markets.

Optional Stochastic Oscillator:

An optional stochastic oscillator filter can be enabled to further refine signals. It checks for overbought conditions (supporting SELL signals) or oversold conditions (supporting BUY signals), thus reducing ambiguity.

Multi-Timeframe Verification

Higher Timeframe Filter:

To align short-term signals with broader market trends, the script calculates an EMA on a higher timeframe as specified by the user. This multi-timeframe approach helps ensure that signals on the primary chart are consistent with the overall trend, thereby reducing false signals.

Dynamic Risk Management with ATR

ATR-Based Calculations:

The Average True Range (ATR) is used to measure current market volatility. This value is multiplied by a user-defined factor to dynamically determine stop loss (SL) and take profit (TP) levels, adapting to changing market conditions.

Visual SL/TP Markers:

The calculated SL and TP levels are plotted on the chart as distinct colored dots, enabling traders to quickly identify recommended exit points.

Optional Trailing Stop:

An optional trailing stop feature is available, which adjusts the stop loss as the trade moves favorably, helping to lock in profits while protecting against sudden reversals.

Risk/Reward Ratio Calculation:

MTF Signal Xpert computes a risk/reward ratio based on the dynamic SL and TP levels. This quantitative measure allows traders to assess whether the potential reward justifies the risk associated with a trade.

Condition Weighting and Signal Scoring

Binary Condition Checks:

Each technical condition—ranging from moving average crossovers, Bollinger Band positioning, and RSI range to MACD, AO, ADX, and volume filters—is assigned a binary score (1 if met, 0 if not).

Cumulative Scoring:

These individual scores are summed to generate cumulative bullish and bearish scores, quantifying the overall strength of the signal and providing traders with an objective measure of its viability.

Detailed Signal Explanation:

A comprehensive explanation string is generated, outlining which conditions contributed to the current BUY or SELL signal. This explanation is displayed on an on‑chart dashboard, offering transparency and clarity into the signal generation process.

On-Chart Visualizations and Debug Information

Chart Elements:

The indicator plots all key components—moving averages, Bollinger Bands, SL and TP markers—directly on the chart, providing a clear visual framework for understanding market conditions.

Combined Dashboard:

A dedicated dashboard displays key metrics such as RSI, ADX, and the bullish/bearish scores, alongside a detailed explanation of the current signal. This consolidated view allows traders to quickly grasp the underlying logic.

Debug Table (Optional):

For advanced users, an optional debug table is available. This table breaks down each individual condition, indicating which criteria were met or not met, thus aiding in further analysis and strategy refinement.

Mashup Justification and Originality

MTF Signal Xpert is more than just an aggregation of existing indicators—it is an original synthesis designed to address real-world trading complexities. Here’s how its components work together:

Integrated Trend, Volatility, and Momentum Analysis:

By combining moving averages, Bollinger Bands, and multiple oscillators (RSI, MACD, AO, ADX, and an optional stochastic), the indicator captures diverse market dynamics. Each component reinforces the others, reducing noise and filtering out false signals.

Multi-Timeframe Analysis:

The inclusion of a higher timeframe filter aligns short-term signals with longer-term trends, enhancing overall reliability and reducing the potential for contradictory signals.

Adaptive Risk Management:

Dynamic stop loss and take profit levels, determined using ATR, ensure that the risk management strategy adapts to current market conditions. The optional trailing stop further refines this approach, protecting profits as the market evolves.

Quantitative Signal Scoring:

The condition weighting system provides an objective measure of signal strength, giving traders clear insight into how each technical component contributes to the final decision.

How to Use MTF Signal Xpert:

Input Customization:

Adjust the moving average type and period settings, ATR multipliers, and oscillator thresholds to align with your trading style and the specific market conditions.

Enable or disable the optional stochastic oscillator and trailing stop based on your preference.

Interpreting the Signals:

When a BUY or SELL signal appears, refer to the on‑chart dashboard, which displays key metrics (e.g., RSI, ADX, bullish/bearish scores) along with a detailed breakdown of the conditions that triggered the signal.

Review the SL and TP markers on the chart to understand the associated risk/reward setup.

Risk Management:

Use the dynamically calculated stop loss and take profit levels as guidelines for setting your exit points.

Evaluate the provided risk/reward ratio to ensure that the potential reward justifies the risk before entering a trade.

Debugging and Verification:

Advanced users can enable the debug table to see a condition-by-condition breakdown of the signal generation process, helping refine the strategy and deepen understanding of market dynamics.

Disclaimer:

MTF Signal Xpert is intended for educational and analytical purposes only. Although it is based on robust technical analysis methods and has undergone extensive backtesting, past performance is not indicative of future results. Traders should employ proper risk management and adjust the settings to suit their financial circumstances and risk tolerance.

MTF Signal Xpert represents a comprehensive, original approach to trading signal generation. By blending trend detection, volatility assessment, momentum analysis, multi-timeframe alignment, and adaptive risk management into one integrated system, it provides traders with actionable signals and the transparency needed to understand the logic behind them.

Risk Matrix [QuantraSystems]Risk Matrix

The Risk Matrix is a sophisticated tool that aggregates a variety of fundamental inputs, primarily external (non-crypto) market data is used to assess investor risk appetite. By combining external macroeconomic factors and proxies for liquidity data with specific signals from the cryptomarket - the Risk Matrix provides a holistic view of market risk conditions. These insights are designed to help traders and investors make informed decisions on when to adopt a risk-on or risk-off approach.

Core Concept

The Risk Matrix functions as a dynamic risk assessment tool that integrates both fundamental and technical market indicators to generate an aggregated Z-score. This score helps traders to identify where the market is in a risk-off or risk-on state, The system provides both binary risk signals and a more nuanced “risk seasonality” mode for deeper analysis.

Key Features

Global Liquidity Aggregate - The Liquidity score is a custom measure of global liquidity, built by combining a variety of traditional financial metrics. These include data from central bank balance sheets, reverse repo operations and credit availability. This data is sourced from organizations such as the U.S. Federal Reserve, the European Central Bank, and the People’s Bank of China. The purpose of this aggregate is to gauge how much liquidity is available in the global financial system - which often correlates with risk sentiment. Rising liquidity tends to boost risk-on appetite, while liquidity contractions signal increased caution (risk-off) in the markets. The data sources used in this global liquidity aggregate include:

- U.S. Commercial Bank Credit data

- Federal Reserve balance sheet and reverse repo operations

- Liquidity from major central banks including the Fed, Bank of Japan, ECB, and PBoC

- Asset performance from major global financial indices such as the S&P 500, TLT, DXY (U.S. Dollar Index), MOVE (bond market volatility), and commodities like gold and oil.

Other key Z-scores (measured individually) - The Risk Matrix also incorporates other major Z-scores that represent different facets of the financial markets:

- Collateral Risk - A measure of US bond volatility, where higher values indicate higher interest rate risk - leading to potential market instability and cautious market behaviors.

- Stablecoin Dominance - The dominance of stablecoins in the crypto markets - which can signal risk aversion the total capital allocated to stables increases relative to other cryptocurrencies.

- US Currency Strength - The U.S. Dollar Index Z-score reflects currency market strength, with higher values typically indicating risk aversion as investors sell more volatile assets and flock to the dollar.

- Trans-pacific Monetary Bias - Signals capital flow and monetary trends that link between the East and West, heavily influencing global risk sentiment.

- Total - A measure of the total cryptocurrency market cap, signaling broader risk sentiment with the crypto market.

Neural Network Synthesis - The NNSYNTH component adds a machine learning inspired layer to the Risk Matrix. This custom indicator synthesizes inputs from various technical indicators (such as RSI, MACD, Bollinger Bands, and others) to generate a composite signal that reflects the health of the cryptomarket. While highly complex in its design, the NNSYNTH ultimately helps detect market shifts early by synthesizing multiple signals into one cohesive output. This score is particularly useful for gauging momentum and identifying potential turning points in market trends. Because the NNSYNTH is a closed source indicator, and it is included here, the Risk Matrix by extension is a closed source indicator.

How it Works

Z-score Aggregation - The Risk Matrix computes a final risk score by aggregating several Z-scores from different asset classes and data sources, all of which contribute proportionally to the overall market risk assessment. Each input is equally weighted - normalization allows for direct comparisons across global liquidity trends, currency fluctuations, bond market volatility and crypto market conditions. Furthermore, this system employs multi-calibration aggregation - where each individual matrix is itself an aggregate of multiple Z-scores derived from various timeframes. This ensures that each matrix captures a distinct average across different time horizons before being combined into the overall Risk Matrix. This layered, multi timeframe approach enhances the precision and robustness of the final Z-score.

Risk-On / Risk-Off Mode - The system’s binary mode provides a clear Risk On and Off signal. This nature of this signal is determined by the behavior of the Z-score relative to the midline, or Standard Deviation Bands, depending on specific conditions:

Risk-On is signaled when the aggregated final Z-score crosses above 0. However, in extreme oversold conditions, Risk-On can trigger early if the upper standard deviation band falls below the zero line. In such cases, the Risk-On signal is triggered when the z-score crosses the upper standard deviation band - without waiting to cross the midline.

Risk-Off is signaled when the final Z-score moves below 0. Similarly, Risk-Off can also be triggered early if the lower standard deviation band rises above the midline. In this instance, Risk-Off is triggered when the Z-score crosses below the lower band.

Risk Seasonality Mode - This mode offers a more gradual transition between risk states, measuring the change in the Z-score to visualize the shifts in risk appetite over time. It's useful for traders seeking to understand broader market cycles and risk phases. The seasonality view breaks down the market into the following phases:

Risk-On - High risk appetite where risk/cyclical markets are generally bullish.

Weakening - Markets showing signs of cooling off, here the higher beta assets tend to sell off first.

Risk-Off - Investors pull back, and bearish sentiment prevails.

Recovery - Signs of bottoming out, potential for market re-entry.

Component Matrices - Each individual Z-score is visualized as part of the component matrices - scaled to a 3 Sigma range. These component matrices allow traders to view how each data source is contributing to the overall risk assessment in real time - offering transparency and granularity.

Visuals and UI

Main Risk Matrix - The aggregated Z-Score is displayed saliently in the main risk matrix. Traders and investors can quickly see what season the Risk Matrix is signaling and adjust their strategies accordingly.

Overview Table - A detailed overview table shows the current confirmed Z-scores for each component, along with values from 2, and 3 bars back. This helps traders spot trends and the rate of change (RoC) between signals, offering additional insights for shorter-term risk management.

Customizability - Users can customize the visual elements of the matrix, including color palettes, table sizes, and positions. This allows for optimal integration into any trader’s existing workspace.

Usage Summary

The Risk Matrix is an incredibly versatile tool. It is especially valuable as a means of achieving a cross-market view of risk, incorporating both crypto-specific and macroeconomic factors. Some key use cases include:

Adjusting Capital Allocation Based on Risk Seasons - Traders can use the Risk Matrix to adjust their capital allocation dynamically. During Risk-On periods, they might increase exposure to long positions, capitalizing on stronger market conditions. Conversely, during Risk-Off periods, traders could reduce or hedge long positions and potentially scale up short positions or move into safer assets.

Complementing Other Trading Systems - The Risk Matrix can work alongside other technical systems to provide context to market moves. For instance, a trend-following strategy might suggest an entry, but the Risk Matrix could be used to verify whether the broader market conditions support this trade. If the Matrix is in a Risk-Off period, a trader might opt for more conservative trade sizes or avoid the trade entirely.

This flexibility allows traders to adjust their strategies and portfolio risk dynamically, enhancing decision making based on broader market conditions - as indicated by external macroeconomic factors, liquidity, and risk sentiment.

Important Note

The Risk Matrix always uses the most up-to-date data available, ensuring analysis reflects the latest market conditions and macroeconomic inputs. In rare cases, governments or financial institutions revise past data - and the Risk Matrix will adjust accordingly. This behavior can only be seen in the Liquidity Matrix. and can affect the final score. While this is uncommon, it highlights the benefit of using a system that adapts in real-time, incorporating the most accurate and current information to enhance decision making processes.

[GYTS-CE] Signal Provider | WaveTrend 4D with GDMWaveTrend 4D with Gradient Divergence Measure (Community Edition)

🌸 " 📡 Signal Provider" in GoemonYae Trading System (GYTS) 🌸

WaveTrend 4D (WT4D) is an extension of the incredible WaveTrend 3D (2022, Justin Dehorty) . This oscillator elevates the classic WaveTrend by integrating advanced mathematical models for a multi-dimensional view of market momentum, capturing subtle shifts and trends that traditional indicators might miss. Each oscillator layer uses a combination of normalised derivatives, hyperbolic tangent transformations, and dual-pole filtering (John Ehlers' SuperSmoother), providing normalised and smooth signals with minimised lag.

The name "WaveTrend 4D" is derived from the usage of 4 dimensions, representing different frequencies or timeframes. Next to the "fast", "normal" and "slow" frequency, the fourth frequency is called "lethargic" (very slow). This gives the opportunity utilise more dimensions without having abundant signals, since we quantify and filter the quality of signals.

WT4D strives to help discriminating high-quality signals from the indicator by introducing the Gradient Divergence Measure (GDM) and Quantile Median Crosses (QMC). For simplicity, speed and focus, this particular indicator includes only the GDM part. Check the other 🤲Community Edition of this indicator that focuses on the QMC. For GDM, see below for more information.

🌸 --- GRADIENT DIVERGENCE MEASURE (GDM) --- 🌸

💮 Introduction

--

The GDM dynamically calculates a composite measure based on multiple factors. Unlike traditional binary divergence indicators, GDM employs a continuous value system to capture the nuanced dynamics of market behaviour. This methodology allows traders and analysts to assess the potency of divergence signals with greater precision, facilitating more informed decision-making processes.

💮 Methodology

--

The GDM is calculated using a composite formula that integrates various market dynamics. At its core, it consists of six components listed below, each weighted to optimize the indicator's responsiveness to market conditions:

The magnitude of relative change between waves -- A larger difference between the waves, i.e. lower high or higher low could signify a stronger divergence.

The absolute value of the latest wave -- The strength of the latest wave provides insight into the extremity of the market conditions.

Slope of the divergence -- The slope between the two points of divergence essentially measures the rate of change in the frequency\'s value over time. It captures both the direction and the steepness of the indicator’s move between two waves.

The magnitude of relative change of the price -- A divergence means that the oscillator shows an opposite pattern than price action. Thus, if the price makes a significantly higher high or lower low, but the indicator does not, this discrepancy can be used to measure the divergence strength. This components measures the price's extrema during the crosses of the indicator's waves.

Higher timeframe's frequency trend -- Similarly, instead of looking at the price directly, this component measures the more general trend of the price by using the higher timeframe frequency (i.e. the slow frequency when looking at divergences of the normal frequency).

Time duration -- Lastly, the time duration between the two points of a divergence can also be an important factor. A divergence that spans over a longer period might indicate a more significant market sentiment shift.

💮 Tuning the GDM

--

The 6 components discussed above are not independent, e.g. the slope is actually the result of the magnitude between waves, the absolute value and time duration. However, the default GDM is carefully tuned to include all these features without being too sensitive to outliers.

This makes this indicator very user-friendly. The only core parameter is the the "sensitivity". This controls the extent of normalisation between signals, and essentially affects how often strong GDMs appear. At the conservative end (higher sensitivity), the strong GDMs are less frequent but are relatively significant, while with a lower sensitivity the strong GDMs appear more frequent.

💮 GDM on the Oscillator

--

The GDMs are represented by triangles and their value represents the strength. A value close to `1` signifies a strong bearish divergence and thus a possible reversal of continuation of a downtrend. Similarly, a value close to `-1` signifies a strong bullish divergence.

Note that there are two colour sets which can be enabled and disabled. One uses crosses between the fast and normal frequencies (with the slow frequency acting as the price trend with which there should be an opposite interaction -- hence a "divergence"). Similarly, crosses between the normal and slow frequencies (with the lethargic (the most slow) frequency acting as the price trend) are used to find divergences on a higher timeframe.

Another handy feature is a threshold to more strikingly visualise "strong" GDMs.

🌸 --- GOEMONYAE TRADING SYSTEM --- 🌸

As previously mentioned, this indicator is a 📡 Signal Provider, part of the suite of the GoemonYae Trading System (🤲 Community Edition). The greatest value comes from connecting multiple 📡 Signal Providers to the 🧬 Flux Composer to find confluence between signals. Contrary to most other indicators that connect with each other, the signals that are passed are not just binary signals ("buy" or "sell") but pass the actual GDM and QMC values. This gives the opportunity in the 🧬 Flux Composer to more accurately use multiple signals with different strengths to finally give an overall signal. On its turn, the Flux Composer can be connected to the GYTS "🎼 Order Orchestrator" for backtesting and trade automation.

[GYTS-Pro] Signal Provider | WaveTrend 4D with GDM + QMCWaveTrend 4D with GDM + QMC (Professional Edition)

🌸 " 📡 Signal Provider" in GoemonYae Trading System (GYTS) 🌸

WaveTrend 4D (WT4D) is an extension of the incredible WaveTrend 3D (2022, Justin Dehorty) . This oscillator elevates the classic WaveTrend by integrating advanced mathematical models for a multi-dimensional view of market momentum, capturing subtle shifts and trends that traditional indicators might miss. Each oscillator layer uses a combination of normalised derivatives, hyperbolic tangent transformations, and dual-pole filtering (John Ehlers' SuperSmoother), providing a normalised and smooth signals.

WT4D strives to help discriminating high-quality signals from the indicator by introducing the Gradient Divergence Measure (GDM) and Quantile Median Crosses (QMC) -- see below for more information.

WaveTrend 4D is a "📡 Signal Provider" in the 🌸 GoemonYae Trading System (GYTS) 🌸. Multiple 📡 Signal Providers connect to a GYTS "🧬 Flux Composer" to find confluence. On its turn, the Flux Composer can be connected to the GYTS "🎼 Order Orchestrator" for backtesting and trade automation. However, WaveTrend 4D is a wonderful indicator on its own as well.

🌸 --- MAIN FEATURES --- 🌸

- The focus is on two type of signals: divergences between the overall trend and the waves (GDM) and the weakening of strong trends (QMC)

- The name "WaveTrend 4D" is derived from the usage of 4 dimensions, representing different frequencies or timeframes. This gives the opportunity to use 2 sets of 3 frequencies to find divergences. Next to the "fast", "normal" and "slow" frequency, the fourth frequency is called "lethargic" (very slow).

- High probability trading involves diligently determining the significance of signals. For this purpose, a novel "Gradient Divergence Measure" (GDM) is developed to signify the strength of divergence signals and are drawn as triangles next to the divergence circles.

- Another and powerful approach is to use the frequencies' crossing of the median (zero) line. We seek to only signal reversals after a significant trend, and call this the "Quantile Median Crosses" (QMC).

More information the GDM and QMC and details of all features are described below.

🌸 --- GRADIENT DIVERGENCE MEASURE (GDM) --- 🌸

💮 Introduction

--

The GDM dynamically calculates a composite measure based on multiple factors. Unlike traditional binary divergence indicators, GDM employs a continuous value system to capture the nuanced dynamics of market behaviour. This methodology allows traders and analysts to assess the potency of divergence signals with greater precision, facilitating more informed decision-making processes.

💮 Methodology

--

The GDM is calculated using a composite formula that integrates various market dynamics. At its core, it consists of six components listed below, each weighted to optimize the indicator's responsiveness to market conditions:

The magnitude of relative change between waves -- A larger difference between the waves, i.e. lower high or higher low could signify a stronger divergence.

The absolute value of the latest wave -- The strength of the latest wave provides insight into the extremity of the market conditions.

Slope of the divergence -- The slope between the two points of divergence essentially measures the rate of change in the frequency\'s value over time. It captures both the direction and the steepness of the indicator’s move between two waves.

The magnitude of relative change of the price -- A divergence means that the oscillator shows an opposite pattern than price action. Thus, if the price makes a significantly higher high or lower low, but the indicator does not, this discrepancy can be used to measure the divergence strength. This components measures the price's extrema during the crosses of the indicator's waves.

Higher timeframe's frequency trend -- Similarly, instead of looking at the price directly, this component measures the more general trend of the price by using the higher timeframe frequency (i.e. the slow frequency when looking at divergences of the normal frequency).

Time duration -- Lastly, the time duration between the two points of a divergence can also be a factor. A divergence that spans over a longer period might indicate a more significant market sentiment shift.

Note that these 6 components are not independent, e.g. the slope is actually the result of the magnitude between waves, the absolute value and time duration. However, the default GDM is carefully tuned to include all these features without being too sensitive to outliers.

💮 Tuning the GDM

--

At the same time, different people have different ideas of what factors are important to denote a "strong" divergence. For this reason, in the 🧰 Professional Edition of this indicator, as opposed to the 🤲 Community Edition, the user can select between different "GDM profiles" that resemble a certain approach:

Upon initiating the GDM indicator, users are prompted to select one of six distinct profiles. Each profile adjusts the indicator’s parameters to optimize performance under different market scenarios:

balanced : Offers a general approach, with a balanced assessment of market conditions without specific focus on any one aspect.

regular divergence : Emphasises price action, ideal for identifying classical divergence patterns where price and momentum diverge.

wavetrend focus : Minimises the influence of price action, concentrating on the WaveTrend oscillator’s behaviour for trend analysis.

short-term waves : Prioritises the slope of the waves, targeting traders interested in short-term market movements and potential inflection points.

long-term waves : Extends the analysis period, focusing on longer-term market trends and wave duration for strategic positioning.

overbought/oversold : Highlights extreme conditions in market valuation, useful for identifying potential reversal points from overbought or oversold levels.

The 🎩 Ultimate Edition takes it a step further and gives full freedom to dial in weights for each of the 6 components. The GDM formula is set up in such way to accommodate ease of use and react logically to these parameters. Having said that, the default GDM calculation should be more than sufficient for most cases.

Another way of tuning the GDM is to dial in the "sensitivity". This controls the extent of normalisation between signals, and essentially affects how often strong GDMs appear. At the conservative end (higher sensitivity), the strong GDMs are less frequent but are relatively significant, while with a lower sensitivity the strong GDMs appear more frequent.

💮 GDM on the Oscillator

--

Coming back to the indicator, the GDMs are represented by triangles and their value represents the strength. A value close to `1` signifies a strong bearish divergence and thus a possible reversal of continuation of a downtrend. Similarly, a value close to `-1` signifies a strong bullish divergence.

Note that there are two colour sets which can be enabled and disabled. One uses crosses between the fast and normal frequencies (with the slow frequency acting as the price trend with which there should be an opposite interaction -- "divergence"). Similarly, crosses between the normal and slow frequencies (with the lethargic (the most slow) frequency acting as the price trend) are used to find divergences on a higher timeframe.

🌸 --- QUANTILE MEDIAN CROSSES (QMC) --- 🌸

💮 Introduction

--

A different and powerful approach is to use the frequencies' crossing of the median (zero) line. This would signify a continuation of the reversal. However, also here, not all of those crossings would be trades with a high probability of success. For this reason, we seek to only consider reversals after the most strong trends start to show weakness. We call these reversals the "Quantile Median Crosses" (QMC), derived from the methodology.

💮 Methodology

--

To find this "most strong trends", we calculate the integral ("the area") of a frequency between all historical median crosses, and take an upper quantile of those integrals. This means that when the series is crossing the median in often (consolidation), the ares between those crosses would be small. But if there was a strong momentum, and the series would separate itself significantly from the median and would do so for a long time, its area would be large.

So after considering all the past integrals, we take the upper quantile of those (i.e. sort all integral and for example take the top 5%) and if the latest trend's integral was in this upper quantile, it is considered "significant". Hence, the name "quantile" in the name "Quantile Median Cross"

💮 Tuning the QMC

--

The QMC is easily tuned by its "sensitivity". This basically represents a set of quantile bounds for the normal, slow and lethargic series. We have set these 3 parameters for each sensitivity profile after careful testing. The 🎩 Ultimate Edition gives full control for each quantile bound.

💮 QMC on the Oscillator

--

The QMC is shown as a label "🔴" above the median or with "🟢" below the median. In the 🎩 Ultimate Edition, the user instead sees the exact quantile and the number of samples. The normal frequency has a "bronze" colour, the slow frequency "silver" and the lethargic is "gold". In addition to the labels, there are also diamond shapes in the same colour drawn on the median in the oscillator. This represents the previous median crossing, and helps the user to see between which two points the integral is calculated.

🌸 --- DETAILED FEATURES --- 🌸

As discussed, at its core, the main signals are the Gradient Divergence Signals (GDM) and Quantile Median Crosses (QMC). However, there are more very powerful features that this 📡 Signal Provider can include. Below is a list of all features and we differentiate the availability of a feature per 📡 Signal Provider version by using these icons: 🤲 Community Edition; 🧰 Professional Edition; 🎩 Ultimate Edition.

Before going into the features, there are two important aspects to note: As this is a 📡 Signal Provider, it can be connected to the GYTS 🧬 Flux Composer and this is possible for each edition (i.e. the 🤲 Community Edition 📡 Signal Composer works with the 🤲 Community Edition 🧬 Flux Composer, and the same holds for the 🧰 Professional and 🎩 Ultimate Editions). Contrary to most other indicators that connect with each other, the signals that are passed are not just binary signals ("buy" or "sell") but pass the actual GDM and QMC values. This gives the opportunity in the 🧬 Flux Composer to more accurately use multiple signals with different strengths to finally give an overall signal.

The second important aspect is that for the 🤲 Community Edition, there are two versions of this 📡 Signal Provider: one that has the GDM feature and another the QMC feature. Besides that, the list below depicts a fairly complete overview of all the features across different versions:

( 🤲 🧰 🎩 ) Four Dimensions -- All four dimensions are available for each edition. The input data can also be transformed with an EMA or CoG as in the original WaveTrend 3D.

( -- 🧰 🎩 ) Both GDM and QMC -- Only the Pro and Ult versions include both the GDM and QMC in one indicator

( 🤲 🧰 🎩 ) Custom indicator name -- There's an option to give a name to the indicator which will be displayed on the chart. On its own, it might not be helpful, but in the GoemonYae Trading System (GYTS) suite, it helps to identify the different Signal Providers.

( 🤲 🧰 🎩 ) Visual improvements -- As in the original WaveTrend 3D, there are various ways the indicator can be displayed, including emphasising a certain frequency, a "mirror mode" and separating each frequency. We have expanded on some of these options. For example, the divergences, GDMs and QMCs are also displayed when the frequencies are separated, the mirror mode works with the emphasised frequency, there are more options to control the width of the emphasised frequency and each frequency can be enabled or disabled.

( 🤲 🧰 🎩 ) Support for HTF -- The indicator works on higher timeframes than the current chart and all parameters and calculations are scaled accordingly.

( __ 🧰 🎩 ) Support for other tickers -- There is also an option to select another ticker than the current chart. This especially makes sense in the 🌸 GYTS suite 🌸, where multiple Signal Providers are combined to find confluence. For example, a common approach is to use a certain ETF (or BTC in crypto) on a higher timeframe as filter to determine overall market direction.

( __ __ 🎩 ) Disable "only true divergences" -- In the Ultimate Edition, less signals can be filtered out when disabling looking at the third frequency. In general, this is not the best idea but it can be helpful when filtering signals with other means.

( __ 🧰 __ ) GDM profiles -- As mentioned, the GDM is carefully tuned and we consider it an excellent method to signify the strength of a divergence. Therefore, the standard calculation in the Community Edition is sufficient. Nevertheless, the Pro Edition has profiles (as previously described) so the user can select how (s)he feels a "strong divergence" should be.

( __ __ 🎩 ) GDM weights -- Full control over the weights of the 6 components of the GDM instead of using the profiles. The GDM algorithm is set up in such way that this is possible in an intuitive way.

( __ __ 🎩 ) Disable asymmetric GDM calculation -- Calculate the bullish and bearish GDMs independently (asymmetric calculation) or normalise them altogether (symmetric calculation). This can sometimes be helpful to filter out weaker GDMs depending on market conditions.

( 🤲 🧰 🎩 ) QMC calculation -- Using the QMC is possible in all versions, and each of the Normal, Slow and Lethargic frequencies can be toggled on and off.

( __ 🧰 __ ) QMC sensitivity -- Similar to the GDM profiles, in the Pro version there are presets to make the sensitivity higher (and thus get more signals) or lower.

( __ __ 🎩 ) QMC quantile threshold -- Instead of the sensitivity presets, in the Ult Edition the quantile threshold for each frequency is set. The user also sees the actual quantile and number of samples in the label

( 🤲 🧰 🎩 ) WaveTrend 4D settings -- Possibility to adjust the core WaveTrend settings

( 🤲 🧰 🎩 ) Alerts -- When alerts are enabled, TradingView will notify when there is a bullish/bearish strong GDM (i.e. within the zone) and a bullish/bearish QMC.

PhiSmoother Moving Average Ribbon [ChartPrime]DSP FILTRATION PRIMER:

DSP (Digital Signal Processing) filtration plays a critical role with financial indication analysis, involving the application of digital filters to extract actionable insights from data. Its primary trading purpose is to distinguish and isolate relevant signals separate from market noise, allowing traders to enhance focus on underlying trends and patterns. By smoothing out price data, DSP filters aid with trend detection, facilitating the formulation of more effective trading techniques.

Additionally, DSP filtration can play an impactful role with detecting support and resistance levels within financial movements. By filtering out noise and emphasizing significant price movements, identifying key levels for entry and exit points become more apparent. Furthermore, DSP methods are instrumental in measuring market volatility, enabling traders to assess volatility levels with improved accuracy.

In summary, DSP filtration techniques are versatile tools for traders and analysts, enhancing decision-making processes in financial markets. By mitigating noise and highlighting relevant signals, DSP filtration improves the overall quality of trading analysis, ultimately leading to better conclusions for market participants.

APPLYING FIR FILTERS:

FIR (Finite Impulse Response) filters are indispensable tools in the realm of financial analysis, particularly for trend identification and characterization within market data. These filters effectively smooth out price fluctuations and noise, enabling traders to discern underlying trends with greater fidelity. By applying FIR filters to price data, robust trading strategies can be developed with grounded trend-following principles, enhancing their ability to capitalize on market movements.

Moreover, FIR filter applications extend into wide-ranging utility within various fields, one being vital for informed decision-making in analysis. These filters help identify critical price levels where assets may tend to stall or reverse direction, providing traders with valuable insights to aid with identification of optimal entry and exit points within their indicator arsenal. FIRs are undoubtedly a cornerstone to modern trading innovation.

Additionally, FIR filters aid in volatility measurement and analysis, allowing traders to gauge market volatility accurately and adjust their risk management approaches accordingly. By incorporating FIR filters into their analytical arsenal, traders can improve the quality of their decision-making processes and achieve better trading outcomes when contending with highly dynamic market conditions.

INTRODUCTORY DEBUT:

ChartPrime's " PhiSmoother Moving Average Ribbon " indicator aims to mark a significant advancement in technical analysis methodology by removing unwanted fluctuations and disturbances while minimizing phase disturbance and lag. This indicator introduces PhiSmoother, a powerful FIR filter in it's own right comparable to Ehlers' SuperSmoother.

PhiSmoother leverages a custom tailored FIR filter to smooth out price fluctuations by mitigating aliasing noise problematic to identification of underlying trends with accuracy. With adjustable parameters such as phase control, traders can fine-tune the indicator to suit their specific analytical needs, providing a flexible and customizable solution.

Mathemagically, PhiSmoother incorporates various color coding preferences, enabling traders to visualize trends more effectively on a volatile landscape. Whether utilizing progression, chameleon, or binary color schemes, you can more fluidly interpret market dynamics and make informed visual decisions regarding entry and exit points based on color-coded plotting.

The indicator's alert system further enhances its utility by providing notifications of specifically chosen filter crossings. Traders can customize alert modes and messages while ensuring they stay informed about potential opportunities aligned with their trading style.

Overall, the "PhiSmoother Moving Average Ribbon" visually stands out as a revolutionary mechanism for technical analysis, offering traders a comprehensive solution for trend identification, visualization, and alerting within financial markets to achieve advantageous outcomes.

NOTEWORTHY SETTINGS FEATURES:

Price Source Selection - The indicator offers flexibility in choosing the price source for analysis. Traders can select from multiple options.

Phase Control Parameter - One of the notable standout features of this indicator is the phase control parameter. Traders can fine-tune the phase or lag of the indicator to adapt it to different market conditions or timeframes. This feature enables optimization of the indicator's responsiveness to price movements and align it with their specific trading tactics.

Coloring Preferences - Another magical setting is the coloring features, one being "Chameleon Color Magic". Traders can customize the color scheme of the indicator based on their visual preferences or to improve interpretation. The indicator offers options such as progression, chameleon, or binary color schemes, all having versatility to dynamically visualize market trends and patterns. Two colors may be specifically chosen to reduce overlay indicator interference while also contrasting for your visual acuity.

Alert Controls - The indicator provides diverse alert controls to manage alerts for specific market events, depending on their trading preferences.

Alertable Crossings: Receive an alert based on selectable predefined crossovers between moving average neighbors

Customizable Alert Messages: Traders can personalize alert messages with preferred information details

Alert Frequency Control: The frequency of alerts is adjustable for maximum control of timely notifications

Weighted Average Volume Depth [QuantraSystems]Weighted Average Volume Depth

Introduction

The Weighted Average Volume Depth (𝓦𝓐𝓥𝓓) indicator is calibrated to provide extensive insights, calculated using volumetric price action and volume depth, and provides dynamic adjustments based upon historical volatility.

This indicator is a valuable asset for traders and investors, aiming to capture trends, measure dynamic volatility, and provide market reversion analysis in a systematic way.

Legend

Volumetric Top Cap: Plotted at y = 0, this line represents the probabilistic maximum value, or ‘cap’ for the signal line. It is colored using a binary color scheme, and indicates the dominant trend direction - green for an uptrend and purple for a downtrend.

Base Line: Calculated using a volume-weighted volatility measurement, this line is used as the benchmark to calculate momentum in the 𝓦𝓐𝓥𝓓 indicator.

Signal Line: The signal line represents the volume and volatility weighted measurements, and oscillates between the Base Line and Top Cap. Its position between these levels provides the depth of insights available in this script.

When the signal line is remaining in close proximity to the base line, this is indicative of a low volatility market environment. These periods are also reflected as muted bar coloring when the ‘Trend Intensity’ setting is enabled.

Conversely, when the signal line approaches, or even breaks above the Top Cap, this is characteristic of an unsustainable trending action - and probabilistically speaking, a reversion or consolation is likely to occur at these levels.

Highlighting: When this setting is enabled, background coloring is applied when the Signal Line breaks above the Top Cap. This highlights green as an oversold zone, and purple as an overbought zone.

Reversal Signals: When price begins to reverse from a zone of overextension, a signal is plotted when this reversion occurs from a high probability zone.

Circle - Shows a possible bullish reversal.

Cross - Shows a possible bearish reversal.

Case Study

In the above image, we showcase three distinct trades in short succession, showcasing the 𝓦𝓐𝓥𝓓’s speed and accuracy under the right conditions.

The first long trade was initiated upon receiving a bullish reversal signal. The trade was then closed after the price experienced a sharp upwards movement - and an overbought signal was indicated by the purple shading.

The second, short trade was entered on the next bar, after a bearish reversal signal was printed by the indicator (a white cross). Similarly, this trade was closed upon the oversold signal.

Once again, a reversal signal was indicated by the 𝓦𝓐𝓥𝓓 indicator. This time a bullish signal (a white circle), and hence a long position was opened. However, this trade was held until a negative trend confirmation (signaled by the Top Cap’s shift in color). This makes apparent the indicator’s flexible nature, and showcases the multiple signaling types available for traders to use.

Recommended Settings

The optimal settings for the 𝓦𝓐𝓥𝓓 indicator will vary upon the chosen asset’s average level volatility, as well as the timeframe it is applied to.

Due to increased volatility levels on lower timeframes, it is recommended to increase the 'Top Cap Multiplier' to take into account the increased frequency of false signals found in these trading environments. The same can be said when used on highly volatile assets - a trader will likely benefit from using a higher 'Top Cap Multiplier.'

On more price-stable assets, as well as any asset on higher timeframes, there is merit to tightening the length of the 'Top Cap Multiplier,' due to the slower nature of price action.

Methodology

The 𝓦𝓐𝓥𝓓 starts with calculating the volume weighted average price and the volume weighted variance - which is the expectation of the squared deviation of a variable from its mean, giving insights into the distribution of trading volume.

Using the volume weighted variance, a standard deviation value is calculated based on user input. This value acts as the ‘Volumetric Top Cap’ - seen in the 𝓦𝓐𝓥𝓓 indicator window as the zero line.

The signal line is calculated as the difference between the current price and the theoretical upper or lower VWAP deviation bands. This line acts as the trigger for identifying prevailing trends and high probability reversal points.

The base line serves as a reference point for historical momentum. It is calculated using an exponential moving average of the lowest signal line values over a defined lookback period. This baseline helps in assessing whether the current momentum is high or low relative to historical norms.

Notes

Bar coloring can be turned off - especially useful when stacking multiple indicators as recommended, or set to 'Trend Intensity,' or 'Binary Trend' (which reflects the top cap coloring).

It is always recommended to never rely on a single indicator - and instead build and test multiple strategies utilizing more than one indicator as confirmation.

Pattern Probability with EMA FilterThe provided code is a custom indicator that identifies specific price patterns on a chart and uses a 14-period Exponential Moving Average (EMA) as a filter to display only certain patterns based on the EMA trend direction. These code identifies patterns display them as upward and downward arrows indicates potential price corrections and short term trend reversals in the direction of the arrow. Use with indicators such as RSI that inform overbought and oversold condition to add reliability and confluence.

Code Explanation:

The code first calculates three values 'a', 'b', and 'c' based on the difference between the current high, low, and close prices, respectively, and their respective previous moving average values.

Binary values are then assigned to 'a', 'b', and 'c', where each value is set to 1 if it's greater than 0, and 0 otherwise.

The 'pattern_type' is determined based on the binary values of 'a', 'b', and 'c', combining them into a single number (ranging from 0 to 7) to represent different price patterns.

The code calculates a 14-period Exponential Moving Average (EMA) of the closing price.

It determines the EMA trend direction by comparing the current EMA value with the previous EMA value, setting 'ema_going_up' to true if the EMA is going up and 'ema_going_down' to true if the EMA is going down.

The indicator then plots arrows on the chart for specific pattern_type values while considering the EMA trend direction as a filter. It displays different colored arrows for each pattern_type.

The 14-period EMA is also plotted on the chart, with the color changing to green when the EMA is going up and red when the EMA is going down.

Concept:

pattern_type = 0: H- L- C- (Downward trend continuation) - Indicates a continuation of the downward trend, suggesting further losses ahead.

pattern_type = 1: H- L- C+ (Likely trend change: Downwards to upwards) - Implies the upward trend or price movement change.

pattern_type = 2: H- L+ C- (Likely trend change: Upwards to downwards) - Suggests a potential reversal from an uptrend to a downtrend, but further confirmation is needed.

pattern_type = 3: H- L+ C+ (Trend uncertainty: Potential reversal) - Indicates uncertainty in the trend, potential for a reversal, but further price action confirmation is required.

pattern_type = 4: H+ L- C- (Downward trend continuation with lower volatility) - Suggests the downward trend may continue, but with reduced price swings or lower volatility.

pattern_type = 5: H+ L- C+ (Likely trend change: Downwards to upwards) - Implies a potential reversal from a downtrend to an uptrend, with buying interest increasing.

(pattern_type = 6: H+ L+ C- (Likely trend change: Upwards to downwards) - Suggests a potential reversal from an uptrend to a downtrend, with selling pressure increasing.

pattern_type = 7: H+ L+ C+ (Upward trend continuation) - Indicates a continuation of the upward trend, suggesting further gains ahead.

In the US market, when analyzing a 15-minute chart, we observe the following proportions of the different pattern_type occurrences: The code will plot the low frequency patterns (P1 - P6)

P0 (H- L- C-): 37.60%

P1 (H- L- C+): 3.60%

P2 (H- L+ C-): 3.10%

P3 (H- L+ C+): 3.40%

P4 (H+ L- C-): 2.90%

P5 (H+ L- C+): 2.70%

P6 (H+ L+ C-): 3.50%

P7 (H+ L+ C+): 43.50%

When analyzing higher time frames, such as daily or weekly charts, the occurrence of these patterns is expected to be even lower, but they may carry more significant implications due to their rarity and potential impact on longer-term trends.

TMA Legacy - "The Arty"This is a script based on the original "The Arty" indicator by PhoenixBinary.