OTT CollectionIf you are not yet familiar with OTT, this script could provide an introduction to help you get started.

"Optimized Trend Tracker" (OTT) is an effective trend-following indicator created by Anıl Özekşi . It aims to detect the current trend direction based on an elegant mathematical construct. The key defining characteristic of OTT is its reliance on a trailing-stop mechanism. This enables OTT to identify price movements and follow the price until a reversal occurs. The widespread adoption of OTT in various algo-trading platforms has fostered the development of diverse applications of the indicator over time. Examining its history, eight distinct applications emerge.

1) OTT - Optimized Trend Tracker

2) TOTT - Twin Ott

3) OTT Channel - Half Channel & Fibonacci Channel

4) RISOTTO - Rsi Ott

5) SOTT - Stochastic Ott

6) HOTT & LOTT - Highest-Lowest Ott + Sum Option

7) ROTT - Relative Ott

8) FT - "Fırsatçı" Trend

BONUS: RTR - Relative True Range

Each system functions as an independent indicator and the "OTT Collection" is intended to present all of them in a single script.

ORIGINALITY

Primarily, this script introduces previously unreleased OTT applications on Tradingview (RISOTTO, ROTT, FT). In contrast to previously published examples that treat OTT as a variable, this script portrays OTT as a function, rendering it adaptable for more intricate computations. Consequently, OTT has evolved into a versatile tool capable of facilitating complex analyses. Furthermore, this script offers an innovative feature that permits the blocking of consecutive signals in the same direction, catering to user preferences. (This feature is crucial for all indicators utilizing band structures such as TOTT and HOTT-LOTT).

USAGE

It is simple to use. The settings section of the indicator groups the parameters. In first group, the System parameter allows you to select the OTT system you want to display on the chart. Activating the Pyramiding parameter enables the display of consecutive signals in the same direction (for TOTT and HOTT-LOTT). In the second group you can change the display options with the Barcolor, Signal and Bars parameters. The OTT system you select is configured with the parameters in the group with the corresponding system heading. (For example, suppose you select OTT CHANNEL in the system parameter. The parameters defining the channels are grouped under the heading "OTT CHANNELS" in the settings section.) Also the parameters you chose are displayed in table form on the chart screen. The table also presents the total number of bars on the chart and the number of signals generated by the selected system.

MECHANICS

Let's take a look at how the indicator works. This indicator incorporates eight distinct OTT systems, each characterized by unique parameters, lines, and signals. (Exception: OTT Channel does not include any referenced signals.)

1) WHAT IS "OTT"?

OTT comprises two lines: Support and Target. There's an up-trending market when the Support is superior to the Target, and a down-trending market when the Support is inferior to the Target. It is governed by two parameters. The Support (moving average) is determined by the Length parameter, while the Multiplier parameter is employed for percentage calculations. Lower values are adept at capturing short-term fluctuations, whereas higher values are more adept at identifying long-term trends. These principles apply to all parameters within the indicator.

DETAILED INFO : The OTT function in the script automatically performs the calculation process described in this section. So, if you know how OTT works you can skip the details. To comprehend its functioning, it's essential to grasp the "MOST" indicator, also devised by Anıl Özekşi. The fundamental principle of MOST involves creating bands that function akin to a trailing stop-loss. Initially, a moving average, referred to as the 'Support,' is established. (Anıl Özekşi employs VAR/VIDYA as the moving average type in all his systems.) Subsequently, the Support line is adjusted both upward and downward by a percentage multiplier to establish a band system. In the context of the trailing stop-loss concept, when the Support line approaches either the lower or upper band, the respective band ceases to move in parallel with the Support line and becomes horizontal. Consequently, the Support always intersects the band at some point. The values of the upper or lower bands, determined by this intersection, are referred to as the MOST line. OTT is generated by consolidating the values of MOST shifted upwards and downwards by half the coefficient percentage into a single line using the same method as above, and calculating the value of this line from two bars ago. Support is the data series of OTT and it serves as a source in OTT function. The OTT line is named as "Target" in this scipt. Support and Target will automatically vary according to the OTT application selected in the "System" parameter.

2) WHAT IS "TOTT"?

Twin OTT , also known as the "OTT Band," involves three parameters: Length, Multiplier, and Band Multiplier. It consists of three lines: Support, Upper Line, and Lower Line. OTT is determined by the Length and Multiplier parameters, while TOTT is calculated by adjusting OTT upwards and downwards as per the Band Multiplier parameter. The indicator generates signals based on the intersections of the Support and these two new OTT levels.

3) WHAT IS "OTT CHANNEL"?

Similar to TOTT, the OTT CHANNEL is also based on shifted OTT levels, employing a similar calculation method. The primary distinction lies in the fact that TOTT has a single Band Multiplier, whereas OTT CHANNEL incorporates two line multipliers for the band. It encompasses four parameters: Length, Multiplier, Upper Line Multiplier, and Lower Line Multiplier. OTT is defined by the Length and Multiplier parameters. The Upper Line Multiplier and Lower Line Multiplier parameters establish the channel boundaries by shifting the OTT line. Subsequently, levels are drawn between the upper and lower lines. The additional Channel Type parameter determines which levels are displayed on the chart. The "Half Channel" option draws channels shifted by half the coefficient. The "Fibonacci Channel" option draws channels shifted by 0.382 and 0.618 coefficients. The "Both" option plots all levels.

4) WHAT IS "RISOTTO"?

OTT also has application examples in momentum oscillators. RISOTTO utilizes the RSI indicator and operates with three parameters. The RSI is defined by the Length 1 parameter, while the Support is determined by the Length 2 parameter. The Multiplier parameter is utilized for percentage calculations. RISOTTO comprises two lines: Support and Target. To ensure more stable calculations, a constant (+1000) is added to the oscillator average when applying OTT to momentum oscillators. This approach eradicates nonsensical results stemming from percentage calculations when the oscillator reaches a value of 0. The indicator generates signals based on the intersection of these two lines.

5) WHAT IS "SOTT"?

Stochastic OTT is an another example of application on oscillator. Its working principle is akin to that of RISOTTO. It operates with three parameters. The Stochastic %k is defined by the Length 1 parameter, while the Stochastic %d is determined by the Length 2 parameter. The Multiplier parameter is utilized for percentage calculations. SOTT comprises two lines: Support and Target. The indicator generates signals based on the intersection of these two lines.

6) WHAT IS "HOTT-LOTT"?

OTT can be applied to the highest and lowest series as well. HOTT-LOTT operates with three parameters: Length, Multiplier, and Sum N Bars. The highest and lowest series are defined by the Length parameter. The Multiplier parameter is utilized for percentage calculations. It encompasses two lines: Upper Line and Lower Line, where HOTT employs the highest series and LOTT uses the lowest series. If the 'High' price surpasses HOTT, the indicator generates Long signals. Similarly, if the 'Low' price falls below LOTT, the indicator generates Short signals. When the Sum N Bars option is activated, signals are generated based on the confirmation concept for N bars.

7) WHAT IS "ROTT"?

Relative OTT serves as a valuable tool for long-period filters. ROTT operates with two parameters. The Support is determined by the length parameter and equals twice the moving average. The Multiplier parameter is utilized for percentage calculations. The indicator generates signals based on the intersection of these two lines.

8) WHAT IS "FT"?

"Fırsatçı" (opportunistic) Trend is a system that revolves around two levels, namely major and minor OTT. It operates with three parameters: Length, Major Multiplier, and Minor Multiplier. FT comprises two lines, Support and Target. The indicator generates signals based on the intersection of these two lines.

9) WHAT IS "RTR"?

Relative True Range is not an OTT system; however, it serves as a complementary feature. It does not have any referenced signals. RTR is devised to obtain a normalized result of the current market volatility. It operates with two parameters: ATR, which is determined by the Length 1 parameter, and RTR, defined by the Length 2 parameter.

A TIP

If any indicator is defined in function form instead of the OTT function, the applications can also be adapted for different indicators. E.g. Supertrend, PMAX, AlphaTrend, etc.

UPDATE

Anıl Özekşi is a competent algotrader who shares his work with open sources. I will update the indicator as new applications are released.

DISCLEIMER

This is just an indicator, nothing more. The script is for informational and educational purposes only. The use of the script does not constitute professional and/or financial advice. The responsibility for risks associated with the use of the script is solely owned by the user. Do not forget to manage your risk. And trade as safely as possible. Good luck!

ค้นหาในสคริปต์สำหรับ "band"

SuperTrend Adaptive (STD Smooth)Supertrend Adaptive (Smoothed StdDev)

Supertrend Adaptive is a refined trend-following indicator based on the classic Supertrend. It enhances the original by incorporating smoothed standard deviation into the volatility calculation, instead of relying solely on ATR. This hybrid approach enables more responsive and adaptive trend detection, reducing noise and false signals in volatile or ranging markets. The indicator also features confidence-weighted signal labels and a clean, uncluttered display, making it practical for any trading timeframe.

🔍 Detailed Methodology and Conceptual Foundation

Unlike traditional Supertrend indicators that use only absolute volatility (ATR) to define trend bands, this version blends standard deviation — a relative volatility measure — into the calculation. Standard deviation helps capture the dispersion of price, not just its range, and when smoothed, it filters out erratic jumps caused by sudden spikes or drops.

This fusion creates trend bands that expand and contract dynamically based on recent price variability. As a result:

Fewer whipsaws : The trend bands adjust to both low and high volatility environments, which helps avoid unnecessary signal flips during consolidation.

Stronger trend adherence : Signals are less reactive to momentary price movements. This allows the indicator to hold positions longer in trending markets, giving traders the opportunity to ride extended moves.

Bollinger Band-style adaptation : By including standard deviation, this indicator behaves similarly to Bollinger Bands — accounting for relative price change rather than absolute moves alone.

These enhancements make the tool suitable not only for identifying directional bias, but also for refining entries and exits with more context-aware volatility filtering.

📈 How to Use the Indicator

Trend Direction: The script draws a colored line beneath (uptrend) or above (downtrend) price. Green indicates bullish trend, red indicates bearish.

Buy/Sell Labels: Only the most recent signal is shown to reduce clutter:

🟢 Green "Buy" label = trend reversal to bullish, with strong confidence.

🔵 Blue "Buy" label = same reversal, but with lower volume confidence.

🔴 Red "Sell" label = trend reversal to bearish, with strong confidence.

🟠 Orange "Sell" label = bearish signal with lower volume confidence.

These color codes are derived from comparing current volume to its average — a higher-than-average volume gives greater confidence to the signal.

Settings:

ATR Period: Controls the smoothing window for volatility calculation.

ATR Multiplier: Adjusts the size of the trend bands.

Std Smooth: Controls smoothing applied to standard deviation to reduce jitter.

Change ATR Method: Option to toggle between default and smoothed ATR.

Show Signals: Toggle for label display.

📢 Alerts

The script includes three built-in alert conditions:

Buy Signal: Triggered when the trend flips to bullish.

Sell Signal: Triggered when the trend flips to bearish.

Trend Direction Change: Alerts on any switch in trend regardless of confidence level.

These alerts allow traders to automate notifications or integrations with bots or trading platforms.

🧼 Clean Chart Display

To ensure clarity and comply with best practices:

The chart shows only this indicator.

Trend lines are drawn in real time for visual context.

Only one label per direction is shown — the most recent one — to keep the chart readable.

No drawings or unrelated indicators are included.

This setup ensures the script’s signals and structure are immediately understandable at a glance.

📌 Best Use Cases

This tool is designed for:

Traders who want adaptive volatility filters instead of rigid ATR-based models.

Scalpers and swing traders who prefer clean charts with minimal lag and fewer false signals.

Any asset class — works well on crypto, FX, and equities.

Shortcoming of this tool is sideway price action (will be tackled in next versions).

Credit for www.tradingview.com the version which this script extends.

Expected Intraday MovementThis indicator pretends to represent the "probable" maximum movement of an asset, for the rest of the day.

This indicator should be used "only" in intraday timeframe. You will not be able to see it if you select a longer timeframe.

To calculate the probable maximum movement, the indicator uses the VIX value for each minute.

On the first candle of the day, it also calculates the probable maximum movement for the whole day, and plots it in horizontal lines.

It also allows adding a couple of extra lines (for visual purposes only).

It also allows the creation of alerts, so that when the value of the asset is close to one of the limits, it can send you an alert using the Tradingview alert system.

Summary of parameters:

Intraday bands: allows you to show/hide the bands for each minute.

Intraday first candle projection: allows to show/hide the estimated projection from the first candle of the day.

Enable alert: allows to enable/disable alerts.

Upper and lower band offset: optional offset where alarms will be triggered (e.g. 10 points before the limit is reached).

Intraday Extra Projection: allows to show/hide extra levels (for visual purposes only)

Upper and lower extra: values for extra levels.

As always, no indicator is meant to provide a single, reliable strategy to your trading regimen and no indicator or group of indicators should be relied on solely. Be sure to do your own analysis and assessments of the stock prior to taking any trades.

Safe trades everyone!

RSI + BB + ATR Short SignalThis indicator highlights potential short setups by combining three conditions:

RSI Overbought – RSI must be above the user-defined level.

Bollinger Band Break – Price must close above the upper Bollinger Band.

Extended Above the 5-Day Low – Price must sit at least X ATR above the recent 5-day low.

When all conditions line up on the same bar, the script plots a red triangle above the candle and triggers an alert so you can act immediately.

To help visualise the setup, the script also plots the full Bollinger Bands (upper, middle, lower) and a line showing the threshold of 5-day-low + ATR × multiplier. You can adjust RSI length and level, Bollinger settings, ATR length, and the ATR multiplier.

triple Keltner Channels with Z-Score V2This script expands on the classic Keltner Channel by plotting three adaptive volatility bands around an EMA baseline and introducing a dynamic Z-Score calculation to quantify price positioning within or beyond those bands.

Features

Three Keltner Channels:

Inner Channel at ×2 ATR

Outer Channel at ×3 ATR

Extended Channel at ×3.5 ATR

Customizable Inputs: EMA length, ATR length, and multipliers can be adjusted to suit different market conditions or asset volatility.

Z-Score Integration: Converts price location relative to the channels into standardized scores (from +2.5 to –2.5). Positive Z indicate a good value/zone to buy while negative one is the contrary (do not use it alone, use it with other indicators )

This provides a statistical lens for identifying overextended, neutral, or mean-reverting conditions.

Visual Clarity: Channel fills highlight volatility zones, while an on-chart label dynamically displays the current Z-Score.

How to Use

Overbought/Oversold Signals: Extreme Z-Score readings (±2 and beyond) suggest stretched conditions that often precede pullbacks or reversions.

Mean Reversion vs Breakout: Traders can assess whether price is likely to revert to the mean (EMA) or sustain momentum beyond outer bands.

Originality

Unlike a standard Keltner Channel, this one:

Uses three progressively wider ATR multiples for deeper volatility mapping.

Adds a Z-Score framework to statistically measure price displacement.

Provides a visual + numerical hybrid output (bands + live Z-Score label).

use only on 1W timeframe

20-34 Dual Dot Alerts OnlyPine Script that uses dual Donchian Channels (20-period and 34-period) and places tiny blue dots above candles when the highest price touches any upper Donchian Channel and below candles when the lowest price touches any lower Donchian Channel, without displaying the channels themselves, you can use the code.

### Explanation of the Code:

1. **Indicator Declaration**: The script is named "Dual Donchian Channels Dots Only" and overlays on the price chart.

2. **Input for Lengths**: Users can set lengths for two Donchian Channels (20 and 34 periods).

3. **Calculating Bands**: The upper and lower bands are calculated using `ta.highest` and `ta.lowest` functions over the specified periods.

4. **Touch Conditions**:

- `upperTouch`: Checks if the highest price of the current candle touches either of the upper bands.

- `lowerTouch`: Checks if the lowest price of the current candle touches either of the lower bands.

5. **Plotting Dots**:

- A tiny blue dot is plotted above bars where `upperTouch` is true.

- A tiny blue dot is plotted below bars where `lowerTouch` is true.

### How to Use:

1. Copy this script into TradingView’s Pine Script editor.

2. Save it and add it to your chart.

3. You will see tiny blue dots appear above or below candles based on whether they touch any of the upper or lower Donchian Bands.

This setup provides a clear visual indication of price interactions with both Donchian Channels while keeping the chart uncluttered by hiding the channel lines.

[EmreKB] BB Trend MagicThe BB Magic indicator is a trend-following tool that operates similarly to the Trend Magic indicator but uses the upper and lower values of Bollinger Bands. It works by dynamically adjusting its reference point based on the price's relationship with the Bollinger Bands.

Initially, the indicator uses the Bollinger Bands' lower value (BB Lower) as its reference. If the price reaches a higher BB Lower value, the BB Magic value is updated to this new BB Lower. This process continues as long as the price remains above the BB Magic value.

However, if the price closes below the BB Magic value, the reference point switches to the Bollinger Bands' upper value (BB Upper). In this case, the BB Magic value is updated to the new BB Upper value if the price creates a lower BB Upper. This mechanism helps capture downtrends effectively.

Whenever the price crosses above the BB Magic value again, the reference point switches back to BB Lower, and the cycle repeats. This approach allows the BB Magic indicator to adapt to price movements and trend changes more accurately, providing a reliable tool for traders to analyze market trends and make informed decisions.

Feel free to share your experiences and feedback on using the BB Magic indicator.

200 EMA Trend Strategy Anti meanDescription:

The "200 EMA Trend Strategy" is a versatile technical analysis tool designed for day trading and long-term investing. It aims to identify potential trend reversal points in the market based on the interaction between the price and the 200-period Exponential Moving Average (EMA). This strategy utilizes the 200 EMA, standard deviation bands, and basic trend analysis to generate buy and sell signals.

Key Features:

200-period Exponential Moving Average (EMA): The indicator plots the 200-period Exponential Moving Average, a reliable trend-following indicator that smooths out price data to identify the underlying trend direction.

Standard Deviation Bands: Upper and lower bands around the 200 EMA are calculated based on a specified standard deviation multiplier. These bands help identify potential overbought and oversold levels in the market.

Trend Signals: Buy signals are generated when the price crosses above the 200 EMA, indicating a potential bullish trend, while sell signals are generated when the price crosses below the 200 EMA, indicating a potential bearish trend.

Exit Signals: Exit signals are triggered when the price moves beyond the standard deviation bands in the opposite direction of the current trend. Most trades will be exited with minimal losses, aiming to grow the trading account over time. Multiple exit signals may be displayed, but only the first signal will be considered, ignoring subsequent signals to minimize drawdown.

Usage:

Day Trading: For intraday trading, traders can use a one-minute chart and fix the indicator's timeframe to five minutes. This allows for quick decision-making and minimizes drawdown by focusing on short-term price movements.

Long-Term Investing: For long-term investing, traders can utilize a four-hour or two-hour chart and fix the indicator's timeframe to daily or one-day timeframe. This provides a broader perspective of the market trends and allows for strategic positioning over longer time horizons.

Risk Management: Employ proper risk management techniques and position sizing strategies to mitigate losses and maximize profits. Use the indicator's exit signals to exit trades with minimal losses and allow profitable trades to grow the trading account over time.

Risk Disclosure: Trading involves risks, and this indicator should be used as part of a comprehensive trading strategy. It is essential to consider risk management principles and employ proper position sizing techniques when trading based on the signals generated by this indicator.

Contrarian DC Strategy - w Entry SL Pause and TrailingStopDonchian Channel Setup:

The strategy uses a tool called the Donchian Channel. Imagine this as two lines (bands) on a chart that show the highest and lowest prices over a certain number of past trading days (default is 20 days).

There's also a centerline, which is the average of these two bands.

Entry Conditions for Trades:

Buying (Going Long): The strategy considers buying when the price touches or falls below the lower band of the Donchian Channel. However, this only happens if there has been a pause after a previous losing trade. This pause is a number of candles where no new trades are taken.

Selling (Going Short): Similarly, the strategy considers selling when price reaches or exceeds the upper band of the Donchian Channel. Again, this is subject to a pause after a losing trade.

Stop Loss and Take Profit:

Each trade has a "Stop Loss" and "Take Profit" set. The Stop Loss is a preset price level where the trade will close to prevent further losses if the market moves against your position. The Take Profit does the same but locks in profit if the market moves in your favor.

The Stop Loss is set based on a percentage of the price at which you entered the trade.

The Take Profit is determined by the Risk/Reward Ratio. This ratio helps balance how much you're willing to risk versus the potential reward.

Trailing Stop Loss:

When a trade is profitable, the strategy should involve a "Trailing Stop Loss." This means the Stop Loss level moves (or trails) the price movement to lock in profits as the market moves in your favor.

For a buy trade, if the price moves above the centerline of the Donchian Channel, the Trailing Stop Loss should be adjusted in the middle between the entry price and the centerline. Viceversa for a sell trade, it should be adjusted in the same way if the price goes below the centerline.

IMPORTANT: There's no allert for the trailing stop at the moment.

Post-Stop Loss Pause:

If a trade hits the Stop Loss (i.e., it's a losing trade), the strategy takes a break before opening another trade in the same direction. This pause helps to avoid entering another trade immediately in a potentially unfavorable market.

In summary, this strategy is designed to make trades based on the Donchian Channel, with specific rules for when to enter and exit trades, and mechanisms to manage risk and protect profits. It's contrarian because it tends to buy when the price is low and sell when the price is high, which is opposite to what many traders might do.

Asymmetric Market Momentum Channel█ OVERVIEW

"Asymmetric Market Momentum Channel" is a dynamic channel indicator that adjusts its width based on the actual strength and asymmetry of market momentum. Thanks to the asymmetric band expansion triggered by strong candles, it significantly reduces false breakouts while remaining highly sensitive to genuine moves.

█ CONCEPTS

Traditional volatility channels react too slowly or too uniformly. This indicator introduces asymmetry:

- After a strong bullish candle with a large body and long upper wick, the upper band is pushed much farther than the lower one.

- After a strong bearish candle, the lower band expands more.

As a result, the channel "remembers" the direction of the last real momentum.

- With wide bands (default base_scale 200+), it excels in contrarian (reversal) strategies – price tends to return to the midline, producing clean reversal signals.

- With narrow bands (base_scale set to 100–150), it behaves like a sensitive breakout channel – breakouts from a tight channel deliver very high-quality trend-continuation signals.

█ FEATURES

Fully adjustable asymmetric momentum channel:

- length – SMA period for midline and average range (default 30)

- base_scale – base channel width in % of average candle range (default 200%)

- strength – asymmetry intensity (higher = stronger expansion after powerful candles)

- smooth_len – EMA smoothing of the expansion (default 10)

Visualization:

- Upper band – red, lower band – green

- Midline SMA – gray

- Gradient background fill (enabled by default) – red above midline, green below; intensity controlled by Background Intensity (85 = strong, 95 = very subtle)

Signal modes:

- Contrarian (Reversal) – reversal signals on price returning inside the channel after exceeding it + confirming candle color

- Trend Continuation (Breakout) – classic breakout signals (recommended to lower base_scale to 100–150 for faster triggers)

- Both – displays both types simultaneously

Visual signals:

- Small green triangles below the bar → bullish signal

- Small red triangles above the bar → bearish signal

Alerts: Bullish Signal, Bearish Signal, Any Signal, Breakout Up, Breakout Down

█ HOW TO USE

Add the indicator to your TradingView chart and adjust the settings:

Key parameter:

- base_scale – defines the indicator’s character:

→ 200–300% → wide channel → Contrarian (reversal) mode

→ 100–150% → narrow channel → Trend Continuation (breakout) mode

- strength (default 1.0)

- length (30) – higher values = smoother, more trend-following behavior

smooth_len (10) – lower values = faster reaction to new momentum

Interpretation:

- Wide channel (base_scale ≥ 200) + Contrarian mode → mean-reversion trading

- Narrow channel (base_scale 100–150) + Breakout mode → aggressive trend-following on breakouts

- Both mode works universally – simply change base_scale to completely switch the indicator’s behavior

█ APPLICATIONS

- Scalping & daytrading – narrow channel + Breakout mode on 5–15 min

- Swing trading – narrow or wide channel + Both mode on H1–D1

- Mean-reversion – wide channel + Contrarian mode

- Trend filter – longs only above midline, shorts only below

█ NOTES

- In very strong one-sided trends, contrarian signals generate many false entries – switch exclusively to Trend Continuation (Breakout) mode with a narrow channel.

- Best performance on instruments with clear volatility and volume.

- Always match base_scale to your strategy (wide = reversal, narrow = breakout).

- Combining with volume, support/resistance levels, or indicators like MACD/RSI dramatically improves signal quality.

Closing Price Donchian Channels//@version=5

indicator("Closing Price Donchian Channels", overlay=true)

// Input parameters

length = input.int(20, "Period", minval=1)

showMid = input.bool(true, "Show Middle Line")

// Calculate upper and lower bands based on closing prices

upper = ta.highest(close, length)

lower = ta.lowest(close, length)

mid = (upper + lower) / 2

// Plot the bands

upperBand = plot(upper, "Upper Band", color=color.rgb(0, 184, 222))

lowerBand = plot(lower, "Lower Band", color=color.rgb(0, 184, 222))

midLine = plot(showMid ? mid : na, "Middle Line", color=color.rgb(209, 212, 220))

// Fill the area between bands

fill(upperBand, lowerBand, color=color.rgb(0, 184, 222, 90), title="Channel Fill")

Closing Price Donchian Channels Rayner//@version=5

indicator("Closing Price Donchian Channels", overlay=true)

// Input parameters

length = input.int(20, "Period", minval=1)

showMid = input.bool(true, "Show Middle Line")

// Calculate upper and lower bands based on closing prices

upper = ta.highest(close, length)

lower = ta.lowest(close, length)

mid = (upper + lower) / 2

// Plot the bands

upperBand = plot(upper, "Upper Band", color=color.rgb(0, 184, 222))

lowerBand = plot(lower, "Lower Band", color=color.rgb(0, 184, 222))

midLine = plot(showMid ? mid : na, "Middle Line", color=color.rgb(209, 212, 220))

// Fill the area between bands

fill(upperBand, lowerBand, color=color.rgb(0, 184, 222, 90), title="Channel Fill")

Log Regression Channel (Dezza Fixed v2)This custom indicator builds a curved Logarithmic Regression Channel designed for long-term Bitcoin and macro asset analysis. It performs a linear regression on the logarithm of price to estimate the market’s fair-value growth curve, then converts that back into price space to form upper and lower deviation bands.

It helps identify where price sits relative to its long-term exponential trend — showing potential overvaluation (upper band) or undervaluation (lower band) zones.

Best used on weekly or monthly charts to visualise market cycles and fair-value reversion. Adjustable inputs let you control lookback length, band width, and midline visibility.

Log Regression Channel (Dezza)This custom indicator builds a curved Logarithmic Regression Channel designed for long-term Bitcoin and macro asset analysis. It performs a linear regression on the logarithm of price to estimate the market’s fair-value growth curve, then converts that back into price space to form upper and lower deviation bands.

It helps identify where price sits relative to its long-term exponential trend — showing potential overvaluation (upper band) or undervaluation (lower band) zones.

Best used on weekly or monthly charts to visualise market cycles and fair-value reversion. Adjustable inputs let you control lookback length, band width, and midline visibility.

Session VWAP & ATR H/L ZonesThis script is a comprehensive tool for day traders, designed to visualize key price levels and zones based on volume and volatility within a specific trading session.

Traders would use your script to identify potential areas of support and resistance, gauge the session's trend, and spot opportunities for mean reversion or breakout trades.

Core Concepts Explained

Your script plots three main types of information on the chart, each serving a different purpose for a trader.

1. Session VWAP (Volume-Weighted Average Price) 📈

What it is: The yellow line is the VWAP, which is the average price of an asset for the current trading session, weighted by the volume traded at each price level. It essentially shows the "fair" price for the day according to the market's activity.

How it's used:

Trend Gauge: If the price is consistently trading above the VWAP, it's generally considered a bullish intraday trend. If it's below, the trend is bearish.

Dynamic Support/Resistance: During a trend, traders often look for the price to pull back to the VWAP to find an entry point (e.g., buying a dip to the VWAP in an uptrend).

VWAP Bands: The optional gray, red, and green bands are standard deviations from the VWAP. They measure how far the price has strayed from its "fair value."

2. ATR High/Low Zones (Support & Resistance) 🎯

What they are: These are the shaded green and red areas at the top and bottom of the session's price range.

The red zone (resistance) is calculated by taking the session's current high and subtracting a value based on the Average True Range (ATR), which is a measure of recent volatility.

The green zone (support) is calculated by taking the session's current low and adding the ATR-based value.

How they're used: These are not just lines; they are zones of interest.

Profit-Taking Areas: A trader who is long might consider taking profits when the price enters the red resistance zone.

Reversal Signals: When the price enters one of these zones and shows signs of stalling (e.g., with specific candlestick patterns), it could signal a potential reversal.

3. Previous Session High & Low 📊

What they are: The script plots the high and low from the previous trading session as straight horizontal lines (teal and fuchsia by default).

How they're used: These are extremely significant static levels that many traders watch.

Price Magnets: Price is often drawn to these levels.

Key Inflection Points: A decisive break above the previous day's high can signal strong bullish momentum. Conversely, a failure to break it can indicate weakness. These levels frequently act as strong support or resistance.

VWAP table with color

## 📊 VWAP Table with Color – Clear VWAP Deviation at a Glance

This script displays a **VWAP (Volume-Weighted Average Price)** table in a non-intrusive, color-coded panel on your chart. It helps you **quickly assess where the current price stands relative to VWAP**, classified into sigma bands (standard deviations). The goal is to provide valuable VWAP insight **without cluttering the chart with multiple lines**.

---

### 🔍 Purpose & Concept

VWAP is a powerful tool used by institutional traders to measure the average price an asset has traded at throughout the day, based on both volume and price.

In this script:

- We **do not plot traditional VWAP lines** with multiple ±1σ, ±2σ, etc., on the chart.

- Instead, we **summarize VWAP and its relative position in a table**, color-coded by deviation.

- This provides the **same information**, but in a **cleaner, minimal, and visually digestible format**.

---

### 🧠 VWAP Deviation Classification

The script calculates how far the current price is from the VWAP, in units of **standard deviation (σ)**.

The formula is:

```plaintext

VWAP Delta σ = (Current Price - VWAP) / Standard Deviation

```

This gives you a normalized value for deviation from VWAP, and it is **clamped between -3 and +3** to avoid extreme outliers.

Each range is color-coded and classified as:

| VWAP Δσ | Zone | Interpretation | Color |

|---------|---------------|------------------------------------------|--------------|

| -3σ | Far Below | Strongly below VWAP – potentially oversold | 🔴 Red |

| -2σ | Below | Below VWAP – bearish territory | 🟠 Orange |

| -1σ | Slightly Below| Slightly under VWAP – weak signal | 🟡 Yellow |

| 0σ | At VWAP | Price is around VWAP – neutral zone | ⚪ Gray |

| +1σ | Slightly Above| Slightly above VWAP – weak bullish | 🟢 Lime Green |

| +2σ | Above | Above VWAP – bullish signal | 🟢 Green |

| +3σ | Far Above | Strongly above VWAP – potentially overbought | 🟦 Teal |

This **compact summary in the table** provides a clear situational view while keeping the chart clean.

---

### ⚙️ User Customization

Users can configure:

- **VWAP σ Multiplier** (default 0.1) to set the width of the optional VWAP band on the chart.

- **Table Position** (Top Center, Bottom Right, etc.).

- **Text Size** and **Text Color**.

- **Hide VWAP logic**: VWAP data can be hidden automatically on higher timeframes (e.g., daily or weekly).

- **Enable/disable the VWAP ±σ band lines** (optional visual aid).

---

### 📐 Technical Highlights

- VWAP is recalculated each day using `ta.vwap(hlc3, isNewPeriod, 1)`.

- The band width uses standard deviation and the selected multiplier: `VWAP ± σ * multiplier`.

- Table updates dynamically with the new VWAP values each day.

- To **avoid floating-point rounding issues**, `vwapDelta` is rounded before comparison, ensuring correct background color display.

---

### ✅ Why Use This?

- Keeps your chart **visually clean and readable**.

- Gives **immediate context** to current price action relative to VWAP.

- Helps **discretionary traders** or **scalpers** decide whether price is stretched too far from the mean.

- Easier than tracking multiple σ bands manually.

---

### Example Usage:

- On intraday timeframes, you can identify price exhaustion as it hits ±2σ or ±3σ.

- On a 5-minute chart, if price touches `+3σ`, you may consider taking profits on longs.

- On reversal setups, watch for price at `-3σ` with bullish divergence.

---

### 🧩 Future Enhancements (Optional Ideas)

- Add alerts for when `vwapDelta` crosses thresholds like ±2σ or ±3σ.

- Let user select the timeframe for VWAP source (e.g., 1H, 5M, etc.).

- Extend to display VWAP on session or weekly basis.

---

Let me know if you want a version of this script formatted and cleaned up for direct TradingView publication (with annotations, credits, and formatting). Would you like that?

BAS EnhancedBAS Enhanced Indicator – A Powerful Market Trend & Volatility Tool

The BAS Enhanced Indicator is a cutting-edge trading tool designed to help traders analyze market trends, volatility, and price momentum with precision. This indicator builds upon traditional Bollinger Bands concepts, integrating adaptive price action tracking, dynamic band width analysis, and advanced smoothing techniques to generate clear and actionable trading insights.

🔹 Key Features & Benefits:

✅ Smart Price Selection – Choose between Close, High, Low, HL2, or HLC3 to tailor the indicator to different market conditions.

✅ Dynamic Band Analysis – Measures price movements relative to dynamically calculated upper and lower bands for real-time market assessment.

✅ Volatility & Trend Strength Measurement – The indicator uses a unique Width Calculation (wd) to gauge market volatility, helping traders understand the strength of price movements.

✅ Composite Indicator Calculation – Combines price position and band width with customizable power functions to provide a more refined momentum signal.

✅ Smoothing for Accuracy – Uses Exponential Moving Average (EMA) and Simple Moving Average (SMA) for a clearer trend visualization, reducing noise in volatile markets.

✅ Two Signal Lines for Confirmation – Includes customizable bullish and bearish signal lines, allowing traders to identify breakouts and reversals with greater confidence.

✅ Visual & Alert-Based Trading Signals – The indicator plots:

Smoothed Composite Indicator (Blue Line) – Tracks market momentum

%D Moving Average (Red Line) – A secondary smoothing layer for trend confirmation

Mid Values (Orange & Purple Lines) – Additional volatility references

Signal Lines (Green & Red Horizontal Lines) – Key breakout levels

✅ Built-in Alerts for Trade Signals – Get notified instantly when:

Bullish Alert 🚀 – The indicator crosses above the upper signal line

Bearish Alert 📉 – The indicator crosses below the lower signal line

📈 How to Use the BAS Enhanced Indicator?

🔹 Trend Trading: Use crossovers above Signal Line 2 as a potential buy signal and crossovers below Signal Line 1 as a potential sell signal.

🔹 Volatility Monitoring: When the band width (wd) expands, market volatility is increasing – ideal for breakout traders. When wd contracts, market volatility is low, signaling potential consolidation.

🔹 Momentum Confirmation: Use the %D Moving Average to confirm sustained trend movements before entering a trade.

🚀 Why Use BAS Enhanced?

This indicator is perfect for day traders, swing traders, and trend-followers looking to enhance their market timing, filter false signals, and improve decision-making. Whether you're trading stocks, forex, or crypto, BAS Enhanced helps you stay ahead of market movements with precision and clarity.

🔔 Add BAS Enhanced to your TradingView toolkit today and trade smarter with confidence!

Margen de confianzaIt uses two moving averages (20 and 80). Based on their crossovers, you draw parallel bands.

The zone between these bands signals “confidence.” A downside break warns of risk; an upside break suggests price could push to new highs.

Son 2 medias moviles. Una de 20 y otra de 80. Utilizando los cruces se puede trazar lineas paralelas.

En las zonas que quedan entre estas lineas hay "confianza". Si el precio atraviesa para abajo hay peligro y si atraviesa para arriba puede ir a romper maximos

Maiko Range Scalper (Sideways BB + RSI) – v4 cleanPurpose

It’s a range scalping strategy for crypto. It tries to take small, repeatable trades inside a sideways market: buy near the bottom of the range, sell near the middle/top (and the reverse for shorts).

Core idea (two timeframes)

Define the trading range on a higher timeframe (HTF)

You choose the HTF (e.g., 15m or 1h).

The script finds the highest high and lowest low over a lookback window (e.g., last 96 HTF candles) → these become HTF Resistance and HTF Support.

It also calculates the midline (average of support/resistance).

Trade signals on your lower timeframe (LTF)

You run the strategy on a fast chart (e.g., 1m or 5m).

Entries are only allowed inside the HTF range.

Entry logic (mean reversion)

Indicators on the LTF:

Bollinger Bands (length & std dev configurable).

RSI (length & thresholds configurable).

Optional VWAP proximity filter (price must be within X% of VWAP).

Long setup:

Price touches/under-cuts the lower Bollinger band AND RSI ≤ threshold (default 30) AND price is inside the HTF range (and passes VWAP filter if enabled).

Short setup:

Price touches/exceeds the upper Bollinger band AND RSI ≥ threshold (default 70) AND price is inside the HTF range (and passes VWAP filter if enabled).

Exits and risk

Stop-loss: placed just outside the HTF range with a configurable buffer %:

Long SL = HTF Support × (1 − buffer).

Short SL = HTF Resistance × (1 + buffer).

Take-profit (selectable):

Mid band (the Bollinger basis) → conservative, faster exits.

Opposite band / HTF boundary → more aggressive, higher RR but more give-backs.

Position sizing

A simple cap: maximum position size = percent of account equity (e.g., 20%).

The script calculates quantity from that cap and current price.

Plots you’ll see on the chart

HTF Resistance (red) and HTF Support (green) via plot().

HTF Midline (gray dashed) drawn with a line.new() object (because plot() cannot do dashed).

Bollinger basis/upper/lower on the LTF.

Optional VWAP line (only shown if you enable the filter).

Signal markers (green triangle up for Long setups, red triangle down for Short setups).

Alerts

Two alertconditions:

“Long Setup” – when a long entry condition appears.

“Short Setup” – when a short entry condition appears.

Create alerts from these to get notified in real time.

How to use it (quick start)

Add to a 1m or 5m chart of a liquid coin (BTC, ETH, SOL).

Set HTF timeframe (start with 1h) and lookback (e.g., 96 = ~4 days on 1h).

Keep default Bollinger/RSI first; tune later.

Choose TP mode:

“Mid band” for quick scalps.

“Opposite band/Range” if the range is very clean and you want bigger targets.

Set SL buffer (0.15–0.30% is common; adjust for volatility).

Set Max position % to control size (e.g., 20%).

(Optional) Enable VWAP filter to skip stretched moves.

When it works best

Clearly sideways markets with visible support/resistance on the HTF.

High-liquidity pairs where spreads/fees are small relative to your scalp target.

Limitations & safety notes

True breakouts will invalidate mean-reversion logic—your SL outside the range is there to cut losses fast.

Fees can eat into small scalps—prefer limit orders, rebates, and liquid pairs.

Backtest results vary by exchange data; always forward-test on small size.

If you want, I can:

Add an ATR-based stop/target option.

Provide a study-only version (signals/alerts, no trading engine).

Pre-set risk to your €5,000 plan (e.g., ~0.5% max loss/trade) with calculated qty.

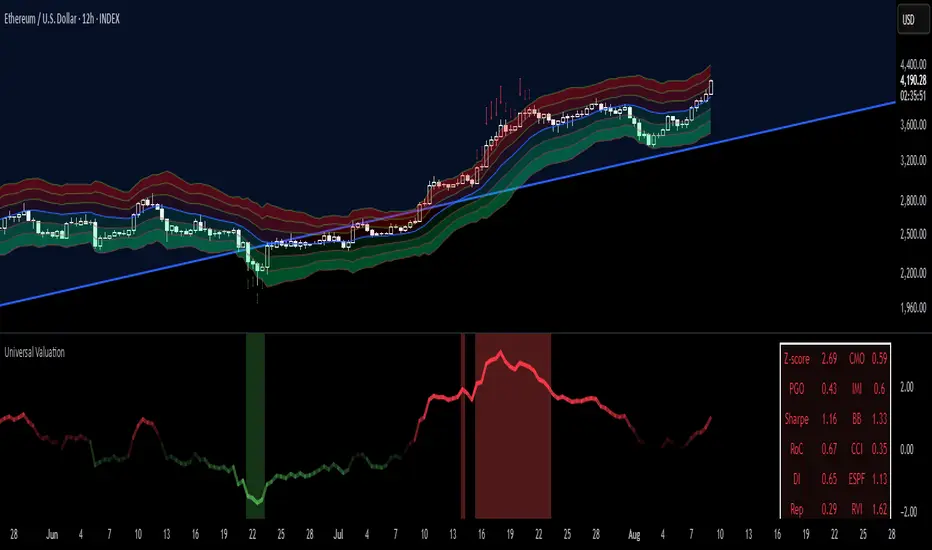

Universal Valuation[public code]Universal valuation indicator for all assets. Consists of 12 different indicators which are z-scored and averaged out.

> Volatility bands via Keltner Channels with a NWMA

> Confluence when price > vol.bands and valuation is high/low. The confluence is marked with red arrows when above the upper third band(green when below the lower on the downside), and 50% transparency when between 2/3 band(green when below the lower 2/3 bands on the downside.)

> Can be used separately of course.

> Can be used as valuation of indicators, when possible. (eg. Global Liquidity index valuation)

Code is a mess a bit, but parts can be extracted and a new strategy/indicator can be made.

*Big probs to the creator of this indicator . Inspired by him. I want to make it possible for people to extrapolate and create their own indicators/strategies. And of course, so I can do the same.

Advanced Donchian ChannelsJust an indicator I got ChatGPT to cook up for my own use, sharing it in case anyone else finds it useful. I have included a screenshot of my own settings as well for reference.

This indicator enhances the classic Donchian Channel with powerful contextual features to support modern breakout and volatility-based trading strategies.

🔹 Core Features:

Donchian Bands: Plots the highest high and lowest low over a configurable lookback period.

Dynamic Fill Shading:

- Color-coded based on the slope of the midline (Basis): Default settings are Green for uptrend, Red for downtrend, Silver for flat, Gray for narrow volatility.

- All fill colors are fully customizable.

Volatility Filter:

- Detects when the channel width is narrow using either a fixed value or a percentage of price.

- Optionally shades only during low-volatility (compression) periods.

Customizable Style:

- Adjustable opacity, offsets, and color settings to suit your charting style.

🛠 Use Cases:

- Spot potential breakout setups after periods of low volatility.

- Identify trend direction via basis slope shading.

- Combine with momentum or volume tools for high-probability entries.

Flashtrader´s Statistical BandwidthsThe vast majority of traders exclusively concern

themselves with trend-following in all its facets. Scoring

points with trends on a regular basis is a difficult task

since prices do not constantly move in one direction

or another. In the case of the DAX future, for example,

only about 30 per cent of all trading days in a year are

trend days. And of these, there are x percent long ones

and x per cent short ones. Catching the very days when

prices rise or fall from the opening to the close is a major

challenge for a trader who also needs to have previously

recognised the corresponding direction.

However, there are also other ways of profit-taking

every day – for example, by using the mean reversion

strategy. The idea behind this is the fact that prices reach

a high and a low every day – but very rarely close at the

high or the low. This means that prices always move

away from these extreme points and the closing price is

somewhere in between. A profitable trading strategy can

be developed out of this.

But how can you know where the high and the low

will be tomorrow? Is it possible for you to know this in

advance? No – because no one can predict the future. Or

can they? At least it can be statistically determined how

high or low prices could go tomorrow. There is a high

degree of probability that one of the two possibilities

will materialise. It will then be necessary to act.

Calculation

Classic pivot points for the following day are calculated

from the high, low and closing price. But does it really

make sense to use such a mix? I don’t think so and

use a different calculation for this strategy. In a first step,

only the differences between the start and the high or low

are calculated on a daily basis. To avoid being dependent

on individual days and outliers, it is advisable to calculate,

in a second step, the average of these differences over

the past five days. Finally, this average will then be added

at the opening price of the current trading day for the

upper statistical bandwidth and subtracted for the lower

bandwidth.

upper bandwidth = oSTB (violet dashed line in the chart)

lower bandwidth = uSTB (violet dashedline in the chart)

The second interesting question is, if the previous day's high has been exceeded, how much further can the price rise from a mathematical/statistical point of view?

These calculated previous day highs expansions are shown as red dashed lines

Previous day's high expansion = VTHA

Previous day's low expansion = VTTA

For further orientation, the previous day's high (VTH) and the previous day's low (VTT) are shown in light blue dashed lines

And as a supplement, the previous day's close in the DAX Future at 10:00 p.m. VTSA in violet solid lines and the previous day's close in the cash register at 5:30 p.m. VTSN in yellow solid lines

Reaching the calculated extreme values does not mean that the trend has to change immediately, but there is at least temporary exhaustion potential with which you can earn a few points every day in the area of scalping.

Example for cheap entry long:

Example for cheap entry short:

Deutsch:

Die Masse der Trader beschäftigt sich ausschließlich mit Trendfolge in all ihren Facetten. Mit Trends regelmäßig zu punkten ist ein schwieriges Unterfangen, da die Kurse nicht ständig in die eine oder andere Richtung laufen. Beim DAX-Future zum Beispiel sind von allen Börsentagen im Jahr lediglich zirka 30 Prozent Trendtage. Davon sind dann auch noch x Prozent Long und x Prozent Short. Hier genau die Tage abzupassen, an denen die Kurse von Börsenbeginn bis zum Schluss steigen beziehungsweise fallen, ist eine große Herausforderung – wobei der Trader zuvor noch die entsprechende Richtung erkannt haben muss. Es gibt jedoch auch noch andere Methoden täglich Gewinne mitzunehmen, zum Beispiel mit der Mean-Reversion-Strategie (Mittelwertumkehr).

Hintergrund ist die Tatsache, dass die Kurse jeden Tag ein Hoch und ein Tief erreichen – aber sehr selten am Hoch oder am Tief schließen. Das bedeutet, dass die Preise sich immer wie der von diesen Extrempunkten wegbewegen und der Schlusskurs irgendwo dazwischen liegt. Hieraus lässt sich eine profitable Handelsstrategie entwickeln. Aber woher kannst Du wissen, wo morgen das Hoch und das Tief sein wird? Kannst Du das vorher schon wissen? Nein – denn niemand kann die Zukunft vorhersagen. Oder doch? Statistisch lässt sich zumindest bestimmen, wie hoch und wie tief die Kurse morgen steigen oder fallen könnten. Eine Seite wird mit sehr hoher Wahrscheinlichkeit ein treffen. Dann gilt es zu handeln.

Berechnung Klassischer Pivot-Punkte für den folgenden Tag werden aus Hoch, Tief und Schlusskurs berechnet. Aber ist es wirklich sinnvoll, einen solchen Mix zu verwenden? Ich finde das nicht und verwenden für diese Strategie eine andere Berechnung. Im ersten Schritt werden täglich die Differenzen nur vom Start bis zum Hoch beziehungsweise Tief errechnet. Um nicht von einzelnen Tagen und Ausreißern abhängig zu sein, empfiehlt es sich, in einem zweiten Schritt den Durchschnitt dieser Differenzen über die letzten fünf Tage zu errechnen. Zuletzt wird dann dieser Durchschnitt zum Eröffnungskurs des aktuellen Handelstages für die obere statistische Bandbreite addiert und für die untere Bandbreite subtrahiert.

Obere statistische Bandbreite = oSTB (violette gestrichelte Linie im Chart)

Untere statistische Bandbreite = uSTB (violette gestrichelte Linie im Chart)

Die zweite interessante Frage ist, wenn das Vortageshoch überschritten wurde, wie weit kann der Kurs dann noch steigen aus mathematisch/statistischer Sicht?

Diese berechneten Vortagesextremausdehnungen sind als rote gestrichelte Linien dargestellt

Vortageshochausdehnung = VTHA

Vortagestiefausdehnung = VTTA

Für die weitere Orientierung sind die Vortageshochs (VTH) und die Vortagestiefs (VTT) als hellblaue gestrichelte Linien abgebildet.

Als Ergänzung wird noch der Vortages Schluss im Dax Future um 22:00 Uhr VTSA mit einer violetten durchgezogenen Linie und der Kassamarktschluss um 17:30 Uhr mit einer gelben durchgezogenen Linie gezeigt.

Das Erreichen der berechneten Extremwerte bedeutet nicht, das der Trend sofort drehen muss, aber es sind zumindest temporäre Erschöpfungspotentiale mit denen sich im Bereich scalping täglich einige Punkte verdienen lassen.

Beispiel für günstigen Einstieg Long:

Beispiel für günstigen Einstieg Short:

Future SD ProjectionFuture Standard Deviation Projector

This innovative indicator projects price volatility into the future, helping traders anticipate potential price ranges and breakouts. It calculates standard deviation bands based on recent price action and extends them forward, providing a unique perspective on future price movement possibilities.

Key Features:

- Projects standard deviation bands into the future

- Customizable lookback period for volatility calculation

- Adjustable future projection timeframe

- Flexible standard deviation multiplier

- Clear visual signals for band breaches

How it works:

1. Calculates standard deviation from recent closing prices

2. Projects upper and lower bands into the future

3. Plots these bands on the chart

4. Signals with arrows when closing price crosses projected bands

Use this indicator to:

- Gauge potential future price ranges

- Identify possible breakout levels

- Assess market volatility expectations

- Enhance your trading strategy with forward-looking volatility projections

Customize the settings to align with your trading timeframe and risk tolerance. Remember, while this tool offers valuable insights, it should be used in conjunction with other analysis methods for comprehensive trading decisions.

Note: Past performance and projections do not guarantee future results. Always manage your risk appropriately.