Luxy Momentum, Trend, Bias and Breakout Indicators V7

TABLE OF CONTENTS

This is Version 7 (V7) - the latest and most optimized release. If you are using any older versions (V6, V5, V4, V3, etc.), it is highly recommended to replace them with V7.

Why This Indicator is Different

Who Should Use This

Core Components Overview

The UT Bot Trading System

Understanding the Market Bias Table

Candlestick Pattern Recognition

Visual Tools and Features

How to Use the Indicator

Performance and Optimization

FAQ

---

### CREDITS & ATTRIBUTION

This indicator implements proven trading concepts using entirely original code developed specifically for this project.

### CONCEPTUAL FOUNDATIONS

• UT Bot ATR Trailing System

- Original concept by @QuantNomad: (search "UT-Bot-Strategy"

- Our version is a complete reimplementation with significant enhancements:

- Volume-weighted momentum adjustment

- Composite stop loss from multiple S/R layers

- Multi-filter confirmation system (swing, %, 2-bar, ZLSMA)

- Full integration with multi-timeframe bias table

- Visual audit trail with freeze-on-touch

- NOTE: No code was copied - this is a complete reimplementation with enhancements.

• Standard Technical Indicators (Public Domain Formulas):

- Supertrend: ATR-based trend calculation with custom gradient fills

- MACD: Gerald Appel's formula with separation filters

- RSI: J. Welles Wilder's formula with pullback zone logic

- ADX/DMI: Custom trend strength formula inspired by Wilder's directional movement concept, reimplemented with volume weighting and efficiency metrics

- ZLSMA: Zero-lag formula enhanced with Hull MA and momentum prediction

### Custom Implementations

- Trend Strength: Inspired by Wilder's ADX concept but using volume-weighted pressure calculation and efficiency metrics (not traditional +DI/-DI smoothing)

- All code implementations are original

### ORIGINAL FEATURES (70%+ of codebase)

- Multi-Timeframe Bias Table with live updates

- Risk Management System (R-multiple TPs, freeze-on-touch)

- Opening Range Breakout tracker with session management

- Composite Stop Loss calculator using 6+ S/R layers

- Performance optimization system (caching, conditional calcs)

- VIX Fear Index integration

- Previous Day High/Low auto-detection

- Candlestick pattern recognition with interactive tooltips

- Smart label and visual management

- All UI/UX design and table architecture

### DEVELOPMENT PROCESS

**AI Assistance:** This indicator was developed over 2+ months with AI assistance (ChatGPT/Claude) used for:

- Writing Pine Script code based on design specifications

- Optimizing performance and fixing bugs

- Ensuring Pine Script v6 compliance

- Generating documentation

**Author's Role:** All trading concepts, system design, feature selection, integration logic, and strategic decisions are original work by the author. The AI was a coding tool, not the system designer.

**Transparency:** We believe in full disclosure - this project demonstrates how AI can be used as a powerful development tool while maintaining creative and strategic ownership.

---

1. WHY THIS INDICATOR IS DIFFERENT

Most traders use multiple separate indicators on their charts, leading to cluttered screens, conflicting signals, and analysis paralysis. The Suite solves this by integrating proven technical tools into a single, cohesive system.

Key Advantages:

All-in-One Design: Instead of loading 5-10 separate indicators, you get everything in one optimized script. This reduces chart clutter and improves TradingView performance.

Multi-Timeframe Bias Table: Unlike standard indicators that only show the current timeframe, the Bias Table aggregates trend signals across multiple timeframes simultaneously. See at a glance whether 1m, 5m, 15m, 1h are aligned bullish or bearish - no more switching between charts.

Smart Confirmations: The indicator doesn't just give signals - it shows you WHY. Every entry has multiple layers of confirmation (MA cross, MACD momentum, ADX strength, RSI pullback, volume, etc.) that you can toggle on/off.

Dynamic Stop Loss System: Instead of static ATR stops, the SL is calculated from multiple support/resistance layers: UT trailing line, Supertrend, VWAP, swing structure, and MA levels. This creates more intelligent, price-action-aware stops.

R-Multiple Take Profits: Built-in TP system calculates targets based on your initial risk (1R, 1.5R, 2R, 3R). Lines freeze when touched with visual checkmarks, giving you a clean audit trail of partial exits.

Educational Tooltips Everywhere: Every single input has detailed tooltips explaining what it does, typical values, and how it impacts trading. You're not guessing - you're learning as you configure.

Performance Optimized: Smart caching, conditional calculations, and modular design mean the indicator runs fast despite having 15+ features. Turn off what you don't use for even better performance.

No Repainting: All signals respect bar close. Alerts fire correctly. What you see in history is what you would have gotten in real-time.

What Makes It Unique:

Integrated UT Bot + Bias Table: No other indicator combines UT Bot's ATR trailing system with a live multi-timeframe dashboard. You get precision entries with macro trend context.

Candlestick Pattern Recognition with Interactive Tooltips: Patterns aren't just marked - hover over any emoji for a full explanation of what the pattern means and how to trade it.

Opening Range Breakout Tracker: Built-in ORB system for intraday traders with customizable session times and real-time status updates in the Bias Table.

Previous Day High/Low Auto-Detection: Automatically plots PDH/PDL on intraday charts with theme-aware colors. Updates daily without manual input.

Dynamic Row Labels in Bias Table: The table shows your actual settings (e.g., "EMA 10 > SMA 20") not generic labels. You know exactly what's being evaluated.

Modular Filter System: Instead of forcing a fixed methodology, the indicator lets you build your own strategy. Start with just UT Bot, add filters one at a time, test what works for your style.

---

2. WHO WHOULD USE THIS

Designed For:

Intermediate to Advanced Traders: You understand basic technical analysis (MAs, RSI, MACD) and want to combine multiple confirmations efficiently. This isn't a "one-click profit" system - it's a professional toolkit.

Multi-Timeframe Traders: If you trade one asset but check multiple timeframes for confirmation (e.g., enter on 5m after checking 15m and 1h alignment), the Bias Table will save you hours every week.

Trend Followers: The indicator excels at identifying and following trends using UT Bot, Supertrend, and MA systems. If you trade breakouts and pullbacks in trending markets, this is built for you.

Intraday and Swing Traders: Works equally well on 5m-1h charts (day trading) and 4h-D charts (swing trading). Scalpers can use it too with appropriate settings adjustments.

Discretionary Traders: This isn't a black-box system. You see all the components, understand the logic, and make final decisions. Perfect for traders who want tools, not automation.

Works Across All Markets:

Stocks (US, international)

Cryptocurrency (24/7 markets supported)

Forex pairs

Indices (SPY, QQQ, etc.)

Commodities

NOT Ideal For :

Complete Beginners: If you don't know what a moving average or RSI is, start with basics first. This indicator assumes foundational knowledge.

Algo Traders Seeking Black Box: This is discretionary. Signals require context and confirmation. Not suitable for blind automated execution.

Mean-Reversion Only Traders: The indicator is trend-following at its core. While VWAP bands support mean-reversion, the primary methodology is trend continuation.

---

3. CORE COMPONENTS OVERVIEW

The indicator combines these proven systems:

Trend Analysis:

Moving Averages: Four customizable MAs (Fast, Medium, Medium-Long, Long) with six types to choose from (EMA, SMA, WMA, VWMA, RMA, HMA). Mix and match for your style.

Supertrend: ATR-based trend indicator with unique gradient fill showing trend strength. One-sided ribbon visualization makes it easier to see momentum building or fading.

ZLSMA : Zero-lag linear-regression smoothed moving average. Reduces lag compared to traditional MAs while maintaining smooth curves.

Momentum & Filters:

MACD: Standard MACD with separation filter to avoid weak crossovers.

RSI: Pullback zone detection - only enter longs when RSI is in your defined "buy zone" and shorts in "sell zone".

ADX/DMI: Trend strength measurement with directional filter. Ensures you only trade when there's actual momentum.

Volume Filter: Relative volume confirmation - require above-average volume for entries.

Donchian Breakout: Optional channel breakout requirement.

Signal Systems:

UT Bot: The primary signal generator. ATR trailing stop that adapts to volatility and gives clear entry/exit points.

Base Signals: MA cross system with all the above filters applied. More conservative than UT Bot alone.

Market Bias Table: Multi-timeframe dashboard showing trend alignment across 7 timeframes plus macro bias (3-day, weekly, monthly, quarterly, VIX).

Candlestick Patterns: Six major reversal patterns auto-detected with interactive tooltips.

ORB Tracker: Opening range high/low with breakout status (intraday only).

PDH/PDL: Previous day levels plotted automatically on intraday charts.

VWAP + Bands : Session-anchored VWAP with up to three standard deviation band pairs.

---

4. THE UT BOT TRADING SYSTEM

The UT Bot is the heart of the indicator's signal generation. It's an advanced ATR trailing stop that adapts to market volatility.

Why UT Bot is Superior to Fixed Stops:

Traditional ATR stops use a fixed multiplier (e.g., "stop = entry - 2×ATR"). UT Bot is smarter:

It TRAILS the stop as price moves in your favor

It WIDENS during high volatility to avoid premature stops

It TIGHTENS during consolidation to lock in profits

It FLIPS when price breaks the trailing line, signaling reversals

Visual Elements You'll See:

Orange Trailing Line: The actual UT stop level that adapts bar-by-bar

Buy/Sell Labels: Aqua triangle (long) or orange triangle (short) when the line flips

ENTRY Line: Horizontal line at your entry price (optional, can be turned off)

Suggested Stop Loss: A composite SL calculated from multiple support/resistance layers:

- UT trailing line

- Supertrend level

- VWAP

- Swing structure (recent lows/highs)

- Long-term MA (200)

- ATR-based floor

Take Profit Lines: TP1, TP1.5, TP2, TP3 based on R-multiples. When price touches a TP, it's marked with a checkmark and the line freezes for audit trail purposes.

Status Messages: "SL Touched ❌" or "SL Frozen" when the trade leg completes.

How UT Bot Differs from Other ATR Systems:

Multiple Filters Available: You can require 2-bar confirmation, minimum % price change, swing structure alignment, or ZLSMA directional filter. Most UT implementations have none of these.

Smart SL Calculation: Instead of just using the UT line as your stop, the indicator suggests a better SL based on actual support/resistance. This prevents getting stopped out by wicks while keeping risk controlled.

Visual Audit Trail: All SL/TP lines freeze when touched with clear markers. You can review your trades weeks later and see exactly where entries, stops, and targets were.

Performance Options: "Draw UT visuals only on bar close" lets you reduce rendering load without affecting logic or alerts - critical for slower machines or 1m charts.

Trading Logic:

UT Bot flips direction (Buy or Sell signal appears)

Check Bias Table for multi-timeframe confirmation

Optional: Wait for Base signal or candlestick pattern

Enter at signal bar close or next bar open

Place stop at "Suggested Stop Loss" line

Scale out at TP levels (TP1, TP2, TP3)

Exit remaining position on opposite UT signal or stop hit

---

5. UNDERSTANDING THE MARKET BIAS TABLE

This is the indicator's unique multi-timeframe intelligence layer. Instead of looking at one chart at a time, the table aggregates signals across seven timeframes plus macro trend bias.

Why Multi-Timeframe Analysis Matters:

Professional traders check higher and lower timeframes for context:

Is the 1h uptrend aligning with my 5m entry?

Are all short-term timeframes bullish or just one?

Is the daily trend supportive or fighting me?

Doing this manually means opening multiple charts, checking each indicator, and making mental notes. The Bias Table does it automatically in one glance.

Table Structure:

Header Row:

On intraday charts: 1m, 5m, 15m, 30m, 1h, 2h, 4h (toggle which ones you want)

On daily+ charts: D, W, M (automatic)

Green dot next to title = live updating

Headline Rows - Macro Bias:

These show broad market direction over longer periods:

3 Day Bias: Trend over last 3 trading sessions (uses 1h data)

Weekly Bias: Trend over last 5 trading sessions (uses 4h data)

Monthly Bias: Trend over last 30 daily bars

Quarterly Bias: Trend over last 13 weekly bars

VIX Fear Index: Market regime based on VIX level - bullish when low, bearish when high

Opening Range Breakout: Status of price vs. session open range (intraday only)

These rows show text: "BULLISH", "BEARISH", or "NEUTRAL"

Indicator Rows - Technical Signals:

These evaluate your configured indicators across all active timeframes:

Fast MA > Medium MA (shows your actual MA settings, e.g., "EMA 10 > SMA 20")

Price > Long MA (e.g., "Price > SMA 200")

Price > VWAP

MACD > Signal

Supertrend (up/down/neutral)

ZLSMA Rising

RSI In Zone

ADX ≥ Minimum

These rows show emojis: GREEB (bullish), RED (bearish), GRAY/YELLOW (neutral/NA)

AVG Column:

Shows percentage of active timeframes that are bullish for that row. This is the KEY metric:

AVG > 70% = strong multi-timeframe bullish alignment

AVG 40-60% = mixed/choppy, no clear trend

AVG < 30% = strong multi-timeframe bearish alignment

How to Use the Table:

For a long trade:

Check AVG column - want to see > 60% ideally

Check headline bias rows - want to see BULLISH, not BEARISH

Check VIX row - bullish market regime preferred

Check ORB row (intraday) - want ABOVE for longs

Scan indicator rows - more green = better confirmation

For a short trade:

Check AVG column - want to see < 40% ideally

Check headline bias rows - want to see BEARISH, not BULLISH

Check VIX row - bearish market regime preferred

Check ORB row (intraday) - want BELOW for shorts

Scan indicator rows - more red = better confirmation

When AVG is 40-60%:

Market is choppy, mixed signals. Either stay out or reduce position size significantly. These are low-probability environments.

Unique Features:

Dynamic Labels: Row names show your actual settings (e.g., "EMA 10 > SMA 20" not generic "Fast > Slow"). You know exactly what's being evaluated.

Customizable Rows: Turn off rows you don't care about. Only show what matters to your strategy.

Customizable Timeframes: On intraday charts, disable 1m or 4h if you don't trade them. Reduces calculation load by 20-40%.

Automatic HTF Handling: On Daily/Weekly/Monthly charts, the table automatically switches to D/W/M columns. No configuration needed.

Performance Smart: "Hide BIAS table on 1D or above" option completely skips all table calculations on higher timeframes if you only trade intraday.

---

6. CANDLESTICK PATTERN RECOGNITION

The indicator automatically detects six major reversal patterns and marks them with emojis at the relevant bars.

Why These Six Patterns:

These are the most statistically significant reversal patterns according to trading literature:

High win rate when appearing at support/resistance

Clear visual structure (not subjective)

Work across all timeframes and assets

Studied extensively by institutions

The Patterns:

Bullish Patterns (appear at bottoms):

Bullish Engulfing: Green candle completely engulfs prior red candle's body. Strong reversal signal.

Hammer: Small body with long lower wick (at least 2× body size). Shows rejection of lower prices by buyers.

Morning Star: Three-candle pattern (large red → small indecision → large green). Very strong bottom reversal.

Bearish Patterns (appear at tops):

Bearish Engulfing: Red candle completely engulfs prior green candle's body. Strong reversal signal.

Shooting Star: Small body with long upper wick (at least 2× body size). Shows rejection of higher prices by sellers.

Evening Star: Three-candle pattern (large green → small indecision → large red). Very strong top reversal.

Interactive Tooltips:

Unlike most pattern indicators that just draw shapes, this one is educational:

Hover your mouse over any pattern emoji

A tooltip appears explaining: what the pattern is, what it means, when it's most reliable, and how to trade it

No need to memorize - learn as you trade

Noise Filter:

"Min candle body % to filter noise" setting prevents false signals:

Patterns require minimum body size relative to price

Filters out tiny candles that don't represent real buying/selling pressure

Adjust based on asset volatility (higher % for crypto, lower for low-volatility stocks)

How to Trade Patterns:

Patterns are NOT standalone entry signals. Use them as:

Confirmation: UT Bot gives signal + pattern appears = stronger entry

Reversal Warning: In a trade, opposite pattern appears = consider tightening stop or taking profit

Support/Resistance Validation: Pattern at key level (PDH, VWAP, MA 200) = level is being respected

Best combined with:

UT Bot or Base signal in same direction

Bias Table alignment (AVG > 60% or < 40%)

Appearance at obvious support/resistance

---

7. VISUAL TOOLS AND FEATURES

VWAP (Volume Weighted Average Price):

Session-anchored VWAP with standard deviation bands. Shows institutional "fair value" for the trading session.

Anchor Options: Session, Day, Week, Month, Quarter, Year. Choose based on your trading timeframe.

Bands: Up to three pairs (X1, X2, X3) showing statistical deviation. Price at outer bands often reverses.

Auto-Hide on HTF: VWAP hides on Daily/Weekly/Monthly charts automatically unless you enable anchored mode.

Use VWAP as:

Directional bias (above = bullish, below = bearish)

Mean reversion levels (outer bands)

Support/resistance (the VWAP line itself)

Previous Day High/Low:

Automatically plots yesterday's high and low on intraday charts:

Updates at start of each new trading day

Theme-aware colors (dark text for light charts, light text for dark charts)

Hidden automatically on Daily/Weekly/Monthly charts

These levels are critical for intraday traders - institutions watch them closely as support/resistance.

Opening Range Breakout (ORB):

Tracks the high/low of the first 5, 15, 30, or 60 minutes of the trading session:

Customizable session times (preset for NYSE, LSE, TSE, or custom)

Shows current breakout status in Bias Table row (ABOVE, BELOW, INSIDE, BUILDING)

Intraday only - auto-disabled on Daily+ charts

ORB is a classic day trading strategy - breakout above opening range often leads to continuation.

Extra Labels:

Change from Open %: Shows how far price has moved from session open (intraday) or daily open (HTF). Green if positive, red if negative.

ADX Badge: Small label at bottom of last bar showing current ADX value. Green when above your minimum threshold, red when below.

RSI Badge: Small label at top of last bar showing current RSI value with zone status (buy zone, sell zone, or neutral).

These labels provide quick at-a-glance confirmation without needing separate indicator windows.

---

8. HOW TO USE THE INDICATOR

Step 1: Add to Chart

Load the indicator on your chosen asset and timeframe

First time: Everything is enabled by default - the chart will look busy

Don't panic - you'll turn off what you don't need

Step 2: Start Simple

Turn OFF everything except:

UT Bot labels (keep these ON)

Bias Table (keep this ON)

Moving Averages (Fast and Medium only)

Suggested Stop Loss and Take Profits

Hide everything else initially. Get comfortable with the basic UT Bot + Bias Table workflow first.

Step 3: Learn the Core Workflow

UT Bot gives a Buy or Sell signal

Check Bias Table AVG column - do you have multi-timeframe alignment?

If yes, enter the trade

Place stop at Suggested Stop Loss line

Scale out at TP levels

Exit on opposite UT signal

Trade this simple system for a week. Get a feel for signal frequency and win rate with your settings.

Step 4: Add Filters Gradually

If you're getting too many losing signals (whipsaws in choppy markets), add filters one at a time:

Try: "Require 2-Bar Trend Confirmation" - wait for 2 bars to confirm direction

Try: ADX filter with minimum threshold - only trade when trend strength is sufficient

Try: RSI pullback filter - only enter on pullbacks, not chasing

Try: Volume filter - require above-average volume

Add one filter, test for a week, evaluate. Repeat.

Step 5: Enable Advanced Features (Optional)

Once you're profitable with the core system, add:

Supertrend for additional trend confirmation

Candlestick patterns for reversal warnings

VWAP for institutional anchor reference

ORB for intraday breakout context

ZLSMA for low-lag trend following

Step 6: Optimize Settings

Every setting has a detailed tooltip explaining what it does and typical values. Hover over any input to read:

What the parameter controls

How it impacts trading

Suggested ranges for scalping, day trading, and swing trading

Start with defaults, then adjust based on your results and style.

Step 7: Set Up Alerts

Right-click chart → Add Alert → Condition: "Luxy Momentum v6" → Choose:

"UT Bot — Buy" for long entries

"UT Bot — Sell" for short entries

"Base Long/Short" for filtered MA cross signals

Optionally enable "Send real-time alert() on UT flip" in settings for immediate notifications.

Common Workflow Variations:

Conservative Trader:

UT signal + Base signal + Candlestick pattern + Bias AVG > 70%

Enter only at major support/resistance

Wider UT sensitivity, multiple filters

Aggressive Trader:

UT signal + Bias AVG > 60%

Enter immediately, no waiting

Tighter UT sensitivity, minimal filters

Swing Trader:

Focus on Daily/Weekly Bias alignment

Ignore intraday noise

Use ORB and PDH/PDL less (or not at all)

Wider stops, patient approach

---

9. PERFORMANCE AND OPTIMIZATION

The indicator is optimized for speed, but with 15+ features running simultaneously, chart load time can add up. Here's how to keep it fast:

Biggest Performance Gains:

Disable Unused Timeframes: In "Time Frames" settings, turn OFF any timeframe you don't actively trade. Each disabled TF saves 10-15% calculation time. If you only day trade 5m, 15m, 1h, disable 1m, 2h, 4h.

Hide Bias Table on Daily+: If you only trade intraday, enable "Hide BIAS table on 1D or above". This skips ALL table calculations on higher timeframes.

Draw UT Visuals Only on Bar Close: Reduces intrabar rendering of SL/TP/Entry lines. Has ZERO impact on logic or alerts - purely visual optimization.

Additional Optimizations:

Turn off VWAP bands if you don't use them

Disable candlestick patterns if you don't trade them

Turn off Supertrend fill if you find it distracting (keep the line)

Reduce "Limit to 10 bars" for SL/TP lines to minimize line objects

Performance Features Built-In:

Smart Caching: Higher timeframe data (3-day bias, weekly bias, etc.) updates once per day, not every bar

Conditional Calculations: Volume filter only calculates when enabled. Swing filter only runs when enabled. Nothing computes if turned off.

Modular Design: Every component is independent. Turn off what you don't need without breaking other features.

Typical Load Times:

5m chart, all features ON, 7 timeframes: ~2-3 seconds

5m chart, core features only, 3 timeframes: ~1 second

1m chart, all features: ~4-5 seconds (many bars to calculate)

If loading takes longer, you likely have too many indicators on the chart total (not just this one).

---

10. FAQ

Q: How is this different from standard UT Bot indicators?

A: Standard UT Bot (originally by @QuantNomad) is just the ATR trailing line and flip signals. This implementation adds:

- Volume weighting and momentum adjustment to the trailing calculation

- Multiple confirmation filters (swing, %, 2-bar, ZLSMA)

- Smart composite stop loss system from multiple S/R layers

- R-multiple take profit system with freeze-on-touch

- Integration with multi-timeframe Bias Table

- Visual audit trail with checkmarks

Q: Can I use this for automated trading?

A: The indicator is designed for discretionary trading. While it has clear signals and alerts, it's not a mechanical system. Context and judgment are required.

Q: Does it repaint?

A: No. All signals respect bar close. UT Bot logic runs intrabar but signals only trigger on confirmed bars. Alerts fire correctly with no lookahead.

Q: Do I need to use all the features?

A: Absolutely not. The indicator is modular. Many profitable traders use just UT Bot + Bias Table + Moving Averages. Start simple, add complexity only if needed.

Q: How do I know which settings to use?

A: Every single input has a detailed tooltip. Hover over any setting to see:

What it does

How it affects trading

Typical values for scalping, day trading, swing trading

Start with defaults, adjust gradually based on results.

Q: Can I use this on crypto 24/7 markets?

A: Yes. ORB will not work (no defined session), but everything else functions normally. Use "Day" anchor for VWAP instead of "Session".

Q: The Bias Table is blank or not showing.

A: Check:

"Show Table" is ON

Table position isn't overlapping another indicator's table (change position)

At least one row is enabled

"Hide BIAS table on 1D or above" is OFF (if on Daily+ chart)

Q: Why are candlestick patterns not appearing?

A: Patterns are relatively rare by design - they only appear at genuine reversal points. Check:

Pattern toggles are ON

"Min candle body %" isn't too high (try 0.05-0.10)

You're looking at a chart with actual reversals (not strong trending market)

Q: UT Bot is too sensitive/not sensitive enough.

A: Adjust "Sensitivity (Key×ATR)". Lower number = tighter stop, more signals. Higher number = wider stop, fewer signals. Read the tooltip for guidance.

Q: Can I get alerts for the Bias Table?

A: The Bias Table is a dashboard for visual analysis, not a signal generator. Set alerts on UT Bot or Base signals, then manually check Bias Table for confirmation.

Q: Does this work on stocks with low volume?

A: Yes, but turn OFF the volume filter. Low volume stocks will never meet relative volume requirements.

Q: How often should I check the Bias Table?

A: Before every entry. It takes 2 seconds to glance at the AVG column and headline rows. This one check can save you from fighting the trend.

Q: What if UT signal and Base signal disagree?

A: UT Bot is more aggressive (ATR trailing). Base signals are more conservative (MA cross + filters). If they disagree, either:

Wait for both to align (safest)

Take the UT signal but with smaller size (aggressive)

Skip the trade (conservative)

There's no "right" answer - depends on your risk tolerance.

---

FINAL NOTES

The indicator gives you an edge. How you use that edge determines results.

For questions, feedback, or support, comment on the indicator page or message the author.

Happy Trading!

ค้นหาในสคริปต์สำหรับ "adx"

RSI Cloud v1.0 [PriceBlance] RSI Cloud v1.0 — Ichimoku-style Cloud on RSI(14), not on price.

Recalibrated baselines: EMA9 (Tenkan) for speed, WMA45 (Kijun) for stability.

Plus ADX-on-RSI to grade strength so you know when momentum persists or fades.

1. Introduction

RSI Cloud v1.0 applies an Ichimoku Cloud directly on RSI(14) to reveal momentum regimes earlier and cleaner than price-based views. We replaced Tenkan with EMA9 (faster, more responsive) and Kijun with WMA45 (slower, more stable) to fit a bounded oscillator (0–100). Forward spans (+26) and a lagging line (−26) provide a clear framework for trend bias and transitions.

To qualify signals, the indicator adds ADX computed on RSI—highlighting whether strength is weak, strong, or very strong, so you can decide when to follow, fade, or stand aside.

2. Core Mapping (Hook + Bullets)

At a glance: Ichimoku on RSI(14) with recalibrated baselines for a bounded oscillator.

Source: RSI(14)

Tenkan → EMA9(RSI) (fast, responsive)

Kijun → WMA45(RSI) (slow, stable)

Span A: classic Ichimoku midline, displaced +26

Span B: classic Ichimoku baseline, displaced +26

Lagging line: RSI shifted −26

3. Key Benefits (Why traders care)

Momentum regimes on RSI: position vs. Cloud = bull / bear / transition at a glance.

Cleaner confirmations: EMA9/WMA45 pairing cuts noise vs. raw 30/70 flips.

Earlier warnings: Cloud breaks on RSI often lead price-based confirmations.

4. ADX on RSI (Enhanced Strength Normalization)

Grade strength inside the RSI domain using ADX from ΔRSI:

ADX ≤ 20 → Weak (transparency = 60)

ADX ≤ 40 → Strong (transparency = 15)

ADX > 40 → Very strong (transparency = 0)

Use these tiers to decide when to trust, fade, or ignore a signal.

5. How to Read (Quick rules)

Bias / Regime

Bullish: RSI above Cloud and RSI > WMA45

Bearish: RSI below Cloud and RSI < WMA45

Neutral / Transition: all other cases

6. Settings (Copy & use)

RSI Length: 14 (default)

Tenkan: EMA9 on RSI · Kijun: WMA45 on RSI

Displacement: +26 (Span A/B) · −26 (Lagging)

Theme: PriceBlance Dark/Light

Visibility toggles: Cloud, Baselines, Lagging, labels/panel, Overbought/Oversold, Divergence, ADX-on-RSI (via transparency coloring)

7. Credits & License

Author/Brand: PriceBlance

Version: v1.0 (Free)

Watermark: PriceBlance • RSI Cloud v1.0

Disclaimer: Educational content; not financial advice.

8. CTA

If this helps, please ⭐ Star and Follow for updates & new tools.

Feedback is welcome—comment what you’d like added next (alerts, presets, visuals).

Pro Momentum Table + Trade Alerts📊 Indicator Name: Pro Momentum Table – ADX + DI + ATR + Astro Timing

🧠 Concept:

This indicator is designed for professional scalpers and intraday traders who want to capture only strong momentum waves — not noise. It combines trend strength, volatility, directional movement, momentum oscillation, vega divergence, and astrological timing into a single compact table on your chart.

⚙️ Components Explained:

Metric Description

ADX (Average Directional Index) Measures the strength of the trend. Values above 20 indicate that a meaningful move is starting.

+DI / -DI (Directional Indicators) Show whether buyers (+DI) or sellers (-DI) are dominating. Increasing +DI with ADX rising = bullish momentum. Increasing -DI with ADX rising = bearish momentum.

ATR (Average True Range) Shows volatility and expected range. Used for setting realistic stop-loss and multi-level targets (1×, 1.5×, 2×, 2.5× ATR).

Price Displays the current price level for quick reference.

CMO (Chande Momentum Oscillator) Measures short-term momentum direction and strength. Helps identify overbought/oversold conditions in trend continuation.

Vega Divergence Shows a synthetic reading of volatility pressure — "Bullish" when volatility expansion supports upward moves, "Bearish" for downward pressure, and "Neutral" otherwise.

Astro Remark Suggests ideal time windows based on planetary cycles for scalping entries. “Bullish Window” often aligns with high-probability long trades; “Bearish Window” favors shorts.

Trade Signal The core momentum condition: “Bullish Momentum” if ADX > 20 and +DI rising, “Bearish Momentum” if ADX > 20 and -DI rising, else “No Clear Momentum.”

📈 How to Use:

Wait for ADX > 20 – This confirms that the market is entering a strong momentum phase.

Check DI direction:

✅ +DI rising: Buyers gaining strength → look for long setups.

✅ -DI rising: Sellers gaining strength → look for short setups.

Use ATR to plan exits:

🎯 TP1 = Entry ± 1 × ATR

🎯 TP2 = Entry ± 1.5 × ATR

🎯 TP3 = Entry ± 2 × ATR

🎯 TP4 = Entry ± 2.5 × ATR

CMO & Vega Divergence: Confirm momentum direction and volatility expansion before committing.

Astro Remark: Align your scalping activity with the planetary support window for higher probability trades.

🪙 Pro Tips for Scalpers:

Only trade when ADX > 20 and DI is consistently rising. Ignore signals in choppy or sideways phases.

Avoid trades if Vega is neutral and CMO is flat – these usually indicate fake breakouts.

If targets aren’t hit within expected ATR-based time, treat the move as false and exit early.

Combine with 9 EMA and 20 EMA (hidden) for wave structure confirmation without cluttering the chart.

💡 Summary:

This indicator acts as a real-time trade decision dashboard. It removes clutter from the chart and delivers everything a professional scalper needs — strength, direction, volatility, momentum, timing, and actionable trade bias — all in one elegant table.

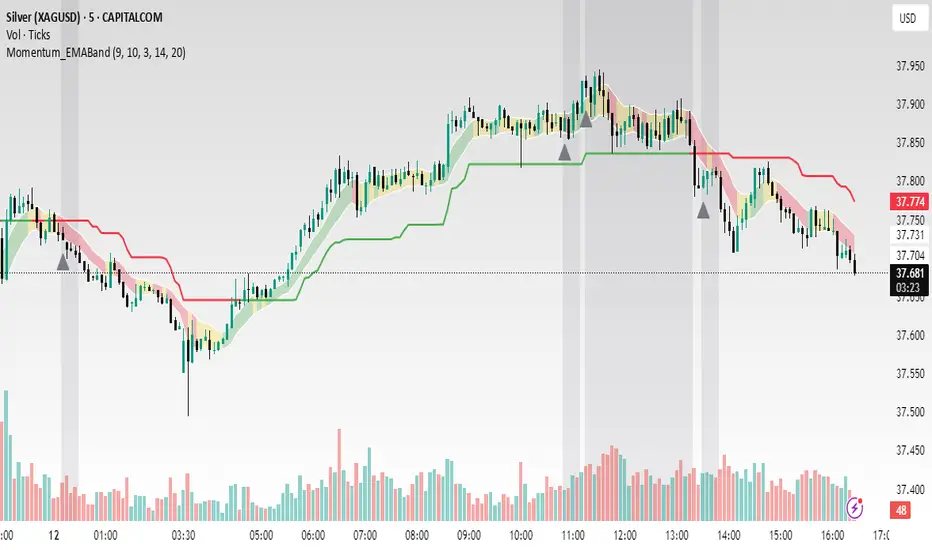

Momentum_EMABand📢 Reposting Notice

I am reposting this script because my earlier submission was hidden due to description requirements under TradingView’s House Rules. This updated version fully explains the originality, the reason for combining these indicators, and how they work together. Follow me for future updates and refinements.

🆕 Momentum EMA Band, Rule-Based System

Momentum EMA Band is not just a mashup — it is a purpose-built trading tool for intraday traders and scalpers that integrates three complementary technical concepts into a single rules-based breakout & retest framework.

Originality comes from the specific sequence and interaction of these three filters:

Supertrend → Sets directional bias.

EMA Band breakout with retest logic → Times precise entries.

ADX filter → Confirms momentum strength and avoids noise.

This system is designed to filter out weak setups and false breakouts that standalone indicators often fail to avoid.

🔧 How the Indicator Works — Combined Logic

1️⃣ EMA Price Band — Dynamic Zone Visualization

Plots upper & lower EMA bands (default: 9-period EMA).

Green Band → Price above upper EMA = bullish momentum

Red Band → Price below lower EMA = bearish pressure

Yellow Band → Price within band = neutral zone

Acts as a consolidation zone and breakout trigger level.

2️⃣ Supertrend Overlay — Reliable Trend Confirmation

ATR-based Supertrend adapts to volatility:

Green Line = Uptrend bias

Red Line = Downtrend bias

Ensures trades align with the prevailing trend.

3️⃣ ADX-Based No-Trade Zone — Choppy Market Filter

Manual ADX calculation (default: length 14).

If ADX < threshold (default: 20) and price is inside EMA Band → gray background marks low-momentum zones.

🧩 Why This Mashup Works

Supertrend confirms trend direction.

EMA Band breakout & retest validates the breakout’s strength.

ADX ensures the market has enough trend momentum.

When all align, entries are higher probability and whipsaws are reduced.

📈 Example Trade Walkthrough

Scenario: 5-minute chart, ADX threshold = 20.

Supertrend turns green → trend bias is bullish.

Price consolidates inside the yellow EMA Band.

ADX rises above 20 → trend momentum confirmed.

Price closes above the green EMA Band after retesting the band as support.

Entry triggered on candle close, stop below band, target based on risk-reward.

Exit when Supertrend flips red or ADX momentum drops.

This sequence prevents premature entries, keeps trades aligned with trend, and avoids ranging markets.

🎯 Key Features

✅ Multi-layered confirmation for precision trading

✅ Built-in no-trade zone filter

✅ Fully customizable parameters

✅ Clean visuals for quick decision-making

⚠ Disclaimer: This is Version 1. Educational purposes only. Always use with risk management.

UngliMulti-Indicator Confluence System

This is a **multi-indicator confluence trading signal system** called "Ungli" that combines RSI, ADX, and MACD to identify high-probability momentum opportunities when used alongside chart pattern and trend line breakouts.

## Core Concept

The script identifies moments when multiple technical indicators align to suggest potential price momentum moves, specifically looking for oversold and overbought conditions with momentum confirmation. Use green and red highlights along with chart patterns and trend line breakouts that signal a breakout for confluence for a likely momentum move.

## Technical Indicators Used

**RSI (Relative Strength Index)**

- Default 14-period RSI

- Oversold threshold: < 40

- Overbought threshold: > 60

**ADX (Average Directional Index)**

- Default 14-period ADX with DI+ and DI-

- Threshold: 21

- Looks for ADX below threshold but ticking upward (momentum building)

**MACD (Moving Average Convergence Divergence)**

- Fast: 12, Slow: 26, Signal: 9

- Uses MACD line direction as trend filter

## Signal Logic

**Green Background (Bullish Momentum Signal):**

- RSI > 60 (overbought)

- ADX < 21 AND rising

- MACD line trending upward

**Red Background (Bearish Momentum Signal):**

- RSI < 40 (oversold)

- ADX < 21 AND rising

- MACD line trending downward

## Key Strategy Elements

1. **Confluence Approach**: Requires all three indicators to align, reducing false signals

2. **Momentum Filter**: ADX must be building (rising) even if low, indicating emerging trend strength

3. **Trend Confirmation**: MACD direction must match the expected move

4. **Visual Simplicity**: Clean background highlighting without chart clutter

5. **Pattern Integration**: Designed to work with chart patterns and breakout strategies

## Use Case

This indicator is designed for swing trading and breakout strategies, identifying moments when oversold/overbought conditions coincide with building momentum in the expected direction. The ADX filter helps avoid choppy, trendless markets. Best used in conjunction with:

- Support/resistance breakouts

- Chart pattern breakouts (triangles, flags, channels)

- Trend line breaks

- Key level violations

The background highlights serve as confluence confirmation when combined with your chart analysis and breakout setups.

DMI-LuminateIndicator Description: DMI-Luminate (DMI-LMT)

DMI-Luminate is an enhanced version of the Directional Movement Index (DMI) indicator that combines multiple moving averages for smoothing and offers various options to customize the calculation of ADX, +DM, -DM, DX, and ADXR. It is ideal for traders looking to analyze trend strength and equilibrium points between buyers and sellers.

Components and Features

+DM and -DM: Indicators measuring positive and negative directional movement, helping identify trend direction.

DX (Directional Movement Index): Measures the relative difference between +DM and -DM, indicating the current trend strength.

ADX (Average Directional Index): A smoothed line showing trend strength regardless of direction. Values above 25 generally indicate a strong trend.

ADXR (Average Directional Movement Rating): A moving average of ADX that detects trend strength changes with less sensitivity.

Equilibrium Points: Visual markers (blue circles) that appear when +DM and -DM cross, signaling potential reversals or changes in trend strength.

Customizable Settings

DM Length: The period used to calculate directional movements.

ADX Smoothing: The smoothing period for ADX.

MA Type Universal: Select the moving average type used for smoothing calculations. Options include SMA, EMA, WMA, ALMA, T3, and advanced averages like DNA⚡ and RNA🐢.

T3 Hot Factor: Parameter to adjust the intensity of the T3 moving average (when selected).

Show Lines: Toggle the display of ADX, ADXR, DX, and +DM/-DM lines as you prefer.

Show Equilibrium Points: Enable to visualize crossing points between +DM and -DM.

Background Color and Offset: Customize the background color and offset for better visibility.

How to Use

Trend Identification

Watch the ADX line to gauge trend strength. When ADX is above 25, the trend is considered strong. The +DM and -DM lines indicate if the trend is bullish (+DM > -DM) or bearish (-DM > +DM).

Entry/Exit Signals

Use the equilibrium points (blue circles) to identify potential reversals or changes in trend dynamics based on +DM and -DM crossings.

Moving Average Selection

Experiment with different moving averages to smooth the data and tailor the indicator to your trading style and asset. Faster averages like EMA react better in volatile markets, while SMMA and ALMA suit more stable conditions.

Using ADXR

ADXR offers a smoother view of trend strength to avoid false signals during sideways markets.

Visual Customization

Adjust colors and background to improve readability, especially across different chart themes.

Recommendations

Combine DMI-Luminate with other indicators (e.g., volume, RSI, chart patterns) to confirm entries and exits.

Adjust DM Length and ADX Smoothing according to the timeframe you trade.

Use different moving average types to find the setup that works best for your asset and strategy.

RSI Strength & Consolidation Zones (Zeiierman)█ Overview

RSI Strength & Consolidation Zones (Zeiierman) is a hybrid momentum and volatility visualization tool that blends enhanced RSI interpretation with ADX-driven consolidation detection. This indicator doesn't just show where RSI is trending — it interprets how strong that trend is, when that strength changes, and where the market may be consolidating in anticipation of breakout movement.

Using a combination of Kalman-filtered RSI, custom-built DMI/ADX, and low-volatility zone recognition, it gives traders a dynamic RSI with strength-based coloring, while also highlighting consolidation zones to spot breakout opportunities.

█ Its uniqueness

Traditional RSI indicators lack context. They may show you when the market is overbought or oversold, but they won’t tell you how strong that condition is, or whether it’s likely to result in continuation or consolidation.

This tool aims to solve that by introducing adaptive strength metrics and structural compression zones, allowing traders to anticipate when the market is likely preparing for a move.

█ How It Works

⚪ Enhanced RSI

Combines traditional RSI and a custom RSI implementation

Smooths both through a Kalman filter for trend direction

Final RSI line reflects smoothed consensus between manual and built-in RSI

Adds an RSI + Strength overlay to show when the directional conviction is increasing

⚪ ADX-Driven Strength Layer

Directional Movement Index (DMI) is calculated both manually and with built-in smoothing

The average ADX value is used to calculate a strength modifier

When ADX exceeds 20, RSI is dynamically enhanced or dampened to reflect directional force

Resulting visual: RSI appears stronger or weaker based on confirmed trend conditions

⚪ Consolidation Zone Detection

When ADX falls below 20, the indicator enters a consolidation zone state

Boxes are drawn dynamically to contain the price within these low-volatility structures

Once the price breaks out of the zone, the indicator plots a breakout signal (▲ or ▼)

⚪ Breakouts

Breakout markers are placed at the first close outside the consolidation box

These signals serve as early indicators for potential trend continuation or reversal

█ How to Use

⚪ Confirm Momentum Strength

Use the RSI + Strength line to determine whether current momentum is backed by trend conviction. If strength expands alongside rising RSI, the move has confirmation.

⚪ Consolidations Zones

When RSI is around the midline, and a consolidation box appears, expect lower volatility and a range-bound market, followed by a breakout.

⚪ Use Breakout Signals for Entry

Look for ▲ or ▼ markers as early triggers. These often coincide with volume expansions or structural breaks.

█ Settings Explained

RSI Length – Number of bars used for RSI. Shorter = more sensitive.

DMI Length – Used in both custom and built-in ADX/DI calculations.

ADX Smoothing – Smooths the trend strength signal. Higher values = smoother strength detection.

Trend Confirmation (Filter Strength) – Adjusts the responsiveness of the Kalman filter.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Range Filter Buy and Sell 5min## **Enhanced Range Filter Strategy: A Comprehensive Overview**

### **1. Introduction**

The **Enhanced Range Filter Strategy** is a powerful technical trading system designed to identify high-probability trading opportunities while filtering out market noise. It utilizes **range-based trend filtering**, **momentum confirmation**, and **volatility-based risk management** to generate precise entry and exit signals. This strategy is particularly useful for traders who aim to capitalize on trend-following setups while avoiding choppy, ranging market conditions.

---

### **2. Key Components of the Strategy**

#### **A. Range Filter (Trend Determination)**

- The **Range Filter** smooths price fluctuations and helps identify clear trends.

- It calculates an **adjusted price range** based on a **sampling period** and a **multiplier**, ensuring a dynamic trend-following approach.

- **Uptrends:** When the current price is above the range filter and the trend is strengthening.

- **Downtrends:** When the price falls below the range filter and momentum confirms the move.

#### **B. RSI (Relative Strength Index) as Momentum Confirmation**

- RSI is used to **filter out weak trades** and prevent entries during overbought/oversold conditions.

- **Buy Signals:** RSI is above a certain threshold (e.g., 50) in an uptrend.

- **Sell Signals:** RSI is below a certain threshold (e.g., 50) in a downtrend.

#### **C. ADX (Average Directional Index) for Trend Strength Confirmation**

- ADX ensures that trades are only taken when the trend has **sufficient strength**.

- Avoids trading in low-volatility, ranging markets.

- **Threshold (e.g., 25):** Only trade when ADX is above this value, indicating a strong trend.

#### **D. ATR (Average True Range) for Risk Management**

- **Stop Loss (SL):** Placed **one ATR below** (for long trades) or **one ATR above** (for short trades).

- **Take Profit (TP):** Set at a **3:1 reward-to-risk ratio**, using ATR to determine realistic price targets.

- Ensures volatility-adjusted risk management.

---

### **3. Entry and Exit Conditions**

#### **📈 Buy (Long) Entry Conditions:**

1. **Price is above the Range Filter** → Indicates an uptrend.

2. **Upward trend strength is positive** (confirmed via trend counter).

3. **RSI is above the buy threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **📉 Sell (Short) Entry Conditions:**

1. **Price is below the Range Filter** → Indicates a downtrend.

2. **Downward trend strength is positive** (confirmed via trend counter).

3. **RSI is below the sell threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **🚪 Exit Conditions:**

- **Stop Loss (SL):**

- **Long Trades:** 1 ATR below entry price.

- **Short Trades:** 1 ATR above entry price.

- **Take Profit (TP):**

- Set at **3x the risk distance** to achieve a favorable risk-reward ratio.

- **Ranging Market Exit:**

- If ADX falls below the threshold, indicating a weakening trend.

---

### **4. Visualization & Alerts**

- **Colored range filter line** changes based on trend direction.

- **Buy and Sell signals** appear as labels on the chart.

- **Stop Loss and Take Profit levels** are plotted as dashed lines.

- **Gray background highlights ranging markets** where trading is avoided.

- **Alerts trigger on Buy, Sell, and Ranging Market conditions** for automation.

---

### **5. Advantages of the Enhanced Range Filter Strategy**

✅ **Trend-Following with Noise Reduction** → Helps avoid false signals by filtering out weak trends.

✅ **Momentum Confirmation with RSI & ADX** → Ensures that only strong, valid trades are executed.

✅ **Volatility-Based Risk Management** → ATR ensures adaptive stop loss and take profit placements.

✅ **Works on Multiple Timeframes** → Effective for day trading, swing trading, and scalping.

✅ **Visually Intuitive** → Clearly displays trade signals, SL/TP levels, and trend conditions.

---

### **6. Who Should Use This Strategy?**

✔ **Trend Traders** who want to enter trades with momentum confirmation.

✔ **Swing Traders** looking for medium-term opportunities with a solid risk-reward ratio.

✔ **Scalpers** who need precise entries and exits to minimize false signals.

✔ **Algorithmic Traders** using alerts for automated execution.

---

### **7. Conclusion**

The **Enhanced Range Filter Strategy** is a powerful trading tool that combines **trend-following techniques, momentum indicators, and risk management** into a structured, rule-based system. By leveraging **Range Filters, RSI, ADX, and ATR**, traders can improve trade accuracy, manage risk effectively, and filter out unfavorable market conditions.

This strategy is **ideal for traders looking for a systematic, disciplined approach** to capturing trends while **avoiding market noise and false breakouts**. 🚀

Enhanced Range Filter Strategy with ATR TP/SLBuilt by Omotola

## **Enhanced Range Filter Strategy: A Comprehensive Overview**

### **1. Introduction**

The **Enhanced Range Filter Strategy** is a powerful technical trading system designed to identify high-probability trading opportunities while filtering out market noise. It utilizes **range-based trend filtering**, **momentum confirmation**, and **volatility-based risk management** to generate precise entry and exit signals. This strategy is particularly useful for traders who aim to capitalize on trend-following setups while avoiding choppy, ranging market conditions.

---

### **2. Key Components of the Strategy**

#### **A. Range Filter (Trend Determination)**

- The **Range Filter** smooths price fluctuations and helps identify clear trends.

- It calculates an **adjusted price range** based on a **sampling period** and a **multiplier**, ensuring a dynamic trend-following approach.

- **Uptrends:** When the current price is above the range filter and the trend is strengthening.

- **Downtrends:** When the price falls below the range filter and momentum confirms the move.

#### **B. RSI (Relative Strength Index) as Momentum Confirmation**

- RSI is used to **filter out weak trades** and prevent entries during overbought/oversold conditions.

- **Buy Signals:** RSI is above a certain threshold (e.g., 50) in an uptrend.

- **Sell Signals:** RSI is below a certain threshold (e.g., 50) in a downtrend.

#### **C. ADX (Average Directional Index) for Trend Strength Confirmation**

- ADX ensures that trades are only taken when the trend has **sufficient strength**.

- Avoids trading in low-volatility, ranging markets.

- **Threshold (e.g., 25):** Only trade when ADX is above this value, indicating a strong trend.

#### **D. ATR (Average True Range) for Risk Management**

- **Stop Loss (SL):** Placed **one ATR below** (for long trades) or **one ATR above** (for short trades).

- **Take Profit (TP):** Set at a **3:1 reward-to-risk ratio**, using ATR to determine realistic price targets.

- Ensures volatility-adjusted risk management.

---

### **3. Entry and Exit Conditions**

#### **📈 Buy (Long) Entry Conditions:**

1. **Price is above the Range Filter** → Indicates an uptrend.

2. **Upward trend strength is positive** (confirmed via trend counter).

3. **RSI is above the buy threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **📉 Sell (Short) Entry Conditions:**

1. **Price is below the Range Filter** → Indicates a downtrend.

2. **Downward trend strength is positive** (confirmed via trend counter).

3. **RSI is below the sell threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **🚪 Exit Conditions:**

- **Stop Loss (SL):**

- **Long Trades:** 1 ATR below entry price.

- **Short Trades:** 1 ATR above entry price.

- **Take Profit (TP):**

- Set at **3x the risk distance** to achieve a favorable risk-reward ratio.

- **Ranging Market Exit:**

- If ADX falls below the threshold, indicating a weakening trend.

---

### **4. Visualization & Alerts**

- **Colored range filter line** changes based on trend direction.

- **Buy and Sell signals** appear as labels on the chart.

- **Stop Loss and Take Profit levels** are plotted as dashed lines.

- **Gray background highlights ranging markets** where trading is avoided.

- **Alerts trigger on Buy, Sell, and Ranging Market conditions** for automation.

---

### **5. Advantages of the Enhanced Range Filter Strategy**

✅ **Trend-Following with Noise Reduction** → Helps avoid false signals by filtering out weak trends.

✅ **Momentum Confirmation with RSI & ADX** → Ensures that only strong, valid trades are executed.

✅ **Volatility-Based Risk Management** → ATR ensures adaptive stop loss and take profit placements.

✅ **Works on Multiple Timeframes** → Effective for day trading, swing trading, and scalping.

✅ **Visually Intuitive** → Clearly displays trade signals, SL/TP levels, and trend conditions.

---

### **6. Who Should Use This Strategy?**

✔ **Trend Traders** who want to enter trades with momentum confirmation.

✔ **Swing Traders** looking for medium-term opportunities with a solid risk-reward ratio.

✔ **Scalpers** who need precise entries and exits to minimize false signals.

✔ **Algorithmic Traders** using alerts for automated execution.

---

### **7. Conclusion**

The **Enhanced Range Filter Strategy** is a powerful trading tool that combines **trend-following techniques, momentum indicators, and risk management** into a structured, rule-based system. By leveraging **Range Filters, RSI, ADX, and ATR**, traders can improve trade accuracy, manage risk effectively, and filter out unfavorable market conditions.

This strategy is **ideal for traders looking for a systematic, disciplined approach** to capturing trends while **avoiding market noise and false breakouts**. 🚀

MLB Momentum IndicatorMLB Momentum Indicator is a no‐lookahead technical indicator designed to signal intraday trend shifts and potential reversal points. It combines several well‐known technical components—Moving Averages, MACD, RSI, and optional ADX & Volume filters—to deliver high‐probability buy/sell signals on your chart.

Below is an overview of how it works and what each part does:

1. Moving Average Trend Filter

The script uses two moving averages (fast and slow) to determine the primary trend:

isUpTrend if Fast MA > Slow MA

isDownTrend if Fast MA < Slow MA

You can select the MA method—SMA, EMA, or WMA—and customize lengths.

Why it matters: The indicator only gives bullish signals if the trend is up, and bearish signals if the trend is down, helping avoid trades that go against the bigger flow.

2. MACD Confirmation (Momentum)

Uses MACD (with user‐defined Fast, Slow, and Signal lengths) to check momentum:

macdBuySignal if the MACD line crosses above its signal line (bullish)

macdSellSignal if the MACD line crosses below its signal line (bearish)

Why it matters: MACD crossovers confirm an emerging momentum shift, aligning signals with actual price acceleration rather than random fluctuation.

3. RSI Overbought/Oversold Filter

RSI (Relative Strength Index) is calculated with a chosen length, plus Overbought & Oversold thresholds:

For long signals: the RSI must be below the Overbought threshold (e.g. 70).

For short signals: the RSI must be above the Oversold threshold (e.g. 30).

Why it matters: Prevents buying when price is already overbought or shorting when price is too oversold, filtering out possible poor‐risk trades.

4. Optional ADX Filter (Trend Strength)

If enabled, ADX must exceed a chosen threshold (e.g., 20) for a signal to be valid:

This ensures you’re only taking trades in markets that have sufficient directional momentum.

Why it matters: It weeds out choppy, sideways conditions where signals are unreliable.

5. Optional Volume Filter (High‐Participation Moves)

If enabled, the indicator checks whether current volume is above a certain multiple of its moving average (e.g., 1.5× average volume).

Why it matters: High volume often indicates stronger institutional interest, validating potential breakouts or reversals.

6. ATR & Chandelier (Visual Reference)

For reference only, the script can display ATR‐based stop levels or a Chandelier Exit line:

ATR (Average True Range) helps gauge volatility and can inform stop‐loss distances.

Chandelier Exit is a trailing stop technique that adjusts automatically as price moves.

Why it matters: Though this version of the script doesn’t execute trades, these lines help you see how far to place stops or how to ride a trend.

7. Final Bullish / Bearish Signal

When all conditions (trend, MACD, RSI, optional ADX, optional Volume) line up for a long, a green “Long” arrow appears.

When all conditions line up for a short, a red “Short” arrow appears.

Why it matters: You get a clear, on‐chart signal for each potential entry, rather than needing to check multiple indicators manually.

8. Session & Date Filtering

The script allows choosing a start/end date and an optional session window (e.g. 09:30–16:00).

Why it matters: Helps limit signals to a specific historical backtest range or trading hours, which can be crucial for day traders (e.g., stock market hours only).

Putting It All Together

Primary Trend → ensures you trade in line with the bigger direction.

MACD & RSI → confirm momentum and avoid overbought/oversold extremes.

ADX & Volume → optional filters for strong trend strength & genuine interest.

Arrows → each potential buy (Long) or sell (Short) signal is clearly shown on your chart.

Use Cases

5‐Minute Scalping: Shorter RSI/MACD lengths to catch small, frequent intraday moves.

Swing Trading: Larger MAs, bigger RSI thresholds, and using ADX to filter only major trends.

Cautious Approach: Enable volume & ADX filters to reduce false signals in choppy markets.

Benefits & Limitations

Benefits:

Consolidates multiple indicators into one overlay.

Clear buy/sell signals with optional dynamic volatility references.

Flexible user inputs adapt to different trading styles/timeframes.

Limitations:

Like all technical indicators, it can produce false signals in sideways or news‐driven markets.

Success depends heavily on user settings and the particular market’s behavior.

Summary

The MLB Momentum Indicator combines a trend filter (MAs), momentum check (MACD), overbought/oversold gating (RSI), and optional ADX/Volume filters to create clear buy/sell arrows on your chart. This approach encourages trading in sync with both trend and momentum, and helps avoid suboptimal entries when volume or trend strength is lacking. It can be tailored to scalp micro‐moves on lower timeframes or used for higher‐timeframe swing trading by adjusting the input settings.

Rosiz Support 2### **Indicator Name**: Custom RSI, Stochastic, and ADX

### **Description**:

This is a multi-functional indicator that combines three popular technical analysis tools—**RSI (Relative Strength Index)**, **Stochastic Oscillator**, and **ADX (Average Directional Index)**—into a single, customizable pane. This indicator helps traders analyze momentum, overbought/oversold conditions, and trend strength simultaneously, making it a powerful tool for making informed trading decisions.

---

### **Features**:

1. **RSI (Relative Strength Index)**:

- Measures the speed and change of price movements.

- Helps identify overbought (>70) and oversold (<30) conditions.

- Includes customizable length and source options.

- Background shading visually highlights overbought and oversold zones.

2. **Stochastic Oscillator**:

- Determines momentum by comparing a security's closing price to its price range over a specific period.

- Includes %K and %D lines for crossovers, which signal potential entry or exit points.

- Highlights overbought (>80) and oversold (<20) zones with background fill.

3. **ADX (Average Directional Index)**:

- Measures trend strength (higher values indicate stronger trends).

- Includes customizable smoothing and DI (Directional Indicator) length.

---

### **How to Use**:

- **RSI**: Look for overbought or oversold conditions for potential reversal points. Divergences between price and RSI may signal weakening trends.

- **Stochastic Oscillator**: Watch for %K and %D crossovers near overbought or oversold zones to confirm buy or sell signals.

- **ADX**: Use ADX values to assess trend strength:

- **ADX > 25**: Strong trend.

- **ADX < 20**: Weak or ranging market.

---

### **Customization Options**:

- **RSI Settings**: Adjust length, source, and visual parameters.

- **Stochastic Settings**: Modify %K and %D lengths and smoothing factors.

- **ADX Settings**: Fine-tune smoothing and directional index lengths.

---

### **Advantages**:

- Combines three indicators into one, reducing chart clutter.

- Customizable inputs for flexibility in various trading strategies.

- Visual enhancements (background fills and lines) for better readability.

This indicator is perfect for traders looking to combine momentum analysis, overbought/oversold signals, and trend strength in a single tool!

Detecting Sideways Market or Strong Trends| Copy Trade Tungdubai**Tool Description**:

The **"Detecting Sideways Market or Strong Trends | Copy Trade Tungdubai"** tool is designed to help traders identify two key market conditions:

1. **Sideways Market**:

- This condition is detected when the ADX is below 20, the price stays within the Bollinger Bands, and the RSI is between 45 and 55.

- When the market is sideways, the chart background will turn yellow as a visual alert.

2. **Strong Trend Market**:

- This condition is identified when the ADX is above 25, and either the price breaks out of the Bollinger Bands or the RSI surpasses the overbought (70) or oversold (30) levels.

- When the market is in a strong trend, the chart background will turn blue as a visual alert.

**Key Components of the Tool**:

- **ADX**: Measures the strength of the market trend, with key thresholds at 20 and 25.

- **Bollinger Bands**: Helps determine volatility and checks if the price is within or outside the bands.

- **RSI**: Measures momentum, helping identify overbought and oversold levels.

**Visual Features on the Chart**:

- ADX, RSI, and Bollinger Bands are clearly plotted with their respective key thresholds for easier recognition of market conditions.

- The chart background changes color to reflect the current market condition (yellow for sideways, blue for strong trends).

**Alerts**:

- Alerts are triggered when the market enters either a sideways or strong trend phase, providing notifications to help users act promptly.

This tool serves as a practical aid in recognizing market conditions, allowing traders to make informed decisions aligned with their strategies.

**Mô tả công cụ**:

Công cụ **"Detecting Sideways Market or Strong Trends | Copy Trade Tungdubai"** được thiết kế để giúp các nhà giao dịch xác định hai trạng thái chính của thị trường:

1. **Thị trường đi ngang (Sideways)**:

- Điều kiện được xác định dựa trên chỉ số ADX thấp hơn ngưỡng 20, giá nằm trong dải Bollinger Bands, và chỉ số RSI dao động trong khoảng từ 45 đến 55.

- Khi thị trường đi ngang, nền của biểu đồ sẽ chuyển sang màu vàng để cảnh báo trực quan.

2. **Thị trường bùng nổ sóng mạnh (Strong Trend)**:

- Điều kiện được xác định khi ADX vượt qua ngưỡng 25 và giá phá vỡ dải Bollinger Bands (hoặc) chỉ số RSI vượt ngưỡng quá mua 70 hoặc quá bán 30.

- Khi thị trường bùng nổ sóng mạnh, nền biểu đồ sẽ chuyển sang màu xanh để cảnh báo trực quan.

**Các thành phần chính của công cụ**:

- **ADX**: Được sử dụng để đo sức mạnh xu hướng thị trường, với các ngưỡng quan trọng là 20 và 25.

- **Bollinger Bands**: Được sử dụng để xác định mức độ biến động và kiểm tra giá nằm trong hay ngoài dải.

- **RSI**: Dùng để đo mức độ quá mua/quá bán, xác định động lượng giá.

**Hiển thị trên biểu đồ**:

- Các đường ADX, RSI, và Bollinger Bands được vẽ rõ ràng, cùng với các ngưỡng quan trọng (hỗ trợ nhận biết trạng thái thị trường).

- Nền biểu đồ thay đổi màu sắc tương ứng với điều kiện thị trường.

**Cảnh báo**:

- Cảnh báo sẽ được kích hoạt khi thị trường rơi vào trạng thái đi ngang hoặc bùng nổ sóng mạnh, với các thông báo giúp người dùng hành động kịp thời.

Công cụ này là một trợ thủ hữu ích trong việc nhận biết trạng thái thị trường, từ đó giúp các nhà giao dịch đưa ra quyết định phù hợp với chiến lược của mình.

Artaking 2Components of the Indicator:

Moving Averages:

Short-Term Moving Average (MA): This is a 50-period Simple Moving Average (SMA) applied to the closing price. It is used to track the short-term trend of the market.

Long-Term Moving Average (MA): This is a 200-period SMA used to track the long-term trend.

Day Trading Moving Average: A 20-period SMA is used specifically for day trading signals, focusing on shorter-term price movements.

Purpose:

The crossing of these moving averages (short-term crossing above or below long-term) provides basic buy and sell signals, indicative of potential trend reversals or continuations.

ADX (Average Directional Index) for Trend Strength:

ADX Calculation: The ADX is calculated using a 14-period length with 14-period smoothing. The ADX value indicates the strength of a trend, regardless of direction.

Strong Trend Condition: The indicator considers a trend to be strong if the ADX value is above 25. This threshold helps filter out trades during weak or sideways markets.

Purpose:

To ensure that the strategy only generates signals when there is a strong trend, thus avoiding whipsaws in low volatility or range-bound conditions.

Support Levels:

Support Level Calculation: The indicator calculates the lowest close over the last 100 periods. This level is used to identify significant support zones where the price might find a floor.

Purpose:

Support levels are critical in identifying potential areas where the price might bounce, making them ideal for setting stop losses or identifying buy opportunities.

Volatility Spike (Proxy for News Trading):

ATR (Average True Range) Calculation: The indicator uses a 14-period ATR to measure market volatility. A volatility spike is identified when the ATR is greater than 1.5 times the 14-period SMA of the ATR.

Purpose:

This serves as a proxy for news events or other sudden market movements that could make the market unpredictable. The indicator avoids generating signals during these periods to reduce the risk of being caught in a volatile, potentially news-driven move.

Fibonacci Retracement Levels:

61.8% Fibonacci Level: Calculated from the highest high and lowest low over the long MA period, this retracement level is widely regarded as a significant support or resistance level.

Purpose:

Position traders often use Fibonacci levels to identify potential reversal points. The indicator incorporates the 61.8% level to fine-tune entries and exits.

Candlestick Patterns for Price Action Trading:

Bullish Engulfing Pattern: A bullish reversal pattern where a green candle fully engulfs the previous red candle.

Bearish Engulfing Pattern: A bearish reversal pattern where a red candle fully engulfs the previous green candle.

Purpose:

These patterns are classic signals used in price action trading to identify potential reversals at key levels, especially when they align with other conditions like support/resistance or Fibonacci levels.

Signal Generation:

The indicator generates buy and sell signals by combining the above elements:

Buy Signal:

A buy signal is triggered when:

The short-term MA crosses above the long-term MA (indicating a potential uptrend).

The trend is strong (ADX > 25).

The current price is near or below the 61.8% Fibonacci retracement level, suggesting a potential reversal.

No significant volatility spike is detected, ensuring the market isn’t reacting unpredictably to news.

Sell Signal:

A sell signal is triggered when:

The short-term MA crosses below the long-term MA (indicating a potential downtrend).

The trend is strong (ADX > 25).

The current price is near or above the 61.8% Fibonacci retracement level, suggesting potential resistance.

No significant volatility spike is detected.

Day Trading Signals:

Independent of the main trend signals, the indicator also generates intraday buy and sell signals when the price crosses above or below the 20-period day trading MA.

Price Action Signals:

The indicator can trigger buy or sell signals based purely on price action, such as the occurrence of bullish or bearish engulfing patterns. This is optional and can be enabled or disabled.

Alerts:

The indicator includes built-in alert conditions that notify the trader when a buy or sell signal is generated. This allows traders to act immediately without having to constantly monitor the charts.

Practical Application:

This indicator is versatile and can be used across various trading styles:

Position Trading: The long-term MA, Fibonacci retracement, and ADX provide a solid foundation for identifying long-term trends and potential entry/exit points.

Day Trading: The short-term MA and day trading MA offer quick signals for intraday trading.

Price Action: Candlestick pattern recognition allows for precise entry points based on market sentiment and behavior.

News Trading: The volatility spike filter helps avoid trading during periods of market instability, often driven by news events.

Conclusion:

The Comprehensive Trading Strategy Indicator is a robust tool designed to help traders navigate various market conditions by integrating multiple strategies into a single, coherent framework. It provides clear, actionable signals while filtering out potentially dangerous trades during volatile or weak market conditions. Whether you're a long-term trader, a day trader, or someone who relies on price action, this indicator can be a valuable addition to your trading toolkit.

RSI/MFI Selling Sentiment IndexPsychological Sales Index (Psychological Sales Index)

Fundamental Indicators of Market Sentiment: The Importance of MFI and RSI

The two fundamental indicators that best reflect market sentiment are Money Flow Index (MFI) and Relative Strength Index (RSI). MFI is an indicator of the flow of funds in a market by combining price and volume, which is used to determine whether a stock is over-bought or over-selling. RSI is an indicator of the overheating of the market by measuring the rise and fall of prices, which is applied to the analysis of the relative strength of stock prices. These two indicators allow a quantitative assessment of the market's buying and selling pressure, which provides important information to understand the psychological state of market participants.

Using timing and fundamental metrics

In order to grasp the effective timing of the sale, in-depth consideration was needed on how to use basic indicators. MFI and RSI represent the buying and selling pressures of the market, respectively, but there is a limit to reflecting the overall trend of the market alone. As a result, a study on how to capture more accurate selling points was conducted by comprehensively considering technical analysis along with psychological factors of the market.

The importance of ADX integration and weighting

The "Average Regional Index (ADX)" was missing in the early version. ADX is an indicator of the strength of a trend, and has experienced a problem of less accuracy in selling sentiment indicators, especially in the upward trend. To address this, we incorporated ADX and adopted a method of adjusting the weights of MFI and RSI according to the values of ADX. A high ADX value implies the existence of a strong trend, in which case it is appropriate to reduce the influence of MFI and RSI to give more importance to the strength of the trend. Conversely, a low ADX value increases the influence of MFI and RSI, putting more weight on the psychological elements of the market.

How to use and interpret

The user can adjust several parameters. Key inputs include 'Length', 'Overbought Threshold', 'DI Length', and 'ADX Smoothing'. These parameters are used to set the calculation period, overselling threshold, DI length, and ADX smoothing period of the indicator, respectively. The script calculates the psychological selling index based on MFI, RSI, and ADX. The calculated index is normalized to values between 0 and 100 and is displayed in the graph. Values above 'Overbought Threshold' indicate an overselling state, which can be interpreted as a potential selling signal. This index allows investors to comprehensively evaluate the psychological state of the market and the strength of trends, which can be used to make more accurate selling decisions.

Multi-Timeframe (MTF) Dashboard by RiTzMulti-Timeframe Dashboard

Shows values of different Indiactors on Multiple-Timeframes for the selected script/symbol

VWAP : if LTP is trading above VWAP then Bullish else if LTP is trading below VWAP then Bearish.

ST(21,1) : if LTP is trading above Supertrend (21,1) then Bullish , else if LTP is trading below Supertrend (21,1) then Bearish.

ST(14,2) : if LTP is trading above Supertrend (14,2) then Bullish , else if LTP is trading below Supertrend (14,2) then Bearish.

ST(10,3) : if LTP is trading above Supertrend (10,3) then Bullish , else if LTP is trading below Supertrend (10,3) then Bearish.

RSI(14) : Shows value of RSI (14) for the current timeframe.

ADX : if ADX is > 75 and DI+ > DI- then "Bullish ++".

if ADX is < 75 but >50 and DI+ > DI- then "Bullish +".

if ADX is < 50 but > 25 and DI+ > DI- then "Bullish".

if ADX is above 75 and DI- > DI+ then "Bearish ++".

if ADX is < 75 but > 50 and DI- > DI+ then "Bearish+".

if ADX is < 50 but > 25 and DI- > DI+ then "Bearish".

if ADX is < 25 then "Neutral".

MACD : if MACD line is above Signal Line then "Bullish", else if MACD line is below Signal Line then "Bearish".