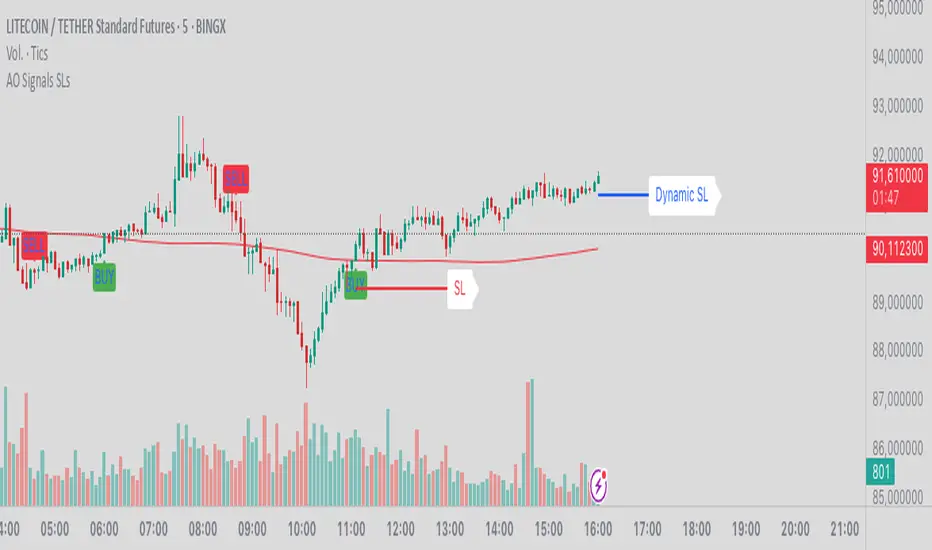

AO Smart Scalper – 5M Dynamic SL Edition📈 AO Signals with Fixed and Dynamic SL – Optimized for 5-Minute Charts 📉

This indicator is built for 5-minute timeframe trading, combining powerful momentum signals from the Awesome Oscillator (AO) with both Fixed and Dynamic Stop Loss (SL) levels to enhance trade management and risk control.

✅ Buy/Sell Signals:

The indicator generates clear BUY and SELL signals based on the AO crossing above or below the zero line, helping traders capture momentum shifts early.

🛑 Fixed Stop Loss:

Each trade signal comes with a Fixed SL, calculated based on the high (for shorts) or low (for longs) of the previous candle, with a customizable percentage offset. This SL is plotted with a red line, providing a clear initial risk level.

⚡ Dynamic Stop Loss: Continuous Presence, Strategic Use:

A secondary Dynamic SL line is plotted, which is continuously present on the chart. This dynamic level responds to market conditions and can serve as a trailing stop or key decision point.

💡 Recommended Use: It is recommended to actively start using the Dynamic SL once the trade has moved into profit. This allows protecting obtained profits and minimizing the risk of losses in case of a market reversal.

🛡️ Enhanced Dynamic Stop-Loss Strategy:

🔒 Initial Protection: Utilize the Fixed SL as the initial stop-loss, placed below relevant lows (for longs) or above relevant highs (for shorts), or as provided by the fixed SL indicator.

🛤️ Dynamic Tracking:

🟢 Long Trades: Once in profit, the Dynamic SL will dynamically adjust, moving upwards as higher lows are formed, effectively trailing the price and securing profits.

🔴 Short Trades: Conversely, in short trades, once in profit, the Dynamic SL will move downwards as lower highs are formed, protecting gains.

🔄 Alternatively the dynamic stop loss will follow the dynamic SL line provided by the indicator.

🚪 Exiting Trades: When the price crosses below the Dynamic SL line in a LONG trade, or above it in a SHORT trade, the recommended action is to exit the trade.

↩️ Re-entry Consideration: You may consider re-entering only if the price clearly returns above the Dynamic SL (for longs) or below it (for shorts).

⚠️ IMPORTANT - 5-Minute Strategy Guidance ⏱️

This tool is specifically optimized for the 5-minute timeframe. This approach helps filter out weak setups and maintain discipline in volatile market conditions.

✨ Additional Features:

👁️ Visual and editable SL levels

📊 200-period SMA for trend context

💻 Simple and effective interface for intraday trading setups

🎯 Ideal for traders seeking a clean, rule-based system that combines momentum entry signals with layered stop loss protection.

🔑 Key Changes:

It was emphasized that the Dynamic SL is always present, but its active use is recommended once the trade is in profit.

It was clarified the use of the Fixed SL, giving the option to use the one provided by the indicator, or to place it according to the price action.

ค้นหาในสคริปต์สำหรับ "Trailing stop"

[3Commas] Turtle StrategyTurtle Strategy

🔷 What it does: This indicator implements a modernized version of the Turtle Trading Strategy, designed for trend-following and automated trading with webhook integration. It identifies breakout opportunities using Donchian channels, providing entry and exit signals.

Channel 1: Detects short-term breakouts using the highest highs and lowest lows over a set period (default 20).

Channel 2: Acts as a confirmation filter by applying an offset to the same period, reducing false signals.

Exit Channel: Functions as a dynamic stop-loss (wait for candle close), adjusting based on market structure (default 10 periods).

Additionally, traders can enable a fixed Take Profit level, ensuring a systematic approach to profit-taking.

🔷 Who is it for:

Trend Traders: Those looking to capture long-term market moves.

Bot Users: Traders seeking to automate entries and exits with bot integration.

Rule-Based Traders: Operators who prefer a structured, systematic trading approach.

🔷 How does it work: The strategy generates buy and sell signals using a dual-channel confirmation system.

Long Entry: A buy signal is generated when the close price crosses above the previous high of Channel 1 and is confirmed by Channel 2.

Short Entry: A sell signal occurs when the close price falls below the previous low of Channel 1, with confirmation from Channel 2.

Exit Management: The Exit Channel acts as a trailing stop, dynamically adjusting to price movements. To exit the trade, wait for a full bar close.

Optional Take Profit (%): Closes trades at a predefined %.

🔷 Why it’s unique:

Modern Adaptation: Updates the classic Turtle Trading Strategy, with the possibility of using a second channel with an offset to filter the signals.

Dynamic Risk Management: Utilizes a trailing Exit Channel to help protect gains as trades move favorably.

Bot Integration: Automates trade execution through direct JSON signal communication with your DCA Bots.

🔷 Considerations Before Using the Indicator:

Market & Timeframe: Best suited for trending markets; higher timeframes (e.g., H4, D1) are recommended to minimize noise.

Sideways Markets: In choppy conditions, breakouts may lead to false signals—consider using additional filters.

Backtesting & Demo Testing: It is crucial to thoroughly backtest the strategy and run it on a demo account before risking real capital.

Parameter Adjustments: Ensure that commissions, slippage, and position sizes are set accurately to reflect real trading conditions.

🔷 STRATEGY PROPERTIES

Symbol: BINANCE:ETHUSDT (Spot).

Timeframe: 4h.

Test Period: All historical data available.

Initial Capital: 10000 USDT.

Order Size per Trade: 1% of Capital, you can use a higher value e.g. 5%, be cautious that the Max Drawdown does not exceed 10%, as it would indicate a very risky trading approach.

Commission: Binance commission 0.1%, adjust according to the exchange being used, lower numbers will generate unrealistic results. By using low values e.g. 5%, it allows us to adapt over time and check the functioning of the strategy.

Slippage: 5 ticks, for pairs with low liquidity or very large orders, this number should be increased as the order may not be filled at the desired level.

Margin for Long and Short Positions: 100%.

Indicator Settings: Default Configuration.

Period Channel 1: 20.

Period Channel 2: 20.

Period Channel 2 Offset: 20.

Period Exit: 10.

Take Profit %: Disable.

Strategy: Long & Short.

🔷 STRATEGY RESULTS

⚠️Remember, past results do not guarantee future performance.

Net Profit: +516.87 USDT (+5.17%).

Max Drawdown: -100.28 USDT (-0.95%).

Total Closed Trades: 281.

Percent Profitable: 40.21%.

Profit Factor: 1.704.

Average Trade: +1.84 USDT (+1.80%).

Average # Bars in Trades: 29.

🔷 How to Use It:

🔸 Adjust Settings:

Select your asset and timeframe suited for trend trading.

Adjust the periods for Channel 1, Channel 2, and the Exit Channel to align with the asset’s historical behavior. You can visualize these channels by going to the Style tab and enabling them.

For example, if you set Channel 2 to 40 with an offset of 40, signals will take longer to appear but will aim for a more defined trend.

Experiment with different values, a possible exit configuration is using 20 as well. Compare the results and adjust accordingly.

Enable the Take Profit (%) option if needed.

🔸Results Review:

It is important to check the Max Drawdown. This value should ideally not exceed 10% of your capital. Consider adjusting the trade size to ensure this threshold is not surpassed.

Remember to include the correct values for commission and slippage according to the symbol and exchange where you are conducting the tests. Otherwise, the results will not be realistic.

If you are satisfied with the results, you may consider automating your trades. However, it is strongly recommended to use a small amount of capital or a demo account to test proper execution before committing real funds.

🔸Create alerts to trigger the DCA Bot:

Verify Messages: Ensure the message matches the one specified by the DCA Bot.

Multi-Pair Configuration: For multi-pair setups, enable the option to add the symbol in the correct format.

Signal Settings: Enable the option to receive long or short signals (Entry | TP | SL), copy and paste the messages for the DCA Bots configured.

Alert Setup:

When creating an alert, set the condition to the indicator and choose "alert() function call only".

Enter any desired Alert Name.

Open the Notifications tab, enable Webhook URL, and paste the Webhook URL.

For more details, refer to the section: "How to use TradingView Custom Signals".

Finalize Alerts: Click Create, you're done! Alerts will now be sent automatically in the correct format.

🔷 INDICATOR SETTINGS

Period Channel 1: Period of highs and lows to trigger signals

Period Channel 2: Period of highs and lows to filter signals

Offset: Move Channel 2 to the right x bars to try to filter out the favorable signals.

Period Exit: It is the period of the Donchian channel that is used as trailing for the exits.

Strategy: Order Type direction in which trades are executed.

Take Profit %: When activated, the entered value will be used as the Take Profit in percentage from the entry price level.

Use Custom Test Period: When enabled signals only works in the selected time window. If disabled it will use all historical data available on the chart.

Test Start and End: Once the Custom Test Period is enabled, here you select the start and end date that you want to analyze.

Check Messages: Check Messages: Enable this option to review the messages that will be sent to the bot.

Entry | TP | SL: Enable this options to send Buy Entry, Take Profit (TP), and Stop Loss (SL) signals.

Deal Entry and Deal Exit: Copy and paste the message for the deal start signal and close order at Market Price of the DCA Bot. This is the message that will be sent with the alert to the Bot, you must verify that it is the same as the bot so that it can process properly.

DCA Bot Multi-Pair: You must activate it if you want to use the signals in a DCA Bot Multi-pair in the text box you must enter (using the correct format) the symbol in which you are creating the alert, you can check the format of each symbol when you create the bot.

👨🏻💻💭 We hope this tool helps enhance your trading. Your feedback is invaluable, so feel free to share any suggestions for improvements or new features you'd like to see implemented.

__

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

Supertrend and Fast and Slow EMA StrategyThis strategy combines Exponential Moving Averages (EMAs) and Average True Range (ATR) to create a simple, yet effective, trend-following approach. The strategy filters out fake or sideways signals by incorporating the ATR as a volatility filter, ensuring that trades are only taken during trending conditions. The key idea is to buy when the short-term trend (Fast EMA) aligns with the long-term trend (Slow EMA), and to avoid trades during low volatility periods.

How It Works:

EMA Crossover:

1). Buy Signal: When the Fast EMA (shorter-term, e.g., 20-period) crosses above the Slow EMA (longer-term, e.g., 50-period), this indicates a potential uptrend.

2). Sell Signal: When the Fast EMA crosses below the Slow EMA, this indicates a potential downtrend.

ATR Filter:

1). The ATR (Average True Range) is used to measure market volatility.

2). Trending Market: If the ATR is above a certain threshold, it indicates high volatility and a trending market. Only when ATR is above the threshold will the strategy generate buy/sell signals.

3). Sideways Market: If ATR is low (sideways or choppy market), the strategy will suppress signals to avoid entering during non-trending conditions.

When to Buy:

1). Condition 1: The Fast EMA crosses above the Slow EMA.

2). Condition 2: The ATR is above the defined threshold, indicating that the market is trending (not sideways or choppy).

When to Sell:

1). Condition 1: The Fast EMA crosses below the Slow EMA.

2). Condition 2: The ATR is above the defined threshold, confirming that the market is in a downtrend.

When Not to Enter the Trade:

1). Sideways Market: If the ATR is below the threshold, signaling low volatility and sideways or choppy market conditions, the strategy will not trigger any buy or sell signals.

2). False Crossovers: In low volatility conditions, price action tends to be noisy, which could lead to false signals. Therefore, avoiding trades during these periods reduces the risk of false breakouts.

Additional Factors to Consider Adding:

=> RSI (Relative Strength Index): Adding an RSI filter can help confirm overbought or oversold conditions to avoid buying into overextended moves or selling too low.

1). RSI Buy Filter: Only take buy signals when RSI is below 70 (avoiding overbought conditions).

2). RSI Sell Filter: Only take sell signals when RSI is above 30 (avoiding oversold conditions).

=> MACD (Moving Average Convergence Divergence): Using MACD can help validate the strength of the trend.

1). Buy when the MACD histogram is above the zero line and the Fast EMA crosses above the Slow EMA.

2). Sell when the MACD histogram is below the zero line and the Fast EMA crosses below the Slow EMA.

=> Support/Resistance Levels: Adding support and resistance levels can help you understand market structure and decide whether to enter or exit a trade.

1). Buy when price breaks above a significant resistance level (after a valid buy signal).

2). Sell when price breaks below a major support level (after a valid sell signal).

=> Volume: Consider adding a volume filter to ensure that buy/sell signals are supported by strong market participation. You could only take signals if the volume is above the moving average of volume over a certain period.

=> Trailing Stop Loss: Instead of a fixed stop loss, use a trailing stop based on a percentage or ATR to lock in profits as the trade moves in your favor.

=> Exit Signals: Besides the EMA crossover, consider adding Take Profit or Stop Loss levels, or even using a secondary indicator like RSI to signal an overbought/oversold condition and exit the trade.

Example Usage:

=> Buy Example:

1). Fast EMA (20-period) crosses above the Slow EMA (50-period).

2). The ATR is above the threshold, confirming that the market is trending.

3). Optionally, if RSI is below 70, the buy signal is further confirmed as not being overbought.

=> Sell Example:

1). Fast EMA (20-period) crosses below the Slow EMA (50-period).

2). The ATR is above the threshold, confirming that the market is trending.

3). Optionally, if RSI is above 30, the sell signal is further confirmed as not being oversold.

Conclusion:

This strategy helps to identify trending markets and filters out sideways or choppy market conditions. By using Fast and Slow EMAs combined with the ATR volatility filter, it provides a reliable approach to catching trending moves while avoiding false signals during low-volatility, sideways markets.

High-Low Breakout Strategy with ATR traling Stop LossThis script is a TradingView Pine Script strategy that implements a High-Low Breakout Strategy with ATR Trailing Stop.created by SK WEALTH GURU, Here’s a breakdown of its key components:

Features and Functionality

Custom Timeframe and High-Low Detection

Allows users to select a custom timeframe (default: 30 minutes) to detect high and low levels.

Tracks the high and low within a user-specified period (e.g., first 30 minutes of the session).

Draws horizontal lines for high and low, persisting for a specified number of days.

Trade Entry Conditions

Long Entry: If the closing price crosses above the recorded high.

Short Entry: If the closing price crosses below the recorded low.

The user can choose to trade Long, Short, or Both.

ATR-Based Trailing Stop & Risk Management

Uses Average True Range (ATR) with a multiplier (default: 3.5) to determine a dynamic trailing stop-loss.

Trades reset daily, ensuring a fresh start each day.

Trade Execution and Partial Profit Taking

Stop-loss: Default at 1% of entry price.

Partial profit: Books 50% of the position at 3% profit.

Max 2 trades per day: If the first trade hits stop-loss, the strategy allows one re-entry.

Intraday Exit Condition

All positions close at 3:15 PM to ensure no overnight risk.

Adaptive Fractal Grid Scalping StrategyThis Pine Script v6 component implements an "Adaptive Fractal Grid Scalping Strategy" with an added volatility threshold feature.

Here's how it works:

Fractal Break Detection: Uses ta.pivothigh and ta.pivotlow to identify local highs and lows.

Volatility Clustering: Measures volatility using the Average True Range (ATR).

Adaptive Grid Levels: Dynamically adjusts grid levels based on ATR and user-defined multipliers.

Directional Bias Filter: Uses a Simple Moving Average (SMA) to determine trend direction.

Volatility Threshold: Introduces a new input to specify a minimum ATR value required to activate the strategy.

Trade Execution Logic: Places limit orders at grid levels based on trend direction and fractal levels, but only when ATR exceeds the volatility threshold.

Profit-Taking and Stop-Loss: Implements profit-taking at grid levels and a trailing stop-loss based on ATR.

How to Use

Inputs: Customize the ATR length, SMA length, grid multipliers, trailing stop multiplier, and volatility threshold through the input settings.

Visuals: The script plots fractal points and grid levels on the chart for easy visualization.

Trade Signals: The strategy automatically places buy/sell orders based on the detected fractals, trend direction, and volatility threshold.

Profit and Risk Management: The script includes logic for taking profits and setting stop-loss levels to manage trades effectively.

This strategy is designed to capitalize on micro-movements during high volatility and avoid overtrading during low-volatility trends. Adjust the input parameters to suit your trading style and market conditions.

Gold Trade Setup Strategy

Title: Profitable Gold Setup Strategy with Adaptive Moving Average & Supertrend

Introduction:

This trading strategy for Gold (XAU/USD) combines the Adaptive Moving Average (AMA) and Supertrend, tailored for high-probability setups during specific trading hours. The AMA identifies the trend, while the Supertrend confirms entry and exit points. The strategy is optimized for swing and intraday traders looking to capitalize on Gold’s price movements with precise trade timing.

Strategy Components:

1. Adaptive Moving Average (AMA):

• Reacts dynamically to market conditions, filtering noise in choppy markets.

• Serves as the primary trend indicator.

2. Supertrend:

• Confirms entry signals with clear buy and sell levels.

• Acts as a trailing stop-loss to protect profits.

Trading Rules:

Trading Hours:

• Only take trades between 8:30 AM and 10:30 PM IST.

• Avoid trading outside these hours to reduce noise and low-volume setups.

Buy Setup:

1. Trend Confirmation: The Adaptive Moving Average (AMA) must be green.

2. Signal Confirmation: The Supertrend should turn green after the AMA is green.

3. Trigger: Take the trade when the high of the trigger candle (the candle that turned Supertrend green) is broken.

Sell Setup (Optional if included):

• Reverse the rules for a short trade: AMA and Supertrend should both indicate bearish conditions (red), and take the trade when the low of the trigger candle is broken.

Stop-Loss and Targets:

• Place the stop-loss at the low of the trigger candle for long trades.

• Set a 1:2 risk-reward ratio or use the Supertrend line as a trailing stop-loss.

Timeframes:

• Recommended timeframes: 1H, 4H, or Daily for swing trading.

• For intraday trading, use 15-minute or 30-minute charts.

Why This Strategy Works:

• Combines trend-following (AMA) with momentum-based entries (Supertrend).

• Focused trading hours filter out low-probability setups.

• Provides precise entry, stop-loss, and target levels for disciplined trading.

Conclusion:

This Gold Setup Strategy is designed for traders seeking a structured approach to trading Gold. Follow the rules strictly, backtest the strategy extensively, and share your results. Let’s master the Gold market together!

Tags: #Gold #XAUUSD #SwingTrading #Intraday #Supertrend #AMA #TechnicalAnalysis #GoldStrategy

MicuRobert EMA Cross StrategyThis is a repost of a old strategy that cant be updated anymore, it was a request for a user made in Oct, 6, 2015

Here's a possible engaging description for the tradingview script:

**MicuRobert EMA Cross V2: A Powerful Trading Strategy**

Join the ranks of successful traders with this advanced strategy, designed to help you profit from market trends. The MicuRobert EMA Cross V2 combines two essential indicators - Exponential Moving Average (EMA) and Divergence EMA (DEMA) - to generate buy and sell signals.

**Key Features:**

* **Trading Session Filter**: Only trade during your preferred session, ensuring you're in sync with market conditions.

* **Trailing Stop**: Automatically adjust stop-loss levels to lock in profits or limit losses.

* **Customizable Trade Size**: Set the size of each trade based on your risk tolerance and trading goals.

**How it Works:**

The script uses two EMAs (5-period and 34-period) to identify trends. When the shorter EMA crosses above the longer one, a buy signal is generated. Conversely, when the shorter EMA falls below the longer one, a sell signal is triggered. The strategy also incorporates divergence analysis between price action and the EMAs.

**Visual Aids:**

* **EMA Plots**: Visualize the two EMAs on your chart to gauge market momentum.

* **Buy/Sell Signals**: See when buy or sell signals are generated, along with their corresponding entry prices.

* **Trailing Stop Lines**: Monitor stop-loss levels as they adjust based on price action.

**Get Started:**

Download this script and start trading like a pro! With its robust features and customizable settings, the MicuRobert EMA Cross V2 is an excellent addition to any trader's arsenal.

~Llama3

Formation Defined Moving Support and ResistanceThe script was originally coded in 2018 with Pine Script version 3, and it was in protected code status. It has been updated and optimised for Pine Script v5 and made completely open source.

The Formation Defined Moving Support and Resistance indicator is a sophisticated tool for identifying dynamic support and resistance levels based on specific price formations and level interactions. This indicator goes beyond traditional static support and resistance by updating levels based on predefined formation patterns and market behaviour, providing traders with a more responsive view of potential support and resistance zones.

Features:

The indicator detects essential price levels:

Lower Low (LL)

Higher Low (HL)

Higher High (HH)

Lower High (LH)

Equal Lower Low (ELL)

Equal Higher Low (EHL)

Equal Higher High (EHH)

Equal Lower High (ELH)

By identifying these key points, the script builds a foundation for tracking and responding to changes in price structure.

Pre-defined Formations and Comparisons:

The indicator calculates and recognises nine different pre-defined formations, such as bullish and bearish formations, based on the sequence of price levels.

These formations are compared against previous levels and formations, allowing for a sophisticated understanding of recent market movements and momentum shifts.

This formation-based approach provides insights into whether the price is likely to maintain, break, or reverse key levels.

Dynamic Support and Resistance Levels:

The indicator offers an option to toggle Moving Support and Resistance Levels.

When enabled, the support and resistance levels dynamically adjust:

Upon a change in the detected formation.

When the bar’s closing price breaks the last defined support or resistance level.

This feature ensures that the support and resistance levels adapt quickly to market changes, giving a more accurate and responsive perspective.

Customisable Price Source:

Users can choose the price source for level detection, selecting between close or high/low prices.

This flexibility allows the indicator to adapt to different trading styles, whether the focus is on closing prices for more conservative levels or on highs and lows for more sensitive level tracking.

This indicator can benefit traders relying on dynamic support and resistance rather than fixed, historical levels. It adapts to recent price actions and market formations, making it useful for identifying entry and exit points, trend continuation or reversal, and setting trailing stops based on updated support and resistance levels.

Breadth Thrust Strategy with Volatility Stop-LossThe "Breadth Thrust Strategy with Volatility Stop-Loss" is a trading strategy designed to capitalize on market momentum while managing risk through volatility-based stop-losses. Here's a detailed breakdown of the strategy:

Strategy Overview:

Market Breadth Analysis: The strategy uses the "Breadth Thrust Indicator," which evaluates market momentum by calculating the ratio of advancing stocks to the total number of stocks on the New York Stock Exchange (NYSE). This indicator helps identify bullish market conditions. An optional feature allows for the inclusion of volume data in this calculation, enhancing the signal's robustness.

Signal Generation: A long position is triggered when the smoothed breadth ratio (or the combined breadth and volume ratio) crosses above a specified low threshold (e.g., 0.4). This crossover indicates a potential shift towards positive market momentum.

Key Parameters:

Smoothing Length (length): Defines the period over which the breadth or combined ratio is smoothed using a simple moving average (SMA) to reduce noise and highlight the underlying trend.

Low Threshold (threshold_low): The level below which the smoothed ratio must fall before crossing back above to trigger a long signal.

Hold Periods (hold_periods): The minimum number of periods for which the position will be held once entered, ensuring the strategy captures a meaningful move.

Volatility Multiplier (volatility_multiplier): A multiplier applied to the Average True Range (ATR) to determine the distance of the stop-loss from the entry price, which adjusts according to market volatility.

Trade Management:

Entry Signal: The strategy enters a long position when the smoothed combined ratio crosses above the low threshold, signaling a potential bullish reversal.

ATR-Based Stop-Loss: Upon entering a trade, the strategy calculates a stop-loss level based on the ATR, which measures market volatility. The stop-loss is set at a distance from the entry price, determined by multiplying the ATR by the specified volatility multiplier. This adaptive stop-loss mechanism helps protect the position from adverse market moves.

Stop-Loss Adjustment: While the position is open, the stop-loss level is dynamically updated, ensuring it never decreases (trailing stop-loss effect) but can be adjusted upwards to reflect the latest price action relative to volatility.

Position Closure: The position is closed if:

The market price falls to or below the stop-loss level.

The position has been held for the specified number of periods (hold_periods), after which it is automatically closed.

Additional Settings:

Initial Capital: The strategy starts with an initial capital of $10,000.

Commissions and Slippage: Each trade incurs a commission of $5 per order, and slippage is accounted for at $1 per trade.

Background Highlighting: The chart background turns green when a position is open, providing a clear visual indication of the active trade.

This strategy is designed to identify and capitalize on upward momentum in the market while employing a volatility-adjusted stop-loss to manage risk. By combining market breadth analysis with volatility-based stop-losses, the strategy aims to balance profit potential with protection against sudden market reversals.

RSI Trail [UAlgo]The RSI Trail indicator is a technical analysis tool designed to assist traders in making informed decisions by utilizing the Relative Strength Index (RSI) and various moving average calculations. This indicator dynamically plots support and resistance levels based on RSI values, providing visual cues for potential bullish and bearish signals. The inclusion of a trailing stop mechanism allows traders to adapt to market volatility, ensuring optimal entry and exit points.

🔶 Key Features

Multiple Moving Average Types: Choose from Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), Running Moving Average (RMA), and McGinley Dynamic for diverse analytical approaches.

Configurable RSI Bounds: Tailor the RSI lower and upper bounds to your specific trading preferences, with default settings at 40 and 60.

Signals: The indicator determines bullish and bearish market states and plots corresponding signals on the chart.

Customizable Visualization: Options to display the midline and color candles based on market state enhance visual analysis.

Alerts: Integrated alert conditions notify you of bullish and bearish signals.

🔶 Calculations

The RSI Trail indicator calculates dynamic support and resistance levels using a combination of moving averages and the Relative Strength Index (RSI). It starts by computing a chosen moving average (SMA, EMA, WMA, RMA, or McGinley) over a period of 27 using the typical price (ohlc4).

The indicator then defines upper and lower bounds based on customizable RSI levels (default 40 and 60) and adjusts these bounds using the Average True Range (ATR) to account for market volatility. The upper bound is calculated by adding a volatility-adjusted value to the moving average, while the lower bound is found by subtracting this value. Bullish signals occur when the price crosses above the upper bound, and bearish signals when it falls below the lower bound.

The RSI Trail indicator also can be used to identify pullback opportunities. When the price high/low crosses above/below the calculated upper/lower bound, it indicates a potential pullback, suggesting a favorable point to enter a trade during a pullback.

🔶 Disclaimer

This indicator is for informational purposes only and should not be considered financial advice.

Always conduct your own research and due diligence before making any trading decisions. Past performance is not necessarily indicative of future results.

KumoTrade Ichimoku StrategyThe KumoTrade Ichimoku Strategy is an advanced trading strategy designed to help users identify market trends and potential trading opportunities using the Ichimoku Kinko Hyo technical analysis indicator. This strategy leverages the Ichimoku cloud (Kumo) along with other crucial indicators such as the Tenkan-sen and Kijun-sen lines to generate strong signals.

Main Components of the Strategy:

Tenkan-sen (Conversion Line): Indicates the short-term direction of the price, typically calculated as the average of the highest high and the lowest low over the past 9 periods.

Kijun-sen (Base Line): Indicates the medium-term direction of the price, usually calculated as the average of the highest high and the lowest low over the past 26 periods.

Senkou Span A and Senkou Span B: These two lines form the cloud (Kumo), which projects future support and resistance levels.

Chikou Span (Lagging Span): Plots the current closing price 26 periods back to measure the market's momentum.

Strategy Rules:

Bullish Bias (Bias Bull): Indicates that the prices are in a long-term uptrend. In this strategy, this is confirmed if the low prices are above the daily EMA (Exponential Moving Average).

Kijun Sen Touch Down: Occurs when prices cross below the Kijun-sen line and then close back above it, indicating a potential bullish reversal.

Tenkan-Kijun Cross Up: A bullish signal generated when the Tenkan-sen line crosses above the Kijun-sen line.

Close Over Tenkan and Kijun: A strong bullish signal when the close price crosses above both the Tenkan-sen and Kijun-sen lines.

Trading Setups:

Long Setup: Generated when the Kijun-sen is above the highest point of the Kumo (senkou_max) and the closing price is below the lowest point of the Kumo (senkou_min). This setup is checked over the last 21 bars.

Short Setup: Generated when the Kijun-sen is below the lowest point of the Kumo (senkou_min) and the closing price is above the highest point of the Kumo (senkou_max). This setup is also checked over the last 21 bars. (Not avalible yet)

Entry Conditions:

Ultra Long Entry: This condition checks for a bullish bias, the Tenkan-Kijun cross up or Kijun Sen touch down, high volume, and that the price is not within the Kumo cloud.

Main Long Entry: This condition requires the closing price to be above the Kumo cloud, a green Kumo cloud, a bullish bias, the Tenkan rule, and that the price is not within the Kumo cloud.

Exit Conditions:

A trailing stop loss is implemented to protect profits. The stop loss level is dynamically updated based on the highest high of the last 5 bars minus three times the ATR (Average True Range) value.

Visuals on the Chart:

The Tenkan-sen and Kijun-sen lines are plotted for visual reference.

The Kumo cloud is displayed with different colors indicating bullish (green) or bearish (red) conditions.

Entry points are marked on the chart, and the trailing stop loss levels are plotted as well.

The KumoTrade Ichimoku Strategy aims to provide a comprehensive approach to trading by combining multiple aspects of the Ichimoku indicator to generate reliable trading signals and manage risk effectively.

Triple EMA + QQE Trend Following Strategy [TradeDots]The "Triple EMA + QQE Trend Following Strategy" harnesses the power of two sophisticated technical indicators, the Triple Exponential Moving Average (TEMA) and the Qualitative Quantitative Estimation (QQE), to generate precise buy and sell signals. This strategy excels in capturing shifts in trends by identifying short-term price momentum and dynamic overbought or oversold conditions.

HOW IT WORKS

This strategy integrates two pivotal indicators:

Triple Exponential Moving Average (TEMA): TEMA enhances traditional moving averages by reducing lag and smoothing the data more effectively. It achieves this by applying the EMA formula three times onto the price, as follows:

tema(src, length) =>

ema1 = ta.ema(src, length)

ema2 = ta.ema(ema1, length)

ema3 = ta.ema(ema2, length)

tema = 3*ema1 - 3*ema2 + ema3

This computation helps to sharpen the sensitivity to price movements.

Qualitative Quantitative Estimation (QQE): The QQE indicator improves upon the standard RSI by incorporating a smoothing mechanism. It starts with the standard RSI, overlays a 5-period EMA on this RSI, and then enhances the result using a double application of a 27-period EMA. A slow trailing line is then derived by multiplying the result with a factor number. This approach establishes a more refined and less jittery trend-following signal, complementing the TEMA to enhance overall market timing during fluctuating conditions.

APPLICATION

Referenced from insights on "Trading Tact," the strategy implementation follows:

First of all, we utilize two TEMA lines: one set at a 20-period and the other at a 40-period. Then following the rules below:

40-period TEMA is rising

20-period TEMA is above 40-period TEMA

Price closes above 20-period TEMA

Today is not Monday

RSI MA crosses the Slow trailing line

This strategy does not employ an active take profit mechanism; instead, it utilizes a trailing stop loss to allow the price to reach the stop loss naturally, thereby maximizing potential profit margins.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and style.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Reference:

Trading Tact. What Is the QQE Indicator? Retrieved from: tradingtact.com

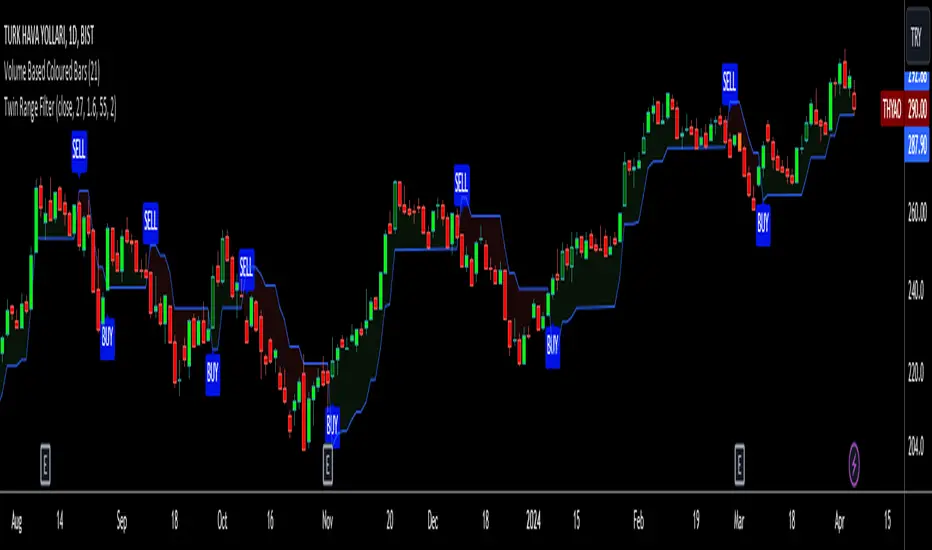

Twin Range Filter VisualizedVisulaized version of @colinmck's Twin Range Filter version on TradingView.

On @colinmck's Twin Range Filter version, you can only see Long and Short signals on the chart.

But in this version of TRF, users can visually see the BUY and SELL signals on the chart with an added line of TRF.

TRF is an average of two smoothed Exponential Moving Averages, fast one has 27 bars of length and the slow one has 55 bars.

The purpose is to obtain two ranges that price fluctuates between (upper and lower range) and have LONG AND SHORT SIGNALS when close price crosses above the upper range and conversely crosses below lower range.

I personally combine the upper and lower ranges on one line to see the long and short signals with my own eyes so,

-BUY when price is higher or equal to the upper range level and the indicator line turns to draw the lower range to follow the price just under the bars as a trailing stop loss indicator like SuperTrend.

-SELL when price is lower or equal to the lower range levelline under the bars and then the indicator line turns to draw the upper range to follow the price just over the bars in that same trailing stop loss logic.

There are also two coefficients that adjusts the trailing line distance levels from the price multiplying the effect of the faster and slower moving averages.

The default values of the multipliers:

Fast range multiplier of Fast Moving Average(27): 1.6

Slow range multiplier of fSlow Moving Average(55): 2

Remember that if you enlarge these multipliers you will enlarge the ranges and have less but lagging signals. Conversely, decreasing the multipliers will have small ranges (line will get closer to the price and more signals will occur)

Long EMA Strategy with Advanced Exit OptionsThis strategy is designed for traders seeking a trend-following system with a focus on precision and adaptability.

**Core Strategy Concept**

The essence of this strategy lies in use of Exponential Moving Averages (EMAs) to identify potential long (buy) positions based on the relative positions of short-term, medium-term, and long-term EMAs. The use of EMAs is a classic yet powerful approach to trend detection, as these indicators smooth out price data over time, emphasizing the direction of recent price movements and potentially signaling the beginning of new trends.

**Customizable Parameters**

- **EMA Periods**: Users can define the periods for three EMAs - long-term, medium-term, and short-term - allowing for a tailored approach to capture trends based on individual trading styles and market conditions.

- **Volatility Filter**: An optional Average True Range (ATR)-based volatility filter can be toggled on or off. When activated, it ensures that trades are only entered when market volatility exceeds a user-defined threshold, aiming to filter out entries during low-volatility periods which are often characterized by indecisive market movements.

- **Trailing Stop Loss**: A trailing stop loss mechanism, expressed as a percentage of the highest price achieved since entry, provides a dynamic way to manage risk by allowing profits to run while cutting losses.

- **EMA Exit Condition**: This advanced exit option enables closing positions when the short-term EMA crosses below the medium-term EMA, serving as a signal that the immediate trend may be reversing.

- **Close Below EMA Exit**: An additional exit condition, which is disabled by default, allows positions to be closed if the price closes below a user-selected EMA. This provides an extra layer of flexibility and risk management, catering to traders who prefer to exit positions based on specific EMA thresholds.

**Operational Mechanics**

Upon activation, the strategy evaluates the current price in relation to the set EMAs. A long position is considered when the current price is above the long-term EMA, and the short-term EMA is above the medium-term EMA. This setup aims to identify moments where the price momentum is strong and likely to continue.

The strategy's versatility is further enhanced by its optional settings:

- The **Volatility Filter** adjusts the sensitivity of the strategy to market movements, potentially improving the quality of the entries during volatile market conditions.

The Average True Range (ATR) is a key component of this filter, providing a measure of market volatility by calculating the average range between the high and low prices over a specified number of periods. Here's how you can adjust the volatility filter settings for various market conditions, focusing on filtering out low-volatility markets:

Setting Examples for Volatility Filter

1. High Volatility Markets (e.g., Cryptocurrencies, Certain Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: Setting the multiplier to a lower value, such as 1.0 or 1.2, can be beneficial in high-volatility markets. This sensitivity allows the strategy to react to volatility changes more quickly, ensuring that you're entering trades during periods of significant movement.

2. Medium Volatility Markets (e.g., Major Equity Indices, Medium-Volatility Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: A multiplier of 1.5 (default) is often suitable for medium volatility markets. It provides a balanced approach, ensuring that the strategy filters out low-volatility conditions without being overly restrictive.

3. Low Volatility Markets (e.g., Some Commodities, Low-Volatility Forex Pairs):

ATR Periods: Increasing the ATR period to 20 or 25 can smooth out the volatility measure, making it less sensitive to short-term fluctuations. This adjustment helps in focusing on more significant trends in inherently stable markets.

ATR Multiplier: Raising the multiplier to 2.0 or even 2.5 increases the threshold for volatility, effectively filtering out low-volatility conditions. This setting ensures that the strategy only triggers trades during periods of relatively higher volatility, which are more likely to result in significant price movements.

How to Use the Volatility Filter for Low-Volatility Markets

For traders specifically interested in filtering out low-volatility markets, the key is to adjust the ATR Multiplier to a higher level. This adjustment increases the threshold required for the market to be considered sufficiently volatile for trade entries. Here's a step-by-step guide:

Adjust the ATR Multiplier: Increase the ATR Multiplier to create a higher volatility threshold. A multiplier of 2.0 to 2.5 is a good starting point for very low-volatility markets.

Fine-Tune the ATR Periods: Consider lengthening the ATR calculation period if you find that the strategy is still entering trades in undesirable low-volatility conditions. A longer period provides a more averaged-out measure of volatility, which might better suit your needs.

Monitor and Adjust: Volatility is not static, and market conditions can change. Regularly review the performance of your strategy in the context of current market volatility and adjust the settings as necessary.

Backtest in Different Conditions: Before applying the strategy live, backtest it across different market conditions with your adjusted settings. This process helps ensure that your approach to filtering low-volatility conditions aligns with your trading objectives and risk tolerance.

By fine-tuning the volatility filter settings according to the specific characteristics of the market you're trading in, you can enhance the performance of this strategy

- The **Trailing Stop Loss** and **EMA Exit Conditions** provide two layers of exit strategies, focusing on capital preservation and profit maximization.

**Visualizations**

For clarity and ease of use, the strategy plots the three EMAs and, if enabled, the ATR threshold on the chart. These visual cues not only aid in decision-making but also help in understanding the market's current trend and volatility state.

**How to Use**

Traders can customize the EMA periods to fit their trading horizon, be it short, medium, or long-term trading. The volatility filter and exit options allow for further customization, making the strategy adaptable to different market conditions and personal risk tolerance levels.

By offering a blend of trend-following principles with advanced risk management features, this strategy aims to cater to a wide range of trading styles, from cautious to aggressive. Its strength lies in its flexibility, allowing traders to fine-tune settings to their specific needs, making it a potentially valuable tool in the arsenal of any trader looking for a disciplined approach to navigating the markets.

OTT CollectionIf you are not yet familiar with OTT, this script could provide an introduction to help you get started.

"Optimized Trend Tracker" (OTT) is an effective trend-following indicator created by Anıl Özekşi . It aims to detect the current trend direction based on an elegant mathematical construct. The key defining characteristic of OTT is its reliance on a trailing-stop mechanism. This enables OTT to identify price movements and follow the price until a reversal occurs. The widespread adoption of OTT in various algo-trading platforms has fostered the development of diverse applications of the indicator over time. Examining its history, eight distinct applications emerge.

1) OTT - Optimized Trend Tracker

2) TOTT - Twin Ott

3) OTT Channel - Half Channel & Fibonacci Channel

4) RISOTTO - Rsi Ott

5) SOTT - Stochastic Ott

6) HOTT & LOTT - Highest-Lowest Ott + Sum Option

7) ROTT - Relative Ott

8) FT - "Fırsatçı" Trend

BONUS: RTR - Relative True Range

Each system functions as an independent indicator and the "OTT Collection" is intended to present all of them in a single script.

ORIGINALITY

Primarily, this script introduces previously unreleased OTT applications on Tradingview (RISOTTO, ROTT, FT). In contrast to previously published examples that treat OTT as a variable, this script portrays OTT as a function, rendering it adaptable for more intricate computations. Consequently, OTT has evolved into a versatile tool capable of facilitating complex analyses. Furthermore, this script offers an innovative feature that permits the blocking of consecutive signals in the same direction, catering to user preferences. (This feature is crucial for all indicators utilizing band structures such as TOTT and HOTT-LOTT).

USAGE

It is simple to use. The settings section of the indicator groups the parameters. In first group, the System parameter allows you to select the OTT system you want to display on the chart. Activating the Pyramiding parameter enables the display of consecutive signals in the same direction (for TOTT and HOTT-LOTT). In the second group you can change the display options with the Barcolor, Signal and Bars parameters. The OTT system you select is configured with the parameters in the group with the corresponding system heading. (For example, suppose you select OTT CHANNEL in the system parameter. The parameters defining the channels are grouped under the heading "OTT CHANNELS" in the settings section.) Also the parameters you chose are displayed in table form on the chart screen. The table also presents the total number of bars on the chart and the number of signals generated by the selected system.

MECHANICS

Let's take a look at how the indicator works. This indicator incorporates eight distinct OTT systems, each characterized by unique parameters, lines, and signals. (Exception: OTT Channel does not include any referenced signals.)

1) WHAT IS "OTT"?

OTT comprises two lines: Support and Target. There's an up-trending market when the Support is superior to the Target, and a down-trending market when the Support is inferior to the Target. It is governed by two parameters. The Support (moving average) is determined by the Length parameter, while the Multiplier parameter is employed for percentage calculations. Lower values are adept at capturing short-term fluctuations, whereas higher values are more adept at identifying long-term trends. These principles apply to all parameters within the indicator.

DETAILED INFO : The OTT function in the script automatically performs the calculation process described in this section. So, if you know how OTT works you can skip the details. To comprehend its functioning, it's essential to grasp the "MOST" indicator, also devised by Anıl Özekşi. The fundamental principle of MOST involves creating bands that function akin to a trailing stop-loss. Initially, a moving average, referred to as the 'Support,' is established. (Anıl Özekşi employs VAR/VIDYA as the moving average type in all his systems.) Subsequently, the Support line is adjusted both upward and downward by a percentage multiplier to establish a band system. In the context of the trailing stop-loss concept, when the Support line approaches either the lower or upper band, the respective band ceases to move in parallel with the Support line and becomes horizontal. Consequently, the Support always intersects the band at some point. The values of the upper or lower bands, determined by this intersection, are referred to as the MOST line. OTT is generated by consolidating the values of MOST shifted upwards and downwards by half the coefficient percentage into a single line using the same method as above, and calculating the value of this line from two bars ago. Support is the data series of OTT and it serves as a source in OTT function. The OTT line is named as "Target" in this scipt. Support and Target will automatically vary according to the OTT application selected in the "System" parameter.

2) WHAT IS "TOTT"?

Twin OTT , also known as the "OTT Band," involves three parameters: Length, Multiplier, and Band Multiplier. It consists of three lines: Support, Upper Line, and Lower Line. OTT is determined by the Length and Multiplier parameters, while TOTT is calculated by adjusting OTT upwards and downwards as per the Band Multiplier parameter. The indicator generates signals based on the intersections of the Support and these two new OTT levels.

3) WHAT IS "OTT CHANNEL"?

Similar to TOTT, the OTT CHANNEL is also based on shifted OTT levels, employing a similar calculation method. The primary distinction lies in the fact that TOTT has a single Band Multiplier, whereas OTT CHANNEL incorporates two line multipliers for the band. It encompasses four parameters: Length, Multiplier, Upper Line Multiplier, and Lower Line Multiplier. OTT is defined by the Length and Multiplier parameters. The Upper Line Multiplier and Lower Line Multiplier parameters establish the channel boundaries by shifting the OTT line. Subsequently, levels are drawn between the upper and lower lines. The additional Channel Type parameter determines which levels are displayed on the chart. The "Half Channel" option draws channels shifted by half the coefficient. The "Fibonacci Channel" option draws channels shifted by 0.382 and 0.618 coefficients. The "Both" option plots all levels.

4) WHAT IS "RISOTTO"?

OTT also has application examples in momentum oscillators. RISOTTO utilizes the RSI indicator and operates with three parameters. The RSI is defined by the Length 1 parameter, while the Support is determined by the Length 2 parameter. The Multiplier parameter is utilized for percentage calculations. RISOTTO comprises two lines: Support and Target. To ensure more stable calculations, a constant (+1000) is added to the oscillator average when applying OTT to momentum oscillators. This approach eradicates nonsensical results stemming from percentage calculations when the oscillator reaches a value of 0. The indicator generates signals based on the intersection of these two lines.

5) WHAT IS "SOTT"?

Stochastic OTT is an another example of application on oscillator. Its working principle is akin to that of RISOTTO. It operates with three parameters. The Stochastic %k is defined by the Length 1 parameter, while the Stochastic %d is determined by the Length 2 parameter. The Multiplier parameter is utilized for percentage calculations. SOTT comprises two lines: Support and Target. The indicator generates signals based on the intersection of these two lines.

6) WHAT IS "HOTT-LOTT"?

OTT can be applied to the highest and lowest series as well. HOTT-LOTT operates with three parameters: Length, Multiplier, and Sum N Bars. The highest and lowest series are defined by the Length parameter. The Multiplier parameter is utilized for percentage calculations. It encompasses two lines: Upper Line and Lower Line, where HOTT employs the highest series and LOTT uses the lowest series. If the 'High' price surpasses HOTT, the indicator generates Long signals. Similarly, if the 'Low' price falls below LOTT, the indicator generates Short signals. When the Sum N Bars option is activated, signals are generated based on the confirmation concept for N bars.

7) WHAT IS "ROTT"?

Relative OTT serves as a valuable tool for long-period filters. ROTT operates with two parameters. The Support is determined by the length parameter and equals twice the moving average. The Multiplier parameter is utilized for percentage calculations. The indicator generates signals based on the intersection of these two lines.

8) WHAT IS "FT"?

"Fırsatçı" (opportunistic) Trend is a system that revolves around two levels, namely major and minor OTT. It operates with three parameters: Length, Major Multiplier, and Minor Multiplier. FT comprises two lines, Support and Target. The indicator generates signals based on the intersection of these two lines.

9) WHAT IS "RTR"?

Relative True Range is not an OTT system; however, it serves as a complementary feature. It does not have any referenced signals. RTR is devised to obtain a normalized result of the current market volatility. It operates with two parameters: ATR, which is determined by the Length 1 parameter, and RTR, defined by the Length 2 parameter.

A TIP

If any indicator is defined in function form instead of the OTT function, the applications can also be adapted for different indicators. E.g. Supertrend, PMAX, AlphaTrend, etc.

UPDATE

Anıl Özekşi is a competent algotrader who shares his work with open sources. I will update the indicator as new applications are released.

DISCLEIMER

This is just an indicator, nothing more. The script is for informational and educational purposes only. The use of the script does not constitute professional and/or financial advice. The responsibility for risks associated with the use of the script is solely owned by the user. Do not forget to manage your risk. And trade as safely as possible. Good luck!

TradingView.To Strategy Template (with Dyanmic Alerts)Hello traders,

If you're tired of manual trading and looking for a solid strategy template to pair with your indicators, look no further.

This Pine Script v5 strategy template is engineered for maximum customization and risk management.

Best part?

This Pine Script v5 template facilitates the dynamic construction of TradingView.TO alerts, sparing users the time and effort of mastering the TradingView.TO syntax and manually create alert commands.

This powerful tool gives much power to those who don't know how to code in Pinescript and want to automate their indicators' signals via TradingView.TO bot.

IMPORTANT NOTES

TradingView.TO is a trading bot software that forwards TradingView alerts to your brokers (examples: Binance, Oanda, Coinbase, Bybit, Metatrader 4/5, ...) for automating trading.

Many traders don't know how to create TradingView.TO dynamically-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to break options from your script and then create the orders accordingly.

This script showcases how to create TradingView.TO alerts dynamically.

TRADINGVIEW ALERTS

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example: 1 alert for BTC/USDT on the 5 minutes chart, 1 alert for BTC/USDT on the 15-minute chart (assuming you want your bot to trade the BTC/USDT on the 5 and 15-minute timeframes)

2) Select the Order fills and alert() function calls condition

3) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

4) TradingView.TO uses webhook technology - setting a webhook URL from the alerts notifications tab is required.

KEY FEATURES

I) Modular Indicator Connection

* plug your existing indicator into the template.

* Only two lines of code are needed for full compatibility.

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

To do so:

1) Find in your indicator where the conditions print the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator, whether a MACD , ZigZag, Pivots , higher-highs, lower-lows or whatever indicator with clear buy and sell conditions.

//@version=5

indicator("Supertrend", overlay = true, timeframe = "", timeframe_gaps = true)

atrPeriod = input.int(10, "ATR Length", minval = 1)

factor = input.float(3.0, "Factor", minval = 0.01, step = 0.01)

= ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, display = display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps = false)

buy = ta.crossunder(direction, 0)

sell = ta.crossunder(direction, 0)

//////// CONNECTOR SECTION ////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title = "Signal", display = display.data_window)

//////// CONNECTOR SECTION ////////

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal and -1 for the bearish signal

Now, you can connect your indicator to the Strategy Template using the method below or that one.

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings, and in the Data Source field, select your 🔌Connector🔌 (which comes from your indicator)

Note it doesn’t have to be named 🔌Connector🔌 - you can name it as you want - however, I recommend an explicit name you can easily remember.

From then, you should start seeing the signals and plenty of other stuff on your chart.

🔥 Note that whenever you update your indicator values, the strategy statistics and visuals on your chart will update in real-time

II) BOT Risk Management:

- Max Drawdown:

Mode: Select whether the max drawdown is calculated in percentage (%) or USD.

Value: If the max drawdown reaches this specified value, set a value to halt the bot.

- Max Consecutive Days:

Use Max Consecutive Days BOT Halt: Enable/Disable halting the bot if the max consecutive losing days value is reached.

- Max Consecutive Days: Set the maximum number of consecutive losing days allowed before halting the bot.

- Max Losing Streak:

Use Max Losing Streak: Enable/Disable a feature to prevent the bot from taking too many losses in a row.

- Max Losing Streak Length: Set the maximum length of a losing streak allowed.

Margin Call:

- Use Margin Call: Enable/Disable a feature to exit when a specified percentage away from a margin call to prevent it.

Margin Call (%): Set the percentage value to trigger this feature.

- Close BOT Total Loss:

Use Close BOT Total Loss: Enable/Disable a feature to close all trades and halt the bot if the total loss is reached.

- Total Loss ($): Set the total loss value in USD to trigger this feature.

Intraday BOT Risk Management:

- Intraday Losses:

Use Intraday Losses BOT Halt: Enable/Disable halting the bot on reaching specified intraday losses.

Mode: Select whether the intraday loss is calculated in percentage (%) or USD.

- Max Intraday Losses (%): Set the value for maximum intraday losses.

Limit Intraday Trades:

- Use Limit Intraday Trades: Enable/Disable a feature to limit the number of intraday trades.

- Max Intraday Trades: Set the maximum number of intraday trades allowed.

Restart Intraday EA:

III) Order Types and Position Sizing

- Choose between market or limit orders.

- Set your position size directly in the template.

Please use the position size from the “Inputs” and not the “Properties” tab.

I know it's redundant. - the template needs this value from the "Inputs" tab to build the alerts, and the Backtester needs it from the "Properties" tab.

IV) Advanced Take-Profit and Stop-Loss Options

- Choose to set your SL/TP in either USD or percentages.

- Option for multiple take-profit levels and trailing stop losses.

- Move your stop loss to break even +/- offset in USD for “risk-free” trades.

V) Miscellaneous:

Retry order openings if they fail.

Order Types:

Select and specify order type and price settings.

Position Size:

Define the type and size of positions.

Leverage:

Leverage settings, including margin type and hedge mode.

Session:

Limit trades to specific sessions.

Dates:

Limit trades to a specific date range.

Trades Direction:

Direction: Specify the market direction for opening positions.

VI) Logger

The TradingView.TO commands are logged in the TradingView logger.

You'll find more information about it in this TradingView blog post .

WHY YOU MIGHT NEED THIS TEMPLATE

1) Transform your indicator into a TradingView.TO trading bot more easily than before

Connect your indicator to the template

Create your alerts

Set your EA settings

2) Save Time

Auto-generated alert messages for TradingView.TO.

I tested them all and checked with the support team what could/couldn’t be done.

3) Be in Control

Manage your trading risks with advanced features.

4) Customizable

Fits various trading styles and asset classes.

REQUIREMENTS

* Make sure you have your TradingView.TO account

* If there is any issue with the template, ask me in the comments section - I’ll answer quickly.

BACKTEST RESULTS FROM THIS POST

1) I connected this strategy template to a dummy Supertrend script.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with TradingView.TO.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

This strategy is a template to be connected to any indicator - the sky is the limit. :)

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

* Initial Capital: 100000 USD

* Position Size: 1%

* Commission Percent: 0.075%

* Slippage: 1 tick

* No margin/leverage used

Pineconnector Strategy Template (Connect Any Indicator)Hello traders,

If you're tired of manual trading and looking for a solid strategy template to pair with your indicators, look no further.

This Pine Script v5 strategy template is engineered for maximum customization and risk management.

Best part?

It’s optimized for Pineconnector, allowing seamless integration with MetaTrader 4 and 5.

This powerful tool gives a lot of power to those who don't know how to code in Pinescript and are looking to automate their indicators' signals on Metatrader 4/5.

IMPORTANT NOTES

Pineconnector is a trading bot software that forwards TradingView alerts to your Metatrader 4/5 for automating trading.

Many traders don't know how to dynamically create Pineconnector-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to break options from your script and then create the orders accordingly.

This script showcases how to create Pineconnector alerts dynamically.

Pineconnector doesn't support alerts with multiple Take Profits.

As a workaround, for 2 TPs, I had to open two trades.

It's not optimal, as we end up paying more spreads for that extra trade - however, depending on your trading strategy, it may not be a big deal.

TRADINGVIEW ALERTS

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example: 1 alert for EUR/USD on the 5 minutes chart, 1 alert for EUR/USD on the 15-minute chart (assuming you want your bot to trade the EUR/USD on the 5 and 15-minute timeframes)

2) Select the Order fills and alert() function calls condition

3) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

4) Don't forget to set the Pineconnector webhook URL in the Notifications tab of the TradingView alerts UI.

You’ll find the URL on the Pineconnector documentation website.

EA CONFIGURATION

1) The Pyramiding in the EA on Metatrader must be set to 2 if you want to trade with 2 TPs => as it's opening 2 trades.

If you only want 1 TP, set the EA Pyramiding to 1.

Regarding the other EA settings, please refer to the Pineconnector documentation on their website.

2) In the EA, you can set a risk (= position size type) in %/lots/USD, as in the TradingView backtest settings.

KEY FEATURES

I) Modular Indicator Connection

* plug in your existing indicator into the template.

* Only two lines of code are needed for full compatibility.

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

To do so:

1) Find in your indicator where the conditions print the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator, whether it's a MACD , ZigZag , Pivots , higher-highs, lower-lows, or whatever indicator with clear buy and sell conditions.

//@version=5

indicator("Supertrend", overlay = true, timeframe = "", timeframe_gaps = true)

atrPeriod = input.int(10, "ATR Length", minval = 1)

factor = input.float(3.0, "Factor", minval = 0.01, step = 0.01)

= ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, display = display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps = false)

buy = ta.crossunder(direction, 0)

sell = ta.crossunder(direction, 0)

//////// CONNECTOR SECTION ////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title = "Signal", display = display.data_window)

//////// CONNECTOR SECTION ////////

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal and -1 for the bearish signal

Now, you can connect your indicator to the Strategy Template using the method below or that one.

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings, and in the Data Source field, select your 🔌Connector🔌 (which comes from your indicator)

Note it doesn’t have to be named 🔌Connector🔌 - you can name it as you want - however, I recommend an explicit name you can easily remember.

From then, you should start seeing the signals and plenty of other stuff on your chart.

🔥 Note that whenever you update your indicator values, the strategy statistics and visuals on your chart will update in real-time

II) Customizable Risk Management

- Choose between percentage or USD modes for maximum drawdown.

- Set max consecutive losing days and max losing streak length.

- I used the code from my friend @JosKodify for the maximum losing streak. :)

Will halt the EA and backtest orders fill whenever either of the safeguards above are “broken”

III) Intraday Risk Management

- Limit the maximum intraday losses both in percentage or USD.

- Option to set a maximum number of intraday trades.

- If your EA gets halted on an intraday chart, auto-restart it the next day.

IV) Spread and Account Filters

- Trade only if the spread is below a certain pip value.

- Set requirements based on account balance or equity.

V) Order Types and Position Sizing

- Choose between market, limit, or stop orders.

- Set your position size directly in the template.

Please use the position size from the “Inputs” and not the “Properties” tab.

Reason : The template sends the order on the same candle as the entry signals - at those entry signals candles, the position size isn’t computed yet, and the template can’t then send it to Pineconnector.

However, you can use the position size type (USD, contracts, %) from the “Properties” tab for backtesting.

In the EA, you can define the position size type for your orders in USD or lots or %.

VI) Advanced Take-Profit and Stop-Loss Options

- Choose to set your SL/TP in either pips or percentages.

- Option for multiple take-profit levels and trailing stop losses.

- Move your stop loss to break even +/- offset in pips for “risk-free” trades.

VII) Logger

The Pineconnector commands are logged in the TradingView logger.

You'll find more information about it in this TradingView blog post .

WHY YOU MIGHT NEED THIS TEMPLATE

1) Transform your indicator into a Pineconnector trading bot more easily than before

Connect your indicator to the template

Create your alerts

Set your EA settings

2) Save Time

Auto-generated alert messages for Pineconnector.

I tested them all, and I checked with the support team what could/can’t be done

3) Be in Control

Manage your trading risks with advanced features.

4) Customizable

Fits various trading styles and asset classes.

REQUIREMENTS

* Make sure you have your Pineconnector license ID.

* Create your alerts with the Pineconnector webhook URL

* If there is any issue with the template, ask me in the comments section - I’ll answer quickly.

BACKTEST RESULTS FROM THIS POST

1) I connected this strategy template to a dummy Supertrend script.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with Pineconnector.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

This strategy is a template to be connected to any indicator - the sky is the limit. :)

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

* Initial Capital: 100000 USD

* Position Size: 1 contract

* Commission Percent: 0.075%

* Slippage: 1 tick

* No margin/leverage used

WHAT’S COMING NEXT FOR YOU GUYS?

I’ll make the same template for ProfitView, then for AutoView, and then for Alertatron.

All of those are free and open-source.

I have no affiliations with any of those companies - I'm publishing those templates as they will be useful to many of you.

Dave

Heatmap MACD Strategy - Pineconnector (Dynamic Alerts)Hello traders

This script is an upgrade of this template script.

Heatmap MACD Strategy

Pineconnector

Pineconnector is a trading bot software that forwards TradingView alerts to your Metatrader 4/5 for automating trading.

Many traders don't know how to dynamically create Pineconnector-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to breakeven options from your script and then create the orders accordingly.

This script showcases how to create Pineconnector alerts dynamically.

Pineconnector doesn't support alerts with multiple Take Profits.

As a workaround, for 2 TPs, I had to open two trades.

It's not optimal, as we end up paying more spreads for that extra trade - however, depending on your trading strategy, it may not be a big deal.

TradingView Alerts

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example : 1 alert for EUR/USD on the 5 minutes chart, 1 alert for EUR/USD on the 15-minute chart (assuming you want your bot to trade the EUR/USD on the 5 and 15-minute timeframes)

2) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

3) Don't forget to set the webhook URL in the Notifications tab of the TradingView alerts UI.

EA configuration

The Pyramiding in the EA on Metatrader must be set to 2 if you want to trade with 2 TPs => as it's opening 2 trades.

If you only want 1 TP, set the EA Pyramiding to 1.

Regarding the other EA settings, please refer to the Pineconnector documentation on their website.

Logger

The Pineconnector commands are logged in the TradingView logger.

You'll find more information about it from this TradingView blog post

Important Notes

1) This multiple MACDs strategy doesn't matter much.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with Pineconnector.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

Initial Capital: 100000 USD

Position Size: 1 contract

Commission Percent: 0.075%

Slippage: 1 tick

No margin/leverage used

For example, those are realistic settings for trading CFD indices with low timeframes but not the best possible settings for all assets/timeframes.

Concept

The Heatmap MACD Strategy allows selecting one MACD in five different timeframes.

You'll get an exit signal whenever one of the 5 MACDs changes direction.

Then, the strategy re-enters whenever all the MACDs are in the same direction again.

It takes:

long trades when all the 5 MACD histograms are bullish

short trades when all the 5 MACD histograms are bearish

You can select the same timeframe multiple times if you don't need five timeframes.

For example, if you only need the 30min, the 1H, and 2H, you can set your timeframes as follow:

30m

30m

30m