TradZoo - EMA Crossover IndicatorDescription:

This EMA Crossover Trading Strategy is designed to provide precise Buy and Sell signals with confirmation, defined targets, and stop-loss levels, ensuring strong risk management. Additionally, a 30-candle gap rule is implemented to avoid frequent signals and enhance trade accuracy.

📌 Strategy Logic

✅ Exponential Moving Averages (EMAs):

Uses EMA 50 & EMA 200 for trend direction.

Buy signals occur when price action confirms EMA crossovers.

✅ Entry Confirmation:

Buy Signal: Occurs when either the current or previous candle touches the 200 EMA, and the next candle closes above the previous candle’s close.

Sell Signal: Occurs when either the current or previous candle touches the 200 EMA, and the next candle closes below the previous candle’s close.

✅ 30-Candle Gap Rule:

Prevents frequent entries by ensuring at least 30 candles pass before the next trade.

Improves signal quality and prevents excessive trading.

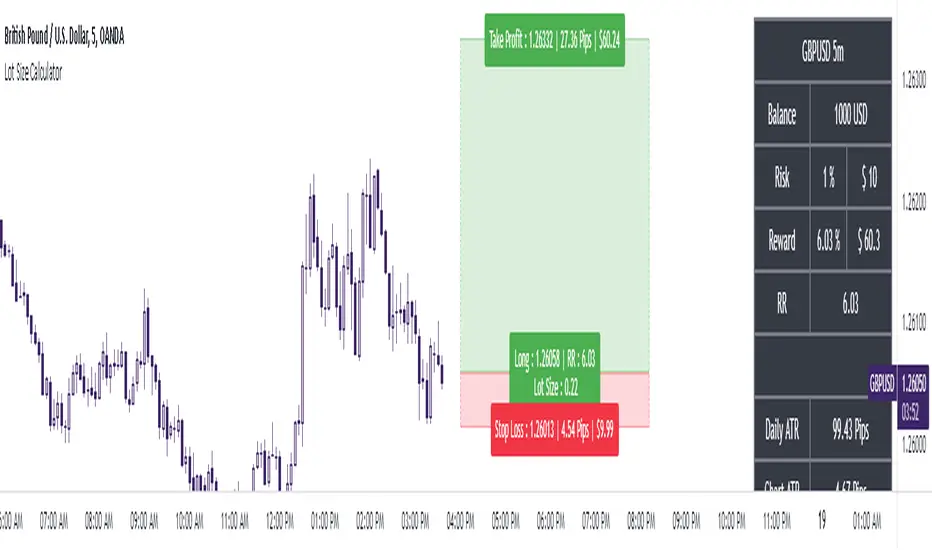

🎯 Target & Stop-Loss Calculation

✅ Buy Position:

Target: 2X the difference between the last candle’s close and the lowest low of the last 2 candles.

Stop Loss: The lowest low of the last 2 candles.

✅ Sell Position:

Target: 2X the difference between the last candle’s close and the highest high of the last 2 candles.

Stop Loss: The highest high of the last 2 candles.

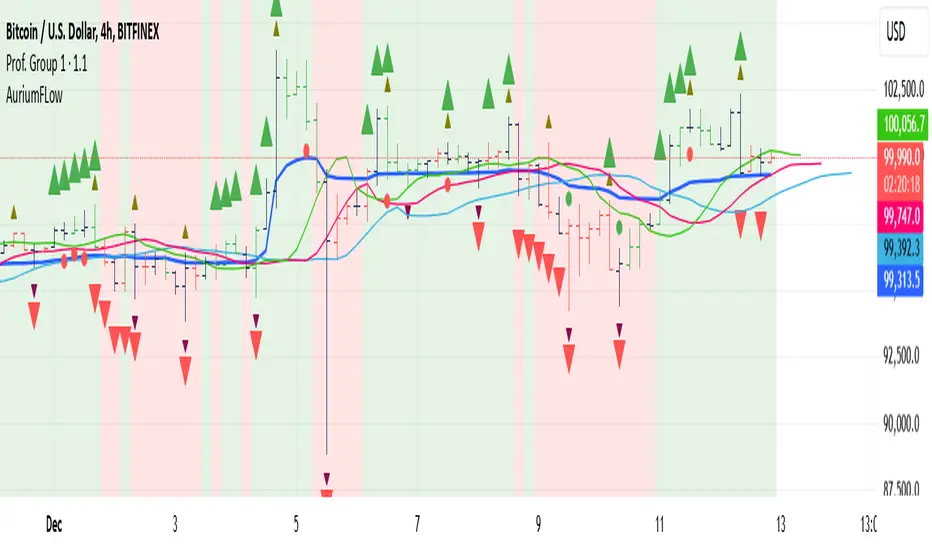

📊 Visual Features

✅ Buy & Sell Signals:

Green Upward Arrow → Buy Signal

Red Downward Arrow → Sell Signal

✅ Target Levels:

Green Dotted Line: Buy Target

Red Dotted Line: Sell Target

✅ Stop Loss Levels:

Dark Red Solid Line: Stop Loss for Buy/Sell

💡 How to Use

🔹 Ideal for trend-following traders using EMAs.

🔹 Works best in volatile & trending markets (avoid sideways ranges).

🔹 Can be combined with RSI, MACD, or price action levels for added confluence.

🔹 Recommended timeframes: 1M, 5M, 15m, 1H, 4H, Daily (for best results).

🚀 Try this strategy and enhance your trading decisions with structured risk management!

อินดิเคเตอร์ Pine Script®