Nq/ES daily CME risk intervalReverse engineering the risk interval for CME (Chicago Mercantile Exchange) products based on margin requirements involves understanding the relationship between margin requirements, volatility, and the risk interval (price movement assumed for margin calculation)

The CME uses a methodology called SPAN (Standard Portfolio Analysis of Risk) to calculate margins. At a high level, the initial margin is derived from:

Initial Margin = Risk Interval × Contract Size × Volatility Adjustment Factor

Where:

Risk Interval: The price movement range used in the margin calculation.

Contract Size: The unit size of the futures contract.

Volatility Adjustment Factor: A measure of how much price fluctuation is expected, often tied to historical volatility.

To calculate an approximate of the daily CME risk interval, we need:

Initial Margin Requirement: Available on the CME Group website or broker platforms.

Contract Size: The size of one futures contract (e.g., for the S&P 500 E-mini, it is $50 × index points).

Volatility Adjustment Factor: This is derived from historical volatility or CME's implied volatility estimates.

As we do not have access to CME calculations , the volatility adjustment factor can be estimated using historical volatility: We calculate the standard deviation of daily returns over a specific period (e.g., 20 or 30 or 60 days).

Key Considerations

The exact formulas and parameters used by CME for CME's implied volatility estimates are proprietary, so this calculation based on standard deviation of daily returns is an approximation.

How to use:

Input the maintenance margin obtained from the CME website.

Adjust volatility period calculation.

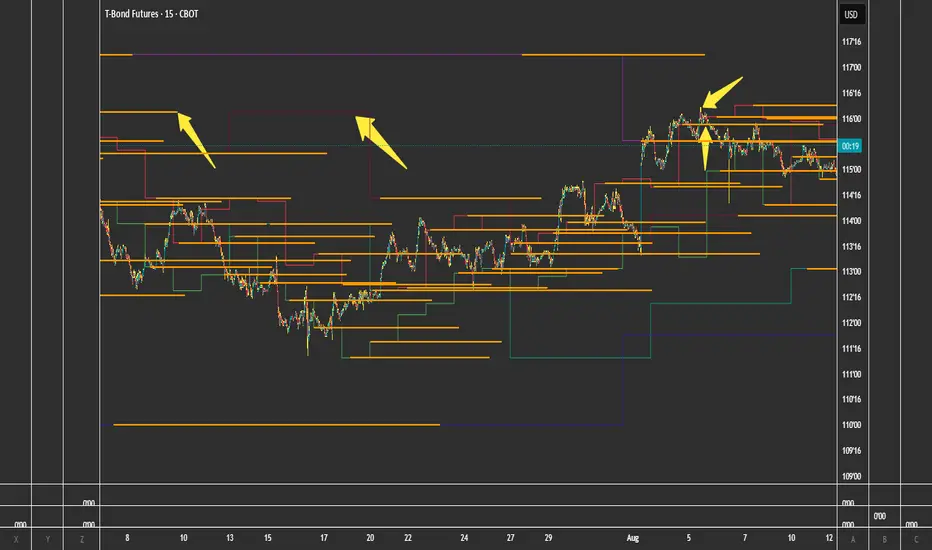

The indicator displays the range high and low for the trading day.

1.Lines can be used as targets intraday

2.Market tends to snap back in between the lines and close the day in the range

ค้นหาในสคริปต์สำหรับ "Futures"

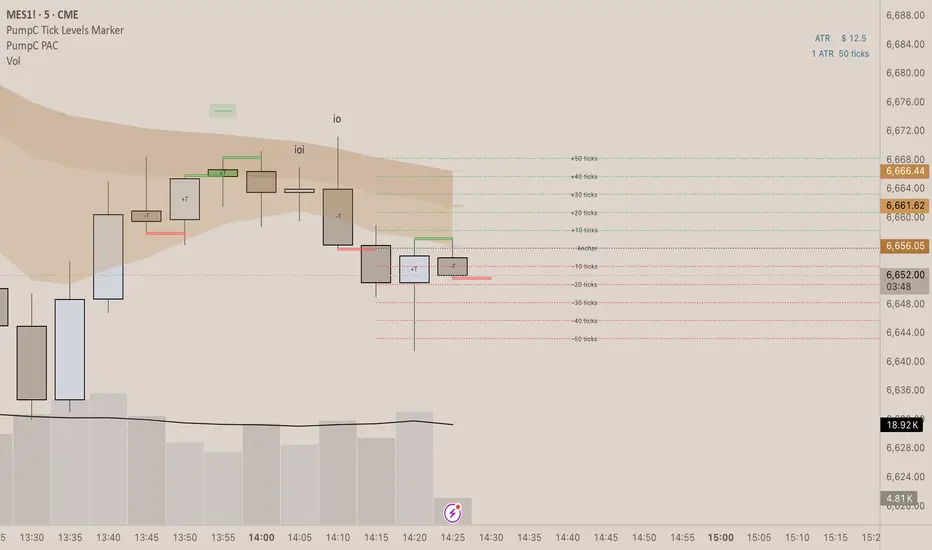

PumpC Tick Levels Marker🧾 Description

PumpC Tick Levels Marker

A precision price-level visualization tool designed for futures and tick-based traders.

Easily mark a single reference price and automatically plot symmetrical tick levels above and below it.

🔍 How It Works

Select your Anchor Price — this acts as the central reference point.

The script automatically plots upward and downward tick levels spaced by your chosen tick multiple.

Labels display tick distance (+/- ticks) and can be offset to the right by a set number of bars for clean alignment near the price scale.

⚙️ Key Features

One-click anchor control — define a single reference price.

Custom tick spacing — choose your tick multiple and number of levels to show (up to 10 in each direction).

Independent Up/Down toggles — display only the levels you need.

Label offset control — move labels closer or farther from the price scale.

Fully customizable styling — line color, width, and style (solid, dashed, dotted).

Efficient cleanup logic — lines and labels refresh dynamically on update.

🧩 Perfect For

Futures and index traders tracking tick increments (e.g., ES, NQ, CL).

Measuring quick scalp targets or ATR-based micro-ranges.

Visualizing equidistant price steps from a key breakout or reversal point.

Created by: PumpC Trading Tools

Version: 1.0 (Pine Script v6)

License: Open for personal use — please credit “PumpC Tick Levels Marker” if reused or modified.

Session Opens by TradeSeekersIt doesn't get much simpler than this indicator for futures traders wanting to track four key session open prices.

Sessions

1. ETH open - extended hours starts

2. Midnight open - new calendar day starts

3. CME open - Chicago exchange opens, data releases

4. RTH open - regular trading hours, volume cometh

Usage

All four of these prices / areas are important for futures traders to pay attention to.

RTH opens far below ETH sometimes will retrace, CME and RTH together can act as a powerful range.

Midnight open sometimes has little importance for the day, but then again it's provided beautiful bounces. Again each level I find to be impactful nearly every session, so I like to keep them close by in an understated manner.

Timezone

If you're not EST, adjust the timezone string accordingly (refer to TradingView docs for string formats).

Proximity Detection

Also, I added proximity detection that aims to keep level collisions from occurring. If a particular session open isn't shown it may be due to being exactly the same price as another open or it's too close to another open.

The proximity sensitivity can be adjusted in settings. The on chart appearance doesn't impact the alerting capability.

Aesthetics

I don't like boring charts so I added a fun "glow" effect, I went with a palette that reminded me of clear sky colors at those times of day (if you're EST).

Alerting

Alerting can be done with just a single alert, first open the indicator config and uncheck any session opens you don't want to be alerted on (why!?), and then use the standard alert menus in TradingView to set the alert on "Any alert() function call".

Why does this beautiful indicator exist?

While there are a handful of indicators that plot open prices with some overlap to this one, I didn't see any that alerted automatically without much fuss.

Free Stock ScreenerMissing great trade opportunities is annoying, and unless you have 12 screens or only trade one market, you are missing a lot of trades. To fix that, we created this free stock screener so you get notified instantly of potential great trading conditions in real time, right on your chart.

You get notified of trading benchmarks being met by the value being displayed on the scanner as well as a color change so that it grabs your attention and makes you aware that you should take a look at the other market and look for a potential trade. It also has built in alerts so you can have an alert notification go off when any of your trading conditions are met instead of needing to watch the scanner for color changes.

The screener will change the ticker symbol background color to red green when price is above or below the previous daily range and above or below both VWAPs. This signals that the ticker is trending, which typically means it is a great time to trade that market and follow the trend.

This free stock screener allows you to scan up to 10 different markets at the same time for various different conditions so you always know what is going on with your favorite trading symbols. If you want to scan more tickers, just add the indicator to your chart again and change the table position to the other side of the screen and update the tickers on the 2nd screener, allowing you to have 20 tickers at a time.

The scanner can be fully customized by changing the markets that it screens and turning on or off as many of them as you would like. You can also turn on or off any of the different data sets so that you only get information about trading conditions that matter to you.

The screener can provide data on any type of market, such as stocks, crypto, futures, forex and more. Each ticker can be adjusted to whatever market you would like it to scan for data in the settings panel, the only limitation is that it will not provide data for the VWAP and volume trend score if the ticker you are screening does not provide volume data.

Screener Features

The scanner will provide the following types of data for each ticker that is turned on:

Volume - Provides a volume score compared to the average volume and notifies you of higher than normal volume and volume spikes on individual bars by changing colors.

Volatility - Provides a volatility score compared to the average volatility and notifies you of higher than normal volatility by changing colors.

Oscillator - Choose between the RSI or CCI. The value of that oscillator will be displayed and will notify you when values are in extreme ranges such as overbought or oversold conditions according to the threshold values you enter in the settings panel. When those thresholds have been breached, you will be notified by it changing color.

Big Candles - Compares the current candle to average previous candle sizes, and changes color to notify you of big candles including a big top wick, big bottom wick, big candle body and big candle high to low range.

Daily Level Touches & Trends - Calculates and displays various daily candle and intraday open price levels that act as support and resistance. Notifies you when price is touching any of the daily levels that are turned on. The levels you can have on are as follows: previous day high, previous day low or previous day open. It also will notify you when price is touching the current day’s open, NY 930am open, Asia 8pm open, London 2am open and NY midnight 12am open. It will also say “Above” if price is above the previous day’s high or it will say “Below” if price is below the previous day’s low. The color of the cell will also change when a level touch is happening or price is above the previous day high or below the previous day low.

VWAP - Choose from 2 different VWAP lengths, default settings are daily and weekly VWAPs. You will get notified if price touches either of the VWAPs and they will also say “Above” or “Below” if price is currently above or below each VWAP.

How To Use The Screener To Help You Trade

The main purpose of the screener is to scan other markets and notify you of potential good trading opportunities such as price bouncing off of the daily levels or VWAPs. It can also be used to know when price is trending according to the VWAPs and daily levels. Lastly, you can use it to know how the volume and volatility trends are currently which gives you more confidence in taking a trade with this data when volume and volatility are present.

Volume Score

When volume is high, this represents a good time to trade because there are many market participants and price is likely to be volatile while there is high volume which can present a lot of good trade setups for you to take.

The volume score shown on the screener measures the current volume trend compared to previous volume trends and calculates that into a score based on 100 being the same as the previous volume trend. So any value above 100 means it is high volume and any value less than 100 means it is lower volume than normal.

In the settings panel, you can adjust the volume threshold that needs to be met for a volume notification to show up. The default setting is at 120, so you will get notified when the current volume trend score is 120 or higher or you can adjust that threshold value to whatever value you prefer.

It also will notify you when there is a volume spike on the current bar. This is determined by calculating an average of the recent volume totals and then checking to see if the current bar is greater than or equal to that average multiplied by 3. So if a single bar has volume that is greater than 3 times what the average volume is, then you will get a notification that says “Spike” to make you aware of that volume spike.

The volume trend threshold, volume spike multiplier and lookback length for the average volume used in volume spike calculations can all be adjusted in the settings panel to fit your desired preferences.

Volatility Score

High volatility can mean it is a great time to trade because the market is moving quickly and providing large enough movements that you can get in and out in a short amount of time, while still accruing decent sized trade PnL.

The volatility score will calculate the current volatility for each market compared to previous conditions and then divide the current volatility by the average volatility to give you a volatility score. Anything over 100 means the market is decently volatile and you should look at that market to find potential trade setups to execute on. Anything below 100 means the market is not very volatile and it is usually best to just wait until volatility returns before you start trading again.

The screener will notify you when the volatility score is above the threshold you set. The default value is set to 90, but can be adjusted to your preference. Pay attention to any market that shows an alert and take a look at that chart because the high volatility may present a good trade setup for you in the near future.

Oscillator Score

The oscillator data can be switched between Relative Strength Index(RSI) and Commodity Channel Index(CCI).

The RSI provides a value between 0 and 100 that indicates the momentum and strength of the recent price action. Many traders use the extremes of the 0-100 range to signal overbought or oversold conditions and use that as a sign to look for price to reverse in the near future. The typical values used for this and the default settings to provide notifications are: 70 for overbought and 30 for oversold. The scanner will notify you when the RSI value is considered overbought or oversold so you know to take a look at the chart and analyze if it is ready for a trade to be taken.

The CCI provides a value that can be used to determine the trend strength of the underlying asset when the oscillator moves above 100 or below -100. These extreme values are outside of the normal accumulation range and signify that price is moving strongly in that direction so it may be a good time to take a trade in the direction of the trend. The scanner will show you the value of the CCI for each market and notify you if that value is above 100 or below -100.

Both RSI and CCI settings can be adjusted in the settings panel to your desired settings so you have the exact oscillator settings you prefer to use as well as the exact values that you want to use for being notified.

Big Candles

Big candles can mean that many traders are buying or selling at the same time and many times indicate a good signal to trade in that same direction. That is why we included this calculation in the screener, so you are always aware when a large candle prints.

It calculates the average size of the recent candles and then uses that average as the benchmark to determine if the current candle is considered big and worthy of notifying you to take a look at that chart.

You can adjust the multiplier used for the big candle threshold to whatever you desire, but the default setting is 3 which means the candle will be considered big and notify you if it is 3 times as large as an average candle.

The big candles data will track the following candle values and notify you with these labels:

High to Low candle size = HL

Candle Body from open to close candle size = OC

Top Wick size = TW

Bottom Wick size = BW

Daily Level Touches & Trend

Daily level touches are excellent levels to watch for price to bounce because they often act as support and resistance levels for intraday trading. The scanner will track each market and notify you when the current candle is touching any of the daily levels that you have turned on in the settings panel.

The main levels that are turned on by default and are useful for all markets and how they will be labeled on the scanner are as follows:

Previous Day High = High

Previous Day Low = Low

Previous Day Open = < Open

Previous Day Close = Close

Current Day Open = Open

We also included some extra levels that are useful for futures traders. They are as follows:

NY 930am Open = 930am

NY 12am Midnight Open = 12am

Asia Open at 8pm NY time = Asia

London Open at 2am NY Time = London

Watch how price reacts to these levels and then trade the bounces off of these levels if the price action confirms that it is going to respect that level.

When price is currently above the previous day high, the scanner will say “Above” and show a green color, indicating a bullish trend and that price is above the previous daily candle’s high.

When price is currently below the previous day low, the scanner will say “Below” and show a red color, indicating a bearish trend and that price is below the previous daily candle’s low.

Pay attention to when price is trending above or below the previous daily candle as those trends can provide excellent trend trading opportunities.

The daily levels that you have turned on in the settings will also show as lines on the chart and include a label next to them, identifying each level so you know what each line represents. You can turn on or off all of the lines shown on the chart in the main settings or turn them off one by one in the style panel of the settings. Labels can also be turned on or off for all of the lines in the main settings panel. You can adjust the label positioning in the Label Offset section of the settings panel.

VWAP Touches & Trend

VWAP stands for volume weighted average price and is a very popular tool that traders use to determine trend direction based on volume as well as an excellent level to trade price bounces off of.

The typical VWAP time period used is Daily, which means the volume weighted average price will reset at the beginning of a new day. We set the first VWAP to be the daily VWAP by default and the second one to be the weekly VWAP. You can adjust both of the time periods to be any of the provided time lengths that you choose.

The screener will show “Above” with a green background color when price is above the VWAP, indicating a bullish trend. It will show “Below” with a red background color when price is below the VWAP, indicating a bearish trend. When both VWAPs are showing Above or Below, you can expect price to trend in that direction, so look for pullbacks you can trade in the direction of the trend. If the VWAPs are showing different directions, then you should expect to bounce back and forth between the VWAPs, but be careful and watch out for price to break beyond either one and start a trend.

When the current candle is touching the VWAP, the scanner will change colors and say VWAP to notify you that price is touching the VWAP and you should look at that chart and analyze the market for a potential bounce off of the VWAP to trade.

Trending Market Signals

Strong trends are excellent markets to trade and can many times provide excellent trading opportunities that don’t require expert price action reading skills to be able to take winning trades from. That is why we included a signal to notify you of a strong trending market.

The strong trending market will show up as a green or red background color for the ticker name. If the color of the ticker name is green, it is notifying you that the price is above the previous daily high, above VWAP 1 and above VWAP 2 and is a good market to look for bullish trend trades. If the color of the ticker name is red, it is notifying you that the price is below the previous daily low, below VWAP 1 and below VWAP 2 and is a good market to look for bearish trend trades.

Changing The Tickers It Scans

To change the tickers that the indicator scans, scroll near the bottom of the settings panel and select the ticker symbol you want to update and then search for the exact symbol you want to use. If you want to scan less tickers, then just turn some of the tickers off that you don’t need.

Scanning More Than 10 Tickers

If you want to scan more than 10 tickers, you can add the scanner to your chart again and then just change the table position to the other side of the screen. This will allow you to scan 10 more tickers that will show up separately. Then if you want even more, just add the indicator to your chart again and update the table position until you have as many markets as you want. The table position setting can be found at the bottom of the main settings panel.

Alerts

The screener has alerts that can be used to notify you when any of the data set thresholds have been met or if price is touching one of the levels. You can set alerts for the following events:

Bullish Trend Alert - Price is above the previous daily high and above both VWAPs.

Bearish Trend Alert - Price is below the previous daily low and below both VWAPs.

High Volume Alert - Volume is higher than the threshold or a volume spike is detected.

High Volatility Alert - Volatility is higher than the threshold.

Oscillator Is Extended Alert - Oscillator value has exceeded the upper or lower threshold.

Big Candle Alert - A big candle has been detected.

Daily Level Touch Alert - One of the daily levels that is turned on is being touched.

VWAP Touch Alert - One of the 2 VWAPs are being touched.

An alert will trigger when any one of tickers on your scanner meets the alert conditions, so when you see the alert, you will need to go to your chart and look at the scanner to see which ticker it was and then navigate to that chart to look for potential trade setups.

The alerts will use the exact same settings you have configured in the settings panel to send you alert notifications. With normal settings, this could give you a lot of alerts, so if you only want alerts to fire when abnormal conditions are being met, try setting up a second screener on your chart that has very high threshold values and only has the most important level touches on. Then turn the setting "Do Not Show The Screener On The Chart" to off so the calculations will still run and fire alerts, but won't clog up your charts. This way you can only get alert notifications when major events happen but still have your normal screener settings available on your chart.

Markets This Can Be Used On

This screener uses the price action and volume data so you can use it to scan any type of market you would like as long as the ticker you are scanning has price and volume data feeds. If a market does not have volume data, then it will just show NaN in the volume row and the VWAP rows will not show anything.

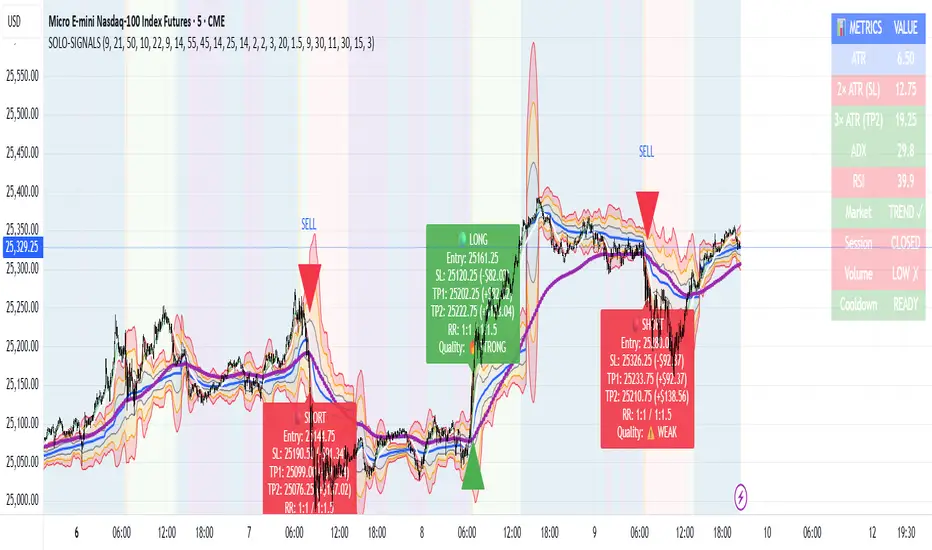

MNQ Morning Indicator | Clean SignalsMNQ Morning Trading Indicator Summary

What It Does

This is a TradingView indicator designed for day trading MNQ (Micro Nasdaq-100 futures) during morning sessions. It generates BUY and SELL signals only when multiple technical conditions align, helping traders identify high-probability trade setups.

Core Strategy

BUY Signal Requirements (All must be true):

✅ Price above VWAP (volume-weighted average price)

✅ Fast EMA (9) above Slow EMA (21) - uptrend confirmation

✅ Price above 15-minute 50 EMA - higher timeframe confirmation

✅ MACD histogram positive - momentum confirmation

✅ RSI above 55 - strength confirmation

✅ ADX above 25 - trending market (not choppy)

✅ Volume 1.5x above average - strong participation

SELL Signal (opposite conditions)

Key Features

🎯 Risk Management

Stop Loss: 2× ATR (Average True Range)

Take Profit 1: 2× ATR (1:2 risk-reward)

Take Profit 2: 3× ATR (1:3 risk-reward)

Dollar values: Calculates P&L based on MNQ's $2/point value

⏰ Session Filter

Default: 9:30 AM - 11:30 AM ET (customizable)

Safety feature: Avoids first 15 minutes (high volatility period)

Won't generate signals outside trading hours

🛡️ Signal Quality

Rates each signal: 🔥 STRONG, ⚡ MEDIUM, or ⚠️ WEAK

Requires minimum 15 bars between signals (prevents overtrading)

📊 Visual Dashboard

Shows real-time metrics:

ATR values

ADX (trend strength)

RSI (momentum)

Market condition (TREND/CHOP)

Session status

Volume status

Signal cooldown timer

Visual Elements

📈 VWAP with standard deviation bands (1σ, 2σ, 3σ)

📉 Multiple EMAs with trend-based coloring

🟢/🔴 Buy/Sell arrows on chart

📋 Detailed trade labels showing entry, SL, TPs, and risk-reward ratios

🎨 Background highlighting for market conditions

Safety Features

Cooldown period between signals

Session restrictions (no trading outside set hours)

First 15-minute avoidance (post-open volatility)

Multi-confirmation requirement (all 7 conditions must align)

Trend filter (ADX minimum to avoid choppy markets)

Best For

Day traders focused on morning sessions

MNQ futures traders

Traders who prefer systematic, rule-based entries

Those wanting pre-calculated risk management levels

Customization

All parameters are adjustable:

EMA periods

MACD settings

RSI thresholds

ADX minimum

ATR multipliers

Session times

Visual preferences

This indicator is designed to be conservative — it waits for strong confirmation before signaling, which means fewer but potentially higher-quality trades.

Session-Conditioned Regime ATRWhy this exists

Classic ATR is great—until the open. The first few bars often inherit overnight gaps and 24-hour noise that have nothing to do with the intraday regime you actually trade. That inflates early ATR, scrambles thresholds, and invites hyper-recency bias (“today is crazy!”) when it’s just the open being the open.

This tool was built to:

Separate session reality from 24h noise. Measure volatility only inside your defined session (e.g., NYSE 09:30–16:00 ET).

Judge candles against the current regime, not the last 2–3 bars. A rolling statistic from the last N completed sessions defines what “typical” means right now.

Label “large” and “small” objectively. Bars are colored only when True Range meaningfully departs from the session regime—no gut feel, no open-bar distortion (gap inclusion optional).

Overview

Purpose: objectively identify unusually big or small candles within the active trading session, compared to the recent session regime.

Use cases: volatility filters, entry/exit confirmation, session bias detection, adaptive sizing.

This indicator replaces generic ATR with a session-conditioned, regime-aware measure. It colors candles only when their True Range (TR) is abnormally large/small versus the last N completed sessions of the same session window.

How it works

Session gating: Only bars inside the selected session are evaluated (presets for NYSE, CME RTH, FX NY; custom supported).

Per-bar TR: TR = max(high, prevRef) − min(low, prevRef).

prevRef is the prior close for in-session bars.

First bar of the session can include the overnight gap (optional; default off).

Regime statistic: For any bar in session k, aggregate all in-session TRs from the previous N completed sessions (k−N … k−1), then compute Median (default) or Mean.

Today’s anchor: Running statistic from today’s session start → current bar (for context and the on-chart ratio).

Color logic:

Big if TR ≥ bigMult × RegimeStat

Small if TR ≤ smallMult × RegimeStat

Colored states: big bull, big bear, small bull, small bear.

Non-triggering bars retain the chart’s native colors.

Panel (top-right by default)

Regime ATR (Nd): session-conditioned statistic over the past N completed sessions.

Today ATR (anchored): running statistic for the current session.

Ratio (Today/Regime): intraday volatility vs regime.

Sample size n: number of bars used in the regime calculation.

Inputs

Session Preset: NYSE (09:30–16:00 ET), CME RTH (08:30–15:00 CT), FX NY (08:00–17:00 ET), Custom (session + IANA timezone).

Regime Window: number of completed sessions (default 5).

Statistic: Median (robust) or Mean.

Include Open Gap: include overnight gap in the first in-session bar’s TR (default off).

Big/Small thresholds: multipliers relative to RegimeStat (defaults: Big=1.5×, Small=0.67×).

Colors: four independent colors for big/small × bull/bear.

Panel position & text size.

Hidden outputs: expose RegimeStat, TodayStat, Ratio, and Z-score to other scripts.

Alerts

RegimeATR: BIG bar — triggers when a bar meets the “Big” condition.

RegimeATR: SMALL bar — triggers when a bar meets the “Small” condition.

Hidden outputs (for strategies/screeners)

RegimeATR_stat, TodayATR_stat, Today_vs_Regime_Ratio, BarTR_Zscore.

Notes & limitations

No look-ahead: calculations only use information available up to that bar. Historical colors reflect what would have been known then.

Warm-up: colors begin once there are at least N completed sessions; before that, regime is undefined by design.

Changing inputs (session window, multipliers, median/mean, gap toggle) recomputes the full series using the same rolling regime logic per bar.

Designed for standard candles. Styling respects existing chart colors when no condition triggers.

Practical tips

For a broader or tighter notion of “unusual,” adjust Big/Small multipliers.

Prefer Median in markets prone to outliers; use Mean if you want Z-score alignment with the panel’s regime mean/std.

Use the Ratio readout to spot compression/expansion days quickly (e.g., <0.7× = compressed session, >1.3× = expanded).

Roadmap

More session presets:

24h continuous (crypto, index CFDs).

23h/Globex futures (CME ETH with a 60-minute maintenance break).

Regional equities (LSE, Xetra, TSE), Asia/Europe/NY overlaps for FX.

Half-day/holiday templates and dynamic calendars.

Multi-regime comparison: track multiple overlapping regimes (e.g., RTH vs ETH for futures) and show separate stats/ratios.

Robust stats options: trimmed mean, MAD/Huber alternatives; optional percentile thresholds instead of fixed multipliers.

Subpanel visuals: rolling TodayATR and Ratio plots; optional Z-score ribbon.

Screener/strategy hooks: export boolean series for BIG/SMALL, plus a lightweight strategy template for backtesting entries/exits conditioned on regime volatility.

Performance/QOL: per-symbol presets, smarter warm-up, and finer control over sample caps for ultra-low TF charts.

Changelog

v0.9b (Beta)

Session presets (NYSE/CME RTH/FX NY/Custom) with timezone handling.

Panel enhancements: ratio + sample size n.

Four-state bar coloring (big/small × bull/bear).

Alerts for BIG/SMALL bars.

Hidden Z-score stream for downstream use.

Gap-in-TR toggle for the first in-session bar.

Disclaimer

For educational purposes only. Not investment advice. Validate thresholds and session settings across symbols/timeframes before live use.

Crypto Exchange PremiumDescription: Crypto Exchange Premium

The Crypto Exchange Premium indicator is designed to quantify and visualize price disparities between different types of crypto markets — specifically between spot and perpetual futures markets, or between any two customizable sources of price data. By consolidating live data from multiple major exchanges, it creates a unified, cross-market measure of premium (or discount), helping traders identify institutional activity (i. e. by comparing exchanges with high institutional activity against others), arbitrage opportunities, and shifts in market sentiment before they become visible in price action alone.

Concept and Purpose

In cryptocurrency markets, price divergence between spot and perpetual pairs reflects the real-time interaction of demand and liquidity across market segments.

When perpetual prices trade above spot, it implies aggressive long positioning or bullish leverage (positive funding expectations).

Conversely, when spot trades above perps, it may reflect net selling pressure in futures or strong spot accumulation.

Unlike most tools that rely on funding rates or open interest alone, this indicator measures the actual traded price spread dynamically across exchanges. This allows traders to visualize the “premium curve” of the crypto market in a clear, data-driven format.

How It Works

The indicator aggregates real-time prices from a wide selection of exchanges, normalizes them into groups, and computes the difference (“premium”) between two chosen reference markets.

1. Exchange Aggregation:

Users can toggle individual exchanges for both spot and perpetual aggregation groups.

The script automatically calculates group averages by dividing the sum of all enabled exchange prices by the number of valid feeds.

Non-USD exchanges (e.g., KRW pairs on Upbit or Bithumb) are automatically converted into USD using live FX data (USDKRW) for accurate normalization.

2. Flexible Comparison Logic:

Each leg of the comparison (First vs. Second Source) can be chosen as one of:

Local chart symbol

Custom symbol

Aggregated Spot group

Aggregated Perpetual group

This allows users to compare, for example:

Binance Spot vs. Global Perp Average

Coinbase Spot vs. Binance Perp

BTCUSD vs. BTCUSDT.P (or any cross-exchange combination)

3. Premium Calculation:

The final value is computed as:

Premium = First Source Price − Second Source Price

and is plotted as a histogram (positive = green, negative = red). This visual instantly shows whether the first source trades at a premium or discount relative to the second.

How to Use

Select Data Sources:

Configure the “First Symbol” and “Second Symbol” in the settings. For most use cases:

First Symbol → Perps (Aggregated)

Second Symbol → Spot (Aggregated)

Adjust Exchange Selection:

Enable or disable individual exchanges to fine-tune your data set. For instance, disabling Korean exchanges filters out regional FX distortions.

Originality and Value

While many exchange difference or “premium indicators” track one or two exchanges, this script introduces multi-exchange aggregation, cross-market normalization, and user-configurable pairing, resulting in a more holistic and accurate reflection of market structure.

It bridges a gap between macro market breadth and microstructural price dynamics, empowering traders to:

Detect arbitrage inefficiencies between spot and perps.

Track regional price dislocations (USD vs. KRW).

Gauge the intensity of speculative leverage over time.

Anticipate funding rate shifts and liquidation clusters before they happen.

ES/NQ Price Action Sync See when ES & NQ move in syncSee when ES & NQ move in sync — revealing real market momentum at a glance.”

⚖️ ES/NQ Price Action Sync

Discover when the market moves as one.

This indicator tracks when S&P 500 Futures (ES1!) and Nasdaq Futures (NQ1!) align in momentum — helping you spot broad-market confirmation or early divergence in real time.

🧠 Concept

The ES/NQ relationship often reveals the market’s underlying strength or hesitation. When both indices turn bullish or bearish together with meaningful movement, that’s a sign of true market alignment.

When they disagree — expect mixed momentum and possible reversals.

⚙️ Features

✅ Highlights new bullish and bearish syncs on chart

✅ Dynamic info table showing % change and direction for each index

✅ Optional triangle markers for clean visual cues

✅ Alert conditions for new sync events

✅ Adjustable lookback and minimum-move filters

💡 How to Use

Use this as a market-context tool, not a direct buy/sell signal.

When both indices sync, intraday trends often hold better; when they diverge, momentum may fade.

Combine it with your own system or higher-time-frame analysis for confirmation.

📊 Why Traders Love It

Simple idea — powerful insight.

This tool helps traders instantly see when “the market machine” is running in harmony… or pulling in opposite directions.

⚠️ Disclaimer:

This script is for educational and analytical purposes only.

It does not provide financial advice or trading signals. Always perform your own research before making trading decisions.

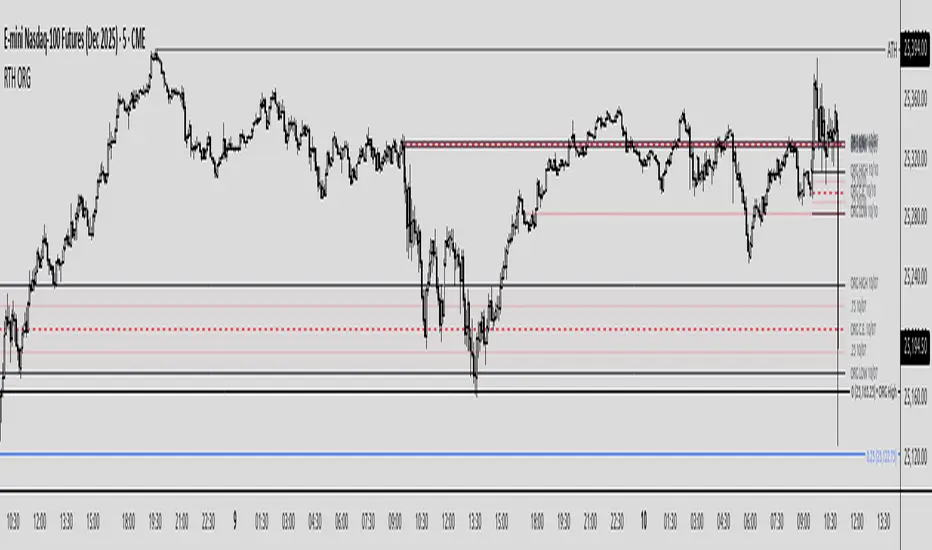

Regular Trading Hours Opening Range Gap (RTH ORG)### Regular Trading Hours (RTH) Gap Indicator with Quartile Levels

**Overview**

Discover overnight gaps in index futures like ES, YM, and NQ, or stocks like SPY, with this enhanced Pine Script v6 indicator. It visualizes the critical gap between the previous RTH close (4:15 PM ET for futures, 4:00 PM for SPY) and the next RTH open (9:30 AM ET), helping traders spot potential price sensitivity formed during after-hours trading.

**Key Features**

- **Standard Gap Boxes**: Semi-transparent boxes highlight the gap range, with optional text labels showing day-of-week and "RTH" identifier.

- **Midpoint Line**: A customizable dashed line at the 50% level, with price labels for quick reference.

- **New: Quartile Lines (25% & 75%)**: Dotted lines (default width 1) mark the quarter and three-quarter points within the gap, ideal for finer intraday analysis. Toggle on/off, adjust style/color/width, and add labels.

- **High-Low Gap Variant**: Optional boxes and midlines for gaps between the prior close's high/low and the open's high/low—perfect for wick-based overlaps on lower timeframes (5-min or below recommended).

- **RTH Close Lines**: Extend previous close levels with dotted lines and price tags.

- **Customization Galore**: Extend elements right, limit historical displays (default: 3 gaps), no-plot sessions (e.g., avoid weekends), and time offsets for non-US indices.

**How to Use**

Apply to 15-min or lower charts for best results. Toggle "extend right" for ongoing levels. SPY auto-adjusts for its 4 PM close.

Tested on major indices—enhance your gap trading strategy today! Questions? Drop a comment.

Thanks to twingall for supplying the original code.

Thanks to The Inner Circle Trader (ICT) for the logical and systematic application.

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Volume weighted Forex Overwiew True Strenght IndexAdding volume weighting to the FOTSI strategy improves its effectiveness by making the indicator more sensitive to periods of high market activity. Here’s how:

Market Relevance: Futures volume reflects institutional and large trader participation. When volume is high, price moves are more likely to be meaningful and less likely to be noise.

Dynamic Weighting: By multiplying each currency’s momentum by its normalized futures volume, the indicator gives more weight to currencies that are actively traded at that moment, making signals more robust.

Filtering Out Noise: Low-volume periods are down-weighted, reducing the impact of illiquid or less relevant price changes.

Better Timing: Signals generated during high-volume periods are more likely to coincide with real market moves, improving entry and exit timing.

Multi-TF 👀### Multi-Timeframe Analysis (MTF-Analysis)

**Overview**

The Multi-Timeframe Analysis indicator is a powerful visualization tool designed for traders who incorporate multi-timeframe (MTF) strategies into their decision-making process. It overlays compact, customizable candle representations from up to four higher timeframes directly on your chart, positioned to the right of the last bar for quick reference. This allows you to monitor price action, momentum via EMAs, and key levels like Fair Value Gaps (FVGs) across multiple resolutions without switching charts. Built with efficiency in mind, it supports automatic timeframe detection, real-time updates, and a clean, non-intrusive design that enhances your trading workflow.

Ideal for day traders, swing traders, and scalpers, this indicator helps identify alignments between timeframes, spot potential reversals or continuations, and validate entries/exits based on higher-timeframe context. It leverages Pine Script v6 for smooth performance, with optimizations to handle up to 5000 bars back and extensive drawing limits.

**Key Features**

- **Multi-Timeframe Candle Display**: Renders recent candles (configurable from 5 to 100 per timeframe) from selected higher timeframes (e.g., 5m, 15m, 1H, 4H) as compact bars with customizable width, spacing, and padding. Bullish and bearish candles are color-coded for instant recognition.

- **Automatic Timeframe Adaptation**: When enabled, the indicator intelligently selects complementary timeframes based on your chart's resolution (e.g., on a 1m chart, it might show 5m, 15m, and 1H). Manual overrides are available for full control.

- **EMA Overlays**: Plots EMA9, EMA21, and EMA50 on each MTF section using a user-defined source (e.g., OHLC/4, close). EMAs can be dashed for clarity and enabled/disabled per timeframe, helping to gauge momentum and trend strength.

- **Fair Value Gaps (FVGs)**: Detects bullish (+FVG) and bearish (-FVG) gaps with a configurable lookback length (5-50 bars). Gaps are visualized as dotted boxes extending from the candle, highlighting potential support/resistance zones or imbalances.

- **Time Labels and Debugging**: Displays timestamp labels under every fourth candle for chronological context. A debug mode expands spacing and adds detailed labels (e.g., OHLC, volume, EMA values) for testing and verification.

- **Customization Options**: Extensive inputs for colors (bodies, wicks, EMAs, FVGs), label sizes/styles, and layout ensure seamless integration with your chart theme. Supports futures symbols with a time offset adjustment.

- **Performance Optimizations**: Uses arrays for efficient data management, clears drawings on realtime updates or timeframe changes, and limits buffer sizes to prevent overload.

**How to Use**

1. Add the indicator to your chart via TradingView's "Indicators" menu.

2. Configure timeframes: Enable/disable up to four TFs and set the number of candles to display. Use "Auto Timeframe" for smart defaults.

3. Adjust EMAs: Select the source type and toggle per TF to focus on relevant momentum signals (e.g., EMA9 crossovers for short-term trades).

4. Enable FVGs: Activate per TF and tweak the length to suit your market (shorter for volatile assets, longer for trends).

5. Fine-tune appearance: Modify padding, candle width, and colors to avoid clutter. Use debug mode during setup.

6. Interpret: Align your chart's price action with MTF candles—look for confluence in trends, FVGs filling as support/resistance, or EMA alignments for high-probability setups.

**Input Settings**

- **General**: Hour offset for time adjustments (useful for futures).

- **Timeframes**: Enable TFs 1-4, select resolutions (e.g., "5m"), and set candle counts. Auto mode simplifies this.

- **FVG/iFVG**: Toggle per TF, customize colors and detection length.

- **EMA**: Enable per TF, choose source, colors, and dashed style.

- **Candle Appearance**: Bull/bear colors for bodies/wicks, width/spacing/padding, label size/color.

- **Debug**: Expands view for detailed inspection.

**Notes**

- This indicator is non-repainting and updates in realtime, but performance may vary on lower timeframes with many candles—reduce counts if needed.

- FVGs are calculated locally on recent bars for efficiency; historical gaps beyond the buffer aren't shown.

- Compatible with all symbols, but best on volatile markets like forex, crypto, or indices.

- Feedback welcome—updates may include more MA types or advanced FVG filters.

Enhance your edge with multi-timeframe insights—try MTF-Analysis today!

Bar Statistics - DELTA/OI/TOTAL/BUY/SELL/LONGS/SHORTSBar Statistics - Advanced Volume & Open Interest Analysis

Overview

The Bar Statistics indicator is a comprehensive analytical tool designed to provide traders with detailed insights into market microstructure through advanced volume analysis, open interest tracking, and market flow detection. This indicator transforms complex market data into easily digestible visual information, displaying six key metrics in customizable colored boxes that update in real-time.

Unlike traditional volume indicators that only show basic volume data, this indicator combines multiple data sources to reveal the underlying forces driving price movement, including volume delta calculations from lower timeframes, open interest changes, and estimated market positioning.

What Makes This Indicator Unique

1. Multi-Timeframe Volume Delta Precision

The indicator utilizes lower timeframe data (default 1-second) to calculate highly accurate volume delta measurements, providing much more precise buy/sell pressure analysis than standard timeframe-based calculations. This approach captures intraday volume dynamics that are often missed by conventional indicators.

2. Real-Time Updates

Unlike many indicators that only update on bar completion, this tool provides live updates for the developing candle, allowing traders to see evolving market conditions as they happen.

3. Market Flow Analysis

The unique "L/S" (Long/Short) metric combines open interest changes with price/volume direction to estimate net market positioning, helping identify when participants are accumulating or distributing positions.

4. Adaptive Visual Intensity

The gradient color system automatically adjusts based on historical context, making it easy to identify when current values are significant relative to recent market activity.

5. Complete Customization

Every aspect of the display can be customized, from the order of metrics to individual color schemes, allowing traders to adapt the tool to their specific analysis needs.

6.All In One Solution

6 Metrics in one indicator no more using 5 different indicators.

Core Features Explained

DELTA (Volume Delta)

What it shows: Net difference between aggressive buy volume and aggressive sell volume

Calculation: Uses lower timeframe data to determine whether each trade was initiated by buyers or sellers

Interpretation:

Positive values indicate aggressive buying pressure

Negative values indicate aggressive selling pressure

Magnitude indicates the strength of directional pressure

OI Δ (Open Interest Change)

What it shows: Change in open interest from the previous bar

Data source: Fetches open interest data using the "_OI" symbol suffix

Interpretation:

Positive values indicate new positions entering the market

Negative values indicate positions being closed

Combined with price direction, reveals market participant behavior

L/S (Net Long/Short Bias)

What it shows: Estimated net change in long vs short market positions

Calculation method: Combines open interest changes with price/volume direction using configurable logic

Scenarios analyzed:

New Longs: Rising OI + Rising Price/Volume = Long position accumulation

Liquidated Longs: Falling OI + Falling Price/Volume = Long position exits

New Shorts: Rising OI + Falling Price/Volume = Short position accumulation

Covered Shorts: Falling OI + Rising Price/Volume = Short position exits

Result: Net bias toward long (positive) or short (negative) market sentiment

TOTAL (Total Volume)

What it shows: Standard volume for the current bar

Purpose: Provides context for other metrics and baseline activity measurement

Enhanced display: Uses gradient intensity based on recent volume history

BUY (Estimated Buy Volume)

What it shows: Estimated aggressive buy volume

Calculation: (Total Volume + Delta) / 2

Use case: Helps quantify the actual buying pressure in monetary/contract terms

SELL (Estimated Sell Volume)

What it shows: Estimated aggressive sell volume

Calculation: (Total Volume - Delta) / 2

Use case: Helps quantify the actual selling pressure in monetary/contract terms

Configuration Options

Timeframe Settings

Custom Timeframe Toggle: Enable/disable custom lower timeframe selection

Timeframe Selection: Choose the precision level for volume delta calculations

Auto-Selection Logic: Automatically selects optimal timeframe based on chart timeframe

Net Positions Calculation

Direction Method: Choose between Price-based or Volume Delta-based direction determination

Value Method: Select between Open Interest Change or Volume for position size calculations

Display Customization

Row Order: Completely customize which metrics appear and in what order (6 positions available)

Color Schemes: Individual color selection for positive/negative values of each metric

Gradient Intensity: Configurable lookback period (10-200 bars) for relative intensity calculations

Visual Elements

Box Format: Clean, professional box display with clear labels

Color Coding: Intuitive color schemes with customizable transparency gradients

Real-time Updates: Live updating for developing candles with historical stability

How to Use This Indicator

For Day Traders

Volume Confirmation: Use DELTA to confirm breakout validity - strong directional moves should show corresponding volume delta

Entry Timing: Watch for volume delta divergences at key levels to time entries

Exit Signals: Monitor when aggressive volume shifts against your position

For Swing Traders

Market Flow: Focus on the L/S metric to identify when participants are accumulating or distributing

Open Interest Analysis: Use OI Δ to confirm whether moves are backed by new money or position adjustments

Trend Validation: Combine multiple metrics to validate trend strength and sustainability

For Scalpers

Real-time Edge: Utilize the live updates to see developing imbalances before bar completion

Quick Decision Making: Focus on DELTA and BUY/SELL for immediate market pressure assessment

Volume Profile: Use TOTAL volume context for optimal entry/exit sizing

Setup Recommendations

Futures Markets: Enable OI tracking and use Volume Delta direction method

Crypto Markets: Focus on DELTA and volume metrics; OI may not be available

Stock Markets: Use Price direction method with volume value calculations

High-Frequency Analysis: Set lower timeframe to 1S for maximum precision

Technical Implementation

Data Accuracy

Utilizes TradingView's ta.requestVolumeDelta() function for precise buy/sell classification

Implements error checking for data availability

Handles missing data gracefully with fallback calculations

Performance Optimization

Efficient array management with configurable lookback periods

Smart box creation and deletion to prevent memory issues

Optimized real-time updates without historical data corruption

Compatibility

Works on all timeframes from seconds to daily

Compatible with futures, forex, crypto, and stock markets

Automatically adjusts calculation methods based on available data

Risk Disclaimers

This indicator is designed for educational and analytical purposes. It provides statistical analysis of market data but does not guarantee trading success. Users should:

Combine with other forms of analysis

Practice proper risk management

Understand that past performance doesn't predict future results

Be aware that volume delta and open interest data quality varies by market and data provider

Conclusion

The Bar Statistics indicator represents a significant advancement in retail trader access to professional-grade market analysis tools. By combining multiple data sources into a single, customizable display, it provides the depth of analysis needed for comprehensive market microstructure understanding while maintaining the simplicity required for effective decision-making.

EMA / WMA RibbonMomentum Flow Ribbon

Unlock a clear, visual edge in identifying short-term momentum shifts with the Momentum Flow Ribbon.

This indicator was born from a simple yet powerful concept: to visually represent the dynamic relationship between a fast-reacting Exponential Moving Average (EMA) and the smoother, more methodical Wilder's Moving Average (WMA). While both moving averages use the same length, their unique calculation methods cause them to separate and cross, creating a "ribbon" that provides an immediate and intuitive gauge of market momentum.

This tool is designed for the disciplined trader who values clean charts and actionable signals, helping you to execute your strategies with greater confidence and precision.

How It Works

The script plots an EMA and a Wilder's Moving Average (referred to as rma in Pine Script) of the same length. The space between these two lines is then filled with a colored ribbon:

Bullish Green/Teal: The ribbon turns bullish when the faster EMA crosses above the slower Wilder's MA, indicating that short-term momentum is strengthening to the upside.

Bearish Red: The ribbon turns bearish when the EMA crosses below the Wilder's MA, signaling that short-term momentum is shifting to the downside.

The inherent "lag" of the Wilder's MA, a feature designed by J. Welles Wilder Jr. himself, acts as a steady baseline against which the more sensitive EMA can be measured. The result is a simple, zero-lag visual that filters out insignificant noise and highlights meaningful changes in trend direction.

Key Features

Customizable Length and Source: Easily adjust the moving average length and price source (close, hl2, etc.) to fit your specific trading style and the instrument you are trading, from futures like MES and MNQ to cryptocurrencies and forex.

Customizable Colors: Tailor the ribbon's bullish and bearish colors to match your personal chart aesthetic.

Built-in Alerts: The script includes pre-configured alerts for both bullish (EMA crosses above WMA) and bearish (EMA crosses below WMA) signals. Never miss a potential momentum shift again.

Clean & Lightweight: No clutter. Just a simple, effective ribbon that integrates seamlessly into any trading system.

Practical Application for the Discerning Trader

For a futures trader, timing is everything. This ribbon is not just another indicator; it's a tool for confirmation.

Imagine you've identified a key level—a Volume Profile POC, the previous day's low, or a critical accumulation zone. As price approaches this level pre-London session, you're watching for a sign of institutional activity. A flip in the ribbon's color at that precise moment can provide the powerful confirmation you need to enter a trade, trusting that you are aligning with the building liquidity and momentum heading into the New York open.

This is a tool for those who aspire to greatness in their trading—who understand that the edge is found not in complexity, but in the flawless execution of a simple, well-defined plan.

Add the Momentum Flow Ribbon to your chart and start seeing momentum in a clearer light.

Open Interest OverlayOpen Interest Overlay

Overview

This indicator displays Open Interest (OI) data directly on your price chart as an overlay, eliminating the need for separate panes while preserving authentic OI movement patterns. Perfect for traders who want to analyze OI correlations without sacrificing chart real estate.

Key Features

📊 Smart Price Scaling

• Automatically maps Open Interest values to fit within your chart's price range

• Preserves all directional movements, timing, and relative magnitude relationships

• Uses official TradingView Open Interest feed for accuracy

🎨 Full Customization

• Custom Colors: Choose your own colors for rising/falling OI (defaults: teal/red)

• Line Style: Toggle between step-line (traditional) or smooth line display

• Optional Fill: Shade area between OI line and mid-price for better visual reference

• Smoothing Options: Apply moving average smoothing to reduce noise

⚙️ Intelligent Settings

• Normalization Window: 300-bar lookback (customizable) for scaling calculations

• Auto Timeframe: Uses daily data for intraday charts on traditional assets, chart timeframe for crypto

• Real Value Display: Shows actual (unscaled) OI value on the last bar

How It Works

The indicator performs proportional mapping of Open Interest data:

1. Calculates OI range (high/low) over the lookback period

2. Maps this range to your chart's price range during the same period

3. Displays OI movements that maintain authentic patterns and timing

Perfect For

✅ Correlation Analysis - See how OI moves with price in real-time

✅ Divergence Spotting - Identify when OI and price trends diverge

✅ Clean Charts - No need for separate panes or window splitting

✅ Pattern Recognition - Spot OI building/declining during key price levels

✅ Cross-Market Analysis - View any symbol's OI overlay on your current chart (e.g., Bitcoin OI while viewing Ethereum prices)

What You Get vs Traditional OI Indicators

Advantages:

• Authentic OI movement patterns preserved

• Direct visual correlation with price action

• No chart real estate sacrifice

• Immediate trend and divergence recognition

Trade-offs:

• Shows relative OI changes rather than absolute values

• Scaling is relative to the selected lookback period

Ideal For

• Day traders monitoring intraday OI flow

• Swing traders analyzing OI trends with price movements

• Futures traders tracking institutional interest

• Anyone wanting clean, correlation-focused OI analysis

Compatible With

• Futures contracts with Open Interest data

• Any timeframe (auto-adjusts for optimal data)

• All TradingView-supported OI symbols

Funding Rate Aggregated (Lite)Funding Rate Aggregated (Lite) provides traders with a consolidated view of perpetual futures funding rates across multiple major exchanges. Instead of monitoring each market individually, the script aggregates the available data into a single, average funding rate series—streamlining analysis and helping identify market-wide positioning imbalances.

The indicator supports Binance, Bybit, OKX, Bitget, and Coinbase, with user-controlled toggles to enable or disable specific venues. For exchanges offering multiple quote currencies (e.g., USDT, USD, or USDC pairs) inclusion is based on whether their trading activity (volume) is relevant (determined manually, not via code). Each available rate is checked and included in the calculation only if valid, ensuring the average reflects actual market conditions.

From a technical standpoint, the script:

Retrieves real-time funding rate data directly via request.security for the current symbol’s base currency.

Applies standard formatting similar to TradingView's official indicator.

Visualizes the average funding rate with color-coded plotting (green for positive, red for negative), alongside a neutral zero reference line.

Why it is useful:

Funding rates are a direct measure of long/short market bias in perpetual swaps. Persistently high positive rates often indicate overcrowded longs, while negative rates can reveal excessive shorting.

By combining multiple exchanges into one metric, traders gain a more robust signal, reducing noise from isolated exchange-specific anomalies.

This aggregated perspective can assist in timing contrarian trades, spotting funding-driven inefficiencies, and gauging overall market sentiment.

Applications in trading include:

Sentiment analysis: Assess whether perpetual futures traders are leaning heavily long or short.

Cross-exchange confirmation: Ensure that extreme funding isn’t confined to a single venue.

Risk management: Identify periods of elevated funding costs that may erode profitability in longer-term positions.

Strategy filters: Integrate the aggregated rate as a condition for entries/exits, or to adjust position sizing during extremes.

The Lite designation emphasizes simplicity and efficiency: the indicator avoids unnecessary visual and data-driven clutter and focuses on delivering one clear, aggregated signal that can be adapted to a wide range of trading styles.

Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

Cumulative Volume Delta Candles Aggregated (Lite)Cumulative Volume Delta Candles Aggregated (Lite)

Multi-Exchange CVD Visualization in Candle Format

This indicator provides an aggregated Cumulative Volume Delta (CVD) view across multiple major perpetual futures exchanges in one chart. It is designed for traders who want a broader perspective on buying and selling pressure without switching between multiple charts or relying on a single exchange feed.

What It Does

Combines volume delta data from Binance, Bybit, OKX, Bitget, and Coinbase into a unified representation.

Displays CVD as candlesticks, where each candle reflects the open, high, low, and close of cumulative delta for the selected period.

Offers a clear visual of how buying and selling pressure evolves across markets in a structured, familiar candle format.

Key Features

✔ Exchange Aggregation: Incorporates data from several top futures markets available on TradingView.

✔ Anchor Reset: Allows you to set an anchor timeframe (e.g., daily) to reset cumulative values for better readability and analysis.

✔ Unit Normalization: Since exchanges report volumes in different units, the indicator normalizes all data and outputs values denominated in the base currency (coins) for consistency.

✔ Hidden OHLC Outputs: Provides open, high, low, and close values as hidden plots for use with other indicators or strategies.

✔ Lightweight Design: Optimized for efficiency while handling multiple real-time data requests.

Why It’s Different

Unlike standard single-exchange CVD tools, this indicator aggregates the majority of perpetual volume data available on TradingView, offering a more representative view of market sentiment. The candle-based representation of CVD introduces an additional layer of structure, helping traders identify shifts in momentum and pressure with more context than a simple cumulative line.

Use Cases

- Spotting aggregated buy/sell pressure trends across multiple exchanges.

- Confirming breakout or reversal signals with broader volume delta context.

- Serving as a custom data source for other indicators or algorithmic strategies.

ForecastForecast (FC), indicator documentation

Type: Study, not a strategy

Primary timeframe: 1D chart, most plots and the on-chart table only render on daily bars

Inspiration: Robert Carver’s “forecast” concept from Advanced Futures Trading Strategies, using normalized, capped signals for comparability across markets

⸻

What the indicator does

FC builds a volatility-normalized momentum forecast for a chosen symbol, optionally versus a benchmark. It combines an EWMAC composite with a channel breakout composite, then caps the result to a common scale. You can run it in three data modes:

• Absolute: Forecast of the selected symbol

• Relative: Forecast of the ratio symbol / benchmark

• Combined: Average of Absolute and Relative

A compact table can summarize the current forecast, short-term direction on the forecast EMAs, correlation versus the benchmark, and ATR-scaled distances to common price EMAs.

⸻

PineScreener, relative-strength screening

This indicator is excellent for screening on relative strength in PineScreener, since the forecast is volatility-normalized and capped on a common scale.

Available PineScreener columns

PineScreener reads the plotted series. You will see at least these columns:

• FC, the capped forecast

• from EMA20, (price − EMA20) / ATR in ATR multiples

• from EMA50, (price − EMA50) / ATR in ATR multiples

• ATR, ATR as a percent of price

• Corr, weekly correlation with the chosen benchmark

Relative mode and Combined mode are recommended for cross-sectional screens. In Relative mode the calculation uses symbol / benchmark, so ensure the ratio ticker exists for your data source.

⸻

How it works, step by step

1. Volatility model

Compute exponentially weighted mean and variance of daily percent returns on D, annualize, optionally blend with a long lookback using 10y %, then convert to a price-scaled sigma.

2. EWMAC momentum, three legs

Daily legs: EMA(8) − EMA(32), EMA(16) − EMA(64), EMA(32) − EMA(128).

Divide by price-scaled sigma, multiply by leg scalars, cap to Cap = 20, average, then apply a small FDM factor.

3. Breakout momentum, three channels

Smoothed position inside 40, 80, and 160 day channels, each scaled, then averaged.

4. Composite forecast

Average the EWMAC composite and the breakout composite, then cap to ±20.

Relative mode runs the same logic on symbol / benchmark.

Combined mode averages Absolute and Relative composites.

5. Weekly correlation

Pearson correlation between weekly closes of the asset and the benchmark over a user-set length.

6. Direction overlay

Two EMAs on the forecast series plus optional green or red background by sign, and optional horizontal level shading around 0, ±5, ±10, ±15, ±20.

⸻

Plots

• FC, capped forecast on the daily chart

• 8-32 Abs, 8-32 Rel, single-leg EWMAC plus breakout view

• 8-32-128 Abs, 8-32-128 Rel, three-leg composite views

• from EMA20, from EMA50, (price − EMA) / ATR

• ATR, ATR as a percent of price

• Corr, weekly correlation with the benchmark

• Forecast EMA1 and EMA2, EMAs of the forecast with an optional fill

• Backgrounds and guide lines, optional sign-based background, optional 0, ±5, ±10, ±15, ±20 guides

Most plots and the table are gated by timeframe.isdaily. Set the chart to 1D to see them.

⸻

Inputs

Symbol selection

• Absolute, Relative, Combined

• Vs. benchmark for Relative mode and correlation, choices: SPY, QQQ, XLE, GLD

• Ticker or Freeform, for Freeform use full TradingView notation, for example NASDAQ:AAPL

Engine selection