TRIZONACCI_Mean reversal_signalsMarket State Engine

Deterministic Confidence-Scoring System for TradingView

A professional-grade PineScript v5 indicator that scores market conditions from 0-100, helping traders identify high-quality trading opportunities through systematic structure analysis, VWAP positioning, order flow dynamics, and time-based context.

🎯 Overview

The Market State Engine is not a trading bot—it's a noise-reduction and opportunity-ranking system designed to filter market conditions and surface only the highest-quality setups.

Instead of blindly taking every signal, this indicator:

✅ Scores market conditions objectively (0-100 scale)

✅ Filters out low-probability setups automatically

✅ Classifies opportunities into A, A+, and A++ grades

✅ Alerts only on confirmed structure shifts with supporting context

✅ Keeps the human in control - provides intelligence, not automation

Philosophy: Reduce Noise. Enforce Discipline. Surface Quality.

🚀 Key Features

Deterministic Scoring - No black boxes, fully explainable logic

Multi-Factor Analysis - Combines 4 independent market state components

Structure-First Approach - Only alerts on confirmed pivot breaks

VWAP Mean Reversion Logic - Directional filtering based on VWAP zones

Order Flow Proxy - CVD divergence and confirmation detection

Session-Aware Scoring - Prioritizes high-volume New York sessions

Alert De-Duplication - One alert per unique structure shift

Zero Repainting - Uses confirmed pivots only (left=2, right=2)

Fully Configurable - All parameters exposed as inputs

Visual Feedback - VWAP bands, setup labels, and real-time score panel

📊 Scoring System (0-100)

The Market State Engine evaluates four independent components, each contributing up to 25 points for a maximum total score of 100.

🎯 Component Breakdown

Component Max Points Description

VWAP Context 25 Measures price deviation from session VWAP

Structure Shift 25 Confirms pivot breakout (HARD GATE)

CVD Alignment 25 Detects order flow divergence/confirmation

Time-of-Day 25 Identifies high-probability trading sessions

1️⃣ VWAP Context (Max 25 Points)

Purpose: Identifies extreme price deviations from fair value for mean-reversion opportunities.

VWAP (Volume-Weighted Average Price) is calculated session-anchored to New York market time, with standard deviation bands creating zones of opportunity.

Band Structure:

1st Band: ±1σ from VWAP (fair value zone)

2nd Band: ±2σ from VWAP (moderate deviation)

3rd Band: ±3σ from VWAP (extreme deviation)

Scoring Logic (Exclusive):

Price in 3rd VWAP Band (>2σ and ≤3σ) → +25 points

Price in 2nd VWAP Band (>1σ and ≤2σ) → +15 points

Otherwise (inside 1σ or beyond 3σ) → 0 points

Key Insight: The further price stretches from VWAP, the higher the probability of mean reversion.

2️⃣ Structure Shift (Max 25 Points) — HARD GATE

Purpose: Confirms momentum shift through confirmed pivot breakouts.

⚠️ CRITICAL: Structure shift is mandatory. If no valid structure shift occurs, the total score becomes 0 regardless of other factors.

Detection Method:

Uses TradingView's ta.pivothigh() and ta.pivotlow() functions with locked parameters:

Left bars: 2

Right bars: 2

Source: Configurable (Wick or Body)

Break confirmation: Candle close only

Bullish Structure Shift:

✅ Prior swing high exists (confirmed pivot)

✅ Current candle closes above swing high + tick buffer

✅ Must occur in VWAP 2nd or 3rd band

✅ VWAP Filter: Price must be at or below VWAP (lower bands)

Bearish Structure Shift:

✅ Prior swing low exists (confirmed pivot)

✅ Current candle closes below swing low - tick buffer

✅ Must occur in VWAP 2nd or 3rd band

✅ VWAP Filter: Price must be at or above VWAP (upper bands)

Scoring:

Valid structure shift → +25 points

No structure shift → Total score = 0

Tick Buffer: Default 5 ticks (configurable) - prevents false breaks from minor price noise.

3️⃣ CVD Alignment (Max 25 Points)

Purpose: Detects institutional order flow through volume delta analysis.

CVD (Cumulative Volume Delta) is a proxy for order flow:

Close > Open → +Volume (buying pressure)

Close < Open → -Volume (selling pressure)

Scoring Logic:

Condition Points Description

Divergence +25 Price makes higher high + CVD makes lower high (bearish)

Price makes lower low + CVD makes higher low (bullish)

Confirmation +20 Price and CVD both make higher highs or lower lows

Neutral 0 No clear divergence or confirmation

Lookback Window: Last 20 bars (configurable) - prevents stale divergences.

Key Insight: Divergences suggest weakening momentum, while confirmations validate the trend.

4️⃣ Time-of-Day Context (Max 25 Points)

Purpose: Prioritizes high-volume, high-volatility New York sessions.

Scored Sessions (America/New_York timezone):

Session Time Range (NY) Points Description

Pre-Market 03:00 - 04:00 +25 Early liquidity injection

Market Open 09:30 - 11:30 +25 Highest volume period

Off-Hours All other times 0 Lower probability setups

Key Insight: Structure shifts during active sessions have higher follow-through probability.

🏆 Setup Classification

Setups are graded based on total score thresholds (configurable):

Grade Score Range Typical Components Quality Level

A++ Setup ≥90 All 4 factors aligned

(VWAP 3rd band + Structure + CVD + Session) Premium - Rare

A+ Setup ≥75 Structure + VWAP + CVD or Session

(3 of 4 factors) High - Select

A Setup ≥60 Structure + VWAP + Session

(Minimum viable setup) Good - Regular

No Grade <60 Insufficient confluence Filtered out

Default Thresholds:

A Setup: 60 points

A+ Setup: 75 points

A++ Setup: 90 points

📥 Installation

Step 1: Download the Indicator

Download the market_state_engine.pine file from this repository.

Step 2: Add to TradingView

Open TradingView

Open the Pine Editor (bottom panel)

Click "New" → "Blank indicator"

Delete all default code

Paste the contents of market_state_engine.pine

Click "Add to Chart"

Step 3: Configure for Your Symbol

Click the gear icon next to the indicator name

Adjust Tick Size for your instrument:

ES futures: 0.25

NQ futures: 0.25

Stocks: 0.01

Save settings

⚙️ Configuration

Symbol Settings

Parameter Default Description

Tick Size 0.25 Minimum price movement for your symbol

Tick Buffer Count 5 Ticks beyond swing for valid break

VWAP Settings

Parameter Default Description

VWAP Band 1 (σ) 1.0 1st standard deviation multiplier

VWAP Band 2 (σ) 2.0 2nd standard deviation multiplier

VWAP Band 3 (σ) 3.0 3rd standard deviation multiplier

Session Settings

Parameter Default Description

Session 1 0300-0400 Pre-market window (NY time)

Session 2 0930-1130 Market open window (NY time)

Score Thresholds

Parameter Default Description

A Setup Threshold 60 Minimum score for A grade

A+ Setup Threshold 75 Minimum score for A+ grade

A++ Setup Threshold 90 Minimum score for A++ grade

CVD Settings

Parameter Default Description

CVD Divergence Lookback 20 Maximum bars for divergence detection

Swing Settings

Parameter Default Options Description

Swing Detection Method Wick Wick / Body Use high/low or open/close for pivots

Visual Settings

Parameter Default Description

Show VWAP Bands ✅ Display VWAP and standard deviation bands

Show Setup Labels ✅ Display setup markers on chart

Show Score Panel ✅ Display real-time score breakdown

📖 How to Use

Step 1: Apply to 1-Minute Chart

⚠️ The indicator is locked to 1-minute timeframe - do not use on other timeframes.

Step 2: Understand the Visual Signals

Setup Labels

Green Triangle (▲) - Bullish (Long) setup detected

Red Triangle (▼) - Bearish (Short) setup detected

Label shows Grade (A/A+/A++) and Total Score

VWAP Bands

Yellow Line - Session VWAP (fair value)

Blue Bands - ±1σ (fair value zone)

Purple Bands - ±2σ (moderate deviation)

Red Bands - ±3σ (extreme deviation)

Score Panel (Top Right)

Real-time breakdown of all four components:

Component Score

VWAP Zone 15/25

Structure 25/25

CVD 20/25

Session 25/25

TOTAL 85/100 (A+)

Step 3: Interpret Signals

Valid Long Setup:

✅ Green triangle below candle

✅ Price in lower VWAP bands (below VWAP)

✅ Structure shift breaks swing high

✅ Score ≥60

Valid Short Setup:

✅ Red triangle above candle

✅ Price in upper VWAP bands (above VWAP)

✅ Structure shift breaks swing low

✅ Score ≥60

Step 4: Set Up Alerts (See Alert Conditions section)

🚦 Signal Filters (VWAP Zone Logic)

The indicator uses directional VWAP filtering to prevent counter-trend signals:

Long Signals (Green)

Only allowed when price is AT or BELOW VWAP

✅ Lower 2nd band (-2σ to -1σ)

✅ Lower 3rd band (-3σ to -2σ)

✅ At VWAP exactly

❌ BLOCKED in upper bands (above VWAP)

Logic: Longs when price is stretched below fair value (mean reversion)

Short Signals (Red)

Only allowed when price is AT or ABOVE VWAP

✅ Upper 2nd band (+1σ to +2σ)

✅ Upper 3rd band (+2σ to +3σ)

✅ At VWAP exactly

❌ BLOCKED in lower bands (below VWAP)

Logic: Shorts when price is stretched above fair value (mean reversion)

🎨 Visual Elements

Chart Overlays

Element Color Description

VWAP Line Yellow Session-anchored fair value

±1σ Bands Blue Fair value zone (no score)

±2σ Bands Purple Moderate deviation (15 pts)

±3σ Bands Red Extreme deviation (25 pts)

Swing Highs Red ▼ Confirmed pivot highs

Swing Lows Green ▲ Confirmed pivot lows

Session Background Light Green Active high-value session

Setup Labels

Bullish Setup:

A+

▲ 75

Green label below candle, shows grade and score

Bearish Setup:

A++

▼ 90

Red label above candle, shows grade and score

Score Panel

Real-time table in top-right corner:

Individual component scores (0-25 each)

Total score (0-100)

Current setup grade (A/A+/A++)

Updates in real-time as market conditions change

🔔 Alert Conditions

Setting Up Alerts

Method 1: Built-in Alert Conditions

Click "Create Alert" in TradingView

Select Market State Engine as condition

Choose alert type:

Bullish Setup - Long signals only

Bearish Setup - Short signals only

Any Setup - All signals

Set to "Once Per Bar Close"

Configure notification method (app, email, webhook)

Method 2: Custom Alert Message

Alert messages include full breakdown:

A+ Setup Detected (Score: 85)

Components: VWAP(25) + Structure(25) + CVD(20) + Time(15)

CVD State: Confirmation

Direction: Long

Timeframe: 1m

Alert Behavior

✅ One alert per unique pivot break - no spam

✅ Fires on candle close only - no repainting

✅ Minimum score filter - only A grade or higher (≥60)

✅ Direction-specific - separate bullish/bearish conditions

⚠️ No cooldown between different pivots - multiple alerts per session allowed if different swing levels break

🔧 Technical Details

Timeframe Lock

Required: 1-minute chart only

Reason: Scoring model calibrated for 1m micro-structure

Future: Multi-timeframe support planned for v2

Timezone Configuration

Hard-coded: America/New_York

Session Detection: Uses TradingView's native session functions

Consistency: All time-based logic uses NY timezone

Swing Detection Parameters

Locked to specification:

ta.pivothigh(source, left=2, right=2)

ta.pivotlow(source, left=2, right=2)

Implications:

Pivots confirmed 2 bars after formation

No repainting - historical pivots don't move

4-bar minimum swing structure (2 left + pivot + 2 right)

VWAP Calculation

Type: Session-anchored (resets daily)

Source: Typical price (high + low + close) / 3

Weighting: Volume-weighted

Standard Deviation: True population standard deviation

CVD Proxy Formula

barDelta = close > open ? volume : close < open ? -volume : 0

CVD = cumulative sum of barDelta (session-reset)

Performance Limits

Max Labels: 500 (TradingView limit)

Max Bars Back: 500

Memory: Lightweight - uses only essential variables

💡 Best Practices

1. Use as a Filter, Not a Strategy

❌ Don't: Blindly take every signal

✅ Do: Use score as confluence for your existing analysis

2. Higher Grades = Better Probability

A Setups (60-74): Regular opportunities, still require discretion

A+ Setups (75-89): High-quality, multiple factors aligned

A++ Setups (90-100): Rare premium opportunities, strongest edge

3. Respect the VWAP Zone Filter

The indicator automatically blocks:

Longs in upper VWAP bands (counter-trend)

Shorts in lower VWAP bands (counter-trend)

Trust this logic - it enforces mean reversion discipline.

4. Monitor the Score Panel

Watch which components are scoring to understand why a setup formed:

Missing CVD score? → No order flow confirmation

Missing Time score? → Outside high-volume sessions

Low VWAP score? → Weak deviation from fair value

5. Combine with Risk Management

The indicator provides opportunity scoring, not position sizing:

Use stop losses based on swing structure

Scale position size with setup grade (larger on A++, smaller on A)

Set profit targets at VWAP or opposing band

6. Session Awareness

Prioritize signals during active sessions:

03:00-04:00 NY: Pre-market momentum

09:30-11:30 NY: Highest volume, tightest spreads

Off-hours signals (0 time score) are lower probability but still valid if other factors strong.

7. Understand the Hard Gate

If no structure shift occurs:

Total score = 0

No alerts fire

Other components irrelevant

Why? Structure shift confirms momentum change - without it, there's no tradable opportunity.

8. Avoid Over-Optimization

Default settings are well-calibrated:

Don't chase "perfect" parameters

Test changes on historical data before live use

Document any modifications

9. Leverage Alert De-Duplication

The indicator prevents spam automatically:

One alert per unique swing break

New swing levels = new alerts

No need to manually filter notifications

10. Supplement with Price Action

Use the indicator alongside:

Support/resistance levels

Order flow footprint charts

Volume profile

Market internals (breadth, TICK, etc.)

📚 Example Scenarios

Example 1: A++ Premium Setup (Score: 95)

Price: In lower 3rd VWAP band (-2.8σ) → VWAP: 25 pts

Structure: Close breaks swing high → Structure: 25 pts

CVD: Price LL + CVD HL (bullish div) → CVD: 25 pts

Time: 10:15 AM NY (market open) → Time: 25 pts

Direction: LONG (price below VWAP) → Valid

Grade: A++ (95/100)

Interpretation: All factors aligned - premium mean-reversion long opportunity.

Example 2: A+ Strong Setup (Score: 80)

Price: In upper 2nd VWAP band (+1.5σ) → VWAP: 15 pts

Structure: Close breaks swing low → Structure: 25 pts

CVD: Price HH + CVD LH (bearish div) → CVD: 25 pts

Time: 2:00 PM NY (off-hours) → Time: 0 pts

Direction: SHORT (price above VWAP) → Valid

Grade: A+ (65/100)

Interpretation: Strong setup despite off-hours, bearish divergence adds confidence.

Example 3: Filtered Setup (Score: 0)

Price: In upper 3rd VWAP band (+2.5σ) → VWAP: 25 pts (if allowed)

Structure: Close breaks swing high → Structure: BLOCKED

CVD: Price HH + CVD HH (confirmation) → CVD: 20 pts (if allowed)

Time: 10:00 AM NY → Time: 25 pts (if allowed)

Direction: LONG (price ABOVE VWAP) → ❌ INVALID ZONE

Grade: None (0/100) - NO ALERT

Interpretation: VWAP filter blocked long signal in upper band - prevents counter-trend trade.

🛠️ Troubleshooting

No Signals Appearing

✅ Verify you're on 1-minute chart

✅ Check Tick Size matches your symbol

✅ Ensure VWAP Bands are visible

✅ Wait for confirmed pivots (requires at least 5 bars of history)

Alerts Not Firing

✅ Confirm alert is set to "Once Per Bar Close"

✅ Check score threshold (must be ≥60 by default)

✅ Verify VWAP zone filter isn't blocking signals

✅ Check that structure shift is actually occurring

Score Always Zero

✅ No structure shift detected (hard gate active)

✅ Price may not be in valid VWAP zone (2nd or 3rd band)

✅ Insufficient swing history (wait for pivots to form)

Too Many/Too Few Signals

Too many signals:

Increase A Setup Threshold (e.g., 70 instead of 60)

Increase Tick Buffer Count (reduces false breaks)

Too few signals:

Decrease A Setup Threshold (e.g., 50 instead of 60)

Decrease Tick Buffer Count (more sensitive to breaks)

📜 License

This indicator is provided under the Mozilla Public License 2.0.

🤝 Credits

Developed as a professional trading tool for systematic opportunity identification.

Philosophy: Reduce noise. Enforce discipline. Keep the human in control.

📞 Support

For questions, issues, or feature requests, please consult:

This README documentation

The specification document (pinescript_market_state_engine_spec.docx)

Inline code comments in market_state_engine.pine

🔄 Version History

v1.0 (Current)

Initial release

4-component scoring model (VWAP + Structure + CVD + Time)

VWAP zone directional filtering

Alert de-duplication

Configurable inputs

Real-time score panel

Session-aware logic

🎓 Understanding the Numbers

Quick Reference Card

Score Range Grade Quality Typical Use

90-100 A++ Premium Highest conviction trades

75-89 A+ High Strong probability setups

60-74 A Good Acceptable with discretion

0-59 None Filtered Skip or wait for confluence

Component Contribution Examples

Minimum A Setup (60 points):

Structure (25) + VWAP 3rd band (25) + Time (25) = 75 ✅

Typical A+ Setup (75 points):

Structure (25) + VWAP 2nd band (15) + CVD confirm (20) + Time (25) = 85 ✅

Maximum A++ Setup (100 points):

Structure (25) + VWAP 3rd band (25) + CVD divergence (25) + Time (25) = 100 ✅

🎯 Final Reminder

This is NOT a trading bot.

This is NOT financial advice.

This is a decision-support tool.

Always:

✅ Use proper risk management

✅ Understand the logic before trading

✅ Backtest on your symbols

✅ Keep the human in control

Happy Trading! 📈

ค้นหาในสคริปต์สำหรับ "Futures"

AssetCorrelationUtils

- Open source Library Used for Indicators that utilize correlation between assets for divergence calculations. It has no drawing elements.

ASSET CORRELATION UTILS

PineScript library for automatic detection of correlated asset pairs and triads for multi-asset analysis.

WHAT IT DOES

This library automatically identifies correlated assets based on the current chart symbol. It returns properly configured asset pairings for use in SMT divergence detection, inter-market analysis, and multi-asset comparison tools.

HOW IT WORKS

The library matches your chart symbol against known correlation groups:

Index Futures: NQ/ES/YM/RTY triads (including micros)

Metals: Gold/Silver/Copper triads (futures and CFD)

Forex: EUR/GBP/DXY and USD/JPY/CHF triads

Energy: Crude/Gasoline/Heating Oil triads

Treasury: ZB/ZF/ZN bond triads

Crypto: BTC/ETH/TOTAL3 and major altcoin pairings

Inversion flags are automatically computed for assets that move inversely (e.g., DXY vs EUR pairs).

HOW TO USE

import fstarcapital/AssetCorrelationUtils/1 as acu

// Simple: auto-detect from current chart

config = acu.resolveCurrentChart()

// Access resolved assets

primary = config.primary

secondary = config.secondary

tertiary = config.tertiary

EXPORTED FUNCTIONS

resolveCurrentChart(): One-call auto-detection using chart syminfo

resolveAssets(): Full detection with custom parameters

resolveTriad() / resolveDyad(): Manual resolution with inversion logic

detect*() functions: Category-specific detectors for custom workflows

TYPES

AssetPairing: Core structure for primary/secondary/tertiary tickers with inversion flags

AssetConfig: Full resolution result with detection status and asset category

DISCLAIMER

This library is a utility for building multi-asset indicators. Asset correlations are not guaranteed and may change over time. Always validate pairings for your specific trading context.

Full Default Function @type and @field descriptions below.

Library "AssetCorrelationUtils"

detectIndicesFutures(ticker)

Detects Index Futures (NQ/ES/YM/RTY + micro variants)

Parameters:

ticker (string) : The ticker string to check (typically syminfo.ticker)

Returns: AssetPairing with secondary and tertiary assets configured

detectMetalsFutures(ticker)

Detects Metal Futures (GC/SI/HG + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectForexFutures(ticker)

Detects Forex Futures (6E/6B + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectEnergyFutures(ticker)

Detects Energy Futures (CL/RB/HO + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectTreasuryFutures(ticker)

Detects Treasury Futures (ZB/ZF/ZN)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectCryptoFutures(ticker)

Detects CME Crypto Futures (BTC/ETH + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectCADFutures(ticker)

Detects CAD Forex Futures (6C + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectForexCFD(ticker, tickerId)

Detects Forex CFD pairs (EUR/GBP/DXY, USD/JPY/CHF triads)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID (syminfo.tickerid) for primary asset

Returns: AssetPairing with secondary and tertiary assets configured

detectCrypto(ticker, tickerId)

Detects major Crypto assets (BTC, ETH, SOL, XRP, alts)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID for primary asset

Returns: AssetPairing with secondary and tertiary assets configured

detectMetalsCFD(ticker, tickerId)

Detects Metals CFD (XAU/XAG/Copper)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID for primary asset

Returns: AssetPairing with secondary and tertiary assets configured

detectIndicesCFD(ticker, tickerId)

Detects Indices CFD (NAS100/SP500/DJ30)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID for primary asset

Returns: AssetPairing with secondary and tertiary assets configured

detectEUStocks(ticker, tickerId)

Detects EU Stock Indices (GER40/EU50) - Dyad only

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID for primary asset

Returns: AssetPairing with secondary asset configured (tertiary empty for dyad)

getDefaultFallback(tickerId)

Returns default fallback assets (chart ticker only, no correlation)

Parameters:

tickerId (string) : The full ticker ID for primary asset

Returns: AssetPairing with chart ticker as primary, empty secondary/tertiary (no correlation)

applySessionModifierWithBackadjust(tickerStr, sessionType)

Applies futures session modifier to ticker WITH back adjustment

Parameters:

tickerStr (string) : The ticker to modify

sessionType (string) : The session type (syminfo.session)

Returns: Modified ticker string with session and backadjustment.on applied

applySessionModifierNoBackadjust(tickerStr, sessionType)

Applies futures session modifier to ticker WITHOUT back adjustment

Parameters:

tickerStr (string) : The ticker to modify

sessionType (string) : The session type (syminfo.session)

Returns: Modified ticker string with session and backadjustment.off applied

isTriadMode(pairing)

Checks if a pairing represents a valid triad (3 assets)

Parameters:

pairing (AssetPairing) : The AssetPairing to check

Returns: True if tertiary is non-empty (triad mode), false for dyad

getAssetTicker(tickerId)

Extracts clean ticker string from full ticker ID

Parameters:

tickerId (string) : The full ticker ID (e.g., "BITGET:BTCUSDT.P")

Returns: Clean ticker string (e.g., "BTCUSDT.P")

resolveTriad(chartTickerId, pairing)

Resolves triad asset assignments with proper inversion flags

Parameters:

chartTickerId (string) : The current chart's ticker ID (syminfo.tickerid)

pairing (AssetPairing) : The detected AssetPairing

Returns: Tuple

resolveDyad(chartTickerId, pairing)

Resolves dyad asset assignment with proper inversion flag

Parameters:

chartTickerId (string) : The current chart's ticker ID

pairing (AssetPairing) : The detected AssetPairing (dyad: tertiary is empty)

Returns: Tuple

resolveAssets(ticker, tickerId, assetType, sessionType, useBackadjust)

Main auto-detection entry point. Detects asset category and returns fully resolved config.

Parameters:

ticker (string) : The ticker string to check (typically syminfo.ticker)

tickerId (string) : The full ticker ID (typically syminfo.tickerid)

assetType (string) : The asset type (typically syminfo.type)

sessionType (string) : The session type for futures (typically syminfo.session)

useBackadjust (bool) : Whether to apply back adjustment for futures session alignment

Returns: AssetConfig with fully resolved assets, inversion flags, and detection status

resolveCurrentChart()

Simplified auto-detection using current chart's syminfo values

Returns: AssetConfig with fully resolved assets, inversion flags, and detection status

AssetPairing

Core asset pairing structure for triad/dyad configurations

Fields:

primary (series string) : The primary (chart) asset ticker ID

secondary (series string) : The secondary correlated asset ticker ID

tertiary (series string) : The tertiary correlated asset ticker ID (empty for dyad)

invertSecondary (series bool) : Whether secondary asset should be inverted for divergence calc

invertTertiary (series bool) : Whether tertiary asset should be inverted for divergence calc

AssetConfig

Full asset resolution result with mode detection and computed values

Fields:

detected (series bool) : Whether auto-detection succeeded

isTriadMode (series bool) : True if triad (3 assets), false if dyad (2 assets)

primary (series string) : The resolved primary asset ticker ID

secondary (series string) : The resolved secondary asset ticker ID

tertiary (series string) : The resolved tertiary asset ticker ID (empty for dyad)

invertSecondary (series bool) : Computed inversion flag for secondary asset

invertTertiary (series bool) : Computed inversion flag for tertiary asset

assetCategory (series string) : String describing the detected asset category

Lot Size + Margin InfoThis indicator is designed to give Futures & Options traders instant access to lot size and estimated margin requirements for the instrument they are viewing — directly on their TradingView chart. It combines real-time symbol detection with a built-in, regularly updated margin lookup table (sourced from Kotak Securities’ published margin requirements), while also handling fallback logic for unknown or unsupported symbols.

---

### What It Does

* Automatically Detects the Instrument Type

Identifies whether the current chart’s symbol is a futures contract, option, or a cash/spot instrument.

* Shows Accurate Lot Size

For supported F\&O symbols, it fetches the correct lot size directly from exchange data.

For options, it retrieves the lot size from the option’s point value.

For cash/spot symbols with linked futures, it uses the futures lot size.

* Calculates Estimated Margin

* For futures: `Lot Size × Current Price × Margin%` (Margin% sourced from the internal lookup table).

* For options: `Lot Size × Current Price` (simple multiplication, as options margin ≈ premium cost).

* For unsupported or non-FnO symbols: Displays "No FnO".

* Fallback Margin Logic

If a symbol is missing from the margin lookup table, the script applies a user-defined default margin percentage and highlights the data in orange to indicate it’s using fallback values.

* Debug Mode for Transparency

A toggle to display the exact symbol string used for fetching lot size and margin, so traders can verify the data source.

---

### How It Works

1. Symbol Normalization

The script standardizes symbol names to match the margin table format (e.g., converting `"NIFTY1!"` to `"NIFTY"`).

2. Type-Based Handling

* Futures – Uses point value for lot size, applies specific margin % from the table.

* Options – Uses option point value for lot size, margin is simply premium × lot size.

* Cash Symbols with Linked Futures – Attempts to find and use the associated futures contract for lot/margin data.

* Unsupported Symbols – Displays `"No FnO"`.

3. Margin Table Integration

The margin % table is manually updated from a reliable broker’s margin sheet (Kotak Securities) — ensuring alignment with real trading conditions.

4. Customizable Display

* Position (Top Right / Bottom Left / Bottom Right)

* Table background color, text color, font size, border width

* Editable label text for lot size and margin display

* Toggleable lot size and margin sections

---

### How to Use

1. Add the Indicator to Your Chart – Works on any NSE Futures, Options, or Cash symbol with linked F\&O.

2. Configure Display Settings – Choose whether to show lot size, margin, or both, and place the info table where you prefer.

3. Adjust Fallback Margin % – If you trade less common contracts, set your default margin % to reflect your broker’s requirement.

4. Enable Debug Mode (Optional) – To see the exact symbol source the script is using.

---

### Best For

* Intraday & Positional F\&O Traders who need instant clarity on lot size and margin before entering trades.

* Options Sellers & Buyers who want quick cost estimates.

* Traders Switching Symbols Quickly — saves time by removing the need to check the broker’s margin sheet manually.

---

💡 Pro Tip: Since margin requirements can change, keep the script updated whenever your broker revises margin data. This version’s margin table is updated as of 13-08-2025.

BTC Future Gamma-Weighted Momentum Model (BGMM)The BTC Future Gamma-Weighted Momentum Model (BGMM) is a quantitative trading strategy that utilizes the Gamma-weighted average price (GWAP) in conjunction with a momentum-based approach to predict price movements in the Bitcoin futures market. The model combines the concept of weighted price movements with trend identification, where the Gamma factor amplifies the weight assigned to recent prices. It leverages the idea that historical price trends and weighting mechanisms can be utilized to forecast future price behavior.

Theoretical Background:

1. Momentum in Financial Markets:

Momentum is a well-established concept in financial market theory, referring to the tendency of assets to continue moving in the same direction after initiating a trend. Any observed market return over a given time period is likely to continue in the same direction, a phenomenon known as the “momentum effect.” Deviations from a mean or trend provide potential trading opportunities, particularly in highly volatile assets like Bitcoin.

Numerous empirical studies have demonstrated that momentum strategies, based on price movements, especially those correlating long-term and short-term trends, can yield significant returns (Jegadeesh & Titman, 1993). Given Bitcoin’s volatile nature, it is an ideal candidate for momentum-based strategies.

2. Gamma-Weighted Price Strategies:

Gamma weighting is an advanced method of applying weights to price data, where past price movements are weighted by a Gamma factor. This weighting allows for the reinforcement or reduction of the influence of historical prices based on an exponential function. The Gamma factor (ranging from 0.5 to 1.5) controls how much emphasis is placed on recent data: a value closer to 1 applies an even weighting across periods, while a value closer to 0 diminishes the influence of past prices.

Gamma-based models are used in financial analysis and modeling to enhance a model’s adaptability to changing market dynamics. This weighting mechanism is particularly advantageous in volatile markets such as Bitcoin futures, as it facilitates quick adaptation to changing market conditions (Black-Scholes, 1973).

Strategy Mechanism:

The BTC Future Gamma-Weighted Momentum Model (BGMM) utilizes an adaptive weighting strategy, where the Bitcoin futures prices are weighted according to the Gamma factor to calculate the Gamma-Weighted Average Price (GWAP). The GWAP is derived as a weighted average of prices over a specific number of periods, with more weight assigned to recent periods. The calculated GWAP serves as a reference value, and trading decisions are based on whether the current market price is above or below this level.

1. Long Position Conditions:

A long position is initiated when the Bitcoin price is above the GWAP and a positive price movement is observed over the last three periods. This indicates that an upward trend is in place, and the market is likely to continue in the direction of the momentum.

2. Short Position Conditions:

A short position is initiated when the Bitcoin price is below the GWAP and a negative price movement is observed over the last three periods. This suggests that a downtrend is occurring, and a continuation of the negative price movement is expected.

Backtesting and Application to Bitcoin Futures:

The model has been tested exclusively on the Bitcoin futures market due to Bitcoin’s high volatility and strong trend behavior. These characteristics make the market particularly suitable for momentum strategies, as strong upward or downward movements are often followed by persistent trends that can be captured by a momentum-based approach.

Backtests of the BGMM on the Bitcoin futures market indicate that the model achieves above-average returns during periods of strong momentum, especially when the Gamma factor is optimized to suit the specific dynamics of the Bitcoin market. The high volatility of Bitcoin, combined with adaptive weighting, allows the model to respond quickly to price changes and maximize trading opportunities.

Scientific Citations and Sources:

• Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65–91.

• Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637–654.

• Fama, E. F., & French, K. R. (1992). The Cross-Section of Expected Stock Returns. The Journal of Finance, 47(2), 427–465.

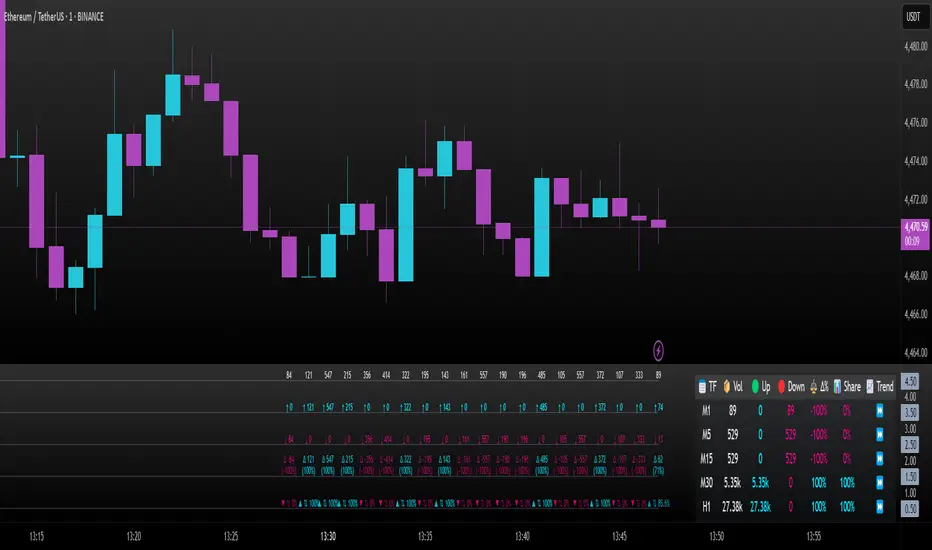

Intrabar Volume Delta — RealTime + History (Stocks/Crypto/Forex)Intrabar Volume Delta Grid — RealTime + History (Stocks/Crypto/Forex)

# Short Description

Shows intrabar Up/Down volume, Delta (absolute/relative) and UpShare% in a compact grid for both real-time and historical bars. Includes an MTF (M1…D1) dashboard, contextual coloring, density controls, and alerts on Δ and UpShare%. Smart historical splitting (“History Mode”) for Crypto/Futures/FX.

---

# What it does (Quick)

* **UpVol / DownVol / Δ / UpShare%** — visualizes order-flow inside each candle.

* **Real-time** — accumulates intrabar volume live by tick-direction.

* **History Mode** — splits Up/Down on closed bars via simple or range-aware logic.

* **MTF Dashboard** — one table view across M1, M5, M15, M30, H1, H4, D1 (Vol, Up/Down, Δ%, Share, Trend).

* **Contextual opacity** — stronger signals appear bolder.

* **Label density** — draw every N-th bar and limit to last X bars for performance.

* **Alerts** — thresholds for |Δ|, Δ%, and UpShare%.

---

# How it works (Real-Time vs History)

* **Real-time (open bar):** volume increments into **UpVolRT** or **DownVolRT** depending on last price move (↑ goes to Up, ↓ to Down). This approximates live order-flow even when full tick history isn’t available.

* **History (closed bars):**

* **None** — no split (Up/Down = 0/0). Safest for equities/indices with unreliable tick history.

* **Approx (Close vs Open)** — all volume goes to candle direction (green → Up 100%, red → Down 100%). Fast but yields many 0/100% bars.

* **Price Action Based** — splits by Close position within High-Low range; strength = |Close−mid|/(High−Low). Above mid → more Up; below mid → more Down. Falls back to direction if High==Low.

* **Auto** — **Stocks/Index → None**, **Crypto/Futures/FX → Approx**. If you see too many 0/100 bars, switch to **Price Action Based**.

---

# Rows & Meaning

* **Volume** — total bar volume (no split).

* **UpVol / DownVol** — directional intrabar volume.

* **Delta (Δ)** — UpVol − DownVol.

* **Absolute**: raw units

* **Relative (Δ%)**: Δ / (Up+Down) × 100

* **Both**: shows both formats

* **UpShare%** — UpVol / (Up+Down) × 100. >50% bullish, <50% bearish.

* Helpful icons: ▲ (>65%), ▼ (<35%).

---

# MTF Dashboard (🔧 Enable Dashboard)

A single table with **Vol, Up, Down, Δ%, Share, Trend (🔼/🔽/⏭️)** for selected timeframes (M1…D1). Great for a fast “panorama” read of flow alignment across horizons.

---

# Inputs (Grouped)

## Display

* Toggle rows: **Volume / Up / Down / Delta / UpShare**

* **Delta Display**: Absolute / Relative / Both

## Realtime & History

* **History Mode**: Auto / None / Approx / Price Action Based

* **Compact Numbers**: 1.2k, 1.25M, 3.4B…

## Theme & UI

* **Theme Mode**: Auto / Light / Dark

* **Row Spacing**: vertical spacing between rows

* **Top Row Y**: moves the whole grid vertically

* **Draw Guide Lines**: faint dotted guides

* **Text Size**: Tiny / Small / Normal / Large

## 🔧 Dashboard Settings

* **Enable Dashboard**

* **📏 Table Text Size**: Tiny…Huge

* **🦓 Zebra Rows**

* **🔲 Table Border**

## ⏰ Timeframes (for Dashboard)

* **M1…D1** toggles

## Contextual Coloring

* **Enable Contextual Coloring**: opacity by signal strength

* **Δ% cap / Share offset cap**: saturation caps

* **Min/Max transparency**: solid vs faint extremes

## Label Density & Size

* **Show every N-th bar**: draw labels only every Nth bar

* **Limit to last X bars**: keep labels only in the most recent X bars

## Colors

* Up / Down / Text / Guide

## Alerts

* **Delta Threshold (abs)** — |Δ| in volume units

* **UpShare > / <** — bullish/bearish thresholds

* **Enable Δ% Alert**, **Δ% > +**, **Δ% < −** — relative delta levels

---

# How to use (Quick Start)

1. Add the indicator to your chart (overlay=false → separate pane).

2. **History Mode**:

* Crypto/Futures/FX → keep **Auto** or switch to **Price Action Based** for richer history.

* Stocks/Index → prefer **None** or **Price Action Based** for safer splits.

3. **Label Density**: start with **Limit to last X bars = 30–150** and **Show every N-th bar = 2–4**.

4. **Contextual Coloring**: keep on to emphasize strong Δ% / Share moves.

5. **Dashboard**: enable and pick only the TFs you actually use.

6. **Alerts**: set thresholds (ideas below).

---

# Alerts (in TradingView)

Add alert → pick this indicator → choose any of:

* **Delta exceeds threshold** (|Δ| > X)

* **UpShare above threshold** (UpShare% > X)

* **UpShare below threshold** (UpShare% < X)

* **Relative Delta above +X%**

* **Relative Delta below −X%**

**Starter thresholds (tune per symbol & TF):**

* **Crypto M1/M5**: Δ% > +25…35 (bullish), Δ% < −25…−35 (bearish)

* **FX (tick volume)**: UpShare > 60–65% or < 40–35%

* **Stocks (liquid)**: set **Absolute Δ** by typical volume scale (e.g., 50k / 100k / 500k)

---

# Notes by Market Type

* **Crypto/Futures**: 24/7 and high liquidity — **Price Action Based** often gives nicer history splits than Approx.

* **Forex (FX)**: TradingView volume is typically **tick volume** (not true exchange volume). Treat Δ/Share as tick-based flow, still very useful intraday.

* **Stocks/Index**: historical tick detail can be limited. **None** or **Price Action Based** is a safer default. If you see too many 0/100% shares, switch away from Approx.

---

# “All Timeframes” accuracy

* Works on **any TF** (M1 → D1/W1).

* **Real-time accuracy** is strong for the open bar (live accumulation).

* **Historical accuracy** depends on your **History Mode** (None = safest, Approx = fastest/simplest, Price Action Based = more nuanced).

* The MTF dashboard uses `request.security` and therefore follows the same logic per TF.

---

# Trade Ideas (Use-Cases)

* **Scalping (M1–M5)**: a spike in Δ% + UpShare>65% + rising total Vol → momentum entries.

* **Intraday (M5–M30–H1)**: when multiple TFs show aligned Δ%/Share (e.g., M5 & M15 bullish), join the trend.

* **Swing (H4–D1)**: persistent Δ% > 0 and UpShare > 55–60% → structural accumulation bias.

---

# Advantages

* **True-feeling live flow** on the open bar.

* **Adaptable history** (three modes) to match data quality.

* **Clean visual layout** with guides, compact numbers, contextual opacity.

* **MTF snapshot** for quick bias read.

* **Performance controls** (last X bars, every N-th bar).

---

# Limitations & Care

* **FX uses tick volume** — interpret Δ/Share accordingly.

* **History Mode is an approximation** — confirm with trend/structure/liquidity context.

* **Illiquid symbols** can produce noisy or contradictory signals.

* **Too many labels** can slow charts → raise N, lower X, or disable guides.

---

# Best Practices (Checklist)

* Crypto/Futures: prefer **Price Action Based** for history.

* Stocks: **None** or **Price Action Based**; be cautious with **Approx**.

* FX: pair Δ% & UpShare% with session context (London/NY) and volatility.

* If labels overlap: tweak **Row Spacing** and **Text Size**.

* In the dashboard, keep only the TFs you actually act on.

* Alerts: start around **Δ% 25–35** for “punchy” moves, then refine per asset.

---

# FAQ

**1) Why do some closed bars show 0%/100% UpShare?**

You’re on **Approx** history mode. Switch to **Price Action Based** for smoother splits.

**2) Δ% looks strong but price doesn’t move — why?**

Δ% is an **order-flow** measure. Price also depends on liquidity pockets, sessions, news, higher-timeframe structure. Use confirmations.

**3) Performance slowdown — what to do?**

Lower **Limit to last X bars** (e.g., 30–100), increase **Show every N-th bar** (2–6), or disable **Draw Guide Lines**.

**4) Dashboard values don’t “match” the grid exactly?**

Dashboard is multi-TF via `request.security` and follows the history logic per TF. Differences are normal.

---

# Short “Store” Marketing Blurb

Intrabar Volume Delta Grid reveals the order-flow inside every candle (Up/Down, Δ, UpShare%) — live and on history. With smart history splitting, an MTF dashboard, contextual emphasis, and flexible alerts, it helps you spot momentum and bias across Crypto, Forex (tick volume), and Stocks. Tidy labels and compact numbers keep the panel readable and fast.

Clean Multi-Indicator Alignment System

Overview

A sophisticated multi-indicator alignment system designed for 24/7 trading across all markets, with pure signal-based exits and no time restrictions. Perfect for futures, forex, and crypto markets that operate around the clock.

Key Features

🎯 Multi-Indicator Confluence System

EMA Cross Strategy: Fast EMA (5) and Slow EMA (10) for precise trend direction

VWAP Integration: Institution-level price positioning analysis

RSI Momentum: 7-period RSI for momentum confirmation and reversal detection

MACD Signals: Optimized 8/17/5 configuration for scalping responsiveness

Volume Confirmation: Customizable volume multiplier (default 1.6x) for signal validation

🚀 Advanced Entry Logic

Initial Full Alignment: Requires all 5 indicators + volume confirmation

Smart Continuation Entries: EMA9 pullback entries when trend momentum remains intact

Flexible Time Controls: Optional session filtering or 24/7 operation

🎪 Pure Signal-Based Exits

No Forced Closes: Positions exit only on technical signal reversals

Dual Exit Conditions: EMA9 breakdown + RSI flip OR MACD cross + EMA20 breakdown

Trend Following: Allows profitable trends to run their full course

Perfect for Swing Scalping: Ideal for multi-session position holding

📊 Visual Interface

Real-Time Status Dashboard: Live alignment monitoring for all indicators

Color-Coded Candles: Instant visual confirmation of entry/exit signals

Clean Chart Display: Toggle-able EMAs and VWAP with professional styling

Signal Differentiation: Clear labels for entries, X-crosses for exits

🔔 Alert System

Entry Notifications: Separate alerts for buy/sell signals

Exit Warnings: Technical breakdown alerts for position management

Mobile Ready: Push notifications to TradingView mobile app

Market Applications

Perfect For:

Gold Futures (GC): 24-hour precious metals trading

NASDAQ Futures (NQ): High-volatility index scalping

Forex Markets: Currency pairs with continuous operation

Crypto Trading: 24/7 cryptocurrency momentum plays

Energy Futures: Oil, gas, and commodity swing trades

Optimal Timeframes:

1-5 Minutes: Ultra-fast scalping during high volatility

5-15 Minutes: Balanced approach for most markets

15-30 Minutes: Swing scalping for trend following

🧠 Smart Position Management

Tracks implied position direction

Prevents conflicting signals

Allows trend continuation entries

State-aware exit logic

⚡ Scalping Optimized

Fast-reacting indicators with shorter periods

Volume-based confirmation reduces false signals

Clean entry/exit visualization

Minimal lag for time-sensitive trades

Configuration Options

All parameters fully customizable:

EMA Lengths: Adjustable from 1-30 periods

RSI Period: 1-14 range for different market conditions

MACD Settings: Fast (1-15), Slow (1-30), Signal (1-10)

Volume Confirmation: 0.5-5.0x multiplier range

Visual Preferences: Colors, displays, and table options

Risk Management Features

Clear visual exit signals prevent emotion-based decisions

Volume confirmation reduces false breakouts

Multi-indicator confluence improves signal quality

Optional time filtering for session-specific strategies

Best Use Cases

Futures Scalping: NQ, ES, GC during active sessions

Forex Swing Trading: Major pairs during overlap periods

Crypto Momentum: Bitcoin, Ethereum trend following

24/7 Automated Systems: Algorithmic trading implementation

Multi-Market Scanning: Portfolio-wide signal monitoring

SA Trump Volatility Pattern Wick + Volume Shock ReversalDisclaimer (read first)

Educational use only — not financial advice. This script does not provide entries/exits, targets, position sizing, or profit guarantees. Trading (especially options/futures) involves substantial risk and can result in loss of principal (and more for leveraged products). Use at your own discretion.

Best use cases on the 2-Hour timeframe

On 2H, this script becomes a high-signal-quality “shock reversal” detector instead of a noisy candle toy. You’re essentially filtering for:

Large wick rejection

Small real body

Statistically unusual volume (Z-score > threshold)

Context alignment (trend filter + prior bar direction + optional RSI)

What 2H is best for

1) Detecting “event shock” reversals

2H bars often capture:

Macro headlines

Fed commentary

earnings reactions (for equities)

sudden volatility expansions

When the script fires on 2H, it often means:

“Aggressive push happened, liquidity got rejected, and participation was unusually high.”

That’s a structural clue, not a trade instruction.

2) Filtering false breakouts / breakdowns

The wick requirement is basically “failed continuation.”

On 2H, this is powerful around:

prior day highs/lows

weekly pivots

obvious consolidation edges

key moving averages (fast SMA / slow SMA gate)

Bull pattern = flush + reclaim behavior.

Bear pattern = pop + rejection behavior.

3) Options traders: timing “premium exposure windows”

On 2H, this is great for options traders who want to avoid buying premium into a fake move.

BullTrump on 2H can be used as a “don’t chase puts / be cautious short” context shift.

BearTrump on 2H can be used as a “don’t chase calls / be cautious long” context shift.

It’s a “regime hint” for the next few sessions, not a one-bar command.

4) Futures traders: rotation vs continuation framework

A 2H “Trump Candle” often marks:

the end of a liquidation leg

a stop-run / squeeze peak

a pivot moment where the market shifts from impulse to balance

Use it to decide whether you’re in:

continuation mode (trend carries)

or rotation mode (mean-reversion / two-way)

How to use it (2H workflow)

Step A — Keep it strict at first

Recommended defaults for 2H:

wickFracThreshold: 0.40–0.55

bodyMaxFrac: 0.35–0.45

volZThresh: 1.0–1.5

useRSIFilter: ON

RSI bull min / bear max: 45 / 55 (good baseline)

Step B — Treat triggers as “context events”

When it prints, ask 3 questions:

Where did it happen? (key level or random spot)

Was it aligned with trend gate? (SMA fast/slow)

Did volume Z-score spike? (true shock vs normal wick)

Higher quality triggers happen when:

the wick pierces a known level (prior swing / range edge)

and the close re-enters the range

and volume Z-score is meaningfully positive

Step C — Confirm with the next 1–2 candles (optional)

On 2H, it’s reasonable to wait for:

a follow-through close

or a hold above/below fast SMA

or a second “acceptance” candle

You can do this manually without changing code.

Other recommended timeframes (best to worst)

✅ 4H (even cleaner, fewer signals)

Use for:

swing context

multi-day pivots

big reversal points

✅ 1H (more signals, still structured)

Use for:

intraday + overnight context

day-trade bias shifts

✅ 30m (for active traders)

Use for:

tighter responsiveness

more setups

But requires more discretion; noise increases.

⚠️ 15m and below (only if you increase strictness)

If you want to run it on 5m/15m:

raise volZThresh (ex: 1.5–2.0)

raise wickFracThreshold (ex: 0.50–0.65)

lower bodyMaxFrac (ex: 0.25–0.35)

Otherwise it will trigger too often.

Best markets for this script

Works best on:

Index futures: /NQ, /ES (big volume makes Z-score meaningful)

Liquid ETFs: SPY, QQQ

High-volume large caps (AAPL, MSFT, NVDA etc.)

Less reliable on:

thin small caps (volume Z-score gets weird)

low-volume premarket candles

illiquid options underlyings

Signal Inside the Script ✅ SA ZoneEngine Bias Filtered is a market-structure bias and confirmation tool designed for futures To request access: 👉 Purchase here: trianchor.gumroad.com

Best GBT for this indicator

chatgpt.com

chatgpt.com

chatgpt.com

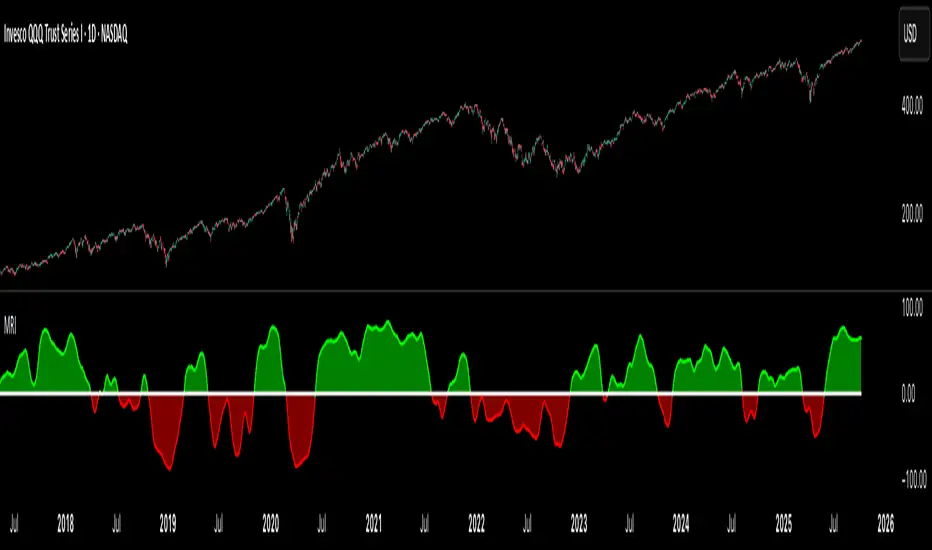

Market Regime IndexThe Market Regime Index is a top-down macro regime nowcasting tool that offers a consolidated view of the market’s risk appetite. It tracks 32 of the world’s most influential markets across asset classes to determine investor sentiment by applying trend-following signals to each independent asset. It features adjustable parameters and a built-in alert system that notifies investors when conditions transition between Risk-On and Risk-Off regimes. The selected markets are grouped into equities (7), fixed income (9), currencies (7), commodities (5), and derivatives (4):

Equities = S&P 500 E-mini Index Futures, Nasdaq-100 E-mini Index Futures, Russell 2000 E-mini Index Futures, STOXX Europe 600 Index Futures, Nikkei 225 Index Futures, MSCI Emerging Markets Index Futures, and S&P 500 High Beta (SPHB)/Low Beta (SPLV) Ratio.

Fixed Income = US 10Y Treasury Yield, US 2Y Treasury Yield, US 10Y-02Y Yield Spread, German 10Y Bund Yield, UK 10Y Gilt Yield, US 10Y Breakeven Inflation Rate, US 10Y TIPS Yield, US High Yield Option-Adjusted Spread, and US Corporate Option-Adjusted Spread.

Currencies = US Dollar Index (DXY), Australian Dollar/US Dollar, Euro/US Dollar, Chinese Yuan/US Dollar, Pound Sterling/US Dollar, Japanese Yen/US Dollar, and Bitcoin/US Dollar.

Commodities = ICE Brent Crude Oil Futures, COMEX Gold Futures, COMEX Silver Futures, COMEX Copper Futures, and S&P Goldman Sachs Commodity Index (GSCI) Futures.

Derivatives = CBOE S&P 500 Volatility Index (VIX), ICE US Bond Market Volatility Index (MOVE), CBOE 3M Implied Correlation Index, and CBOE VIX Volatility Index (VVIX)/VIX.

All assets are directionally aligned with their historical correlation to the S&P 500. Each asset contributes equally based on its individual bullish or bearish signal. The overall market regime is calculated as the difference between the number of Risk-On and Risk-Off signals divided by the total number of assets, displayed as the percentage of markets confirming each regime. Green indicates Risk-On and occurs when the number of Risk-On signals exceeds Risk-Off signals, while red indicates Risk-Off and occurs when the number of Risk-Off signals exceeds Risk-On signals.

Bullish Signal = (Fast MA – Slow MA) > (ATR × ATR Margin)

Bearish Signal = (Fast MA – Slow MA) < –(ATR × ATR Margin)

Market Regime = (Risk-On signals – Risk-Off signals) ÷ Total assets

This indicator is designed with flexibility in mind, allowing users to include or exclude individual assets that contribute to the market regime and adjust the input parameters used for trend signal detection. These parameters apply to each independent asset, and the overall regime signal is smoothed by the signal length to reduce noise and enhance reliability. Investors can position according to the prevailing market regime by selecting factors that have historically outperformed under each regime environment to minimise downside risk and maximise upside potential:

Risk-On Equity Factors = High Beta > Cyclicals > Low Volatility > Defensives.

Risk-Off Equity Factors = Defensives > Low Volatility > Cyclicals > High Beta.

Risk-On Fixed Income Factors = High Yield > Investment Grade > Treasuries.

Risk-Off Fixed Income Factors = Treasuries > Investment Grade > High Yield.

Risk-On Commodity Factors = Industrial Metals > Energy > Agriculture > Gold.

Risk-Off Commodity Factors = Gold > Agriculture > Energy > Industrial Metals.

Risk-On Currency Factors = Cryptocurrencies > Foreign Currencies > US Dollar.

Risk-Off Currency Factors = US Dollar > Foreign Currencies > Cryptocurrencies.

In summary, the Market Regime Index is a comprehensive macro risk-management tool that identifies the current market regime and helps investors align portfolio risk with the market’s underlying risk appetite. Its intuitive, color-coded design makes it an indispensable resource for investors seeking to navigate shifting market conditions and enhance risk-adjusted performance by selecting factors that have historically outperformed. While it has proven historically valuable, asset-specific characteristics and correlations evolve over time as market dynamics change.

Synthetic Implied APROverview

The Synthetic Implied APR is an artificial implied APR, designed to imitate the implied APR seen when trading cryptocurrency funding rates. It combines real-time funding rates with premium data to calculate an artificial market expectation of the annualized funding rate.

The (actual) implied APR is the market's expectation of the annualized funding rate. This is dependent on bid/ask impacts of the implied APR, something which is currently unavailable to fetch with TradingView. In essence, an implied APR of X% means traders believe that asset's funding fees to average X% when annualized.

What's important to understand, is that the actual value of the synthetic implied APR is not relevant. We only simply use its relative changes when we trade (i.e if it crosses above/below its MA for a given weight). Even for the same asset, the implied APRs will change depending on days to maturity.

How it calculates

The synthetic implied APR is calculated with these steps:

Collects premium data from perpetual futures markets using optimized lower timeframe requests (check my 'Predicted Funding Rates' indicator)

Calculates the funding rate by adding the premium to an interest rate component (clamped within exchange limits)

Derives the underlying APR from the 8-hour funding rate (funding rate × 3 × 365)

Apply a weighed formula that imitates both the direction (underlying APR) with the volatility of prices (from the premium index and funding)

premium_component = (prem_avg / 50 ) * 365

weighedprem = (weight * fr) + ((1 - weight) * apr) + (premium_component * 0.3)

impliedAPR = math.avg(weighedprem, ta.sma(apr, maLength))

How to use it: Generally

Preface: Funding rates are an indication of market sentiment

If funding is positive, generally the market is bullish as longs are willing to pay shorts funding

If funding is negative, generally the market is bearish as shorts are willing to pay longs funding

So, this script can be used like a typical oscillator:

Bullish: If implied APR > MA OR if implied APR MA is green

Bearish: If implied APR < MA OR if implied APR MA is red

The components:

Synthetic Implied APR: The main metric. At current setting of 0.7, it imitates volatility

Weight: The higher the value, the smoother the synthetic implied APR is (and MA too). This value is very important to the imitation. At 0.7, it imitates the actual volatility of the implied APR. At weight = 1, it becomes very smooth. Perfect for trading

Synthetic Implied APR Moving Average: A moving average of the Synthetic implied APR. Can choose from multiple selections, (SMA, EMA, WMA, HMA, VWMA, RMA)

How to use it: Trading Funding

When trading funding there're multiple ways to use it with different settings

Trade funding rates with trend changes

Settings: Weight = 1

Method 1: When the implied APR MA turns green, long funding rates (or short if red)

Method 2: When the implied APR crosses above the MA, long funding rates (or short when crosses below)

Trade funding rates with MA pullbacks

Settings: Weight = 0.7, timeframe 15m

In an uptrend: When implied APR crosses below then above the script, long funding opportunity

In an downtrend: When implied APR crosses above then below the script, shortfunding opportunity

You can determine the trend with the method before, using a weight of 1

To trade funding rates, it's best to have these 3 scripts at these settings:

Predicted Funding Rates: This allows you to see the predicted funding rates and see if they've maxxed out for added confluence too (+/-0.01% usually for Binance BTC futures)

Synthetic implied APR: At weight 1, the MA provides a good trend (whether close above/below or colour change)

Synthetic implied APR: At weight 0.7, it provides a good imitation of volatility

How to use it: Trading Futures

When trading futures:

You can determine roughly what the trend is, if the assumption is made that funding rates can help identify trends if used as a sentiment indicator. It should be supplemented with traditional trend trading methods

To prevent whipsaws, weight should remain high

Long trend: When the implied APR MA turns green OR when it crosses above its MA

Short trend: When the implied APR MA turns red OR when it below above its MA

Why it's original

This indicator introduces a unique synthetic weighting system that combines funding rates, underlying APR, and premium components in a way not found in existing TradingView scripts. Trading funding rates is a niche area, there aren't that many scripts currently available. And to my knowledge, there's no synthetic implied APR scripts available on TradingView either. So I believe this script to be original in that sense.

Notes

Because it depends on my triangular weighting algos, optimal accuracy is found on timeframes that are 4H or less. On higher timeframes, the accuracy drops off. Best timeframes for intraday trading using this are 15m or 1 hour

The higher the timeframe, the lower the MA one should use. At 1 hour, 200 or higher is best. At say, 4h, length of 50 is best

Only works for coins that have a Binance premium index

Inputs

Funding Period - Select between "1 Hour" or "8 Hour" funding cycles. 8 hours is standard for Binance

Table - Toggle the information dashboard on/off to show or hide real-time metrics including funding rate, premium, and APR value

Weight - Controls the balance between funding rate (higher values = smoother) and APR (lower values = more responsive) in the calculation, ranging from 0.0 to 1.0. Default is 0.7, this imitates the volatility

Auto Timeframe Implied Length - Automatically calculates optimal smoothing length based on your chart timeframe for consistent behavior across different time periods

Manual Implied Length - Sets a fixed smoothing length (in bars) when auto mode is disabled, with lower values being more responsive and higher values being smoother

Show Implied APR MA - Displays an additional moving average line of the Synthetic Implied APR to help identify trend direction and crossover signals

MA Type for Implied APR - Selects the calculation method (SMA, EMA, WMA, HMA, VWMA, or RMA) for the moving average, each offering different responsiveness and lag characteristics

MA Length for Implied APR - Sets the lookback period (1-500 bars) for the moving average, with shorter lengths providing more signals and longer lengths filtering noise

Show Underlying APR - Displays the raw APR calculation (without synthetic weighting) as a reference line to compare against the main indicator

Bullish Color - Sets the color for positive values in the table and rising MA line

Bearish Color - Sets the color for negative values in the table and falling MA line

Table Background - Customizes the background color and transparency of the information dashboard

Table Text Color - Sets the color for label text in the left column of the information table

Table Text Size - Controls the font size of table text with options from Tiny to Huge

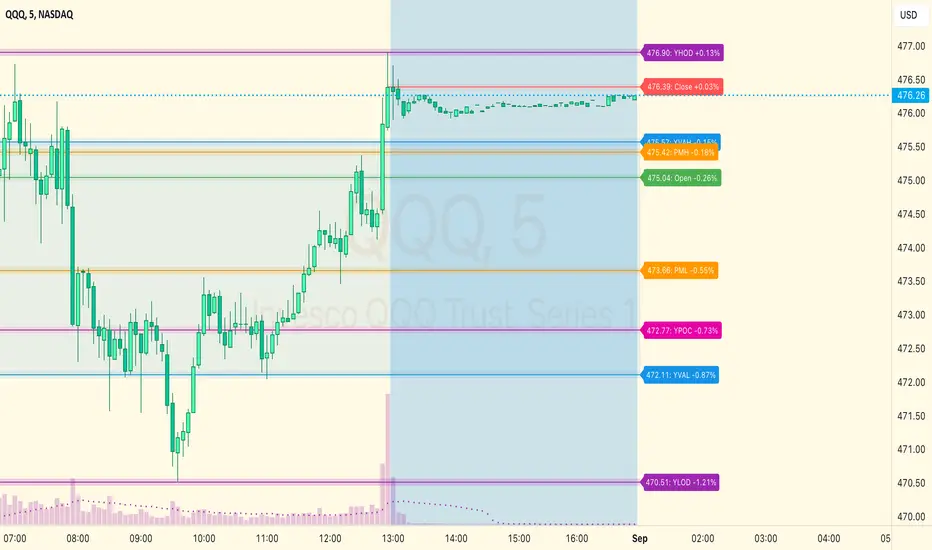

VWAP Momentum Oscillator How It Works

Core Calculation Method

The oscillator combines four key market measurements into a single, normalized reading:

1. Price-VWAP Deviation: `(Close - VWAP) / VWAP × 100`

2. VWAP-MA Momentum: `(VWAP - MovingAverage) / MovingAverage × 100`

3. Anchored VWAP Strength: Average of high/low anchor deviations from rolling VWAP

4. Range Position: `(Close - PeriodLow) / (PeriodHigh - PeriodLow) × 100 - 50`

Dynamic Signal Line

The signal line uses an EMA that automatically adjusts its length based on your chart timeframe:

- Futures: Always covers 23 hours of trading (1,380 minutes)

- Stocks: Always covers 6.5 hours of trading (390 minutes)

- Examples: 276 periods on 5-min futures chart, 1,380 periods on 1-min futures chart

Trading Signals

🟢 Buy Signals

- Condition: Main oscillator crosses above signal line while below zero

- Logic: Momentum turning bullish from oversold conditions

- Visual: Green "BUY" label below price action

🔴 Sell Signals

- Condition: Main oscillator crosses below signal line while above zero

- Logic: Momentum turning bearish from overbought conditions

- Visual: Red "SELL" label above price action

⚠️ Extreme Warnings

- Extreme Overbought: Red triangle when oscillator crosses above +4.0

- Extreme Oversold: Green triangle when oscillator crosses below -4.0

- Purpose: Risk management alerts, not entry/exit signals

Oscillator Zones

Interpretation Guide

- Above +2.0: Strong bullish momentum zone (green background)

- 0 to +2.0: Mild bullish territory

- 0 to -2.0: Mild bearish territory

- Below -2.0: Strong bearish momentum zone (red background)

- Above +4.0: Extreme overbought (caution advised)

- Below -4.0: Extreme oversold (potential reversal zone)

Customization Options

Moving Average Settings

- EMA/SMA Toggle: Choose between exponential or simple moving average

- Color Customization: Adjust MA line color and width

Visual Controls

- Bullish/Bearish Colors: Customize momentum zone colors

- Signal Line: Toggle visibility and adjust color

- Line Widths: Control thickness of all plot lines

Anchor Modes

- NY Session Only: Anchors reset at NY market open (9:30 AM ET)

- 24H NY Day: Anchors reset at NY calendar day change (midnight ET)

Best Practices

Timeframe Selection

- Scalping: 1-5 minute charts for quick momentum changes

- Day Trading: 5-15 minute charts for clearer trend signals

- Swing Trading: 1-4 hour charts for major momentum shifts

Signal Confirmation

- Wait for crossovers: Don't trade on oscillator position alone

- Respect extreme levels: Exercise caution above +4 or below -4

- Use with price action: Combine with support/resistance levels

Risk Management

- Extreme zones: Reduce position size when oscillator is extended

- Failed signals: Exit quickly if momentum doesn't follow through

- Market context: Consider overall trend direction and market volatility

Technical Specifications

Calculation Components

- Base Length: 1,380 periods (futures) / 390 periods (stocks)

- Signal Line: Dynamic EMA covering one full trading day

- Smoothing: 3-period SMA on raw oscillator (adjustable)

- Update Frequency: Real-time on every price tick

Performance Notes

- Resource Efficient: Optimized calculations minimize CPU usage

- Memory Friendly: Uses incremental VWAP calculations

- Fast Loading: Minimal historical data requirements

Version History & Development

This oscillator evolved from advanced VWAP overlay strategies, transforming complex multi-line analysis into a single, actionable momentum gauge. The indicator maintains the sophistication of institutional VWAP analysis while providing the clarity needed for retail trading decisions.

Core Philosophy

Traditional VWAP indicators show where price is relative to volume-weighted averages, but they don't quantify momentum or provide clear entry/exit signals. This oscillator solves that problem by normalizing all VWAP relationships into a single, bounded indicator that works consistently across all timeframes and asset classes.

---

Open Source License: This indicator is provided free for the TradingView community. Feel free to modify and enhance according to your trading needs.

Commitment of Traders: Legacy Metrics█ OVERVIEW

This indicator displays the Commitment of Traders (COT) legacy data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents data from the legacy report, which is broken down by exchange. Legacy reports break down the reportable open interest positions into two classifications: non-commercial and commercial traders.

Our other COT indicators are:

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Financial Metrics

• Commitment of Traders: Total

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

Metric

Each metric represents a different column of the Commitment of Traders report. Details are available in the explanatory notes on the CFTC's website .

Here is a summary of the metrics:

• "Open Interest" is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc.

The aggregate of all long open interest is equal to the aggregate of all short open interest.

• "Traders Total" is the number of all unique reportable traders, regardless of the trading direction.

• "Traders Total Reportable/Traders Noncommercial/Traders Commercial" are the quantities of traders reported to hold any position with the specified direction.

All of a trader's reported futures positions in a commodity are classified as commercial if the trader uses futures contracts in that particular commodity for hedging.

To determine the total number of reportable traders in a market, a trader is counted only once, whether or not the trader appears in more than one category.

• "Total Reportable/Noncommercial/Commercial Positions" are all positions held by all reportable/non-commercial/commercial traders.

• "Non-reportable Positions" is derived by subtracting total long and short "Reportable Positions" from the total open interest.

Accordingly, the number of traders involved and the commercial/non-commercial classification of each trader are unknown.

• "Concentration Gross/Net LT 4/8 TDR" is the percentage of open interest held by 4/8 of the largest traders, by gross/net positions,

without regard to whether they are classified as commercial or non-commercial. The Net position ratios are computed after offsetting each trader’s equal long and short positions.

A reportable trader with relatively large, balanced long and short positions in a single market, therefore,

may be among the four and eight largest traders in both the gross long and gross short categories, but will probably not be included among the four and eight largest traders on a net basis.

Direction

Each metric is available for a particular set of directions. Valid directions for each metric are specified with its name in the "Metric" field's dropdown menu.

Type

Possible values are: All, Old, Other. When commodities have a well-defined marketing season or crop year (e.g. Wheat or Lean Hogs futures), this determines how the data is aggregated. Detailed explanation can be found in the "Old and Other Futures" section of the CTFC Explanatory Notes linked above. The "Major Markets for Which the COT Data Is Shown by Crop Year" table in the Explanatory Notes specifies the commodities that this distinction applies to; selecting "Old" for any of the commodities not in that list will return the same data as in "All", while selecting "Other" will return 0.

COT Selection Mode

This field's value determines how the script determines which COT data to return from the chart's symbol:

- "Root" uses the root of a futures symbol ("ES" for "ESH2020").

- "Base currency" uses the base currency in a forex pair ("EUR" for "EURUSD").

- "Currency" uses the quote currency, i.e., the currency the symbol is traded in ("JPY" for "TSE:9984" or "USDJPY").

- "Auto" tries all modes, in turn.

If no COT data can be found, a runtime error is generated.

Note that if the "CTFC Code" input field contains a code, it will override this input.

Futures/Options

Specifies the type of Commitment of Traders data to display: data concerning only Futures, only Options, or both.

CTFC Code

Instead of letting the script generate the CFTC COT code from the chart and the "COT Selection Mode" input when this field is empty, you can specify an unrelated CFTC COT code here, e.g., 001602 for wheat futures.

Look first. Then leap.

Commitment of Traders: Disaggregated Metrics█ OVERVIEW

This indicator displays the Commitment of Traders (COT) Disaggregated data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents data from the Disaggregated report. The disaggregated reports are broken down by agriculture, petroleum and products, natural gas and products, electricity and metals and other physical contracts. The Disaggregated reports break down the reportable open interest positions into four classifications: Producer/Merchant/Processor/User, Swap Dealers, Managed Money, and Other Reportables.

Our other COT indicators are:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Financial Metrics

• Commitment of Traders: Total

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

Metric

Each metric represents a different column of the Commitment of Traders report. Details are available in the explanatory notes on the CFTC's website .

Here is a summary of the metrics:

• "Open Interest" is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc.

The aggregate of all long open interest is equal to the aggregate of all short open interest.

• "Traders Total" is the quantity of all unique reportable traders, regardless of the trading direction.

• "Traders Producer Merchant" is the number of traders classified as a "producer/merchant/processor/user" reported holding any position with the specified direction.

A "producer/merchant/processor/user" is an entity that predominantly engages in the production, processing, packing or handling of a physical commodity and

uses the futures markets to manage or hedge risks associated with those activities.

• "Traders Swap" is the number of traders classified as "swap dealers" reported holding any position with the specified direction.

A "swap dealer" is an entity that deals primarily in swaps for a commodity and uses the futures markets to manage or hedge the risk associated with those swaps transactions.

The swap dealer’s counterparties may be speculative traders, like hedge funds, or traditional commercial clients that are managing risk arising from their dealings in the physical commodity.