Portfolio Index Generator [By MUQWISHI]▋ INTRODUCTION:

The “Portfolio Index Generator” simplifies the process of building a custom portfolio management index, allowing investors to input a list of preferred holdings from global securities and customize the initial investment weight of each security. Furthermore, it includes an option for rebalancing by adjusting the weights of assets to maintain a desired level of asset allocation. The tool serves as a comprehensive approach for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investment. The output includes an index value, a table of holdings, and chart plotting, providing a deeper understanding of the portfolio's historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom portfolio index. I created this index and named it “My Portfolio Performance”, which comprises several global companies and crypto assets.

_______________________

▋ OUTPUTS:

The output can be divided into 4 sections:

1. Portfolio Index Title (Name & Value).

2. Portfolio Specifications.

3. Portfolio Holdings.

4. Portfolio Index Chart.

1. Portfolio Index Title, displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Portfolio Specifications, displays the essential information on portfolio performance, including the investment date range, initial capital, returns, assets, and equity.

3. Portfolio Holdings, a list of the holding securities inside a table that contains the ticker, average entry price, last price, return percentage of the portfolio's initial capital, and customized weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Index Chart, display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Style Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Equity or Return (%)}, and the plot type for the index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any indicator’s components.

Section(2): Performance Settings

(1) Calculation window period: from DateTime to DateTime.

(2) Initial Capital and specifying currency.

(3) Option to enable portfolio rebalancing in {Monthly, Quarterly, or Yearly} intervals.

Section(3): Portfolio Holdings

(1) Enable and count security in the investment portfolio.

(2) Initial weight of security. For example, if the initial capital is $100,000 and the weight of XYZ stock is 4%, the initial value of the shares would be $4,000.

(3) Select and add up to 30 symbols that interested in.

Please let me know if you have any questions.

การจัดการพอร์ตการลงทุน

[KF] Sector & Industry RemappingThis script remaps TradingView's sector and industry categories to standard classifications and displays them in the top-right corner of the chart making it easy to quickly identify a security's sector and industry. This tool is useful for traders and analysts who prefer standard industry classifications while using TradingView's charts.

BB Position CalculatorPosition Size Calculator Instructions

Overview

The Position Size Calculator is designed to help traders automatically determine the appropriate lot size based on the dollar amount they are willing to risk. It includes features for automatic lot sizing, fixed lot risk calculations, take profit calculations (both automatic and fixed), max run-up, and max drawdown. Calculated values are displayed in ticks, points, and USD.

Key Features

• Automatic Lot Sizing: Automatically calculates lot size based on the amount of money you are willing to risk.

• Fixed Lot Risk Calculations: Provides risk calculations for fixed lot sizes.

• Take Profit Calculations: Offers both automatic and fixed take profit calculations.

• Max Run-Up and Max Drawdown: Monitors and displays the maximum run-up and drawdown of your trade.

• Detailed Metrics: Displays all calculated values in ticks, points, and USD.

Setup Instructions

1. Add and Remove for Each Position: The calculator is designed to be added to your chart for each new position. Once your preferences are set the first time, save them as your default to retain your settings for future use.

2. Adding the Indicator to Favorites:

• Use the TradingView keyboard shortcut “/” then type “pos.”

• Use the arrow key to select the Position Size Calculator and press enter.

• Close the indicator selection pop-up.

3. Setting the Trigger Price:

• A blue pop-up labeled “SET TRIGGER PRICE” will appear at the bottom of the chart.

• Click on the chart at the price level where you want to enter the trade.

4. Setting the Stop Loss:

• The pop-up will change to “SET STOP LOSS.”

• Click on the chart at the price level where your stop loss will be set.

5. Setting the Take Profit:

• The pop-up will change to “SET TAKE PROFIT.”

• Click on the chart at the price level where you want to take profit. If you have selected the option to overwrite with a set risk/reward ratio (R:R), the calculation will use this price level.

6. Setting the Trade Window Start:

• The pop-up will change to “SET TRADE WINDOW START.”

• Click on the bar in time where you want the indicator to start monitoring for price to trigger the position.

7. Adjusting the Position:

• Clicking on any part of the indicator will display draggable lines, allowing you to fine-tune the position that was previously plotted by the first four chart clicks.

Additional Notes

• Compatibility: This calculator has only been tested with futures trading.

• Customization: Once your preferences are set, save them as your default to make setup quicker for future trades.

• Support: If you have any questions or feature requests, please feel free to reach out.

SL ManagerSTOP LOSS MANAGER

Overview:

The "SL Manager" indicator is designed to assist traders in managing their stop loss (SL) and take profit (TP) levels for both long and short positions. This tool helps you visualize intermediate levels, enhancing your trading decisions by providing crucial information on the chart.

Usage:

This indicator is particularly useful for traders who want to manage their trades more effectively by visualizing potential adjustment points for their stop loss and take profit levels. It helps in making informed decisions to maximize profits and minimize risks by providing clear levels to take partial profits and adjust stop losses.

Features:

Position Input: Select between "long" and "short" positions.

Entry Price: Specify the entry price of your trade.

Take Profit: Define the price level at which you want to take profit.

Stop Loss: Set the stop loss price level to manage your risk.

Intermediate Levels:

For both long and short positions, the indicator calculates and plots the following intermediate levels:

50% Take Profit (TP 50%): Midway between the entry price and the take profit level, where you can take partial profits and move your SL up to the 25% mark.

75% Take Profit (TP 75%): Three-quarters of the way from the entry price to the take profit level, where you can take partial profits and move your SL to breakeven.

Stop Loss Move to 25% (SL Move to 25%): A level where the stop loss can be adjusted to lock in profits.

Visualization:

The indicator plots the calculated levels directly on the chart, provided the data for the current day is available. Different color codes and line styles distinguish between the various levels:

TP 50% and TP 75% are plotted in green.

SL Move to 25% is plotted in red .

Entry/Breakeven is plotted in blue.

Position Size CalculatorThe Position Size Calculator (PSC) is a comprehensive tool designed to assist traders in managing their trades risk by accurately calculating the optimal position size based on account settings, trade levels, and risk management parameters. This indicator helps traders make informed decisions by providing critical information about potential profit and loss , risk-reward ratio (RRR) , and position size (PS) .

█ Key Features

• Customizable Account Settings: Define your account size , currency , risk tolerance , and commission structure to personalize the calculations.

• Real-Time Trade Levels: Easily input your entry , stop loss , and take profit prices directly on the chart for immediate calculations.

• Visual Indicators: Clearly see your entry, stop loss, and take profit levels with customizable colors and labels.

• Comprehensive Position Information: View detailed information about your position, including potential profit and loss , risk-reward ratio , and position size .

• Currency Conversion: Automatically convert prices to your account currency, making it easy to manage trades in different markets.

• Hide Metrics : Choose which metrics to display to avoid emotional influence on your trading decisions (e.g., hiding PnL).

█ Conclusion

The Position Size Calculator is an essential tool for traders looking to optimize their trading strategies and manage risk effectively . By providing detailed calculations and visual indicators, this tool helps you make informed decisions, improving your overall trading performance.

█ Important

• Ensure that your stop loss and take profit levels are correctly set relative to your entry price to avoid errors.

• The default commission setting considers both entry and exit commissions. Adjust accordingly if only one commission is applicable.

Consider using this tool to manage every trade risk correctly and prevent significant drawdowns.

Hope you like it. Happy trading!

SP500 Earnings Yield Spread: SP500 vs 3 Month & 10 Year TreasuryAdd the SP500 ttm Earnings Yield Spreads vs the 3 Month and 10 Year Treasury Rates.

Short Spread = SP500 E/P ttm - 3 Month Treasury Rate

Long Spread = SP500 E/P ttm - 10 Year Treasury Rate

Symbol "SP500_EARNINGS_YIELD_MONTH" as the SP500 Earnings Yield

Symbol "US03MY" as the 3 Month Treasury Rate

Symbol "US10Y" as the 10 Year Treasury Rate

Based on research suggesting Earnings Yield and Interest Rates may have predictive power of future returns:

- Market-Timing Strategies That Worked? - Pu Shen

- Valuation Ratios and the Long-Run Stock Market Outlook - Campbell and Shiller

Inputs:

Short Term Spread - Line for Short Term Spread

Long Term Spread - Line for Long Term Spread

Zero Line - Horizontal line at 0

Color Lines Based on Spread - Color the spreads green/red if spread is positive/negative

Short 10th PCT - Line for Short Term Spread 10th percentile of historical values

Long 10th PCT - Line for Long Term Spread 10th percentile of historical values

Shade Below 10 PCT: Spread Must be Negative - Requirement the spread is negative to shade background

Shade Background Below Short 10th Percentile - Shade the background if the Short Term Spread is below its 10th percentile. (and spread is negative if input above chosen)

Shade Background Below Long 10th Percentile - Shade the background if the Long Term Spread is below its 10th percentile. (and spread is negative if input above chosen)

Several Fundamentals in One [aep]

**Financial Ratios Indicator**

This comprehensive Financial Ratios Indicator combines various essential metrics to help traders and investors evaluate the financial health of companies at a glance. The following categories are included:

### Valuation Ratios

- **P/B Ratio (Price to Book Ratio)**: Assesses if a stock is undervalued or overvalued by comparing its market price to its book value.

- **P/E Ratio TTM (Price to Earnings Ratio Trailing Twelve Months)**: Indicates how many years of earnings would be needed to pay the current stock price by comparing the stock price to earnings per share over the last twelve months.

- **P/FCF Ratio TTM (Price to Free Cash Flow Ratio Trailing Twelve Months)**: Evaluates a company's ability to generate free cash flow by comparing the market price to free cash flow per share over the last twelve months.

- **Tobin Q Ratio**: Indicates whether the market is overvaluing or undervaluing a company’s assets by comparing market value to replacement cost.

- **Piotroski F-Score (0-9)**: A scoring system that identifies financially strong companies based on fundamental metrics.

### Efficiency

- **Net Margin % TTM**: Measures profitability by calculating the percentage of revenue that becomes net profit after all expenses and taxes.

- **Free Cashflow Margin %**: Indicates a company’s efficiency in generating free cash flow from its revenues by showing the percentage of revenue that translates into free cash flow.

- **ROE%, ROIC%, ROA%**: Evaluate a company’s efficiency in generating profits from equity, invested capital, and total assets, respectively.

### Liquidity Metrics

- **Debt to Equity Ratio**: Shows the level of debt relative to equity, helping assess financial leverage.

- **Current Ratio**: Measures a company's ability to pay short-term debts by comparing current assets to current liabilities.

- **Long Term Debt to Assets**: Evaluates the level of long-term debt in relation to total assets.

### Dividend Policy

- **Retention Ratio % TTM**: Indicates the proportion of earnings reinvested in the company instead of distributed as dividends.

- **Dividend/Earnings Ratio % TTM**: Measures the percentage of earnings paid out as dividends to shareholders.

- **RORE % TTM (Return on Retained Earnings)**: Assesses how effectively a company utilizes retained earnings to generate additional profits.

- **Dividend Yield %**: Indicates the dividend yield of a stock by comparing annual dividends per share to the current stock price.

### Growth Ratios

- **EPS 1yr Growth %**: Measures the percentage growth of earnings per share over the last year.

- **Revenue 1yr Growth %**: Evaluates the percentage growth of revenue over the last year.

- **Sustainable Growth Rate**: Indicates the growth rate a company can maintain without increasing debt, assessing sustainable growth using internal resources.

Utilize this indicator to streamline your analysis of financial performance and make informed trading decisions.

CAGR - Candle based BackTesterThe "CAGR - Candle based BackTester" is a tool for traders and investors seeking precise insights into individual candle performance!

Do you want to backtest based on candles and understand their CAGR? Curious about the average CAGR of all candles? Interested in comparing how an individual candle performs against others? Then this tool is your go-to solution.

How It Works:

Candle Selection: Specify a start date, and watch as the script tracks investments from that point forward.

Dynamic Calculations: Experience real-time CAGR calculations that adapt as market conditions evolve.

CAGR Display: At the final candle, gain insights into individual CAGR, average CAGR of all candles, alpha (difference), and outperformance percentage—all conveniently displayed for informed decision-making.

Key Features:

Accurate Candle-based CAGR Calculation: Gain clarity on investment performance with precise CAGR metrics.

Lumpsum Investment Tracking: Track lumpsum investments seamlessly with detailed share and investment calculations.

Outperformance Metrics: Measure how your investment performs relative to others with dedicated outperformance metrics.

User-Friendly Visualization: Access intuitive charts and visuals that simplify complex financial data.

ICT Market Structure Screener (Zeiierman)█ Overview

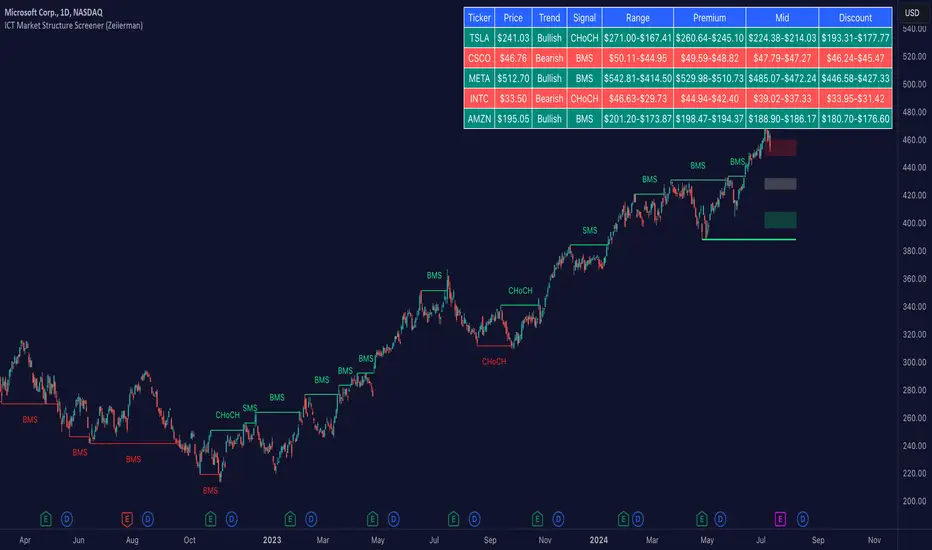

The ICT Market Structure Screener (Zeiierman) is designed to identify and display key market structure levels and patterns based on Smart Money Concepts. It highlights bullish and bearish structures, premium and discount levels, and generates alerts for significant market structure changes, making it a valuable tool for traders looking to understand institutional trading behaviors and market trends. A key feature of this indicator is its screener function, which allows traders to monitor multiple symbols simultaneously. This feature provides a consolidated view of the market structure for various assets, making it easier to identify trading opportunities across a diverse portfolio.

█ How It Works

The ICT Market Structure Screener operates by identifying high and low pivot points within a specified period, then analyzing these pivots to determine changes in market structure. The indicator tracks price movements and categorizes them into bullish or bearish structures, indicating potential trend reversals or continuations. By plotting premium and discount levels, it helps traders identify overbought and oversold conditions. The indicator also provides real-time updates and alerts for significant changes in the market structure.

█ Terminology

ChoCH (Change of Character): Indicates a potential reversal in market direction. It is identified when the price breaks a significant high or low, suggesting a shift from a bullish to bearish trend or vice versa.

SMS (Smart Money Shift): Represents the transition phase in market structure where smart money begins accumulating or distributing assets. It typically follows a BMS and indicates the start of a new trend.

BMS (Bullish/Bearish Market Structure): Confirms the trend direction. Bullish Market Structure (BMS) confirms an uptrend, while Bearish Market Structure (BMS) confirms a downtrend. It is characterized by a series of higher highs and higher lows (bullish) or lower highs and lower lows (bearish).

Premium: A zone where the price is considered overbought. It is calculated as the upper range of the current market structure and indicates a potential area for selling or shorting.

Mid Range: The midpoint between the high and low of the market structure. It often acts as a support or resistance level, helping traders identify potential reversal or continuation points.

Discount: A zone where the price is considered oversold. It is calculated as the lower range of the current market structure and indicates a potential area for buying or going long.

█ How to Use

The ICT Market Structure Screener allows traders to follow smart money moves in the market more effectively. By identifying key market levels and monitoring bullish and bearish structures, traders can easily spot trend changes and strong trends. The indicator's premium and discount levels help identify overbought and oversold conditions, providing valuable entry and exit points. Alerts for ChoCH, SMS, and BMS keep traders informed about significant market changes, enabling real-time adjustments to trading strategies.

The screener functionality is particularly valuable for monitoring multiple markets simultaneously. The screener table displays critical information such as current price, trend direction, signal type, and premium/discount levels for each symbol. This makes it easier to track the market structure of various assets at a glance and quickly identify trading opportunities across different markets.

Example Strategies:

⚪ Trend Following: Use the indicator to identify the current market trend (bullish or bearish) and trade in the direction of the trend. Enter trades on pullbacks to premium (for shorts) or discount (for longs) levels.

⚪ Reversal Trading: Look for ChoCH signals to identify potential trend reversals. Enter trades when the price breaks a significant high or low and confirms a change in market structure, or wait for a retest of the nearest Orderblock that was formed.

⚪ Support and Resistance: Utilize the mid-range, premium, and discount levels as support and resistance zones. Enter trades when the price approaches these levels and shows signs of reversal or continuation.

⚪ Multi-Symbol Analysis: Use the screener table to monitor multiple symbols and quickly assess their market structure. This helps in diversifying trading opportunities and managing a portfolio of assets efficiently.

█ Settings

Period: The pivot period for calculating the structure. Increasing the period captures broader trends, making the structure more representative of long-term movements. Decreasing the period focuses on shorter-term trends, increasing sensitivity.

Response: Enabling this option uses the response period instead of the pivot period, providing more flexibility in capturing short-term or long-term structures. The period for the response, which determines the structure's sensitivity. Increasing the response period smoothens the structure, making it less reactive to short-term fluctuations. Decreasing the response period makes the structure more responsive to short-term changes.

Structure Display: Choose between displaying the active range or the previous range. 'Active Range' shows real-time premium, discount, and mid-range levels based on the current structure. 'Previous Range' displays past ranges, useful for analyzing historical support/resistance levels.

Ticker Symbols: List of symbols to include in the screener. Enabling the option includes the symbol in the screener, allowing the user to track its structure. Disabling it excludes the symbol from the screener, reducing the number of tracked symbols.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Nebula SAR Echo📈 Overview:

The "Nebula SAR Echo" is a sophisticated technical analysis tool designed for traders seeking enhanced trend detection. This indicator combines the robust Parabolic SAR mechanism with gradient color coding to provide clear visual insights into market trends.

🎯 Key Features:

Advanced Parabolic SAR Calculation:

Utilizes dynamic coefficients for more responsive and accurate trend detection.

Highlights trend reversals with visual markers for immediate identification.

Gradient Color Coding:

Gradient colors dynamically reflect the strength and direction of the trend.

Bullish trends are represented in shades of green, while bearish trends are shown in shades of red.

User-Friendly Customization:

Easily adjustable parameters for acceleration factors and gradient color use.

💡 Benefits:

Enhanced Decision Making:

Combines real-time trend analysis to assist traders in making more informed decisions.

Visual Clarity:

Clear visual markers and gradient color coding simplify the interpretation of market trends.

Helps traders quickly identify key turning points and potential future price paths.

🔍 Use Cases:

Trend Identification:

Ideal for identifying ongoing trends and potential reversals in various market conditions.

Useful for both short-term trading strategies and long-term investment planning.

Risk Management:

Gradient color coding aids in assessing trend strength and potential volatility.

Traders can set more precise stop-loss and take-profit levels based on the trend strength.

⚙️ How to Use:

1. Parameter Setup:

Set the desired acceleration factors (start, increment, and max) for the Parabolic SAR.

Enable or disable gradient colors based on personal preference.

2. Interpretation:

Use the SAR values and gradient colors to gauge current market trends.

3. Alerts:

Set up alert conditions for bullish and bearish reversals to stay notified of significant market changes.

🔹 Conclusion:

The "Nebula SAR Echo" is a versatile and powerful tool for traders who require an in-depth analysis of market trends. By leveraging the advanced Parabolic SAR calculation and gradient color coding, this indicator provides a comprehensive view of market conditions, making it an indispensable addition to any trader's toolkit.

Easy Scalping Lot Calculator for ForexThe calculator was created to make it easier to calculate the lot size on Forex. I planned to use it for the following pairs: AUDCAD, AUDCHF, AUDJPY, AUDUSD, EURAUD, EURCAD, EURCHF, EURGBP, EURJPY, EURNZD, EURUSD, GBPCHF, GBPJPY, GBPUSD, NZDUSD, USDCAD, USDCHF, USDJPY, XAUUSD.

The indicator is a table that shows the calculation of the lot for a predetermined stop loss.

For example, you are planning a trade, have calculated a stop loss of 15 points, and by checking the table you understand approximately what lot you need to use to limit your risk.

In the settings you can change the risk and also determine the stop loss value in points.

The calculator does not take into account the spread in the calculations.

There are websites where you can accurately calculate the lot, but if you trade on small time frames this is not suitable for you.

The calculator uses the formula:

Lot size = maximum risk / stop loss (in pips) / minimum pip value x minimum trading lot.

Position Size Calculator for ContractDescription:

Position Size Calculator is a versatile Pine Script tool designed to help traders manage their risk and position sizing effectively. This script calculates essential trading metrics and visualizes them directly on your chart, helping you make informed trading decisions.

Features:

- Account Size & Risk Management:

- Account Size: Input your total account balance to calculate position sizes.

- Maximum Risk: Define how much of your account you are willing to risk per trade in dollars.

- Pip Value: Set the value of a single pip for one contract, which is crucial for calculating risk

and position size.

Trade Setup Visualization:

- Entry Price: Specify the price at which you plan to enter the trade.

- Stop Loss: Define your stop loss level to manage your risk.

- Take Profit: Set your target profit level for the trade.

- Visualize the Entry, Stop Loss, and Take Profit levels on your chart with customizable line

colors and text sizes.

- View the distance in pips between the Entry, Stop Loss, and Take Profit levels.

Position Size Calculation:

- Calculates the number of contracts to open based on your risk tolerance and the pip value.

- Displays the maximum number of contracts you can open given your risk parameters.

Customizable Table Display:

- Table Position: Choose the position of the summary table on the chart (Top-Left, Top-Right,

Bottom-Left, Bottom-Right, etc.).

- Table Text Size: Adjust the text size for the summary table.

- Table Background Color: Set the background color for the summary table.

- Table Border Color: Customize the border color of the summary table.

How to Use:

1- Input your Account Size: Enter your current account balance.

2- Set Maximum Risk and Pip Value: Define how much you're willing to risk per trade and the

pip value for your contract.

3- Define Trade Levels: Input your desired Entry Price, Stop Loss, and Take Profit levels.

4- Customize Visuals: Adjust the line styles and table settings to fit your preferences.

5- View Calculations: The script will display the distance in pips and the calculated position

size directly on your chart.

Example Usage:

Example to calculate the value of 1 pips with 1 contract:

Inputs:

Account Size: Your total trading account balance.

Maximum Risk: Risk amount per trade in dollars.

Pip Value: Value of one pip for a single contract.

Entry Price: The price at which you plan to enter the trade.

Stop Loss: The level at which you will exit the trade to cut losses.

Take Profit: The target price to lock in profits.

Line Text Size: Size of the text for the Entry, Stop Loss, and Take Profit lines.

Line Extend: Option to extend the lines for visual clarity.

Table Position: Position of the summary table on the chart.

Table Text Size: Size of the text in the summary table.

Table Background Color: Background color of the summary table.

Table Border Color: Border color of the summary table.

Visuals:

Entry Price, Stop Loss, and Take Profit levels are clearly marked on the chart.

Summary Table with important trade metrics displayed.

[INVX] Trailing StopDescription:

The Adjustable Trailing Stop Indicator is a practical tool designed to enhance your trading strategy by allowing for automatic modifications of stop-loss orders according to your specified parameters. This indicator provides a dynamic alternative to the traditional static stop-loss orders, assisting in managing your potential profits and curbing possible losses.

Features and Functionality:

The Trailing Stop Indicator provides three main inputs for customization:

"Trailing Stop Start Date" : This input enables you to set the start date for the trailing stop. From this date forward, the indicator begins tracking price changes and adjusts the stop-loss order in response.

"Trigger Delta (%)" : This represents the percentage for the trailing stop. It denotes the set percentage at which the stop order adjusts.

"Order" : This input determines whether the trailing stop applies to a Buy or Sell order. Depending on the selection, the indicator adjusts the stop price as the price escalates (for Sell order) or declines (for Buy order).

How Does the Trailing Stop Indicator Work?

The Trailing Stop Indicator functions by dynamically adjusting the stop price in line with market fluctuations. If the market price rises (for Sell order), the stop price automatically ascends, securing potential profits. In a declining market (for Buy order), the stop price descends according to the market.

This indicator eliminates the need for constant manual adjustments, reducing the impact of emotional trading and helping traders maintain their risk management strategy. By using this tool, traders can implement a more disciplined and systematic approach to trading.

BTC outperform atrategy### Code Description

This Pine Script™ code implements a simple trading strategy based on the relative prices of Bitcoin (BTC) on a weekly and a three-month basis. The script plots the weekly and three-month closing prices of Bitcoin on the chart and generates trading signals based on the comparison of these prices. The code can also be applied to Ethereum (ETH) with similar effectiveness.

### Explanation

1. **Inputs and Variables**:

- The user selects the trading symbol (default is "BINANCE:BTCUSDT").

- `weeklyPrice` retrieves the closing price of the selected symbol on a weekly interval.

- `monthlyPrice` retrieves the closing price of the selected symbol on a three-month interval.

2. **Plotting Data**:

- The weekly price is plotted in blue.

- The three-month price is plotted in red.

3. **Trading Conditions**:

- A long position is suggested if the weekly price is greater than the three-month price.

- A short position is suggested if the three-month price is greater than the weekly price.

4. **Strategy Execution**:

- If the long condition is met, the strategy enters a long position.

- If the short condition is met, the strategy enters a short position.

This script works equally well for Ethereum (ETH) by changing the symbol input to "BINANCE:ETHUSDT" or any other desired Ethereum trading pair.

Analyst Table (Zeiierman)█ Overview

The Analyst Table (Zeiierman) provides a comprehensive visual representation of analyst estimates and recommendations for any stock. This indicator displays crucial analyst data, including the highest, average, and lowest price targets, directly on the price chart. Additionally, it features a well-organized table summarizing various types of analyst recommendations, offering traders valuable insights into market sentiment and expectations. This tool is ideal for traders seeking a quick overview of analyst opinions and recommendations on specific stocks.

█ How It Works

The indicator works by retrieving analyst data such as price targets and recommendations from the TradingView data feed. It visually represents these estimates on the chart and creates a structured table for easy reference, consolidating all the information in an organized format.

Key Components:

High Estimate Line: A dotted line representing the highest price target.

Low Estimate Line: A dotted line representing the lowest price target.

Target Estimate Box: A box representing the range between the average and median price targets.

Analyst Table: A table displaying detailed information about various analyst recommendations and price targets.

█ How to Use

Traders can use this indicator to gain insights into the expectations of financial analysts regarding the future performance of an asset. By observing the highest, lowest, and average price targets, traders can assess the range of possible future prices as predicted by analysts. The recommendation table helps in understanding the general sentiment among analysts, whether it's bullish, bearish, or neutral.

Visual Analysis: Use the visual indicators to quickly gauge where the current price stands relative to analyst targets.

Sentiment Assessment: Refer to the table to understand the distribution of buy, hold, and sell recommendations.

█ Settings

The indicator settings allow users to enable or disable different target lines, select colors for the lines and table cells, and choose the position and size of the analyst table on the chart.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Long/Short Entry with Customizable TP/SLThis TradingView indicator is designed to help traders visualize potential trade entries along with their corresponding stop-loss (SL) and take-profit (TP) levels. It offers a high degree of customization, allowing users to:

Choose Entry Type: Select whether the anticipated trade is a Long or Short position.

Set Entry Price: Specify the exact price level at which you intend to enter the trade.

Customize TP/SL:

Enable/Disable: Choose whether to include a stop-loss (SL) and up to five take-profit (TP) levels.

Distance: Set the distance (in price points) for each SL and TP level from the entry price.

Add/Update Trade: Clicking the "Add/Update Trade" button will plot the entry line, SL line (if enabled), and TP lines (if enabled) on the chart, along with their corresponding labels. The lines and boxes will start two candles before the current bar and extend into the future.

Reset Trade: Clicking the "Reset Trade" button will clear all the lines, boxes, and labels from the chart, allowing you to start fresh with a new trade idea.

Visual Cues:

The indicator uses color-coded lines and boxes to distinguish between entry, SL, and TP levels.

Labels are provided next to each line, displaying the type of level (e.g., "Entry," "SL," "TP1") and its corresponding price.

Key Features:

Highly Customizable: Tailor the indicator to your specific trading style and risk management preferences.

Visual Clarity: Clearly visualize potential trade setups and their outcomes.

Easy to Use: The intuitive interface makes it simple to add, update, and reset trades.

Flexibility: Supports both long and short positions.

Limitations:

The indicator is designed for visualization and planning purposes only. It does not automatically execute trades.

The simulated "Add Trade" and "Reset Trade" buttons require manual unchecking after each click.

Rolling Correlation with Bitcoin V1.1 [ADRIDEM]Overview

The Rolling Correlation with Bitcoin script is designed to offer a comprehensive view of the correlation between the selected ticker and Bitcoin. This script helps investors understand the relationship between the performance of the current ticker and Bitcoin over a rolling period, providing insights into their interconnected behavior. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Bitcoin Comparison : Allows users to compare the correlation of the current ticker with Bitcoin, providing an analysis of their relationship.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the correlation coefficient, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 4 bars.

Visual Indicators : Plots the smoothed correlation coefficient between the current ticker and Bitcoin, with distinct colors for easy interpretation. Additionally, horizontal lines help identify key levels of correlation.

Dynamic Background Color : Adds dynamic background colors to highlight areas of strong positive and negative correlations, enhancing visual clarity.

Originality and Usefulness

This script uniquely combines the analysis of rolling correlation for a current ticker with Bitcoin, providing a comparative view of their relationship. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the correlation between the assets:

Rolling Correlation with Bitcoin : Plotted as a red line, this represents the smoothed rolling correlation coefficient between the current ticker and Bitcoin.

Horizontal Lines and Background Color : Lines at -0.5, 0, and 0.5 help to quickly identify regions of strong negative, weak, and strong positive correlations.

These features assist in identifying the strength and direction of the relationship between the current ticker and Bitcoin.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling correlation coefficient. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 4.

Bitcoin Ticker (`bitcoin_ticker`) : The ticker symbol for Bitcoin. Default is "BINANCE:BTCUSDT".

Functionality

Correlation Calculation : The script calculates the daily returns for both Bitcoin and the current ticker and computes their rolling correlation coefficient.

```pine

bitcoin_close = request.security(bitcoin_ticker, timeframe.period, close)

bitcoin_dailyReturn = ta.change(bitcoin_close) / bitcoin_close

current_dailyReturn = ta.change(close) / close

rolling_correlation = ta.correlation(current_dailyReturn, bitcoin_dailyReturn, length)

```

Smoothing : A simple moving average is applied to the rolling correlation coefficient to smooth the data.

```pine

smoothed_correlation = ta.sma(rolling_correlation, smoothing_length)

```

Plotting : The script plots the smoothed rolling correlation coefficient and includes horizontal lines for key levels.

```pine

plot(smoothed_correlation, title="Rolling Correlation with Bitcoin", color=color.rgb(255, 82, 82, 50), linewidth=2)

h_neg1 = hline(-1, "-1 Line", color=color.gray)

h_neg05 = hline(-0.5, "-0.5 Line", color=color.red)

h0 = hline(0, "Zero Line", color=color.gray)

h_pos05 = hline(0.5, "0.5 Line", color=color.green)

h1 = hline(1, "1 Line", color=color.gray)

fill(h_neg1, h_neg05, color=color.rgb(255, 0, 0, 90), title="Strong Negative Correlation Background")

fill(h_neg05, h0, color=color.rgb(255, 165, 0, 90), title="Weak Negative Correlation Background")

fill(h0, h_pos05, color=color.rgb(255, 255, 0, 90), title="Weak Positive Correlation Background")

fill(h_pos05, h1, color=color.rgb(0, 255, 0, 90), title="Strong Positive Correlation Background")

```

How to Use

Configuring Inputs : Adjust the rolling window length and smoothing length as needed. Ensure the Bitcoin ticker is set to the desired asset for comparison.

Interpreting the Indicator : Use the plotted correlation coefficient and horizontal lines to assess the strength and direction of the relationship between the current ticker and Bitcoin.

Signal Confirmation : Look for periods of strong positive or negative correlation to identify potential co-movements or divergences. The background colors help to highlight these key levels.

This script provides a detailed comparative view of the correlation between the current ticker and Bitcoin, aiding in more informed decision-making by highlighting the strength and direction of their relationship.

Rolling Calmar Ratio with Ref Ticker V1.0 [ADRIDEM]Overview

The Rolling Calmar Ratio with Ref Ticker script is designed to offer a comprehensive view of the Calmar ratios for a selected reference ticker and the current ticker. This script helps investors compare risk-adjusted returns between two assets over a rolling period, providing insights into their relative performance and risk. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Reference Ticker Comparison : Allows users to compare the Calmar ratio of the current ticker with a reference ticker, providing a relative performance analysis. Default ticker is BTCUSDT but can be changed.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the Calmar ratios, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 14 bars.

Visual Indicators : Plots the smoothed Calmar ratios for both the reference ticker and the current ticker, with distinct colors for easy comparison. Additionally, a horizontal line helps identify key levels.

Dynamic Background Color : Adds a gray-blue transparent background between the Calmar ratio levels of 0 and 1, highlighting the critical region where risk-adjusted returns are assessed.

Originality and Usefulness

This script uniquely combines the analysis of Calmar ratios for a reference ticker and the current ticker, providing a comparative view of their risk-adjusted returns. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the risk-adjusted returns of the assets:

Reference Ticker Calmar Ratio : Plotted as a red line, this represents the smoothed Calmar ratio for the user-selected reference ticker.

Current Ticker Calmar Ratio : Plotted as a white line, this represents the smoothed Calmar ratio for the current ticker.

Horizontal Lines and Background Color : A line at 0 helps to quickly identify the regions of positive and negative risk-adjusted returns.

These features assist in identifying relative performance differences and confirming the strength or weakness of risk-adjusted returns between the two tickers.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling Calmar ratio. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 14.

Reference Ticker (`ref_ticker`) : The ticker symbol for the reference asset. Default is "BINANCE:BTCUSDT".

Functionality

Calmar Ratio Calculation : The script calculates the cumulative returns and maximum drawdown for both the reference ticker and the current ticker. These values are used to compute the Calmar ratio.

```pine

ref_cumulativeReturn = (ref_close / ta.valuewhen(ta.lowest(ref_close, length) == ref_close, ref_close, 0)) - 1

ref_rollingMax = ta.highest(ref_close, length)

ref_drawdown = (ref_close - ref_rollingMax) / ref_rollingMax

ref_maxDrawdown = ta.lowest(ref_drawdown, length)

ref_calmarRatio = ref_cumulativeReturn / math.abs(ref_maxDrawdown)

current_cumulativeReturn = (close / ta.valuewhen(ta.lowest(close, length) == close, close, 0)) - 1

current_rollingMax = ta.highest(close, length)

current_drawdown = (close - current_rollingMax) / current_rollingMax

current_maxDrawdown = ta.lowest(current_drawdown, length)

current_calmarRatio = current_cumulativeReturn / math.abs(current_maxDrawdown)

```

Smoothing : A simple moving average is applied to the Calmar ratios to smooth the data.

```pine

smoothed_ref_calmarRatio = ta.sma(ref_calmarRatio, smoothing_length)

smoothed_current_calmarRatio = ta.sma(current_calmarRatio, smoothing_length)

```

Plotting : The script plots the smoothed Calmar ratios for both the reference ticker and the current ticker, along with a horizontal line.

```pine

plot(smoothed_ref_calmarRatio, title="Ref Ticker Calmar Ratio", color=color.rgb(255, 82, 82, 50), linewidth=2)

plot(smoothed_current_calmarRatio, title="Current Ticker Calmar Ratio", color=color.white, linewidth=2)

h0 = hline(0, "Zero Line", color=color.gray)

fill(h0, h1, color=color.rgb(33, 150, 243, 90), title="Background")

```

How to Use

Configuring Inputs : Adjust the detection length and smoothing length as needed. Set the reference ticker to the desired asset for comparison.

Interpreting the Indicator : Use the plotted Calmar ratios and horizontal line to assess the relative risk-adjusted returns of the reference and current tickers.

Signal Confirmation : Look for differences in the Calmar ratios to identify potential performance advantages or weaknesses. The horizontal line helps to highlight key levels of risk-adjusted returns.

This script provides a detailed comparative view of risk-adjusted returns, aiding in more informed decision-making by highlighting key differences between the reference ticker and the current ticker.

Rolling Sortino Ratio with Ref Ticker V1.0 [ADRIDEM]Overview

The Rolling Sortino Ratio with Ref Ticker script is designed to offer a comprehensive view of the Sortino ratios for a selected reference ticker and the current ticker. This script helps investors compare risk-adjusted returns between two assets over a rolling period, providing insights into their relative performance and risk. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Reference Ticker Comparison : Allows users to compare the Sortino ratio of the current ticker with a reference ticker, providing a relative performance analysis. Default ticker is BTCUSDT but can be changed.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the Sortino ratios, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 4 bars.

Visual Indicators : Plots the smoothed Sortino ratios for both the reference ticker and the current ticker, with distinct colors for easy comparison. Additionally, horizontal lines and a shaded background help identify key levels.

Dynamic Background Color : Adds a gray-blue transparent background between the Sortino ratio levels of 0 and 1, highlighting the critical region where risk-adjusted returns are assessed.

Originality and Usefulness

This script uniquely combines the analysis of Sortino ratios for a reference ticker and the current ticker, providing a comparative view of their risk-adjusted returns. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the risk-adjusted returns of the assets:

Reference Ticker Sortino Ratio : Plotted as a red line, this represents the smoothed Sortino ratio for the user-selected reference ticker.

Current Ticker Sortino Ratio : Plotted as a white line, this represents the smoothed Sortino ratio for the current ticker.

Horizontal Lines and Background Color : Lines at 0 and 1, along with a shaded background between these levels, help to quickly identify the regions of positive and strong risk-adjusted returns.

These features assist in identifying relative performance differences and confirming the strength or weakness of risk-adjusted returns between the two tickers.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling Sortino ratio. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 4.

Annual Risk-Free Rate (`riskFreeRate`) : The annual risk-free rate used in the Sortino ratio calculation. Default is 0.02 (2%).

Reference Ticker (`ref_ticker`) : The ticker symbol for the reference asset. Default is "BINANCE:BTCUSDT".

Functionality

Sortino Ratio Calculation : The script calculates the daily returns, mean return, and downside deviation for both the reference ticker and the current ticker. These values are used to compute the annualized Sortino ratio.

```pine

ref_dailyReturn = ta.change(ref_close) / ref_close

ref_meanReturn = ta.sma(ref_dailyReturn, length)

ref_downsideDeviation = ta.stdev(math.min(ref_dailyReturn, 0), length)

ref_annualizedReturn = ref_meanReturn * length

ref_annualizedDownsideDev = ref_downsideDeviation * math.sqrt(length)

ref_sortinoRatio = (ref_annualizedReturn - riskFreeRate) / ref_annualizedDownsideDev

```

Smoothing : A simple moving average is applied to the Sortino ratios to smooth the data.

```pine

smoothed_ref_sortinoRatio = ta.sma(ref_sortinoRatio, smoothing_length)

smoothed_current_sortinoRatio = ta.sma(current_sortinoRatio, smoothing_length)

```

Plotting : The script plots the smoothed Sortino ratios for both the reference ticker and the current ticker, along with horizontal lines and a shaded background.

```pine

plot(smoothed_ref_sortinoRatio, title="Ref Ticker Sortino Ratio", color=color.rgb(255, 82, 82, 50), linewidth=2)

plot(smoothed_current_sortinoRatio, title="Current Ticker Sortino Ratio", color=color.white, linewidth=2)

h0 = hline(0, "Zero Line", color=color.gray)

h1 = hline(1, "One Line", color=color.gray)

fill(h0, h1, color=color.rgb(33, 150, 243, 90), title="Background")

```

How to Use

Configuring Inputs : Adjust the detection length, smoothing length, and risk-free rate as needed. Set the reference ticker to the desired asset for comparison.

Interpreting the Indicator : Use the plotted Sortino ratios and background shading to assess the relative risk-adjusted returns of the reference and current tickers.

Signal Confirmation : Look for differences in the Sortino ratios to identify potential performance advantages or weaknesses. The background shading helps to highlight key levels of risk-adjusted returns.

This script provides a detailed comparative view of risk-adjusted returns, aiding in more informed decision-making by highlighting key differences between the reference ticker and the current ticker.

Rolling Sharpe Ratio with Ref Ticker V1.0 [ADRIDEM]Overview

The Rolling Sharpe Ratio with Ref Ticker script is designed to offer a comprehensive view of the Sharpe ratios for a selected reference ticker and the current ticker. This script helps investors compare risk-adjusted returns between two assets over a rolling period, providing insights into their relative performance and risk. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Reference Ticker Comparison : Allows users to compare the Sharpe ratio of the current ticker with a reference ticker, providing a relative performance analysis. Default ticker is BTCUSDT but can be changed.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the Sharpe ratios, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 4 bars.

Visual Indicators : Plots the smoothed Sharpe ratios for both the reference ticker and the current ticker, with distinct colors for easy comparison. Additionally, horizontal lines and a shaded background help identify key levels.

Dynamic Background Color : Adds a gray-blue transparent background between the Sharpe ratio levels of 0 and 1, highlighting the critical region where risk-adjusted returns are assessed.

Originality and Usefulness

This script uniquely combines the analysis of Sharpe ratios for a reference ticker and the current ticker, providing a comparative view of their risk-adjusted returns. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the risk-adjusted returns of the assets:

Reference Ticker Sharpe Ratio : Plotted as a red line, this represents the smoothed Sharpe ratio for the user-selected reference ticker.

Current Ticker Sharpe Ratio : Plotted as a white line, this represents the smoothed Sharpe ratio for the current ticker.

Horizontal Lines and Background Color : Lines at 0 and 1, along with a shaded background between these levels, help to quickly identify the regions of positive and strong risk-adjusted returns.

These features assist in identifying relative performance differences and confirming the strength or weakness of risk-adjusted returns between the two tickers.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling Sharpe ratio. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 4.

Annual Risk-Free Rate (`riskFreeRate`) : The annual risk-free rate used in the Sharpe ratio calculation. Default is 0.02 (2%).

Reference Ticker (`ref_ticker`) : The ticker symbol for the reference asset. Default is "BINANCE:BTCUSDT".

Functionality

Sharpe Ratio Calculation : The script calculates the daily returns, mean return, and standard deviation for both the reference ticker and the current ticker. These values are used to compute the annualized Sharpe ratio.

```pine

ref_dailyReturn = ta.change(ref_close) / ref_close

ref_meanReturn = ta.sma(ref_dailyReturn, length)

ref_stdDevReturn = ta.stdev(ref_dailyReturn, length)

ref_annualizedReturn = ref_meanReturn * length

ref_annualizedStdDev = ref_stdDevReturn * math.sqrt(length)

ref_sharpeRatio = (ref_annualizedReturn - riskFreeRate) / ref_annualizedStdDev

```

Smoothing : A simple moving average is applied to the Sharpe ratios to smooth the data.

```pine

smoothed_ref_sharpeRatio = ta.sma(ref_sharpeRatio, smoothing_length)

smoothed_current_sharpeRatio = ta.sma(current_sharpeRatio, smoothing_length)

```

Plotting : The script plots the smoothed Sharpe ratios for both the reference ticker and the current ticker, along with horizontal lines and a shaded background.

```pine

plot(smoothed_ref_sharpeRatio, title="Ref Ticker Sharpe Ratio", color=color.rgb(255, 82, 82, 50), linewidth=2)

plot(smoothed_current_sharpeRatio, title="Current Ticker Sharpe Ratio", color=color.white, linewidth=2)

h0 = hline(0, "Zero Line", color=color.gray)

h1 = hline(1, "One Line", color=color.gray)

fill(h0, h1, color=color.rgb(33, 150, 243, 90), title="Background")

```

How to Use

Configuring Inputs : Adjust the detection length, smoothing length, and risk-free rate as needed. Set the reference ticker to the desired asset for comparison.

Interpreting the Indicator : Use the plotted Sharpe ratios and background shading to assess the relative risk-adjusted returns of the reference and current tickers.

Signal Confirmation : Look for differences in the Sharpe ratios to identify potential performance advantages or weaknesses. The background shading helps to highlight key levels of risk-adjusted returns.

This script provides a detailed comparative view of risk-adjusted returns, aiding in more informed decision-making by highlighting key differences between the reference ticker and the current ticker.

High Probability OS/OB {DCAquant}DCAquant - High Probability OS/OB

The DCAquant - High Probability OS/OB Pine Script is a sophisticated indicator that provides insights into overbought (OB) and oversold (OS) conditions based on Hull Moving Averages (HMA) and Volume Weighted Moving Averages (VWMA). Here's a detailed breakdown of its functionality:

-------------------------------------------------------------------------------------

THIS INDICATOR IS ONLY WRITTEN FOR BTC, ETH and TOTAL!!!!!!!!!!!!!

-------------------------------------------------------------------------------------

Functionality

The script identifies high-probability OB and OS zones by combining multiple moving averages (MAs).

1. Volume Weighted Moving Average (VWMA)

The VWMA function computes the VWMA over a specified length, incorporating both the price and volume.

2. Hull Moving Average with Volume Weight (HMA-VW)

The hullma_vw function calculates the HMA using the VWMA. This involves:

Computing VWMAs over the full length and half-length.

Using these VWMAs to derive the HMA-VW through a weighted approach.

5. Standard Hull Moving Average (HMA)

The hull function computes the HMA using the standard weighted moving average (WMA).

4. Smoothed HMA-VW

This is an Exponential Moving Average (EMA) of the HMA-VW to smooth out short-term fluctuations.

How this works

First, the distance between the 2 MA's is calculated.

The distance is scored against the average price of the last 100 days.

By getting this score we can calculate extremes

The Extremes are categorized into 4 levels. The transparency of the background color distinguishes these 4 levels.

Only the MOST extremes are plotted ON THE CHART. Within the indicator, all 4 levels are plotted.

Usage

Extreme Buy zone: Consider entering the market when the indicator shows deep negative values (oversold). These are highlighted with a cyan background, with increasing opacity indicating stronger buy signals (Level 4 Zones).

Extreme Sell Zone: Consider exiting the market when the indicator shows high positive values (overbought). These are highlighted with a magenta background, with increasing opacity indicating stronger sell signals (Level 4 Zones).

Disclaimer

This indicator should not be used in isolation. It is recommended to use this as part of a systematic approach, incorporating other tools and analysis methods to confirm signals and make well-informed trading decisions.

Wolf DCA CalculatorThe Wolf DCA Calculator is a powerful and flexible indicator tailored for traders employing the Dollar Cost Averaging (DCA) strategy. This tool is invaluable for planning and visualizing multiple entry points for both long and short positions. It also provides a comprehensive analysis of potential profit and loss based on user-defined parameters, including leverage.

Features

Entry Price: Define the initial entry price for your trade.

Total Lot Size: Specify the total number of lots you intend to trade.

Percentage Difference: Set the fixed percentage difference between each DCA point.

Long Position: Toggle to switch between long and short positions.

Stop Loss Price: Set the price level at which you plan to exit the trade to minimize losses.

Take Profit Price: Set the price level at which you plan to exit the trade to secure profits.

Leverage: Apply leverage to your trade, which multiplies the potential profit and loss.

Number of DCA Points: Specify the number of DCA points to strategically plan your entries.

How to Use

1. Add the Indicator to Your Chart:

Search for "Wolf DCA Calculator" in the TradingView public library and add it to your chart.

2. Configure Inputs:

Entry Price: Set your initial trade entry price.

Total Lot Size: Enter the total number of lots you plan to trade.

Percentage Difference: Adjust this to set the interval between each DCA point.

Long Position: Use this toggle to choose between a long or short position.

Stop Loss Price: Input the price level at which you plan to exit the trade to minimize losses.

Take Profit Price: Input the price level at which you plan to exit the trade to secure profits.

Leverage: Set the leverage you are using for the trade.

Number of DCA Points: Specify the number of DCA points to plan your entries.

3. Analyze the Chart:

The indicator plots the DCA points on the chart using a stepline style for clear visualization.

It calculates the average entry point and displays the potential profit and loss based on the specified leverage.

Labels are added for each DCA point, showing the entry price and the lots allocated.

Horizontal lines mark the Stop Loss and Take Profit levels, with corresponding labels showing potential loss and profit.

Benefits

Visual Planning: Easily visualize multiple entry points and understand how they affect your average entry price.

Risk Management: Clearly see your Stop Loss and Take Profit levels and their impact on your trade.

Customizable: Adapt the indicator to your specific strategy with a wide range of customizable parameters.

[MAD] Entrytool / Bybit-LinearThis indicator, "Entry Tool," was coded at request for Sandmann .

It is designed to provide traders with real-time feedback for strategizing entries, exits, and liquidation levels for trades initiated at that given moment.

The tool visualizes average entry prices, stop-loss levels, multiple take-profit targets, and potential liquidation prices, offering a comprehensive overview of possible trade outcomes. It aids traders in pre-planning their trades by visually simulating the impact of different trading decisions directly on the live chart. Each setting and parameter can be customized to align with individual trading strategies and risk tolerances, making this tool versatile for various trading styles, including day trading, swing trading, and position trading.

------------------------------

Steps to Use the Indicator:

1. Basic Setup:

Setup Type: Choose between "Long" or "Short" to set the direction of the trade.

Leverage: Adjust the leverage to understand its impact on your potential returns and liquidation price.

Tracking follows the close price, alternative you can enter a specific price.

2. Position Setup:

Initial Entry Amount: Set the starting amount for the trade.

Distance: First Increment Percentage from Entry price

Amount: Define the increase for the first incremental addition to the position and specify the amount to be added.

Distance: Second Increment Percentage from Entry

Amount: Set the increase for the second incremental addition and the corresponding amount.

3. Risk Management:

Stop-Loss (SL) Percentage: Set the percentage below or above the average entry price at which the position should be closed to minimize losses.

Take-Profit (TP) Percentages: Define up to four different profit target levels by specifying the percentage above or below the average entry price.

4. Visual Settings:

Box Colors: Customize the colors of the boxes that represent long and short positions to differentiate easily on the chart.

Box Extension: Determine the length by which the box extends beyond the current bar, which helps in visualizing the potential price movement.

Line Colors and Extensions: Select colors for various lines such as the Average Entry Line, Stop-Loss Line, Take-Profit Lines, and Liquidations Line. Adjust the length of these lines for better visibility.

Label Settings: Configure the distance of labels from their corresponding lines and set the font size for better readability.

5. Additional Features:

Liquidation Price Visualization: This new feature calculates and displays the liquidation price based on the current leverage and margin settings, giving traders a critical insight into their risk exposure.

Interactive Drag Point: Adjust the start price manually by dragging the point on the chart, which dynamically updates entry and exit levels as well as risk metrics.

Detailed Leverage Data Array: Input different scenarios with specific leverage, initial margin, and maintenance rates to see how these factors impact potential liquidation points.

6. Informations about leverage calculation

The data used are fetched from Bybit for Linear pairs to calculate the liquidations like in their documentation.

Keep in mind that other exchanges may calulate based on another formular.