Adaptive Resonance Oscillator [AlgoAlpha]Introducing the Adaptive Resonance Oscillator , an advanced momentum-based oscillator designed to dynamically adjust to changing market conditions. This innovative indicator detects market frequency through a Hilbert Transform approach, adapting in real-time to identify overbought and oversold conditions with improved accuracy. With built-in divergence detection, trend analysis, and customizable smoothing, this tool is perfect for traders looking to refine their entries and exits based on adaptive oscillation mechanics.

🚀 Key Features :

🔹 Adaptive Frequency Detection – Uses Hilbert Transform principles to dynamically determine market cycle length for precise oscillator calculation.

⚙️ Customizable Smoothing – Option to apply a Hull Moving Average (HMA) for enhanced signal clarity.

📈 Divergence Detection – Identifies bullish and bearish divergences with visual markers, helping traders spot early trend reversals.

🟢 Overbought & Oversold Signals – Highlights extreme momentum conditions with adjustable thresholds.

🔔 Real-Time Alerts – Get notified for crossovers, divergences, and strong trend shifts directly on your TradingView chart.

🎨 Fully Customizable Appearance – Modify colors, divergence sensitivity, and smoothing options to fit your trading style.

🛠 How to Use :

Add the Adaptive Resonance Oscillator to your TradingView chart by clicking the ★ to favorite it.

Monitor the Charts , switch between smoothed and I smoothed modes to identify trend and price swings, use divergences and reversal signals for potential entry/exits.

Set alerts for bullish/bearish crossovers and divergence signals to stay ahead of market moves.

⚙ How It Works :

The indicator begins by applying a Hilbert Transform frequency estimation to the price series, identifying the dominant market cycle length. This is used to calculate a period for the RSI that matches its resonant frequency with the dominant market frequency, dynamically adjusting the Oscillator. The oscillator then applies an optional Hull Moving Average (HMA) smoothing for signal refinement. Additionally, the indicator scans for bullish and bearish divergences by comparing oscillator movements against price action, plotting signals accordingly. When overbought/oversold conditions or divergence events occur, alerts are triggered to notify the trader in real time.

Meanreversion

Overextension Oscillator [by DanielM]The Overextension Oscillator is an indicator that detects when a market move has extended significantly beyond its typical range, signaling potential areas for a correction or reversal. Unlike traditional oscillators that rely on fixed overbought/oversold levels, this tool dynamically adjusts its thresholds based on historical swing high and swing low movements.

By analyzing all swing points on the chart, the indicator determines the expected range of price movements and identifies when the price extends beyond normal levels. Since every asset has different price behavior and volatility, swing lengths may vary from asset to asset, ensuring that overextension is measured relative to each market's historical price behavior.

How It Works

1️⃣ Swing Detection & Data Collection

The indicator scans all available swing highs and swing lows on the chart to gather a complete dataset of past price fluctuations.

It records the percentage differences between swings to determine how much price typically moves in a given market.

2️⃣ Overextension Calculation

Using the stored swing data, the indicator calculates:

Average Swing Difference – Measures the average percentage difference between swings.

Average Move Percentage – Determines the typical magnitude of price moves within a trend cycle.

These values are used to create dynamic overextension thresholds that adjust based on historical data.

3️⃣ Price Distance & Overextension Measurement

The indicator calculates the distance between the current price and the closest historical swing point. If this distance exceeds the predefined threshold based on past swings, the move is considered overextended. The greater the deviation, the higher the probability of a pullback or short-term reversal.

4️⃣ Buy/Sell Signal Generation

A Buy signal is generated when the price has dropped below an overextended threshold relative to a past swing low.

A Sell signal is generated when the price has risen beyond an overextended threshold relative to a past swing high.

These signals indicate that the price has reached a level where it historically tends to slow down or reverse.

Two-Pole Oscillator [BigBeluga]

The Two-Pole Oscillator is an advanced smoothing oscillator designed to provide traders with precise market signals by leveraging deviation-based calculations combined with a unique two-pole filtering technique. It offers clear visual representation and actionable signals for smart trading decisions.

🔵Key Features:

Two-Pole Filtering: Smooths out the main oscillator signal to reduce noise, providing a cleaner and more reliable view of market momentum and trend strength.

// Two-pole smooth filter function

f_two_pole_filter(source, length) =>

var float smooth1 = na

var float smooth2 = na

alpha = 2.0 / (length + 1)

if na(smooth1)

smooth1 := source

else

smooth1 := (1 - alpha) * smooth1 + alpha * source

if na(smooth2)

smooth2 := smooth1

else

smooth2 := (1 - alpha) * smooth2 + alpha * smooth1

Deviation-Based Oscillator: Utilizes price deviations from the mean to generate dynamic signals, making it ideal for detecting overbought and oversold conditions.

float sma1 = ta.sma(close, 25)

float sma_n1 = ((close - sma1) - ta.sma(close - sma1, 25)) / ta.stdev(close - sma1, 25)

Signal Gradient Strength: Signals on the main oscillator line feature gradient coloring based on their proximity to the 0 level:

➔ Closer to 0: More transparent, indicating weaker signals.

➔ Closer to 1 or -1: Less transparent, highlighting stronger signals.

Level-Based Signal Validation: Parallel levels are plotted on the chart for each signal:

➔ If a level is crossed by price, the signal is invalidated, marked by an "X" at the invalidation point.

Trend Continuation

Invalidation Levels: Serve as potential stop-loss or trade-reversal zones, enabling traders to make more informed and disciplined trading decisions.

Dynamic Chart Plotting: Signals are plotted directly on the chart with corresponding levels, providing a comprehensive visual representation for easy interpretation.

🔵How It Works:

The oscillator calculates price deviation from a mean value and applies two-pole filtering to smooth the resulting signal.

Gradient-colored signals reflect their strength, with transparency indicating proximity to the 0 level on the oscillator scale.

Buy and sell signals are generated based on crossovers and crossunders of the oscillator line with a signal line.

If a level is crossed, the corresponding signal is marked with a "X" plotted on the chart at the crossover point.

🔵Use Cases:

Detecting overbought or oversold market conditions with a smoother, noise-free oscillator.

Using invalidation levels to set clear stop-loss or trade exit points.

Identifying strong momentum signals and filtering out weaker, less reliable ones.

Combining oscillator signals with price action for more precise trade entries and exits.

This indicator is perfect for traders seeking a refined approach to oscillator analysis, combining signal strength visualization with actionable invalidation levels to enhance trading precision and strategy.

Bearish Wick Reversal█ STRATEGY OVERVIEW

The "Bearish Wick Reversal Strategy" identifies potential bullish reversals following significant bearish price rejection (long lower wicks). This counter-trend approach enters long positions when bearish candles show exaggerated downside wicks relative to closing prices, then exits on bullish confirmation signals. Includes optional EMA trend filtering for improved reliability.

█ What is a Bearish Wick?

A price rejection pattern where:

Bearish candle (close < open) forms with extended lower wick

Wick represents failed selloff: Low drops significantly below close

Measured as: (Low - Close)/Close × 100 (Negative percentage indicates downward extension)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Bearish candle forms with close < open

Lower wick exceeds user-defined threshold (Default: -1% of close price)

The signal occurs within the specified time window

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average)

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: Volatile instruments with frequent price rejections

Key Risk: False signals in sustained bearish trends

Optimization Tip: Test various thresholds

Filter Impact: EMA reduces trades but improves win rate and reduces drawdown

Gap Down Reversal Strategy█ STRATEGY OVERVIEW

The "Gap Down Reversal Strategy" capitalizes on price recovery patterns following bearish gap-down openings. This mean-reversion approach enters long positions on confirmed intraday recoveries and exits when prices breach previous session highs. This strategy is NOT optimized.

█ What is a Gap Down Reversal?

A gap down reversal occurs when:

An instrument opens significantly below its prior session's low (price gap)

Selling pressure exhausts itself during the session

Buyers regain control, pushing price back above the opening level

Creates a candlestick with:

• Open < Prior Session Low (true gap)

• Close > Open (bullish reversal candle)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Previous candle closes BELOW its opening price (bearish candle)

Current session opens BELOW prior candle's low (gap down)

Current candle closes ABOVE its opening price (bullish reversal)

Executes market order at session close

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: High volatility instruments with frequent gaps

Key Risk: False reversals in sustained downtrends

Optimization Tip: Test varying gap thresholds (1-3% ranges)

3 Down, 3 Up Strategy█ STRATEGY DESCRIPTION

The "3 Down, 3 Up Strategy" is a mean-reversion strategy designed to capitalize on short-term price reversals. It enters a long position after consecutive bearish closes and exits after consecutive bullish closes. This strategy is NOT optimized and can be used on any timeframes.

█ WHAT ARE CONSECUTIVE DOWN/UP CLOSES?

- Consecutive Down Closes: A sequence of trading bars where each close is lower than the previous close.

- Consecutive Up Closes: A sequence of trading bars where each close is higher than the previous close.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The price closes lower than the previous close for Consecutive Down Closes for Entry (default: 3) consecutive bars.

The signal occurs within the specified time window (between Start Time and End Time).

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average).

2. EXIT CONDITION

A Sell Signal is generated when the price closes higher than the previous close for Consecutive Up Closes for Exit (default: 3) consecutive bars.

█ ADDITIONAL SETTINGS

Consecutive Down Closes for Entry: Number of consecutive lower closes required to trigger a buy. Default = 3.

Consecutive Up Closes for Exit: Number of consecutive higher closes required to exit. Default = 3.

EMA Filter: Optional 200-period EMA filter to confirm long entries in bullish trends. Default = disabled.

Start Time and End Time: Restrict trading to specific dates (default: 2014-2099).

█ PERFORMANCE OVERVIEW

Designed for volatile markets with frequent short-term reversals.

Performs best when price oscillates between clear support/resistance levels.

The EMA filter improves reliability in trending markets but may reduce trade frequency.

Backtest to optimize consecutive close thresholds and EMA period for specific instruments.

RSI OB/OS Strategy Analyzer█ OVERVIEW

The RSI OB/OS Strategy Analyzer is a comprehensive trading tool designed to help traders identify and evaluate overbought/oversold reversal opportunities using the Relative Strength Index (RSI). It provides visual signals, performance metrics, and a detailed table to analyze the effectiveness of RSI-based strategies over a user-defined lookback period.

█ KEY FEATURES

RSI Calculation

Calculates RSI with customizable period (default 14)

Plots dynamic overbought (70) and oversold (30) levels

Adds background coloring for OB/OS regions

Reversal Signals

Identifies signals based on RSI crossing OB/OS levels

Two entry strategies available:

Revert Cross: Triggers when RSI exits OB/OS zone

Cross Threshold: Triggers when RSI enters OB/OS zone

Trade Direction

Users can select a trade bias:

Long: Focuses on oversold reversals (bullish signals)

Short: Focuses on overbought reversals (bearish signals)

Performance Metrics

Calculates three key statistics for each lookback period:

Win Rate: Percentage of profitable trades

Mean Return: Average return across all trades

Median Return: Median return across all trades

Metrics calculated as percentage changes from entry price

Visual Signals

Dual-layer signal display:

BUY: Green triangles + text labels below price

SELL: Red triangles + text labels above price

Semi-transparent background highlighting in OB/OS zones

Performance Table

Interactive table showing metrics for each lookback period

Color-coded visualization:

Win Rate: Gradient from red (low) to green (high)

Returns: Green for positive, red for negative

Time Filtering

Users can define a specific time window for the indicator to analyze trades, ensuring that performance metrics are calculated only for the desired period.

Customizable Display

Adjustable table font sizes: Auto/Small/Normal/Large

Toggle option for table visibility

█ PURPOSE

The RSI OB/OS Strategy Analyzer helps traders:

Identify mean-reversion opportunities through RSI extremes

Backtest entry strategy effectiveness across multiple time horizons

Optimize trade timing through visual historical performance data

Quickly assess strategy robustness with color-coded metrics

█ IDEAL USERS

Counter-Trend Traders: Looking to capitalize on RSI extremes

Systematic Traders: Needing quantitative strategy validation

Educational Users: Studying RSI behavior in different market conditions

Multi-Timeframe Analysts: Interested in forward returns analysis

Internal Bar Strength (IBS) Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a long position when the IBS indicates oversold conditions and exits when the IBS reaches overbought levels. This strategy was designed to be used on the daily timeframe.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- **Low IBS (≤ 0.2)**: Indicates the close is near the bar's low, suggesting oversold conditions.

- **High IBS (≥ 0.8)**: Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The IBS value drops below the Lower Threshold (default: 0.2).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the IBS value rises to or above the Upper Threshold (default: 0.8). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy exits trades. Default is 0.8.

Lower Threshold: The IBS level at which the strategy enters long positions. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for ranging markets and performs best when prices frequently revert to the mean.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

Bollinger Bands Reversal Strategy Analyzer█ OVERVIEW

The Bollinger Bands Reversal Overlay is a versatile trading tool designed to help traders identify potential reversal opportunities using Bollinger Bands. It provides visual signals, performance metrics, and a detailed table to analyze the effectiveness of reversal-based strategies over a user-defined lookback period.

█ KEY FEATURES

Bollinger Bands Calculation

The indicator calculates the standard Bollinger Bands, consisting of:

A middle band (basis) as the Simple Moving Average (SMA) of the closing price.

An upper band as the basis plus a multiple of the standard deviation.

A lower band as the basis minus a multiple of the standard deviation.

Users can customize the length of the Bollinger Bands and the multiplier for the standard deviation.

Reversal Signals

The indicator identifies potential reversal signals based on the interaction between the price and the Bollinger Bands.

Two entry strategies are available:

Revert Cross: Waits for the price to close back above the lower band (for longs) or below the upper band (for shorts) after crossing it.

Cross Threshold: Triggers a signal as soon as the price crosses the lower band (for longs) or the upper band (for shorts).

Trade Direction

Users can select a trade bias:

Long: Focuses on bullish reversal signals.

Short: Focuses on bearish reversal signals.

Performance Metrics

The indicator calculates and displays the performance of trades over a user-defined lookback period ( barLookback ).

Metrics include:

Win Rate: The percentage of trades that were profitable.

Mean Return: The average return across all trades.

Median Return: The median return across all trades.

These metrics are calculated for each bar in the lookback period, providing insights into the strategy's performance over time.

Visual Signals

The indicator plots buy and sell signals on the chart:

Buy Signals: Displayed as green triangles below the price bars.

Sell Signals: Displayed as red triangles above the price bars.

Performance Table

A customizable table is displayed on the chart, showing the performance metrics for each bar in the lookback period.

The table includes:

Win Rate: Highlighted with gradient colors (green for high win rates, red for low win rates).

Mean Return: Colored based on profitability (green for positive returns, red for negative returns).

Median Return: Colored similarly to the mean return.

Time Filtering

Users can define a specific time window for the indicator to analyze trades, ensuring that performance metrics are calculated only for the desired period.

Customizable Display

The table's font size can be adjusted to suit the user's preference, with options for "Auto," "Small," "Normal," and "Large."

█ PURPOSE

The Bollinger Bands Reversal Overlay is designed to:

Help traders identify high-probability reversal opportunities using Bollinger Bands.

Provide actionable insights into the performance of reversal-based strategies.

Enable users to backtest and optimize their trading strategies by analyzing historical performance metrics.

█ IDEAL USERS

Swing Traders: Looking for reversal opportunities within a trend.

Mean Reversion Traders: Interested in trading price reversals to the mean.

Strategy Developers: Seeking to backtest and refine Bollinger Bands-based strategies.

Performance Analysts: Wanting to evaluate the effectiveness of reversal signals over time.

Buy on 5 day low Strategy█ STRATEGY DESCRIPTION

The "Buy on 5 Day Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous five days. It enters a long position when specific conditions are met and exits when the price exceeds the high of the previous day. This strategy is optimized for use on daily or higher timeframes.

█ WHAT IS THE 5-DAY LOW?

The 5-Day Low is the lowest price observed over the last five days. This level is used as a reference to identify potential oversold conditions and reversal points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous five days (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous day (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support levels.

It is sensitive to oversold conditions, as indicated by the 5-Day Low, and overbought conditions, as indicated by the previous day's high.

Backtesting results should be analyzed to optimize the strategy for specific instruments and market conditions.

3-Bar Low Strategy█ STRATEGY DESCRIPTION

The "3-Bar Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous three bars. It enters a long position when specific conditions are met and exits when the price exceeds the highest high of the previous seven bars. This strategy is suitable for use on various timeframes.

█ WHAT IS THE 3-BAR LOW?

The 3-Bar Low is the lowest price observed over the last three bars. This level is used as a reference to identify potential oversold conditions and reversal points.

█ WHAT IS THE 7-BAR HIGH?

The 7-Bar High is the highest price observed over the last seven bars. This level is used as a reference to identify potential overbought conditions and exit points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous three bars (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

If the EMA Filter is enabled, the close price must also be above the 200-period Exponential Moving Average (EMA).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

MA Period: The lookback period for the 200-period EMA used in the EMA Filter. Default is 200.

Use EMA Filter: Enables or disables the EMA Filter for long entries. Default is disabled.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support and resistance levels.

It is sensitive to oversold conditions, as indicated by the 3-Bar Low, and overbought conditions, as indicated by the 7-Bar High.

Backtesting results should be analyzed to optimize the MA Period and EMA Filter settings for specific instruments.

Bollinger Bands Reversal + IBS Strategy█ STRATEGY DESCRIPTION

The "Bollinger Bands Reversal Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price deviates below the lower Bollinger Band and the Internal Bar Strength (IBS) indicates oversold conditions. It enters a long position when specific conditions are met and exits when the IBS indicates overbought conditions. This strategy is suitable for use on various timeframes.

█ WHAT ARE BOLLINGER BANDS?

Bollinger Bands consist of three lines:

- **Basis**: A Simple Moving Average (SMA) of the price over a specified period.

- **Upper Band**: The basis plus a multiple of the standard deviation of the price.

- **Lower Band**: The basis minus a multiple of the standard deviation of the price.

Bollinger Bands help identify periods of high volatility and potential reversal points.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) is a measure of where the closing price is relative to the high and low of the bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

A low IBS value (e.g., below 0.2) indicates that the close is near the low of the bar, suggesting oversold conditions. A high IBS value (e.g., above 0.8) indicates that the close is near the high of the bar, suggesting overbought conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The IBS value is below 0.2, indicating oversold conditions.

The close price is below the lower Bollinger Band.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the IBS value exceeds 0.8, indicating overbought conditions. This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Length: The lookback period for calculating the Bollinger Bands. Default is 20.

Multiplier: The number of standard deviations used to calculate the upper and lower Bollinger Bands. Default is 2.0.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently deviates from the Bollinger Bands.

It is sensitive to oversold and overbought conditions, as indicated by the IBS, which helps to identify potential reversals.

Backtesting results should be analyzed to optimize the Length and Multiplier parameters for specific instruments.

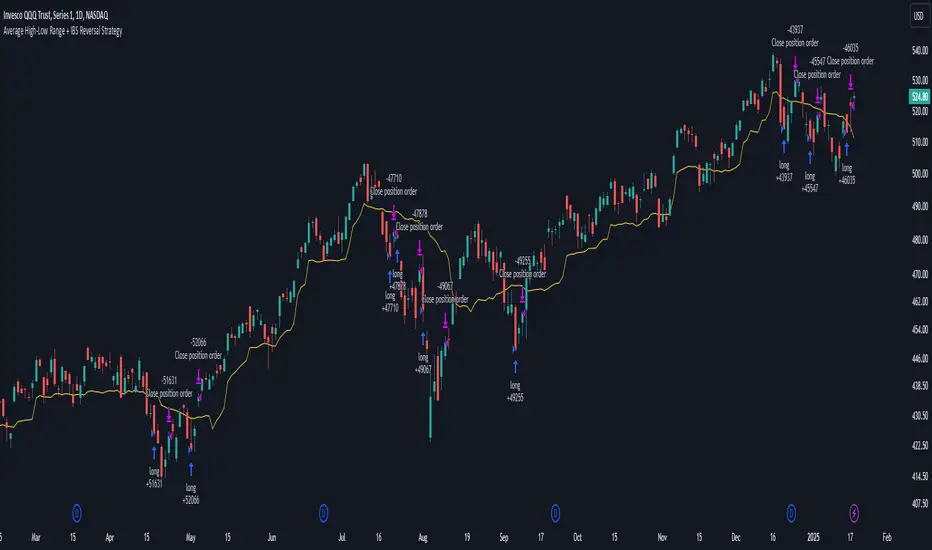

Average High-Low Range + IBS Reversal Strategy█ STRATEGY DESCRIPTION

The "Average High-Low Range + IBS Reversal Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price deviates significantly from its average high-low range and the Internal Bar Strength (IBS) indicates oversold conditions. It enters a long position when specific conditions are met and exits when the price shows strength by exceeding the previous bar's high. This strategy is suitable for use on various timeframes.

█ WHAT IS THE AVERAGE HIGH-LOW RANGE?

The Average High-Low Range is calculated as the Simple Moving Average (SMA) of the difference between the high and low prices over a specified period. It helps identify periods of increased volatility and potential reversal points.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) is a measure of where the closing price is relative to the high and low of the bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

A low IBS value (e.g., below 0.2) indicates that the close is near the low of the bar, suggesting oversold conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been below the buy threshold (calculated as `upper - (2.5 * hl_avg)`) for a specified number of consecutive bars (`bars_below_threshold`).

The IBS value is below the specified buy threshold (`ibs_buy_treshold`).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Length: The lookback period for calculating the average high-low range. Default is 20.

Bars Below Threshold: The number of consecutive bars the price must remain below the buy threshold to trigger a Buy Signal. Default is 2.

IBS Buy Threshold: The IBS value below which a Buy Signal is triggered. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently deviates from its average high-low range.

It is sensitive to oversold conditions, as indicated by the IBS, which helps to identify potential reversals.

Backtesting results should be analyzed to optimize the Length, Bars Below Threshold, and IBS Buy Threshold parameters for specific instruments.

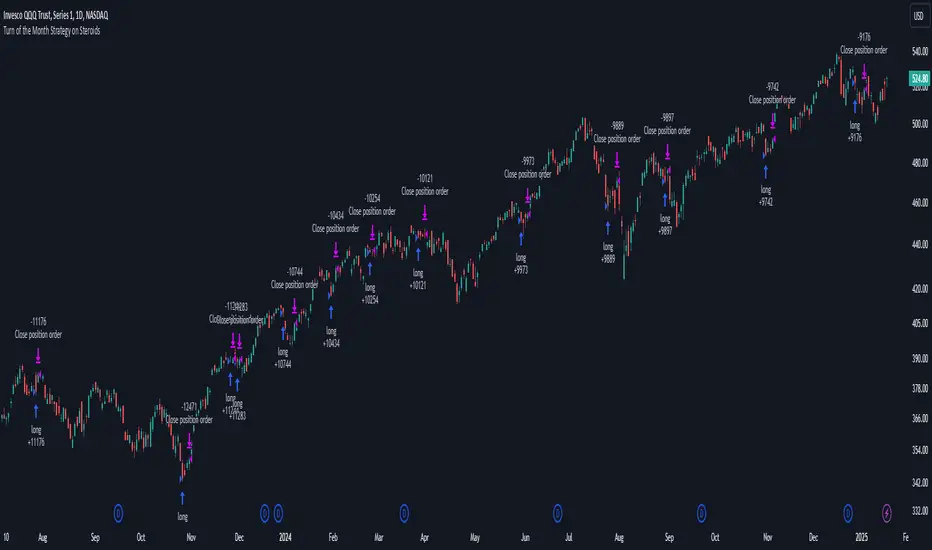

Turn of the Month Strategy on Steroids█ STRATEGY DESCRIPTION

The "Turn of the Month Strategy on Steroids" is a seasonal mean-reversion strategy designed to capitalize on price movements around the end of the month. It enters a long position when specific conditions are met and exits when the Relative Strength Index (RSI) indicates overbought conditions. This strategy is optimized for use on daily or higher timeframes.

█ WHAT IS THE TURN OF THE MONTH EFFECT?

The Turn of the Month effect refers to the observed tendency of stock prices to rise around the end of the month. This strategy leverages this phenomenon by entering long positions when the price shows signs of a reversal during this period.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The current day of the month is greater than or equal to the specified `dayOfMonth` threshold (default is 25).

The close price is lower than the previous day's close (`close < close `).

The previous day's close is also lower than the close two days ago (`close < close `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

There is no existing open position (`strategy.position_size == 0`).

2. EXIT CONDITION

A Sell Signal is generated when the 2-period RSI exceeds 65, indicating overbought conditions. This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Day of Month: The day of the month threshold for triggering a Buy Signal. Default is 25.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed to exploit seasonal price patterns around the end of the month.

It performs best in markets where the Turn of the Month effect is pronounced.

Backtesting results should be analyzed to optimize the `dayOfMonth` threshold and RSI parameters for specific instruments.

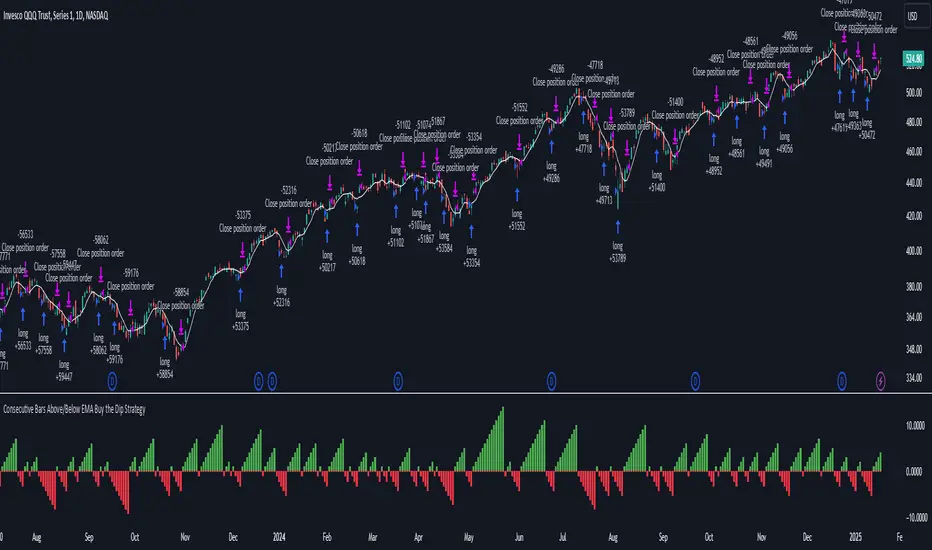

Consecutive Bars Above/Below EMA Buy the Dip Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above/Below EMA Buy the Dip Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price dips below a moving average for a specified number of consecutive bars. It enters a long position when the dip condition is met and exits when the price shows strength by exceeding the previous bar's high. This strategy is suitable for use on various timeframes.

█ WHAT IS THE MOVING AVERAGE?

The strategy uses either a Simple Moving Average (SMA) or an Exponential Moving Average (EMA) as a reference for identifying dips. The type and length of the moving average can be customized in the settings.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the selected moving average for a specified number of consecutive bars (`consecutiveBarsTreshold`).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Consecutive Bars Threshold: The number of consecutive bars the price must remain below the moving average to trigger a Buy Signal. Default is 3.

MA Type: The type of moving average used (SMA or EMA). Default is SMA.

MA Length: The length of the moving average. Default is 5.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around the moving average.

It is sensitive to the number of consecutive bars below the moving average, which helps to identify potential dips.

Backtesting results should be analysed to optimize the Consecutive Bars Threshold, MA Type, and MA Length for specific instruments.

Turn around Tuesday on Steroids Strategy█ STRATEGY DESCRIPTION

The "Turn around Tuesday on Steroids Strategy" is a mean-reversion strategy designed to identify potential price reversals at the start of the trading week. It enters a long position when specific conditions are met and exits when the price shows strength by exceeding the previous bar's high. This strategy is optimized for ETFs, stocks, and other instruments on the daily timeframe.

█ WHAT IS THE STARTING DAY?

The Starting Day determines the first day of the trading week for the strategy. It can be set to either Sunday or Monday, depending on the instrument being traded. For ETFs and stocks, Monday is recommended. For other instruments, Sunday is recommended.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The current day is the first day of the trading week (either Sunday or Monday, depending on the Starting Day setting).

The close price is lower than the previous day's close (`close < close `).

The previous day's close is also lower than the close two days ago (`close < close `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

If the MA Filter is enabled, the close price must also be above the 200-period Simple Moving Average (SMA).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Starting Day: Determines the first day of the trading week. Options are Sunday or Monday. Default is Sunday.

Use MA Filter: Enables or disables the 200-period SMA filter for long entries. Default is disabled.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for markets with frequent weekly reversals.

It performs best in volatile conditions where price movements are significant at the start of the trading week.

Backtesting results should be analysed to optimize the Starting Day and MA Filter settings for specific instruments.

Mean Reversion Pro Strategy [tradeviZion]Mean Reversion Pro Strategy : User Guide

A mean reversion trading strategy for daily timeframe trading.

Introduction

Mean Reversion Pro Strategy is a technical trading system that operates on the daily timeframe. The strategy uses a dual Simple Moving Average (SMA) system combined with price range analysis to identify potential trading opportunities. It can be used on major indices and other markets with sufficient liquidity.

The strategy includes:

Trading System

Fast SMA for entry/exit points (5, 10, 15, 20 periods)

Slow SMA for trend reference (100, 200 periods)

Price range analysis (20% threshold)

Position management rules

Visual Elements

Gradient color indicators

Three themes (Dark/Light/Custom)

ATR-based visuals

Signal zones

Status Table

Current position information

Basic performance metrics

Strategy parameters

Optional messages

📊 Strategy Settings

Main Settings

Trading Mode

Options: Long Only, Short Only, Both

Default: Long Only

Position Size: 10% of equity

Starting Capital: $20,000

Moving Averages

Fast SMA: 5, 10, 15, or 20 periods

Slow SMA: 100 or 200 periods

Default: Fast=5, Slow=100

🎯 Entry and Exit Rules

Long Entry Conditions

All conditions must be met:

Price below Fast SMA

Price below 20% of current bar's range

Price above Slow SMA

No existing position

Short Entry Conditions

All conditions must be met:

Price above Fast SMA

Price above 80% of current bar's range

Price below Slow SMA

No existing position

Exit Rules

Long Positions

Exit when price crosses above Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

Short Positions

Exit when price crosses below Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

💼 Risk Management

Position Sizing

Default: 10% of equity per trade

Initial capital: $20,000

Commission: 0.01%

Slippage: 2 points

Maximum one position at a time

Risk Control

Use daily timeframe only

Avoid trading during major news events

Consider market conditions

Monitor overall exposure

📊 Performance Dashboard

The strategy includes a comprehensive status table displaying:

Strategy Parameters

Current SMA settings

Trading direction

Fast/Slow SMA ratio

Current Status

Active position (Flat/Long/Short)

Current price with color coding

Position status indicators

Performance Metrics

Net Profit (USD and %)

Win Rate with color grading

Profit Factor with thresholds

Maximum Drawdown percentage

Average Trade value

📱 Alert Settings

Entry Alerts

Long Entry (Buy Signal)

Short Entry (Sell Signal)

Exit Alerts

Long Exit (Take Profit)

Short Exit (Take Profit)

Alert Message Format

Strategy name

Signal type and direction

Current price

Fast SMA value

Slow SMA value

💡 Usage Tips

Consider starting with Long Only mode

Begin with default settings

Keep track of your trades

Review results regularly

Adjust settings as needed

Follow your trading plan

⚠️ Disclaimer

This strategy is for educational and informational purposes only. It is not financial advice. Always:

Conduct your own research

Test thoroughly before live trading

Use proper risk management

Consider your trading goals

Monitor market conditions

Never risk more than you can afford to lose

📋 Release Notes

14 January 2025

Added New Fast & Slow SMA Options:

Fibonacci-based periods: 8, 13, 21, 144, 233, 377

Additional period: 50

Complete Fast SMA options now: 5, 8, 10, 13, 15, 20, 21, 34, 50

Complete Slow SMA options now: 100, 144, 200, 233, 377

Bug Fixes:

Fixed Maximum Drawdown calculation in the performance table

Now using strategy.max_drawdown_percent for accurate DD reporting

Previous version showed incorrect DD values

Performance metrics now accurately reflect trading results

Performance Note:

Strategy tested with Fast/Slow SMA 13/377

Test conducted with 10% equity risk allocation

Daily Timeframe

For Beginners - How to Modify SMA Levels:

Find this line in the code:

fastLength = input.int(title="Fast SMA Length", defval=5, options= )

To add a new Fast SMA period: Add the number to the options list, e.g.,

To remove a Fast SMA period: Remove the number from the options list

For Slow SMA, find:

slowLength = input.int(title="Slow SMA Length", defval=100, options= )

Modify the options list the same way

⚠️ Note: Keep the periods that make sense for your trading timeframe

💡 Tip: Test any new combinations thoroughly before live trading

"Trade with Discipline, Manage Risk, Stay Consistent" - tradeviZion

Top G indicator [BigBeluga]Top G Indicator is a straightforward yet powerful tool designed to identify market extremes, helping traders spot potential tops and bottoms effectively.

🔵 Key Features:

High Probability Signals:

𝔾 Label: Indicates high-probability market bottoms based on specific conditions such as low volatility and momentum shifts.

Top Label: Highlights high-probability market tops using key price action dynamics.

Simple Signals for Potential Extremes:

^ (Caret): Marks potential bottom areas with less certainty than 𝔾 labels.

v (Inverted Caret): Signals potential top areas with less certainty than Top labels.

Midline Visualization:

A smoothed midline helps identify the center of the current range, providing additional context for trend and range trading.

Range Highlighting:

Dynamic bands around the highest and lowest points of the selected period, color-coded for easy identification of the market range.

🔵 Usage:

Spot Extremes: Use 𝔾 and Top labels to identify high-probability reversal points for potential entries or exits.

Monitor Potential Reversals: Leverage ^ and v marks for additional signals on potential turning points, especially during range-bound conditions.

Range Analysis: Use the midline and dynamic bands to determine the market's range and its center, aiding in identifying consolidation or breakout scenarios.

Confirmation Tool: Combine this indicator with other tools to confirm reversal or trend continuation setups.

Top G Indicator is a simple yet effective tool for spotting market extremes, designed to assist traders in making timely decisions by identifying potential tops and bottoms with clarity.

Kalman Step Signals [AlgoAlpha]Take your trading to the next level with the Kalman Step Signals indicator by AlgoAlpha! This advanced tool combines the power of Kalman Filtering and the Supertrend indicator, offering a unique perspective on market trends and price movements. Designed for traders who seek clarity and precision in identifying trend shifts and potential trade entries, this indicator is packed with customizable features to suit your trading style.

Key Features

🔍 Kalman Filter Smoothing : Dynamically smooths price data with user-defined parameters for Alpha, Beta, and Period, optimizing responsiveness and trend clarity.

📊 Supertrend Overlay : Incorporates a classic Supertrend indicator to provide clear visual cues for trend direction and potential reversals.

🎨 Customizable Appearance : Adjust colors for bullish and bearish trends, along with optional exit bands for more nuanced analysis.

🔔 Smart Alerts : Detect key moments like trend changes or rejection entries for timely trading decisions.

📈 Advanced Visualization : Includes optional entry signals, exit bands, and rejection markers to pinpoint optimal trading opportunities.

How to Use

Add the Indicator : Add the script to your TradingView favorites. Customize inputs like Kalman parameters (Alpha, Beta, Period) and Supertrend settings (Factor, ATR Period) based on your trading strategy.

Interpret the Signals : Watch for trend direction changes using Supertrend lines and directional markers. Utilize rejection entries to identify price rejections at trendlines for precision entry points.

Set Alerts : Enable the built-in alert conditions for trend changes or rejection entries to act swiftly on trading opportunities without constant chart monitoring.

How It Works

The indicator leverages a Kalman Filter to smooth raw price data, balancing responsiveness and noise reduction using user-controlled parameters. This refined price data is then fed into a Supertrend calculation, combining ATR-based volatility analysis with dynamic upper and lower bands. The result is a clear and reliable trend-detection system. Additionally, it features rejection markers for bullish and bearish reversals when prices reject the trendline, along with exit bands to visualize potential price targets. The integration of customizable alerts ensures traders never miss critical market moves.

Add the Kalman Step Signals to your TradingView charts today and enjoy a smarter, more efficient trading experience! 🚀🌟

Adaptive Trend Flow [QuantAlgo]Adaptive Trend Flow 📈🌊

The Adaptive Trend Flow by QuantAlgo is a sophisticated technical indicator that harnesses the power of volatility-adjusted EMAs to navigate market trends with precision. By seamlessly integrating a dynamic dual-EMA system with adaptive volatility bands, this premium tool enables traders and investors to identify and capitalize on sustained market moves while effectively filtering out noise. The indicator's unique approach to trend detection combines classical technical analysis with modern adaptive techniques, providing traders and investors with clear, actionable signals across various market conditions and asset class.

💫 Indicator Architecture

The Adaptive Trend Flow provides a sophisticated framework for assessing market trends through a harmonious blend of EMA dynamics and volatility-based boundary calculations. Unlike traditional moving average systems that use fixed parameters, this indicator incorporates smart volatility measurements to automatically adjust its sensitivity to market conditions. The core algorithm employs a dual EMA system combined with standard deviation-based volatility bands, creating a self-adjusting mechanism that expands and contracts based on market volatility. This adaptive approach allows the indicator to maintain its effectiveness across different market phases - from ranging to trending conditions. The volatility-adjusted bands act as dynamic support and resistance levels, while the gradient visualization system provides instant visual feedback on trend strength and duration.

📊 Technical Composition and Calculation

The Adaptive Trend Flow is composed of several technical components that create a dynamic trending system:

Dual EMA System: Utilizes fast and slow EMAs for primary trend detection

Volatility Integration: Computes and smooths volatility for adaptive band calculation

Dynamic Band Generation: Creates volatility-adjusted boundaries for trend validation

Gradient Visualization: Provides progressive visual feedback on trend strength

📈 Key Indicators and Features

The Adaptive Trend Flow utilizes customizable length parameters for both EMAs and volatility calculations to adapt to different trading styles. The trend detection component evaluates price action relative to the dynamic bands to validate signals and identify potential reversals.

The indicator incorporates multi-layered visualization with:

Color-coded basis and trend lines (bullish/bearish)

Adaptive volatility-based bands

Progressive gradient background for trend duration

Clear trend reversal signals (𝑳/𝑺)

Smooth fills between key levels

Programmable alerts for trend changes

⚡️ Practical Applications and Examples

✅ Add the Indicator: Add the indicator to your TradingView chart by clicking on the star icon to add it to your favorites ⭐️

👀 Monitor Trends: Watch the basis line and trend band interactions to identify trend direction and strength. The gradient background intensity indicates trend duration and conviction.

🎯 Track Signals: Pay attention to the trend reversal markers that appear on the chart:

→ Long signals (𝑳) appear when price action confirms a bullish trend reversal

→ Short signals (𝑺) indicate validated bearish trend reversals

🔔 Set Alerts: Configure alerts for trend changes in both bullish and bearish directions, ensuring you never miss significant technical developments.

🌟 Summary and Tips

The Adaptive Trend Flow by QuantAlgo is a sophisticated technical tool designed to support trend-following strategies across different market environments and asset class. By combining dual EMA analysis with volatility-adjusted bands, it helps traders and investors identify significant trend changes while filtering out market noise, providing validated signals. The tool's adaptability through customizable EMA lengths, volatility smoothing, and sensitivity settings makes it suitable for various trading timeframes and styles, allowing users to capture trending opportunities while maintaining protection against false signals.

Key parameters to optimize for your trading and/or investing style:

Main Length: Adjust for more or less sensitivity to trend changes (default: 10)

Smoothing Length: Fine-tune volatility calculations for signal stability (default: 14)

Sensitivity: Balance band width for trend validation (default: 2.0)

Visual Settings: Customize appearance with color and display options

The Adaptive Trend Flow is particularly effective for:

Identifying sustained market trends

Detecting trend reversals with confirmation

Measuring trend strength and duration

Filtering out market noise and false signals

Remember to:

Allow the indicator to validate trend changes before taking action

Use the gradient background to gauge trend strength

Combine with volume analysis for additional confirmation

Consider multiple timeframes for a complete market view

Adjust sensitivity based on market volatility conditions

Support and Resistance Non-Repainting [AlgoAlpha]Elevate your technical analysis with the Non-Repainting Support and Resistance indicator from AlgoAlpha. Designed for traders who value precision, this tool highlights key support and resistance zones without repainting, ensuring reliable signals for better market decisions.

Key Features

🔍 Concise Zones: Identifies critical levels in real-time without repainting.

🖍 Customizable Appearance: Choose your preferred colors for bullish and bearish zones.

📏 Pivot Sensitivity Settings: Adjust the lookback period to fit different market conditions.

🔔 Visual Alerts: Highlights zones on your chart with clear, dynamic boxes and lines.

How to Use

Add the Indicator : Add it to your favorites chart by clicking the star icon. Adjust the lookback period, max zone duration, and colors to match your strategy.

Analyze the Chart : Look for zones where prices frequently react, indicating strong support or resistance.

Set Alerts : Enable notifications for new zone formations and zone invalidations, ensuring you never miss critical market moves.

How It Works

The indicator detects pivot highs and lows using a specified lookback period. When a pivot is confirmed, it draws corresponding support or resistance zones using TradingView’s built-in drawing tools. These zones extend until price breaks through them or they expire based on a maximum allowed duration. The indicator continuously checks if price interacts with any active zones and adjusts accordingly, ensuring accurate and real-time visualization.

LRI Momentum Cycles [AlgoAlpha]Discover the LRI Momentum Cycles indicator by AlgoAlpha, a cutting-edge tool designed to identify market momentum shifts using trend normalization and linear regression analysis. This advanced indicator helps traders detect bullish and bearish cycles with enhanced accuracy, making it ideal for swing traders and intraday enthusiasts alike.

Key Features :

🎨 Customizable Appearance : Set personalized colors for bullish and bearish trends to match your charting style.

🔧 Dynamic Trend Analysis : Tracks market momentum using a unique trend normalization algorithm.

📊 Linear Regression Insight : Calculates real-time trend direction using linear regression for better precision.

🔔 Alert Notifications : Receive alerts when the market switches from bearish to bullish or vice versa.

How to Use :

🛠 Add the Indicator : Favorite and apply the indicator to your TradingView chart. Adjust the lookback period, linear regression source, and regression length to fit your strategy.

📊 Market Analysis : Watch for color changes on the trend line. Green signals bullish momentum, while red indicates bearish cycles. Use these shifts to time entries and exits.

🔔 Set Alerts : Enable notifications for momentum shifts, ensuring you never miss critical market moves.

How It Works :

The LRI Momentum Cycles indicator calculates trend direction by applying linear regression on a user-defined price source over a specified period. It compares historical trend values, detecting bullish or bearish momentum through a dynamic scoring system. This score is normalized to ensure consistent readings, regardless of market conditions. The indicator visually represents trends using gradient-colored plots and fills to highlight changes in momentum. Alerts trigger when the momentum state changes, providing actionable trading signals.

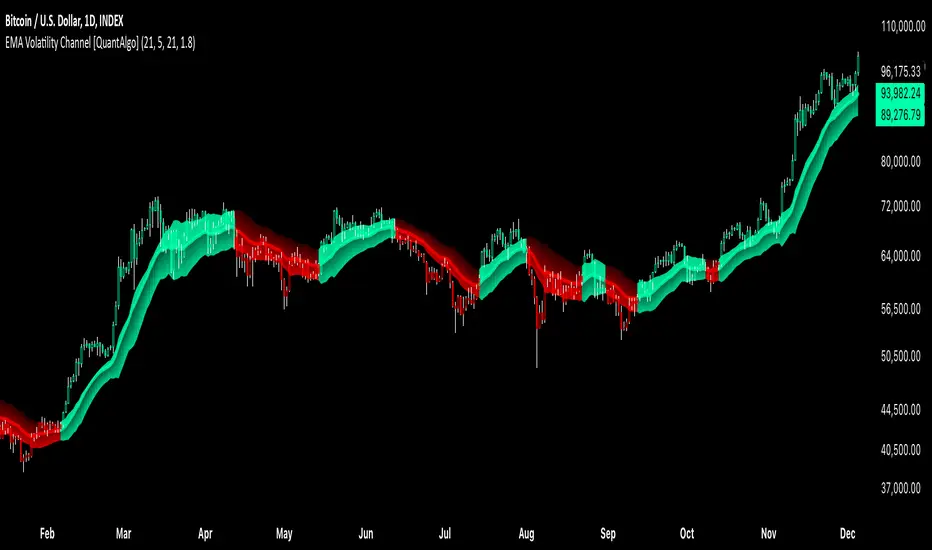

EMA Volatility Channel [QuantAlgo]EMA Volatility Channel 🌊📈

The EMA Volatility Channel by QuantAlgo is an advanced technical indicator designed to capture price volatility and trend dynamics through adaptive channels based on exponential moving averages. This sophisticated system combines EMA-based trend analysis with dynamic volatility-adjusted bands to help traders and investors identify trend direction, potential reversals, and market volatility conditions. By evaluating both price momentum and volatility together, this tool enables users to make informed trading decisions while adapting to changing market conditions.

💫 Dynamic Channel Architecture

The EMA Volatility Channel provides a unique framework for assessing market trends through a blend of exponential moving averages and volatility-based channel calculations. Unlike traditional channel indicators that use fixed-width bands, this system incorporates dynamic volatility measurements to adjust channel width automatically, helping users determine whether price movements are significant relative to current market conditions. By combining smooth EMA trends with adaptive volatility bands, it evaluates both directional movement and market volatility, while the smoothing parameters ensure stable yet responsive channel adjustments. This adaptive approach allows users to identify trending conditions while remaining aware of volatility expansions and contractions, enhancing both trend-following and reversal strategies.

📊 Indicator Components & Mechanics

The EMA Volatility Channel is composed of several technical components that create a dynamic channel system:

EMA Midline: Calculates a smoothed exponential moving average that serves as the channel's centerline, providing a clear reference for trend direction.

Volatility Measurement: Computes average price movement to determine dynamic channel width, adapting to changing market conditions automatically.

Smooth Band Calculation: Applies additional smoothing to the channel bands, reducing noise while maintaining responsiveness to significant price movements.

📈 Key Indicators and Features

The EMA Volatility Channel combines various technical tools to deliver a comprehensive analysis of market conditions.

The indicator utilizes exponential moving averages with customizable length and smoothing parameters to adapt to different trading styles. Volatility calculations are applied to determine channel width, providing context-aware boundaries for price movement. The trend detection component evaluates price action relative to the channel bands, helping validate trends and identify potential reversals.

The indicator incorporates multi-layered visualization with color-coded channels and bars to signal both trend direction and market position. These adaptive visual cues, combined with programmable alerts for channel breakouts, help traders and investors track both trend changes and volatility conditions, supporting both trend-following and mean-reversion strategies.

⚡️ Practical Applications and Examples

✅ Add the Indicator: Add the indicator to your TradingView chart by clicking on the star icon to add it to your favorites ⭐️

👀 Monitor Channel Position: Watch the price position relative to the channel bands to identify trend direction and potential reversals. When price moves outside the channel, consider potential trend changes or extreme conditions.

🔔 Set Alerts: Configure alerts for channel breakouts and trend changes, ensuring you can act on significant technical developments promptly.

🌟 Summary and Tips

The EMA Volatility Channel by QuantAlgo is a versatile technical tool, designed to support both trend following and volatility analysis across different market environments. By combining smooth EMA trends with dynamic volatility-based channels, it helps traders and investors identify significant price movements while measuring market volatility, providing reliable technical signals. The tool's adaptability across timeframes makes it suitable for both trend-following and reversal strategies, allowing users to capture opportunities while maintaining awareness of changing market conditions.