First Passage Time - Distribution AnalysisThe First Passage Time (FPT) Distribution Analysis indicator is a sophisticated probabilistic tool that answers one of the most critical questions in trading: "How long will it take for price to reach my target, and what are the odds of getting there first?"

Unlike traditional technical indicators that focus on what might happen, this indicator tells you when it's likely to happen.

Mathematical Foundation: First Passage Time Theory

What is First Passage Time?

First Passage Time (FPT) is a concept in stochastic processes that measures the time it takes for a random process to reach a specific threshold for the first time. Originally developed in physics and mathematics, FPT has applications in:

Quantitative Finance: Option pricing, risk management, and algorithmic trading

Neuroscience: Modeling neural firing patterns

Biology: Population dynamics and disease spread

Engineering: Reliability analysis and failure prediction

The Mathematics Behind It

This indicator uses Geometric Brownian Motion (GBM), the same stochastic model used in the Black-Scholes option pricing formula:

dS = μS dt + σS dW

Where:

S = Asset price

μ = Drift (trend component)

σ = Volatility (uncertainty component)

dW = Wiener process (random walk)

Through Monte Carlo simulation, the indicator runs 1,000+ price path simulations to statistically determine:

When each threshold (+X% or -X%) is likely to be hit

Which threshold is hit first (directional bias)

How often each scenario occurs (probability distribution)

🎯 How This Indicator Works

Core Algorithm Workflow:

Calculate Historical Statistics

Measures recent price volatility (standard deviation of log returns)

Calculates drift (average directional movement)

Annualizes these metrics for meaningful comparison

Run Monte Carlo Simulations

Generates 1,000+ random price paths based on historical behavior

Tracks when each path hits the upside (+X%) or downside (-X%) threshold

Records which threshold was hit first in each simulation

Aggregate Statistical Results

Calculates percentile distributions (10th, 25th, 50th, 75th, 90th)

Computes "first hit" probabilities (upside vs downside)

Determines average and median time-to-target

Visual Representation

Displays thresholds as horizontal lines

Shows gradient risk zones (purple-to-blue)

Provides comprehensive statistics table

📈 Use Cases

1. Options Trading

Selling Options: Determine if your strike price is likely to be hit before expiration

Buying Options: Estimate probability of reaching profit targets within your time window

Time Decay Management: Compare expected time-to-target vs theta decay

Example: You're considering selling a 30-day call option 5% out of the money. The indicator shows there's a 72% chance price hits +5% within 12 days. This tells you the trade has high assignment risk.

2. Swing Trading

Entry Timing: Wait for higher probability setups when directional bias is strong

Target Setting: Use median time-to-target to set realistic profit expectations

Stop Loss Placement: Understand probability of hitting your stop before target

Example: The indicator shows 85% upside probability with median time of 3.2 days. You can confidently enter long positions with appropriate position sizing.

3. Risk Management

Position Sizing: Larger positions when probability heavily favors one direction

Portfolio Allocation: Reduce exposure when probabilities are near 50/50 (high uncertainty)

Hedge Timing: Know when to add protective positions based on downside probability

Example: Indicator shows 55% upside vs 45% downside—nearly neutral. This signals high uncertainty, suggesting reduced position size or wait for better setup.

4. Market Regime Detection

Trending Markets: High directional bias (70%+ one direction)

Range-bound Markets: Balanced probabilities (45-55% both directions)

Volatility Regimes: Compare actual vs theoretical minimum time

Example: Consistent 90%+ bullish bias across multiple timeframes confirms strong uptrend—stay long and avoid counter-trend trades.

First Hit Rate (Most Important!)

Shows which threshold is likely to be hit FIRST:

Upside %: Probability of hitting upside target before downside

Downside %: Probability of hitting downside target before upside

These always sum to 100%

⚠️ Warning: If you see "Low Hit Rate" warning, increase this parameter!

Advanced Parameters

Drift Mode

Allows you to explore different scenarios:

Historical: Uses actual recent trend (default—most realistic)

Zero (Neutral): Assumes no trend, only volatility (symmetric probabilities)

50% Reduced: Dampens trend effect (conservative scenario)

Use Case: Switch to "Zero (Neutral)" to see what happens in a pure volatility environment, useful for range-bound markets.

Distribution Type

Percentile: Shows 10%, 25%, 50%, 75%, 90% levels (recommended for most users)

Sigma: Shows standard deviation levels (1σ, 2σ)—useful for statistical analysis

⚠️ Important Limitations & Best Practices

Limitations

Assumes GBM: Real markets have fat tails, jumps, and regime changes not captured by GBM

Historical Parameters: Uses recent volatility/drift—may not predict regime shifts

No Fundamental Events: Cannot predict earnings, news, or macro shocks

Computational: Runs only on last bar—doesn't give historical signals

Remember: Probabilities are not certainties. Use this indicator as part of a comprehensive trading plan with proper risk management.

Created by: Henrique Centieiro. feedback is more than welcome!

Historical Volatility

Omega ATR Indicator📖 Introduction

The Ω ATR Indicator was created to provide a more complete and professional framework for volatility analysis than the classic Average True Range (ATR).

While the traditional ATR is a useful tool, it has limitations: it delivers a simple rolling average of volatility, but it does not adapt to market regimes, it does not highlight extreme events, and it often leaves the trader with incomplete information about risk.

The Ω ATR takes the same foundation and elevates it into a multi-dimensional volatility dashboard, adding statistical layers, adaptive calculations, and clear visual references that allow traders to interpret volatility in a way that is immediately actionable.

🔎 What makes it different from a standard ATR?

This indicator introduces several features beyond the classic formula:

True Range Core – plots the raw True Range (TR) for each bar, providing a direct, bar-by-bar view of volatility impulses.

Standard & Adjusted ATR – includes both the conventional ATR (smoothed average) and an Adjusted ATR that automatically corrects for extreme conditions by incorporating percentile rescaling.

Percentile Volatility Levels – dynamically calculated extreme thresholds (99.8%, 75%, 50%, 25%), plotted as dotted levels across the chart. These act as reference lines for “normal” vs. “abnormal” volatility, useful for spotting unusual price expansions or contractions.

Linear Regression Volatility Trend – overlays a regression line of volatility, showing whether the market is moving toward expansion (rising vol), contraction (falling vol), or stability.

Monetary Value Translation – the indicator converts volatility into points, ticks, and dollar values (based on the instrument’s point value). This allows futures traders and high-value instruments users to immediately see how much volatility is “worth” in cash terms.

Interactive Table Display – a real-time statistics table is displayed directly on the chart, showing:

SMA of ATR in $ and points

Percentile-based volatility range (VAR) in $ and points

Tick equivalences, for quick position sizing

⚡ How traders can use it

The Ω ATR Indicator is designed to be versatile, fitting both discretionary traders and systematic strategy developers.

Risk Management: ATR-based stop losses and position sizing are significantly improved by using the adjusted ATR and percentile thresholds. Traders can size their positions according to volatility regimes, not just raw averages.

Breakout & Exhaustion Detection: When TR or ATR values spike above the 99.8% or 95% percentile levels, this often corresponds to breakout conditions or volatility exhaustion — useful for breakout strategies, mean-reversion setups, and volatility fades.

Market Regime Identification: The regression line helps distinguish if volatility is rising (trending environment, larger swings expected) or compressing (range-bound environment, lower risk opportunities).

Multi-Asset Flexibility: Works equally well on equities, futures, crypto, and FX. Its point/tick/dollar conversion makes it especially powerful for futures traders who need to quantify risk precisely.

Scalping to Swing Trading: On lower timeframes, it acts as a micro-volatility detector; on higher timeframes, it functions as a strategic risk gauge for position management.

⚙️ Settings and Customization

Length: The ATR lookback period (default = 34).

Shorter lengths (14–21) for intraday traders who want fast response.

Longer lengths (34–55) for swing/position traders who want smoother readings.

AVG / ADJ AVG: Toggle to display the standard ATR or the adjusted ATR.

Volatility Levels: Enable/disable up to 4 percentile-based levels (1st = 25%, 2nd = 50%, 3rd = 75%, 4th = 99.8%). Recommended: keep 3 levels active for clarity.

Color Controls: All plots and levels are fully customizable to match your chart style.

Table Display: Positioned on the chart (default: middle-right) with key values updated in real time.

🧭 Best Practices for Use

Combine with Trend Tools: Volatility readings are most powerful when combined with trend filters or volume analysis. For example, a breakout with both high volatility and trend confirmation is stronger than either alone.

ATR Stops: Use the Adjusted ATR rather than the standard one when trailing stops in highly volatile instruments like crypto or Nasdaq futures, as it adapts to outlier spikes.

Dollar Risk Translation: Use the dollar-value outputs to predefine maximum acceptable risk per trade (e.g., “I only risk $250 per position”). This bridges volatility to portfolio risk management.

Event Monitoring: Around economic events or earnings, expect volatility spikes above higher percentile levels. The indicator makes these moves instantly visible.

📌 Summary

The Ω ATR Indicator is not just “another ATR.” It is a comprehensive volatility framework that transforms volatility from a simple statistic into an actionable trading signal.

By combining:

the classic ATR,

an adjusted ATR,

percentile extremes,

regression-based volatility trends,

and real-time dollar conversions,

…this tool allows traders to precisely understand, visualize, and act on volatility in ways that a standard ATR simply cannot provide.

Whether you are scalping intraday moves, swing trading equities, or managing futures positions, the Ω ATR equips you with a professional-grade volatility dashboard that clarifies risk, highlights opportunity, and adapts across all markets and timeframes.

👉 Designed and developed by OmegaTools for traders who demand precision, clarity, and adaptability in their volatility analysis.

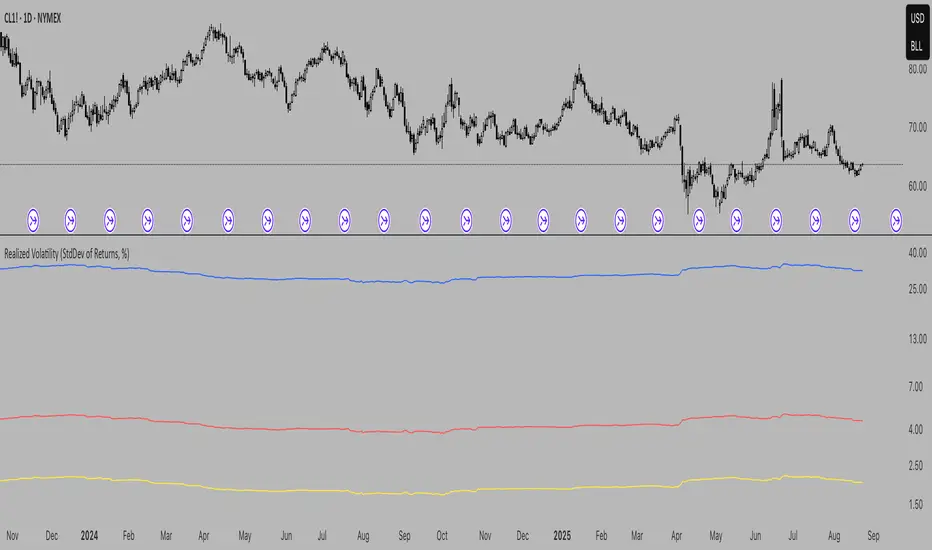

Realized Volatility (StdDev of Returns, %)Realized Volatility (StdDev of Returns, %)

This indicator measures realized (historical) volatility by calculating the standard deviation of log returns over a user-defined lookback period. It helps traders and analysts observe how much the price has varied in the past, expressed as a percentage.

How it works:

Computes close-to-close logarithmic returns.

Calculates the standard deviation of these returns over the selected lookback window.

Provides three volatility measures:

Daily Volatility (%): Standard deviation over the chosen period.

Annualized Volatility (%): Scaled using the square root of the number of trading days per year (default = 250).

Horizon Volatility (%): Scaled to a custom horizon (default = 5 days, useful for short-term views).

Inputs:

Lookback Period: Number of bars used for volatility calculation.

Trading Days per Year: Used for annualizing volatility.

Horizon (days): Adjusts volatility to a shorter or longer time frame.

Notes:

This is a statistical measure of past volatility, not a forecasting tool.

If you change the scale to logarithmic, the indicator readibility improves.

It should be used for analysis in combination with other tools and not as a standalone signal.

Realized Volatility (StdDev of Returns, %)📌 Realized Volatility (StdDev of Returns, %)

This indicator measures realized volatility directly from price returns, instead of the common but misleading approach of calculating standard deviation around a moving average.

🔹 How it works:

Computes close-to-close log returns (the most common way volatility is measured in finance).

Calculates the standard deviation of these returns over a chosen lookback period (default = 200 bars).

Converts results into percentages for easier interpretation.

Provides three key volatility measures:

Daily Realized Vol (%) – raw standard deviation of returns.

Annualized Vol (%) – scaled by √250 trading days (market convention).

Horizon Vol (%) – volatility over a custom horizon (default = 5 days, i.e. weekly).

🔹 Why use this indicator?

Shows true realized volatility from historical returns.

More accurate than measuring deviation around a moving average.

Useful for traders analyzing risk, position sizing, and comparing realized vs implied volatility.

⚠️ Note:

It is best used on the Daily Chart!

By default, this uses log returns (which are additive and standard in quant finance).

If you prefer, you can easily switch to simple % returns in the code.

Volatility estimates depend on your chosen lookback length and may vary across timeframes.

Monthly Expected Move (IV + Realized)What it does

Overlays 1-month expected move bands on price using both forward-looking options data and backward-looking realized movement:

IV30 band — from your pasted 30-day implied vol (%)

Straddle band — from your pasted ATM ~30-DTE call+put total

HV band — from Historical Volatility computed on-chart

ATR band — from ATR% extrapolated to ~1 trading month

Use it to quickly answer: “How much could this stock move in ~1 month?” and “Is the market now pricing more/less movement than we’ve actually been getting?”

Inputs (quick)

Implied (forward-looking)

Use IV30 (%) — paste annualized IV30 from your options platform.

Use ATM 30-DTE Straddle — paste Call+Put total (per share) at the ATM strike, ~30 DTE.

Realized (backward-looking)

HV lookback (days) — default 21 (≈1 trading month).

ATR length — default 14.

Note: TradingView can’t fetch option data automatically. Paste the IV30 % or the straddle total you read from your broker (use Mark/mid prices).

How it’s calculated

IV band (±%) = IV30 × √(21/252) (annualized → ~1-month).

Straddle band (±%) = (ATM Call + Put) / Spot to that expiry (≈30 DTE).

HV band (±%) = stdev(log returns, N) × √252 × √(21/252).

ATR band (±%) = (ATR(len)/Close) × √21.

All bands are plotted as upper/lower envelopes around price, plus an on-chart readout of each ±% for quick scanning.

How to use it (at a glance)

IV/Straddle bands wider than HV/ATR → market expects bigger movement than recent actuals (possible catalyst/expansion).

All bands narrow → likely a low-mover; look elsewhere if you want action.

HV > IV → realized swings exceed current pricing (mean-reversion or vol bleed often follows).

Pro tips

For ATM straddle: pick the expiry closest to ~30 DTE, use the ATM strike (closest to spot), and add Call Mark + Put Mark (per share). If the exact ATM strike isn’t quoted, average the two neighboring strikes.

The simple straddle/spot heuristic can read slightly below the IV-derived 1σ; that’s normal.

Keep the chart on daily timeframe—the math assumes trading-day conventions (~252/yr, ~21/mo).

ATR Dynamische Candles 1.2 (by Droes)This script visualizes ATR values as candles to the right of the last candle at today's high and today's low.

ATR Daily Viz V30.0This script visualizes ATR values as candles to the right of the last candle at today's high and low.

This is the first version.

ATR Daily Viz V30.0This script visualizes ATR values as candles to the right of the last candle at today's high and low.

This is the first version.

Synthetic VX3! & VX4! continuous /VX futuresTradingView is missing continuous 3rd and 4th month VIX (/VX) futures, so I decided to try to make a synthetic one that emulates what continuous maturity futures would look like. This is useful for backtesting/historical purposes as it enables traders to see how their further out VX contracts would've performed vs the front month contract.

The indicator pulls actual realtime data (if you subscribe to the CBOE data package) or 15 minute delayed data for the VIX spot (the actual non-tradeable VIX index), the continuous front month (VX1!), and the continuous second month (VX2!) continually rolled contracts. Then the indicator's script applies a formula to fairly closely estimate how 3rd and 4th month continuous contracts would've moved.

It uses an exponential mean‑reversion to a long‑run level formula using:

σ(T) = θ+(σ0−θ)e−kT

You can expect it to be off by ~5% or so (in times of backwardation it might be less accurate).

Adaptive Squeeze Momentum +Adaptive Squeeze Momentum+ (Auto-Timeframe Version)

Overview

Adaptive Squeeze Momentum+ is an enhanced volatility and momentum indicator designed to identify compression and expansion phases in price action. It is inspired by the classic Squeeze Momentum Indicator by LazyBear but introduces automatic parameter adaptation to any timeframe, making it simpler to use across different markets without manual configuration.

Concepts and Methodology

The script combines Bollinger Bands (BB) and Keltner Channels (KC) to detect periods when volatility contracts (squeeze) or expands (release).

A squeeze occurs when BB are inside KC, suggesting low volatility and potential breakout scenarios.

A squeeze release is detected when BB expand outside KC.

Momentum is derived using a linear regression applied to the difference between price and a midrange reference level.

Original Improvements

Compared to the original Squeeze Momentum Indicator, this version offers several enhancements:

Automatic Adaptation: BB and KC lengths and multipliers are dynamically adjusted based on the chart’s timeframe (from 1 minute up to 1 month), removing the need for manual tuning.

Simplified Visualization: A clean, minimalist histogram and clear squeeze state cross markers allow for faster interpretation.

Flexible Application: Designed to work consistently on intraday, daily, and higher timeframes across crypto, forex, stocks, and indices.

Features

Dynamic Squeeze Detection:

Gray Cross: Neutral (no squeeze detected)

Blue Cross: Active squeeze

Yellow Cross: Squeeze released

Momentum Histogram:

Positive/negative momentum shown with slope-based coloring.

Timeframe-Aware Parameters:

Automatically sets optimal BB/KC configurations.

Usage

Watch for blue crosses indicating an active squeeze phase that may precede a directional move.

Use the histogram color and slope to gauge momentum strength and direction.

Combine squeeze release signals with momentum confirmation for potential entries or exits.

Credits and Licensing

This script was inspired by LazyBear’s OLD “Squeeze Momentum Indicator” (). The implementation here significantly expands upon the original by introducing auto-adaptive parameters, restructured logic, and a new visualization approach. Published under the Mozilla Public License 2.0.

Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Use at your own risk.

volatility-adjusted breakout envelopethis indicator is designed to help traders visually identify potential entry and exit points based on volatility-adjusted price thresholds. it works by calculating a dynamic expected price move around the previous close using historical volatility data smoothed by exponential moving averages to reduce noise and present a clear range boundary on the chart.

the indicator first computes the logarithmic returns over a user-defined lookback period and calculates the standard deviation of these returns, which represents raw volatility. it annualizes this volatility according to the chart timeframe selected, then uses it to estimate an expected price movement for the current timeframe. this expected move is smoothed to avoid sudden spikes or drops that could cause confusing signals.

using this expected move, the indicator generates two key threshold lines: an upper threshold and a lower threshold. these lines create a volatility-based range around the smoothed previous close price. the thresholds themselves are further smoothed with exponential moving averages to produce smooth, easy-to-interpret lines that adapt to changing market conditions without being choppy.

the core trading signals are generated when the price closes outside of these smoothed threshold ranges. specifically, a long entry signal is indicated when the price closes above the upper threshold for the first time, signaling potential upward momentum beyond normal volatility expectations. a short entry signal occurs when the price closes below the lower threshold for the first time, indicating potential downward momentum.

once an entry signal is triggered, the indicator waits for the price to close back inside the threshold range before signaling an exit. when this occurs, an exit marker is displayed to indicate that the price has returned within normal volatility bounds, which may suggest that the previous trend is losing strength or the breakout has ended.

these signals are visually represented on the chart using small shapes: triangles pointing upwards mark the initial long entries, triangles pointing downwards mark short entries, and x shapes mark the exits for both long and short positions. the colors of these shapes are customizable to suit user preferences.

to use this indicator effectively, traders should watch for the first close outside the smoothed volatility range to consider entering a position in the breakout direction. the exit signals help identify when price action reverts back into the expected range, which can be used to close or reduce the position. this method emphasizes trading breakouts supported by statistically significant moves relative to recent volatility while providing a clear exit discipline.

this indicator is best applied to intraday or daily charts with consistent volatility and volume characteristics. users should adjust the volatility lookback period, smoothing factor, and trading session times to match their specific market and trading style. because it relies on price volatility rather than fixed price levels, it can adapt to changing market conditions but should be combined with other analysis tools and proper risk management.

overall, this indicator provides a smoothed, dynamic volatility envelope with clear visual entry and exit cues based on first closes outside and back inside these envelopes, making it a helpful assistant for manual traders seeking to capture statistically significant breakouts while maintaining disciplined exits.

VWAP Deviation Channels with Probability (Lite)VWAP Deviation Channels with Probability (Lite)

Version 1.2

Overview

This indicator is a powerful tool for intraday traders, designed to identify high-probability areas of support and resistance. It plots the Volume-Weighted Average Price (VWAP) as a central "value" line and then draws statistically-based deviation channels around it.

Its unique feature is a dynamic probability engine that analyzes thousands of historical price bars to calculate and display the real-time likelihood of the price touching each of these deviation levels. This provides a quantifiable edge for making trading decisions.

Core Concepts Explained

This indicator is built on three key concepts:

The VWAP (Volume-Weighted Average Price): The dotted midline of the channels is the session VWAP. Unlike a Simple Moving Average (SMA) which only considers price, the VWAP incorporates volume into its calculation. This makes it a much more significant benchmark, as it represents the true average price where the most business has been transacted during the day. It's heavily used by institutional traders, which is why price often reacts strongly to it.

Standard Deviation Channels: The channels above and below the VWAP are based on standard deviations. Standard deviation is a statistical measure of volatility.

- Wide Bands: When the channels are wide, it signifies high volatility.

- Narrow Bands: When the channels are tight and narrow, it signifies low volatility and

consolidation (a "squeeze").

The Conditional Probability Engine: This is the heart of the indicator. For every deviation level, the script displays a percentage. This percentage answers a very specific question:

"Based on thousands of previous bars, when the last candle had a certain momentum (bullish or bearish), what was the historical probability that the price would touch this specific level?"

The probabilities are calculated separately depending on whether the previous candle was green (bullish) or red (bearish). This provides a nuanced, momentum-based edge. The level with the highest probability is highlighted, acting as a "price magnet."

How to Use This Indicator

Recommended Timeframes:

This indicator is designed specifically for intraday trading. It works best on timeframes like the 1-minute, 5-minute, and 15-minute charts. It will not display correctly on daily or higher timeframes.

Recommended Trading Strategy: Mean Reversion

The primary strategy for this indicator is "Mean Reversion." The core idea is that as the price stretches to extreme levels far away from the VWAP (the "mean"), it is statistically more likely to "snap back" toward it.

Here is a step-by-step guide to trading this setup:

1. Identify the Extreme: Wait for the price to push into one of the outer deviation bands (e.g., the -2, -3, or -4 bands for a buy setup, or the +2, +3, or +4 bands for a sell setup).

2. Look for the High-Probability Zone: Pay close attention to the highlighted probability label. This is the level that has historically acted as the strongest magnet for price. A touch of this level represents a high-probability area for a potential reversal.

3. Wait for Confirmation: Do not enter a trade just because the price has touched a band. Wait for a confirmation candle that shows momentum is shifting.

- For a Buy: Look for a strong bullish candle (e.g., a green engulfing candle or a hammer/pin

bar) to form at the lower bands.

- For a Sell: Look for a strong bearish candle (e.g., a red engulfing candle or a shooting star)

to form at the upper bands.

Define Your Exit:

- Take Profit: A logical primary target for a mean reversion trade is the VWAP (midLine).

- Stop Loss: A logical place for a stop-loss is just outside the next deviation band. For

example, if you enter a long trade at the -3 band, your stop loss could be placed just

below the -4 band.

Disclaimer: This indicator is a tool for analysis and should not be considered a standalone trading system. Trading involves significant risk, and past performance is not indicative of future results. Always use this indicator in conjunction with other forms of analysis and sound risk management practices.

ATR Screener with Labels and ShapesWeekly Daily ATR Pine Scanner

To find out tightness or contraction in a stock we needs to check if volatality is decreasing as well as compared to previous 14 or 10 bars volatility . we check this for weekly and then for Daily , so that we can enter in a stock which is tightest in recent times.

Condition is :

1. Weekly Candle ATR x 0.8 < 10 Week ATR

2. Daily Candle ATR x 0.6 < 14 Day ATR

When both of the conditions are met then they signifies that the stock has tightened in weekly and daily aswell . so now we can find ways to enter during max squeeze.

How to scan in Pine Scanner ?

FIrst add indicator as favourite and Go to pine scanner page in trading view and then scan your watchlist and there you will see 3 columns 1 with only Weekly conditions met , 2 with only Daily and 3rd with Both conditions met .

Select stocks and move to new watchlist and now you have those stocks which has contracted the most in recent times .

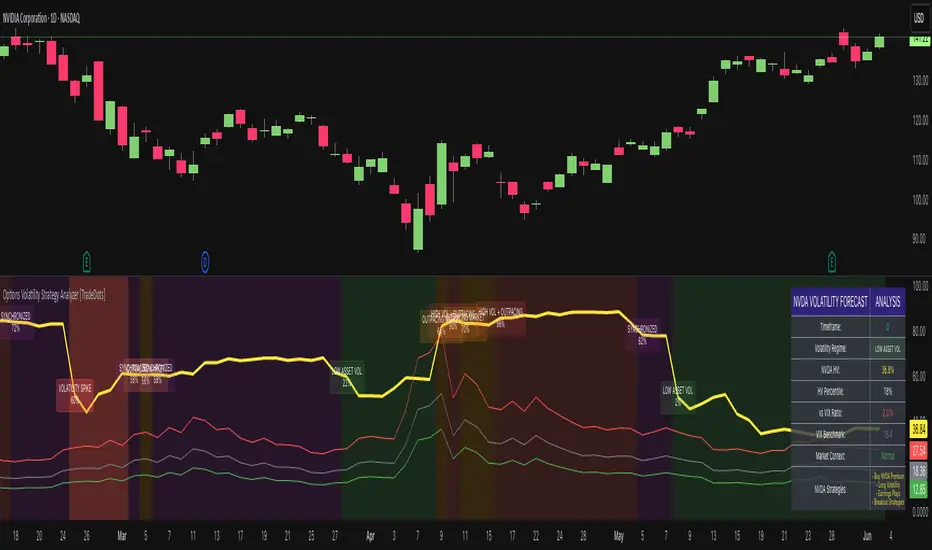

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Support and Resistance Profile with Volatility ClusteringThe indicator begins by looking at recent volatility behavior in the market: it measures the average true range over your chosen “Length” and compares it to the average true range over ten times that period. When volatility over the short window is high relative to longer-term volatility, we mark that period as a “cluster.” As price moves through these clusters—whether in a quiet period or a sudden burst of activity—the script isolates each cluster and examines the sequence of closing prices within it.

Within every cluster, the algorithm next finds the points along the price path that matter most to a human eye, smoothing out minor wobbles and highlighting the peaks and valleys that define the cluster’s shape. It does this by drawing a straight line between the beginning and end of the cluster, then repeatedly snapping the single point that deviates most from that line back onto it and re-interpolating, until it has identified a fixed number of perceptually important points. Those points capture where price really turned or accelerated, stripping away noise so that you see the genuine memory-markers in each volatility episode.

Each of those important points inherits a “weight” based on the cluster’s normalized volatility—essentially how large the average true range in that cluster was relative to its average close. Over your “Main Length for Profile” window, every time one of these weighted points occurs at a particular price level, it adds to a running total in that level’s bin. At the end of the window you see a silhouette of boxes extending to the right of the chart: where boxes are wide, many important points (with high volatility weight) have happened there in the past; where boxes are thin or absent, price memory is light.

For a trader, the value of this profile lies in spotting zones where the market has repeatedly “remembered” price extremes during volatile episodes—those are areas where support or resistance is likely to be strongest. Conversely, gaps in the profile—price levels with little weighted history—suggest frictionless zones. If price enters such a gap, it may move swiftly until it encounters another region of heavy memory. You can use this in several ways: as a filter on breakouts and breakdowns (only trade through a gap when you see sufficient momentum), as a guide for scaling into positions (add when price enters a low-memory zone and tighten stops where memory boxes thicken), or to anticipate where price might pause or reverse (when it reaches a band of wide boxes). By turning raw volatility clusters into a human-readable map of price memory, this tool helps you see at a glance where the market is likely to push or pause—and plan entries, exits, and risk targets accordingly.

Statistical Reliability Index (SRI)Statistical Reliability Index (SRI)

The Statistical Reliability Index (SRI) is a professional financial analysis tool designed to assess the statistical stability and reliability of market conditions. It combines advanced statistical methods to gauge whether current market trends are statistically consistent or prone to erratic behavior. This allows traders to make more informed decisions when navigating trending and choppy markets.

Key Concepts:

1. Extrapolation of Cumulative Distribution Functions (CDF)

What is CDF?

A Cumulative Distribution Function (CDF) is a statistical tool that models the probability of a random variable falling below a certain value.

How it’s used in SRI:

The SRI utilizes the 95th percentile CDF of recent returns to estimate the likelihood of extreme price movements. This helps identify when a market is experiencing statistically significant changes, crucial for forecasting potential breakouts or breakdowns.

Weight in SRI:

The weight of the CDF extrapolation can be adjusted to emphasize its impact on the overall reliability index, allowing customization based on the trader's preference for tail risk analysis.

2. Bias Factor (BF)

What is the Bias Factor?

The Bias Factor measures the ratio of the current market price to the expected mean price calculated over a defined period. It represents the deviation from the typical price level.

How it’s used in SRI:

A higher bias factor indicates that the current price significantly deviates from the historical average, suggesting a potential mean reversion or trend exhaustion.

Weight in SRI:

Adjusting the Bias Factor weight lets users control how much this deviation influences the SRI, balancing between momentum trading and mean reversion strategies.

3. Coefficient of Variation (CV)

What is CV?

The Coefficient of Variation (CV) is a statistical measure that expresses the ratio of the standard deviation to the mean. It indicates the relative variability of asset returns, helping gauge the risk-to-return consistency.

How it’s used in SRI:

A lower CV indicates more stable and predictable price behavior, while a higher CV signals increased volatility. The SRI incorporates the inverse of the normalized CV to reflect price stability positively.

Weight in SRI:

By adjusting the CV weight, users can prioritize consistent price movements over erratic volatility, aligning the indicator with risk tolerance and strategy preferences.

Interpreting the SRI:

1. SRI Plot:

The SRI plot dynamically changes color to reflect market conditions:

Aqua Line: Indicates uptrend stability, signaling statistically consistent upward movements.

Fuchsia Line: Indicates downtrend stability, where statistically reliable downward movements are present.

The overlay background shifts between colors:

Aqua Background: Signifies statistical stability, where trends are historically consistent.

Fuchsia Background: Indicates statistical instability, often associated with trend uncertainty.

Yellow Background: Marks choppy periods, where statistical data suggests that market conditions are not conducive to reliable trading.

2. SRI Volatility Plot:

Displays the volatility of the SRI itself to detect when the indicator is stable or unstable:

Blue Area Fill: Signifies that the SRI is stable, indicating trending conditions.

Yellow Area Fill: Represents choppy or unstable SRI movements, suggesting sideways or unreliable market conditions.

A Chop Threshold Line (dotted yellow) highlights the maximum acceptable SRI volatility before the market is considered too unpredictable.

3. Stability Assessment:

Stable Trend (No Chop):

The SRI is smooth and consistent, often accompanied by aqua or fuchsia lines.

Volatility remains below the chop threshold, indicating a low-risk, trend-following environment.

Chop Mode:

The SRI becomes erratic, and the volatility plot spikes above the threshold.

Marked by a yellow shaded background, indicating uncertain and non-trending conditions.

[Trend Identification:

Use the color-coded SRI line and background to determine uptrend or downtrend reliability.

Be cautious when the SRI volatility plot shows yellow, as this signals trading conditions may not be reliable.

Practical Use Cases:

Trend Confirmation:

Utilize the SRI plot color and background to confirm whether a detected trend is statistically reliable.

Chop Mode Filtering:

During yellow chop periods, it is advisable to reduce trading activity or adopt range-bound strategies.

Strategy Filter:

Combine the SRI with trend-following indicators (like moving averages) to enhance entry and exit accuracy.

Volatility Monitoring:

Pay attention to the SRI volatility plot, as spikes often precede erratic price movements or trend reversals.

Disclaimer:

The Statistical Reliability Index (SRI) is a technical analysis tool designed to aid in market stability assessment and trend validation. It is not intended as a standalone trading signal generator. While the SRI can help identify statistically reliable trends, it is essential to incorporate additional technical and fundamental analysis to make well-informed trading decisions.

Trading and investing involve substantial risk, and past performance does not guarantee future results. Always use risk management practices and consult with a financial advisor to tailor strategies to your individual risk profile and objectives.

Daily Price RangeThe indicator is designed to analyze an instrument’s volatility based on daily extremes (High-Low) and to compare the current day’s range with the typical (median) range over a selected period. This helps traders assess how much of the "usual" daily movement has already occurred and how much may still be possible during the trading day.

[NIC] Volatility Anomaly Indicator (Inspired by Jeff Augen)Volatility Anomaly Indicator (Inspired by Jeff Augen)

The Volatility Anomaly Indicator, inspired by Jeff Augen’s The Volatility Edge in Options Trading, helps traders spot price distortions by analyzing volatility imbalances. It compares short-term (10-day) and long-term (30-day) historical volatility (HV), plotting the ratio in a subgraph with clusters of dots to highlight anomalies—red for volatility spikes (potential sells) and green for calm periods (potential buys).

Originality: This indicator uniquely adapts Augen’s volatility concepts into a visual tool, focusing on relative volatility distortions rather than absolute levels, making it ideal for volatile assets like $TQQQ.

Features:

Calculates the ratio of short-term to long-term volatility.

Detects spikes (ratio > 1.5) and calm periods (ratio < 0.67) with customizable thresholds.

Plots volatility ratio as a blue line, with red/green dots for anomalies.

Includes optional buy/sell signals on the main chart (if overlay is enabled).

How It Works

The indicator computes historical volatility using log returns, then calculates the short-term to long-term volatility ratio. Spikes and calm periods are marked with dots in the subgraph, and threshold lines (1.5 and 0.67) provide context. Buy signals (green triangles) trigger during calm periods, and sell signals (red triangles) during spikes.

How to Use

Apply to any chart (e.g., NASDAQ:TQQQ daily).

Adjust inputs: Short Volatility Period (10), Long Volatility Period (30), Volatility Spike Threshold (1.5).

Watch for red dot clusters (spikes, potential sells) and green dot clusters (calm, potential buys).

Combine with price action or RSI for confirmation.

Why Use This Indicator?

Focuses on volatility-driven price inefficiencies.

Clear visualization with dot clusters.

Customizable for different assets and timeframes.

Limitations

Not a standalone system; requires confirmation.

May give false signals in choppy markets.

Volatility Regime Classifier | ATRP Percentile ZonesThis indicator helps you understand the current volatility environment of any asset by comparing recent ATR-based values to its historical range.

It defines four regimes:

🔴 Low Volatility: Volatility is decreasing

🟢 Normal: Volatility is increasing but still below average

🟠 High: Volatility is elevated

🟣 Extreme: Volatility is very high compared to recent history

⚙️ How it works

We calculate the Average True Range (ATR) as a percentage of price (ATRP), then compare a short-term ATR to a longer-term one. Their difference shows whether volatility is picking up or slowing down.

To make the signal more adaptive, we look at the distribution of recent volatility over a rolling window. We compute the 50th and 70th percentiles of that history to set dynamic thresholds.

About distribution & percentiles

Volatility in financial markets doesn't follow a normal (Gaussian) distribution, it's often skewed, with sudden spikes and fat tails. That means fixed thresholds (like "ATR > 20") can be misleading or irrelevant across assets and timeframes.

Using percentiles solves this:

The 50th percentile marks the middle of the recent volatility range.

The 70th percentile captures a zone where volatility is unusually high, but not too rare, which keeps the signal usable and not overly sensitive.

These levels offer a balance:

⚖️ not too reactive, not too slow — just enough to highlight meaningful shifts.

✅ Use cases

Spot changes in market conditions

Filter or adapt strategies depending on the regime

Adjust position sizing and risk dynamically

Tremor Tracker [theUltimator5]Tremor Tracker is a volatility monitoring tool that visualizes the "tremors" of price action by measuring and analyzing the average volatility of the current trading range, working on any timeframe. This indicator is designed to help traders detect when the market is calm, when volatility is building, and when it enters a potentially unstable or explosive state by using a lookback period to determine the average volatility and highlights outliers.

🔍 What It Does

Calculates bar-level volatility as the percentage difference between the high and low of each candle.

Applies a user-selected moving average (SMA, EMA, or WMA) to smooth out short-term noise and highlight trends in volatility.

Compares current volatility to its long-term average over a configurable lookback period.

Dynamically colors each volatility bar based on how extreme it is relative to historical behavior:

🟢 Lime — Low volatility (subdued, ranging conditions)

🟡 Yellow — Moderate or building volatility

🟣 Fuchsia — Elevated or explosive volatility

⚙️ Customizable Settings

Low Volatility Limit and High Volatility Limit: Define the thresholds for color changes based on volatility's ratio to its average.

Volatility MA Length: Adjust the smoothing period for the volatility moving average.

Average Volatility Lookback: Set how many bars are used to calculate the long-term average.

MA Type: Choose between SMA, EMA, or WMA for smoothing.

Show Volatility MA Line?: Toggle the display of the smoothed volatility trendline.

Show Raw Volatility Bars?: Toggle the display of raw per-bar volatility with dynamic coloring.

🧠 Use Cases

Identify breakout conditions: When volatility spikes above average, it may signal the onset of a new trend or a news-driven breakout.

Avoid chop zones: Prolonged periods of low volatility often precede sharp moves — a classic “calm before the storm” setup.

Timing reversion trades: Detect overextended conditions when volatility is well above historical norms.

Adapt strategies by volatility regime: Use color feedback to adjust risk, position sizing, or strategy selection based on real-time conditions.

📌 Notes

Volatility is expressed as a percentage, making this indicator suitable for use across different timeframes and asset classes.

The tool is designed to be visually intuitive, so traders can quickly spot evolving volatility states without diving into raw numbers.

ATR % Oscillator - DolphinTradeBot1️⃣ Overview

🔸 This is a simplified version of ATR and TR that shows volatility as percentage changes , making it easier to compare two symbols.

🔸 The indicator compares the volatility of two different assets by calculating the percentage-based price ranges and their moving averages .

📌 This is especially useful for pair traders, as it helps identify which symbol is more volatile, allowing for strategic decisions based on relative movement rather than overall market direction.

2️⃣ How Is It Work?

🔸 For each symbol, it calculates the absolute percentage difference between either:

• Close and Open (net price change), or

• High and Low (daily price range).

🔸 The results are visualized as column bars — the taller the bar, the higher the volatility.

🔸 It also plots a moving average line (SMA) based on the selected range length.

📌 These calculations are independent of the chart you're on — they work purely based on the two selected symbols.

If no symbols are selected, it defaults to using the current chart's symbol.

3️⃣ How to Use It?

With this indicator, you can:

🔸 Compare the volatility between two assets.

🔸 Detect sudden volatility spikes that may signal upcoming momentum.

🔸 Support spread, arbitrage, or correlation-based strategies .

🔸 See which symbol is gaining market attention (a larger difference = more activity).

Example: Compare BTC vs ETH to see which one is dominating in terms of price action or volatility.

4️⃣⚙️ Settings

🔸 Symbol Settings

• Symbol-1 / Symbol-2: Choose the two assets to compare.

• Checkboxes: Enable/disable visibility for each symbol's data.

🔸 Calculation Settings

• Range Average: The number of bars used for the moving average.

• Calculation Source:

- Close-Open: Measures net price movement.

- High-Low: Measures total price range.

(US) Historical Trade WarsHistorical U.S. Trade Wars Indicator

Overview

This indicator visualizes major U.S. trade wars and disputes throughout modern economic history, from the McKinley Tariff of 1890 to recent U.S.-China tensions. This U.S.-focused timeline is perfect for macro traders, economic historians, and anyone looking to understand how America's trade conflicts correlate with market movements.

Features

Comprehensive U.S. Timeline: Covers 130+ years of U.S.-centered trade disputes with historically accurate dates.

Color-Coded Events:

🔴 Red: Marks the beginning of a U.S. trade war or major dispute.

🟡 Yellow: Highlights significant events within a trade conflict.

🟢 Green: Shows resolutions or ends of trade disputes.

Global Partners/Rivals: Tracks U.S. trade relations with China, Japan, EU, Canada, Mexico, Brazil, Argentina, and others.

Country Flags: Uses emoji flags for easy visual identification of nations in trade relations with the U.S.

Major Trade Wars Covered:

McKinley Tariff (1890-1894)

Smoot-Hawley Tariff Act (1930-1934)

U.S.-Europe Chicken War (1962-1974)

Multifiber Arrangement Quotas (1974-2005)

Japan-U.S. Trade Disputes (1981-1989)

NAFTA and Softwood Lumber Disputes

Clinton and Bush-Era Steel Tariffs

Obama-Era China Tire Tariffs

Rare Earth Minerals Dispute (2012-2014)

Solar Panel Dispute (2012-2015)

TPP and TTIP Negotiations

U.S.-China Trade War (2018-present)

Airbus-Boeing Dispute

Usage

Analyze how markets historically responded to trade war initiations and resolutions.

Identify patterns in market behavior during periods of trade tensions.

Use as an overlay with price action to examine correlations.

Perfect companion for macro analysis on daily, weekly, or monthly charts.

About

This indicator is designed as a historical reference tool for traders and economic analysts focusing on U.S. trade policy and its global impact. The dates and events have been thoroughly researched for accuracy. Each label includes emojis to indicate the U.S. and its trade partners/rivals, making it easy to track America's evolving trade relationships across time.

Note: This indicator works best on larger timeframes (daily, weekly, monthly) due to the historical span covered.

PumpC Opening Range Breakout (ORB) Stretch RangePumpC ORB Stretch

The PumpC ORB Stretch is a volatility-based indicator that helps traders identify potential breakout zones by analyzing how price typically behaves around the open. This tool is inspired by concepts introduced by Toby Crabel in his well-known book “Day Trading with Short-Term Price Patterns and Opening Range Breakout.”

Rather than predicting market direction, this indicator highlights areas where price is likely to expand based on recent volatility. It is designed for traders who prefer dynamic, data-driven breakout levels over static support and resistance zones.

What Is the "Stretch"?

In Toby Crabel’s framework, the Stretch is the average of the smaller of two price moves:

The distance from the open to the high of the bar

The distance from the open to the low of the bar

This smaller value captures the “quiet side” of the candle and reflects recent price compression. Averaged over multiple periods (commonly 10 daily bars), it creates a baseline to assess how far price may move away from the open under typical market conditions.

How the Indicator Works

The PumpC ORB Stretch follows this process:

Uses a higher timeframe (such as daily) to calculate the open, high, and low.

For each bar, measures the smaller of the two distances: open to high or open to low.

Applies a moving average to the result over a user-defined number of bars (default is 10).

Multiplies the average stretch by customizable levels (e.g., 0.382, 1.0, 2.0).

Plots breakout levels above and below the open of the selected timeframe.

The result is a set of adaptive levels that expand or contract with market volatility.

Customization Options

Stretch Timeframe: Choose the timeframe used for stretch calculation (default: Daily).

Stretch Length: Set the number of bars to include in the moving average.

Breakout Levels: Enable or disable individual levels and define multipliers.

Color Settings: Customize colors for each range level for easy visual distinction.

Plot Style: Circular markers are used to reduce chart clutter and improve readability.

How to Use It

Use plotted levels to anticipate possible breakouts from the open.

Adjust stretch length to reflect short-term or longer-term volatility trends.

Combine this tool with momentum indicators, volume, or price action for confirmation.

Use levels to help guide stop placement or profit targets in breakout strategies.

Important Notes

This script is based on an interpretation of Crabel’s concepts and is not affiliated with Crabel Capital or the original author.

The indicator does not predict direction; it is a tool for context and structure.

It is recommended that users test and validate this tool in a simulated environment before applying it to live trading.

This indicator is intended for educational purposes only.

Licensing and Attribution

This script is built entirely in Pine Script v5 and follows TradingView’s open-source standards. It does not include any third-party or proprietary code. If you modify or share it, please credit the original idea and follow all TradingView script publishing rules.