Market Cap Landscape 3DHello, traders and creators! 👋

Market Cap Landscape 3D. This project is more than just a typical technical analysis tool; it's an exploration into what's possible when code meets artistry on the financial charts. It's a demonstration of how we can transcend flat, two-dimensional lines and step into a vibrant, three-dimensional world of data.

This project continues a journey that began with a previous 3D experiment, the T-Virus Sentiment, which you can explore here:

The Market Cap Landscape 3D builds on that foundation, visualizing market data—particularly crypto market caps—as a dynamic 3D mountain range. The entire landscape is procedurally generated and rendered in real-time using the powerful drawing capabilities of polyline.new() and line.new() , pushed to their creative limits.

This work is intended as a guide and a design example for all developers, born from the spirit of learning and a deep love for understanding the Pine Script™ language.

---

🧐 Core Concept: How It Works

The indicator synthesizes multiple layers of information into a single, cohesive 3D scene:

The Surface: The mountain range itself is a procedurally generated 3D mesh. Its peaks and valleys create a rich, textured landscape that serves as the canvas for our data.

Crypto Data Integration: The core feature is its ability to fetch market cap data for a list of cryptocurrencies you provide. It then sorts them in descending order and strategically places them onto the 3D surface.

The Summit: The highest point on the mountain is reserved for the asset with the #1 market cap in your list, visually represented by a flag and a custom emblem.

The Mountain Labels: The other assets are distributed across the mountainside, with their rank determining their general elevation. This creates an intuitive visual hierarchy.

The Leaderboard Pole: For clarity, a dedicated pole in the back-right corner provides a clean, ranked list of the symbols and their market caps, ensuring the data is always easy to read.

---

🧐 Example of adjusting the view

To evoke the feeling of flying over mountains

To evoke the feeling of looking at a mountain peak on a low plain

🧐 Example of predefined colors

---

🚀 How to Use

Getting started with the Market Cap Landscape 3D:

Add to Chart: Apply the "Market Cap Landscape 3D" indicator to your active chart.

Open Settings: Double-click anywhere on the 3D landscape or click the "Settings" icon next to the indicator's name.

Customize Your Crypto List: The most important setting is in the Crypto Data tab. In the "Symbols" text area, enter a comma-separated list of the crypto tickers you want to visualize (e.g., BTC,ETH,SOL,XRP ). The indicator supports up to 40 unique symbols.

> Important Note: This indicator exclusively uses TradingView's `CRYPTOCAP` data source. To find valid symbols, use the main symbol search bar on your chart. Type `CRYPTOCAP:` (including the colon) and you will see a list of available options. For example, typing `CRYPTOCAP:BTC` will confirm that `BTC` is a valid ticker for the indicator's settings. Using symbols that do not exist in the `CRYPTOCAP` index will result in a script error. or, to display other symbols, simply type CRYPTOCAP: (including the colon) and you will see a list of available options.

Adjust Your View: Use the settings in the Camera & Projection tab to rotate ( Yaw ), tilt ( Pitch ), and scale the landscape until you find a view you love.

Explore & Customize: Play with the color palettes, flag design, and other settings to make the landscape truly your own!

---

⚙️ Settings & Customization

This indicator is highly customizable. Here’s a breakdown of what each setting does:

#### 🪙 Crypto Data

Symbols: Enter the crypto tickers you want to track, separated by commas. The script automatically handles duplicates and case-insensitivity.

Show Market Cap on Mountain: When checked, it displays the full market cap value next to the symbol on the mountain. When unchecked, it shows a cleaner look with just the symbol and a colored circle background.

#### 📷 Camera & Projection

Yaw (°): Rotates the camera view horizontally (side to side).

Pitch (°): Tilts the camera view vertically (up and down).

Scale X, Y, Z: Stretches or compresses the landscape in width, depth, and height, respectively. Fine-tune these to get the perfect perspective.

#### 🏞️ Grid / Surface

Grid X/Y resolution: Controls the detail level of the 3D mesh. Higher values create a smoother surface but may use more resources.

Fill surface strips: Toggles the beautiful color gradient on the surface.

Show wireframe lines: Toggles the visibility of the grid lines.

Show nodes (markers): Toggles the small dots at each grid intersection point.

#### 🏔️ Peaks / Mountains

Fill peaks volume: Draws vertical lines on high peaks, giving them a sense of volume.

Fill peaks surface: Draws a cross-hatch pattern on the surface of high peaks.

Peak height threshold: Defines the minimum height for a peak to receive the fill effect.

Peak fill color/density: Customizes the appearance of the fill lines.

#### 🚩 Flags (3D)

Show Flag on Summit: A master switch to show or hide the flag and emblem entirely.

Flag height, width, etc.: Provides full control over the dimensions and orientation of the flag on the highest peak.

#### 🎨 Color Palette

Base Gradient Palette: Choose from 13 stunning, pre-designed color themes for the landscape, from the classic SUNSET_WAVE to vibrant themes like NEON_DREAM and OCEANIC .

#### 🛡️ Emblem / Badge Controls

This section gives you granular control over every element of the custom emblem on the flag. Tweak rotation, offsets, and scale to design your unique logo.

---

👨💻 Developer's Corner: Modifying the Core Logic

If you're a developer and wish to customize the indicator's core data source, this section is for you. The script is designed to be modular, making it easy to change what data is being ranked and visualized.

The heart of the data retrieval and ranking logic is within the f_getSortedCryptoData() function. Here’s how you can modify it:

1. Changing the Data Source (from Market Cap to something else):

The current logic uses request.security("CRYPTOCAP:" + syms.get(i), ...) to fetch market capitalization data. To change this, you need to modify this line.

Example: Ranking by RSI (14) on the Daily timeframe.

First, you'll need a function to calculate RSI. Add this function to the script:

f_getRSI(symbol, timeframe, length) =>

request.security(symbol, timeframe, ta.rsi(close, length))

Then, inside f_getSortedCryptoData() , find the `for` loop that populates the `caps` array and replace the `request.security` call:

// OLD LINE:

// caps.set(i, request.security("CRYPTOCAP:" + syms.get(i), timeframe.period, close))

// NEW LINE for RSI:

// Note: You'll need to decide how to format the symbol name (e.g., "BINANCE:" + syms.get(i) + "USDT")

caps.set(i, f_getRSI("BINANCE:" + syms.get(i) + "USDT", "D", 14))

2. Changing the Data Formatting:

The ranking values are formatted for display using the f_fmtCap() function, which currently formats large numbers into "M" (millions), "B" (billions), etc.

If you change the data source to something like RSI, you'll want to change the formatting. You can modify f_fmtCap() or create a new formatting function.

Example: Formatting for RSI.

// Modify f_fmtCap or create f_fmtRSI

f_fmtRSI(float v) =>

str.tostring(v, "#.##") // Simply format to two decimal places

Remember to update the calls to this function in the main drawing loop where the labels are created (e.g., str.format("{0}: {1}", crypto.symbol, f_fmtCap(crypto.cap)) ).

By modifying these key functions ( f_getSortedCryptoData and f_fmtCap ), you can adapt the Market Cap Landscape 3D to visualize and rank almost any dataset you can imagine, from technical indicators to fundamental data.

---

We hope you enjoy using the Market Cap Landscape 3D as much as we enjoyed creating it. Happy charting! ✨

อินดิเคเตอร์และกลยุทธ์

ZigzagLiteLibrary "ZigzagLite"

Lighter version of the Zigzag Library. Without indicators and sub-component divisions

method getPrices(pivots)

Gets the array of prices from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot prices

method getBars(pivots)

Gets the array of bars from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot bar indices

method getPoints(pivots)

Gets the array of chart.point from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot points

method getPoints(this)

Namespace types: Zigzag

Parameters:

this (Zigzag)

method calculate(this, ohlc, ltfHighTime, ltfLowTime)

Calculate zigzag based on input values and indicator values

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

ohlc (float ) : Array containing OHLC values. Can also have custom values for which zigzag to be calculated

ltfHighTime (int) : Used for multi timeframe zigzags when called within request.security. Default value is current timeframe open time.

ltfLowTime (int) : Used for multi timeframe zigzags when called within request.security. Default value is current timeframe open time.

Returns: current Zigzag object

method calculate(this)

Calculate zigzag based on properties embedded within Zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: current Zigzag object

method nextlevel(this)

Namespace types: Zigzag

Parameters:

this (Zigzag)

method clear(this)

Clears zigzag drawings array

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing ) : array

Returns: void

method clear(this)

Clears zigzag drawings array

Namespace types: ZigzagDrawingPL

Parameters:

this (ZigzagDrawingPL ) : array

Returns: void

method drawplain(this)

draws fresh zigzag based on properties embedded in ZigzagDrawing object without trying to calculate

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

Returns: ZigzagDrawing object

method drawplain(this)

draws fresh zigzag based on properties embedded in ZigzagDrawingPL object without trying to calculate

Namespace types: ZigzagDrawingPL

Parameters:

this (ZigzagDrawingPL) : ZigzagDrawingPL object

Returns: ZigzagDrawingPL object

method drawfresh(this, ohlc)

draws fresh zigzag based on properties embedded in ZigzagDrawing object

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

Returns: ZigzagDrawing object

method drawcontinuous(this, ohlc)

draws zigzag based on the zigzagmatrix input

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

Returns:

PivotCandle

PivotCandle represents data of the candle which forms either pivot High or pivot low or both

Fields:

_high (series float) : High price of candle forming the pivot

_low (series float) : Low price of candle forming the pivot

length (series int) : Pivot length

pHighBar (series int) : represents number of bar back the pivot High occurred.

pLowBar (series int) : represents number of bar back the pivot Low occurred.

pHigh (series float) : Pivot High Price

pLow (series float) : Pivot Low Price

Pivot

Pivot refers to zigzag pivot. Each pivot can contain various data

Fields:

point (chart.point) : pivot point coordinates

dir (series int) : direction of the pivot. Valid values are 1, -1, 2, -2

level (series int) : is used for multi level zigzags. For single level, it will always be 0

ratio (series float) : Price Ratio based on previous two pivots

sizeRatio (series float)

ZigzagFlags

Flags required for drawing zigzag. Only used internally in zigzag calculation. Should not set the values explicitly

Fields:

newPivot (series bool) : true if the calculation resulted in new pivot

doublePivot (series bool) : true if the calculation resulted in two pivots on same bar

updateLastPivot (series bool) : true if new pivot calculated replaces the old one.

Zigzag

Zigzag object which contains whole zigzag calculation parameters and pivots

Fields:

length (series int) : Zigzag length. Default value is 5

numberOfPivots (series int) : max number of pivots to hold in the calculation. Default value is 20

offset (series int) : Bar offset to be considered for calculation of zigzag. Default is 0 - which means calculation is done based on the latest bar.

level (series int) : Zigzag calculation level - used in multi level recursive zigzags

zigzagPivots (Pivot ) : array which holds the last n pivots calculated.

flags (ZigzagFlags) : ZigzagFlags object which is required for continuous drawing of zigzag lines.

ZigzagObject

Zigzag Drawing Object

Fields:

zigzagLine (series line) : Line joining two pivots

zigzagLabel (series label) : Label which can be used for drawing the values, ratios, directions etc.

ZigzagProperties

Object which holds properties of zigzag drawing. To be used along with ZigzagDrawing

Fields:

lineColor (series color) : Zigzag line color. Default is color.blue

lineWidth (series int) : Zigzag line width. Default is 1

lineStyle (series string) : Zigzag line style. Default is line.style_solid.

showLabel (series bool) : If set, the drawing will show labels on each pivot. Default is false

textColor (series color) : Text color of the labels. Only applicable if showLabel is set to true.

maxObjects (series int) : Max number of zigzag lines to display. Default is 300

xloc (series string) : Time/Bar reference to be used for zigzag drawing. Default is Time - xloc.bar_time.

curved (series bool) : Boolean field to print curved zigzag - used only with polyline implementation

ZigzagDrawing

Object which holds complete zigzag drawing objects and properties.

Fields:

zigzag (Zigzag) : Zigzag object which holds the calculations.

properties (ZigzagProperties) : ZigzagProperties object which is used for setting the display styles of zigzag

drawings (ZigzagObject ) : array which contains lines and labels of zigzag drawing.

ZigzagDrawingPL

Object which holds complete zigzag drawing objects and properties - polyline version

Fields:

zigzag (Zigzag) : Zigzag object which holds the calculations.

properties (ZigzagProperties) : ZigzagProperties object which is used for setting the display styles of zigzag

zigzagLabels (label )

zigzagLine (series polyline) : polyline object of zigzag lines

ZigzagLibrary "Zigzag"

Zigzag related user defined types. Depends on DrawingTypes library for basic types

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Pivot object to string representation

Namespace types: Pivot

Parameters:

this (Pivot) : ZigzagTypes/Pivot

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Pivot

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts Array of Pivot objects to string representation

Namespace types: Pivot

Parameters:

this (Pivot ) : Pivot object array

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of Pivot object array

method tostring(this)

Converts ZigzagFlags object to string representation

Namespace types: ZigzagFlags

Parameters:

this (ZigzagFlags) : ZigzagFlags object

Returns: string representation of ZigzagFlags

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Zigzag object to string representation

Namespace types: Zigzag

Parameters:

this (Zigzag) : ZigzagTypes/Zigzagobject

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Zigzag

method calculate(this, ohlc, indicators, indicatorNames)

Calculate zigzag based on input values and indicator values

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

ohlc (float ) : Array containing OHLC values. Can also have custom values for which zigzag to be calculated

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns: current Zigzag object

method calculate(this)

Calculate zigzag based on properties embedded within Zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: current Zigzag object

method nextlevel(this)

Calculate Next Level Zigzag based on the current calculated zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: Next Level Zigzag object

method clear(this)

Clears zigzag drawings array

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing ) : array

Returns: void

method drawplain(this)

draws fresh zigzag based on properties embedded in ZigzagDrawing object without trying to calculate

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

Returns: ZigzagDrawing object

method drawfresh(this, ohlc, indicators, indicatorNames)

draws fresh zigzag based on properties embedded in ZigzagDrawing object

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns: ZigzagDrawing object

method drawcontinuous(this, ohlc, indicators, indicatorNames)

draws zigzag based on the zigzagmatrix input

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns:

method getPrices(pivots)

Namespace types: Pivot

Parameters:

pivots (Pivot )

method getBars(pivots)

Namespace types: Pivot

Parameters:

pivots (Pivot )

Indicator

Indicator is collection of indicator values applied on high, low and close

Fields:

indicatorHigh (series float) : Indicator Value applied on High

indicatorLow (series float) : Indicator Value applied on Low

PivotCandle

PivotCandle represents data of the candle which forms either pivot High or pivot low or both

Fields:

_high (series float) : High price of candle forming the pivot

_low (series float) : Low price of candle forming the pivot

length (series int) : Pivot length

pHighBar (series int) : represents number of bar back the pivot High occurred.

pLowBar (series int) : represents number of bar back the pivot Low occurred.

pHigh (series float) : Pivot High Price

pLow (series float) : Pivot Low Price

indicators (Indicator ) : Array of Indicators - allows to add multiple

Pivot

Pivot refers to zigzag pivot. Each pivot can contain various data

Fields:

point (chart.point) : pivot point coordinates

dir (series int) : direction of the pivot. Valid values are 1, -1, 2, -2

level (series int) : is used for multi level zigzags. For single level, it will always be 0

componentIndex (series int) : is the lower level zigzag array index for given pivot. Used only in multi level Zigzag Pivots

subComponents (series int) : is the number of sub waves per each zigzag wave. Only applicable for multi level zigzags

microComponents (series int) : is the number of base zigzag components in a zigzag wave

ratio (series float) : Price Ratio based on previous two pivots

sizeRatio (series float)

subPivots (Pivot )

indicatorNames (string ) : Names of the indicators applied on zigzag

indicatorValues (float ) : Values of the indicators applied on zigzag

indicatorRatios (float ) : Ratios of the indicators applied on zigzag based on previous 2 pivots

ZigzagFlags

Flags required for drawing zigzag. Only used internally in zigzag calculation. Should not set the values explicitly

Fields:

newPivot (series bool) : true if the calculation resulted in new pivot

doublePivot (series bool) : true if the calculation resulted in two pivots on same bar

updateLastPivot (series bool) : true if new pivot calculated replaces the old one.

Zigzag

Zigzag object which contains whole zigzag calculation parameters and pivots

Fields:

length (series int) : Zigzag length. Default value is 5

numberOfPivots (series int) : max number of pivots to hold in the calculation. Default value is 20

offset (series int) : Bar offset to be considered for calculation of zigzag. Default is 0 - which means calculation is done based on the latest bar.

level (series int) : Zigzag calculation level - used in multi level recursive zigzags

zigzagPivots (Pivot ) : array which holds the last n pivots calculated.

flags (ZigzagFlags) : ZigzagFlags object which is required for continuous drawing of zigzag lines.

ZigzagObject

Zigzag Drawing Object

Fields:

zigzagLine (series line) : Line joining two pivots

zigzagLabel (series label) : Label which can be used for drawing the values, ratios, directions etc.

ZigzagProperties

Object which holds properties of zigzag drawing. To be used along with ZigzagDrawing

Fields:

lineColor (series color) : Zigzag line color. Default is color.blue

lineWidth (series int) : Zigzag line width. Default is 1

lineStyle (series string) : Zigzag line style. Default is line.style_solid.

showLabel (series bool) : If set, the drawing will show labels on each pivot. Default is false

textColor (series color) : Text color of the labels. Only applicable if showLabel is set to true.

maxObjects (series int) : Max number of zigzag lines to display. Default is 300

xloc (series string) : Time/Bar reference to be used for zigzag drawing. Default is Time - xloc.bar_time.

ZigzagDrawing

Object which holds complete zigzag drawing objects and properties.

Fields:

zigzag (Zigzag) : Zigzag object which holds the calculations.

properties (ZigzagProperties) : ZigzagProperties object which is used for setting the display styles of zigzag

drawings (ZigzagObject ) : array which contains lines and labels of zigzag drawing.

Angled Volume Profile [Trendoscope]Volume profile is useful tool to understand the demand and supply zones on horizontal level. But, what if you want to measure the volume levels over trend line? In trending markets, the feature to measure volume over angled levels can be very useful for traders who use these measures. Here is an attempt to provide such tool.

🎲 How to use

🎯 Interactive input for selecting starting point and angle.

Upon loading the script, you will be prompted to select

Start time and price - this is a point which you can select by moving the maroon highlighted label.

End price - though this is shown as maroon bullet, this is price only input. Hence, when you click on the bullet, a horizontal line will appear. Users can move the line to use different End price.

Start and End price are used for identifying the angle at which volume profile need to be calculated. Whereas start time is used as starting time of the volume profile. Last bar of the chart is considered as ending bar.

🎯 Other settings.

From settings, users can select the colour of volume profile and style. Step multiplier defines the distance at which the profile lines needs to be drawn. Higher multiplier leads to less dense profile lines whereas lower multiplier leads to higher density of profile lines.

🎲 Limitations

🎯 Max 500 lines

Pinescript only allows max 500 lines on an indicator. Due to this, if we set very low multiplier - this can lead to more than 500 profile lines. Due to this some lines can get removed.

On the contrary, if multiplier is too high, then you will see very few lines which may not be meaningful.

Hence, it is important to select optimal multiplier based on your timeframe

🎯 No updates on new bar

Since the profile can spawn many bars, it is not possible to recalculate the whole volume profile when price creates new bars. Hence, there will not be visual update when new bars are created. But, to update the chart, users only need to make another movement of Start or ending point on interactive input.

MathEasingFunctionsLibrary "MathEasingFunctions"

A collection of Easing functions.

Easing functions are commonly used for smoothing actions over time, They are used to smooth out the sharp edges

of a function and make it more pleasing to the eye, like for example the motion of a object through time.

Easing functions can be used in a variety of applications, including animation, video games, and scientific

simulations. They are a powerful tool for creating realistic visual effects and can help to make your work more

engaging and enjoyable to the eye.

---

Includes functions for ease in, ease out, and, ease in and out, for the following constructs:

sine, quadratic, cubic, quartic, quintic, exponential, elastic, circle, back, bounce.

---

Reference:

easings.net

learn.microsoft.com

ease_in_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

select(v, formula, effect, bounded)

Parameters:

v (float)

formula (string)

effect (string)

bounded (bool)

Treasury Yields Heatmap [By MUQWISHI]▋ INTRODUCTION :

The “Treasury Yields Heatmap” generates a dynamic heat map table, showing treasury yield bond values corresponding with dates. In the last column, it presents the status of the yield curve, discerning whether it’s in a normal, flat, or inverted configuration, which determined by using Pearson's linear regression coefficient. This tool is built to offer traders essential insights for effectively tracking bond values and monitoring yield curve status, featuring the flexibility to input a starting period, timeframe, and select from a range of major countries' bond data.

_______________________

▋ OVERVIEW:

______________________

▋ YIELD CURVE:

It is determined through Pearson's linear regression coefficient and considered…

R ≥ 0.7 → Normal

0.7 > R ≥ 0.35 → Slight Normal

0.35 > R > -0.35 → Flat

-0.35 ≥ R > -0.7 → Slight Inverted

-0.7 ≥ R → Inverted

_______________________

▋ INDICATOR SETTINGS:

#Section One: Table Setting

#Section Two: Technical Setting

(1) Country: Select country’s treasury yields data

(2) Timeframe: Time interval.

(3) Fetch By:

(3A) Date: Retrieve data by beginning of date.

(3B) Period: Retrieve data by specifying the number of time series back.

Enjoy. Please let me know if you have any questions.

Thank you.

Time & Sales (Tape) [By MUQWISHI]▋ INTRODUCTION :

The “Time and Sales” (Tape) indicator generates trade data, including time, direction, price, and volume for each executed trade on an exchange. This information is typically delivered in real-time on a tick-by-tick basis or lower timeframe, providing insights into the traded size for a specific security.

_______________________

▋ OVERVIEW:

_______________________

▋ Volume Dynamic Scale Bar:

It's a way for determining dominance on the time and sales table, depending on the selected length (number of rows), indicating whether buyers or sellers are in control in selected length.

_______________________

▋ INDICATOR SETTINGS:

#Section One: Table Settings

#Section Two: Technical Settings

(1) Implement By: Retrieve data by

(1A) Lower Timeframe: Fetch data from the selected lower timeframe.

(1B) Live Tick: Fetch data in real-time on a tick-by-tick basis, capturing data as soon as it's observed by the system.

(2) Length (Number of Rows): User able to select number of rows.

(3) Size Type: Volume OR Price Volume.

_____________________

▋ COMMENT:

The values in a table should not be taken as a major concept to build a trading decision.

Please let me know if you have any questions.

Thank you.

RSI Radar Multi Time FrameHello All!

First of all many Thanks to Tradingview and Pine Team for developing Pine Language all the time! Now we have a new feature and it's called Polylines and I developed RSI Radar Multi Time Frame . This script is an example and experimental work, you can use it as you wish.

The scripts gets RSI values from 6 different time frames, it doesn't matter the time frame you choose is higher/lower or chart time frame. it means that the script can get RSI values from higher or lower time frames than chart time frame.

It's designed to show RSI Radar all the time on the chart even if you zoom in/out or scroll left/right.

You can set OB/OS or RSI line colors. Also RSI polyline is shown as Curved/Hexagon optionally.

Some screenshots here:

Doesn't matter if you zoom out, it can show RSI radar in the visible area:

Another example:

You can change the colors, or see the RSI as Hexagon:

Time frames from seconds to 1Day in this example while chart time frame is any ( 30mins here )

Enjoy!

Delta Ladder [Kioseff Trading]Hello!

This script presents volume delta data in various forms!

Features

Classic mode: Volume delta boxes oriented to the right of the bar (sell closer / buy further)

On Bar mode: Volume delta boxes oriented on the bar (sell left / buy right)

Pure Ladder mode: Pure volume delta ladder

PoC highlighting

Color-coordinated delta boxes. Marginal volume differences are substantially shaded while large volume differences are lightly shaded.

Volume delta boxes can be merged and delta values removed to generate a color-only canvas reflecting vol. delta differences in price blocks.

Price bars can be split up to 497 times - allowing for greater precision.

Total volume delta for the bar and timestamp included

The image above shows Classic mode - delta blocks are oriented left/right contingent on positive/negative values!

The image above shows the same price sequence; however, delta blocks are superimposed on the price bar. Left-side blocks reflect negative delta while right-side blocks reflect positive delta! To apply this display method - select "On Bar" for the "Data Display Method" setting!

The image above shows "Pure Ladder" mode. Delta blocks remain color-coordinated; however, all delta blocks retain the same x-axis as the price bar they were calculated for!

Additionally, you can select to remove the delta values and merge the delta boxes to generate a color-based canvas indicative of volume delta at traded price levels!

The image above shows the same price sequence; however, the "Volume Assumption" setting is activated.

When active, the indicator assumes a 60/ 40 split when a level is traded at and only one metric - "buy volume" or "sell volume" is recorded. This means there shouldn't be any levels recorded where "buy volume" is greater than 0 and "sell volume" equals 0 and vice versa. While this assumption was performed arbitrarily, it may help better replicate volume delta and OI delta calculations seen on other charting platforms.

This option is configurable; you can select to have the script not assume a 60/ 40 split and instead record volume "as is" at the corresponding price level!

I plan to roll out additional features for the indicator - particularly tick-based price blocks! Stay tuned (:

Thank you!

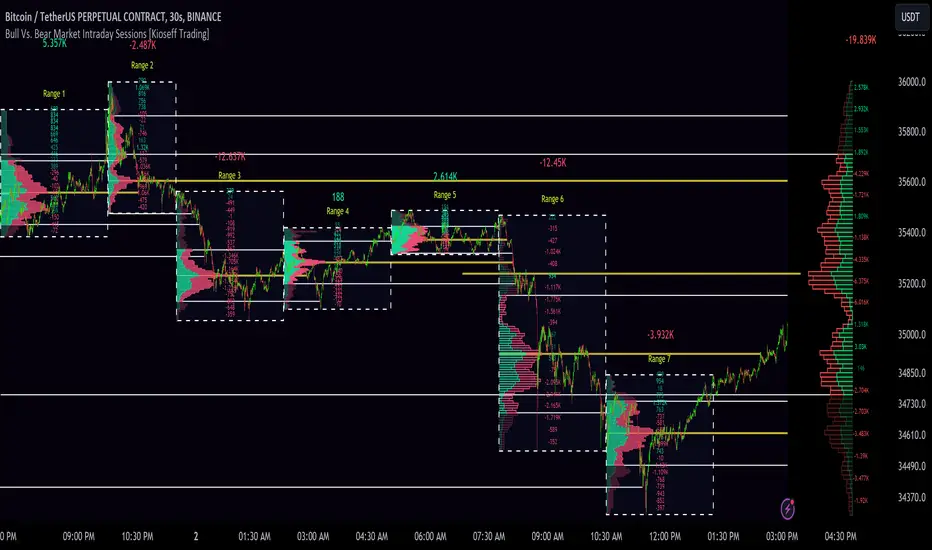

10x Bull Vs. Bear VP Intraday Sessions [Kioseff Trading]Hello!

This script "10x Bull Vs. Bear VP Intraday Sessions" lets the user configure up to 10 session ranges for Bull Vs. Bear volume profiles!

Features

Up To 10 Fixed Ranges!

Volume Profile Anchored to Fixed Range

Delta Ladder Anchored to Range

Bull vs Bear Profiles!

Standard Poc and Value Area Lines, in Addition to Separated POCs and Value Area Lines for Bull Profiles and Bear Profiles

Configurable Value Area Target

Up to 2000 Profile Rows per Visible Range

Stylistic Options for Profiles

This script generates Bull vs. Bear volume profiles for up to 10 fixed ranges!

Up to 2000 volume profile levels (price levels) Can be calculated for each profile, thanks to the new polyline feature, allowing for less aggregation / more precision of volume at price and volume delta.

Bull vs Bear Profiles

The image above shows primary functionality!

Green profiles = buying volume

Red profiles = selling volume

All colors are configurable.

Bullish & bearish POC + value areas for each fixed range are displayable!

That’s about it :D

This indicator is part of a series titled “Bull vs. Bear”.

If you have any suggestions please feel free to share!

T-Virus Sentiment [hapharmonic]🧬 T-Virus Sentiment: Visualize the Market's DNA

Remember the iconic T-Virus vial from the first Resident Evil? That powerful, swirling helix of potential has always fascinated me. It sparked an idea: what if we could visualize the market's underlying health in a similar way? What if we could capture the "genetic code" of market sentiment and contain it within a dynamic, 3D indicator? This project is the result of that idea, brought to life with Pine Script.

The indicator's main goal is to measure the strength and direction of market sentiment by analyzing the "genetic code" of price action through a variety of trusted indicators. The result is displayed as a liquid level within a DNA helix, a bubble density representing buying pressure, and a T-Virus mascot that reflects the overall mood.

🧐 Core Concept: How It Works

The primary output of the indicator is the "Active %" gauge you see on the right side of the vial. This percentage represents the overall sentiment score, calculated as an average from 7 different technical analysis tools. Each tool is analyzed on every bar and assigned a score from 1 (strong bearish pressure) to 5 (strong bullish potential).

In this indicator, we re-imagine market dynamics through the lens of a viral outbreak. A strong bear market is like a virus taking hold, pulling all technical signals down into a state of weakness. Conversely, a powerful bull market is like an antiviral serum ; positive signals rise and spread toward the top of the vial, indicating that the system is being injected with strength.

This is not just another line on a chart. It's a comprehensive sentiment dashboard designed to give an immediate, at-a-glance understanding of the confluence between 7 classic technical indicators. The incredible 3D model of the vial itself was inspired by a design concept found here .

⚛️ The 4 Core Elements of T-Virus Sentiment

These four elements work in harmony to give a complete, multi-faceted picture of market sentiment. Each component tells a different part of the story.

The Virus Mascot: An instant emotional cue. This character provides the quickest possible read on the overall market mood, combining sentiment with volume pressure.

The Antiviral Serum Level: The main quantitative output. This is the liquid level in the DNA helix and the percentage gauge on the right, representing the average sentiment score from all 7 indicators.

Buy Pressure & Bubble Density: This visualizes volume flow. The density of bubbles represents the intensity of accumulation (buying) versus distribution (selling). It's the "power" behind the move.

The Signal Distribution: This shows the confluence (or dispersion) of sentiment. Are all signals bullish and clustered at the top, or are they scattered, indicating a conflicted market? The position of the indicator labels is crucial, as each is assigned to one of five distinct zones:

Base Bottom: The market is at its weakest. Signals here suggest strong bearish control and distribution.

Lower Zone: The market is still bearish, but signals may be showing early signs of accumulation or bottoming.

Neutral Core (Center): A state of balance or sideways consolidation. The market is waiting for a new direction.

Upper Zone: Bullish momentum is becoming clear. Signals are strengthening and showing bullish control.

Top Cap: The market is "heating up" with strong bullish sentiment, potentially nearing overbought conditions.

🐂🐻 The Virus Mascot: The At-a-Glance Indicator

This character acts as a shortcut to confirm market health. It combines the sentiment score with volume, preventing false confidence in a low-volume rally.

Its state is determined by a dual-check: the overall "Antiviral Serum Level" and the "Buy Pressure" must both be above 50%.

Green & Smiling: The 'all clear' signal. This means that not only is the overall technical sentiment bullish, but it's also being supported by real buying pressure. This is a sign of a healthy bull market.

Red & Angry: A warning sign. This appears if either the sentiment is weak, or a bullish sentiment is not being confirmed by buying volume. The latter could indicate a potential "bull trap" or an exhaustive move.

This mascot can be disabled from the settings page under "Virus Mascot Styling" if a cleaner look is preferred.

🫧 Bubble Density: Gauging Buy vs. Sell Pressure

The bubbles visualize the battle between buyers and sellers. There are two modes to control how this is calculated:

Mode 1: Visible Range (The 'Big Picture' View)

This default mode is best for getting a broad, contextual understanding of the current session. It dynamically analyzes the volume of every single candlestick currently visible on the screen to calculate the buy/sell pressure ratio. It answers the question: "Over the entire period I'm looking at, who is in control?" As you zoom in or out, the calculation adapts.

Mode 2: Custom Lookback (The 'Precision' View)

This mode is for traders who need to analyze short-term pressure. You can define a fixed number of recent bars to analyze, which is perfect for scalping or understanding the volume dynamics leading into a key level. It answers the question: "What is happening right now ?" In the example above, a lookback of 2 focuses only on the most recent action, clearly showing intense, immediate selling pressure (few bubbles) and a corresponding drop in the sentiment score to 29%.

ℹ️ Interactive Tooltips: Dive Deeper

We believe in transparency, not 'black box' indicators. This feature transforms the indicator from a visual aid into an active learning tool.

Simply hover the mouse over any indicator label (like EMA, OBV, etc.) to get a detailed tooltip. It will explain the specific data points and thresholds that signal met to be placed in its current zone. This helps build trust in the signals and allows users to fine-tune the indicator settings to better match their own trading style.

🎯 The Scoring Logic Breakdown

The "Antiviral Serum Level" gauge is the average score from 7 technical analysis tools. Each is graded on a 5-point scale (1=Strong Bearish to 5=Strong Bullish). Here’s a detailed, transparent look at how each "gene" is evaluated:

Relative Strength Index (RSI)

Measures momentum and overbought/oversold conditions.

Group 1 (Strong Bearish): RSI > 80 (Extreme Overbought)

Group 2 (Bearish): 70 < RSI ≤ 80 (Overbought)

Group 3 (Neutral): 30 ≤ RSI ≤ 70

Group 4 (Bullish): 20 ≤ RSI < 30 (Oversold)

Group 5 (Strong Bullish): RSI < 20 (Extreme Oversold)

Exponential Moving Averages (EMA)

Evaluates the trend's strength and structure based on the alignment of multiple EMAs (9, 21, 50, 100, 200, 250).

Group 1 (Strong Bearish): A perfect bearish sequence (9 < 21 < 50 < ...)

Group 2 (Bearish Transition): Early signs of a potential reversal (e.g., 9 > 21 but still below 50)

Group 3 (Neutral / Mixed): MAs are intertwined or showing a partial bullish sequence.

Group 4 (Bullish): A strong bullish sequence is forming (e.g., 9 > 21 > 50 > 100)

Group 5 (Strong Bullish): A perfect bullish sequence (9 > 21 > 50 > 100 > 200 > 250)

Moving Average Convergence Divergence (MACD)

Analyzes the relationship between two moving averages to gauge momentum.

Group 1 (Strong Bearish): MACD & Histogram are negative and momentum is falling.

Group 2 (Weakening Bearish): MACD is negative but the histogram is rising or positive.

Group 3 (Neutral / Crossover): A crossover event is occurring near the zero line.

Group 4 (Bullish): MACD & Histogram are positive.

Group 5 (Strong Bullish): MACD & Histogram are positive, rising strongly, and accelerating.

Average Directional Index (ADX)

Measures trend strength, not direction. The score is based on both ADX value and the dominance of DI+ vs DI-.

Group 1 (Bearish / No Trend): ADX < 20 and DI- is dominant.

Group 2 (Developing Bearish Trend): 20 ≤ ADX < 25 and DI- is dominant.

Group 3 (Neutral / Indecision): Trend is weak or DI+ and DI- are nearly equal.

Group 4 (Developing Bullish Trend): 25 ≤ ADX ≤ 40 and DI+ is dominant.

Group 5 (Strong Bullish Trend): ADX > 40 and DI+ is dominant.

Ichimoku Cloud (IKH)

A comprehensive indicator that defines support/resistance, momentum, and trend direction.

Group 1 (Strong Bearish): Price is below the Kumo, Tenkan < Kijun, and Chikou is below price.

Group 2 (Bearish): Price is inside or below the Kumo, with mixed secondary signals.

Group 3 (Neutral / Ranging): Price is inside the Kumo, often with a Tenkan/Kijun cross.

Group 4 (Bullish): Price is above the Kumo with strong primary signals.

Group 5 (Strong Bullish): All signals are aligned bullishly: price above Kumo, bullish Tenkan/Kijun cross, bullish future Kumo, and Chikou above price.

Bollinger Bands (BB)

Measures volatility and relative price levels.

Group 1 (Strong Bearish): Price is below the lower band.

Group 2 (Bearish Territory): Price is between the lower band and the basis line.

Group 3 (Neutral): Price is hovering around the basis line.

Group 4 (Bullish Territory): Price is between the basis line and the upper band.

Group 5 (Strong Bullish): Price is above the upper band.

On-Balance Volume (OBV)

Uses volume flow to predict price changes. The score is based on OBV's trend and its position relative to its moving average.

Group 1 (Strong Bearish): OBV is below its MA and falling.

Group 2 (Weakening Bearish): OBV is below its MA but showing signs of rising.

Group 3 (Neutral): OBV is very close to its MA.

Group 4 (Bullish): OBV is above its MA and rising.

Group 5 (Strong Bullish): OBV is above its MA, rising strongly, and showing signs of a volume spike.

🧭 How to Use the T-Virus Sentiment Indicator

IMPORTANT: This indicator is a sentiment dashboard , not a direct buy/sell signal generator. Its strength lies in showing confluence and providing a quick, holistic view of the market's technical health.

Confirmation Tool: Use the "Active %" gauge to confirm a trade setup from your primary strategy. For example, if you see a bullish chart pattern, a high and rising sentiment score can add confidence to your trade.

Momentum & Trend Gauge: A consistently high score (e.g., > 75%) suggests strong, established bullish momentum. A consistently low score (< 25%) suggests strong bearish control. A score hovering around 50% often indicates a ranging or indecisive market.

Divergence & Warning System: Pay attention to divergences. If the price is making new highs but the sentiment score is failing to follow or is actively decreasing, it could be an early warning sign that the underlying momentum is weakening.

⚙️ Settings & Customization

The indicator is highly customizable to fit any trading style.

Position & Anchor: Control where the vial appears on the chart.

Styling (Vial, Helix, etc.): Nearly every visual element can be color-customized.

Signals: This is where the real power is. All underlying indicator parameters (RSI length, MACD settings, etc.) can be fine-tuned to match a personal strategy. The text labels can also be disabled if the chart feels cluttered.

Enjoy visualizing the market's DNA with the T-Virus Sentiment indicator

Intraday Spark Chart [AstrideUnicorn]The Intraday Spark Chart (ISC) is a minimalist yet powerful tool designed to track an asset’s performance relative to its daily opening price. Inspired by Nasdaq's trading-floor analog dashboards, it visualizes intraday percentage changes as a color-coded sparkline, helping traders quickly gauge momentum and session bias.

Ideal for: Day trading, scalping, and multi-asset monitoring.

Best paired with: 1m to 4H timeframes (auto-warns on higher TFs).

Key metrics:

Real-time % change from daily open.

Final daily % change (updated at session close).

Daily open price labels for orientation.

HOW TO USE

Visual Guide

Sparkline Plot:

A green area/line indicates price is above the daily open (bullish).

A red area/line signals price is below the daily open (bearish).

The baseline (0%) represents the daily open price.

Session Markers:

The dotted vertical lines separate trading days.

Gray labels near the baseline show the exact daily open price at the start of each session.

Dynamic Labels:

The labels in the upper left corner of each session range display the current (or final) daily % change. Color matches the trend (green/red) for instant readability.

Practical Use Cases

Opening Range Breakouts: Spot early momentum by observing how price reacts to the daily open.

Multi-Asset Screening: Compare intraday strength across symbols by choosing an asset in the indicator settings panel.

Session Close Prep: Anticipate daily settlement by tracking the final % change (useful for futures/swing traders).

SETTINGS

Asset (Input Symbol) : Defaults to the current chart symbol. Choose any asset to monitor its price action without switching charts - ideal for intermarket analysis or correlation tracking.

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100