BETABETA (β) value is a risk index, which is used to measure the price fluctuations of individual stocks or mutual funds relative to the entire stock market.

The higher the β value, the greater the volatility of the stock phase on the performance evaluation benchmark, and vice versa.

When β = 1, it means that the income and risks of the stock are consistent with the income and risks of the broader market; when β> 1, it means that the stock income and risk are greater than the income and risk of the broader market index.

Our Beta calculation method is the same as finance.yahoo.com, markets.ft.com, zacks.com and cnbc.com .

Default Beta setting is data over a 5 Years (Monthly) period and base value of 1.0 is S&P 500 Index.

Beta

Beta CalculatorBeta is a measure of an asset's volatility relative to the market (the S&P500 is the most widely used index for this). A beta of 1 indicates that the asset moves exactly like the market, a beta < 1 indicates that the asset is less volatile than the market, and a beta > 1 means that the asset amplifies market movements.

This tool is used to calculate easily the Beta coefficient of an asset using 4 parameters :

- Symbol : The Asset's Ticker

- Reference : The Market Index Ticker

- Lookback Candles : The number of candles to include in the calculation

- (Implict) Resolution : The timeframe you are using, defines the precision

regressLibrary "regress"

produces the slope (beta), y-intercept (alpha) and coefficient of determination for a linear regression

regress(x, y, len) regress: computes alpha, beta, and r^2 for a linear regression of y on x

Parameters:

x : the explaining (independent) variable

y : the dependent variable

len : use the most recent "len" values of x and y

Returns: : alpha is the x-intercept, beta is the slope, an r2 is the coefficient of determination

Note: the chart does not show anything, use the return values to compute model values in your own application, if you wish.

Market Movers: Sectoral IndexThe indicator will show the Sectors which are leading or lagging NIFTY50 index based on Alpha & Beta values. Stock selection can be done based on the respective Sectors.

Look for alpha & beta values.

Prefer one with high beta.

Greens are leaders & Blues are lagers.

This don't completely indicates a trend, but it can give the overview of a major trend & market movers.

Gray line is the base index NIFTY50, it is Zero.

Turn on Indicator Name Label in Settings > Chart Settings.

In intraday or positions, in a leading Sector there will be a leading stock, spot it out.

Make a sector wise watchlist of stocks.

Use higher or Daily timeframe for Swing trades.

Detailed descriptions are available in my previous Alpha & Beta indicators.

Better BollingersThe Bollinger Band strategy is a powerful and effective tool for automated trading in high volatility markets. The trouble is that, by itself, it is not very profitable. We need a way to know if the volatility we're seeing is part of a larger trend in the direction we want to trade in. Doing this, we can avoid entering long trades during a macro downtrending market meaning we can use tighter stop losses and open trades with more confidence than if we didn't have an idea of the larger market trend.

This script is ideal for, and geared towards, users of the 3commas automated trading platform. It behaves similarly to the familiar TA Presets BB-20- family of strategies but includes other indicators to help weed out some of the noise in a highly volatile market. Additionally, users who are not on Binance.com, but using 3commas for trading, now have access to signals comparable to those provided by the builtin signals for Binance.com.

Bollinger Flip Flop StrategyThis strategy combines both long and short Bollinger band strategies with a signal to determine to determine when it's appropriate to use each. Additionally, the strategy has protections in place for market conditions which would normally cause a trade to be stuck due to a long market trend change. Think of it like a stop loss but instead of basing the stop on a percentage from entry, it's based on prevailing market conditions.

This strategy is ideal for controlling trading bots on the 3commas.io platform. To do this, you will need to set up two "simple" bots, one for short trades and one for long trades. Other than their direction, they should be configured identically. Set the parameters for the bot the same as you have them set in the strategy preferences. Once you've done this, set the "Short Bot ID" and "Long Bot ID" fields to the ID numbers for each bot, respectively. Next, set the Email Token parameter (this will be the same for both bots). Once you've done this, you need only configure a single alert per coin pair with the alert message set to {{strategy.order.alert_message}}. Make sure you have all of the strategy settings, including bot IDs and email tokens set correctly before creating the alert . These parameters are saved in the alert and can be safely changed on the active chart once the alert is created without affecting the alert.

Screener: Alpha & Beta IndexThis is a Index Screener which can short list the major Sectors contributing to NIFTY movement that day.

This helps in sector based trading, in which we can trade in the stocks which falls under that particular sector.

No need to roam around all the stocks in the whole watchlist.

It is recommended to create sector wise watchlist of all sectors. It will be easier to concentrate in only one sector.

For example in IT sector index there are certain stocks which contribute to the movement of IT sector.

This will be available in NSE (or exchange website).

For detailed description check out the descriptions in my previous 2 Alpha and Beta indicators.

Combine and use this screener with my previous Alpha & Beta indicator.

Screener: Alpha & BetaThis is a Live Screener for my previous Alpha & Beta indicator, which filters stocks lively based on the given values.

Use 5min timeframe for Live Intraday.

The default stocks in the screener is selected based on high beta value from F&O listed stocks. It may include other stocks also.

User can input stocks of your choice either through the menu or through the Pine editor.

The maximum number of stocks inputs is only 40. The indicator includes only 20 stocks by default.

More number of stocks can be added but it makes the screener slower to load.

Open the indicator in a sperate tab or window to avoided the loading lag.

It is recommended to choose only 10 to 20 stocks based on the weightage from each sectors.

Beta values are dynamic. It changes from day to day based on the trend and sector.

Update the sock list weekly or twice a week or monthly.

Use investing.com screener(preferably) or TradingView screener for shortlisting beta stocks.

Remember that majority of indicators fails in a sideways market, also every indicator is not 100% accurate.

Alpha & BetaHow to use Alpha(α)?

If Alpha is positive the stock outperforms, if the value is negative means the stock underperforms.

α < 0: The investment has earned too little for its risk (or, was too risky for the return)

α = 0: The investment has earned a return adequate for the risk taken

α > 0: The investment has a return in excess of the reward for the assumed risk

How to use Beta(β)?

β = 1: Exactly as volatile as the index

β > 1: More volatile than the index

β < 1 > 0: Less volatile than the index

β = 0: Uncorrelated to the index

β < 0: Negatively correlated to the index

β > 2: Trending stock

Higher the β higher risk/reward

Example: If the beta is 1.1, the share price is like to move by 10% more than the index

Trading Tip

Choose a stock with Alpha greater than 0 and Beta greater than 1.9 for intraday in 5min timeframe for long positions

Remember that such stocks will have high risk and high reward

Shortlist stocks with Beta greater than 1.9 for next day in 5min timeframe

Statistical and Financial MetricsGood morning traders!

This time I want to share with you a little script that, thanks to the use of arrays, allows you to have interesting statistical and financial insights taken from the symbol on chart and compared to those of another symbol you desire (in this case the metrics taken from the perpetual future ETHUSDT are compared to those taken from the perpetual future BTCUSDT, used as a proxy for the direction of cryptocurrency market)

By enabling "prevent repainting", the data retrieved from the compared symbol won't be on real time but they will static since they will belong to the previous closed candle

Here are the metrics you can have by storing data from a variable period of candles (by default 51):

✓ Variance (of the symbol on chart in GREEN; of the compared symbol in WHITE)

✓ Standard Deviation (of the symbol on chart in OLIVE; of the compared symbol in SILVER)

✓ Yelds (of the symbol on chart in LIME; of the compared symbol in GRAY) → yelds are referred to the previous close, so they would be calculated as the the difference between the current close and the previous one all divided by the previous close

✓ Covariance of the two datasets (in BLUE)

✓ Correlation coefficient of the two datasets (in AQUA)

✓ β (in RED) → this insight is calculated in three alternative ways for educational purpose (don't worry, the output would be the same).

WHAT IS BETA (β)?

The BETA of an asset can be interpretated as the representation (in relative terms) of the systematic risk of an asset: in other terms, it allows you to understand how big is the risk (not eliminable with portfolio diversification) of an asset based on the volatilty of its yelds.

We say that this representation is made in relative terms since it is expressed according to the market portfolio: this portfolio is hypothetically the portfolio which maximizes the diversification effects in order to kill all the specific risk of that portfolio; in this way the standard deviation calculated from the yelds of this portfolio will represent just the not-eliminable risk (the systematic risk), without including the eliminable risk (the specific risk).

The BETA of an asset is calculated as the volatilty of this asset around the volatilty of the market portfolio: being more precise, it is the covariance between the yelds of the current asset and those of the market portfolio all divided by the variance of the yelds of market portfolio.

Covariance is calculated as the product between correlation coefficient, standard deviation of the first dataset and standard deviation of the second asset.

So, as the correlation coefficient and the standard deviation of the yelds of our asset increase (it means that the yelds of our asset are very similiar to those of th market portfolio in terms of sign and intensity and that the volatility of these yelds is quite high), the value of BETA increases as well

According to the Capital Asset Pricing Model (CAPM) promoted by William Sharpe (the guy of the "Sharpe Ratio") and Harry Markowitz, in efficient markets the yeld of an asset can be calculated as the sum between the risk-free interest rate and the risk premium. The risk premium of the specific asset would be the risk premium of the market portfolio multiplied with the value of beta. It is simple: if the volatility of the yelds of an asset around the yelds of market protfolio are particularly high, investors would ask for a higher risk premium that would be translated in a higher yeld.

In this way the expected yeld of an asset would be calculated from the linear expression of the "Security Market Line": r_i = r_f + β*(r_m-r_f)

where:

r_i = expected yeld of the asset

r_f = risk free interest rate

β = beta

r_m = yeld of market portfolio

I know that considering Bitcoin as a proxy of the market portfolio involved in the calculation of Beta would be an inaccuracy since it doesn't have the property of maximum diversification (since it is a single asset), but there's no doubt that it's tying the prices of altcoins (upward and downward) thanks to the relevance of its dominance in the capitalization of cryptocurrency market. So, in the lack of a good index of cryptocurrencies (as the FTSE MIB for the italian stock market), and as long the dominance of Bitcoin will persist with this intensity, we can use Bitcoin as a proxy of the market portfolio

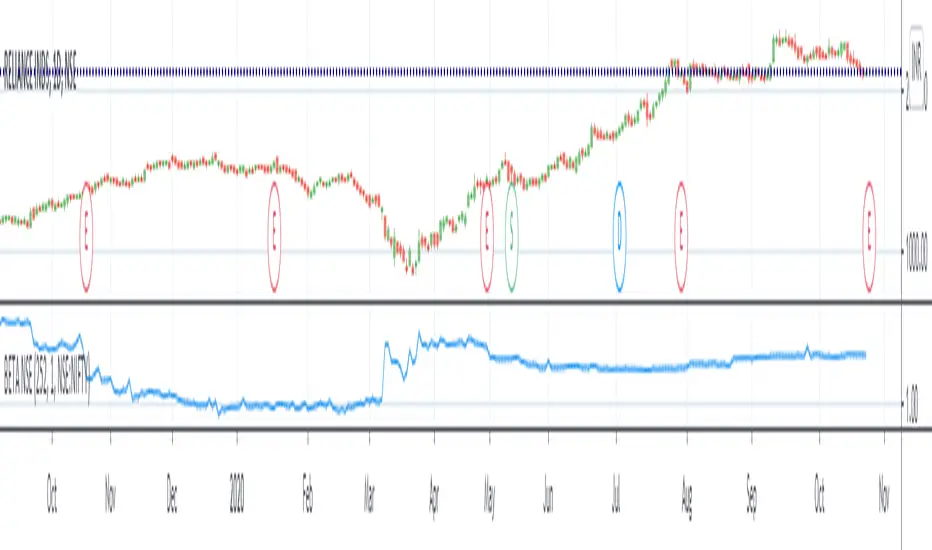

BETA (against any benchmark index - defaulted to NSE:NIFTY)Beta value of a stock relative to benchmark index. Thanks to Ricardo Santos for the original script. This script is adapted from it.

To understand beta, refer Investopedia link: www.investopedia.com

A beta value of 1 means the stock is directly correlated to benchmark index - volatility would be same as overall market.

Beta value less than 1 and greater than 0 means the stock is less volatile than the market.

Beta value more than 1 would mean the stock is more volatile than the market.

A beta value of 1.2 would roughly translate to the stock being 20% more volatile than the overall market.

A negative beta value indicates the stock is inversely correlated to market.

In the example chart, you can see the Beta value change in NSE:RELIANCE with respect to NSE:NIFTY.

Fama-French 3 Factor ModelFama-French 3 Factor Model

Extension of the Capital Asset Pricing Model (CAPM)

CAPM

Ra = Rfr +

where,

Ra = Return of the Asset

Rfr = Risk-Free Rate

βa = Beta Coefficient of the Asset

Rm - Rfr = Market Risk Premium

Fama-French 3 Factor

r = rf + β1*(rm - rf) + β2(smh) +β3(hml)

r = Expected rate of return

rf = Risk-free rate

ß = Factor’s coefficient (sensitivity)

(rm – rf) = Market risk premium

SMB (Small Minus Big) = Historic excess returns of small-cap companies over large-cap companies

HML (High Minus Low) = Historic excess returns of value stocks (high book-to-price ratio) over growth stocks (low book-to-price ratio)

Small is set to $EWSC

Invesco S&P SmallCap 600® Equal Weight ETF

Big is set to $EQLW

Invesco S&P 100 Equal Weight ETF

High is set to $IUSV

iShares Core S&P US Value ETF

Low is set to $IUSG

iShares Core S&P US Growth ETF

returns selections

'returns'

'logarithmic returns' (use for realized (historical) returns)

'geometric returns' (compounded returns)

risk-free rate selections:

$DTB3

$DGS2

$DGS5

$DGS10

$DGS30

tf = primary time-frame

rtf = reference time-frame

Realized Variables for Options ComparisonThese variables can be used in comparison with the implied volatility of options.

Variables:

Realized Volatility

mathematical notation lowercase 'sigma'

Realized Variance

mathematical notation lowercase 'sigma' squared

Realized Beta

mathematical notation lowercase 'beta'

Timeframes:

Yearly = 250 or 365

Quarterly = 50 or 90

Monthly = 20 or 30

Important Note:

Options Contract Expiry = barmerge.lookahead_on

"Merge strategy for the requested data position. Requested barset is merged with current barset in the order of sorting bars by their opening time. This merge strategy can lead to undesirable effect of getting data from "future" on calculation on history. This is unacceptable in backtesting strategies, but can be useful in indicators."

[ All other timeframes barmerge.lookahead is disabled.

Risk Metrics: Crypto VersionRisk Metrics for Crypto.

Market can be set to BTCUSD, BTCEUR, BTCCHF, BTCGBP, BTC1!, BTC2!, SPX, and DTB3

Beta

Correlation

Standard Deviation

Variance

R-squared

Portfolio: alpha, beta, stdev, variance, mean, max drawdown...Portfolio Metrics **New**

'returns'

'log returns'

'geometric returns'

portfolio alpha

portfolio beta

portfolio,market correlation

portfolio standard deviation

portfolio variance

mean portfolio returns

maximum drawdown

maximum gain

Risk Metrics: beta 'β', correl 'ρxy', stdev 'σ', variance 'σ²'Portfolio Risk Metrics (Part I):

beta 'β'

The beta coefficient can be interpreted as follows:

β =1 exactly as volatile as the market

β >1 more volatile than the market

β <1>0 less volatile than the market

β =0 uncorrelated to the market

β <0 negatively correlated to the market

excerpt from the Corporate Finance Institute

correlation coefficient 'ρxy'

The correlation coefficient is a value that indicates the strength of the relationship between variables.

The coefficient can take any values from -1 to 1. The interpretations of the values are:

-1: Perfect negative correlation. The variables tend to move in opposite directions

(i.e., when one variable increases, the other variable decreases).

0: No correlation. The variables do not have a relationship with each other.

1: Perfect positive correlation. The variables tend to move in the same direction

(i.e., when one variable increases, the other variable also increases).

excerpt from the Corporate Finance Institute

standard deviation 'σ'

68% of returns will fall within 1 standard deviation of the arithmetic mean

95% of returns will fall within 2 standard deviations of the arithmetic mean

99% of returns will fall within 3 standard deviations of the arithmetic mean

excerpt from Corporate Finance Institute

variance 'σ²'

In investing, variance is used to compare the relative performance of each asset in a portfolio.

Because the results can be difficult to analyze, standard deviation is often used instead of variance.

In either case, the goal for the investor is to improve asset allocation.

excerpt from Investopedia

Portfolio Metrics = α(Jensen's), β, CAPM(Ra), Sharpe, TreynorPortfolio Metrics...

Standard Deviation

Jensen's Alpha

Beta

Expected Return (CAPM, Ra)

Sharpe Ratio

Treynor Ratio

Alpha & BetaAlpha & Beta Indicators for Portfolio Performance

β = Σ Correlation (RP, RM) * (σP/σM)

α P = E(RP) –

Where,

RP = Portfolio Return (or Investment Return)

RM = Market Return (or Benchmark Index)

RF = Risk-Free Rate

How to use the Indicator

RM = SPX (Default)

The Market Return for the indicator has the options of $SPX, $NDX, or $DJI (S&P 500, Nasdaq 100, Dow 30)

RF = FRED: DTB3

The Risk-Free Rate in the Indicator is set to the 3-Month Treasury Bill: Secondary Market Rate

The Default Timeframe is 1260 or 5-Years (252 Trading Days in One Year)

RP = The symbol you enter

HOWEVER , you can determine your portfolio value by following the following directions below.

Note: I am currently working on an indicator that will allow you to insert the weights of your positions.

Complete Portfolio Analysis Directions

You will first need...

a) spreadsheet application - Google Sheets is Free, but Microsoft Excel will convert ticker symbols to Stocks and Retrieve Data.

b) your current stock tickers, quantity of shares, and last price information

In the spreadsheet,

In the first column list the stock tickers...

AMZN

AAPL

TSLA

In the second column list the quantity of shares you own...

5

10

0.20

In the third column insert the last price

Excel: Three tickers will automatically give you the option to "Convert to Stocks",

after conversion, click once on cell and click the small tab in the upper right-hand of the highlighted cell.

Click the tab and a menu pops up

Find "Price", "Price Extended-Hours", or "Previous Close"...

$3,284.72

$497.48

$2,049.98

Next, multiply the number of shares by the price (Stock Market Value)

Excel: in fourth column type "=(B1*C1)", "=(B2*C2)", "=(B3*C3)"...

= $16,423.60

= $4,974.80

= $410.00

add the three calculated numbers together or click "ΣAutoSum" (Portfolio Market Value)

= $21,808.40

Last, divide the market value of AMZN ($16,423.60) by the Portfolio Market Value ($21,808.40) for each of the stocks.

= 0.7531

= 0.2281

= 0.0188

These values are the weight of the stock in your portfolio.

Go back to TradingView

Enter into the "search box" the following...

AMZN*0.7531 + AAPL*0.2281 + TSLA*0.0188

and click Enter

Now you can use the "Alpha & Beta" Indicator to analyze your entire portfolio!

Beta 252 Days (NIFTY 50) by AkshayThe script derives the Beta Value of 252 days of a stock with Benchmark Index NIFTY 50. Note:- I have edited the script using an existing Beta script by Ricardo Santos. Thank you to him! :)

Hello VWAP "Beta"This is my 1st indicator, and my attention is to plot the VWAP "Volume-weighted average price" using the SMA "Simple Moving Average" over time... IE over the last 50,100,200 bars and just the VWAP... All of them in just one line... I have made it when I have been using the BTC/US chart, but it should work for stocks/forex or any other chart that you want to use...

I am not completely sure about this indicator and I do want to add more to this, that is how come I am posting to the community to show what I have done and people can use it and if they are open to it give me feedback or tips to make it better...

Happy trading...

SPY RelativeShows an instrument's sentiment in a day (or week) compared to the market (SPY default). The Red line shows bearish sentiment compared to the market and the green is bullish. Technically this works like a proxy for Alpha/Beta factor.

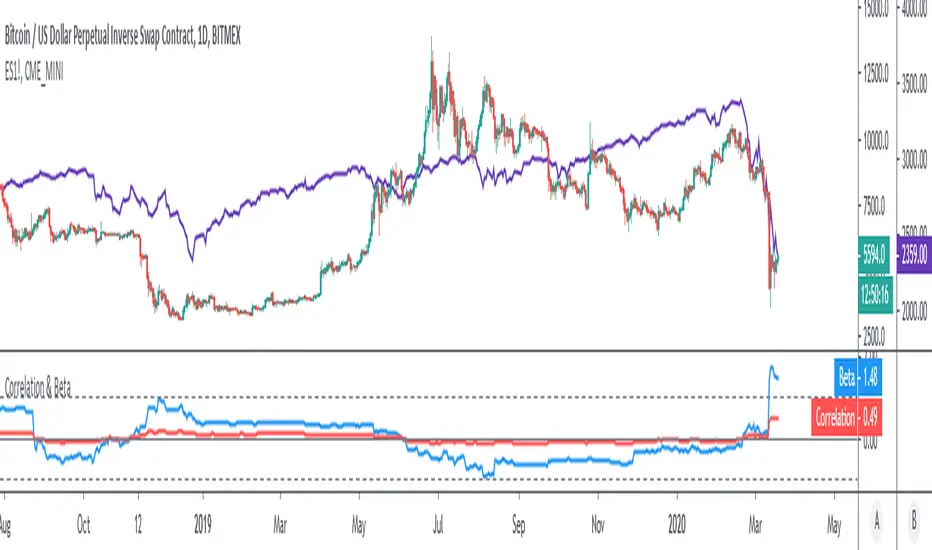

Correlation & BetaDisplay the correlation coefficient and/or Beta of an asset to a specified market.

Options to:

- Specify market (S&P500 futures by default)

- Display one or other metrics

- Modify assessment period (200 bars by default)

- Calculate on price, returns or log-returns