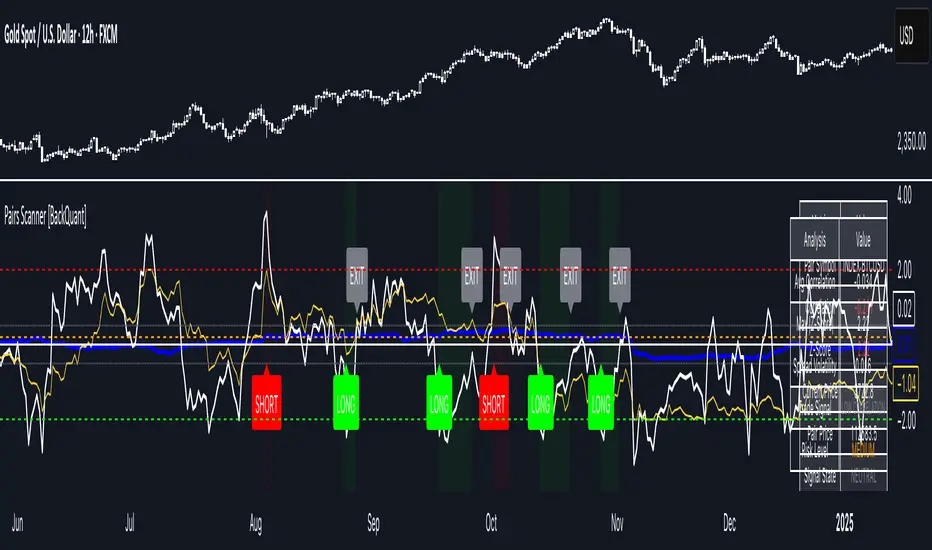

Pairs Trading Scanner [BackQuant]Pairs Trading Scanner

What it is

This scanner analyzes the relationship between your chart symbol and a chosen pair symbol in real time. It builds a normalized “spread” between them, tracks how tightly they move together (correlation), converts the spread into a Z-Score (how far from typical it is), and then prints clear LONG / SHORT / EXIT prompts plus an at-a-glance dashboard with the numbers that matter.

Why pairs at all?

Markets co-move. When two assets are statistically related, their relationship (the spread) tends to oscillate around a mean.

Pairs trading doesn’t require calling overall market direction you trade the relative mispricing between two instruments.

This scanner gives you a robust, visual way to find those dislocations, size their significance, and structure the trade.

How it works (plain English)

Step 1 Pick a partner: Select the Pair Symbol to compare against your chart symbol. The tool fetches synchronized prices for both.

Step 2 Build a spread: Choose a Spread Method that defines “relative value” (e.g., Log Spread, Price Ratio, Return Difference, Price Difference). Each lens highlights a different flavor of divergence.

Step 3 Validate relationship: A rolling Correlation checks if the pair is moving together enough to be tradable. If correlation is weak, the scanner stands down.

Step 4 Standardize & score: The spread is normalized (mean & variability over a lookback) to form a Z-Score . Large absolute Z means “stretched,” small means “near fair.”

Step 5 Signals: When the Z-Score crosses user-defined thresholds with sufficient correlation , entries print:

LONG = long chart symbol / short pair symbol,

SHORT = short chart symbol / long pair symbol,

EXIT = mean reversion into the exit zone or correlation failure.

Core concepts (the three pillars)

Spread Method Your definition of “distance” between the two series.

Guidance:

Log Spread: Focuses on proportional differences; robust when prices live on different scales.

Price Ratio: Classic relative value; good when you care about “X per Y.”

Return Difference: Emphasizes recent performance gaps; nimble for momentum-to-mean plays.

Price Difference: Straight subtraction; intuitive for similar-scale assets (e.g., two ETFs).

Correlation A rolling score of co-movement. The scanner requires it to be above your Min Correlation before acting, so you’re not trading random divergence.

Z-Score “How abnormal is today’s spread?” Positive = chart richer than pair; negative = cheaper. Thresholds define entries/exits with transparent, statistical context.

What you’ll see on the chart

Correlation plot (blue line) with a dashed Min Correlation guide. Above the line = green zone for signals; below = hands off.

Z-Score plot (white line) with colored, dashed Entry bands and dotted Exit bands. Zero line for mean.

Normalized spread (yellow) for a quick “shape read” of recent divergence swings.

Signal markers :

LONG (green label) when Z < –Entry and corr OK,

SHORT (red label) when Z > +Entry and corr OK,

EXIT (gray label) when Z returns inside the Exit band or correlation drops below the floor.

Background tint for active state (faint green for long-spread stance, faint red for short-spread stance).

The two built-in dashboards

Statistics Table (top-right)

Pair Symbol Your chosen partner.

Correlation Live value vs. your minimum.

Z-Score How stretched the spread is now.

Current / Pair Prices Real-time anchors.

Signal State NEUTRAL / LONG / SHORT.

Price Ratio Context for ratio-style setups.

Analysis Table (bottom-right)

Avg Correlation Typical co-movement level over your window.

Max |Z| The recent extremes of dislocation.

Spread Volatility How “lively” the spread has been.

Trade Signal A human-readable prompt (e.g., “LONG A / SHORT B” or “NO TRADE” / “LOW CORRELATION”).

Risk Level LOW / MEDIUM / HIGH based on current stretch (absolute Z).

Signals logic (plain English)

Entry (LONG): The spread is unusually negative (chart cheaper vs pair) and correlation is healthy. Expect mean reversion upward in the spread: long chart, short pair.

Entry (SHORT): The spread is unusually positive (chart richer vs pair) and correlation is healthy. Expect mean reversion downward in the spread: short chart, long pair.

Exit: The spread relaxes back toward normal (inside your exit band), or correlation deteriorates (relationship no longer trusted).

A quick, repeatable workflow

1) Choose your pair in context (same sector/theme or known macro link). Think: “Do these two plausibly co-move?”

2) Pick a spread lens that matches your narrative (ratio for relative value, returns for short-term performance gaps, etc.).

3) Confirm correlation is above your floor no corr, no trade.

4) Wait for a stretch (Z beyond Entry band) and a printed LONG / SHORT .

5) Manage to the mean (EXIT band) or correlation failure; let the scanners’ state/labels keep you honest.

Settings that matter (and why)

Spread Method Defines the “mispricing” you care about.

Correlation Period Longer = steadier regime read, shorter = snappier to regime change.

Z-Score Period The window that defines “normal” for the spread; it sets the yardstick.

Use Percentage Returns Normalizes series when using return-based logic; keep on for mixed-scale assets.

Entry / Exit Thresholds Set your stretch and your target reversion zone. Wider entries = rarer but stronger signals.

Minimum Correlation The gatekeeper. Raising it favors quality over quantity.

Choosing pairs (practical cheat sheet)

Same family: two index ETFs, two oil-linked names, two gold miners, two L1 tokens.

Hedge & proxy: stock vs. sector ETF, BTC vs. BTC index, WTI vs. energy ETF.

Cross-venue or cross-listing: instruments that are functionally the same exposure but price differently intraday.

Reading the cues like a pro

Divergence shape: The yellow normalized spread helps you see rhythm fast spike and snap-back versus slow grind.

Corr-first discipline: Don’t fight the “Min Correlation” line. Good pairs trading starts with a relationship you can trust.

Exit humility: When Z re-centers, let the EXIT do its job. The edge is the journey to the mean, not overstaying it.

Frequently asked (quick answers)

“Long/Short means what exactly?”

LONG = long the chart symbol and short the pair symbol.

SHORT = short the chart symbol and long the pair symbol.

“Do I need same price scales?” No. The spread methods normalize in different ways; choose the one that fits your use case (log/ratio are great for mixed scales).

“What if correlation falls mid-trade?” The scanner will neutralize the state and print EXIT . Relationship first; trade second.

Field notes & patterns

Snap-back days: After a one-sided session, return-difference spreads often flag cleaner intraday mean reversions.

Macro rotations: Ratio spreads shine during sector re-weights (e.g., value vs. growth ETFs); look for steady corr + elevated |Z|.

Event bleed-through: If one symbol reacts to news and its partner lags, Z often flags a high-quality, short-horizon re-centering.

Display controls at a glance

Show Statistics Table Live state & key numbers, top-right.

Show Analysis Table Context/risk read, bottom-right.

Show Correlation / Spread / Z-Score Toggle the sub-charts you want visible.

Show Entry/Exit Signals Turn markers on/off as needed.

Coloring Adjust Long/Short/Neutral and correlation line colors to match your theme.

Alerts (ready to route to your workflow)

Pairs Long Entry Z falls through the long threshold with correlation above minimum.

Pairs Short Entry Z rises through the short threshold with correlation above minimum.

Pairs Trade Exit Z returns to neutral or the relationship fails your correlation floor.

Correlation Breakdown Rolling correlation crosses your minimum; relationship caution.

Final notes

The scanner is designed to keep you systematic: require relationship (correlation), quantify dislocation (Z-Score), act when stretched, stand down when it normalizes or the relationship degrades. It’s a full, visual loop for relative-value trading that stays out of your way when it should and gets loud only when the numbers line up.

Backquant

Dynamic Stop Loss Optimizer [BackQuant]Dynamic Stop Loss Optimizer

Overview

Stop placement decides expectancy. This tool gives you three professional-grade, adaptive stop engines, ATR, Volatility, and Hybrid. So your exits scale with current conditions instead of guessing fixed ticks. It trails intelligently, redraws as the market evolves, and annotates the chart with clean labels/lines and a compact stats table. Pick the engine that fits the trade, or switch on the fly.

What it does

Calculates three adaptive stops in real time (ATR-based, Volatility-based, and Hybrid) and keeps them trailed as price makes progress.

Shows exactly where your risk lives with on-chart levels, color-coded markers (long/short), and precise “Risk %” labels at the current bar.

Surfaces context you actually use - current ATR, daily volatility, selected method, and the live stop level—in a tidy, movable table.

Fires alerts on stop hits so you can automate exits or journal outcomes without staring at the screen.

Why it matters

Adaptive risk control: Stops expand in fast tape and tighten in quiet tape. You’re not punished for volatility; you’re aligned with it.

Consistency across assets: The same playbook works whether you’re trading indexes, FX, crypto, or equities, because the engine normalizes to each symbol’s behavior.

Cleaner decision-making: One chart shows your entry idea and its invalidation in the same breath. If price trespasses, you know it instantly.

The three methods (choose your engine)

1) ATR Based “Structure-aware” distance

This classic approach keys off Average True Range to set a stop just beyond typical bar-to-bar excursion. It adapts smoothly to changing ranges and respects swing structure.

Use when: you want a steady, intuitive buffer that tracks trend legs without hugging price.

See it in action:

2) Volatility Based “Behavior-aware” distance

This engine derives stop distance from current return volatility (annualized, then scaled back down to the session). It reacts to regime shifts quickly and normalizes risk across symbols with very different prices.

Use when: you want the stop to breathe with realized volatility and respond faster to heat-ups/cool-downs.

See it in action:

3) Hybrid “Best of both worlds”

The Hybrid blends the ATR and Volatility distances into one consensus level, then trails it intelligently. You get the structural common sense of ATR and the regime sensitivity of Vol.

Use when: you want robust, all-weather behavior without micromanaging inputs.

See it in action:

How it trails

Longs: The stop ratchets up with favorable movement and holds its ground on shallow pullbacks. If price closes back into the risk zone, the level refreshes to the newest valid distance.

Shorts: Mirror logic ratchets down with trend, resists noise, and refreshes if price reclaims the zone.

Hybrid trailing: Uses the blended distance and the same “no give-backs” principle to keep gains protected as structure builds.

Reading the chart

Markers: Circles = ATR stops, Crosses = Vol stops, Diamonds = Hybrid. Colors indicate long (red level under price) vs short (green level above price).

Lines: The latest active stop is extended with a dashed line so you can see it at a glance.

Labels: “Long SL / Short SL” shows the exact price and current risk % from the last close no math required.

Table: ATR value, Daily Vol %, your chosen Method, the Current SL, and Risk %—all in one compact block that you can pin top-left/right/center.

Quick workflow

Define the idea: Long or Short, and which engine fits the tape (ATR, Vol, or Hybrid).

Place and trail: Let the optimizer print the level; trail automatically as the move develops.

Manage outcomes: If the line is tagged, you’re out clean. If it holds, you’ve contained heat while giving the trade room to work.

Inputs you’ll actually touch

Calculation Settings

ATR Length / Multiplier: Controls the “structural” cushion.

Volatility Length / Multiplier: Controls the “behavioral” cushion.

Trading Days: 252 or 365 to keep the volatility math aligned with the asset’s trading calendar.

Stop Loss Method

ATR Based | Volatility Based | Hybrid : Switch engines instantly to fit the trade.

Position Type

Long | Short | Both : Show only what you need for the current strategy.

Visual Settings

Show ATR / Vol / Hybrid Stops: Toggle families on/off.

Show Labels: Print price + Risk % at the live stop.

Table Position: Park the metrics where you like.

Coloring

Long/Short/Hybrid colors: Set a palette that matches your theme and stands out on your background.

Practical patterns to watch

Trend-pullback continuation: The stop ratchets behind higher lows (long) or lower highs (short). If price tests the level and rejects, that’s your risk-defined continuation cue.

Break-and-run: After a clean break, the Hybrid will usually sit slightly wider than pure Vol, use it to avoid getting shaken on the first retest.

Range compression: When the ATR and Vol distances converge, the table will show small Risk %. That’s your green light to size up with the same dollar risk, or keep it conservative if you expect expansion.

Alerts

Long Stop Loss Hit : Notifies when price crosses below the live long stop.

Short Stop Loss Hit : Notifies when price crosses above the live short stop.

Why this feels “set-and-serious”

You get a single look that answers three questions in real time: “Where’s my line in the sand?”, “How much heat am I taking right now?”, and “Is this distance appropriate for current conditions?” With ATR, Vol, and Hybrid in one tool, you can run the exact same playbook across symbols and regimes while keeping your chart clean and your risk explicit.

Wavelet Kernal ATR [BackQuant]Wavelet Kernal ATR

Introduction

Wavelet Kernal ATR is a closed-source, chart-side tool that fuses an edge-preserving “wavelet kernal” smoother with an ATR-aware regime line. The goal is simple: follow the real move, ignore the static, and give you clean, visual places to manage risk. It can color the trend directly on price, flip states when regime changes, and (optionally) add a secondary moving-average overlay for confirmation all while keeping the chart readable.

What it is

A single adaptive baseline designed to act like a “bias rail.” When it’s up, you favor longs; when it’s down, you favor shorts. It updates in a way that’s responsive to fresh information but resistant to insignificant wiggles. Around that baseline, an ATR-scaled envelope governs how and when the line concedes to volatility, which helps avoid flip-flopping in chop. Because this release is closed source, the following focuses on behavior and practical use rather than internal math.

What it’s used for

Bias & context: Read the backdrop with one glance; green = bullish regime, red = bearish regime.

Timing: Use slope changes and pullbacks to the line for entries aligned with the dominant push.

Risk placement: The line and its volatility envelope give intuitive zones for stops and targets.

Clarity: Paint candles by state and keep other overlays to a minimum to reduce decision noise.

Why “Wavelet Kernal” matters (plain English)

A wavelet kernal is a localized, scale-aware weighting profile. Instead of averaging every bar equally—or with a single, fixed decay—it emphasizes the most informative part of the recent window while softly down-weighting points that are either too old or too extreme. Three practical benefits result:

Edge preservation: Turning points are less “smeared” than with conventional smoothers, so the line can pivot sooner on genuine breakouts without chasing every tick.

Multi-scale sensitivity: The kernal “listens” to structure at multiple scales inside a compact window, helping it track swing-sized movement while suppressing micro-chop.

Lag vs. noise balance: Because the weighting is localized and shape-aware, you get a calmer line at similar responsiveness compared to common filters; fewer false flips, more meaningful ones.

You don’t need to know the internals to use it: think of the wavelet kernal as a smart stethoscope for price. It hears the heartbeat (trend/impulse) and ignores the coughs (random spikes).

How it behaves

Trend mode: When price expands directionally, the line “sticks” to the move and stays colored in that direction. Pullbacks that remain shallow relative to volatility usually do not flip the state.

Transition mode: After a large push, the line may flatten as volatility compresses. Flat + frequent small flips is the platform telling you: edge is low, wait for expansion.

Shock handling: On sudden spikes, the ATR envelope acts like a reality check—minor overreactions are absorbed, while statistically meaningful breaks force the baseline to concede and re-anchor.

Reading the line (quick heuristics)

Green + rising: Bias long; look for pullbacks toward the line that stall and resume.

Red + falling: Bias short; look for rallies into the line that fade.

Flat + rapid color flips: Stand down or scale down—let the next expansion choose the side.

Color flip at a prior S/R: Treat as a higher-quality signal than flips in the middle of nowhere.

Baseline + ATR corridor (concept)

The volatility envelope isn’t drawn as two fat bands here; it’s used internally to keep the baseline honest. You can think of it as a “breathing room” rule: the line is allowed to adapt with trend, but it shouldn’t jump the fence unless price movement is large enough relative to recent volatility. That’s why the tool feels calm in chop and decisive during actual breaks.

Optional MA Overlay (confluence)

You can overlay a moving average of the baseline itself for slower-regime confirmation. When both agree (baseline direction and its MA slope), you have trend alignment. When they diverge, expect digestion or a possible transition. Keep this overlay subtle; it’s a context layer, not another signal firehose.

What it plots

Wavelet ATR line — the adaptive baseline that flips color with regime.

Optional MA of the baseline — slower confirmation, on or off.

Candle painting — bars can inherit long/short state for instant read-through.

Alerts — available for state flips up/down.

Inputs explained (effect on behavior)

Wavelet ATR Calculation

Price Source — Default hlc3 ; choose your preferred composite of OHLC.

Kernal Calculation Length — The horizon the kernal “listens to.” Longer = steadier, fewer flips; shorter = snappier, more flips.

Kernal Alpha — How strongly the kernal prioritizes the freshest data inside that horizon. Higher alpha = quicker to acknowledge new pushes; lower alpha = more patience.

ATR Period — Determines the volatility memory. Shorter = envelope reacts faster; longer = envelope demands more evidence to concede.

ATR Factor — Scales how “strict” the envelope is. Larger factor = more tolerance (fewer flips); smaller = more sensitivity (earlier regime shifts).

Confluence

Show Atr Moving Average — Turns on the secondary overlay.

MA Type — Choose the flavor you read best (simple, exponential, linear regression, etc.).

Moving Average Period — The overlay’s horizon; treat it as a background current.

Volume Factor / Sigma (when applicable) — Specialized parameter used by certain MA types to shape smoothness.

Plotting & UI

Plot Wavelet ATR — Toggle the main line.

Paint Candles According to Trend — Color bars by the baseline’s state.

Long/Short Colors — Match your chart theme.

A practical playbook

Trend-pullback continuation

Setup: Baseline is green and rising. Price pulls back toward it, stalls (small bodies or wicks into the line), then resumes upward.

Idea: Enter on the resumption. Protective stop often lives just below the line or the last swing low. Scale targets through prior highs or measured projections.

Breakout + acceptance

Setup: Baseline flattens after consolidation. Price expands away; baseline turns green/red and stays that way as two or three bars “accept” the new area.

Idea: Join on the first controlled retest toward the line. If the line instantly loses color again, treat it as a fakeout.

Failed test / flip-and-go

Setup: Price challenges the line from the wrong side but cannot close through it convincingly; shortly after, the baseline flips color back in the original direction.

Idea: Use that failed test as a springboard—risk tucked beyond the failed side.

Quality checks before you click

Structure context: Is the flip happening near prior highs/lows, session opens, or well-observed levels? Flips at structure carry more information.

Volatility posture: If range is compressing, be picky. If range is expanding, respect the first pullback after the flip.

Clutter discipline: Use the fewest layers that earn their place. Trend line + candle painting is often enough.

Common questions

“Why did the line not flip on that spike?” Because the move wasn’t large or sustained enough relative to recent volatility. The envelope forces patience.

“Why did it flip and then flip back?” That’s what digestion looks like. The kernal preserves edges, but when the market truly has no edge, brief flips are information: sit tight.

“Do I need the overlay MA?” No. It’s optional context. If it helps you filter marginal trades, keep it. If it adds noise, turn it off.

Troubleshooting & fine-tuning (principles, not prescriptions)

Too many flips? Increase the Kernal Calculation Length or the ATR Factor. You’re asking for a steadier bias.

Feels late on strong trends? Nudge Kernal Alpha higher or shorten the Kernal Length. You’re asking for earlier acknowledgment.

Stops feel random? Place initial risk just beyond the baseline (or the last swing beyond it), then trail only when fresh structure appears.

Charts feel crowded? Keep the baseline + candle coloring; hide the overlay and other ornaments.

Alerts

Wavelet ATR Trend Up

Wavelet ATR Trend Down

Final notes

This tool is built to minimize analysis fatigue: one adaptive line, strong visual feedback, and enough discipline from volatility logic to avoid the “every blip is a signal” trap. The internal math, weighting shapes, and state logic are proprietary and intentionally not disclosed here; you still have full control of behavior through the inputs above. As always, align the settings with your own trade plan, keep the chart readable, and let confluence—not clutter—do the heavy lifting.

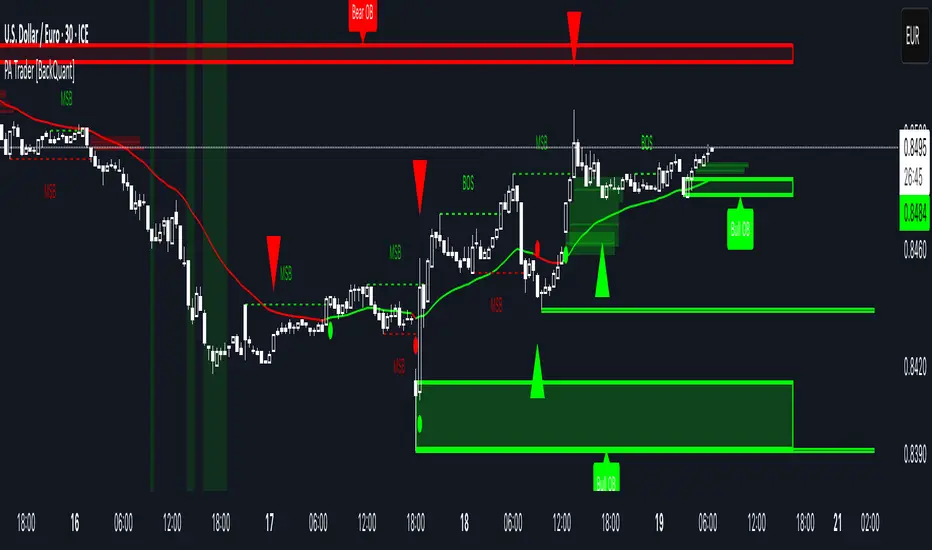

Price Action Trader [BackQuant]Price Action Trader

Introduction

Price Action Trader is an all-in-one, chart-side workflow for reading trend, timing impulses, and mapping high-probability zones the way discretionary traders actually trade. It blends an ensemble trend engine with clean price-action building blocks—Market Structure (BOS/MSB), Fair Value Gaps, Order Blocks, and Volumetric Support/Resistance—so you can form a bias, find confluence, and execute with context.

What is it

A modular “price-action stack” that:

Paints trend bias and impulse shifts on the chart (optional candle coloring).

Auto-annotates internal & swing structure (BOS / MSB).

Finds FVGs on your chosen timeframe and draws them cleanly.

Detects Order Blocks (with optional FVG confirmation).

Builds volumetric S/R levels that adapt to liquidity.

Emits alerts for key events (new levels, touches, breaks, OB creation/touch).

Everything is configurable—keep it minimal (trend + a few zones) or run the full toolkit.

What’s it used for

Bias first, trade second: establish direction/conviction, then execute where structure, gaps, blocks, and volume agree.

Timing: impulse flips and level touches provide actionable triggers.

Risk placement: OB edges, FVG midlines, and volumetric bands give logical stop/target references.

Review & journaling: optional session shading and labeled structures make post-trade notes simple.

Composite Trend Model

A lightweight signal line (default: 30-period) that turns green when the composite regime is bullish and red when bearish. Under the hood, multiple cues (adaptive momentum, de-noised oscillation, volatility-aware filters) are blended into a single directional score; when thresholds flip, the line recolors and optional Long/Short dots appear.

How to use

Treat the line as your bias rail : favor longs while green, shorts while red.

Flat/rapid flips = stand down or reduce size.

Prefer clean charts? Keep only the line and (optionally) trend-painted candles.

Inputs to know

Show Trend Signal Line / Width.

Paint Candles by Trend.

Long/Bearish color controls.

Impulse Model

Highlights short-term pressure shifts with optional impulse candle coloring and ▲/▼ markers. Great for entries in the prevailing trend and for early warnings when impulses fire against bias.

How to use

Up-bias: look for the next impulse-up near structure/FVG/OB or volumetric support.

Down-bias: mirror the logic.

Frequent counter-impulses → expect chop or regime change.

Inputs to know

Show Impulse Signals.

Paint Impulse Candles.

Market Structure

Automatic Internal (tight lookback) and Swing (wider lookback) structure with BOS and MSB (CHoCH) labels. You decide what to show—All, BOS only, MSB only—independently for internal vs swing.

How to use

Use Swing labels for the primary map; Internal for entry refinement.

After a bullish MSB , seek the first HL back into support/FVG/OB.

After a bearish BOS , favor LH fades into resistance/FVG/OB.

Inputs to know

Swing Lookback / Internal Lookback.

Swing/Internal Structure: All | BOS | MSB | None .

Separate bull/bear color controls for both layers.

Fair Value Gaps

Detects bullish/bearish FVGs on the current or higher TF, draws boxes, and can extend them forward. Midlines provide quick visual targeting.

How to use

In-trend fills: in an up-bias, tags of bullish FVGs often offer high-quality continuation entries, especially with structure/OB confluence.

Failed fills: rejections at the midline can signal emerging strength/weakness.

Inputs to know

Show FVG / Show Last N / Extend.

Timeframe (blank = chart TF; set higher TF for macro FVGs).

Bull/Bear colors (tune opacity to taste).

Volumetric Support and Resistance

Builds adaptive S/R from price interaction + relative volume over a rolling lookback. Levels store touch counts; you can show volume stats on labels or inside boxes. Transparency and border thickness can scale with volume so stronger levels are visually louder. Broken levels can auto-remove.

How to use

Use as confluence with structure, OBs, and FVGs. A long at volumetric support + Bull OB + FVG midline is qualitatively different from a naked level.

If a level breaks on strong volume, stop fading—flip expectations or wait for a clean retest.

Inputs to know

Detection Sensitivity / Volume Multiplier.

Analysis Period / Max Levels / Min Distance (%).

Remove Broken / Extend Right / Show Volume Info / Text Inside.

Support/Resistance colors (+ high-vol variants).

Alerts

New Support/Resistance Level Created.

Level Touch.

Level Break.

Order Blocks

Detects bullish/bearish OBs using configurable fractals (3- or 5-bar) with a break confirmation (by Close or High/Low). Optional FVG proximity filter, right-extension, and auto-delete when filled.

How to use

Bullish bias: stalk pullbacks into fresh Bull OBs aligned with a bullish FVG or volumetric support.

If price fills an opposing OB and fails to continue, reassess bias—context may be shifting.

Inputs to know

Fractal Type & Break Method (Close / HL).

Filter with FVG + Max FVG Distance.

Extend Blocks / Delete When Filled / Show Labels.

Alerts

New Order Block Created.

Order Block Touch.

Final Notes

Suggested workflow

Start with Composite Trend (bias).

Mark Swing structure in that direction.

Wait for an Impulse in-direction near an OB / FVG / Volumetric level.

Risk = nearest opposite level or OB edge; targets = FVG midlines / next S/R.

Timeframes & assets

Defaults suit liquid intraday and 1–4H swing.

Slower markets → lengthen lookbacks, lower sensitivity.

Very noisy crypto → keep trend visible, trim drawings (e.g., MSB only, last 3–5 FVGs, 8–12 volume levels).

Keep it readable

Turn off modules you don’t need today—fewer, higher-quality signals beat clutter.

About this release

Internal scoring, smoothing, and detection logic are proprietary. Behavior is controlled via inputs described above.

Trade with a plan, test your settings, and let confluence do the heavy lifting.

PolyFilter [BackQuant]PolyFilter

A flexible, low-lag trend filter with three smoothing engines—optimized for clean bias, fewer whipsaws, and clear alerting.

What it does

PolyFilter draws a single “intelligent” baseline that adapts to price while suppressing noise. You choose the engine— Fractional MA , Ehlers 2-Pole Super Smoother , or a Multi-Kernel blend . The line can color itself by slope (trend) or by position vs price (above/below), and you get four ready-made alerts for flips and crosses.

What it plots

PolyFilter line — your smoothed trend baseline (width set by “Line Width”).

Optional candle & background coloring — choose: color by trend slope or by whether price is above/below the filter.

Signal markers — Arrows with L/S when the slope flips or when price crosses the line (if you enable shapes/alerts).

How the three engines differ

Fractional MA (experimental) — A power-law weighting of past bars (heavier focus on the most recent samples without throwing away history). The Adaptation Speed acts like the “fraction” exponent (default 0.618). Lower values lean more on recent bars; higher values spread weight further back.

Ehlers 2-Pole Super Smoother — Classic low-lag IIR smoother that aggressively reduces high-frequency noise while preserving turns. Great default when you want a steady, responsive baseline with minimal parameter fuss.

Multi-Kernel — A 70/30 blend of a Gaussian window and an exponential kernel. The Gaussian contributes smooth structure; the exponential adds a hint of responsiveness. Useful for assets that oscillate but still trend.

Reading the colors

Trend mode (default) — Line & candles turn green while the filter is rising (signal > signal ) and red while it’s falling.

Above/Below mode — Line & candles reflect price’s position relative to the filter: green when price > filter, red when price < filter. This is handy if you treat the filter like a dynamic “fair value” or bias line.

Inputs you’ll actually use

Calculation Settings

Price Source — Default HLC/3. Switch to Close for stricter trend, or HLC3/HL2 to soften single-print spikes.

Filter Length — Window/period for all engines. Shorter = snappier turns; longer = smoother line.

Adaptation Speed — Only affects Fractional MA . Lower it for faster, more local weighting; raise it for smoother, more global weighting.

Filter Type — Pick one of: Fractional MA, Ehlers 2-Pole, Multi-Kernel.

UI & Plotting

Color based off… — Choose Trend (slope) or > or < Close (position vs price).

Long/Short Colors — Customize bull/bear hues to your theme.

Show Filter Line / Paint candles / Color background — Visual toggles for the line, bars, and backdrop.

Line Width — Make the filter stand out (2–3 works well on most charts).

Signals & Alerts

PolyFilter Trend Up — Slope flips upward (the filter crosses above its prior value). Good for early continuation entries or stop-tightening on shorts.

PolyFilter Trend Down — Slope flips downward. Often used to scale out longs or rotate bias.

PolyFilter Above Price — The filter line crosses up through price (filter > price). This can confirm that mean has “caught up” after a pullback.

PolyFilter Below Price — The filter line crosses down through price (filter < price). Useful to confirm momentum loss on bounces.

Quick starts (suggested presets)

Intraday (5–15m, crypto or indices) — Ehlers 2-Pole, Length 55–80. Trend coloring ON, candle paint ON. Look for pullbacks to a rising filter; avoid fading a falling one.

Swing (1H–4H) — Multi-Kernel, Length 80–120. Background color OFF (cleaner), candle paint ON. Add a higher-TF confirmation (e.g., 4H filter rising when you trade 1H).

Range-prone FX — Fractional MA, Length 70–100, Adaptation ~0.55–0.70. Consider Above/Below mode to trade mean reversion to the line with a strict risk cap.

How to use it in practice

Bias line — Trade in the direction of the filter slope; stand aside when it flattens and color chops back and forth.

Dynamic support/resistance — Treat the line as a moving value area. In trends, entries often appear on shallow tags of the line with structure confluence.

Regime switch — When the filter flips and holds color for several bars, tighten stops on the opposing side and look for first pullback in the new color.

Stacking filters — Many users run PolyFilter on the active chart and a slower instance (longer length) on a higher timeframe as a “macro bias” guardrail.

Tuning tips

If you see too many flips, lengthen the filter or switch to Multi-Kernel.

If turns feel late, shorten the filter or try Ehlers 2-Pole for lower lag.

On thin or very noisy symbols, prefer HLC3 as the source and longer lengths.

Performance note: very large lengths increase computation time for the Multi-Kernel and Fractional engines. Start moderate and scale up only if needed.

Summary

PolyFilter gives you a single, trustworthy baseline that you can read at a glance—either as a pure trend line (slope coloring) or as a dynamic “above/below fair value” reference. Pick the engine that matches your market’s personality, set a sensible length, and let the color and alerts guide bias, entries on pullbacks, and risk on reversals.

Kalman Adjusted Average True Range [BackQuant]Kalman Adjusted Average True Range

A volatility-aware trend baseline that fuses a Kalman price estimate with ATR “rails” to create a smooth, adaptive guide for entries, exits, and trailing risk.

Built on my original Kalman

This indicator is based on my original Kalman Price Filter:

That core smoother is used here to estimate the “true” price path, then blended with ATR to control step size and react proportionally to market noise.

What it plots

Kalman ATR Line the main baseline that turns up/down with the filtered trend.

Optional Moving Average of the Kalman ATR a secondary line for confluence (SMA/Hull/EMA/WMA/DEMA/RMA/LINREG/ALMA).

Candle Coloring (optional) paint bars by the baseline’s current direction.

Why combine Kalman + ATR?

Kalman reduces measurement noise and produces a stable path without the lag of heavy MAs.

ATR rails scale the baseline’s step to current volatility, so it’s calm in chop and more responsive in expansion.

The result is a single, intelligible line you can trade around: slope-up = constructive; slope-down = caution.

How it works (plain English)

Each bar, the Kalman filter updates an internal state (tunable via Process Noise , Measurement Noise , and Filter Order ) to estimate the underlying price.

An ATR band (Period × Factor) defines the allowed per-bar adjustment. The baseline cannot “jump” beyond those rails in one step.

A direction flip is detected when the baseline’s slope changes sign (upturn/downturn), and alerts are provided for both.

Typical uses

Trend confirmation Trade in the baseline’s direction; avoid fading a firmly rising/falling line.

Pullback timing Look for entries when price mean-reverts toward a rising baseline (or exits on tags of a falling one).

Trailing risk Use the baseline as a dynamic guide; many traders set stops a small buffer beyond it (e.g., a fraction of ATR).

Confluence Enable the MA overlay of the Kalman ATR; alignment (baseline above its MA and rising) supports continuation.

Inputs & what they do

Calculation

Kalman Price Source which price the filter tracks (Close by default).

Process Noise how quickly the filter can adapt. Higher = more responsive (but choppier).

Measurement Noise how much you distrust raw price. Higher = smoother (but slower to turn).

Filter Order (N) depth of the internal state array. Higher = slightly steadier behavior.

Kalman ATR

Period ATR lookback. Shorter = snappier; longer = steadier.

Factor scales the allowed step per bar. Larger factors permit faster drift; smaller factors clamp movement.

Confluence (optional)

MA Type & Period compute an MA on the Kalman ATR line , not on price.

Sigma (ALMA) if ALMA is selected, this input controls the curve’s shape. (Ignored for other MA types.)

Visuals

Plot Kalman ATR toggle the main line.

Paint Candles color bars by up/down slope.

Colors choose long/short hues.

Signals & alerts

Trend Up baseline turns upward (slope crosses above 0).

Alert: “Kalman ATR Trend Up”

Trend Down baseline turns downward (slope crosses below 0).

Alert: “Kalman ATR Trend Down”

These are state flips , not “price crossovers,” so you avoid many one-bar head-fakes.

How to start (fast presets)

Swing (daily/4H) ATR Period 7–14, Factor 0.5–0.8, Process Noise 0.02–0.05, Measurement Noise 2–4, N = 3–5.

Intraday (5–15m) ATR Period 5–7, Factor 0.6–1.0, Process Noise 0.05–0.10, Measurement Noise 2–3, N = 3–5.

Slow assets / FX raise Measurement Noise or ATR Period for calmer lines; drop Factor if the baseline feels too jumpy.

Reading the line

Rising & curving upward momentum building; consider long bias until a clear downturn.

Flat & choppy regime uncertainty; many traders stand aside or tighten risk.

Falling & accelerating distribution lower; short bias until a clean upturn.

Practical playbook

Continuation entries After a Trend Up alert, wait for a minor pullback toward the baseline; enter on evidence the line keeps rising.

Exit/reduce If long and the baseline flattens then turns down, trim or exit; reverse logic for shorts.

Filters Add a higher-timeframe check (e.g., only take longs when the daily Kalman ATR is rising).

Stops Place stops just beyond the baseline (e.g., baseline − x% ATR for longs) to avoid “tag & reverse” noise.

Notes

This is a guide to state and momentum, not a guarantee. Combine with your process (structure, volume, time-of-day) for decisions.

Settings are asset/timeframe dependent; start with the presets and nudge Process/Measurement Noise until the baseline “feels right” for your market.

Summary

Kalman ATR takes the noise-reduction of a Kalman price estimate and couples it with volatility-scaled movement to produce a clean, adaptive baseline. If you liked the original Kalman Price Filter (), this is its trend-trading cousin purpose-built for cleaner state flips, intuitive trailing, and confluence with your existing

Key Levels: Daily, Weekly, Monthly [BackQuant]Key Levels: Daily, Weekly, Monthly

Map the market’s “memory” in one glance—yesterday’s range, this week’s chosen day high/low, and D/W/M opens—then auto-clean levels once they break.

What it does

This tool plots three families of high-signal reference lines and keeps them tidy as price evolves:

Chosen Day High/Low (per week) — Pick a weekday (e.g., Monday). For each past week, the script records that day’s session high and low and projects them forward for a configurable number of bars. These act like “memory levels” that price often revisits.

Daily / Weekly / Monthly Opens — Plots the opening price of each new day, week, and month with separate styling. These opens frequently behave like magnets/flip lines intraday and anchors for regime on higher timeframes.

Auto-pruning — When price breaks a stored level, the script can automatically remove it to reduce clutter and refocus you on still-active lines. See: (broken levels removed).

Why these levels matter

Liquidity pockets — Prior day’s high/low and the daily open concentrate stops and pending orders. Mapping them quickly reveals likely sweep or fade zones. Example: previous day highs + daily open highlighting liquidity:

Context & regime — Monthly opens frame macro bias; trading above a rising cluster of monthly opens vs. below gives a clean top-down read. Example: monthly-only “macro outlook” view:

Cleaner charts — Auto-remove broken lines so you focus on what still matters right now.

What it plots (at a glance)

Past Chosen Day High/Low for up to N prior weeks (your choice), extended right.

Current Daily Open , Weekly Open , and Monthly Open , each with its own color, label, and forward extension.

Optional short labels (e.g., “Mon High”) or full labels (with week/month info).

How breaks are detected & cleaned

You control both the evidence and the timing of a “break”:

Break uses — Choose Close (more conservative) or Wick (more sensitive).

Inclusive? — If enabled, equality counts (≥ high or ≤ low). If disabled, you need a strict cross.

Allow intraday breaks? — If on, a level can break during the tracked day; if off, the script only counts breaks after the session completes.

Remove Broken Levels — When a break is confirmed, the line/label is deleted automatically. (See the demo: )

Quick start

Pick a Day of Week to Track (e.g., Monday).

Set how many weeks back to show (e.g., 8–10).

Choose how far to extend each family (bars to the right for chosen-day H/L and D/W/M opens).

Decide if a break uses Close or Wick , and whether equality counts.

Toggle Remove Broken Levels to keep the chart clean automatically.

Tips by use-case

Intraday bias — Watch the Daily Open as a magnet/flip. If price gaps above and holds, pullbacks to the daily open often decide direction. Pair with last day’s high/low for sweep→reversal or true breakout cues. See:

Weekly structure — Track the week’s chosen day (e.g., Monday) high/low across prior weeks. If price stalls near a cluster of old “Monday Highs,” look for sweep/reject patterns or continuation on reclaim.

Macro regime — Hide daily/weekly lines and keep only Monthly Opens to read bigger cycles at a glance (BTC/crypto especially). Example:

Customization

Use wicks or bodies for highs/lows (wicks capture extremes; bodies are stricter).

Line style & thickness — solid/dashed/dotted, width 1–5, plus global transparency.

Labels — Abbreviated (“Mon High”, “D Open”) or full (month/week/day info).

Color scheme — Separate colors for highs, lows, and each of D/W/M opens.

Capacity controls — Set how many daily/weekly/monthly opens and how many weeks of chosen-day H/L to keep visible.

What’s under the hood

On your selected weekday, the script records that session’s true high and true low (using wicks or body-based extremes—your choice), then projects a horizontal line forward for the next bars.

At each new day/week/month , it records the opening price and projects that line forward as well.

Each bar, the script checks your “break” rules; once broken, lines/labels are removed if auto-cleaning is on.

Everything updates in real time; past levels don’t repaint after the session finishes.

Recommended presets

Day trading — Weeks back: 6–10; extend D/W opens: 50–100 bars; Break uses: Close ; Inclusive: off; Auto-remove: on.

Swing — Fewer daily opens, more weekly opens (2–6), and 8–12 weeks of chosen-day H/L.

Macro — Show only Monthly Opens (1–6 months), dashed style, thicker lines for clarity.

Reading the examples

Broken lines disappear — decluttering in action:

Macro outlook — monthly opens as cycle rails:

Liquidity map — previous day highs + daily open:

Final note

These are not “signals”—they’re reference points that many participants watch. By standardising how you draw them and automatically clearing the ones that no longer matter, you turn a noisy chart into a focused map: where liquidity likely sits, where price memory lives, and which lines are still in play.

Quantile Regression Bands [BackQuant]Quantile Regression Bands

Tail-aware trend channeling built from quantiles of real errors, not just standard deviations.

What it does

This indicator fits a simple linear trend over a rolling lookback and then measures how price has actually deviated from that trend during the window. It then places two pairs of bands at user-chosen quantiles of those deviations (inner and outer). Because bands are based on empirical quantiles rather than a symmetric standard deviation, they adapt to skewed and fat-tailed behaviour and often hug price better in trending or asymmetric markets.

Why “quantile” bands instead of Bollinger-style bands?

Bollinger Bands assume a (roughly) symmetric spread around the mean; quantiles don’t—upper and lower bands can sit at different distances if the error distribution is skewed.

Quantiles are robust to outliers; a single shock won’t inflate the bands for many bars.

You can choose tails precisely (e.g., 1%/99% or 5%/95%) to match your risk appetite.

How it works (intuitive)

Center line — a rolling linear regression approximates the local trend.

Residuals — for each bar in the lookback, the indicator looks at the gap between actual price and where the line “expected” price to be.

Quantiles — those gaps are sorted; you select which percentiles become your inner/outer offsets.

Bands — the chosen quantile offsets are added to the current end of the regression line to draw parallel support/resistance rails.

Smoothing — a light EMA can be applied to reduce jitter in the line and bands.

What you see

Center (linear regression) line (optional).

Inner quantile bands (e.g., 25th/75th) with optional translucent fill.

Outer quantile bands (e.g., 1st/99th) with a multi-step gradient to visualise “tail zones.”

Optional bar coloring: bars trend-colored by whether price is rising above or falling below the center line.

Alerts when price crosses the outer bands (upper or lower).

How to read it

Trend & drift — the slope of the center line is your local trend. Persistent closes on the same side of the center line indicate directional drift.

Pullbacks — tags of the inner band often mark routine pullbacks within trend. Reaction back to the center line can be used for continuation entries/partials.

Tails & squeezes — outer-band touches highlight statistically rare excursions for the chosen window. Frequent outer-band activity can signal regime change or volatility expansion.

Asymmetry — if the upper band sits much further from the center than the lower (or vice versa), recent behaviour has been skewed. Trade management can be adjusted accordingly (e.g., wider take-profit upslope than downslope).

A simple trend interpretation can be derived from the bar colouring

Good use-cases

Volatility-aware mean reversion — fade moves into outer bands back toward the center when trend is flat.

Trend participation — buy pullbacks to the inner band above a rising center; flip logic for shorts below a falling center.

Risk framing — set dynamic stops/targets at quantile rails so position sizing respects recent tail behaviour rather than fixed ticks.

Inputs (quick guide)

Source — price input used for the fit (default: close).

Lookback Length — bars in the regression window and residual sample. Longer = smoother, slower bands; shorter = tighter, more reactive.

Inner/Outer Quantiles (τ) — choose your “typical” vs “tail” levels (e.g., 0.25/0.75 inner, 0.01/0.99 outer).

Show toggles — independently toggle center line, inner bands, outer bands, and their fills.

Colors & transparency — customize band and fill appearance; gradient shading highlights the tail zone.

Band Smoothing Length — small EMA on lines to reduce stair-step artefacts without meaningfully changing levels.

Bar Coloring — optional trend tint from the center line’s momentum.

Practical settings

Swing trading — Length 75–150; inner τ = 0.25/0.75, outer τ = 0.05/0.95.

Intraday — Length 50–100 for liquid futures/FX; consider 0.20/0.80 inner and 0.02/0.98 outer in high-vol assets.

Crypto — Because of fat tails, try slightly wider outers (0.01/0.99) and keep smoothing at 2–4 to tame weekend jumps.

Signal ideas

Continuation — in an uptrend, look for pullback into the lower inner band with a close back above the center as a timing cue.

Exhaustion probe — in ranges, first touch of an outer band followed by a rejection candle back inside the inner band often precedes mean-reversion swings.

Regime shift — repeated closes beyond an outer band or a sharp re-tilt in the center line can mark a new trend phase; adjust tactics (stop-following along the opposite inner band).

Alerts included

“Price Crosses Upper Outer Band” — potential overextension or breakout risk.

“Price Crosses Lower Outer Band” — potential capitulation or breakdown risk.

Notes

The fit and quantiles are computed on a fixed rolling window and do not repaint; bands update as the window moves forward.

Quantiles are based on the recent distribution; if conditions change abruptly, expect band widths and skew to adapt over the next few bars.

Parameter choices directly shape behaviour: longer windows favour stability, tighter inner quantiles increase touch frequency, and extreme outer quantiles highlight only the rarest moves.

Final thought

Quantile bands answer a simple question: “How unusual is this move given the current trend and the way price has been missing it lately?” By scoring that question with real, distribution-aware limits rather than one-size-fits-all volatility you get cleaner pullback zones in trends, more honest “extreme” tags in ranges, and a framework for risk that matches the market’s recent personality.

Deadband Hysteresis Supertrend [BackQuant]Deadband Hysteresis Supertrend

A two-stage trend tool that first filters price with a deadband baseline, then runs a Supertrend around that baseline with optional flip hysteresis and ATR-based adverse exits.

What this is

A hybrid of two ideas:

Deadband Hysteresis Baseline that only advances when price pulls far enough from the baseline to matter. This suppresses micro noise and gives you a stable centerline.

Supertrend bands wrapped around that baseline instead of raw price. Flips are further gated by an extra margin so side changes are more deliberate.

The goal is fewer whipsaws in chop and clearer regime identification during trends.

How it works (high level)

Deadband step — compute a per-bar “deadband” size from one of four modes: ATR, Percent of price, Ticks, or Points. If price deviates from the baseline by more than this amount, move the baseline forward by a fraction of the excess. If not, hold the line.

Centered Supertrend — build upper and lower bands around the baseline using ATR and a user factor. Track the usual trailing logic that tightens a band while price moves in its favor.

Flip hysteresis — require price to exceed the active band by an extra flip offset × ATR before switching sides. This adds stickiness at the boundary.

Adverse exit — once a side is taken, trigger an exit if price moves against the entry by K × ATR .

If you would like to check out the filter by itself:

What it plots

DBHF baseline (optional) as a smooth centerline.

DBHF Supertrend as the active trailing band.

Candle coloring by trend side for quick read.

Signal markers 𝕃 and 𝕊 at flips plus ✖ on adverse exits.

Inputs that matter

Price Source — series being filtered. Close is typical. HL2 or HLC3 can be steadier.

Deadband mode — ATR, Percent, Ticks, or Points. This defines the “it’s big enough to matter” zone.

ATR Length / Mult (DBHF) — only used when mode = ATR. Larger values widen the do-nothing zone.

Percent / Ticks / Points — alternatives to ATR; pick what fits your market’s convention.

Enter Mult — scales the deadband you must clear before the baseline moves. Increase to filter more noise.

Response — fraction of the excess applied to baseline movement. Higher responds faster; lower is smoother.

Supertrend ATR Period & Factor — traditional band size controls; higher factor widens and flips less often.

Flip Offset ATR — extra ATR buffer required to flip. Useful in choppy regimes.

Adverse Stop K·ATR — per-trade danger brake that forces an exit if price moves K×ATR against entry.

UI — toggle baseline, supertrend, signals, and bar painting; choose long and short colors.

How to read it

Green regime — candles painted long and the Supertrend running below price. Pullbacks toward the baseline that fail to breach the opposite band often resume higher.

Red regime — candles painted short and the Supertrend running above price. Rallies that cannot reclaim the band may roll over.

Frequent side swaps — reduce sensitivity by increasing Enter Mult, using ATR mode, raising the Supertrend factor, or adding Flip Offset ATR.

Use cases

Bias filter — allow entries only in the direction of the current side. Use your preferred triggers inside that bias.

Trailing logic — treat the active band as a dynamic stop. If the side flips or an adverse K·ATR exit prints, reduce or close exposure.

Regime map — on higher timeframes, the combination baseline + band produces a clean up vs down template for allocation decisions.

Tuning guidance

Fast markets — ATR deadband, modest Enter Mult (0.8–1.2), response 0.2–0.35, Supertrend factor 1.7–2.2, small Flip Offset (0.2–0.5 ATR).

Choppy ranges — widen deadband or raise Enter Mult, lower response, and add more Flip Offset so flips require stronger evidence.

Slow trends — longer ATR periods and higher Supertrend factor to keep you on side longer; use a conservative adverse K.

Included alerts

DBHF ST Long — side flips to long.

DBHF ST Short — side flips to short.

Adverse Exit Long / Short — K·ATR stop triggers against the current side.

Strengths

Deadbanded baseline reduces micro whipsaws before Supertrend logic even begins.

Flip hysteresis adds a second layer of confirmation at the boundary.

Optional adverse ATR stop provides a uniform risk cut across assets and regimes.

Clear visuals and minimal parameters to adjust for symbol behavior.

Putting it together

Think of this tool as two decisions layered into one view. The deadband baseline answers “does this move even count,” then the Supertrend wrapped around that baseline answers “if it counts, which side should I be on and where do I flip.” When both parts agree you tend to stay on the correct side of a trend for longer, and when they disagree you get an early warning that conditions are changing.

When the baseline bends and price cannot reclaim the opposite band , momentum is usually continuing. Pullbacks into the baseline that stall before the far band often resolve in trend.

When the baseline flattens and the bands compress , expect indecision. Use the Flip Offset ATR to avoid reacting to the first feint. Wait for a clean band breach with follow through.

When an adverse K·ATR exit prints while the side has not flipped , treat it as a risk event rather than a full regime change. Many users cut size, re-enter only if the side reasserts, and let the next flip confirm a new trend.

Final thoughts

Deadband Hysteresis Supertrend is best read as a regime lens. The baseline defines your tolerance for noise, the bands define your trailing structure, and the flip offset plus adverse ATR stop define how forgiving or strict you want to be at the boundary. On strong trends it helps you hold through shallow shakeouts. In choppy conditions it encourages patience until price does something meaningful. Start with settings that reflect the cadence of your market, observe how often flips occur, then nudge the deadband and flip offset until the tool spends most of its time describing the move you care about rather than the noise in between.

Theil-Sen Line Filter [BackQuant]Theil-Sen Line Filter

A robust, median-slope baseline that tracks price while resisting outliers. Designed for the chart pane as a clean, adaptive reference line with optional candle coloring and slope-flip alerts.

What this is

A trend filter that estimates the underlying slope of price using a Theil-Sen style median of past slopes, then advances a baseline by a controlled fraction of that slope each bar. The result is a smooth line that reacts to real directional change while staying calm through noise, gaps, and single-bar shocks.

Why Theil-Sen

Classical moving averages are sensitive to outliers and shape changes. Ordinary least squares is sensitive to large residuals. The Theil-Sen idea replaces a single fragile estimate with the median of many simple slopes, which is statistically robust and less influenced by a few extreme bars. That makes the baseline steadier in choppy conditions and cleaner around regime turns.

What it plots

Filtered baseline that advances by a fraction of the robust slope each bar.

Optional candle coloring by baseline slope sign for quick trend read.

Alerts when the baseline slope turns up or down.

How it behaves (high level)

Looks back over a fixed window and forms many “current vs past” bar-to-bar slopes.

Takes the median of those slopes to get a robust estimate for the bar.

Optionally caps the magnitude of that per-bar slope so a single volatile bar cannot yank the line.

Moves the baseline forward by a user-controlled fraction of the estimated slope. Lower fractions are smoother. Higher fractions are more responsive.

Inputs and what they do

Price Source — the series the filter tracks. Typical is close; HL2 or HLC3 can be smoother.

Window Length — how many bars to consider for slopes. Larger windows are steadier and slower. Smaller windows are quicker and noisier.

Response — fraction of the estimated slope applied each bar. 1.00 follows the robust slope closely; values below 1.00 dampen moves.

Slope Cap Mode — optional guardrail on each bar’s slope:

None — no cap.

ATR — cap scales with recent true range.

Percent — cap scales with price level.

Points — fixed absolute cap in price points.

ATR Length / Mult, Cap Percent, Cap Points — tune the chosen cap mode’s size.

UI Settings — show or hide the line, paint candles by slope, choose long and short colors.

How to read it

Up-slope baseline and green candles indicate a rising robust trend. Pullbacks that do not flip the slope often resolve in trend direction.

Down-slope baseline and red candles indicate a falling robust trend. Bounces against the slope are lower-probability until proven otherwise.

Flat or frequent flips suggest a range. Increase window length or decrease response if you want fewer whipsaws in sideways markets.

Use cases

Bias filter — only take longs when slope is up, shorts when slope is down. It is a simple way to gate faster setups.

Stop or trail reference — use the line as a trailing guide. If price closes beyond the line and the slope flips, consider reducing exposure.

Regime detector — widen the window on higher timeframes to define major up vs down regimes for asset rotation or risk toggles.

Noise control — enable a cap mode in very volatile symbols to retain the line’s continuity through event bars.

Tuning guidance

Quick swing trading — shorter window, higher response, optionally add a percent cap to keep it stable on large moves.

Position trading — longer window, moderate response. ATR cap tends to scale well across cycles.

Low-liquidity or gappy charts — prefer longer window and a points or ATR cap. That reduces jumpiness around discontinuities.

Alerts included

Theil-Sen Up Slope — baseline’s one-bar change crosses above zero.

Theil-Sen Down Slope — baseline’s one-bar change crosses below zero.

Strengths

Robust to outliers through median-based slope estimation.

Continuously advances with price rather than re-anchoring, which reduces lag at turns.

User-selectable slope caps to tame shock bars without over-smoothing everything.

Minimal visuals with optional candle painting for fast regime recognition.

Notes

This is a filter, not a trading system. It does not account for execution, spreads, or gaps. Pair it with entry logic, risk management, and higher-timeframe context if you plan to use it for decisions.

Long-Term Trend & Valuation Model [Backquant]Long-Term Trend & Valuation Model

Invite-only. A universal long-term valuation strategy and trend model built to work across markets, with an emphasis on crypto where cycles and volatility are large. Intended primarily for the 1D timeframe. Inputs should be adjusted per asset to reflect its structure and volatility.

If you would like to checkout the simplified and open source valuation, check out:

What this is

A two-layer framework that answers two different questions.

• The Valuation Engine asks “how extended is price relative to its own long-term regime” and outputs a centered oscillator that moves positive in supportive conditions and negative in deteriorating conditions.

• The Trend Model asks “is the market actually trending in a sustained direction” and converts several independent subsystems into a single composite score.

The combination lets you separate “where we are in the cycle” from “what to do about it” so allocation and timing can be handled with fewer conflicts.

Design philosophy

Crypto and many risk assets move in multi-month expansions and contractions. Short tools flip often and can be misleading near regime boundaries. This model favors slower, high-confidence information, then summarizes it in simple visuals and alerts. It is not trying to catch every swing. It is built to help you participate in the meat of long uptrends, de-risk during deteriorations, and identify stretched conditions that deserve caution or patience.

Valuation Engine, high level

The Valuation Engine blends several slow signals into one measure. Exact transforms, windows, and weights are private, but the categories below describe the intent. Each input is standardized so unlike units can be combined without one dominating.

Momentum quality — favors persistent, orderly advances over erratic spikes. Helps distinguish trend continuation from noise.

Mean-reversion pressure — detects when price is far from a long anchor or when oscillators are pulling back toward equilibrium.

Risk-adjusted return — long-window reward to variability. Encourages time in market when advances are efficient rather than merely fast.

Volume imbalance — summarizes whether activity is expanding with advances or with declines, using a slow envelope to avoid day-to-day churn.

Trend distance — expresses how stretched price is from a structural baseline rather than from a short moving average.

Price normalization — a long z-score of price to keep extremes comparable across cycles and symbols.

How the Valuation Engine is shaped

Standardization — components are put on comparable scales over long windows.

Composite blend — standardized parts are combined into one reading with protective weighting. No single family can override the rest on its own.

Smoothing — optional moving average smoothing to reduce whipsaw around zero or around the bands.

Bounded scaling — the composite is compressed into a stable, interpretable range so the mid zone and extremes are visually consistent. This reduces the effect of outliers without hiding genuine stress.

Volatility-aware re-expansion — after compression, the series is allowed to swing wider in high-volatility regimes so “overbought” and “oversold” remain meaningful when conditions change.

Thresholds — fixed OB/OS levels or dynamic bands that float with recent dispersion. Dynamic bands use k times a rolling standard deviation. Fixed bands are simple and comparable across charts.

How to read the Valuation Oscillator

Above zero suggests a supportive backdrop. Rising and positive often aligns with uptrends that are gaining participation.

Below zero suggests deterioration or risk aversion. Falling and negative often aligns with distribution or with trend exhaustion.

Touches of the upper band show stretch on the optimistic side. Repeated tags without breakdown often occur late in cycles, especially in crypto.

Touches of the lower band show stretch on the pessimistic side. They are common in washouts and early bases.

Visual elements

Valuation Oscillator — colored by sign for instant context.

OB/OS guides — fixed or dynamic bands.

Background and bar colors — optional, tied to the sign of valuation for quick scans.

Summary table — optional, shows the standardized contribution of the major categories and the final composite score with a simple status icon.

Trend Model, composite scoring

The trend side aggregates several independent subsystems. Each subsystem issues a vote: long, short, or neutral. Votes are averaged into a composite score. The exact logic of each subsystem is intentionally abstracted. The families below describe roles, not formulas.

Long-horizon price state — checks where price sits relative to multiple structural baselines and whether those baselines are aligned.

Macro regime checks — favors sustained risk-on behavior and penalizes persistent deterioration in breadth or volatility structure.

Ultimate confirmation — a conservative filter that only votes when directional evidence is persistent.

Minimalist sanity checks — keep the model responsive to obvious extremes and prevent “stuck neutral” states.

Higher timeframe or overlay inputs — optional votes that consider slower contexts or relative strength to stabilize borderline periods.

You define two cutoffs for the composite: above the long threshold the state is Long , below the short threshold the state is Short , in between is Cash/Neutral . The script paints a signal line on price for an at-a-glance view and provides alerts when the composite crosses your thresholds.

How it can be used

Cycle framing in crypto — use deep negative valuation as accumulation context, then look for the composite trend to move through your long threshold. Late in cycles, extended positive valuation with weakening composite votes is a caution cue for de-risking or tighter management.

Regime-based allocation — increase risk or loosen take-profits when the composite is firmly Long and valuation is rising. Decrease risk or rotate to stable holdings when the composite is Short and valuation is falling.

Signal gating — run shorter-term entry systems only in the direction of the composite. This reduces counter-trend trades and improves holding discipline during strong uptrends.

Sizing overlay — scale position sizes by the magnitude of the valuation reading. Smaller sizes near the upper band during aging advances, larger sizes near zero after strong resets.

DCA context — for long-only accumulation, schedule heavier adds when valuation is negative and stabilizing, then lighten or pause adds when valuation is very positive and flattening.

Cross-asset rotation — compare symbols on 1D with the same fixed bands. Favor assets with positive valuation that are also in a Long composite state.

Interpreting common patterns

Early build-out — valuation rises from below zero, but the composite is still neutral. This is often the base-building phase. Patience and staged entries can make sense.

Healthy advance — valuation positive and trending up, composite firmly Long. Pullbacks that keep valuation above zero are usually opportunities rather than trend breaks.

Late-cycle stretch — valuation pinned near the upper band while the composite starts to weaken toward neutral. Consider trimming, tightening risk, or shifting to a “let the market prove it” stance.

Distribution and unwind — valuation negative and falling, composite Short. Rallies are treated as counter-trend until both turn.

Settings that matter

Timeframe

This model is intended for 1D as the primary view. It can be inspected on higher or lower frames, but the design choices assume daily bars for crypto and other risk assets.

Asset-specific tuning

Inputs should be adjusted per asset. Coins with high variability benefit from longer lookbacks and slightly wider dynamic bands. Lower-volatility instruments can use shorter windows and tighter bands.

Valuation side

Lookback lengths — longer values make the oscillator steadier and more cycle-aware. Shorter values increase sensitivity but create more mid-zone noise.

Smoothing — enable to reduce flicker around zero and around the bands. Disable if you want faster warnings of regime change.

Dynamic vs fixed thresholds — dynamic bands float with recent dispersion and keep OB/OS comparable across regimes. Fixed bands are simple and make inter-asset comparison easy.

Scaling and re-expansion — keep this enabled if you want extremes to remain interpretable when volatility rises.

Trend side

Composite thresholds — widen the neutral zone if you want fewer flips. Tighten thresholds if you want earlier signals at the cost of more transitions.

Visibility — use the price-pane signal line and bar coloring to keep the regime in view while you focus on structure.

Alerts

Valuation OB/OS enter and exit — the oscillator entering or leaving stretched zones.

Zero-line crosses — valuation turning positive or negative.

Trend flips — composite crossing your long or short threshold.

Strengths

Separates “valuation context” from “trend state,” which improves decisions about when to add, reduce, or stand aside.

Composite voting reduces reliance on any single indicator family and improves robustness across regimes.

Volatility-aware scaling keeps signals interpretable during quiet and wild markets.

Clear, configurable visuals and alerts that support long-horizon discipline rather than frequent toggling.

Final thoughts

This is a universal long-term valuation strategy and trend model that aims to keep you aligned with the dominant regime while giving transparent context for stretch and risk. For crypto on 1D, it helps map accumulation, expansion, distribution, and unwind phases with a single, consistent language. Tune lookbacks, smoothing, and thresholds to the asset you trade, let the valuation side tell you where you are in the cycle, and let the composite trend side tell you what stance to hold until the market meaningfully changes.

Deadband Hysteresis Filter [BackQuant]Deadband Hysteresis Filter

What this is

This tool builds a “debounced” price baseline that ignores small fluctuations and only reacts when price meaningfully departs from its recent path. It uses a deadband to define how much deviation matters and a hysteresis scheme to avoid rapid flip-flops around the decision boundary. The baseline’s slope provides a simple trend cue, used to color candles and to trigger up and down alerts.

Why deadband and hysteresis help

They filter micro noise so the baseline does not react to every tiny tick.

They stabilize state changes. Hysteresis means the rule to start moving is stricter than the rule to keep holding, which reduces whipsaw.

They produce a stepped, readable path that advances during sustained moves and stays flat during chop.

How it works (conceptual)

At each bar the script maintains a running baseline dbhf and compares it to the input price p .

Compute a base threshold baseTau using the selected mode (ATR, Percent, Ticks, or Points).

Build an enter band tauEnter = baseTau × Enter Mult and an exit band tauExit = baseTau × Exit Mult where typically Exit Mult < Enter Mult .

Let diff = p − dbhf .

If diff > +tauEnter , raise the baseline by response × (diff − tauEnter) .

If diff < −tauEnter , lower the baseline by response × (diff + tauEnter) .

Otherwise, hold the prior value.

Trend state is derived from slope: dbhf > dbhf → up trend, dbhf < dbhf → down trend.

Inputs and what they control

Threshold mode

ATR — baseTau = ATR(atrLen) × atrMult . Adapts to volatility. Useful when regimes change.

Percent — baseTau = |price| × pctThresh% . Scale-free across symbols of different prices.

Ticks — baseTau = syminfo.mintick × tickThresh . Good for futures where tick size matters.

Points — baseTau = ptsThresh . Fixed distance in price units.

Band multipliers and response

Enter Mult — outer band. Price must travel at least this far from the baseline before an update occurs. Larger values reject more noise but increase lag.

Exit Mult — inner band for hysteresis. Keep this smaller than Enter Mult to create a hold zone that resists small re-entries.

Response — step size when outside the enter band. Higher response tracks faster; lower response is smoother.

UI settings

Show Filtered Price — plots the baseline on price.

Paint candles — colors bars by the filtered slope using your long/short colors.

How it can be used

Trend qualifier — take entries only in the direction of the baseline slope and skip trades against it.

Debounced crossovers — use the baseline as a stabilized surrogate for price in moving-average or channel crossover rules.

Trailing logic — trail stops a small distance beyond the baseline so small pullbacks do not eject the trade.

Session aware filtering — widen Enter Mult or switch to ATR mode for volatile sessions; tighten in quiet sessions.

Parameter interactions and tuning

Enter Mult vs Response — both govern sensitivity. If you see too many flips, increase Enter Mult or reduce Response. If turns feel late, do the opposite.

Exit Mult — widening the gap between Enter and Exit expands the hold zone and reduces oscillation around the threshold.

Mode choice — ATR adapts automatically; Percent keeps behavior consistent across instruments; Ticks or Points are useful when you think in fixed increments.

Timeframe coupling — on higher timeframes you can often lower Enter Mult or raise Response because raw noise is already reduced.

Concrete starter recipes

General purpose — ATR mode, atrLen=14 , atrMult=1.0–1.5 , Enter=1.0 , Exit=0.5 , Response=0.20 . Balanced noise rejection and lag.

Choppy range filter — ATR mode, increase atrMult to 2.0, keep Response≈0.15 . Stronger suppression of micro-moves.

Fast intraday — Percent mode, pctThresh=0.1–0.3 , Enter=1.0 , Exit=0.4–0.6 , Response=0.30–0.40 . Quicker turns for scalping.

Futures ticks — Ticks mode, set tickThresh to a few spreads beyond typical noise; start with Enter=1.0 , Exit=0.5 , Response=0.25 .

Strengths

Clear, explainable logic with an explicit noise budget.

Multiple threshold modes so the same tool fits equities, futures, and crypto.

Built-in hysteresis that reduces flip-flop near the boundary.

Slope-based coloring and alerts that make state changes obvious in real time.

Limitations and notes

All filters add lag. Larger thresholds and smaller response trade faster reaction for fewer false turns.

Fixed Points or Ticks can under- or over-filter when volatility regime shifts. ATR adapts, but will also expand bands during spikes.

On extremely choppy symbols, even a well tuned band will step frequently. Widen Enter Mult or reduce Response if needed.

This is a chart study. It does not include commissions, slippage, funding, or gap risks.

Alerts

DBHF Up Slope — baseline turns from down to up on the latest bar.

DBHF Down Slope — baseline turns from up to down on the latest bar.

Implementation details worth knowing

Initialization sets the baseline to the first observed price to avoid a cold-start jump.

Slope is evaluated bar-to-bar. The up and down alerts check for a change of slope rather than raw price crossings.

Candle colors and the baseline plot share the same long/short palette with transparency applied to the line.

Practical workflow

Pick a mode that matches how you think about distance. ATR for volatility aware, Percent for scale-free, Ticks or Points for fixed increments.

Tune Enter Mult until the number of flips feels appropriate for your timeframe.

Set Exit Mult clearly below Enter Mult to create a real hold zone.

Adjust Response last to control “how fast” the baseline chases price once it decides to move.

Final thoughts

Deadband plus hysteresis gives you a principled way to “only care when it matters.” With a sensible threshold and response, the filter yields a stable, low-chop trend cue you can use directly for bias or plug into your own entries, exits, and risk rules.

Martingale Strategy Simulator [BackQuant]Martingale Strategy Simulator

Purpose