Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

Drawdown

3 Red / 3 Green Strategy with Volatility CheckStrategy Name: 3 Red / 3 Green Strategy with Volatility Check by AlgoTradeKit

Overview

This long-only strategy is designed for daily bars on NASDAQ (or similar instruments) and combines simple price action with a volatility filter. It “tells it like it is” – enter when the market shows weakness, but only in sufficiently volatile conditions, and exit either on signs of a reversal or after a set number of days.

Entry Conditions

- Price Action :

Enter a long position when there are 3 consecutive red days (each day's close is below its open).

- Volatility Filter :

The entry is allowed only if the current ATR (Average True Range) calculated over the specified ATR Period (default 12) is greater than its 30-day simple moving average. This ensures the market has enough volatility to justify the trade.

Exit Conditions

- Reversal Signal :

Exit the long position when 3 consecutive green days occur (each day's close is above its open), signaling a potential reversal.

- Time Limit :

Regardless of market conditions, any open trade is closed if it reaches the Maximum Trade Duration (default 22 days). This helps limit exposure during stagnant or unfavorable market conditions.

- You can toggle the three-green-day exit if you want to isolate the time-based exit.

Input Parameters

- Maximum Trade Duration (days): Default is 22 days.

- ATR Period: Default is 12.

- Use 3 Green Days Exit: Toggle to enable or disable the three-green-day exit condition.

How It Works

1. Entry: The strategy monitors daily price action for 3 consecutive down days. When this occurs and if the market is volatile enough (current ATR > 30-day ATR average), it opens a long position.

2. Exit: The position is closed if the price action reverses with 3 consecutive up days or if the trade has been open for the maximum allowed duration - i.e. use it on daily chart.

Risk Management

- The built-in maximum trade duration prevents trades from lingering too long in a non-trending or consolidating market.

- The volatility filter helps ensure that trades are only taken when there is sufficient price movement, potentially increasing the odds of a meaningful move.

Disclaimer

This strategy is provided “as is” without any warranties. It is essential to backtest and validate the performance on your specific instrument and market conditions before deploying live capital. Trading involves significant risk, and you should adjust parameters to match your risk tolerance.

Test and tweak this strategy to see if it fits your trading style and market conditions. Happy trading!

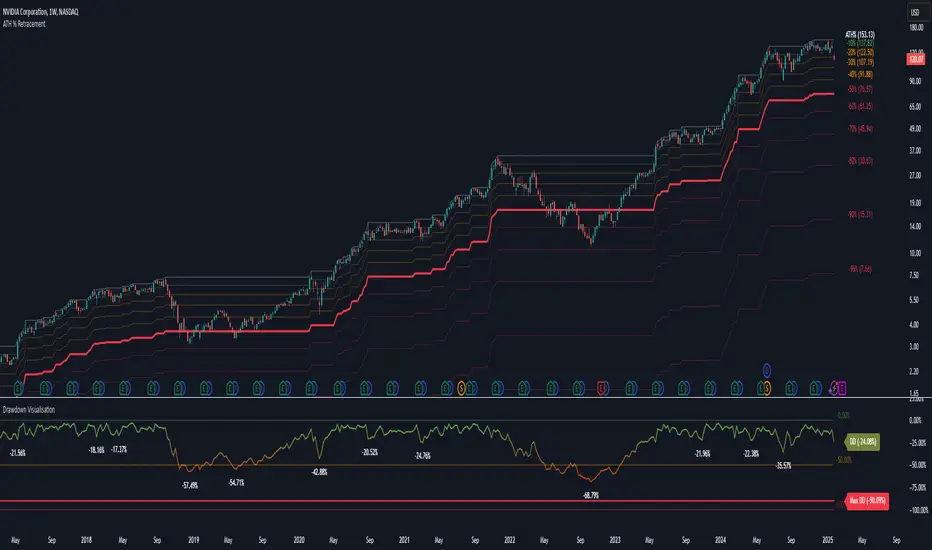

Drawdown Visualisation█ OVERVIEW

The Drawdown Visualisation indicator calculates and displays the instrument’s drawdown (in percent) relative to its all‐time high (ATH) from a user‐defined start date. It provides customisable options for label appearance, threshold lines (0%, –50%, –100%), and can plot historic drawdown levels via pivot detection.

█ USAGE

This indicator should be used with the Percentage Retracement from ATH indicator.

█ KEY FEATURES

Custom Date Settings — Use a custom start date so that only specified price action is considered.

Retracement Level Calculation — Determines ATH and computes multiple retracement levels using percentages from 0% to –100%.

Visual Signals and Customisation — Plots configurable horizontal lines and labels that display retracement percentages and prices.

Time Filtering — Bases calculations on data from the desired time period.

Historic Drawdowns — Display historical drawdowns

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

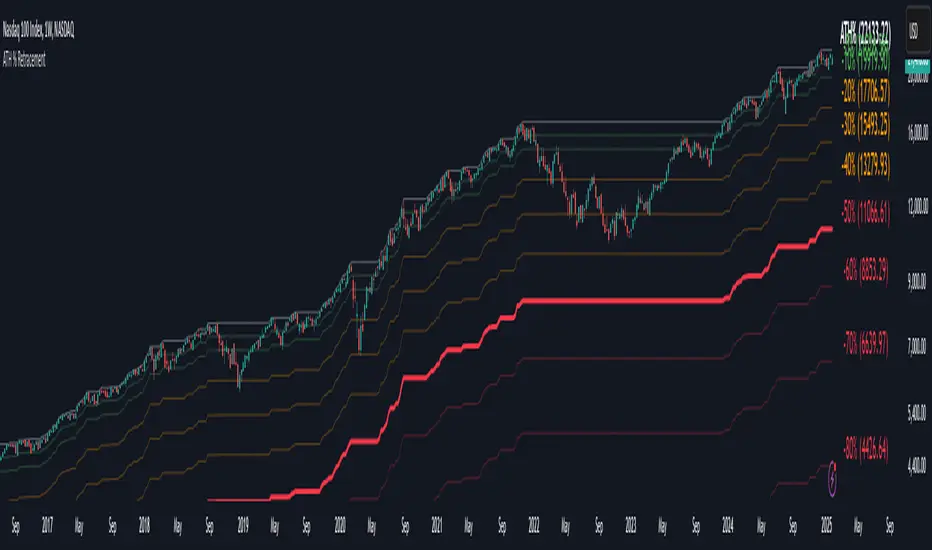

Percentage Retracement from ATH█ OVERVIEW

The Percentage Retracement from ATH indicator is a dynamic trading utility designed to help traders gauge market pullbacks from the peak price. By calculating key retracement levels based on the All-Time High (ATH) and user‑defined percentage inputs, it offers clear visual cues to assist in identifying potential support and resistance zones.

█ KEY FEATURES

Custom Date — Use a custom start date so the indicator only considers specified price action.

Retracement Calculation — Determines ATH and calculates levels based on user‑defined percentages (0% to –100%).

Visual Customisation — Plots configurable horizontal lines and labels showing retracement percentages and prices.

Time Filtering — Uses time filtering to base levels on the desired data period.

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

Bearish Wick Reversal█ STRATEGY OVERVIEW

The "Bearish Wick Reversal Strategy" identifies potential bullish reversals following significant bearish price rejection (long lower wicks). This counter-trend approach enters long positions when bearish candles show exaggerated downside wicks relative to closing prices, then exits on bullish confirmation signals. Includes optional EMA trend filtering for improved reliability.

█ What is a Bearish Wick?

A price rejection pattern where:

Bearish candle (close < open) forms with extended lower wick

Wick represents failed selloff: Low drops significantly below close

Measured as: (Low - Close)/Close × 100 (Negative percentage indicates downward extension)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Bearish candle forms with close < open

Lower wick exceeds user-defined threshold (Default: -1% of close price)

The signal occurs within the specified time window

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average)

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: Volatile instruments with frequent price rejections

Key Risk: False signals in sustained bearish trends

Optimization Tip: Test various thresholds

Filter Impact: EMA reduces trades but improves win rate and reduces drawdown

Monthly Drawdowns and Moves UP This script allows users to analyze the performance of a specific month across multiple years, focusing on maximum drawdowns and maximum upward moves within the selected month. The script offers the following features:

Dynamic Month Selection : Choose any month to analyze using an intuitive dropdown menu.

Maximum Drawdown and Upward Move Calculations :

Calculate the largest percentage drop (drawdown) and rise (move up) for the selected month each year.

Visual Highlights :

The selected month is visually highlighted on the chart with a semi-transparent overlay.

Dynamic Labels:

Labels display the maximum drawdown and upward move directly on the chart for better visualization.

Comprehensive Table Summary:

A table provides a year-by-year summary of the maximum drawdowns and upward moves for the selected month, making it easy to spot trends over time.

Customizable Display Options:

Toggle the visibility of drawdown labels, move-up labels, and the summary table for a clutter-free experience.

This tool is perfect for traders and analysts looking to identify seasonal patterns, assess risk and opportunity, and gain deeper insights into monthly performance metrics across years. Customize, explore, and make informed decisions with this powerful Pine Script indicator.

Risk Radar ProThe "Risk Radar Pro" indicator is a sophisticated tool designed to help investors and traders assess the risk and performance of their investments over a specified period. This presentation will explain each component of the indicator, how to interpret the results, and the advantages compared to traditional metrics.

The "Risk Radar Pro" indicator includes several key metrics:

● Beta

● Maximum Drawdown

● Compound Annual Growth Rate (CAGR)

● Annualized Volatility

● Dynamic Sharpe Ratio

● Dynamic Sortino Ratio

Each of these metrics is dynamically calculated using data from the entire selected period, providing a more adaptive and accurate measure of performance and risk.

1. Start Date

● Description: The date from which the calculations begin.

● Interpretation: This allows the user to set a specific period for analysis, ensuring that all metrics reflect the performance from this point onward.

2. Beta

● Description: Beta measures the volatility or systematic risk of the instrument relative to a reference index (e.g., SPY).

● Interpretation: A beta of 1 indicates that the instrument moves with the market. A beta greater than 1 indicates more volatility than the market, while a beta less than 1 indicates less volatility.

● Advantages: Unlike classic beta, which typically uses fixed historical intervals, this dynamic beta adjusts to market changes over the entire selected period, providing a more responsive measure.

3. Maximum Drawdown

● Description: The maximum observed loss from a peak to a trough before a new peak is achieved.

● Interpretation: This shows the largest single drop in value during the specified period. It is a critical measure of downside risk.

● Advantages: By tracking the maximum drawdown dynamically, the indicator can provide timely alerts when significant losses occur, allowing for better risk management.

4. Annualized Performance

● Description: The mean annual growth rate of the investment over the specified period.

● Interpretation: The Annualized Performance represents the smoothed annual rate at which the investment would have grown if it had grown at a steady rate.

● Advantages: This dynamic calculation reflects the actual long-term growth trend of the investment rather than relying on a fixed time frame.

5. Annualized Volatility

● Description: Measures the degree of variation in the instrument's returns over time, expressed as a percentage.

● Interpretation: Higher volatility indicates greater risk, as the investment's returns fluctuate more.

● Advantages: Annualized volatility calculated over the entire selected period provides a more accurate measure of risk, as it includes all market conditions encountered during that time.

6. Dynamic Sharpe Ratio

● Description: Measures the risk-adjusted return of an investment relative to its volatility.

● Choice of Risk-Free Rate Ticker: Users can select a ticker symbol to represent the risk-free rate in Sharpe ratio calculations. The default option is US03M, representing the 3-month US Treasury bill.

● Interpretation: A higher Sharpe ratio indicates better risk-adjusted returns. This ratio accounts for the risk-free rate to provide a comparison with risk-free investments.

● Advantages: By using returns and volatility over the entire period, the dynamic Sharpe ratio adjusts to changes in market conditions, offering a more accurate measure than traditional static calculations.

7. Dynamic Sortino Ratio

● Description: Similar to the Sharpe ratio, but focuses only on downside risk.

Interpretation: A higher Sortino ratio indicates better risk-adjusted returns, focusing solely on negative returns, which are more relevant to risk-averse investors.

● Choice of Risk-Free Rate Ticker: Similarly, users can choose a ticker symbol for the risk-free rate in Sortino ratio calculations. By default, this is also set to US03M.

● Advantages: This ratio's dynamic calculation considering the downside deviation over the entire period provides a more accurate measure of risk-adjusted returns in volatile markets.

Comparison with Basic Metrics

● Static vs. Dynamic Calculations: Traditional metrics often use fixed historical intervals, which may not reflect current market conditions. The dynamic calculations in "Risk Radar Pro" adjust to market changes, providing more relevant and timely information.

● Comprehensive Risk Assessment: By including metrics like maximum drawdown, Sharpe ratio, and Sortino ratio, the indicator provides a holistic view of both upside potential and downside risk.

● User Customization: Users can customize the start date, reference index, risk-free rate, and table position, tailoring the indicator to their specific needs and preferences.

Conclusion

The "Risk Radar Pro" indicator is a powerful tool for investors and traders looking to assess and manage risk more effectively. By providing dynamic, comprehensive metrics, it offers a significant advantage over traditional static calculations, ensuring that users have the most accurate and relevant information to make informed decisions.

The "Risk Radar Pro" indicator provides analytical tools and metrics for informational purposes only. It is not intended as financial advice. Users should conduct their own research and consider their individual risk tolerance and investment objectives before making any investment decisions based on the indicator's outputs. Trading and investing involve risks, including the risk of loss. Past performance is not indicative of future results.

Drawdown % (with SMA)This script, titled "Drawdown % (with SMA)" and designed for Pine Script version 5

offers a sophisticated tool for traders to monitor drawdown percentages, a crucial metric in assessing investment risks. The script calculates the drawdown as the percentage decrease from the all-time high value of the selected financial instrument.

Blockunity Drawdown Visualizer (BDV)Monitor the drawdown (value of the drop between the highest and lowest points) of assets and act accordingly to reduce your risk.

Introducing BDV, the incredibly intuitive metric that visualizes asset drawdowns in the most visually appealing manner. With its color gradient display, BDV allows you to instantly grasp the state of retracement from the asset’s highest price level. But that’s not all – you have the option to display the oscillator’s colorization directly on your chart, enhancing your analysis even further.

The Idea

The goal is to provide the community with the best and most complete tool for visualizing the Drawdown of any asset.

How to Use

Very simple to use, the indicator takes the form of an oscillator, with colors ranging from red to green depending on the Drawdown level. A table summarizes several key data points.

Elements

On the oscillator, you'll find a line with a color gradient showing the asset's Drawdown. The flatter line represents the Max Drawdown (the lowest value reached).

In addition, the table summarizes several data:

The asset's All Time High (ATH).

Current Drawdown.

The Max Drawdown that has been reached.

Settings

First of all, you can activate a "Bar Color" in the settings (You must also uncheck "Borders" and "Wick" in your Chart Settings):

You can display Fibonacci levels on the oscillator. You'll see that levels can be relevant to drawdown. The color of the levels is also configurable.

In the calculation parameters, you can first choose between taking the High of the candles or the Close. By default this is Close, but if you change the parameter to High, the indication next to ATH in the table will change, and you'll see that the values in the table will be affected.

The second calculation parameter (Start Date) lets you modify the effective start date of the ATH, which will affect the drawdown level. Here's an example:

How it Works

First, we calculate the ATH:

var bdv_top = bdv_source

bdv_top := na(bdv_top ) ? bdv_source : math.max(bdv_source, bdv_top )

Then the drawdown is calculated as follows:

bdv = ((bdv_source / bdv_top) * 100) - 100

Then the max drawdown :

bdv_max = bdv

bdv_max := na(bdv_max ) ? bdv : math.min(bdv, bdv_max )

ATH Drawdown Indicator by Atilla YurtsevenThe ATH (All-Time High) Drawdown Indicator, developed by Atilla Yurtseven, is an essential tool for traders and investors who seek to understand the current price position in relation to historical peaks. This indicator is especially useful in volatile markets like cryptocurrencies and stocks, offering insights into potential buy or sell opportunities based on historical price action.

This indicator is suitable for long-term investors. It shows the average value loss of a price. However, it's important to remember that this indicator only displays statistics based on past price movements. The price of a stock can remain cheap for many years.

1. Utility of the Indicator:

The ATH Drawdown Indicator provides a clear view of how far the current price is from its all-time high. This is particularly beneficial in assessing the magnitude of a pullback or retracement from peak levels. By understanding these levels, traders can gauge market sentiment and make informed decisions about entry and exit points.

2. Risk Management:

This indicator aids in risk management by highlighting significant drawdowns from the ATH. Traders can use this information to adjust their position sizes or set stop-loss orders more effectively. For instance, entering trades when the price is significantly below the ATH could indicate a higher potential for recovery, while a minimal drawdown from the ATH may suggest caution due to potential overvaluation.

3. Indicator Functionality:

The indicator calculates the percentage drawdown from the ATH for each trading period. It can display this data either as a line graph or overlaid on candles, based on user preference. Horizontal lines at -25%, -50%, -75%, and -100% drawdown levels offer quick visual cues for significant price levels. The color-coding of candles further aids in visualizing bullish or bearish trends in the context of ATH drawdowns.

4. ATH Level Indicator (0 Level):

A unique feature of this indicator is the 0 level, which signifies that the price is currently at its all-time high. This level is a critical reference point for understanding the market's peak performance.

5. Mean Line Indicator:

Additionally, this indicator includes a 'Mean Line', representing the average percentage drawdown from the ATH. This average is calculated over more than a thousand past bars, leveraging the law of large numbers to provide a reliable mean value. This mean line is instrumental in understanding the typical market behavior in relation to the ATH.

Disclaimer:

Please note that this ATH Drawdown Indicator by Atilla Yurtseven is provided as an open-source tool for educational purposes only. It should not be construed as investment advice. Users should conduct their own research and consult a financial advisor before making any investment decisions. The creator of this indicator bears no responsibility for any trading losses incurred using this tool.

Please remember to follow and comment!

Trade smart, stay safe

Atilla Yurtseven

Drawdown Dynamics IndicatorDescription :

The Drawdown Dynamics Indicator is a straightforward tool that offers insights into three critical aspects of an asset’s financial performance: Total Max Drawdown, Rolling Period Max Drawdown, and Current Max Drawdown. Inside of the indicator, you can select to view either the rolling period max drawdown or the all-time max drawdown. This is represented by the gray line. The blue line represents the asset's current drawdown.

Rolling Period Max Drawdown is more about a snapshot view, highlighting the maximum loss from a peak to a trough for an adjustable rolling time frame. This is a feature not available with other indicators that exist on TradingView.

Total Max Drawdown gives a broad view, showcasing the all-time deepest decline in an asset’s value.

Current Max Drawdown offers a live update, focusing on the asset's present phase and how it's performing in real-time.

Practical Uses :

The utility of this indicator becomes evident when you start exploring the risks and performance metrics of assets. A notable use of this indicator is in comparing the drawdowns of a trading strategy against the inherent drawdowns of an asset. It helps in painting a clearer picture of risk and performance of both the asset and the strategy.

Risk Understanding : By comparing the strategy drawdown to the asset drawdown, traders get to understand if the risk they’re taking aligns with the asset’s natural risk behavior.

Evaluating Strategy’s Strength : If a strategy can weather the storms of the asset's natural drawdown phases and come out relatively unscathed, it can speak to its strength.

Performance Comparison : It also acts as a benchmark tool. Traders can pit different strategies against each other, using the asset’s drawdown as a baseline, to see which one manages risks better.

Disclaimer : This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

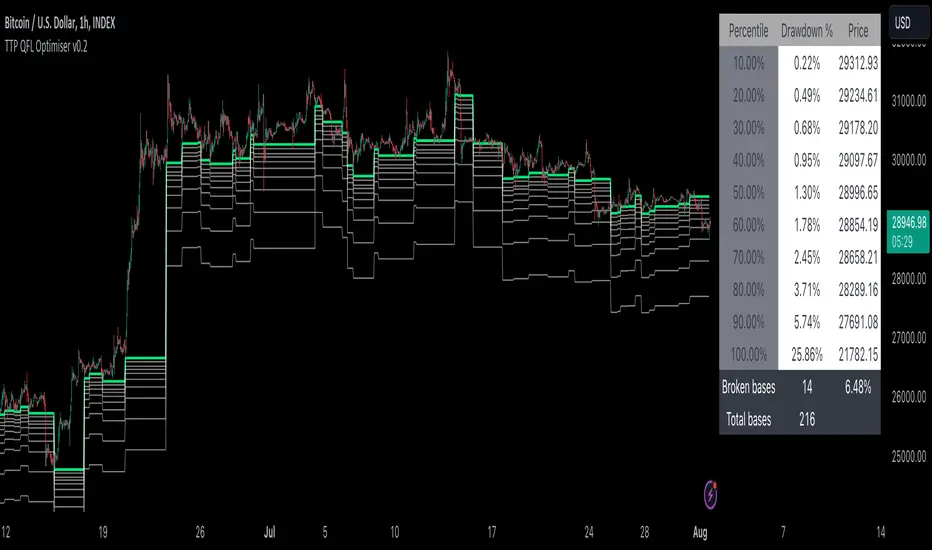

TTP QFL OptimiserThis tool is designed to help finding the best take profit and stop loss levels when trading with QFL bases (Quick Fingers Luc).

You can use it to see the average drawdown among all historic bases broken for an asset and then find the drawdowns that are more frequent using the percentile parameters provided.

For example, by knowing that 98% of the bases got broken with a drawdown of up to 5% can become extremely useful for deciding where to place your take profit or stop loss levels.

It supports QFL 1H, 2H and 4H but make sure to set the chart timeframe to a lower timeframe than QFL to obtain valid results.

Two percentiles are provided to be able to evaluate potential TP and SL at the same time.

Steps:

- Load an asset in the 15min TF

- Select the QFL version: 1H more deals / lower quality vs 4H less deals/ better quality

- Find a percentile that triggers enough deals (example: 70) and then another percentile that doesn't get hit too much (example: 98)

- Confirm the values p1 and p2 provided in the table and the white and grey lines for the results of which drawdown percentages correspond to such selection of percentiles

Once having p1 and p2 use your backtesting and forward testing tools to confirm and adjust accordingly.

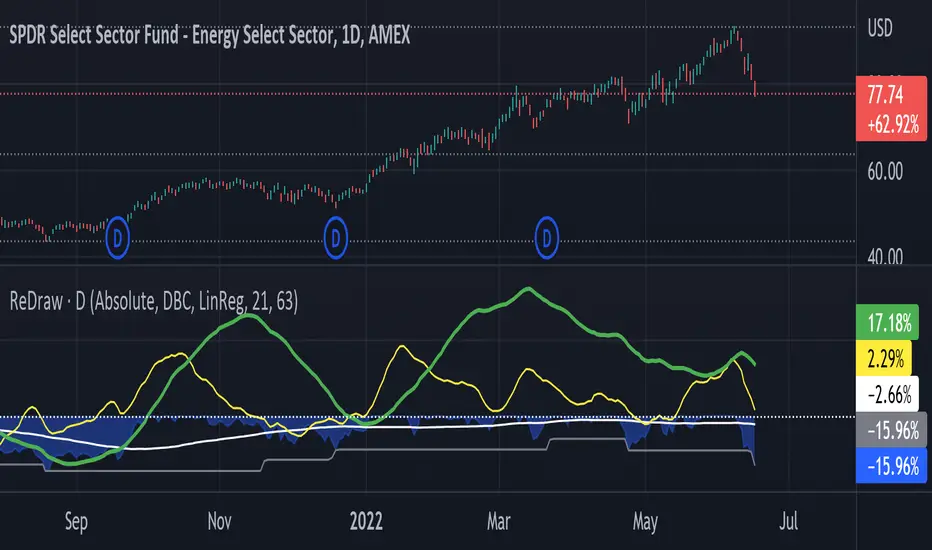

Return & Drawdown

ReDraw script calculates the historical returns and drawdown for the given periods.

By default, the return of the linear regression trends is displayed (can be turned off in settings). In this mode, two linear regression trends are being computed for both long and short periods, and the percent value indicates the "return of the trend" for the corresponding period. Observing the dynamic of the linear regression trends can give a great hint if the trend is slowing down.

When the smoothing method is set to "none" or WMA3/5, the real asset return is shown for both periods, using the formula (LastPrice-FirstPrice)/FirstPrice

The script calculates the maximum drawdown for the long period using the formula (max(Price) - LastPrice) / max(Price).

The white line under the zero is the average maximum drawdown over the long period.

When the mode is set to Compare, ReDraw will display the difference in metrics between the current and selected symbol (SPY by default).

trailing_drawdown

Description:

Drawdown was a tool to measure historical risk, derived from measuring current wealth from its previous peak, casually from portfolio construction (weights allocation), will consider to having a minimum drawdown. In this indicator, the drawdown for individual assets is utilized to measure its value or percentage from its trailing peak (default to 1-yr period).

Drawdown:

drawdown = (price/peaks)-1

Feature:

Static: display drawdown as percentage

Dynamic: display drawdown as value

Yearly Percentage ReturnsAn indicator that lets you visualize the historical Yearly Percentage returns of any symbol .

Key Features:

Displays the yearly returns from start to end of each year

Displays a table showing all yearly returns for current symbol

Displays start of each year as a vertical line

Displays up to 5 custom horizontal levels

Table Settings:

Enable table - Show/Hide the table

Size - Sets the size of the table

Position - Sets the position of the table on the screen

Direction - Sets the direction of the table to display the data (Vertically or Horizontally)

Percent Off All-time High (% Off High)Percent Off All-time High tracks the percentage difference between the previous day’s closing price and the All-Time high price of the security’s entire price history.

This metric tells you how far the price has deviated from/converged on the all-time high price.

Simple/Compounded Returns & Drawdowns TableVery excited to bring this script to the public. This is a very useful table that displays the performance of any strategy you give it in a more detailed view. It runs on all timeframes and at any position on the chart with the replay function. It also updates on tick changes. The table consists of three modes: Simple Equity, Compound Equity and Drawdown.

Simple Equity – shows the change in equity for every month and year. It is calculated by finding the difference in initial equity at the beginning of the month/year and the end of the month/year. The table will thus display strategy performance in blocks of time that are not correlated. It is an excellent way to see individual month/year performance from start to finish but it may not represent true change in equity over time. For example, let's assume that 100% of equity is used on every trade for simplicity. If a loss of 50% is made in the first month and a profit of 100% is made in the next month, the strategy will show 50% profit for the year. This aggregate value might be helpful to know for testing purposes, but in reality, the account is actually at break-even for the year (Initial Equity * 0.5 * 2 = Initial Equity).

Compound Equity – shows compounded change in equity for every month and year. It is calculated by finding the difference in starting equity when the strategy is run and equity at the end of the month/year. The table will thus display the true strategy performance – compounded equity at the end of each month/year.

Drawdown – shows max drawdown for every month and year. It is calculated by finding the difference between the highest equity achieved for the month/year and the trough in equity for the same month/year. Notice: strategy tester might have a max drawdown value higher than any of the drawdown values in the table. This is because the strategy tester calculates the difference between the highest and lowest equity for the entire strategy, whereas the table displays drawdowns for months and years only. Sometimes, the max drawdown for the year will also be the max drawdown for the entire strategy; hence the two values will be the same.

To use this table with your own strategy, simply find " PLACE YOUR STRATEGY CODE HERE " at the bottom of the script and place your strategy code there. Special thanks to QuantNomad for the inspiration. As always, please let me know if there are any bugs or if you need some help. Leave a like if you wish!

Drawdown RangeHello death eaters, presenting a unique script which can be used for fundamental analysis or mean reversion based trades.

Process of deriving this table is as below:

Find out ATH for given day

Calculate the drawdown from ATH for the day and drawdown percentage

Based on the drawdown percentage, increment the count of basket which is based on input iNumber of ranges . For example, if number of ranges is 5, then there will be 5 baskets. First basket will fit drawdown percentage 0-20% and each subsequent ones will accommodate next 20% range.

Repeat the process from start to last bar. Once done, table will plot how much percentage of days belong to which basket.

For example, from the below chart of NASDAQ:AAPL

We can deduce following,

Historically stock has traded within 1% drawdown from ATH for 6.59% of time. This is the max amount of time stock has stayed in specific range of drawdown from ATH.

Stock has traded at the drawdown range of 82-83% from ATH for 0.17% of time. This is the least amount of time the stock has stayed in specific range of drawdown from ATH.

At present, stock is trading 2-3% below ATH and this has happened for about 2.46% of total days in trade

Maximum drawdown the stock has suffered is 83%

Lets take another example of NASDAQ:TSLA

Stock is trading at 21-22% below ATH. But, historically the max drawdown range where stock has traded is within 0-1%. Now, if we make this range to show 20 divisions instead of 100, it will look something like this:

Table suggests that stock is trading about 20-25% below ATH - which is right. But, table also suggests that stock has spent most number of days within this drawdown range when we divide it by 20 baskets instad of 100. I would probably wait for price to break out of this range before going long or short. At present, it seems a stage ranging stage. I might think about selling PUTs or covered CALLs outside this range.

Similarly, if you look at AMEX:SPY , 36% of the time, price has stayed within 5% from ATH - makes it a compelling bull case!!

NYSE:BABA is trading at 50-55% below ATH - which is the most it has retraced so far. In general, it is used to be within 15-20% from ATH

NOW, Bit of explanation on input options.

Number of Ranges : Says how many baskets the drawdown map needs to be divided into.

Reference : You can take ATH as reference or chose a time window between which the highest need to be considered for drawdown. This can be useful for megacaps which has gone beyond initial phase of uncertainity. There is no point looking at 80% drawdown AAPL had during 1990s. More approriate to look at it post 2000s where it started making higher impact and growth.

Cumulative Percentage : When this is unchecked, percentage division shows 0-nth percentage instad of percentage ranges. For example this is how it looks on SPY:

We can see that SPY has remained within 6% from ATH for more than 50% of the time.

Hope this is helpful. Happy trading :)

PS: this can be used in conjunction with Drawdown-Price-vs-Fundamentals to pick value stocks at discounted price while also keeping an eye on range tendencies of it.

Thanks to @mattX5 for the ideas and discussion today :)

Drawdown - Price vs FundamentalsIn this study, we are trying to compare drawdown from ATH of price and fundamentals to understand if price drawdown is really justifyable or if this is the buying opportunity.

For example, NYSE:BABA in the chart below shows that price has come down by more than 50%. But, the fundamentals has not changed upto this extent.

This may be viewed as buying opportunity from the eyes of fundamental based trader.

Similarly NYSE:LPX is trading at 15% below ATH whereas fundamentals are at peak. This again can be considered as buying opportunity.

NASDAQ:AAPL on the other hand is trading almost near ATH whereas fundamentals are having higher drawdown.

Well, this is just one factor to consider. I am about to release another script which can demonstrate amount of time (in terms of percentage) instrument trades at certain drawdown range. This looks something like this:

These two scripts can be used in conjunction to define your fundamental based trade.

I can add more funcamentals to the list. But, the higher value of fundamental should correlate to better position. Hence we cannot use things such as PE (which inversely correlates to value). Also need to keep the factor which includes total number of shares in it so that it is not affected by share dilution. Hence, have considered Total Revenue per Share instead of Total Revenue in this script.

Thanks to @mattX5 for suggesting fundamental based ideas in this line :)

Drawdown over Window (in percentage)Unlike other scripts, which compare against the all time high, this allows you to specify the window over which the high should be searched.

If you want to compare against the all time high, just choose a long enough window.

Momentum Performance This Indicator displays the momentum (performance) of the symbol in percent.

You can compare the performance with other symbols.

The default benchmarks are the S&P 500, the MSCI World and the FTSE All World EX US.

The default length corresponds to one year in the timeframes monthly, weekly and daily.

In intraday the default length is 200, but you can also set your own setting.

You have also the opportunity to display a average momentum performance of the main symbol.

Max Drawdown Calculating Functions (Optimized)Maximum Drawdown and Maximum Relative Drawdown% calculating functions.

I needed a way to calculate the maxDD% of a serie of datas from an array (the different values of my balance account). I didn't find any builtin pinescript way to do it, so here it is.

There are 2 algorithms to calculate maxDD and relative maxDD%, one non optimized needs n*(n - 1)/2 comparisons for a collection of n datas, the other one only needs n-1 comparisons.

In the example we calculate the maxDDs of the last 10 close values.

There a 2 functions : "maximum_relative_drawdown" and "maximum_dradown" (and "optimized_maximum_relative_drawdown" and "optimized_maximum_drawdown") with names speaking for themselves.

Input : an array of floats of arbitrary size (the values we want the DD of)

Output : an array of 4 values

I added the iteration number just for fun.

Basically my script is the implementation of these 2 algos I found on the net :

var peak = 0;

var n = prices.length

for (var i = 1; i < n; i++){

dif = prices - prices ;

peak = dif < 0 ? i : peak;

maxDrawdown = maxDrawdown > dif ? maxDrawdown : dif;

}

var n = prices.length

for (var i = 0; i < n; i++){

for (var j = i + 1; j < n; j++){

dif = prices - prices ;

maxDrawdown = maxDrawdown > dif ? maxDrawdown : dif;

}

}

Feel free to use it.

@version=4

Price DropsThis script calculates the price drops from today's high.

You can modify the percentages of the price drops yourself.